Services on Demand

Journal

Article

English (pdf)

English (pdf)

Article in xml format

Article in xml format Article references

Article references

Send this article by e-mail

Send this article by e-mailIndicators

Related links

-

Cited by Google

Cited by Google -

Similars in Google

Similars in Google

Share

Permalink

PermalinkJournal of Contemporary Management

On-line version ISSN 1815-7440

JCMAN vol.17 spe 2 Meyerton 2020

https://doi.org/10.35683/jcm209.121

RESEARCH ARTICLES

An overview of administrative oversight and accountability at municipalities within the Free State Province

JKT SebakamotseI; T Van NiekerkII,

ICentral University of Technology, Department of Government Management, Faculty of Management Sciences tsebakamotse@yahoo.com

IICentral University of Technology, Department of Government Management, Faculty of Management Sciences edwardst@cut.ac.za: ORCID: https://orcid.org/0000-0002-6608-0395

ABSTRACT

In the South African context, oversight and accountability are constitutionally mandated functions of legislatures to scrutinise and oversee executive actions of any organ of state. Section 152 of the Constitution of the Republic of South Africa, 1996 (hereafter referred to as the Constitution, 1996) determines that local communities must receive democratic and accountable governance. This research aimed to determine the current challenges pertaining to administrative oversight and accountability at municipalities within the Free State province. A qualitative research approach was utilised to gain insight into administrative oversight and accountability practices at municipalities within the Free State province as a case study. Findings from the qualitative research indicated that the lack of oversight and accountability leads to the continued disregard of key local government legislation which hampers administrative oversight and accountability. The research found that municipal managers, as the head of the municipality's administration, must ensure that proper administrative internal controls are in place to promote administrative accountability. It was recommended that the oversight role of political oversight bodies and committees need to be strengthened so that the executive can be held to account.

Key phrases: Oversight; administrative accountability; municipal managers and mechanisms to promote administrative accountability

1. INTRODUCTION AND BACKGROUND

Van der Waldt, Van Niekerk, Doyle, Knipe and du Toit (2001:264) maintain that traditionally the term accountability refers to "being answerable for one's behaviour or actions". On the other hand, oversight is used to define numerous activities executed by legislatures to hold executives (public officials) to account. Khalo (2013:581) is of the opinion that financial accountability refers to an account of how municipal funds were used to implement municipal policies as approved by council. Administrative accountability in the context of local government refers to internal structures, mechanisms and systems of control, which include ethical codes of conduct, administrative performance reviews, norms and standards to promote a system of checks and balances (Sibanda 2017:324). As maintained by Botha and Khan in Hussein (1999:42) that administrative accountability refers to all the control mechanisms created to keep the bureaucracy under surveillance and in check. Responsibility is delegated to public officials to fulfil a specific duty that includes aspects such as consent to perform a specific duty or job, obedience to a higher authority and accountability and liability to be answerable to someone or an authority (Thornhill 2015:7879).

According to Sibanda (2017:320), the municipal manager as the head of the municipality's administration must ensure that proper administrative reporting arrangements are in place to promote accountability of the administrative function of the municipality. The municipal manager may develop a system of delegation to promote administrative and operational efficiency. The municipal manager as the accounting officer of the municipality is answerable to the elected representatives (political office-bearers) of the municipality. On the other hand, the elected representatives of the municipality are accountable to the electorate or broader community concerning service delivery and the performance of the municipality. In this manner administrative oversight and accountability are promoted through participatory governance and representation.

The continued poor performance of municipalities in the Free State province remains a concern. Van der Waldt (2015:52) is of the view that the lack of effective oversight and accountability leads to instability and the dysfunctionality of municipalities and creates an environment open to maladministration, fraud and corruption of municipalities of which the municipalities of the Free State cannot be excluded. The latter corresponds with the findings of the Auditor-General Consolidated General Report on the Audit Outcomes of local government of 2016-2017 (Auditor-General of South Africa (AGSA) 2018:3) that the continued lack of oversight, accountability and continued non-compliance with key local government legislation, were the main causes of governance failures.

In this article, the following are discussed: the statutory and legislative frameworks for local government administrative oversight and accountability, the role of national and provincial government, followed by an overview of institutional arrangements to promote administrative accountability within municipalities. The current challenges of administrative oversight and accountability are provided, followed by a discussion of the findings and results of the semi-structured questionnaire administered in selected municipalities of the Free State province to determine the perceptions of municipal officials, ward councillors and political office-bearers concerning administrative oversight and accountability. Finally, specific recommendations were outlined in the conclusion.

2. STATUTORY AND LEGISLATIVE FRAMEWORK

The statutory and legislative framework establishes a basis for oversight and accountable administration and management of municipalities. In this article the following statutory and legislative prescripts are briefly outlined below.

2.1 Constitution of the Republic of South Africa, 1996

In terms of Section 152 and 153 of the Constitution, 1996, local government must fulfil its developmental mandate in an accountable and democratic manner to local communities, and to promote the involvement of local communities in the affairs of local government. In this regard the Constitution, 1996 requires from local government to structure and manage its administration in such a manner that municipalities must budget and plan effectively to prioritise the needs of local communities (Madumo 2015:156; Sirovha & Thornhill 2017:136).

2.2 Local Government: Municipal Systems Act, 2000 (as amended by Act 7 of 2011)

In terms of Section 4(2) of the Local Government: Municipal Systems Act, 2000 (Act 32 of 2000) (hereafter referred to as MSA 2000) the municipal council is the executive and legislative authority of the municipality. The municipal council, as the highest authority in the municipality, has significant powers of approval and oversight responsibilities. According to Madumo (2015:161), the MSA 2000, Section 6(2) provides that municipal administrations are responsible for the following; to be responsive to the developmental needs of their communities; to promote a culture of accountability and public service amongst its municipal officials; to take steps to prevent corrupt activities; to promote co-operation and communication with local communities; to provide the local community with accurate and reliable information about the level and standard of service delivery; and to inform and involve local communities and community organisations in the affairs of local government.

Section 51 of the MSA 2000, states that the municipal manager of a municipality is accountable for the overall performance and administration of the municipality. Section 55 of the MSA 2000, provides that the municipal manager as the head of administration is responsible and accountable for the development of an effective, efficient, economic and accountable municipal administration. Section 56 of the Act makes provision for the appointment of managers directly accountable to the municipal manager while Section 57 sets out the employment contracts for municipal managers and managers directly accountable to the accounting officer of the municipality. In terms of Section 67 of the Act, a municipality must develop an effective, efficient and transparent municipal administration.

