Services on Demand

Journal

Article

English (pdf)

English (pdf)

Article in xml format

Article in xml format Article references

Article references

Send this article by e-mail

Send this article by e-mailIndicators

Related links

-

Cited by Google

Cited by Google -

Similars in Google

Similars in Google

Share

Permalink

PermalinkSouth African Journal of Economic and Management Sciences

On-line version ISSN 2222-3436Print version ISSN 1015-8812

S. Afr. j. econ. manag. sci. vol.28 n.1 Pretoria 2025

https://doi.org/10.4102/sajems.v28i1.6134

ORIGINAL RESEARCH

The effects of economic crises on capital structure: Evidence from an emerging economy

Molefiseng F. Thabethe; Franz E. Toerien

Department of Financial Management, Faculty of Economic and Management Sciences, University of Pretoria, Pretoria, South Africa

ABSTRACT

BACKGROUND: Economic crises have severely impacted firm capital structure throughout history. Companies rely on a balanced mixture of financing between debt and equity, in order to sustainably finance their investing and operating capital requirements. Recent economic crisis like the 2008 Global Financial Crisis (GFC) and the COVID-19 pandemic have challenged companies' abilities to manage their capital structures

AIM: This study examines how two different crises affected JSE firms' capital structures, identifies which firm-level factors mattered in each period, and assesses which capital structure theories best explain these crisis responses

SETTING: The analysis was based on a sample of 234 firms listed on the JSE during the period 2004-2022

METHOD: The secondary firm-level data were obtained from financial data depositories, Integrated Real-Time Equity Systems and Thomson Reuters DataStream. The study made use of Estimated General Least Squares and random effects regression models

RESULTS: After the 2008 crisis, firms deleveraged and liquidity became the key (negative) determinant of leverage, consistent with pecking order theory. During Covid-19, firms increased leverage, with profitability and growth negatively related to leverage and asset tangibility positively related, reflecting a mix of trade-off and pecking order behaviours

CONCLUSION: Different crises drive distinct financing behaviour: financial crises lead firms to prioritise liquidity and internal funds (pecking order), whereas operational crises push firms toward greater external borrowing despite weaker performance (trade-off). This distinction helps guide financial managers and policymakers in emerging markets when planning for future disruptions

CONTRIBUTION: This study provides new evidence on how different types of economic crises uniquely shape the capital structure decisions of JSE-listed firms. By incorporating crisis-specific interaction terms over an extended panel (2004-2022), it isolates how firm-level determinants behave under financial versus operational shocks, offering clearer insights into crisis-driven financing behaviour in an emerging-market context

Keywords: capital structure; debt; economic crisis; emerging market; equity; risk management.

Introduction

Capital structure refers to a firm's balanced mixture of debt and equity financing (Myers 1984). An optimal balance between debt and equity financing is crucial for a firm's financial stability, cost of capital and survival, especially during economic crises (Balios et al. 2016). Understanding how economic crises impact capital structure is vital for several reasons: it drives key decisions around a firm's financial strategy, provides regulatory policy guidelines and contributes to the financial stability of volatile markets (Campello 2003; Myers 1984; Titman & Wessels 1988). The strategic significance of capital structure derives from the direct impact it has on a firm's value, risk profile and operational efficiency (Danso & Adomako 2014; Elsas & Florysiak 2008; Kruk 2021; Miller 1958; Modigliani & Miller 1958). During stable economic conditions, firms are more financially flexible and target optimal debt-equity levels; however, economic crises restrict financial flexibility and make it more difficult for firms to access financing from banks and capital markets (Demirgüç-Kunt, Martinez Peria & Tressel 2015; Harrison & Widjaja 2014). According to Mouton and Pelcher (2023); Proença, Laureano and Laureano (2014); and Ramjee and Gwatidzo (2012), emerging economies are particularly more sensitive to the impact of economic crises on capital structure, as their capital markets are often more volatile and firms have fewer buffers compared to those in developed economies.

Existing literature has extensively explored how economic crises impact capital structure. For instance, studies by Garay (2003) and Jeasakul, Lim and Lundback (2014) on the Asian Financial Crisis (AFC) highlighted how the impact of foreign investment outflows and currency devaluations resulted in high debt levels, which ultimately created a need for significant policy adjustments. Similarly, studies by Demirgüç-Kunt et al. (2015); Gocmen and Sahin (2014); Proença et al. (2014) and Zarebski and Dimovski (2012) on the Global Financial Crisis (GFC) found how the crisis led to significant adjustments in corporate financing policies because of reduced debt supply and higher borrowing costs. More recently, studies by Deviyanti et al. (2023); Huang and Ye (2021) and Shen et al. (2021) examined the impact of the COVID-19 pandemic on capital structure and identified how firms relied on short-term debt to fund working capital because of a decreased profitability, liquidity and lower growth rates. However, despite this, there remains a gap in the existing literature as it primarily analyses economic crises in isolation among developed markets. Moreover, there are limited studies that explore a comparative analysis on how two different economic crises impact capital structure, the internal company-related factors influencing capital structure decisions, and the capital structure theories adopted by firms during the two economic crises, more specifically in emerging markets.

In order to address this gap, this study analyses firms' financing behaviour during two distinct economic crises using a sample of Johannesburg Stock Exchange (JSE)-listed companies from 2004 to 2022, with the aim of exploring the leverage responses of JSE-listed companies during the 2008 GFC and the COVID-19 pandemic (using debt-to-equity ratios as a proxy for capital structure), linking the observed effects with the relevant and competing capital structure theories (pecking order, trade-off and agency costs) and assessing which internal firm-related factors were most significant during each crisis period.

This study's main objectives were to analyse and compare the impact that the 2008 GFC and COVID-19 pandemic had on JSE-listed companies' capital structure by exploring the different levels and magnitude of leverage adjustments for both periods; to identify the significant determinants of capital structure by analysing which internal firm-related factors (profitability, liquidity, company growth rate, taxation, tangibility, size and risk) were significant predicators during each crisis period; and to evaluate and compare the relevant capital structure theories that were applied during each crisis period.

By exploring and addressing this gap, this study contributes to the existing literature by providing a comparison of how two different economic crises impact capital structure in an emerging market; identifying whether similar or different company-related factors or determinants of capital structure were significant during both crisis periods; and examining whether firms' financing decisions applied similar or different capital structure theories during both economic crisis periods. Moreover, this study contributes towards the financial and business knowledge for companies operating in emerging markets and could be highly beneficial for potential investors and the future economic prospects of developing nations, particularly during economic crises, as the JSE-listed companies represented serve as a proxy for other emerging markets with similar economic conditions and trends.

Literature review

Capital structure foundational theories

Modigliani-Miller theory

The Modigliani-Miller theory by Modigliani and Miller (1958) was developed during the late 1950s and has since become an important topic of reference in corporate finance. According to Modigliani and Miller (1958), a company's value is independent of its capital structure. Modigliani and Miller (1958) proposed that the value of a company is determined solely by its cash flows, risk profile and investment opportunities, stating that all capital structure approaches will ultimately lead to one result in the long run. However, during economic crises, assumptions related to the MM theory, such as bankruptcy costs, perfect market conditions and information asymmetry, become more extreme, as market conditions are highly imperfect, making decisions related to capital structure more critical for a firm's survival (Glen & Pinto 1994).

Trade-off theory

The Trade-off Theory was introduced to balance the benefits and costs of capital structure components (Ju et al. 2005). This theory argues that companies should balance the tax benefits of debt financing with the costs associated with bankruptcy and financial distress (Harris & Raviv 1991). However, during economic crisis periods, the probability of financial distress increases while benefits from tax shields are reduced because of lower profitability (Günay 2002). Moreover, the trade-off theory states that companies should define and adhere to an optimal level of debt to maximise their value, adding that there is a positive relationship between profitability and an optimal leverage ratio (Ju et al. 2005). However, Günay (2002) highlights the complexity of achieving optimal leverage ratios in developing markets, as highly profitable firms tend to deleverage and opt for internal financing, whereas less-profitable firms find it more difficult to access financing from the debt and equity markets because of the strict covenants imposed during economic crises.

