Services on Demand

Article

English (pdf)

English (pdf)

Article in xml format

Article in xml format Article references

Article references

Indicators

Related links

-

Cited by Google

Cited by Google -

Similars in Google

Similars in Google

Share

Permalink

PermalinkSouth African Computer Journal

On-line version ISSN 2313-7835

Print version ISSN 1015-7999

SACJ vol.29 n.1 Grahamstown Jul. 2017

http://dx.doi.org/10.18489/sacj.v29i1.398

RESEARCH ARTICLE

Incorporating sustainability into IT project management in South Africa

Grant ClinningI; Carl MarnewickII

IApplied Information Systems, University of Johannesburg, South Africa. dgclinning@gmail.com

IIApplied Information Systems, University of Johannesburg, South Africa. cmarnewick@uj.ac.za

ABSTRACT

The concept of sustainability is becoming more and more important in the face of dwindling resources and increasing demand. Despite this, there are still many industries and disciplines in which sustainability is not actively addressed. The requirement of meeting current and future needs is not an issue from which IT projects are exempt. Ensuring sustainability requires managing sustainability in all activities. The field of IT and sustainability is one in which literature is appearing, but at a slow pace and this leaves many unanswered questions regarding the state of sustainability in IT projects and the commitment of IT project managers to sustainability. In not knowing what the state of sustainability is, potential shortcomings remain unknown and corrective action cannot be taken.

Quantitative research was conducted through the use of a survey in the form of a structured questionnaire. This research was cross-sectional as the focus was to assess the state of sustainability at a single point in time. IT project managers were randomly sampled to get an objective view of how committed they were to sustainability. This research made use of a project management sustainability maturity model to measure the extent to which sustainability is incorporated into IT projects.

The findings are that IT project managers are not committed to sustainability. While the economic dimension yielded the best results, they were not ideal, and it is in fact the social and environmental dimensions that require the most attention. This lacking commitment to the social and environmental dimensions is not limited to select aspects within each dimension, as each dimension's aspects are addressed to a similarly poor extent. This research suggests that sustainability needs to become a focus for IT project managers, but for this to happen, they require the relevant project management sustainability knowledge.

Keywords: sustainability, project management, IT project management, sustainability maturity

1 INTRODUCTION

In recent years, sustainability in general, but specifically from an organisational perspective, has come under the spotlight as the resources that organisations rely on are no longer perceived as infinite (Azizi, 2005; Kendall & Willard, 2016; Shafiee & Topal, 2009). Sustainability is not merely of environmental concern. Kendall and Willard (2016) recognise the degradation of the 'planetary services' such as a stable climate, access to materials as well as security of energy sources, which threaten the continuity of organisations. Organisations jeopardise their social licence to operate by failing to meet the needs of millions (Kendall & Willard, 2016; Pike, 2012).

Additionally, organisations which fail to innovate and develop lose their competitiveness and place their own sustainability at risk (Hartman, 2001). The sustainability of an organisation is typically ensured through the implementation of projects that are aligned with the strategies of the organisation (Keeys, 2014). A large responsibility is placed on the project management capabilities of an organisation to ensure that not only the financial sustainability of the organisation is considered, but also the sustainability of the planet and its people. Silvius and Schipper (2014b) as well as Wang, Wei, and Sun (2013) maintain that project managers are in a position to significantly impact how sustainability is implemented within the organisation. Gareis, Huemann, Martinuzzi, Weninger, and Sedlacko (2013) recognise that the management paradigm has shifted from viewing sustainability as an optionality to now being concerned with sustainable development.

It is evident that projects play a crucial role in enabling organisations to operate in a sustainable fashion. Projects are even described as temporary organisations so they too ought to include an element of sustainability (Silvius, Schipper, Planko, van den Brink, & Köhler, 2012). There is, however, a paucity of literature on the topic of project management and its link to sustainability (Gareis et al., 2013). Unsustainable practices will continue as long as this topic remains unfamiliar to the parties involved, which emphasises the importance of research in this field. According to Marnewick (2015), literature regarding sustainability and project management is appearing, but at a slow pace. The existing body of literature is confined mainly to construction and is scant as far as the African continent is concerned.

When assessing a more specialised area of project management, namely information technology (IT) project management, the state of sustainability is even more obscure. This leads to the problem of not knowing what is lacking or what needs to be done to correct this. In addition, the apparent void in research regarding sustainability in IT projects hinders an understanding and ability to apply sustainability concepts in project management (Edum-Fotwe & Price, 2009; Herazo, Lizarralde, & Paquin, 2012; Martens & De Carvalho, 2014; Ugwu & Haupt, 2007). This void is even more apparent in the context of the African continent specifically (Hedman & Henningsson, 2011; Herazo et al., 2012; Silvius & Nedeski, 2011).

Another trait of the existing literature regarding sustainability and project management is that it is considered to be interpretive (Silvius & Nedeski, 2011; Silvius et al., 2012) and conceptual (Martens & De Carvalho, 2014). A lack of empirical research in this regard is recognised by Martens and De Carvalho (2014) and described as necessary to develop an understanding of how sustainability concepts can be implemented within project management.

This article comprises the following four sections: the first section provides an overview of sustainability and project management as well as the relationship between these concepts. The second section focuses on the research methodology. The third section covers the analysis of the results and focuses on the perception of IT project managers, the extent to which sustainability is addressed in IT projects and the structure of sustainability in IT projects. The final section concludes the article and indicates the state of sustainability in IT projects.

2 LITERATURE REVIEW

2.1 Sustainability

According to Toman (2006), the term 'sustainability' is inherently ambiguous. Different perspectives allow for different interpretations, which can make understanding sustainability more difficult. According to Keeys (2014) as well as Silvius and Schipper (2014a), the definition that is most commonly accepted is that of the Brundtland Report. The definition reads as follows: "sustainable development is development that meets the needs of the present without compromising the ability of future generations to meet their own needs" (World Commission on Environment and Development, 1987). The term 'sustainable development' is considered to be a synonym for sustainability (Seghezzo, 2009) .

Sustainability, according to the World Commission on Environment and Development (1987), is concerned with three dimensions, namely people, profit and planet. Elkington (1997) identifies sustainability and these dimensions as the triple bottom line (TBL) or Triple-P These dimensions of sustainability are more commonly known as the social, economic and environmental dimensions (J. Dillard, Dujon, & King, 2008; World Commission on Environment and Development, 1987).

Martens and De Carvalho (2014) recognise the importance of the economic dimension as it protects the capital of the organisation's investors. Maximising profit, reducing costs, growing revenue and improving quality are considered to be some of the traditional business imperatives (Watts & Holme, 1999; T. E. Thomas & Lamm, 2012). There are those who place even more importance on the economic dimension, stating that the goods and services by which we live are considered to be a by-product of the expectation to make money (D. Dillard, 1987). Since moving away from a goods bartering system to a money-based economy, organisations and individuals require money to obtain the resources they need and want from others (Handy, 2002; Weatherford, 1997, p. 107). Apart from those who are self-reliant, for example subsistence farmers, money is a necessity for sustaining our way of life.

The social dimension refers to humanity and encompasses the communities in which organisations operate as well as the employees of an organisation (Dempsey, Bramley, Power, & Brown, 2011; J. Dillard et al., 2008). Employees are said to be the most valuable asset of an organisation (Brummet, Flamholtz, & Pyle, 1968; Kaplan & Norton, 2001). As employees are the ones who generate the results of the organisation, they should be treasured by the organisation. The financial results of the organisation are also dependent on how communities support the organisation (customer base), and as such communities should also be looked after. Unfortunately the extent to which employees and communities support organisations before they are exploited is overlooked (Aronson & Neysmith, 1996; Pines & Meyer, 2005).

The environmental dimension is concerned with the environment which people inhabit. Sustain-ability has largely become linked to the preservation of the environment and the failings of humanity to date in preserving it (Gore, 2006; Higgins, 2010). It is evident from literature that the planet has been negatively impacted by the activities of the human race (Douthwaite, 1993; Gore, 2006; Higgins, 2010; Ludwig, Hilborn, & Walters, 1993). As early as 1993 the pursuit of economic goals was perceived to have led to the degradation of the environment which sustains humankind and the sense then was that this would continue (Douthwaite, 1993).