2.3 Local Government: Municipal Finance Management Act, 2003 (Act 56 of 2003)

Section 53(1)(c)(ii) of the Local Government: Municipal Finance Management Act, 2003 (hereafter referred to as the MFMA 2003), provides that the municipalities' Service Delivery and Budget Implementation Plan (SDBIP) serves as a basis for performance agreements. Van der Waldt (2015:55) states that the SDBIP serves as a tool to promote accountability. The SDBIP must further make provision for the service delivery targets and performance indicators (Sibanda 2017:326). In addition, the MFMA, Circular 32 of 2006, provides the guidelines for the establishment of the Municipal Public Accounts Committee (MPAC). The MPAC is one of the key oversight mechanisms within the municipality.

2.4 Local Government: Municipal Structures Act, 1998 (Act 117 of 1998) (as amended by Act 51 of 2002)

The Local Government: Municipal Structures Act, 1998 (hereafter referred to as the Municipal Structures Act,1998), was developed to give effect to the vision of the White Paper on Local Government (WPLG), 1998, which includes among other things the development and implementation of an effective performance management system at the local sphere of government (Tsatsire 2008:132). In terms of Section 44(3) and 56(3) of the Municipal Structures Act 1998, the executive committee or the executive mayor is responsible for the development of a performance management system including the development of evaluation criteria and key performance indicators, whereas the municipal manager must implement and manage the performance management reporting system and provides advice to the municipal council regarding the reporting system that must be adopted. Sections 79 and 80 of the Municipal Structures Act 1998 makes provision for the establishment of portfolio committees to exercise oversight on service delivery projects.

Despite numerous constitutional and legislative prescripts mandated to encourage local government to be accountable, the promotion of local government to be accountable remains a challenge in most municipalities. In this regard, the Auditor-General Consolidated General Report on the Audit Outcomes of local government for 2017-2018 (AGSA 2019:2-3) states that the continued non-compliance with key local government legislation of municipalities of the Free State province results in irregularities and limited consequences for transgressions.

3. LITERATURE REVIEW

3.1 The role of national and provincial government

Section 155(7) of the Constitution, 1996, requires that national and provincial spheres of government have the authority (legislative and executive) to ensure that municipalities perform their functions as provided in Schedules 4 and 5 of the Constitution, 1996. Koma (2017:33) avers that provincial governments must develop the capacity of municipalities to ensure that they perform their functions and manage their own affairs.

Landsberg and Graham (2017:164) state that Section 139 of the Constitution, 1996, provides that provincial governments should intervene in the affairs of a municipality where it fails to fulfil an executive obligation. Such interventions may include instructions to require a provincial government to take over the responsibility to fulfil certain functions. A provincial government may issue instructions to a municipal council to take a particular action, or it may dissolve the municipal council and appoint an administrator. Landsberg and Graham (2017:164) further maintain that except for the Department of Cooperative Governance and Traditional Affairs (CoGTA) other role players such as the Office of the Premier of the nine (9) provincial governments, the Provincial Treasuries and the South African Local Government Association (SALGA) must support and monitor all municipalities to ensure the achievement of their constitutional mandate.

The SALGA further implemented numerous support programmes to capacitate municipalities such as the Councillor Induction Programme, the Municipal Audit Support Programme with the aim to improve the municipal administrative leadership, governance, institutional capacity, financial and administrative practices in local government. Although national and provincial governments are obligated by constitutional prescripts to support local government, a concern was raised by the Auditor-General in the audit report for 2016-2017 (AGSA 2017:3) that national and provincial governments do not sufficiently support municipalities. Ndaba (2019) in The Star confirms that the municipalities in the Free State province placed under administration showed no improvement in the Auditor-General's Consolidated General Report on the Audit Outcomes of local government of the 2017-2018 financial year.

The functionality of the political oversight function of the Free State Provincial government and those of the particular municipalities under administration could be questioned in that municipalities placed under administration in the provinces showed little or no improvement. Therefore, one could argue that provincial governments need to do more to capacitate municipalities to achieve their constitutional mandate.

3.2 Administrative oversight of a municipality

The municipal councils can be seen as an important link in the accountability chain, to create an enabling environment for good governance and to promote accountability (Krishnan, 2008:23). According to Van der Walt, Venter, Phutiagae, Nealer, Khalo & Vyas-Doorgapersad (2014:87), political office-bearers fulfil the oversight role over the administration, to ensure that the municipal council resolutions and policies are executed by the municipal administration. Sirovha and Thornhill (2017:140) state that in municipalities with an executive mayor, the executive mayor or mayoral committee members are responsible for overseeing the administration of the municipality to ensure effectiveness and efficiency in service delivery. In a municipality with a collective executive system the mayor is the chairperson of the executive committee. The major provides general political guidance over the fiscal and financial affairs of the municipality and must oversee the exercise of the responsibilities of the accounting officer and the chief financial officer (Thornhill and Cloete 2014:113).

Section 56(2) of the Municipal Structures Act, 1998 provides that the executive mayor is responsible to make recommendations to the municipal council concerning strategies, programmes and services. De Visser (2010:139) point out that the speaker who is in terms of Section 36 of the Municipal Structures Act, 1998 elected amongst the municipal councillors of the municipal council, fulfils a key oversight role to ensure good management of the political executive authority of a municipality.

Nealer (2011:178) submits that a code of conduct was established in line with Schedule 5 of the Municipal Structures Act, 1998. The SALGA (2006:55) provides that councillors are accountable to the people who elected them, and the code of conduct sets the framework that governs their behaviour. The speaker must ensure that members of the municipal council and committees of the municipal council adhere to the requirements of the Code of Conduct of Councillors. In particular Section 11(a) of the Code of Conduct of Councillors, as contained in Schedule 1 of the MSA, 2000 provides that a councillor may not interfere in the management or administration of any department of the municipal council, unless so mandated by council or by the law. Defaulters must be held to account for their actions, especially since the Auditor-General (AGSA 2018:3) warns that political interference and conflict as a result of political factions weakens the council's oversight function. Pauw, van der Linde, Fourie, and Visser (2015:312) warn that a code of conduct does not make councillors virtuous, but that it should promote moral behaviour. Breaches of the code of conduct are regarded in a serious light; hence the Code of Conduct for Municipal Councillors also spells out procedures for a breach of the code.