Pecking order theory

The Pecking Order Theory opposed the trade-off theory by arguing that companies should rather look towards the most cost-effective source of capital finance to minimise the financial risks associated with overweighted debt financing structures (Chen & Chen 2011; Myers 1984). Furthermore, the pecking order theory suggests that companies should prefer internal financing over external financing because of the understanding and communication between managers and outside investors, with companies preferring to avoid the negative effects of a potential decline in stock price caused by the release of negative economic information (Proença et al. 2014). However, during economic crises, information asymmetry tends to increase, resulting in higher costs related to external financing and more reliance on internal funds (Chatzinas & Papadopoulos 2018). Moreover, when internal funds start depleting (i.e. during the COVID-19 pandemic lockdown period), companies may be forced to ignore the pecking order and accept diluted equity financing or higher debt servicing costs in order to survive (Chatzinas & Papadopoulos 2018). Furthermore, the pecking theory's economic crisis prediction is highly dependent on whether the crisis primarily affects a firm's ability to generate cash (operational impact) or the availability of external financing sources (financial impact) (Jansen et al. 2022).

The agency cost theory

The Agency Cost Theory proposes that companies can use debt financing as a way to reduce agency costs that arise because of conflicts of interest between business managers and shareholders (Kochhar 1996). The agency cost theory assumes that shareholders adhere to strict monitoring and disciplined structures of daily business operational activities to minimise opportunistic behaviour and reduce agency costs (Correia 2019; Kochhar 1996). The agency cost theory establishes accountability and ensures that the managers and shareholders of a firm refrain from investing in high-risk projects and unqualified changes of capital structures and that they monitor potential conflict between shareholders and bondholders (Grigore & Stefan-Duicu 1976). According to Smith (2010), the effects of the 2008 GFC exacerbated this conflict, as managers pursued strategies aimed at satisfying their own interests and job security, shareholders preferred to increase risk in order to maximise and salvage their values, while debtholders become more vigilant (Smith 2010). In emerging markets, where ownership structures are highly concentrated and governance mechanisms are weaker, these dynamics may be altered, as controlling shareholders could potentially expropriate minority investors during economic crises.

Foundational theory predictions for each economic crisis period

During the 2008 GFC, banks reduced the supply of credit, which restricted the access to funding and made the trade-off theory's target leverage ratio assumption less relevant compared to the pecking order theory's importance on financing constraints (Iqbal & Kume 2014). Banks significantly reduced their risk appetite, resulting in firms finding it more difficult to access credit. Moreover, bonds markets froze, while equity valuations decreased significantly, forcing firms to rely more on internal funding regardless of their initially targeted leverage ratios (Benmelech & Bergman 2018). Agency issues also intensified because of debtholders exercising covenants and demanding additional collateral (Smith 2010).

During the COVID-19 pandemic, global trade was highly restricted and numerous firms were forced to suspend operations. Firms experienced decreasing liquidity levels and cash flow constraints during the lockdown period (Mouton & Pelcher 2023). In this instance, the trade-off theory assumes that firms should reduce debt if business risk increases; however, the pecking order theory considers that depleting internal funds may force firms to increase leverage regardless of preferences. In addition, agency issues may arise as managers focus more on operational decisions rather than financial restructuring (Lazarus et al. 2024; Mbatha & Alovokpinhou 2022).

Economic crises and capital structure adjustments

Evidence from financial crises

The 1997 AFC showcased how currency devaluations can change manageable foreign currency debt into unmanageable burdens (Deesomsak, Paudyal & Pescetto 2004). The Asian economy was negatively impacted by sudden outflows of foreign investment capital, currency devaluations and widespread economic turmoil (Garay 2003; Jeasakul et al. 2014). Deesomsak et al. (2004) and Garay (2003) found that Asian firms deleveraged significantly post crisis, and the speed of adjustments varied mainly because of country-specific institutional factors. Moreover, firms operating in countries with better creditor rights and developed bond markets showcased greater financial flexibility (Deesomsak et al. 2004).

The 2008 GFC had a negative effect on firms' financing strategies because of the decreased supply of credit and higher borrowing costs (Hussain 2022). In developed markets, Fosberg (2013) found that US firms increased leverage positions by 5.7% because of declining equity valuations instead of actively targeting optimal debt-to-equity ratios. Conversely, Iqbal and Kume (2014) found that UK-based firms deleveraged and implemented more cost-cutting measures, indicating the importance of country-specific factors in relation to leverage adjustments during economic crises.

Evidence from South Africa by Mouton and Smith (2016) found that JSE Top 40 listed firms deleveraged as concerns related to profitability and risk intensified. Furthermore, Mouton and Smith (2016) found firm size, profitability and tangibility as significant determinants of capital structure during the 2008 GFC; however, their study focused only on the JSE Top 40 and isolated crisis periods. Ramjee and Gwatidzo's (2012) study suggests that firms opted more for the target adjustment approach; however, the speed of adjustments slowed during the 2008 GFC.

Evidence from the COVID-19 pandemic

The COVID-19 Pandemic had a significant and vastly unexpected impact on the world economy, affecting companies and industries in all sectors (Deviyanti et al. 2023; Olowookere et al. 2022). In developed markets, Hotchkiss, Nini and Smith (2021) found that the lockdown period forced the US firms to aggressively drawdown on lines of credit, significantly increasing their leverage positions, before restoring financial flexibility through raising equity. Moreover, Halling, Yu and Zechner's (2020) study found that the COVID-19 pandemic had a contrasting effect on bond and equity markets in the United States and Europe. According to Halling et al. (2020), the intervention of central banks significantly aided bond markets, providing crucial financial lifelines for firms, while equity markets seized up during the crisis period because of heightened economic uncertainty.

Mbatha and Alovokpinhou's (2022) study highlighted the impact of COVID-19 pandemic on South African firms, showing how interest rate cuts by the South African Reserve Bank (SARB) made debt financing less costly and more attractive, as firms significantly increased short-term debt levels. Moreover, Olowookere et al.'s (2022) study on retail companies in Nigeria found that firms increased short-term debt in order to supplement working capital requirements. Lazarus et al. (2024) showcased how firms in Ghana significantly increased leverage because of pressure on liquidity levels, further highlighting how highly tangible firms leveraged more aggressively.

Determinants of capital structure during economic crises

Risk

Risk is a significant factor that can affect the capital structure of a company because higher financial and business risks usually discourage creditors from providing funding for investment and capital financing purposes (Mouton & Smith 2016). During economic crisis, the effects of risk may dominate other factors, making interest rate coverage crucial as earnings start depleting. According to Moradi and Paulet (2019), during economic crises, larger firms with more stable cash flows tend to increase their leverage positions, while their smaller competitors face the potential for financial distress.

Taxation

Miller (1977) found that taxation plays an important role in shaping a company's capital structure by influencing over its cost breakdown and determining the type and proportion of funding sources used by the firm. Kang and Ausloos (2017) identified how large public companies tend to have a higher propensity to utilise the tax advantages provided by debt, such as interest tax shields, to increase company valuations while taking advantage of low external funding. During economic crises, lower profitability may limit tax-shield benefits; however, tax losses carried over may preserve future tax shields, as governments often include tax measures that account for historical losses (Miller 1977).

Profitability

Profitability is also a crucial factor to consider when determining a company's capital structure because companies with higher profits may be more willing to take on debt and service it on a consistent basis, supporting the trade-off theory (Correia 2019). According to Modigliani and Miller (1963), high profits lead to more debt financing because of the tax shields it provides; however, companies with high profits can also refrain from acquiring debt because of the availability of equity, supporting the pecking order theory (Tram 2016). During economic crises, this relationship may be stronger or weaker. For instance, should larger, more profitable firms hold more cash reserves for precautionary reasons, they may choose to aggressively deleverage. Alternatively, should credit markets restrict the supply or access of funds based on company performance, these profitable firms may find it easier and less costly to access debt. Harrison and Widjaja (2014) found a negative correlation between profitability and capital structure during the 2008 GFC, supporting the pecking order theory. Moreover, Mouton and Pelcher (2023) found that retail firms in South Africa deleveraged during the COVID-19 pandemic, as profitability and capital structure were negatively correlated, supporting the pecking order theory.

Tangibility

Tangibility plays a crucial role in determining a company's capital structure because firms with more fixed and tangible assets generally require more long-term capital to fund their operations and projects (Harrison & Widjaja 2014). Furthermore, tangible assets can also be used as collateral for acquiring favourable debt financing agreements. However, during economic crises, re-evaluated assets may reduce collateral. Deesomsak et al. (2004) found that tangibility was a significant determinant of capital structure during the AFC, while Balios et al.'s (2016) study had similar findings during the 2008 GFC.