It has become widely accepted that the wise use of natural resources, social well-being and economic growth cannot be achieved without considering all of the dimensions and their effect on each other. This dictates that a balance between the dimensions must be struck (Elkington, 1997). King (2009) stresses that the board of directors should ensure that the organisational strategy results in sustainable outcomes with regard to the TBL. The Johannesburg Stock Exchange (JSE) instructs companies listed with it to report on all three dimensions (Sonnenberg & Hamann, 2006).

Despite this echoed sentiment for balance, organisations value profit above the other two aspects, resulting in the social and environmental dimensions being neglected (Labuschagne & Brent, 2005; Edum-Fotwe & Price, 2009; Singh, Murty, Gupta, & Dikshit, 2009; Smith, Smith, & Sharicz, 2011; Ullah, Lai, & Marjoribanks, 2013; Martens & De Carvalho, 2014). These authors also note that the social dimension is the one most often neglected.

2.2 Project management

The Project Management Institute (2013) describes a project as an activity that has the following characteristics: (i) projects are temporary in that they have a defined start and end, (ii) projects are unique in that they are not routine operations, and (iii) projects are undertaken by an individual or group of people. Projects are also described as temporary organisations which contribute to the continued existence of the organisation (Marnewick, 2015; Silvius et al., 2012). Projects are temporary organisations in that they use resources, assets and business processes of the permanent organisation for a finite period for the purpose of rendering products/ services or internal business procedures (Silvius et al., 2012; Jacobsson, Lundin, & Söderholm, 2015). As a temporary organisation, a project itself should include sustainability principles (Silvius et al., 2012). According to Gareis et al. (2013), sustainability principles are considered in specific project types. These types include public, engineering and construction projects. Gareis et al. (2013) identify several studies that focus on each of the aforementioned industries with regard to sustainability and projects. There is an apparent void in the literature regarding sustainability and its consideration in information systems projects and IT projects.

2.3 Link between sustainability and projects

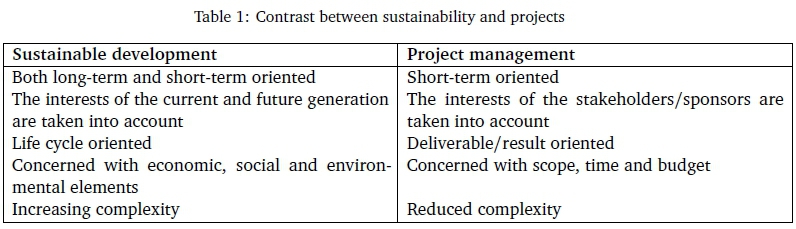

The importance of both projects and sustainability in organisations is echoed by numerous authors, yet projects and sustainability may represent different perspectives (Gareis et al., 2013; Silvius et al., 2012). The characteristics and nature of projects and sustainable development can lead to the conclusion that they are not 'natural friends' or best suited to go together. Table 1 shows the contrast between the nature of projects and sustainability.

Despite the apparent differences, "the need to integrate sustainability in project management has emerged" (Martens & De Carvalho, 2014). Gareis et al. (2013) point out that sustainability is relevant not only to societies and organisations, but also to projects. As society moves towards a more sustainable orientation, it requires the implementation of effective projects in order to realise this change (Silvius et al., 2012). This belief dictates that the nature of projects must change to incorporate the characteristics of sustainability.

Gareis et al. (2013) note that when sustainability has been considered it has been at the strategic level, however operational levels, including projects and programmes, have yet to receive focus. There are some organisations which have embraced sustainability as a fundamental aspect of doing business (Silvius et al., 2012). This embracing of sustainability orientates the business context of projects to address sustainability. This includes the way that projects are managed and executed with regard to sustainability.

Silvius et al. (2012) describe six principles of sustainability that have an implication specifically for projects and project management: (i) sustainability is about balancing or harmonising environmental, social and economic interests, (ii) sustainability is about both short-term and long-term orientation, (iii) sustainability is about local and global orientation, (iv) sustainability is about consuming income, not capital, (v) sustainability is about transparency and accountability and (vi) sustainability is about personal values and ethics. Principles one and two form the basic knowledge that project managers should have with regards to sustainability. Principles three to six further demonstrate that sustainability has specific implications for projects and project management. From these six principles, Silvius et al. (2012) form the following definition of sustainability in projects and project management:

Sustainability in projects and project management is the management, development and delivery of project-organised change in, processes, resources, policies, assets or organisations, with consideration of the six principles of sustainability, in the project, its results and its effects.

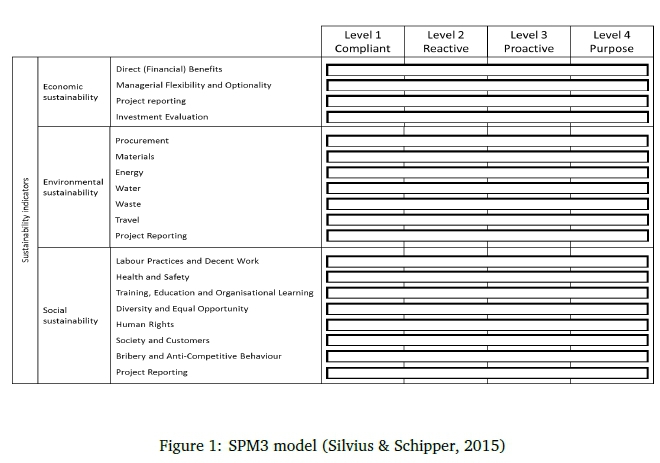

Silvius and Schipper (2010) recognise that with differing views on the scope of sustainability in project management, there are bound to be different extents to which sustainability is addressed in projects. In order to assess this, Silvius and Schipper (2010) developed a maturity model. However, as research in this field is interpretive, the maturity model is for monitoring, assessing and improving the incorporation of the concepts and principles of sustainability within projects (Silvius & Nedeski, 2011). This model, now known as the sustainable project management maturity model (SPM3), has since evolved, moving away from assessing maturity of scope to maturity of the project as a whole with regard to sustainability. The SPM3 model uses a set of four maturity levels, namely compliant, reactive, proactive and purpose, to determine the extent to which sustainability is addressed.

The first level is compliant and is concerned with considering sustainability minimally and implicitly with the intention of only complying with laws and regulations. The second level is reactive and is concerned with considering sustainability explicitly, but only to reduce the negative impacts of the project. The third level is proactive and considers sustainability explicitly and as one of the areas that the project contributes to. The fourth and final level is purpose, which considers making a contribution to sustainability as one of the drivers behind the project and, as such, sustainability considerations are included in the justification of the project.

The model uses a checklist comprising several aspects grouped into one of the three dimensions. This model works by allowing for each dimension to be broken up into smaller aspects and assigning each aspect a level score. This allows for sustainability to be judged in detail as well as for incremental changes to be made, as each aspect is a potential area for improvement. All the aspects in a dimension can be aggregated to give a score for that dimension and all dimensions can be aggregated to give a score for overall sustainability (Silvius & Schipper, 2015).

Based on the literature review, the following research questions were posed:

1. How do IT project managers perceive the importance of the aspects of sustainability?

2. To what extent are the three dimensions of sustainability addressed?

3. To what extent is sustainability as a whole addressed?

4. Are there any correlations between the sustainability dimensions and their aspects? The research methodology that was employed is discussed in the following section.

3 RESEARCH METHODOLOGY

All data that reaches the researcher does so as either numbers or words (G. Thomas, 2013, p. 116). The quantitative research methodology is associated with numbers and the qualitative research methodology is associated with words (G. Thomas, 2013). Erasmus and Marnewick (2012) explain that quantitative research investigates the 'what', 'where' and 'when', whereas qualitative research investigates the 'why' and 'how'. The purpose of this research was to assess to what extent sustainab-ility is incorporated in IT projects. Various statistical methods were employed, making it necessary to express data in numerical form. Research already undertaken in this area by Silvius, Schipper, and Nedeski (2013) followed the quantitative approach, which supports following a quantitative approach in this current research.