Apart from the oversight responsibilities of the political office bearers, there are also committees who must fulfil the functions of oversight over municipal administration to ensure that municipalities are able to meet their constitutional obligations. Such committees include the executive committees, mayoral committees, council portfolio committees, municipal public accounts committees and audit committees. Section 32(1) of the Municipal Structures Act, 1998 submits that a municipal council must develop a system of delegation that will maximise administrative and operational efficiency and allow adequate checks and balances. In accordance with that system, appropriate powers that may be delegated by a municipal council include all powers except the power to approve its integrated development plan. Section 80 and Section 79 committees in terms of the Municipal Structures Act, 1998, are significant structures to promote oversight over the municipal administration. Portfolio committees are classified as Section 80 committees and are permanent structures in the municipal council. Section 80 committees or portfolio committees have to report and are accountable to the mayoral committee, while Section 79 committees or portfolio committees report to the municipal council. The MPAC as a Section 79 portfolio committee is the key oversight structure to hold the municipal administration to account (Kraai, Holtzhausen & Malan 2017:64; Napier 2007:387; Sirovha & Thornhill 2017:151; Van der Waldt 2015:58).

In light of the above, the Auditor-General Consolidated General Reports on the Audit Outcomes of local government of 2016-2017 and 2017-2018 state that the following factors are major contributors to oversight failures in most municipalities; lack of oversight by municipal councils including the mayor; political interferences by councillors in the administration of local government which weakens oversight; not all municipalities implement the recommendations of MPACs because of the inadequate legal mandate of the committees to enforce recommendations; and continued non-compliances with key municipal legislations creates an environment that makes it easy to commit fraud and corruption (AGSA 2017:54-55; AGSA 2019:28). The accountable role of the municipal manager as the head of the municipal administration is discussed below.

3.3 The municipal manager

According to Craythorne (2006:190), it is a statutory requirement of a municipality to have a municipal administration and the administrative leadership of the municipality is vested in the municipal manager and the heads of departments/directorates. The general financial management functions of the municipal manager are provided in Section 62 of the MFMA 2003, while Section 55 of the MSA, 2000 sets out the accountable responsibilities of the municipal manager. The municipal manager as the head of the municipal administration is responsible and accountable to the executive mayor for the administration, management and performance of all the functions as assigned by the municipal council and executive mayor.

The heads of departments/directorates must report to the municipal manager for the performance of their departments/directorates, whilst the municipal manager must submit regular performance reports to the municipal council. The municipal manager may develop a system of delegation to promote administrative and operational efficiency and to provide sufficient accountability mechanisms.

Furthermore, Thornhill (2015:91-92) states that the head of the municipal administration (municipal manager) has to introduce relevant institutional arrangements within the municipality to maintain clear lines of communication and lines of authority among all administrative employees. The municipal manager has to ensure that proper procedures are in place to ensure that each municipal official will be able to render account for their actions and must ensure that relevant control measures and mechanisms are in place to enable the head of the municipal administration to report on the achievement of the objectives as provided in the municipalities IDPs through the most effective use of resources.

As stated by Sibanda (2017:320) the head of the municipality's administration as the accounting officer must ensure that proper administrative arrangements are in place to promote accountability of the administrative function. The Public Audit Amendment Act, 2018, Section 3(1B) stipulates that the Auditor-General has the power to take any appropriate remedial action and to issue a certificate of debt, as prescribed, where an accounting officer or accounting authority has failed to comply with remedial action. Failure to give effect to assigned responsibilities should result in the removal of the municipal manager from office.

3.4 Senior municipal managers

In terms of Section 56 of the MSA, 2000, the municipal council, after consultation with the municipal manager, appoints managers who are directly accountable to the municipal manager. According to SALGA (2015:25), senior managers refer to the managers directly accountable to the municipal manager, including the chief financial officer, heads of departments/directorates, the heads of the internal audit unit and risk management unit as well as other managers appointed in terms of the MSA, 2000, and the Regulations on the Appointment and Condition of Service of Senior Managers.

The municipal manager depends on senior management, including the chief financial officer, for designing and implementing effective financial and performance management controls to promote administrative and financial accountability. Administrative accountability requires that municipal officials be accountable and answerable to the head of the municipal administration for the performance of their administrative functions (Napier 2007:380; Sibanda 2017:320).

Landsberg and Graham (2017:168) aver that in a municipality with an executive mayor, the members of the mayoral committee are assigned to specific departments/directorates to act as the political heads of the departments or directorates to ensure the effective and efficient administration of particular departments/directorates in close collaboration with the head of the departments/directorates. Members of the mayoral committee, are assigned to a specific department as, the political heads of departments/directorates should monitor and fulfil an oversight function and not be involved in the activities and decisions associated with implementation of any administrative functions. In this regard the Auditor-General reports that political office-bearers interference in the administration of municipalities weakens oversight (AGSA 2018:55; AGSA 2019:12). Other mechanisms to promote administrative oversight and accountability are outlined in the discussion below.

3.5 Other mechanisms to promote administrative accountability in municipalities

Mechanisms to promote administrative accountability include the internal control mechanisms produced to keep municipal officials under surveillance and in check.

3.6 Code of conduct for municipal officials

According to Venter (2011:94), the Code of Conduct for Municipal Officials deals primarily with the relationships between the municipal officials and political office-bearers, their relationships with the community and the relationships between municipal officials. Sing and Ntshangase (2003:117) point out that the Code of Conduct for Municipal Officials was established to ensure that the municipal officials address the priority needs of the communities as well as the delivery of services in an effective, efficient and accountable manner. Cloete and Thornhill (2005:211) further state that it should be general practice for each municipal manager to provide a copy of the code of conduct to every municipal official. Schedule 2 of the MSA, 2000, the Code of Conduct for Municipal Officials provides that municipal officials must perform their administrative functions in good faith and in a transparent manner to promote the basic values and principles of public administration as provided in Section 195 of the Constitution of 1996.

Section 14(a) of Schedule 1 of the Municipal Systems Amendment Act, 2011 provides that any breach of the Code of Conduct for Municipal Officials is grounds for dismissal. Sing and Ntshangase (2003:119) maintain that whenever any municipal official has reasonable grounds for believing that the Code of Conduct for Municipal Officials has been breached, the official must immediately report the matter to a supervisory officer and in particular the municipal manager. The municipal manager must ensure that municipal officials adhere to the requirements of the Code of Conduct for Municipal Officials. Disciplinary steps must be taken against defaulters to hold them to account for their actions.

