Serviços Personalizados

Artigo

Inglês (pdf)

Inglês (pdf)

Artigo em XML

Artigo em XML Referências do artigo

Referências do artigo

Indicadores

Links relacionados

-

Citado por Google

Citado por Google -

Similares em Google

Similares em Google

Compartilhar

Permalink

PermalinkJournal of the Southern African Institute of Mining and Metallurgy

versão On-line ISSN 2411-9717

versão impressa ISSN 2225-6253

J. S. Afr. Inst. Min. Metall. vol.123 no.11 Johannesburg Nov. 2023

http://dx.doi.org/10.17159/2411-9717/1578/2023

PROFESSIONAL TECHNICAL AND SCIENTIFIC PAPERS

Cost modelling for dimension stone quarry operations

M.A. RazaI; S. RazaI; M.U. KhanI; M.Z. EmadI; K. JalilII; S.A. SakiI

IUniversity of Engineering and Technology (UET) Lahore, Pakistan. ORCID: M.A. Raza http://orcid.org/0000-0001-5373-8795. M.U.Khan http://orcid.org/0000-0002-6260-6679. M.Z. Emad http://orcid.org/0000-0001-8537-8026

IIKhawar Jalil Mining Consultants (KJMC), Pakistan

SYNOPSIS

Dimension stone mining is Increasing because of growing demand from the building and construction industries. Diamond wire saw cutting is a popular dimension stone mining technique around the world. Estimation of the production cost for this method is critical for these operations. In this research a production cost model was developed for the mining of granite using a diamond wire saw. Cost and production data were collected from a granitic dolerite operation in Pakistan for a 4.5-year period, and analysed to identify the cost components. Fuel (34%), labour (15%), consumables (40%), and maintenance (5%) were found to be the four major cost components in this operation. A regression-based dimension stone production cost model incorporating statistically significant variables was developed. The data presented a strong correlation of production cost with fuel, labour, and consumables costs. Finally, a production cost model based on the consumption cost of diamond wire is presented. The model was verified using actual production cost data, which indicated 95% (R2 = 0.95) variance in the data between the predicted and actual production cost values. The model may help field engineers in computing their dimension stone operational cost during the cutting phase.

Keywords: dimension stone, diamond wire saw, modelling, production cost, granite mining.

Introduction

Dimension stone is a technical and commercial term for all natural stones that can be quarried in blocks of different dimensions and processed by cutting or splitting, and which possess the technical and aesthetic properties required for use in the building and construction industries (PERC, 2021). Traditionally, dimension stone has been mined using common surface mining and rock-breakaging techniques such as splitting using explosives and cutting using various types of saw (Rehman et al., 2018; Ashmole and Motloung, 2008; Mamasaidov, Mendekeev, and Ismanov, 2004. Sawing is becoming more popular as this results in less wastage and a product with fewer cracks (Mendekeev, 2004). Of the various cutting techniques, diamond wire sawing, is the most widely used, and has become increasingly popular during the last three decades (Careddu, Perra, and Masala, 2019).

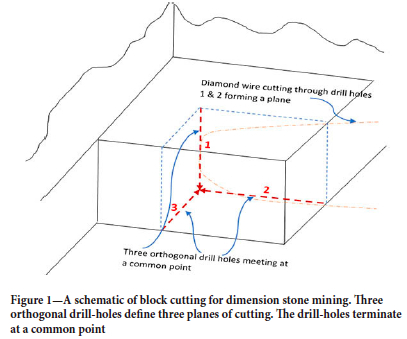

A typical production cycle of this technique consists of five phases: (1) drilling, (2) cutting, (3) block dropping, (4) block slicing. and (5) loading. During the drilling phase, three mutually perpendicular holes are drilled in the rock mass with a common termination point, as illustrated in Figure 1. The cutting phase involves cutting a block in three planes using diamond wire. Other cutting techniques, such as disc cutting, may also be employed. The principle for diamond wire cutting involves pulling a continuous loop of wire, fitted with diamond-bonded steel beads, in a plane. The diamond wire is passed through two drill-holes, forming a closed loop and running over the wire saw pully which is connected to a track-mounted motor. The wire cuts through the plane while tension is maintained in the wire by continuously propelling the motor on the track as shown in Figure 2. Water is continuously fed during cutting to cool the wire. Once one plane is cut, the same procedure is repeated to cut the block in the other two planes. The block is then available for excavation. The remaining three phases of extraction are related to the excavation and loading of the block. During block dropping, the block is separated from the parent rock mass for easier processing. For some benches the block dropping phase may be omitted. During block slicing, smaller slices are cut from the larger block for loading and transportation.