Researchers in many different fields utilise models for various reasons, including clarification, prediction, conceptualisation, simplicity and mathematical manipulations, to assess maturity and as a means to capture the critical components of a process or system (Joseph, 2013; Silvius & Schipper, 2015; Olivier, 2009, p. 45-49). This paper takes the approach of using a model to assess maturity in order to determine the extent to which sustainability is addressed in IT projects. For the purpose of this study the maturity model as presented in Figure 1 was used. The checklist for the model requires that Likert scale data be gathered and by extension quantitative data. Based on these factors the decision to follow a quantitative approach was made.

The survey used in this study is based on the one developed by (Silvius et al., 2012). The survey makes use of two Likert scales. The first scale consists of 5 items on a 5-point Likert scale ranging from 1 (least important) to 5 (most important). The second scale consists of 19 items on a 4-point Likert scale comprising 1 (compliant), 2 (reactive), 3 (proactive) and 4 (purpose). For each item on the 4-point scale the respondents are presented with four options which describe the current state to which sustainability is addressed. These option in turn relate to one of the four levels. The 4-point Likert scale maps directly to the SPM3 model.

IT project managers are the unit of analysis and were randomly surveyed to get an objective view of how sustainability is incorporated in IT projects. Purposive sampling was used to select the IT project managers as they were part of the specific predefined group. The structured questionnaire used was in line with the SPM3 model to allow for the measurement of sustainability in IT projects. In total, 938 responses were used to assess the commitment of IT project managers to sustainability. The data gathered from these managers was processed and analysed using SPSS. Descriptive, inferential and multivariate statistics were used in this research.

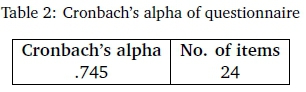

Reliability is a measure of the extent to which a research instrument consistently reflects the construct it is measuring (Field, 2013; G. Thomas, 2013). That is to say, if a study is conducted again at another point in time under similar circumstances, then the results of the second study should be comparable to those of the first. This study made use of scales in the assessment of sustainability and, as such, Cronbach's alpha was used as it is a measure of scale reliability (Field, 2013, p. 674). A Cronbach's alpha value of .7 or greater is used to determine if there is internal consistency (Field, 2013, p. 675). The questionnaire used in this study was tested for reliability by means of Cronbach's alpha as seen in table 2. An alpha value of .745 resulted from the analysis and indicates that there was internal consistency.

The validity relevant in this study was instrument-based validity as the primary concern was whether the research instrument measured what it was supposed to measure. The specific instrument-based validity considered was construct validity, as all other forms of validity are just offshoots of construct validity (G. Thomas, 2013, p. 140). Construct validity is the extent to which the results of the 'test', in this case the survey, conform to the theoretical construct around which the test is designed. The survey used in this study was based on the survey developed by (Silvius et al., 2012) and so construct validity was ensured.

4 RESULTS AND ANALYSIS

The results of this study focus on the perceived importance of sustainability as well as the dimensions of sustainability. A variety of demographic characteristics were examined, including age, job title and qualification level of the respondents, participating industry and affected regions. These characteristics revealed no interesting data even when they were taken into account with the rest of the analysis.

4.1 Perceived importance of the aspects of the sustainability decision

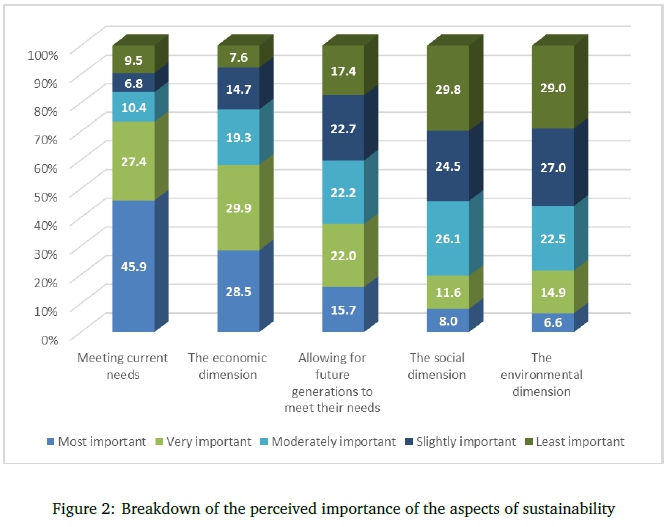

The respondents were given aspects of the definition of sustainability from the Brundtland Report and asked to rank them in order of importance. The aspects are meeting current needs, allowing for future generations to meet their needs, the economic dimension, the social dimension and the environmental dimension. These sustainability definition aspects are single items and do not consist of aspects themselves. Weighted averages of each aspect are used to show their order of importance. The weighted averages are as follows: meeting current needs (3.93), the economic dimension (3.57), allowing for future generations to meet their needs (2.96), the social dimension (2.44) and the environmental dimension (2.43).

A point of interest is the substantial and overwhelming difference between the first two aspects (meeting current needs and the economic dimension) and the last two (the social and environmental dimensions). The most notable order of importance is that of the three dimensions, the economic dimension was regarded as the most important by a substantial margin, with the social dimension placing second with a negligible margin over the environmental dimension. The findings correspond for the most part with what was found in the literature, but in this instance, the social dimension was regarded as more important (Edum-Fotwe & Price, 2009; Labuschagne & Brent, 2005; Martens & De Carvalho, 2014; Smith et al., 2011; Ullah et al., 2013). This difference, even though only marginal, may be due to the nature of IT and those industries which are considered to be relatively clean in terms of energy, water and paper usage (Jeucken & Bouma, 1999; Wang et al., 2013; Marcelino-Sádaba, González-Jaen, & Pérez-Ezcurdia, 2015).

A breakdown of the perceived importance of the aspects of sustainability is illustrated in Figure 2 and ordered according to their weighted averages.

From the breakdown, the extent to which each aspect was favoured is evident. Meeting current needs and the economic dimension collectively represent 74.4% of the most important rating and 57.3% of the very important rating. On the other hand, the social and environmental dimensions collectively only represent 14.6% of the most important rating and 26.5% of the very important rating.

The sustainability definition contains within it a duality which must be understood as a point of compromise and regarded as equal. This duality is meeting current needs while still allowing for future needs to be met. The results show that these two aspects were not regarded as equal, with meeting current needs comprising 73.3% of the most important and very important ratings. Allowing for future needs to be met, on the other hand, only comprises 37.7% of the most important and very important ratings. These results are concerning, as without this duality being treated as equal, the fundamental aim of sustainability will not be met.

4.2 The dimensions of sustainability

s section deals with the extent to which each dimension is addressed and a comparison of the dimensions is made. Each dimension comprises several aspects. The remainder of the results and analysis section refer to the maturity levels (4-point scale). Weighted averages in this study are used purely for comparison purposes. A weighted average of 2.5 or 2.9 for an aspect still means that the aspect is at the second level. This aspect can however be compared to other aspects and where it sits on the scale. The results are ordered by their weighted averages for easy identification of which aspects are better addressed.

4.3 The economic dimension

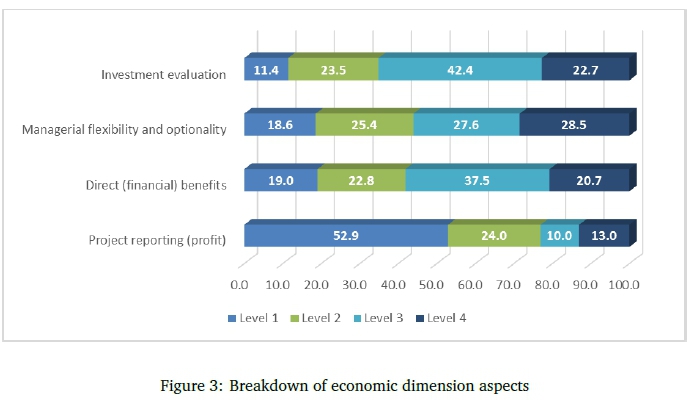

The economic dimension comprises four aspects, namely investment evaluation, managerial flexibility, direct financial benefits and project reporting profit. The weighted averages for each of these aspects are as follows: investment evaluation has the highest average at 2.76, followed by managerial flexibility (2.66), direct financial benefits (2.6) and lastly project reporting profit with an average of 1.83. The first three aspects have similar averages, indicating that they are addressed to a similar extent. On the other hand, project reporting is substantially lower. The breakdown for each of the economic aspects is illustrated in Figure 3. It indicates the percentage of respondents who felt they achieved a certain level in each of the economic dimension aspects.