3.7 Integrated Development Plan and the Service Delivery and Budget Implementation Plan

According to Kwele (2016) as cited in Draai, Van Rooyen & Raga (2016) the IDP as the key strategic management instrument of a municipality must capture the priorities and service delivery needs of the local communities. The IDP is legislated by the MSA, 2000, which supersedes all other plans that guide development in municipalities. Pillay, Tomlinson and Du Toit (2006:15) state that the IDP provides the vision for the municipality, details priorities of the municipal council, co-ordinates and links sectoral plans and strategies and aligns human and financial resources with the priorities and needs of local communities. It supports and promotes environmental sustainability, and it serves as the basis for the annual and medium-term municipal budget.

Landsberg and Graham (2017:169) point out that once the municipal council approves the IDP, the municipal manager and the heads of departments/directorates have to draft a SDBIP. The IDP is operationalised through the SDBIP which is a detailed plan to execute the municipalities' delivery of services, as provided in the IDP and the execution of the annual budget. The SDBIP serves as a measurable implementation plan to give effect to the IDP of the municipality to ensure the operational alignment between the municipality's budget and the IDP, as well as the performance agreements. Each department/directorate must design their own plans to execute programmes and projects as provided in the SDBIP. The senior managers in the municipality must enter annually into their performance agreements to ensure cohesion and alignment of individual plans to the strategic priorities as provided in the IDP and budget (Krishnan 2008:27; Landsberg and Graham 2017:169-170). Thus, the SDBIP can be seen as a key mechanism to promote accountability within the municipality.

3.8 Performance management

In the context of local government, performance management refers to a strategic approach to review or to measure the performance of the municipality and its employees based on specific targets and performance indicators (Fourie & Opperman 2015:353). In terms of Section 44(3) and 56(3) of the Municipal Structures Act, 1998, the executive committee or the executive mayor is responsible for the development of the performance management system as well as the development of evaluation criteria and key performance indicators. On the other hand, the municipal manager is responsible to implement and managed the performance management reporting system and provide advice to the municipal council regarding the reporting system that must be adopted. Section 38 of the MSA, 2000, provides that a municipality must establish a performance management system to achieve the following: administer its affairs in an economical, effective, efficient and accountable manner; promote a culture of performance management among its political structures, political office-bearers, the municipal councillors and its administration (municipal officials); and to ensure that its performance management system is best suited for the specific circumstances and in line with the priorities, objectives, indicators and targets as indicated in the municipality's IDP. Landsberg and Graham (2017:170) point out that performance management is seen as an administrative control mechanism to assign internal accountability. Malefane as cited in Van der Westhuizen (2016:141-142) state that performance management refers to a continuous, systematic process of identifying, appraising, developing, and managing the performance of employees with the ultimate purpose of improving the success of a public institution. On the other hand, performance appraisals refer to the activities to appraise and rating of the performance of employees that indicates the level of performance of employees.

In terms of Section 57(5) of the MSA, 2000, the performance objectives and performance targets must be measurable, practical and based on the key performance indicators provided in the municipality's IDP. Fourie and Opperman (2015:355) maintain that a performance management system of a municipality must demonstrate how the system is managed, how it will be reviewed and how reporting will take place. The rate of reporting and the lines of accountability for performance must be determined. The process of implementing the performance management in accordance with the municipality's IDP process must be explained. The roles and responsibilities of all role payers concerning the development of the performance management system need to be clarified; and it must indicate how the system relates to the performance management of its employees. In light of the above, the performance management system of a municipality can be seen as a key mechanism to promote administrative oversight and accountability.

3.9 Current challenges of administrative oversight and accountability

After 25 years of South Africa's democracy the performance of local governments remains a concern. Koma (2017:36-37) asserts that the South African national government has implemented various interventions over the years to restore performance including the administrative and financial performance of municipalities. These interventions include Project Consolidate that was introduced from 2004 to 2006 to improve integration and coordination of provincial programmes, as well as to capacitate local government service delivery through harmonised national and provincial interventions. The National Department of Co-operative Governance and Traditional Affairs (CoGTA) introduced the Local Government Turn Around Strategy (LGTAS) in 2009, after their State of Local Government Report of 2009 revealed major challenges related to governance, service delivery, financial management, policy management and policy implementation issues. After it became clear that the LGTAS failed to improve the institutional capacity and performance of most of the municipalities, the Local Government Back-to-Basics campaign was introduced in 2014. The Local Government Back-to-Basics campaign focused on the improvement of good governance, public participation, financial management, infrastructure services and institutional capacity. The main objectives of the Back-to-Basics campaign were to ensure a suitable interface between political matters and administration, to develop effective credit control and debt collection policies, develop and implement audit and post-audit action plans, build institutional and administrative capacity, processes and systems and to provide capacity building initiatives for councillors (Koma 2017:28; Kroukamp 2016:113).

In addition to the above strategies and interventions, SALGA also introduced numerous programmes such as the Councillor Induction Programme and the Municipal Audit Support Programme (MASP) to improve municipal leadership, governance, administration, institutional capacity and financial management practices. Koma (2017:28-29) is of the view, that these interventions failed to improve the administration, institutional and financial performance of most municipalities. Koma (2017:35) further points out that current service delivery protests engulfing most municipalities may necessitate the need for national government to revisit national interventions to restore confidence in most municipalities. The Department of Cooperative Governance and Traditional Affairs (CoGTA) introduced the District Development Model (DDM) which was adopted by Parliament on 21 August 2019. The DDM is an inter-governmental relations (IGR) approach to improve joint planning, budgeting and delivery across the three spheres of government with district and metropolitan municipalities as the focal point. One of the key objectives of the DDM is to promote oversight over budgets and projects in an accountable and transparent manner (CoGTA 2021).

The Auditor-General Consolidated General Reports on the audit outcomes of local government of 2016-2017 and 2017-2018 confirm that accountability and the need for appropriate consequences for accountability failures in most municipalities, feature as the prominent elements of the poor performance in most municipalities (AGSA 2018:22; AGSA 2019:12). The slow response by the political and administrative leadership of municipalities in the Free State province to address the weak internal control environment, the lack of consequences, political interference in the administration, and failure to adhere to the requirements of local government legislative frameworks are the main causes of poor performance of all municipalities in the Free State province (AGSA 2018:6; AGSA 2019:3).