Liquidity

Liquidity is essential to the financial management position of a company because it directly affects a firm's ability to meet their daily obligations (Modigliani & Miller 1963). The relationship between liquidity and capital structure reflects competing influences. Firms with higher liquidity levels often reduce their reliance on debt during stable economic conditions or signal creditworthiness to banks, allowing them to increase leverage at lower costs (Eljelly 2004). During economic crises, larger firms in developing markets often take a precautionary approach, choosing to reduce debts and rely on internal financing sources (Mouton & Smith 2016; Šarlija & Harc 2012). However, Sari, Anwar and Faisal (2022) found that liquidity pressures during the COVID-19 pandemic forced firms to rely on more debt as internal funds depleted.

Growth

Glen and Pinto (1994) focused on the relationship between a company's growth stage in the business cycle and its capital structure and found that companies in the growth stage tend to have different capital structures compared to companies in the maturity stage. Glen and Pinto (1994) highlighted how firms in the growth stage require additional external financing, which leads to changes in their capital structure. Growing firms typically increase debt to fund expansions, but economic crises complicate this relationship. During economic crisis, growth opportunities are more limited, reducing the need for funding; however, smaller firms may require debt to survive. De Souza, Carraro and Pinheiro's (2022) study found that limited growth opportunities during the COVID-19 pandemic forced large firms to increase leverage positions and use tangible assets as collateral in order to access lower debt servicing costs.

Size

The size ratio, which is a proxy of total revenue, as it represents the total income from a company's core operations, can provide insights into the size of a firm based on its year-to-year total revenue levels (Correia 2019). During economic crises, larger firms typically increase their leverage positions because of diversification and lower bankruptcy risk (Kurshev & Strebulaev 2015; Pervan & Višić 2012). Larger firms typically maintain mutually beneficial relationships with banks and better market access, while smaller firms face restricted access to external financing sources (Dang, Li & Yang 2018). However, according to Kang and Ausloos (2017), the effect of firm size typically varies by crisis type and market structure, as evidenced during the 2008 GFC when large firms collapsed despite their reputation.

Research hypotheses

Based on the theoretical frameworks and empirical evidence mentioned in the literature review, our study developed the following hypotheses:

H1: We expect the 2008 GFC and the COVID-19 pandemic to impact the capital structure of JSE-listed firms differently.

H2: We expect different internal firm-related factors or determinants of capital structure during the 2008 GFC and the COVID-19 pandemic.

H3: We expect that different capital structure theories be applied during the 2008 GFC and COVID-19 pandemic by JSE-listed firms.

Methods

Research design and approach

This study followed a positivist research approach by employing quantitative methods to test the hypotheses related to the impact that economic crises had on JSE-listed companies' capital structure. The research design used panel data to exploit cross-sectional (firm-level) and time-series (period) variations, which enabled a robust identification of the effects of economic crises while also controlling for firm-specific factors and general time trends (Deesomsak et al. 2004; Demirgüç-Kunt et al. 2015; Tripathy & Asija 2017).

Research sample and data collection

The final sample size for this study included financial data from Integrated Real-Time Equity Systems (IRESS) and Thomson Reuters DataStream for the 234 companies listed on the JSE between 2004 and 2022, resulting in 24 728 total valid values and 13 576 missing values for all variables over the entire period. The following timeframes were used:

2004-2022: This period observes all companies listed on the JSE between 2004 and 2022. The 19-year window provides sufficient pre-crisis observations to establish baseline relationships, encompasses both crisis periods, and includes post-crisis recovery phases.

2008-2009: The GFC; following Mouton and Smith (2016), the crisis period starts with the Bear Stearns collapse (March 2008) and extends into 2009 to capture the full credit market disruption and the economic contraction in South Africa.

2020-2021: The COVID-19 pandemic; the period during the COVID-19 pandemic (01 January 2020 - 31 December 2021) was estimated according to the lockdown restrictions experienced during the pandemic period.

Variable definitions and measurements

Independent variable

Debt-to-Equity Ratio (DE): Calculated as total debt divided by total equity. This market value-based measure captures the relative weights of debt and equity in the capital structure. Unlike debt-to-assets ratios, DE directly reflects the cushion available to debtholders and the financial risk borne by equity holders (Correia 2019; Myers 1984; Zulvia & Linda 2019).

Dependent variable

The dependent variables employed in this study capture key dimensions of firms' financial performance and risk, and are defined and measured as follows:

Return on Assets (ROA): Calculated as net income divided by total assets, measuring profitability efficiency.

Interest Coverage (IC): Calculated as earnings before interest and tax (EBIT) divided by interest expenses, measuring debt service capacity and financial risk.

Current Ratio (CR): Calculated as current assets divided by current liabilities, measuring short-term liquidity.

Company Growth Rate (CGR): Year-over-year percentage change in total assets, representing firms' growth rate.

Taxation (TAX): Calculated as taxes paid divided by pre-tax income.

Tangibility (TATT): Calculated as sales divided by total assets, measuring asset utilisation efficiency.

Total Revenue (TR): Represented as total revenue, a proxy for firm's size.

Economic crisis variables

The following variables capture the effects of major economic crises on firm-level capital structure decisions:

DUMMY (DURINGGFC): Binary variable equal to 1 for observations during 2008-2009 or 0 otherwise.

DUMMY (DURINGCOV): Binary variable equal to 1 for observations during 2020-2021 or 0 otherwise.

Interaction Terms (INT): These are products of the economic crisis dummies with each standardised independent variable capturing crisis-specific effects on the determinants of capital structure.

Statistical analysis

Modelled formulas

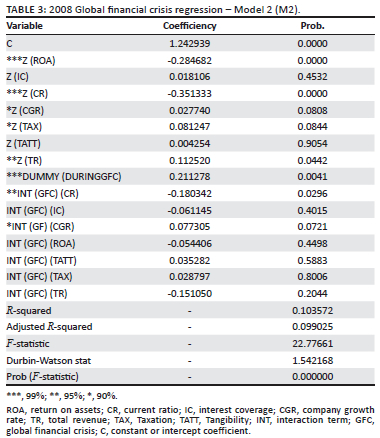

The modelled formulas for this study's final models are denoted next. Similar to Ahmed, Nugraha and Hágen (2024), our study consists of three different formulas. Moreover, all three regression models were conducted on data across the period 2004-2022, thereby necessitating the use of period dummy variables for Model 2 and Model 3 (Ahmed et al. 2024). The two alternative models were utilised for more robustness. For instance, Model 2 is the same regression restricted to the 2008 GFC years (2008-2009) and excludes the COVID-19 terms, while Model 3 is the regression restricted to the COVID-19 pandemic years (2020-2021), excluding the 2008 GFC terms. This allows for greater consistency and provides a comparison of the sub-period results (Ahmed et al. 2024).

To empirically examine the relationship between firm-specific determinants, economic crisis conditions, and capital structure outcomes, the study specifies a series of panel regression models, presented as follows:

Main Model (Model 1): Full period (2004-2022) with both economic crisis dummies and interactions:

Alternative Model (Model 2): Period with only the 2008 GFC crisis effects:

Alternative Model (Model 3): Period with only the COVID-19 pandemic crisis effects:

Here, X represents the vector of firm-specific variables, GFC and COV are crisis dummies and subscripts i and t denote firms and time periods.

Model fit estimation strategies

To ensure the statistical robustness and validity of the estimated models, several diagnostic tests and model-fitting strategies were employed, consistent with established panel data econometric standards:

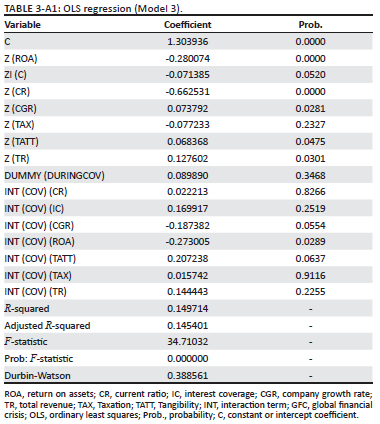

Pooled OLS: Similar to Demirgüç-Kunt et al. (2015), the initial ordinary least squares (OLS) estimation in Appendix 1 (Table 1-A1-Table 3-A1) revealed significant autocorrelation (Durbin-Watson statistics < 0.4) and heteroskedasticity (Breusch-Pagan test p < 0.01), which ultimately violated OLS assumptions (Field 2013).