The investment evaluation aspect is concerned with the evaluation methods used in the selection of IT projects. Level 1 had the smallest percentage of IT projects (11.4%), indicating that only a small portion of IT projects were evaluated and selected based predominantly on the payback period. Nearly a quarter of IT projects (23.5%) were evaluated and selected based primarily on the net present value of the investment or its return on investment. Level 3 had the highest percentage of IT projects (42.4%), implying that most IT projects were evaluated and selected based on a combination of short-/medium- and long-term returns. Just over a fifth of IT projects (22.7%) were categorised as being at the fourth level, which shows that a substantial portion of IT projects were evaluated and selected, based not only on the level 3 criteria, but also the consideration of economic, environmental and social aspects.

The managerial flexibility and optionality aspect is concerned with the extent to which IT projects allow for future decision making. Nearly a fifth of IT projects (18.6%) were at the first level, which indicates that this aspect was only considered implicitly and in accordance with company regulations. The remaining 81.4% of IT projects were considered explicitly, but the 25.4% of IT projects at level 2 indicates that this was only done reactively. The level 3 IT projects (27.6%) imply that this aspect was one of the areas that IT projects contribute to. Level 4 accounted for the highest percentage of IT projects (28.5%), which is in itself is a positive occurrence and indicates that contributing to this aspect was part of the justification for IT projects.

The direct financial benefits aspect is concerned with the types of benefits that are recognised in the business case of the project. The 19% of IT projects at level 1 indicates that nearly a fifth of IT projects recognised benefits implicitly. A further 22.8% of IT projects only recognised benefits in the form of cost savings or reduced use of resources. Level 3 reflected the most IT projects for this aspect (37.5%), which indicates that these IT projects recognised benefits from improved business processes and/or improved models for existing offerings. IT projects at level 4 indicate that just over a fifth (20.7%) of IT projects recognised benefits in terms of increased revenue deriving from improved offerings.

In contrast with the aforementioned economic aspects, the results on project reporting profit aspects gravitate towards the lower levels. This aspect is concerned with which items are included in the project reports, including progress reports. Over half of IT projects (52.9%) only reported on project activities, budget considerations and risk considerations in terms of planned outcomes and actual results achieved. The percentage of level 2 IT projects (24%) implies that nearly a quarter of IT projects reported on lessons learned and project improvements in addition to what was reported at level 1. Only 10% of IT projects reported on project design and delivery changes as well. The remaining 13% of IT projects reported on changes such as market conditions which may impact on the business case of the project and its resulting value, in addition to the previous levels.

For the most part, the economic dimension aspects yielded favourable distributions with investment evaluation (65.1%), managerial flexibility (56.1%) and direct financial benefits (58.2%) being addressed mostly at the third or fourth level. Incidentally, these three aspects appear to have a somewhat similar distribution, implying that they were deemed to be of similar importance. In contrast, the majority of projects for the project reporting profit aspect (52.9%) addressed sustainability only at the first level.

The economic aspects were tested for correlations and while statistically significant positive correlations were found between them, the correlations are weak. The implication of these results is that each of these aspects should be addressed specifically, as performance in one aspect may only have minimal positive impact on the performance in the other aspects of the economic dimension.

4.4 The social dimension

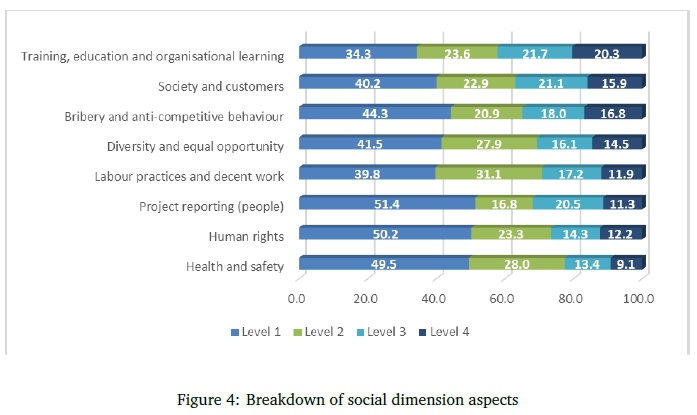

The social dimension comprises eight aspects, namely training, education and organisational learning, society and customers, bribery and anti-competitive behaviour, diversity and equal opportunity, labour practices and decent work, project reporting people, human rights, and health and safety. The weighted averages for these aspects range from 1.82 (health and safety) to 2.28 (training, education and organisational learning). The averages for all of these aspects are notably similar to each other, in contrast to those of the economic dimension. The implication is that they are all of similar importance. Another differentiating factor is how the social dimension aspects have noticeably lower averages than the economic dimension aspects. This indicates that the social dimension is addressed to a lesser extent, which may be an indication that it is perceived as being of less importance. The social dimension being regarded as less important than the economic dimension corresponds with what was found in the literature (Edum-Fotwe & Price, 2009; Labuschagne & Brent, 2005; Martens & De Carvalho, 2014; Singh et al., 2009; Smith et al., 2011; Ullah et al., 2013). The breakdown for each of the social aspects is illustrated in Figure 4.

Due to the low averages of the social dimension aspects, it is not surprising to see that the highest numbers of respondents felt that the first level was the highest level in each aspect at which social sustainability is addressed.

The training, education and organisational learning aspect is concerned with the extent to which IT projects include training, education and development of stakeholders. The largest portion of IT projects (34.3%) only included appropriate training and education of end users as part of the project's deliverable. The second level (23.6%) indicates that these projects included training and education for team members to improve performance in the project. Just over a fifth of the IT projects (21.7%) showed that they included training for improved performance after the project had been completed. The remaining 20.3% of IT projects included activities for developing relevant competences in all stakeholders.

The society and customers aspect is concerned with the extent to which IT projects follow a socially responsible approach towards the society in which they operate. Only recognising social responsibility towards external stakeholders in the society of operation is what was achieved by 40.2% of IT projects at level 1. Close to a quarter of IT projects (22.9%) required that suppliers and partners of the project take on social responsibility towards the societies in which they operated. For just over a fifth of IT projects (21.1%), results of the project were designed in such a way as to translate into social responsibility towards external stakeholders in the society in which they operated. Those IT projects in the level 4 category (15.9%) extended this translation towards society as a whole.

The bribery and anti-competitive behaviour aspect is concerned with the extent to which IT projects reject bribery and anti-competitive behaviour. According to a 2015 bribery survey, bribery within South Africa is a serious issue (Dobie, 2015). The survey found that 74% of the participants knew someone who had been asked to pay a bribe and of those who were asked, 75% ended up paying the bribe. The most disheartening statistic drawn from this survey is the 78% of participants who felt that paying a bribe was a necessity to get through life. This apparent acceptance of bribery is a possible reason for the poor results in the bribery and anti-competitive behaviour aspect. Based on these results, it is not surprising to find that 44.3% of IT projects were at the first level, where the team members were held accountable for rejecting bribery and anti-competitive behaviour. Just over a fifth of IT projects (20.9%) also required that their suppliers and partners reject bribery and anti-competitive behaviour. The 18% of IT projects at the third level indicates that bribery and anti-competitive behaviour was prevented in the organisation by the way the project deliverable and result were designed. The remaining 16.8% of IT projects indicates that bribery and anti-competitive behaviour prevention was also extended to the community within which the project result was directed.

The diversity and equal opportunity aspect is concerned with the extent to which IT projects apply policies or standards for diversity and equal opportunity which reflect the society in which they operate. Due to South Africa's history, the diversity of the workforce is not representative of the population. This necessitates that steps be taken to rectify the injustices of the past. South Africa has a unique regulation known as broad-based black economic empowerment (BBBEE) which has the aim of addressing diversity in the workforce. The inclusion of this regulation in South Africa puts additional pressure on South African organisations to comply with regulations. The added pressure in turn makes it more difficult for these organisations to progress past the first level and may play a role in the results. The highest percentage of IT projects (41.5%) merely complied with applicable standards and regulations regarding equal opportunity in areas such as gender, religion and race. Just under a third of IT projects (27.9%) required such compliance from suppliers and partners as well. Only 16.1% of IT projects designed deliverables to improve diversity and equal opportunity within the organisation and even fewer (14.5%) designed deliverables to improve diversity and equal opportunity within the community as well.