In light of the above, Subban and Wissink (2015:47-48) aver that high vacancy rates in the administration of municipalities remains a challenge, whilst corruption and the lack of consequences amongst functionaries further contribute to a breakdown in the functionality and accountability of municipalities. Ambe (2016:26) points out that the lack of compliance and accountability remains a concern in most municipalities. Most municipalities fail to comply with key local government legislation including supply chain management (SCM) legislative frameworks, and these defaulters have not been held accountable for their actions. Municipal SCM practitioners who form part of the municipality administration have defaulted in SCM processes without any action being taken against them. Thus, the lack of effective oversight and accountability in most municipalities of which the municipalities of the Free State cannot be excluded hampers service delivery and has led to a culture of impunity.

4. RESEARCH METHODOLOGY AND DESIGN

In this research a qualitative research approach was utilised to gain insight into administrative oversight and accountability practices at municipalities within the Free State. A self-administering or semi-structured questionnaire was used to elicit information from the selected municipal officials, municipal managers, chief financial officers, political office bearers such as mayors or executive mayors of the Mangaung Metropolitan Municipality, the four district municipalities namely; Xhariep District Municipality, Lejweleputswa District Municipality, Fezile Dabi District Municipality, Thabo Mofutsanyane District Municipality and 10 of the 18 affiliated local municipalities in the Free State province. The self-administrated, semi-structured questionnaire was also distributed to the ward councillors of the 10 local municipalities. A non-probability, purposive or judgemental sampling method was used to select a sample size of 10 local municipalities, out of a total of 18 local municipalities of the Free State province. Bless, Higson-Smith and Sithole (2014:172) aver that purposive sampling is based on the judgement of a researcher to choose the sample. According to Niewenhuis as cited in Maree (2016:273), the sample size depends rather on what the researcher wants to determine, what is credible and what can be done with the available resources and time. Therefore, the selection of 10 affiliated local municipalities was chosen based on the judgement of what the researcher considers to be a typical unit or characteristics of the population. The selected 10 affiliated local municipalities include Mohokare Local Municipality, Kopanong Local Municipality, Letsemeng Local Municipality, Tokologo Local Municipality, Tswelopele Local Municipality, Nala Local Municipality, Moqhaka Local Municipality, Ngwathe Local Municipality and Metsimaholo Local Municipality. A total of 25 questionnaires were distributed. Only 17 respondents (nine ward councillors, five municipal officials and three political-office bearers such a mayors or executive mayors) completed the semi-structured questionnaires, with a response rate of 68%.

5. FINDINGS AND RESULTS

This section highlights only the most ostensible results using a semi-structured questionnaire to determine the perceptions of municipal officials, mayors or executive mayors and ward councillors regarding municipal administrative oversight and accountability of the selected municipalities of the Free State province.

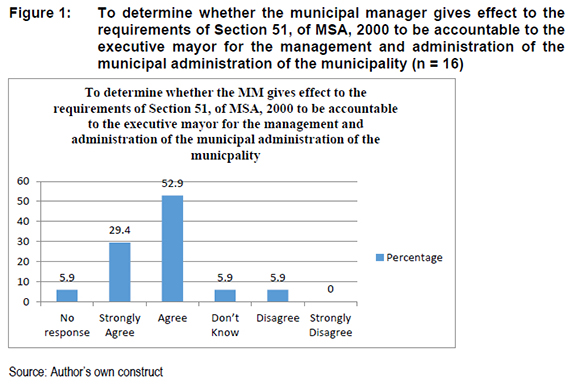

Figure 1 below illustrates the findings regarding the question whether the municipal manager is responsible and accountable to the executive mayor for the management and administration of the municipal administration. The purpose of the statement was to determine whether the municipal manager gives effect to the requirements of Section 51, MSA, 2000 to be responsible and accountable to the executive manager for the management and administration of the municipal administration.

Figure 1 illustrates that 29.4% and 52.9% of respondents respectively strongly agreed and agreed that the municipal manager is responsible and accountable to the executive mayor for the management and administration of the municipal administration. Whilst 5.9% of the respondents did not respond while, 5.9% of the respondents disagreed. In the literature discussion it was accentuated that the municipal manager as head of administration is responsible and accountable to the executive mayor for the management of the administration as well as the performance of the functions and responsibilities assigned to him/her by the municipal council and the executive mayor.

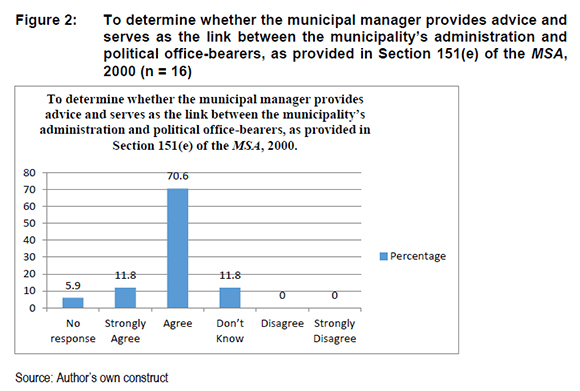

Figure 2 below illustrates the findings of the statement that the MM is tasked with the advising of political structures and political office-bearers and managing communication between the municipalities' administration and its political office-bearers. The purpose of the statement was to confirm whether the municipal manager provides advice and serves as the link between the municipality's administration and political office-bearers, as provided in Section 151(e) of the MSA, 2000.

Figure 2 shows that 11.8% of the respondents strongly agreed, and 70.6% agreed that the municipal manager provides advice and serves as the link between the municipality's administration and political office-bearers, as provided in Section 151(e) of the MSA, 2000, whereas 11.8% of respondents indicated that they did not know and 5.9% did not respond to the question. In the literature discussion it was emphasised that the municipal manager is tasked with the advising of the political structures and political office-bearers of the municipality, managing communications between the municipality's administration and its political office-bearers and carrying out the decisions of the political structures and political office-bearers of the municipality.