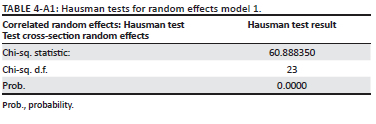

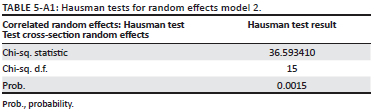

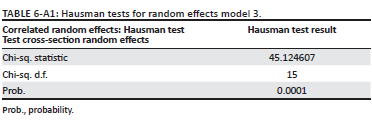

Fixed vs. Random Effects: Similar to Mouton and Smith (2016), panel least squares regression was initially conducted. The results indicated the presence of serial correlation and an likehood ratio (LR) test indicated heterogeneity. The Hausman test in Appendix 1 (Table 4-A1, Table 5-A1, and Table 6-A1) was subsequently used to determine if a fixed or random effect model applies to the data. The Hausman test was significant (p < 0.05), indicating that a fixed effect model applies. As the fixed model results still indicated the presence of serial correlation, a generalised least squares (GLS) model using period Seemingly Unrelated Regression estimates, which corrects for heteroskedasticity and general correlation of observations within a cross-section and provides (robust) panel corrected standard errors, was used.

Generalised Least Squares: To address autocorrelation while also maintaining the random effect's structure, similar to Ahmed et al. (2024), we employed feasible GLS with autoregressive AR(1) disturbances. This approach is particularly suitable for unbalanced panels where firm-specific effects are present but not correlated with the explanatory variables. The GLS regression model addressed both heteroskedasticity and autocorrelation while maintaining efficiency. The correction for autoregressive AR(1) errors is important given that the persistence is typically observed in capital structure (Ahmed et al. 2024; Lyubov & Heshmati 2023).

Diagnostic tests and robustness

Several robustness tests and diagnostic procedures were used to ensure the models' validity:

Multicollinearity: Multicollinearity was assessed using variance inflation factor (VIF). None of the variables exhibited multicollinearity using the VIF threshold of 10, and despite a high correlation between TAX and TR (0.789), the VIFs remained below 10, suggesting that multicollinearity does not severely bias the estimates. A sensitivity analysis excluding TAX yields qualitatively similar results (Field 2013).

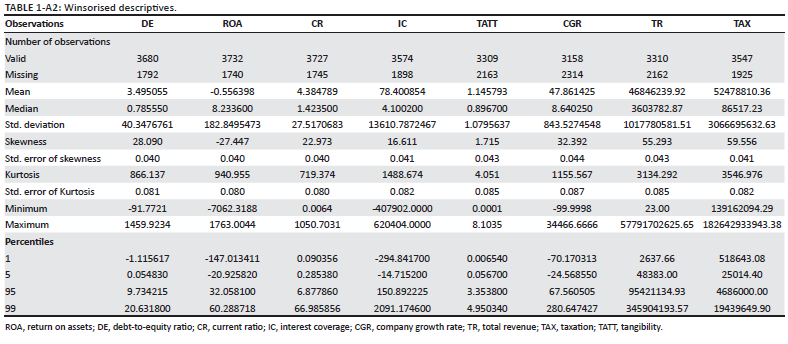

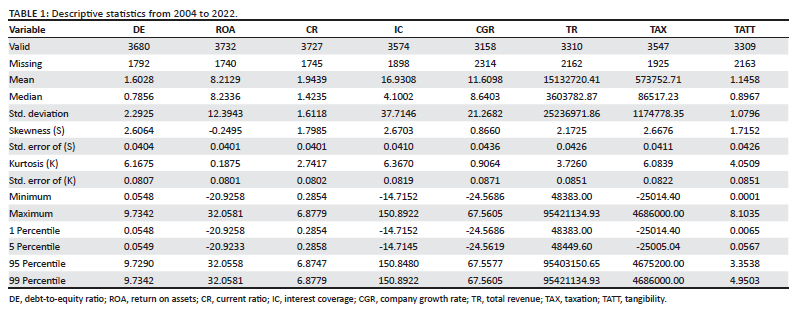

Outliers: Initial descriptive statistics in Appendix 2 (Table 1-A2) were winsorised using 1% and 99% winsorisation, which proved to be insufficient given persistent skewness. Final 5% and 95% winsorisation (Table 1) reduced the influence of extreme observations while preserving crisis-period variation (Singh, Wahi & Kapur 2022).

Autocorrelation: Post-estimation Durbin-Watson statistics in Table 2, Table 3, and Table 4 (1.53-1.54) fall within acceptable ranges (1.5-2.5), confirming that the GLS correction adequately addresses serial correlation (Field 2013).

Model Fit: F-statistics (Table 2-Table 4) are highly significant (p < 0.001) for all models, although R-squared values (10% - 16%) suggest substantial unexplained variation, which is common in capital structure studies given unobserved factors such as management quality and market timing.

Interpretation of the coefficient framework and interaction terms

The coefficient interpretation followed a structured approach that includes:

Main effects (β): Representation of the relationship between determinants of capital structure and debt-to-equity ratios during noneconomic crisis periods.

Crisis dummies (γ): Captured the average shift and change in debt-to-equity ratios during each economic crisis period.

Interaction effects (θ): Measured the importance and significance of each capital structure determinant and how it changes during each economic crisis. A significant interaction term indicates that the economic crisis altered the relationship between that determinant of capital structure and debt-to-equity ratios. The sign and magnitude reveal whether the crisis strengthened, weakened or reversed the normal relationship.

Moreover, unlike dynamic panel models that estimate a 'speed of adjustment' to target leverage, our study focused on static leverage levels across each economic crisis. Our research explored the differences in observed debt-to-equity ratios between crisis and non-crisis periods, rather than modelling the dynamics of how quickly firms revert to a target debt ratio. This choice aligns with many capital structure studies that treat leverage as the dependent level (i.e. cross-sectional panel regressions). Consequently, the regression coefficients captured how capital structure levels vary with firm characteristics and crisis indicators, without imposing a target adjustment process, which would require lagged dependent variables and generalized method of moments (GMM) techniques.

Ethical considerations

An application for full ethical approval was made to the Committee for Research Ethics at the Department of Financial Management, Faculty of Economic and Management Sciences, University of Pretoria, and ethics consent was received on 22 October 2024. The ethics approval number is EMS221/24.

Results

Descriptive analysis

The descriptive statistics presented in Table 1 indicate that the leverage (DE) ratio exhibited substantial variation, with a mean of 1.603 and median of 0.786. Additionally, the positive skewness indicates a subset of highly leveraged JSE-listed firms during the period. The difference between mean and median suggests that the distribution has a long right tail, consistent with a few firms maintaining very high leverage ratios. Profitability (ROA) shows reasonable variation with negative skewness, indicating that some firms experienced losses. The liquidity ratio (CR) displays positive skewness, suggesting that most firms maintain moderate liquidity, with a few holding excessive current assets. Interest coverage (IC) exhibits extreme positive skewness and kurtosis, reflecting a few firms with very high coverage ratios.