The labour practices and decent work aspect is concerned with the extent to which policies or standards for labour practices and decent work are applied to IT projects. The highest percentage of IT projects (39.8%) merely complied with applicable standards and regulations regarding labour practices and decent work. Just over a third of IT projects (31.1%) required such compliance from suppliers and partners as well. Close to a fifth of IT projects (17.2%) designed deliverables to improve labour practices and decent work in the organisation. The remaining 11.9% of IT projects designed deliverables to improve labour practices and decent work in the communities towards whom the result was directed.

The project reporting people aspect is concerned with whether IT projects report on indicators of social sustainability. Just over half of IT projects (51.4%) only reported on what was necessary in order to comply with laws and regulations. Almost a fifth of IT projects (16.8%) reported on social sustainability in terms of the resources used. Just over a fifth of IT projects (20.5%) reported on social sustainability in terms of the project deliverables. The remaining 11.3% of IT projects also reported on social sustainability in terms of the use and disposal of the project deliverables.

The human rights aspect is concerned with the extent to which IT projects apply policies or standards for respecting and improving human rights such as non-discrimination, freedom of association and stopping child labour. Over half of the IT projects (50.2%) only recognised this aspect implicitly and only complied with the necessary laws and regulations. Close to a quarter of IT projects (23.3%) considered this aspect explicitly, but only reactively with the intention of not compromising stakeholder interests. Only 14.3% of IT projects explicitly considered this as an area that the project contributed to. The remaining 12.2% of IT projects considered making a contribution to this aspect as part of the justification for the project.

The health and safety aspect is concerned with the extent to which policies or standards for health and safety are applied in IT projects. Health and safety is an aspect that is more commonly associated with projects in the construction and engineering fields, but this does not mean that IT projects are exempt. Nearly half of IT projects (49.5%) just complied with the applicable standards and regulations regarding health and safety. A further 28% of IT projects required such compliance from suppliers and partners of the project. As little as 13.4% of IT projects designed the deliverables of the project in such a way as to improve health and safety conditions within the organisation. Less than a tenth of IT projects (9.1%) extended this improvement to the communities towards whom the project results were directed.

The similarity between the bribery and anti-competitive behaviour aspect and the majority of the other aspects in the social dimension may indicate similar dispositions towards these aspects. What is more concerning are those aspects that are noticeably in a worse position, such as project reporting people, human rights and health and safety, whose level 1 responses made up 51.4%, 50.2% and 49.5% of their total responses, respectively. The rest of the aspects had a level 1 representation ranging from 34.3% to 44.3%. The highest level 3 and 4 representation was for training, education and organisational learning at 42%. This number drops to 22.5% for health and safety, with the rest of the aspects falling between these two. Overall it is clear that the social dimension is poorly catered for. While the measurements of the social dimension cannot be compared to the literature, what is common in both the literature and this study is that the social dimension is addressed to a lesser extent than the economic dimension.

4.5 The environmental dimension

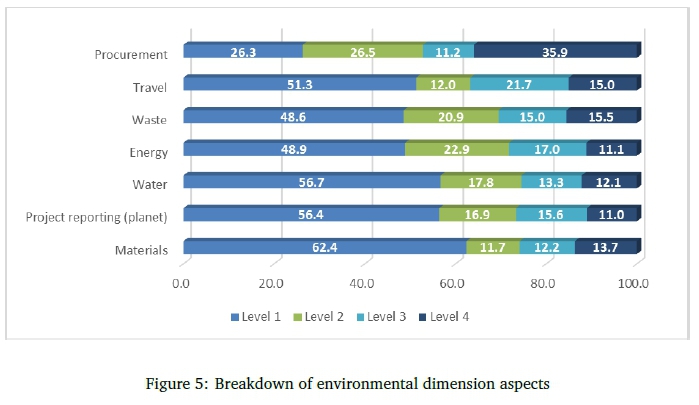

The environmental dimension comprises seven aspects, namely procurement, travel, waste, energy, water, project reporting planet and, lastly, materials. The weighted averages of these aspects range from 1.77 (materials) to 2.57 (procurement). The majority of the aspects have similar averages, with only procurement standing out as the best addressed aspect having the highest average outside of the economic dimension. The procurement average is similar to the investment evaluation, managerial flexibility and direct financial benefits aspects of the economic dimension and this may be due to procurement being associated with the economic dimension. Procurement is considered part of the environmental dimension as this is the way that it was initially placed. Procurement can be considered part of the as it depends on where it takes place. Apart from procurement, the other environmental aspects have similar averages to the aspects of the social dimension. This similarity with the social dimension also having lower averages than the economic dimension corresponds with what was found in the literature. The breakdown for each of the environmental aspects is illustrated in Figure 5.

As in the case of the social dimension aspects, it is not surprising that the environmental dimension aspects have high percentages of level 1 responses.

The procurement aspect is concerned with the criteria against which suppliers for IT projects are selected. Just over a quarter of IT projects (26.3%) selected suppliers based solely on laws and regulations. In South Africa laws and regulations can be increasingly imposing due to additional factors, such as BBBEE, which weigh heavily in the choice of supplier. A very similar portion of IT projects (26.5%) selected suppliers based on cost and location while still ensuring that the interests of stakeholders were not compromised. Only around a tenth of IT projects (11.2%) selected suppliers based on the suppliers' use of natural resources and environment-enhancing policies. Surprising and positive is that the highest percentage of IT projects (35.9%) was at the fourth level, indicating that suppliers were selected based on their ability to help deliver the project in a more sustainable way or aid in the contribution of the project result to sustainability.

The travel aspect is concerned with the extent to which travel policies of the project consider environmental aspects. Travel can form a major part of IT projects as team members may need to meet with various stakeholders. In project rollouts that are geographically dispersed, the need for travel is that much more important. In just over half of IT projects (51.3%) travel was based on necessity for completing project activities and selected based on time and cost. 12% of IT projects based travel on necessity for completing project activities, but the means of travel was selected while taking into account environmental aspects. Just over a fifth of IT projects (21.7%) sought alternatives to travel such as video conferencing when possible. The remaining 15% of IT projects designed their deliverables and results to minimise the required travel.

The waste aspect is concerned with the ways in which the project tries to minimise waste. Just under half of IT projects (48.6%) considered this aspect implicitly and merely ensured compliance with laws and regulations. Just over a fifth of IT projects (20.9%) considered this aspect explicitly, but only reactively with the aim of not compromising stakeholder interests. 15% of IT projects considered this aspect explicitly and as one of the areas the project contributed to. The remaining IT projects (15.5%) considered contributing to this aspect as part of the justification for the project.

The energy aspect is concerned with whether the project has any specific policies regarding energy consumption. Nearly half of IT projects (48.9%) had no specific energy consumption policies and followed the general energy consumption policies of the organisation. Another 22.9% of IT projects had energy consumption policies, but only promoted the smart use of energy and energy-efficient equipment where possible. 17% of IT projects kept energy consumption as low as possible and attempted to acquire the necessary energy from 'green' sources. The remaining 11.1% of IT projects considered minimising energy consumption as one of the parameters in the design of the project.

The water aspect is concerned with whether the project has any specific policies regarding water consumption and pollution. Clean water is a scarce resource in South Africa and while water usage during an IT project's implementation may be low, the project manager should take note of how water is managed in the manufacturing of equipment and how it is managed by the team members. More than half of IT projects (56.7%) had no specific water consumption policies and followed the general water consumption policies of the organisation. Just under a fifth of IT projects (17.8%) had water consumption policies, but they only promoted the smart use of water and water-saving equipment where possible. A further 13.3% of IT projects kept water consumption as low as possible and recycled or purified the water utilised. The remaining 12.1% of IT projects considered minimising water consumption and pollution as one of the parameters in the design of the project. Water was recycled or purified if it was to be disposed of.

The project reporting planet aspect is concerned with whether IT projects report on indicators of environmental sustainability. More than half of IT projects (56.4%) only reported on what was necessary in order to comply with laws and regulations. A further 16.9% reported on environmental sustainability in terms of the resources used. A little over 15% of IT projects (15.6%) reported on environmental sustainability in terms of the project deliverables. The remaining 11% also reported on environmental sustainability in terms of the use and disposal of the project deliverables.