The diamond wire is a multi-strand steel wire with equally spaced steel beads (commonly 25 to 50 per metre based on the cutting requirements) with diamond abrasive. The wire is crimped at intervals to make it resistant to unwinding. The common wire types are manufactured for marbles and granites, both for dry and wet cutting (Tantussi, Lanzetta, and Romoli, 2003; Diamond Pauber, 2023).

Block cutting is the primary cost component for a diamond wire operation in dimension stone mining, as observed in the field and in this research, and therefore should be studied for cost-benefit analysis. The performance of the wire saw machine is critical for optimizing the operations (Jain and Rathore, 2011). The wear of the diamond beads on the wire and the operational parameters are the primary factors that govern the cost and performance of a diamond wire cutting operation (Bortolussi et al., 1995; Korre and Durucan, 2000; Mikaeil et al., 2018; Almasi et al., 2017; Mosch et al., 2011; and Ulyakov, 2015). The wear rate of the diamond wire is higher for harder rocks such as granite than for soft rocks such as marble (Careddu and Marras, 2015).

Pakistan is endowed with large deposits of granite and marble which present good potential for supplying the dimension stone market across the globe. However, a lack of technology and skilled labour, and shortage of area-specific mining knowledge, are major barriers to converting these resources into meaningful revenue and contribution to the country's GDP (Business Recorder, 2012; Express Tribune, 2019). Cost estimation is one of the critical aspects of any dimension stone operation. Unfortunately, little research has been done to estimate and model the costs incurred in the use of diamond wire cutting technology for stone extraction. This paper presents a cost model based on statistical analysis of the cost centres for a dimension stone quarry that may be useful for similar operations in the area or elsewhere. The cost centres were established after a detailed analysis of different cost components of stone extraction. The research was conducted within the specific context of granitic rocks. The outcomes will enable the industry and engineers to realistically estimate the cost and forecast probable production outputs for the incurred costs, thus assisting the planners to prepare realistic feasibility studies for dimension stone mining projects.

Methodology

Data was collected from M/S Indus Mining (Private) Limited (IML), which mines dolerite (termed commercially 'black granite') in Tehsil Oghi, district Mansehra of Pakistan. The deposit is located at approximately 72°55E 34°26' N. The stone is excavated using diamond wire cutting on one active level, yielding blocks as the primary product and boulders as byproduct. One 41 kW wire saw machine (Marini) and a compatible 207 kVA generator operate in two 8-hour shifts. A diamond wire with injected vulcanized rubber is used for cutting the dolerite. This wire has 40 sintered beads per metre with an external bead diameter of about 12 mm. Figure 2 shows the diamond wire saw machine on track at the IML site.

A 4.5-year (January 2013 to June 2017) data-set for stone production and costs was used for this study. In the first step, the collected data was studied and organized for various cost heads. After a thorough examination the cost data was divided into two major components - operating costs and overhead costs. The operating cost was further subdivided into four cost centres: fuel (F), labour (L), maintenance (M), and consumables (C). Other minor costs, such as equipment depreciation and insurance, were grouped collectively as overhead expenses (O). Fuel cost (F) included direct diesel and lubrication expenses. Labour cost (L) included salaries, bonuses, and expenses related to on-site facilities for workers such as food and laundry. Consumable cost (C) included diamond wire and machine jointing costs. Maintenance cost (M) included all expenses incurred for preventative maintenance and breakdowns of generators and wire saw machines. The maintenance cost was estimated based on the costs for parts and technicians' salaries.

Once the cost data was organized, the data was statistically analysed using SPSS (R-17) software using the cost centres identified in the first phase. SPSS is a popular commercial software package for data analysis. The software was chosen due to its user-friendly interface and robust algorithm for statistical data analysis. SPSS has a facility for importing data from Excel, which was handy in this research, and offers multiple tools for data analysis and model creation.

Results and discussion

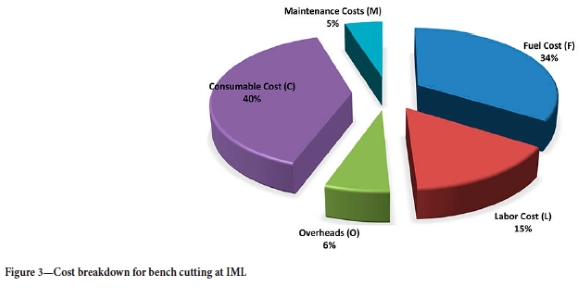

Based on the data collected from the field, percentage costs were generalized for the broader implications (i.e., for all granite-type rocks) as presented in Figure 3 as a pie chart of various cost components. Consumable cost (C) was the highest incurred cost during bench cutting phase, at 39% of total cost, while fuel cost (F) was 34%, labour cost (L) 15%, and maintenance cost (M) was 5%. Overhead expenses (O) were computed at 7% of the total cost. Overhead expenses, although marginally higher than the maintenance cost, were ignored for the purpose of cost modelling as the focus of this research was to investigate the relationship between operating costs and stone production. Overhead are not standardized costs and may vary considerably based on factors such as equipment care policies and dealership support. Maintenance costs, however, contribute to the overall operating costs and are therefore included in the cost modelling.