Economic crisis period comparisons

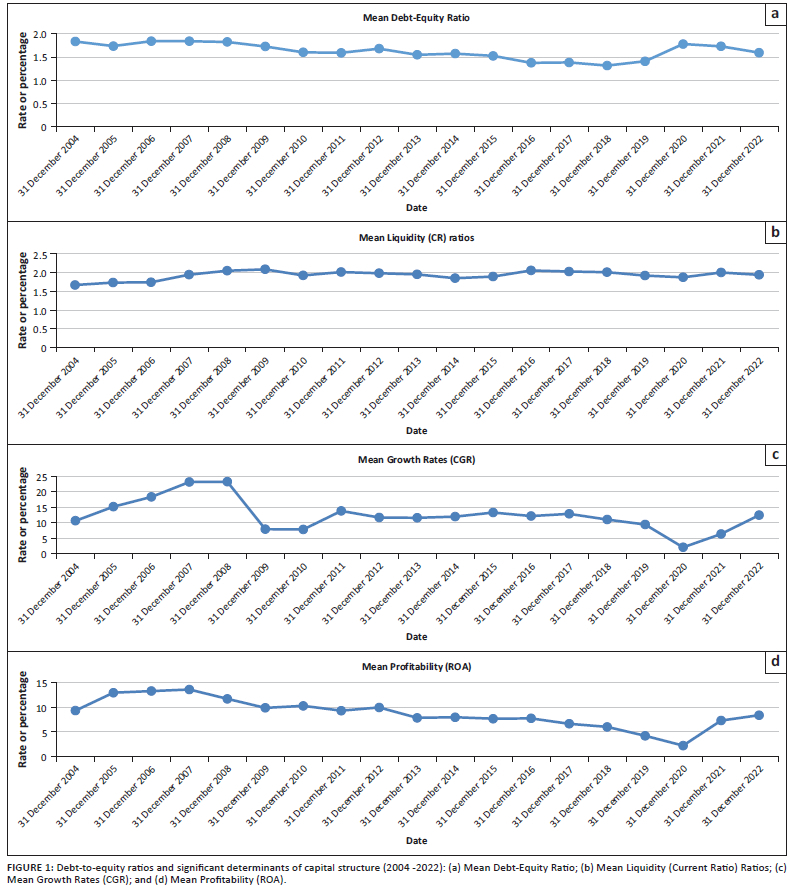

The trends in Figure 1 suggest that during the 2008 GFC, mean DE declined from 1.838 (2007) to 1.725 (2009), indicating a 6.2% deleveraging. Simultaneously, mean CR increased from 1.944 (2007) to 2.087 (2009), indicating liquidity hoarding by JSE-listed firms. Company Growth Rate declined significantly from 23.21% (2008) to 7.87% (2009). However, the COVID-19 pandemic patterns are significantly different. Mean DE increased from 1.406 (2019) to 1.777 (2020), indicating a 26.4% increase in leverage before reducing to 1.727 (2021). Moreover, profitability ROA plummeted from 4.219 (2019) to 2.239 (2020) before recovering to 7.317 (2021). Company Growth Rate showcased a similar V-shaped pattern: 9.39% (2019), 2.01% (2020), 6.32% (2021). These patterns suggest fundamentally different economic crisis responses by JSE-listed firms. They indicate gradual deleveraging during the 2008 GFC in comparison to a sharp increase in leverage followed by a partial reversal during the COVID-19 pandemic.

Regression results

Hypotheses 1

H1: We expect the 2008 global financial crisis and the COVID-19 pandemic to impact the capital structure of Johannesburg Stock Exchange-listed firms differently.

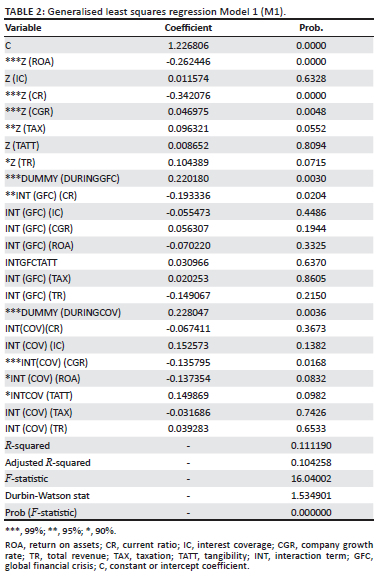

Table 2-Table 4 results indicate that both economic crisis dummy variables were positive and highly significant: DUMMY(DURINGGFC): β = 0.220, p = 0.003 (M1); β = 0.211, p = 0.004 (M2) DUMMY(DURINGCOV): β = 0.228, p = 0.004 (M1); β = 0.212, p = 0.007 (M3); however, the results mask the divergent underlying dynamics. The positive DUMMY(DURINGGFC) coefficient appears paradoxical given the observed deleveraging during the period. However, this is a reflection of the model controlling for deteriorating fundamentals, declining growth and profitability, which would otherwise predict even lower leverage. Moreover, the positive coefficient indicates that (conditional on fundamentals) JSE-listed firms maintained higher leverage positions during the 2008 GFC than the model would predict possibly because of the inability of debt repayments or equity issuance. The DUMMY(DURINGCOV) positive coefficient aligns with observed leverage increases, confirming that JSE-listed firms increased leverage despite deteriorating internal factors. The similar magnitude of coefficients 0.220; 0.228 (M1) and 0.211 (M2); 0.212 (M3) suggests fundamentally different adjustment mechanisms revealed through the interaction terms during the two economic crisis periods.

Hypotheses 2

H2: We expect different internal firm-related factors or determinants of capital structure during the 2008 global financial crisis and the COVID-19 pandemic.

During the 2008 GFC, only the liquidity interaction INT(GFC)(CR) is significant: β = −0.193, p = 0.020 (M1); β = −0.180, p = 0.030 (M2), indicating that liquidity was the dominant determinant of capital structure. The negative coefficient suggests that liquid JSE-listed firms deleveraged more aggressively, which indicates a conservative approach towards leverage and pecking order theory. The marginally significant interaction with growth INT(GFC)(CGR) in Table 3 (M3) (β = 0.077, p = 0.072) suggests that growing JSE-listed firms maintained relatively higher leverage positions possibly because of pre-crisis obligations.

During the COVID-19 pandemic, various determinants of capital structure showcased significant interactions: INT(COV)(CGR) results - β = −0.136, p = 0.020 (M1); β = −0.147, p = 0.009 (M3) - indicate that JSE-listed firms with declining growth levels increased leverage, suggesting desperation borrowing. INT(COV)(ROA) results were moderately significant - β = −0.137, p = 0.083 (M1); β = −0.131, p = 0.098 (M3), suggesting that JSE-listed firms that were less profitable borrowed more, which contradicts the conventional pecking order predictions. Moreover, the moderate significance for INT(COV)(TATT) results - β = 0.143, p = 0.098 (M1) - suggests that JSE-listed firms with more tangible assets leveraged them as collateral. The COVID-19 pandemic trend reveals operational stresses drove the financing needs of JSE-listed firms, regardless of traditional financial constraints and general conservative approach compared to the 2008 GFC.

Hypotheses 3

H3: We expect that different capital structure theories be applied during the 2008 global financial crisis and COVID-19 pandemic by Johannesburg Stock Exchange-listed firms

The 2008 GFC supports the pecking order theory. The significant negative interaction with liquidity combined with the insignificant effect of profitability suggests that JSE-listed firms prioritised internal funds. Moreover, deleveraging despite positive crisis dummy indicates limited quantity and constraints within the debt markets, forcing firms to rely on internal funds, which is consistent with pecking order theory when faced with severe financing constraints.

The COVID-19 pandemic on the other hand supported a mixture of capital structure theories. The negative interaction between profitability and growth suggests trade-off theory, whereby JSE-listed firms balanced the need for survival by increasing leverage. However, the exhaustion of internal funds before borrowing also reflects significantly lower costs of borrowing, as SARB drastically reduced rates during this period or pecking order constraints. The tangibility effect supports both theories providing collateral (trade-off) while enabling borrowing when internal funds start depleting (pecking order).

Discussion

Interpretation of the different crisis responses

The contrasting capital structure adjustments during the 2008 GFC and COVID-19 pandemic indicate fundamental differences in two economic crisis impact and their implications for corporate financing.

The impact of the 2008 global financial crisis

The 2008 GFC originated in financial markets, as the subprime mortgage collapse triggered a global freeze on credit. For JSE-listed firms, this manifested as a knock-on credit shock passed on by the US markets. Commercial banks tightened lending standards, international capital markets became inaccessible, and risk premiums increased. The significant negative interaction between liquidity and leverage INT(GFC)(CR) indicates how this played out. Johannesburg Stock Exchange-listed firms with cash reserves used them to reduce debt, while those without liquidity struggled to refinance existing obligations. This trend is strongly supportive of the pecking order theory. Johannesburg Stock Exchange-listed firms could not access external financing at reasonable costs, forcing them to rely on internal funds. Moreover, the insignificant interaction with profitability suggests that even the more profitable firms faced credit rationing, as they found it difficult to leverage their earnings capacity into borrowing capacity. The gradual deleveraging observed (6.2% over 2 years) reflects the pace at which firms could generate internal funds to pay down debt. Unlike sudden deleveraging through distressed asset sales or emergency equity issuance, this pattern suggests managed adjustment within severe constraints. Moreover, the positive crisis dummy coefficient, after controlling for fundamentals, indicates that JSE-listed firms would have deleveraged more aggressively if possible; however, they were constrained by limited equity market access and the need to maintain operations.