The materials aspect is concerned with the criteria against which materials for the project are selected. Of all the aspects included in this study, the materials aspect had the highest level 1 representation with 62.4% of IT projects falling into this category. While this result appears to be negative, it should be considered in context. IT projects make use of very few materials, with the exception of infrastructure projects, which makes it logical to find such a high level 1 representation for this aspect. These projects indicated that materials for the project were selected solely on cost as well as functional and technical requirements. Just over a tenth of the projects (11.7%) also selected materials for the project based on the waste they caused. A further 12.2% of IT projects selected their materials based also on the energy they consumed and pollution created during their production. The remaining 13.7% of IT projects, in addition to what has been mentioned previously, selected materials based on their reuse capabilities and value.

Procurement (26.3%) is the only environmental aspect that had a level 1 representativeness of less than 48.6%. It also had the highest level 4 representativeness at 35.9%, which is more than double any of the other environmental aspects. Procurement is the most noticeable environmental aspect, with the remaining ones all having similar distributions. The implication is that these other aspects have similar importance. These results also indicate that the environmental dimension is in a poor position, even more so than the social dimension. Once again, the actual measurements cannot be compared to the literature; however, it is clear that the environmental dimension was not addressed to the same extent as the economic dimension, which conforms to what was found in the literature.

4.6 Dimension comparison

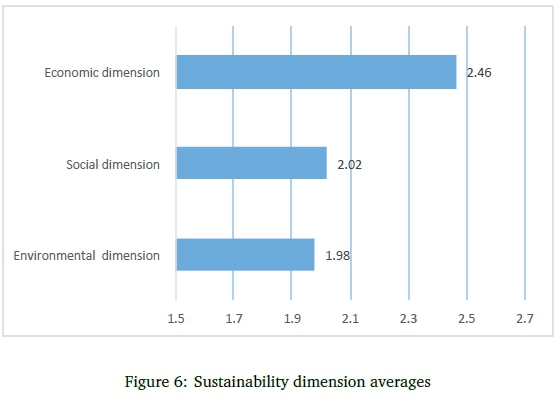

The dimensions as a whole were assessed and compared with each other in order to determine their overall standing within projects and with each other. The weighted dimension standing is determined as the average of all the aspects comprising it. The results are displayed in Figure 6.

Not surprisingly, based on the results from the individual dimension analysis and the definition analysis, the economic dimension has a noticeably higher average than the social and environmental dimensions. These results correspond with what was found in the literature, except for the social dimension appearing to be better addressed than the environmental dimension, albeit only slightly (Edum-Fotwe & Price, 2009; Labuschagne & Brent, 2005; Martens & De Carvalho, 2014; Smith et al., 2011; Ullah et al., 2013). Once again, the balance between the dimensions of sustainability as advocated by the TBL concept is not maintained, reinforcing the point that this is a problem regarding the incorporation of sustainability. The overall average for sustainability is only 2.15, indicating that the extent to which sustainability is incorporated into IT projects is somewhat lacking.

An explanation for the environmental dimension reflecting such poor results in this study, more so than the social dimension, can possibly be attributed, in part, to the adoption of green IT. Utilising green IT is perceived as addressing environmental sustainability within the IT field (Jenkin, Webster, & McShane, 2011). Green IT looks at designing and using IT-related components effectively and efficiently to reduce the impact on the environment as much as possible (du Buisson & Naidoo, 2014). Green IT addresses the development and use of IT components, but does not explicitly address the implementation of IT. The travel and reporting aspects of the environmental dimension are examples of areas that may fall outside the scope of green IT. Furthermore, IT is considered as relatively clean when looking at environmental sustainability with energy consumption being the most prominent aspect, and as such, the other aspects may fall by the wayside.

However, according to Figure 5, the energy aspect is addressed to a similar extent to most of the other environmental dimension aspects. The extent is poor, indicating that environmental sustainability is not of particular importance in IT projects. Procurement, having the highest average of aspects other than those in the economic dimension, highlights that money is still the primary focus. The similarly dismal results are seen in the social dimension, indicating that social sustainability is also not of particular importance in IT projects. The similarity between the social dimension and environmental dimension results may signify that there is a relationship between these dimensions that is separate from the economic dimension.

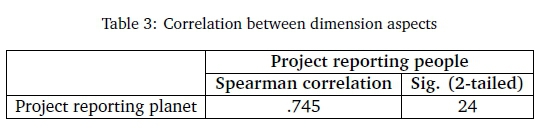

Correlations between the aspects of the dimensions were tested to determine what the relationship between the aspects of differing dimensions may be. Only one correlation was of significant strength to warrant mention and is shown in Table 3.

The correlation found is between project reporting planet from the environmental dimension and project reporting people from the social dimension. The correlation is positive and significant (p < 0.001), indicating that as one is addressed better, so is the other and vice versa. These results support the notion that the social and environmental dimensions are addressed separately from the economic dimension while being linked to each other.

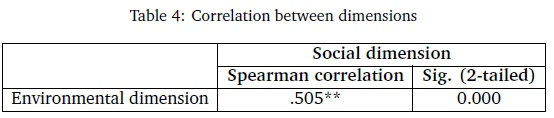

The relationships between the dimensions as a whole were tested for correlations and one noteworthy correlation was found. The correlation found is between the social and environmental dimensions and is shown in Table 4.

The correlation is positive as well as significant (p < 0.001) and further supports the idea that the social and environmental dimensions are linked. As one of the two is better addressed, so is the other. These results may be an indication that the social and environmental dimensions are in fact perceived and/or treated as one dimension. If this is the case, then a fair assessment would be to say that these dimensions are only half addressed.

4.7 State of sustainability in IT projects according to the SPM3 model

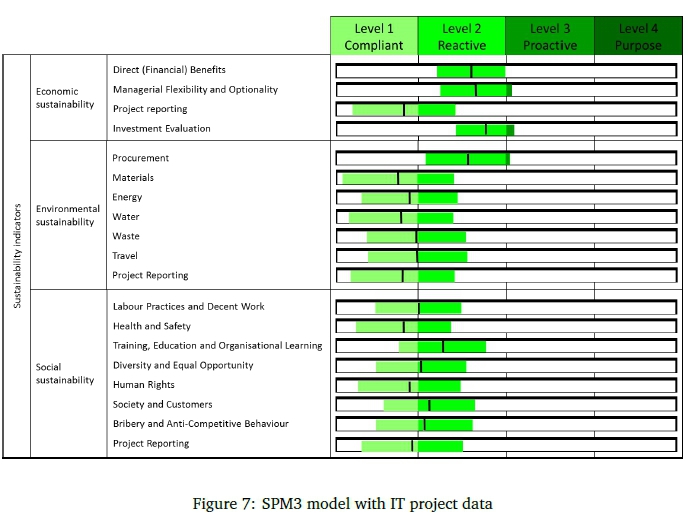

The results of the dimensions analyses are plotted on the SPM3 model and are illustrated in Figure 7.

The SPM3 model was developed to assess the integration of sustainability into a project based on four levels (Silvius & Schipper, 2015). The model is typically used to assess an individual project and therefore the scores for each of the aspects are at definitive levels. In this study many projects were assessed so the mean score as well as the spread about the mean (coefficient of variation) were used instead. The mean is used to assess the position of each aspect and the spread about the mean is used to determine the variability between projects. The mean for each aspect is indicated as the black line separating the upper and lower bound coefficient of variation (shaded area).

The model clearly indicates the poor extent to which sustainability is incorporated into IT projects, with the majority of aspects only being addressed at the first level. The economic dimension is the only dimension where the majority of aspects are comfortably at the second level and more than that, there is an indication of a shift towards the third level. All of the aspects in the environmental dimension, with the exception of procurement, are at the first level, but there is an indication of a shift towards the second level. The majority of the aspects in the social dimension are at the second level. Unlike with the other dimensions' aspects, the aspects in the social dimension show little indication of a shift to the next level.