Diamond wire was the primary consumable item used in the cutting phase, and which mostly defined the consumables cost. Monthly requirements for diamond wire depend on multiple factors such as abrasiveness and hardness of the rock, the wire saw machine's operational parameters, number of working horizons, bench dimensions, and total production. Fuel consumption was a little more than one-third of the total cost. Fuel consumption was dependent on cutting time, which further depended on factors such as motor power, cuttability of the rock, and speed. Cutting time could be a key reason for higher fuel cost. Wire saw operations require high skill levels. The operator needs to manually adjust the parameters such as tension on the wire, cutting speed, and water flow rate, as these have direct impact on machine health and longevity as well as production. These parameters are adjusted on-the-go during cutting and require high skill levels. Small personal and operational errors during operation may lead to severe losses or fatalities. For example, an inexperienced operator trying to achieve higher cutting rates may apply too much tension and use a higher speed, resulting in breaking of the diamond wire which can cause accidents. Highly skilled operators cost more in terms of salaries and other allowances, resulting in higher labour costs compared with other surface mining operations. Maintenance and overheads costs were almost equal for this operation.

A regression model was developed to study correlations between the production and cost centres. Pearson's correlation coefficient was used to find the correlation between total production (tons) and identified cost (PKR) components. For both correlation and regression analyses, a p-value (significance level) of 0.05 was fixed as the benchmark. This is a common standard value for significance testing. Only statistically significant variables were included in the final regression model.

The regression analyses were conducted in SPSS, with production cost as the dependent variable and various cost components as independent variables, resulting in Equation [1], where ß0 is a constant and B1, B2, B3, and B4 are unstandardized regression coefficients associated with different cost variables.

where Pc is the production cost and F, L, C, and M are independent variables for fuel cost, labour cost, consumable, and maintenance cost respectively.

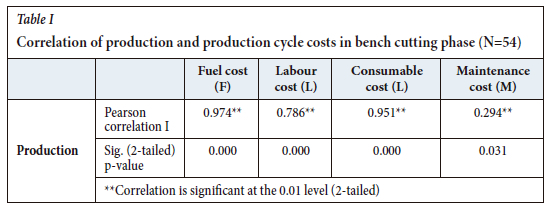

Table I gives the Pearson's correlation coefficients between production (dependent variable) and IL, C, and M (independent variables) incurred during the bench cutting phase.

As depreciation and insurance costs (overheads) are fixed costs, and do not affect the operating cost, these cost components were excluded from the remaining analysis. In Table I, the p-values for correlations of production with fuel cost, labour cost, and consumable cost are zero, which suggests that each correlation is significant at the 0.01 level. However, we could not establish any causality between variables on this basis alone. The p-value for correlation between production and maintenance is 0.0031, which is insignificant.

Strong correlations were observed between production and fuel cost (r = 0.974), between production and consumable cost (r = 0.951), and between production and labour cost (r = 0.786). A weak correlation was observed between production and maintenance cost (r = 0.779). The r values were positive in all cases, indicating that an increase (decrease) in one variable will cause an increase (decrease) in the other.

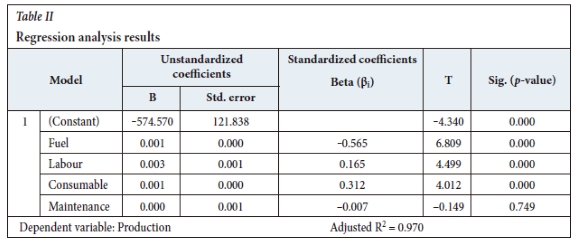

Table II shows the relationship between production and bench cutting cost components obtained through regression analysis. Here again, the p-values for F, L, and C, are 0.000, which is considerably less than 0.05. This suggests that the relationships of these variables with production are statistically significant. In the case of maintenance cost, the p-value is 0.458 which is considerably higher than 0.05. This suggests that the relationship of maintenance cost with production is statistically insignificant. The adjusted R2 value for this analysis is 0.97, which means that the model explains 97% of the variance in the data. There is still a need to omit the statistically insignificant variable of maintenance cost from the optimum cost model.