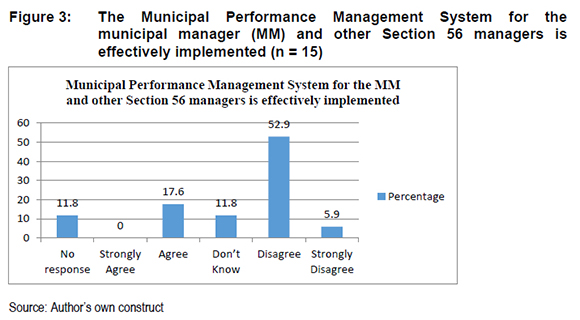

The findings on the statement whether the municipal performance management system for the municipal manager and other Section 56 managers is effectively implemented in the municipality were illustrated in Figure 3 below. The purpose of the statement was to confirm whether the municipal performance management system for the municipal manager and other Section 56 managers is effectively implemented.

Figure 3 outlines that 17.6% of the respondents agreed with the statement, 11.8% indicated that they did not know, 52.9% disagreed and 5.9% strongly disagreed with the statement. Therefore, the majority of the respondents disagreed that the municipal performance management system for the municipal manager and Section 56 managers accountable to the municipal manager is effectively implemented. All municipalities within the province have to ensure that the municipal performance management system for the municipal manager and other Section 56 managers is effectively implemented. One could argue that it could hamper the effective performance of a municipality's administration.

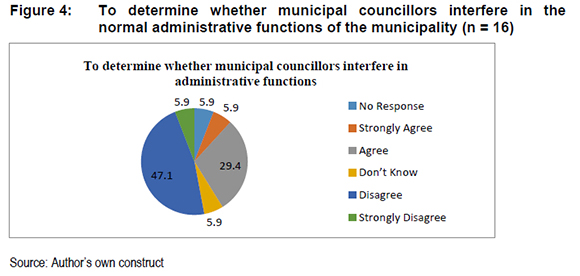

Figure 4 below illustrates the findings on the statement that municipal councillors interfere in the normal administrative functions of the municipality. The purpose of the statement was to determine from the perceptions of the respondents (nine ward councillors, five municipal officials, and only three political-office bearers such a mayors or executive mayors) whether municipal councillors interfere in the administrative functions of a municipality.

Figure 4 shows that 5.9% did not respond to the question, 5.9% strongly agreed, 29.4% agreed, 5.9% indicated that they do not know and 47.1% disagreed whilst 5.9% strongly disagreed. Although the majority of the respondents (47.1%) disagreed with the statement it is a concern that a total of 35.3% of the respondents strongly agreed and agreed that councillors interfere in the administration of the municipality. Section 11(a) of the Code of Conduct for municipal councillors, which clearly provides that a councillor may not, except as provided in law, interfere in the management or administration of any department of a municipality, unless mandated by the municipal council. Thus, all municipalities of the province have to ensure that all municipal councillors adhere to the requirement of Section 11(a) of the Code of Conduct for municipal councillors that a councillor may not, except as provided in law, interfere in the administration of any department of a municipality unless mandated by the municipal council.

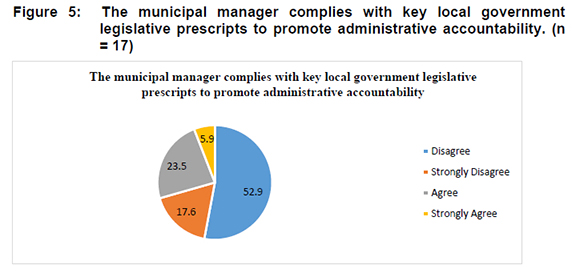

Figure 5 below illustrates the findings on the statement whether the municipal manager complies with key local government legislative prescripts to promote administrative accountability. The purpose of the statement was to determine from the perceptions of the respondents whether the municipal manager complies with key local government legislative prescripts such as the Section 55 (1) of MSA, 2000 and Section 62 of the MFMA, 2003 concerning administrative accountability of municipal managers.

From Figure 5 it can be depicted that 17.69% of the respondents strongly disagreed, 52.9% disagreed, whereas 23.5% agreed and 5.9% strongly agreed, that the municipal manager complies with key local government legislative prescripts to promote administrative accountability. The majority of the respondents strongly disagreed and disagreed that the municipal manager complies with key local government legislative prescripts to promote administrative accountability. In the literature discussion of the article, it was reported by the Auditor-General that most municipalities of the Free State province continue to disregard key local government legislation (AGSA 2018:55).

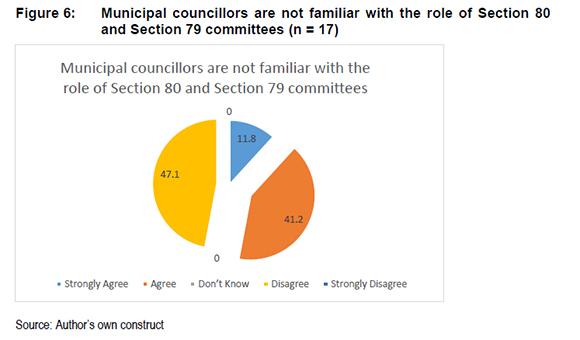

Figure 6 below illustrates the findings on the statement that municipal councillors are not familiar with the role of Section 80 and Section 79 committees. The purpose of this statement was to confirm whether the municipal councillors are familiar with the role of Section 80 and the Section 79 portfolio committees.

Figure 6 illustrates that 11.8% of respondents strongly agreed, 41.2% agreed and 47.1% disagreed with the statement that municipal councillors are not familiar with the role of Section 80 and Section 79 committees. It is a concern that the majority of the respondents strongly agreed or agreed with the above statement. Section 80 and Section 79 committees cannot function effectively if municipal council members are not familiar with their role. The MPAC as a Section 79 committee is one of the key oversight committees.

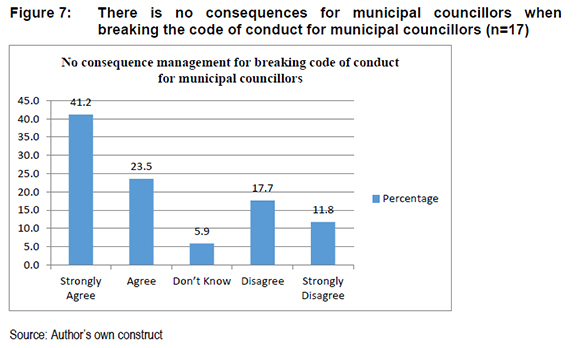

Figure 7 below demonstrates the findings on the statement that there are no consequences for municipal councillors when breaking the code of conduct for municipal councillors. The purpose of this statement was to determine from the perceptions of the respondents whether municipal councillors who are responsible to hold the executives to account are fulfilling their role and adhering to the requirements of the Code of Conduct for Municipal Councillors.