The coefficient of variation reveals some interesting insights as the variability of each aspect can be compared with the others. The economic dimension aspects, with the exception of reporting and the inclusion of procurement, have the smallest coefficients of variation, indicating that there is some consistency in these aspects across IT projects. On the other hand, the aspects from both the social and environmental dimensions have significantly higher coefficients of variation. The implication is that there is little consistency in these aspects across IT projects. These results further support the idea that the economic dimension is better addressed and introduces the notion that the economic dimension aspects are afforded similar importance across IT projects. For the other dimensions it can be seen that their aspects are addressed to a similar extent, on average, but the variability indicates that these aspects do not hold similar importance across IT projects.

5 DISCUSSION

It is clear that the dimensions are not treated equally. The economic dimension is demonstrably better addressed than the social and environmental dimensions. The preferential treatment for the economic dimension as preached by the literature is once again found in this study. While this goes against the balance required to be sustainable, the overall position is poor. Only four out of the nineteen aspects lean towards the third level, with the majority below the second level. While this imbalance is a concern, it may be more prudent to address the overall positions of these aspects. It should be noted that when using the SPM3 model, only the fourth level indicates sustainability. The first three levels indicate progress towards acting sustainably.

The results of the analysis also indicate that the economic dimension is separate from the social and environmental dimensions; but more than that, the social and environmental dimensions are linked. The similar extent to which the social and environmental dimension aspects are addressed, the correlation between reporting people and planet as well as the correlation between the social and environmental dimensions overall make a compelling case. If these dimensions are considered as one, then effort could be diluted between the two instead of addressing each in its own capacity.

In using the SPM3 model to assess sustainability, two flaws are apparent. The first is that the model does not cater for performance that is below the first level. This may be difficult, as admitting such performance may reveal legal violations or 'skeletons in the closet' (hidden unpalatable truths). The second flaw is that the model does not cater for performance that seeks to improve the situation. This may not be a flaw in the model but rather in the definition of sustainability. Doomsayers preach that we have passed the point of no return or that what we believe to be sustainable practices are just delaying the inevitable. Regardless of the truth, however ugly it may be, should the definition of sustainability not extend to attempt to correct the situation which created the concern for sustainability in the first place?

The SPM3 model is a maturity model and so in assessing the extent to which sustainability is incorporated into IT projects, the maturity of IT projects with regard to sustainability is also indicated. The lack of literature on sustainability in IT projects does nothing to aid the apparent low level of project maturity in relation to sustainability, necessitating further research in this vein. Over time, as sustainability becomes more synonymous with project management, this level of maturity is in all likelihood going to improve. The extent to which sustainability is incorporated also sheds light on the commitment of IT project managers to sustainability. As project managers direct project activities, they have control over what standards must be adhered to. Therefore some of the onus for addressing sustainability adequately and holistically falls on them. For them to live up to this duty, they need to understand sustainability in its entirety and how sustainability should be addressed, and they should be held accountable.

6 CONCLUSION

The research was conducted with the objective of assessing the commitment of IT project managers to sustainability. The state of research currently carried out in this regard is considered to be interpretive (Silvius & Nedeski, 2011; Silvius et al., 2012) and conceptual (Martens & De Carvalho, 2014). What this implies is that these studies consider how sustainability could be interpreted within the context of project management rather than the prescriptive approach of how it should be interpreted. As research in the field of project management sustainability is emerging, researchers must rely on concepts. Martens and De Carvalho (2014) state that empirical studies are required to understand how the concepts of sustainability can be implemented within project management. Current research has been conducted on the theoretical aspects of this field, but leaves a void where the practical implementation aspects are concerned.

Sustainability is the concept that future and current needs can be met by ensuring that in all activities a balance is achieved between the economic, social and environmental aspects. The projects of organisations are included as an activity and are therefore not exempt from sustainability consideration. However, a balance between the three dimensions is not regarded as the norm, with the economic dimension taking priority while the social and environmental dimensions are sidelined.

Projects are uniquely positioned to include sustainability as they are the vehicles through which organisations deliver change. They can thus be used to ensure sustainability through the deliverable as well as the manner in which it is delivered. IT projects are no exception; however, how sustainability is addressed may differ as IT projects are inherently different from other projects such as those in construction. Sustainability in projects is measureable through the use of the SPM3 model which indicates the maturity stages of aspects of the project with regard to sustainability.

Asking the respondents to rank the various aspects of sustainability in terms of importance revealed two interesting themes. The first of these is that the 'current' is considered to be substantially more important than the 'future'. This is a point of concern as it contradicts one of the fundamental aims of sustainability, which is to be forward thinking. The second theme is the ranking of the sustainability dimensions. The economic dimension being regarded as more important than the other two corresponds with what was found in the literature. The similar ranking of the social and environmental dimensions also corresponds with what was found in the literature. These results show the perception of the respondents and give insight into how sustainability is addressed.

The assessment of each dimension shows in detail the non-commitment of IT projects to each aspect as well as the respective dimensions overall. The results reveal that the economic dimension, not surprisingly, is in a better position than the other dimensions, with the majority of IT projects addressing sustainability at the third or fourth level for this dimension. The reverse is found in the social and environmental dimensions, with the majority of IT projects addressing sustainability at the first or second level. Such a detailed breakdown allows for areas of poor performance to be identified and addressed, thus aiding in the commitment to sustainability.

The aspects within each dimension were tested for correlations to better understand the relationship between them. Several significant correlations were found, indicating that these aspects are not isolated from each other. The cause of the relationships is unknown, but may be explained by the way they are addressed, that is to say, the policies which affect one aspect also affect another. Such knowledge is crucial to organisations in attempting to better address sustainability within their projects.

In addition to examining each dimension individually, the dimensions were compared overall. Unsurprisingly and conforming to what was found in the literature, the economic dimension is addressed to a better extent than the social and environmental dimensions. The dimensions themselves were tested for correlations and reveal a significant correlation between the social and environmental dimensions. The implications are that the social and environmental dimensions are treated as one and not seen as separate areas to be considered. This may be a potential reason why these dimensions are not addressed to the same extent as the economic dimension, as effort may be diluted across them.

Overall, the commitment of IT project managers to sustainability is clearly lacking. The extent to which IT projects commit to sustainability is poor and is a reflection of the IT project managers' commitment to sustainability.

References

Aronson, J. & Neysmith, S. M. (1996). ''You're not just in there to do the work". Gender & Society, 10(1), 59-77. https://doi.org/10.1177/089124396010001005 [ Links ]

Azizi, M. (2005). Decision making for raw material procurement in paper making factory. In Proceedings of 8th International Symposium oftheAHP, University of Hawaii, Honolulu.

Brummet, R. L., Flamholtz, E. G., & Pyle, W. C. (1968). Human Resource measurement-A challenge for accountants. The Accounting Review, 43(2), 217-224. [ Links ]

Dempsey, N., Bramley, G., Power, S., & Brown, C. (2011). The social dimension of sustainable development: Defining urban social sustainability. Sustainable Development, 19(5), 289-300. https://doi.org/10.1002/sd.417 [ Links ]

Dillard, D. (1987). Money as an institution of capitalism. Journal of Economic Issues, 21(4), 1623-1647. https://doi.org/10.1080/00213624.1987.11504717 [ Links ]

Dillard, J., Dujon, V, & King, M. C. (2008). Understanding the social dimension of sustainability. Routledge.

Dobie, K. (2015). South African citizens' bribery survey 2015. Last accessed 13 Jun 2017. Retrieved from http://www.tei.org.za/images/pdf/CitizensBriberySurveyFINAL2Dec2015.pdf

Douthwaite, R. (1993). The growth illusion: How economic growth enriched the few, impoverished the many, and endangered the planet. Council Oak Books.

du Buisson, W. & Naidoo, R. (2014). Exploring factors influencing IT workers' green computing intention at a South African firm. In Proceedings of the Southern African Institute for Computer Scientist and Information Technologists Annual Conference 2014 (p. 148). ACM. https://doi.org/10.1145/2664591.2664609

Edum-Fotwe, F. T. & Price, A. D. (2009). A social ontology for appraising sustainability of construction projects and developments. International Journal of Project Management, 27(4), 313-322. https://doi.org/10.1016/j.ijproman.2008.04.003 [ Links ]

Elkington, J. (1997). Cannibals with forks: The triple bottom line of 21st century business. Oxford: Capstone Press. [ Links ]

Erasmus, W. & Marnewick, C. (2012). Project management - The saviour in turbulent times? A cross-sector analysis. In Proceedings of the 24th Annual Conference of SAIMS, Stellenbosch.