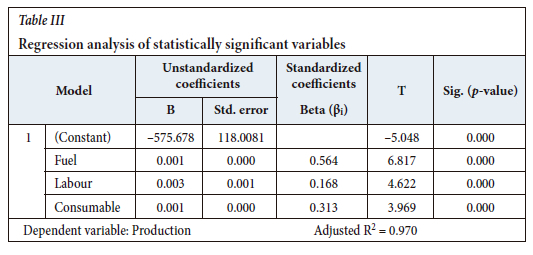

Table III shows the regression analysis results after omitting the statistically insignificant variable of maintenance cost. The adjusted R2 value for the new cost model is again 0.967, which means that this model too describes nearly 97% of the variance in data. However, this model contains all statistically significant independent variables only.

Equation [2] represents the cost model for different cost factors that are involved in bench cutting.

Positive B values for both independent variables suggest a direct relationship between production and the independent variables. The B values define the coefficients for Equation [2] and establish the relationship between production and component costs. Similarly, the standardized coefficients (ßi) suggest variations in the standard deviations. The beta coefficient values also suggest that fuel cost has an approximately 3.5 times stronger influence on production than does labour cost, while consumables cost has approximately 2 times stronger influence.

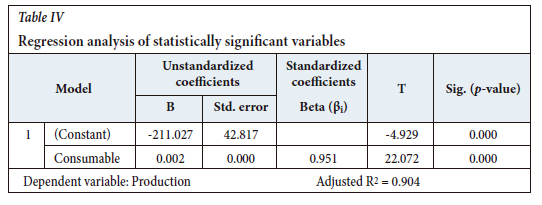

The above model presents the predictive cost model for diamond wire saw production in terms of labour, fuel, and consumables costs. This theoretical model is not ideal for practical use by the estimation engineers, as many combinations of F, L, and M can exist. Furthermore, in our field observation we found that there is more need to estimate production based on diamond wire consumption, i.e., production per unit cost of diamond wire (consumable cost in our case). Therefore, a cost model was derived based on consumables cost only. Table IV presents the regression analysis between P and C only.

The model is simpler, practical, and still explains 95% of the variance in the data.

Model validation

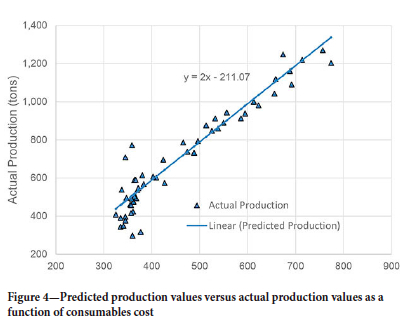

The production cost values were estimated using the model presented in Equation [3]. These values were plotted against the actual production values as a function of consumables, as shown in Figure 4. An R2 value of 0.951 was obtained between the actual and predicted production. The strong correlation proves the validity of the model.

Conclusions

Dimension stone mining practice in Pakistan is experience-based and there is shortage of technical knowledge and expertise in this field. As a result, current operations are conducted using less economical or low productivity techniques. We analysed 4.5 years of historical data from a working stone quarry in Pakistan. The analysis revealed four major cost centres for dimension stone production using diamond wire sawing. A detailed statistical analysis showed that three cost components (fuel, labour, and consumables in the form of diamond wire cost) were statically significant and responsible for 97% of the variance in the data. A predictive production cost model for the diamond wire saw based on the consumables costs, which largely comprise the cost of diamond wire, is presented and verified using actual production data. The cost model predicted 95% of the cost variance at the selected operation.

Although the current production cost model has been developed for a specific operation, it is expected that it should be applicable to similar operations. It is planned to verify the moder on data from a larger pool of dimension stone quarries in Pakistan. Furthermore, the model was based on the cost of diamond wire, which is variable. It could be better to base the model on diamond wire consumption. This will require the relevant data to be recorded at the mine. This is planned for future research as well.

Acknowledgment

The researchers are thankful for the support of Indus Mining (Pvt.) Limited, Pakistan for provision of data for this project.