Figure 7 shows that 41.2% of respondents strongly agreed, 23.5% agreed and 5.9% did not know. On the other hand, 17.7% of respondents disagreed with the statement that indicates that there is no consequence management for breaking the code of conduct for municipal councillors and 11.8% strongly disagreed with the statement. The majority of the respondents (nine ward councillors, five municipal officials, and three political office bearers such a mayors and executive mayors) specify that there are no consequences for municipal councillors when breaking the code of conduct for municipal councillors and this is also stressed in the literature discussion that corruption thrives when laws and policies are flawed and in particular when there are no consequences for corrupt conduct and any acts of unethical conduct and acts of dishonesty. It was further mentioned in the literature discussion of this article that there is a total breakdown in control and poor leadership responses towards improving accountability, that further contributes to a lack of accountability and no consequences for non-compliance with key legislated rules including the code of conduct for municipal councillors in municipalities of the Free State province.

6. CONCLUSIONS

The aim of this article was to determine the perceptions of municipal officials and political office-bearers and ward councillors about municipal administrative oversight and accountability of municipalities of the Free State province. The article further seeks to identify current challenges pertaining to administrative oversight and accountability within municipalities in the Free State province.

It was accentuated in the literature discussion of this article that the political office-bearers such as the speaker, the mayor and in an executive mayoral system the executive mayor fulfils the oversight role over the administration, to ensure that the municipal council resolutions and policies are executed by the administration. Municipalities with an executive mayor, the executive mayor or mayoral committee members are responsible for overseeing the administration of a municipality to ensure effectiveness and efficiency in service delivery. The major in a municipality with a collective executive system must oversee and provide political guidance over the assigned responsibilities of the accounting officer and the chief financial officer. Apart from the accountable functions of political office-bearers certain committees with delegated functions fulfil the roles of oversight of municipal administration to ensure that municipalities are able to meet their constitutional obligations, such as the executive committees, mayoral committees, council portfolio committees and municipal public accounts committees (MPACs). The municipal manager as the accounting officer and head of the administration is accountable for the overall performance and administration of the municipality. It was further emphasised that administrative accountability requires that municipal officials be accountable and answerable to the head of the municipal administration for the performance of their administrative functions.

The findings from the semi-structured questionnaire revealed that the majority of the respondents agreed that the municipal manager as the accounting officer of a municipality is responsible to advise and to manage communication between the municipal administration and the political office-bearers. It was accentuated in the article that disciplinary action must be taken against municipal councillors whose actions are in contradiction with the Code of Conduct for Municipal Councillors.

A further challenge emphasised in this article is the continued disregard of key local government legislation that hampers oversight and accountability. The majority of the respondents strongly disagreed and disagreed that the municipal mangers complied with key local government legislative prescripts. The findings support the findings of the AuditorGenerals report that most municipalities of the Free State province continue to disregard key local government legislation (AGSA 2018:55). It is critical that internal controls that prevent irregularities and deviations from key local government legislation and relevant regulations be reinforced in municipalities of the province. This would be possible if political officebearers fulfil their critical oversight role concerning the implementation of key local government legislation. The continued inaction of municipal councils, mayors, municipal manager's and other relevant executives to implement key local government legislation and relevant regulations weakens their oversight and accountability role, resulting in poor performance of municipalities in the province.

The majority of the respondents confirmed that municipal councillors are not familiar with the role of Section 80 and Section 79 committees. As argued, Section 80 and Section 79 committees cannot function effectively if municipal council members are not familiar with their role. The MPAC as a Section 79 committee is one of the key oversight committees. For this reason, it is recommended that the oversight role of the speaker, municipal council, mayor or executive mayor and the MPAC as a Section 79 committee need to be strengthened in municipalities of the province so that the executive can be held to account. SALGA must ensure that mechanisms are in place to capacitate political office-bearers to clearly understand their oversight role in order to promote accountable local government.

The municipal manager as the accounting officer should personally be held accountable for any loss of allocated funds or assets as a result of any deficiency in the administrative or managerial arrangements of the municipality. Failure to give effect to assigned responsibilities should result in the removal of the municipal manager from office. The Public Audit Amendment Act of 2018 provides that if the accounting officer fails to implement remedial action, the Auditor-General may issue a certificate of debt in the name of the relevant accounting officer.

REFERENCES

AMBE IM. 2016. Insight into supply chain management in a municipal context. Public and Financial Management 5(2):20-29. (DOI:http://dx.doi.org//10.21511/pmf.5(2).2016.02; downloaded on 24 June 2020. [ Links ])

AUDITOR-GENERAL OF SOUTH AFRICA (AGSA). 2018. MFMA, 2003: Consolidated General Report on the audit outcomes of local government 2016-2017. Pretoria: Government Printers. [ Links ]

AUDITOR-GENERAL OF SOUTH AFRICA (AGSA). 2019. MFMA, 2003: Consolidated General Report on the audit outcomes of local government 2017-2018. Pretoria: Government Printers. [ Links ]

BLESS C, HIGSON-SMITH C & SITHOLE SL. 2014. Fundamentals of Social Research Methods - An African Perspective. 5th edition. Lansdowne: Juta and Company. [ Links ]

CLOETE JJN & THORNHILL C. 2005. South African Municipal Government & Administration. Pretoria: Dotsquare Publishing. [ Links ]

CRAYTHORNE DL. 2006. Municipal administration the handbook. Cape Town: Juta and Company. [ Links ]

DEPARTMENT OF COOPERATIVE GOVERNANCE AND TRADITIONAL AFFAIRS (COGTA). 2021. What is the district development model? [Internet:https://www.cogta.gov.za<ddm; downloaded on 20 March 2021. [ Links ]]

DE VISSER J. 2010. The political-administrative interface in South African municipalities assessing the quality of local democracies. Commonwealth Journal of Local Governance (5):86-101. [ Links ]

FOURIE M & OPPERMAN L. 2015. Municipal finance and accounting. 3rd Edition. Pretoria: Van Shaik Publishers. [ Links ]

HUSSEIN MK. 1999. Enhancing Accountability in Local Government: An Assessment of the Enforcing Mechanisms. Johannesburg: Randse Afrikaanse University. (Unpublished mini dissertation. [ Links ])