The impact of the COVID-19 pandemic

The COVID-19 pandemic presented an entirely different crisis effect. The shock began in the real economy when lockdowns halted operations, which resulted in supply chains getting fractured and demand evaporating. Financial markets initially panicked but recovered quickly because of unprecedented central bank intervention. The SARB cut rates aggressively and provided liquidity support, keeping credit markets functional even as the real economy collapsed. This operational crisis created liquidity needs that overwhelmed normal financing preferences for many firms. The significant negative interactions between growth INT(COV)(CGR) and profitability INT(COV)(ROA) suggest desperation borrowing, as JSE-listed firms with collapsing sales and profits borrowed more. Moreover, this finding violates pecking order predictions; however, it supports the trade-off theory. Johannesburg Stock Exchange-listed firms increased leverage to survive, betting that recovery would allow deleveraging before distress costs materialised and rates started increasing. The tangibility interaction INT(COV)(TATT) provides crucial insights, as it suggests that JSE-listed firms with physical assets could collateralise for emergency borrowing, while service-oriented firms faced constraints. This suggests contrasting divergence, as asset-rich firms increased leverage substantially, while asset-light firms may have faced liquidity constraints. Moreover, the 26.4% leverage surge in 2020 followed by partial reversal in 2021 suggests that JSE-listed firms borrowed aggressively during the hard lockdown period and then started deleveraging as operations recovered.

Capital structure implications and possible applications

Traditional pecking order theory assumes financing preferences can be expressed through choices. The 2008 GFC showed that extreme credit rationing can make the hierarchy a constraint rather than a preference. Although firms may desire debt financing, they face quantity rationing regardless of price willingness. The theory requires modification to distinguish between preference-based and constraint-based pecking orders. During COVID-19, the theory's predictions failed because the assumption of available internal funds was violated. When operations halt, even profitable firms exhaust cash reserves quickly. The modified pecking order under operational crises might be: (1) existing cash reserves; (2) emergency credit facilities; (3) asset-backed borrowing; (4) unsecured debt at any price; (5) distressed equity issuance; and (6) liquidation. The traditional trade-off theory assumes that firms can adjust towards target leverage by comparing marginal benefits and costs. Both crises show this assumption fails under extreme conditions. However, during 2008, firms could not reach targets because of market dysfunction. During COVID-19 pandemic, survival concerns dominated optimisation and firms accepted leverage far above normal targets in order to survive. The theory needs crisis-contingent versions acknowledging that target leverage becomes irrelevant when firms face existential threats. The relevant trade-off shifts from 'tax benefits versus bankruptcy costs' to 'survival probability versus future distress costs'. Moreover, this explains why JSE-listed firms rationally accepted seemingly excessive leverage during the COVID-19 because the alternative was immediate failure.

Our findings suggest different theories explain behaviours under different crisis types:

Financial crises: The pecking order theory is supportive, but as a constraint rather than a preference.

Operational crises: A modified trade-off theory applies, with firm survival replacing optimisation and targets.

Normal periods: Conventional theories apply, with firms expressing preferences within their available options.

Examining JSE-listed firms could provide broader lessons for other emerging markets. Emerging markets face amplified crisis impacts because of smaller capital markets, resulting in less financing alternatives when banks restrict access to lending; currency exposure issues because of the depreciation of the South African rand (ZAR) during crises, which results in increased foreign debt burdens; institutional weaknesses because of slower policy responses and weaker creditor protection; and information opacity as greater information asymmetry exacerbates market dysfunction. These factors explain why South African firms showed more extreme adjustments than developed market counterparts during both crises.

Successful navigation of economic crises requires emerging market firms to maintain higher base liquidity, as the premium on cash reserves exceeds developed market norms. Diversifying financial sources because of overreliance on bank lending could be fatal during a financial crisis. Matching currency exposure because of foreign currency debt amplifies crisis impacts. Building firms with more collateral buffers is beneficial because tangible assets provide crucial financing flexibility.

The firms that weathered the storm of both crises successfully exhibited these characteristics prior to the crisis period because crisis management begins with pre-crisis preparation.

Our study also informs policy responses for future crises. Our findings suggest that policy responses should match crisis characteristics. For financial crises, policy responses should focus on bank recapitalisation, credit guarantees and market liquidity. For operational crises, policy responses should focus on government interventions and providing direct support (grants, subsidies) and easier access to credit. However, the South African government's loan guarantee scheme during the COVID-19 pandemic addressed credit access but could not replace lost revenues, alluding to continued financial stress despite policy support. Reducing emerging market vulnerabilities to operational crises requires developing corporate bond markets, alternatives to bank-dependent financing, and equity market depth, which could enable emergency capital raising, as well as derivative markets, which allow firms to manage risk without expanding their balance sheet. These structural improvements could assist in reducing crisis vulnerability more than post-crisis interventions.

Although our findings provide significant insights, the purpose of conducting this study was primarily intended to compare the impact that two different economic crises had on the capital structure of JSE-listed firms, the significant determinants of capital during both crisis periods, and the capital structure theories applied during the two crisis periods. In order to gain further insights into the topic, we suggest that future research should consider survivorship by including failed firms, which could potentially provide more accuracy on the impact of crises; explore industry-specific effects (textile vs. consumer goods/retailers vs. telecoms vs. mining) and include small and medium enterprise (SME) if sufficient data are available. Moreover, from a methodological perspective, future studies should consider dynamic modelling by including speed of adjustment models, which could quantify convergence rates; consider threshold effects, as nonlinear models might capture tipping points in crisis responses; and provide an international comparison, as multicountry studies could isolate institutional factors, especially within emerging markets. These extensions would deepen understanding of crisis-period capital structure dynamics.

Conclusion

This study provides the first systematic comparison of how fundamentally different economic crises affect capital structure in an emerging market context. By examining JSE-listed firms during the 2008 GFC and the COVID-19 pandemic, we document distinct adjustment patterns that challenge universal applications of capital structure theories.

By providing a comparative analysis, this study's findings shed light and provided insights into how two economic crises presented different economic and market conditions, both from a micro and macro perspective, and the different risks associated with each economic crisis. Our findings suggest that the 2008 GFC triggered conservative deleveraging behaviour among JSE-listed firms, which was driven by credit supply constraints. Liquidity emerged as the dominant determinant of capital structure as liquid firms reduced debt levels more aggressively, which supports the pecking order theory; however, it operated as a binding constraint rather than a preference. The 6.2% gradual deleveraging reflects the pace at which internal funds serve as an alternative financing source if the access of external financing is restricted. The COVID-19 pandemic produced contrasting dynamics as firms increased leverage by 26.4% mainly because of operational collapses rather than financial constraints. Profitability and growth became significant negative determinants of capital structure as firms with worse performance levels borrowed more. Moreover, this finding violates traditional pecking order theory predictions but aligns with survival-focused trade-off considerations. This is further confirmed by the subsequent partial deleveraging in 2021, which suggests that this was driven by crisis borrowing rather than structural recapitalisation.

These findings contribute to the existing capital structure theories by demonstrating that crisis type matters, as financial crises and operational crises trigger fundamentally different financing responses that require different capital theoretical approaches. Furthermore, our findings indicate that no single theory explains firm behaviour across all conditions, which suggests that theory contingency is vital during different economic conditions. The pecking order is supportive under credit constraints, while the modified trade-off theory explains survival-driven borrowing. Moreover, as institutional weaknesses and market limitations amplify the impact of crises, modified theoretical predictions can be vital for firms operating in emerging markets. For practitioners, this study highlights how effective crisis responses require accuracy when identifying the type of crisis in order to implement appropriate financing strategies. The generic 'crisis management' approach fails to recognise that credit crunches require strong liquidity positions, while operational disruptions may justify or force firms to increase leverage more aggressively. For policymakers, the findings of this study highlight that crisis interventions must match crisis characteristics. Credit market support could help during financial crises; however, it does not substitute for significant revenue losses during operational disruptions.