References

Almasi, S.N., Bagherpour, R., Mikaeil R., and Ozcelik, Y. 2017. Developing a new rock classification based on the abrasiveness, hardness, and toughness of rocks and pa for the prediction of hard dimension stone sawability in quarrying. Geosystem Engineering, vol. 20. pp. 295-310. [ Links ]

Ashmole, I. and Motloung, M. 2008. Dimension stone: The latest trends in exploration and production technology. Proceedings of Surface Mining 2008. Southern African Institute of Mining and Metallurgy, Johannesburg. pp. 5-8. [ Links ]

Bortolussi, A., Ciccu, R., Manca, RR, and Massacci, G. 1995. Computer simulation of diamond-wire cutting of hard and abrasive rock. International Journal of Rock Mechanics and Mining Sciences & Geomechanics abstracts, | vol. 32. -Doi: 0.1016/0148-9062(95)90156-Y [ Links ]

Careddu, N. and Marras, G. 2015. Marble processing for future uses of CaCO3-microfine dust: a study on wearing out of tools and consumable materials in stoneworking factories. Mineral Processing and Extractive Metallurgy Review, vol. 36. pp. 183-191. [ Links ]

Careddu, N., Perra, E.S., and Masala, O. 2019. Diamond wire sawing in ornamental basalt quarries: Technical, economic and environmental considerations. Bulletin of Engineering Geology and the Environment, vol. 78. pp. 557-568. [ Links ]

Diamond pauber. 2023. Data sheet. Https://www.Diamondpauber.It/stoneproducts [ Links ]

Express tribune. 2019. Pakistan's marble sector declining due to lack of attention. Karachi. Https://tribune.Com.Pk/story/2055198/pakistans-marble-sector-declining-due-lack-attention [ Links ]

Busines recorder. 2012. Issues, problems faced by marble sector highlighted, Karachi. Https://fp.Brecorder.Com/2012/08/201208171228736/ [ Links ]

Jain, S.C. and Rathore, S.S. 2011. Prediction of cutting performance of diamond wire saw machine in quarrying of marble: A neural network approach. Rock Mechanics and Rock Engineering, vol. 44. pp. 367-371. [ Links ]

Korre, A. and Durucan, S. 2000. The effects of granite microstructure on the sawing performance of diamond wires. International Journal of Surface Mining, Reclamation and Environment, vol. 14. pp. 87-102. [ Links ]

Mamasaidov, M.T., Mendekeev, R.A., and Ismanov, M.M. 2004. Generalized model of technology for article production from stone massif. Journal of Mining Science, vol. 40. pp. 521-527. [ Links ]

Mendekeev, R.A. 2004. Analysis of raw material losses in sawing stone blocks into facing products. Journal of Mining Science, vol. 40. pp. 515-520. [ Links ]

Mikaeil, R., Haghshenas, S.S., Ozcelik, Y., and Gharehgheshlagh, H.H. 2018. Performance evaluation of adaptive neuro-fuzzy inference system and group method of data handling-type neural network for estimating wear rate of diamond wire saw. Geotechnical and Geological Engineering, vol. 36. pp. 3779-3791. [ Links ]

Mosch, S., Nikolayew, D., Ewiak, O. and Siegesmund, S. 2011. Optimized extraction of dimension stone blocks. Environmental Earth Sciences, vol. 63. pp. 1911-1924. [ Links ]

Perc. 2021. Pan-European Standard for the Public Reporting of Exploration Results, Mineral Resources and Reserves. Appendix a. Reporting of Exploration Results, Mineral Resources and Mineral Reserves for Dimension Stone, Ornamental and Decorative Stone. Pan-European Reserves and Resources Reporting Committee, brussels. Https://percstandard.Org/wp-content/uploads/2021/09/PERC_REPORTING_STANDARD_2021_RELEASE_01O ct21_full.Pdf [ Links ]

Pershin, G.D. and Ulyakov, M.S. 2015. Enhanced dimension stone production in quarries with complex natural jointing. Journal of Mining Science, vol. 51. pp. 330-334. [ Links ]

Rehman, Z.U., Hussain, S., Mohammad, N., Raza, S., Sherin, S., Khan, M., Tahir, M., and Khan, M. 2018. Comparative analysis of different techniques used for dimension stone mining. Journal of Himalayan Earth Science, vol. 51. pp. 23-33. [ Links ]

Tantussi, G., Lanzetta, M., and Romoli, V. 2003. Diamond wire cutting of marble: state of the art, modeling and experiments with a new testing machine. Proceedings of the 6th International Conference of the Italian Association of Mechanical Technology, Enhancing the Science of Manufacturing. pp. 113-126. https://arpi.Unipi.It/retrieve/handle/11568/190631/17498/artperlinefin.Pdf [ Links ]

Correspondence:

Correspondence:

M.U. Khan

Email:usman@uet.edu.pk

Received: 21 Mar. 2021

Accepted: 29 Aug. 2023

Published: November 2023