KHALO T. 2013. Accountability and Oversight in Municipal Financial Management: The Role of Municipal Public Accounts Committees. Journal of Public Administration 48(4):589-501. [ Links ]

KOMA SB. 2017. A Critical Analysis of Municipal Governance Challenges and Lessons Learnt: The cases of two South African municipalities. Administratio Publica 25(4):23-39. [ Links ]

KRAAI S, HOLTZHAUSEN N & MALAN L. 2017. Oversight mechanisms in local government: a case of Ekurhuleni Metropolitan Municipality in South Africa. African Journal of Public Affairs 9(6):59-72. [Internet:http://hdl.handle.net/2263/61224; downloaded on 09 March 2020. [ Links ]]

KRISHNAN HB. 2008. Public accountability: from concept to practice in the South African local government context. Prepared for: the democracy development programme. Durban. University of KwaZulu-Natal, 5th Annual Local Government Conference, 11-12 August 2008, Southern Sun - Elangeni. [ Links ]

KROUKAMP H. 2016. Strategies to restore confidence in South African Local Government. African Journal of Public Affairs 9(3):105-116. [ Links ]

KWELE L. 2016. Strategic management in local government. In Draai E, Van Rooyen EJ & Raga K. (eds.). A Practical Introduction to Public Management. Cape Town: Oxford University Press. [ Links ]

LANDSBERG C & GRAHAM S. 2017. Government and Politics in South Africa. (eds.). Coming of age. Pretoria: Van Schaik Publishers. [ Links ]

MALEFANE SR. 2016. Appraising and managing performance. In Van der Westhuizen. (Ed). Human Resource Management in Government. A South African perspective on theories politics and processes. Cape Town: Juta and Company. [ Links ]

MADUMO OS. 2015. Developmental Local Government and Progress in South Africa. Administratio Publica 23(2):153-166. [Internet:http://hdl.handle.net/2263/50230; downloaded on 24 March 2020. [ Links ]]

NAPIER CJ. 2007. Accountability: Am Assessment at the Local Government Sphere. Journal of Public Administration 42(4):376-390. [ Links ]

NDABA B. 2019. 25 billion wasted: municipalities in a mess, auditor-general to hold mayors, municipal managers to account. The Star, 27 June. [ Links ]

NEALER E. 2011. Municipal Human Resource Management. In Van der Waldt. (Ed). Municipal Management: Serving the People. Cape Town: Juta and Company. [ Links ]

NIEWENHUIS J. 2016. Qualitative research designs and data gathering techniques. In Maree. (Ed). First steps in Research. 2nd Edition. Pretoria: Van Schaik Publishers. [ Links ]

PAUW JC, VAN DER LINDE GJA, FOURIE D & VISSER CB. 2015. Managing Public Money. 3rd Edition. Cape Town: Pearson Holdings. [ Links ]

PILLAY U, TOMLINSON R & DU TOIT J. 2006. Democracy and Delivery, Urban Policy in South Africa. Cape Town: Human Sciences Research Council. [ Links ]

SIBANDA MM. 2017. Control, ethics and Accountability in The Financial Management Performance of Eastern Cape Municipalities. Journal of Public Administration 52(2):313-339. [ Links ]

SING D & NTSHANGASE B. 2003. Ethics and corruption. In Reddy, P.S, Sing, D and Moodley, S. (eds). Local Government Financing and Development in Southern Africa. Cape Town: Oxford University Press. [ Links ]

SIROVHA KI & THORNHILL C. 2017. Partnership between traditional leaders and municipalities with special reference to Bojanala District Municipality. Administratio Publica 25(3):134-156. [ Links ]

SOUTH AFRICAN LOCAL GOVERNMENT ASSOCIATION (SALGA). 2015. SALGA National Members Assembly, Discussion Documents. Gallagher Convention Centre, Johannesburg, 24-26 March 2015. [ Links ]

REPUBLIC OF SOUTH AFRICA. 1996. The Constitution of the Republic of South Africa. Pretoria: Government Printers. [ Links ]

REPUBLIC OF SOUTH AFRICA. 1998. Local Government: Municipal Structures Act, Act 117 of 1998. Pretoria: Government Printers. [ Links ]

REPUBLIC OF SOUTH AFRICA. 1998. White Paper on Local Government. Pretoria: Government Printers. [ Links ]

REPUBLIC OF SOUTH AFRICA. 2000. Local Government Municipal Systems Act, Act 32 of 2000. Pretoria: Government Printers. [ Links ]

REPUBLIC OF SOUTH AFRICA. 2003. Local Government: Municipal Finance Management Act (MFMA, 2003). Act 56 of 2003. Pretoria: Government Printers. [ Links ]

REPUBLIC OF SOUTH AFRICA. 2006. National Treasury. MFMA, Circular 32 of 15 March 2006. Pretoria: Government Printers. [ Links ]

REPUBLIC OF SOUTH AFRICA. 2018. Public Audit Amendment Act, Act 5 of 2018. Pretoria: Government Printers. [ Links ]

SUBBAN M & WISSINK H. 2015. Key Factors in Assessing the State of Local Government in South Africa. Crisis Management or Facing the Realities of Transformation? Administratio Publica 23(2):33-56. [ Links ]

THORNHILL C. & CLOETE JJN. 2014. South African Municipal Government and Administration. Pretoria: Van Schaik Publishers. [ Links ]

THORNHILL C. 2015. Accountability. A Constitutional Imperative. Administratio Publica 23(1):77-101. [ Links ]

TSATSIRE I. 2008. A critical analysis of challenges facing developmental local government: A case study of the Nelson Mandela Metropolitan Municipality. Port Elizabeth: NMMU. (Unpublished doctoral thesis. [ Links ])

VAN DER WALT C, VENTER A, PHUTIAGAE K, NEALER E, KHALO T & VYAS-DOORGAPERSAD S. 2014. Municipal Management Serving the People. In Van der Waldt G. (ed.). 3rd Edition. Claremont: Juta. [ Links ]

VAN DER WALDT G, VAN NIEKERK D, DOYLE M, KNIPE A & DU TOIT D. 2001. Managing for results in government. Sandown: Heinemann. [ Links ]

VAN DER WALDT G. 2015. Political oversight of municipal projects. An empirical investigation. Administratio Publica 23(3):48-69. [Internet:https://www.researchgate.net/publication/283571493; downloaded on 14 April 2019. [ Links ]]

* corresponding author