As economic uncertainties persist globally, understanding how different shocks could affect corporate financing decisions becomes more vital. This study demonstrates how emerging market firms can successfully navigate diverse economic crises but only with financing strategies that adapt to crisis-specific characteristics and conditions. The contrasting responses to the 2008 GFC and COVID-19 crises provide a roadmap for managing future disruptions, whether they emerge from financial markets, operational challenges or other unknown novel sources. Our findings ultimately suggest that capital structure management in emerging markets requires dynamic, state-contingent approaches that recognise the constraints imposed by underdeveloped financial systems and the opportunities created by policy responses. The static optimisation models give way to survival-focused adaptation, with successful firms being those that maintain the flexibility to adjust strategies as crisis characteristics reveal themselves.

Acknowledgements

The authors would like to acknowledge Dr. Marthi Pohl for her contribution to the data analysis of the study.

Competing interests

The authors declare that they have no financial or personal relationships that may have inappropriately influenced them in writing this article.

Authors' contributions

M.F.T. and F.E.T. contributed to the design and implementation of the research, to the analysis of the results and to the writing of the manuscript. Both M.F.T. and F.E.T. contributed to developing the topic idea, the theory underlying the study, the computations of the data and the interpretations of the results.

Funding information

This research received no specific grant from any funding agency in the public, commercial or not-for-profit sectors.

Data availability

Raw data were generated at the University of Pretoria. Derived data supporting the findings of this study are available from the corresponding author, F.E.T., on request.

Disclaimer

The views and opinions expressed in this article are those of the authors and do not necessarily reflect the official policy or position of any affiliated agency of the authors or that of the publisher. The authors are responsible for this article's results, findings and content.

References

Ahmed, A.M., Nugraha, D.P. & Hágen, I., 2024, 'Assessing the impact of COVID-19 on capital structure dynamics: Evidence from GCC economies', Economies 12(5), 103. https://doi.org/10.3390/economies12050103 [ Links ]

Balios, D., Daskalakis, N., Eriotis, N. & Vasiliou, D., 2016, 'SMEs capital structure determinants during severe economic crisis: The case of Greece', Cogent Economics & Finance 4(1), 1145535. https://doi.org/10.1080/23322039.2016.1145535 [ Links ]

Benmelech, E. & Bergman, N.K., 2018, 'Credit market freezes', NBER Macroeconomics Annual 32(1), 493-526. https://doi.org/10.1086/696065 [ Links ]

Campello, M., 2003, 'Capital structure and product markets interactions: Evidence from business cycles', Journal of Financial Economics 68(3), 353-378. https://doi.org/10.1016/S0304-405X(03)00070-9 [ Links ]

Chatzinas, G. & Papadopoulos, S., 2018, 'Trade-off vs. pecking order theory: Evidence from Greek firms in a period of debt crisis', International Journal of Banking, Accounting and Finance 9(2), 170-191. https://doi.org/10.1504/IJBAAF.2018.092133 [ Links ]

Chen, L.-J. & Chen, S.-Y., 2011, 'How the pecking-order theory explain capital structure', Journal of International Management Studies 6(3), 92-100. [ Links ]

Correia, C., 2019, Financial management, 9th edn., Juta and Company (Pty) Ltd, Cape Town. [ Links ]

Dang, C., Li, Z.F. & Yang, C., 2018, 'Measuring firm size in empirical corporate finance', Journal of Banking & Finance 86, 159-176. https://doi.org/10.1016/j.jbankfin.2017.09.006 [ Links ]

Danso, A. & Adomako, S., 2014, 'The financing behaviour of firms and financial crisis', Managerial Finance 40(12), 1159-1174. https://doi.org/10.1108/MF-04-2014-0098 [ Links ]

De Souza, T.B., Carraro, W.H. & Pinheiro, A.B., 2022, 'COVID-19 pandemic impacts on the relationship between capital structure and performance: Analysis of companies listed on B3', Revista Ibero-Americana de Estratégia - RIAE 21(2), 1-23. https://doi.org/10.5585/riae.v21i2.20899 [ Links ]

Deesomsak, R., Paudyal, K. & Pescetto, G., 2004, 'The determinants of capital structure: Evidence from the Asia Pacific region', Journal of Multinational Financial Management 14(4-5), 387-405. https://doi.org/10.1016/j.mulfin.2004.03.001 [ Links ]

Demirgüç-Kunt, A., Martinez Peria, M.S. & Tressel, T., 2015, 'The impact of the global financial crisis on firms' capital structure', World Bank Policy Research Working Paper 7522, viewed n.d., from https://ssrn.com/abstract=2706884. [ Links ]

Deviyanti, D.R., Ramadhani, H., Ginting, Y.L., Fitria, Y., Yudaruddin, Y.A. & Yudaruddin, R., 2023, 'A global analysis of the COVID-19 pandemic and capital structure in the consumer goods sector', Journal of Risk and Financial Management 16(11), 472. https://doi.org/10.3390/jrfm16110472 [ Links ]

Eljelly, A.M.A., 2004, 'Liquidity-profitability tradeoff: An empirical investigation in an emerging market', International Journal of Commerce and Management 14(2), 48-61. https://doi.org/10.1108/10569210480000179 [ Links ]

Elsas, R. & Florysiak, D., 2008, 'Empirical capital structure research: New ideas, recent evidence, and methodological issues', Discussion Paper 2008-10, Institute for Finance & Banking, Ludwig-Maximilians-University Munich, Munich. [ Links ]

Field, A., 2013, Discovering statistics using IBM SPSS statistics, Sage Publications, London. [ Links ]

Fosberg, R.H., 2013, 'Short-term debt financing during the financial crisis', International Journal of Business and Social Science 4(8), 1-5. [ Links ]

Garay, U., 2003, 'The Asian financial crisis of 1997-1998 and the behavior of Asian stock markets', A Web Journal of Applied Topics in Business and Economics 149, 337-360. [ Links ]

Glen, J.D. & Pinto, B., 1994, 'Emerging capital markets and corporate finance', The Columbia Journal of World Business 29(2), 30-43. https://doi.org/10.1016/0022-5428(94)90003-5 [ Links ]

Gocmen, T. & Sahin, O., 2014, 'The determinants of bank capital structure and the global financial crisis: The case of Turkey', Journal of Applied Finance and Banking 4(5), 55-69. [ Links ]

Grigore, M. & Stefan-Duicu, V., 1976, 'Agency theory and optimal capital structure', Journal of Financial Economics 3, 305-360. https://doi.org/10.1016/0304-405X(76)90026-X [ Links ]

Günay, S.G., 2002, 'The impact of recent economic crisis on the capital structure of Turkish corporations and the test of static trade-off theory: Implications for corporate governance system', in International Conference in Economics, Economic Research Center/METU, Ankara, Turkey, September 11-14, 2002, pp. 1-21. [ Links ]

Halling, M., Yu, J. & Zechner, J., 2020, 'How did COVID-19 affect firms' access to public capital markets?', The Review of Corporate Finance Studies 9(3), 501-533. https://doi.org/10.1093/rcfs/cfaa008 [ Links ]

Harris, M. & Raviv, A., 1991, 'The theory of capital structure', The Journal of Finance 46(1), 297-355. [ Links ]

Harrison, B. & Widjaja, T.W., 2014, 'The determinants of capital structure: Comparison between before and after financial crisis', Economic Issues 19(2), 55-82. [ Links ]

Hotchkiss, E.S., Nini, G. & Smith, D.C., 2021, 'The role of external capital in funding cash flow shocks: Evidence from the COVID-19 pandemic', SSRN Electronic Journal 149, 337-360. https://doi.org/10.2139/ssrn.3723001 [ Links ]

Huang, H. & Ye, Y., 2021, 'Rethinking capital structure decision and corporate social responsibility in response to COVID-19', Accounting & Finance 61(3), 4757-4788. https://doi.org/10.1111/acfi.12740 [ Links ]

Hussain, R.Y., 2022, 'Do leverage decisions mediate the relationship between board structure and insolvency risk? A comparative mediating role of capital structure and debt maturity', South Asian Journal of Business Studies 11(1), 104-121. https://doi.org/10.1108/SAJBS-05-2020-0150 [ Links ]

Iqbal, A. & Kume, O., 2014, 'Impact of financial crisis on firms' capital structure in UK, France, and Germany', Multinational Finance Journal 18(3-4), 249-280. https://doi.org/10.17578/18-3/4-3 [ Links ]

Jansen, K., Michiels, A., Voordeckers, W. & Steijvers, T., 2022, 'Financing decisions in private family firms: A family firm pecking order', Small Business Economics 61, 495-515. https://doi.org/10.1007/s11187-022-00711-9 [ Links ]

Jeasakul, P., Lim, C.H. & Lundback, E., 2014, 'Why was Asia resilient? Lessons from the past and for the future', Journal of International Commerce, Economics and Policy 5(2), 1450002. https://doi.org/10.1142/S1793993314500021 [ Links ]

Ju, N., Parrino, R., Poteshman, A.M. & Weisbach, M.S., 2005, 'Horses and rabbits? Trade-off theory and optimal capital structure', Journal of Financial and Quantitative Analysis 40(2), 259-281. https://doi.org/10.1017/S0022109000002301 [ Links ]

Kang, M. & Ausloos, M., 2017, 'An inverse problem study: Credit risk ratings as a determinant of corporate governance and capital structure in emerging markets: Evidence from Chinese listed companies', Economies 5(4), 47. https://doi.org/10.3390/economies5040047 [ Links ]

Kochhar, R., 1996, 'Explaining firm capital structure: The role of agency theory vs. transaction cost economics', Strategic Management Journal 17(9), 713-728. https://doi.org/10.1002/(SICI)1097-0266(199611)17:9<713::AID-SMJ844>3.0.CO;2-9 [ Links ]

Kruk, S., 2021, 'Impact of capital structure on corporate value - Review of literature', Journal of Risk and Financial Management 14(4), 155. https://doi.org/10.3390/jrfm14040155 [ Links ]

Kurshev, A. & Strebulaev, I.A., 2015, 'Firm size and capital structure', Quarterly Journal of Finance 5(3), 1550008. https://doi.org/10.1142/S2010139215500081 [ Links ]

Lazarus, L.L., Acheampong, A.K., Paul, M., Prince, S., Peter, A. & Rakibu, Z.S., 2024, 'Does the COVID-19 pandemic matter in the capital structure decisions of firms? An empirical study of Ghanaian non-financial listed firms', Open Journal of Business and Management 12(3), 1635-1650. https://doi.org/10.4236/ojbm.2024.123088 [ Links ]

Lyubov, T. & Heshmati, A., 2023, 'Impact of financial crises on the dynamics of capital structure: Evidence from Korean listed companies', The Singapore Economic Review 68(3), 867-898. https://doi.org/10.1142/S0217590819500498 [ Links ]

Mbatha, V.M. & Alovokpinhou, S.A., 2022, 'The structure of the South African stock market network during COVID-19 hard lockdown', Physica A: Statistical Mechanics and Its Applications 590, 126770. https://doi.org/10.1016/j.physa.2021.126770 [ Links ]

Miller, M., 1958, 'The cost of capital, corporation finance and the theory of investment', The American Economic Review 48(3), 261-297. [ Links ]

Miller, M.H., 1977, 'Debt and taxes', The Journal of Finance 32(2), 261-275. https://doi.org/10.1111/j.1540-6261.1977.tb03267.x [ Links ]

Modigliani, F. & Miller, M.H., 1958, 'The cost of capital, corporation finance and the theory of investment', The American Economic Review 48(3), 261-297. [ Links ]

Modigliani, F. & Miller, M.H., 1963, 'Corporate income taxes and the cost of capital: A correction', The American Economic Review 53(3), 433-443. [ Links ]

Moradi, A. & Paulet, E., 2019, 'The firm-specific determinants of capital structure - An empirical analysis of firms before and during the Euro crisis', Research in International Business and Finance 47, 150-161. https://doi.org/10.1016/j.ribaf.2018.07.007 [ Links ]

Mouton, M. & Pelcher, L., 2023, 'Capital structure and COVID-19: Lessons learned from an emerging market', Acta Commercii - Independent Research Journal in the Management Sciences 23(1), 1125. https://doi.org/10.4102/ac.v23i1.1125 [ Links ]

Mouton, M. & Smith, N., 2016, 'Company determinants of capital structure on the JSE Ltd and the influence of the 2008 financial crisis', Journal of Economic and Financial Sciences 9(3), 789-806. https://doi.org/10.4102/jef.v9i3.71 [ Links ]

Myers, S.C., 1984, 'The capital structure puzzle', Journal of Finance 39(3), 575-592. https://doi.org/10.2307/2327916 [ Links ]

Olowookere, J.K., Odetayo, T.A., Adeyemi, A.Z. & Oyedele, O., 2022, 'Impact of COVID-19 on working capital management: A theoretical approach', Journal of Business and Entrepreneurship 10(1), 38-47. https://doi.org/10.46273/jobe.v10i1.224 [ Links ]

Pervan, M. & Višić, J., 2012, 'Influence of firm size on its business success', Croatian Operational Research Review 3(1), 213-223. [ Links ]

Proença, P., Laureano, R.M. & Laureano, L.M., 2014, 'Determinants of capital structure and the 2008 financial crisis: Evidence from Portuguese SMEs', Procedia - Social and Behavioral Sciences 150, 182-191. https://doi.org/10.1016/j.sbspro.2014.09.027 [ Links ]

Ramjee, A. & Gwatidzo, T., 2012, 'Dynamics in capital structure determinants in South Africa', Meditari Accountancy Research 20(1), 52-67. https://doi.org/10.1108/10222521211234228 [ Links ]

Sari, N.W., Anwar, M. & Faisal, Y.A., 2022, 'The effect of capital structure and liquidity on profitability before and during the COVID-19 pandemic in telecommunication companies listed on the Indonesian Stock Exchange', Jurnal Bisnis dan Manajemen 23(2), 92-105. https://doi.org/10.24198/jbm.v23i2.2029 [ Links ]

Šarlija, N. & Harc, M., 2012, 'The impact of liquidity on the capital structure: A case study of Croatian firms', Business Systems Research Journal 3(1), 30-36. https://doi.org/10.2478/v10305-012-0005-1 [ Links ]

Shen, H., Fu, M., Pan, H., Yu, Z. & Chen, Y., 2020, 'The impact of the covid-19 pandemic on firm performance', Emerging Markets Finance and Trade 56(10), 2213-2230. https://doi.org/10.1080/1540496X.2020.1785863 [ Links ]

Singh, S., Wahi, G. & Kapur, M., 2022, 'Banks' credit and investment dynamics: Assessing portfolio rebalancing and crowding-out', Reserve Bank of India Working Paper No. 09, Reserve Bank of India, Department of Economic and Policy Research, Mumbai, IN. [ Links ]

Smith, A.D., 2010, 'Agency theory and the financial crisis from a strategic perspective', International Journal of Business Information Systems 5(3), 248-267. https://doi.org/10.1504/IJBIS.2010.031929 [ Links ]

Titman, S. & Wessels, R., 1988, 'The determinants of capital structure choice', The Journal of Finance 43(1), 1-19. https://doi.org/10.1111/j.1540-6261.1988.tb02585.x [ Links ]

Tram, N.T.B., 2016, Testing static trade-off against pecking order models of capital structure: A case of manufacturing companies listed on Ho Chi Minh Stock Exchange (HOSE), International University - HCMC, Ho Chi Minh City. [ Links ]

Tripathy, N. & Asija, A., 2017, 'The impact of financial crisis on the determinants of capital structure of listed firms in India', Journal of International Business and Economy 18(1), 101-121. https://doi.org/10.51240/jibe.2017.1.5 [ Links ]

Zarebski, P. & Dimovski, B., 2012, 'Determinants of capital structure of A-REITS and the global financial crisis', Pacific Rim Property Research Journal 18(1), 3-19. https://doi.org/10.1080/14445921.2012.11104347 [ Links ]

Zulvia, Y. & Linda, M.R., 2019, 'The determinants of capital structure in manufacturing companies listed on the Indonesia Stock Exchange with the firms' size as a moderating variable', KnE Social Sciences 3(11), 715-735. https://doi.org/10.18502/kss.v3i11.4046 [ Links ]

Correspondence:

Correspondence:

Eduard Toerien

eduard.toerien@up.ac.za

Received: 18 Feb. 2025

Accepted: 13 Oct. 2025

Published: 08 Dec. 2025

Appendix 1

Appendix 2

{kind=link}

{kind=link}