Field, A. (2013). Discovering statistics using SPSS (4th). Sage publications.

Gareis, R., Huemann, M., Martinuzzi, A., Weninger, C., & Sedlacko, M. (2013). Project management and sustainable development principles. Project Management Institute.

Gore, A. (2006). An inconvenient truth: The planetary emergency of global warming and what we can do about it. Rodale.

Handy, C. (2002, December). What is a business for? Harvard Business Review, 49-55. [ Links ]

Hartman, F. (2001). The key to enterprise evolution-Future PM. In Proceedings of the Project Management Institute Annual Seminars and Symposium, Nashville, Tennessee.

Hedman, J. & Henningsson, S. (2011). Three strategies for green IT. IT Professional, 13(1), 54-57. https://doi.org/10.1109/MITP.2010.141 [ Links ]

Herazo, B., Lizarralde, G., & Paquin, R. (2012). Sustainable development in the building sector: A Canadian case study on the alignment of strategic and tactical management. Project Management Journal, 43(2), 84-100. [ Links ]

Higgins, P (2010). Eradicating ecocide: Laws and governance to stop the destruction of the planet. Shepheard-Walwyn, London.

Jacobsson, M., Lundin, R. A., & Söderholm, A. (2015). Researching projects and theorizing families of temporary organizations. Project Management Journal, 46(5), 9-18. https://doi.org/10.1002/pmj.21520 [ Links ]

Jenkin, T. A., Webster, J., & McShane, L. (2011). An agenda for 'green' information technology and systems research. Information and Organization, 21(1), 17-40. https://doi.org/10.1016/j.infoandorg.2010.09.003 [ Links ]

Jeucken, M. H. & Bouma, J. J. (1999). The changing environment of banks. Greener Management International, 27, 21-35. [ Links ]

Joseph, N. (2013). A predictive model for information technology project success (Master's thesis, University of Johannesburg, Johannesburg, South Africa). [ Links ]

Kaplan, R. S. & Norton, D. P (2001). The strategy-focused organization: How balanced scorecard companies thrive in the new business environment. Harvard Business Press. https://doi.org/10.1108/sl.2001.26129cab.002

Keeys, L. (2014). Strategy formation for project sustainable development: Tales of alignment and emergence. In Proceedings of the Project Management Institute Research & Education Conference 2014, Portland, Oregon.

Kendall, G. & Willard, B. (2016). Future-fit business benchmark. Last accessed 15 Jun 2017. Retrieved from http://futurefitbusiness.org/resources/downloads/

King, M. (2009). King code of governance for South Africa 2009. Johannesburg: Institute of Directors in Southern Africa. [ Links ]

Labuschagne, C. & Brent, A. C. (2005). Sustainable project life cycle management: The need to integrate life cycles in the manufacturing sector. International Journal of Project Management, 23(2), 159-168. https://doi.org/10.1016/j.ijproman.2004.06.003 [ Links ]

Ludwig, D., Hilborn, R., & Walters, C. (1993). Uncertainty, resource exploitation, and conservation: Lessons from history. Ecological Applications, 548-549. https://doi.org/10.1126/science.260.5104.17

Marcelino-Sádaba, S., González-Jaen, L. F., & Pérez-Ezcurdia, A. (2015). Using project management as a way to sustainability: From a comprehensive review to a framework definition. Journal of Cleaner Production, 99, 1-16. https://doi.org/10.1016/jjclepro.2015.03.020 [ Links ]

Marnewick, C. (2015). Project management sustainability in an emerging economy. In 3rd IPMA Research Conference. Stellenbosch: IPMA.

Martens, M. L. & De Carvalho, M. (2014). A conceptual framework of sustainability in project management. In Proceedings of the Project Management Institute Research and Education Conference 2014, Portland, Oregon.

Olivier, M. (2009). Information technology research - A practical guide for computer science and informatics. Hatfield. Pretoria: Van Schaik Publishers. [ Links ]

Pike, R. (2012, March). Social license to operate: The relevance of social license to operate for mining companies. Last accessed 13 Jun 2017. Retrieved from http://www.schroders.com/staticfiles/schroders/sites/americas /us%20institutional%202011/pdfs/social-licence-to-operate.pdf

Pines, G. L. & Meyer, D. G. (2005). Stopping the exploitation of workers: An analysis of the effective application of consumer or socio-political pressure. Journal of Business Ethics, 59(1), 155-162. [ Links ]

Seghezzo, L. (2009). The five dimensions of sustainability. Environmental Politics, 18(4), 539-556. [ Links ]

Shafiee, S. & Topal, E. (2009). When will fossil fuel reserves be diminished? Energy Policy, 37(1), 181-189. https://doi.org/10.1016/j.enpol.2008.08.016 [ Links ]

Silvius, A. & Nedeski, S. (2011). Sustainability in IS projects: A case study. Communications of the IIMA, 11(4), 1. [ Links ]

Silvius, A., Schipper, R., Planko, J., van den Brink, J., & Köhler, A. (2012). Sustainability in project management. Surrey, UK: Gower Publishing. [ Links ]

Silvius, A. & Schipper, R. (2010). A maturity model for integrating sustainability in projects and project management. In 24th World Congress of the International Project Management Association (IPMA) Istanbul, Turkey.

Silvius, A. & Schipper, R. (2015). Developing a maturity model for assessing sustainable project management. Journal ofModern Project Management, 3(1). [ Links ]

Silvius, A. & Schipper, R. I? (2014a). Sustainability in project management: A literature review and impact analysis. Social Business, 4(1), 63-96. https://doi.org/10.1362/204440814X13948909253866 [ Links ]

Silvius, A. & Schipper, R. P (2014b). Sustainability in project management competencies: Analyzing the competence gap of project managers. Journal of Human Resource and Sustainability Studies, 2014.

Silvius, A., Schipper, R., & Nedeski, S. (2013). Sustainability in project management: Reality bites.

Singh, R. K., Murty, H. R., Gupta, S. K., & Dikshit, A. K. (2009). An overview of sustainability assessment methodologies. Ecological indicators, 9(2), 189-212. https://doi.org/10.1016/j.ecolind.2008.05.011 [ Links ]

Smith, P A., Smith, P A., & Sharicz, C. (2011). The shift needed for sustainability. The Learning Organization, 18(1), 73-86. https://doi.org/10.1108/09696471111096019 [ Links ]

Snyder, C. S. (2013). A guide to the project management body of knowledge: PMBOK guide (5th).

Sonnenberg, D. & Hamann, R. (2006). The JSE Socially Responsible Investment Index and the state of sustainability reporting in South Africa. Development Southern Africa, 23(2), 305-320. https://doi.org/10.1080/03768350600707942 [ Links ]

Thomas, G. (2013). How to do your research project: A guide for students in education and applied social sciences. Sage.

Thomas, T. E. & Lamm, E. (2012). Legitimacy and organisational sustainability. Journal of Business Ethics, 110(2), 191-203. https://doi.org/10.1007/s10551-012-1421-4 [ Links ]

Toman, M. A. (2006). The difficulty in defining sustainability. The RFF reader in environmental and resource policy, 2.

Ugwu, O. & Haupt, T. (2007). Key performance indicators and assessment methods for infrastructure sustainability-A South African construction industry perspective. Building and Environment, 42(2), 665-680. https://doi.org/10.1016/j.buildenv.2005.10.018 [ Links ]

Ullah, A., Lai, R., & Marjoribanks, T. (2013). A proposed model for business sustainability based on business and information technology. Journal of Software, 8(11), 2796-2806. https://doi.org/10.4304/jsw.8.11.2796-2806 [ Links ]

Wang, N., Wei, K., & Sun, H. (2013). Whole life project management approach to sustainability. Journal of Management in Engineering, 30(2), 246-255. https://doi.org/10.1061/(ASCE)ME.1943-5479.0000185 [ Links ]

Watts, P & Holme, R. (1999). Corporate social responsibility: Meeting changing expectations. World Business Council for Sustainable Development.

Weatherford, J. (1997). The history of money: The struggle over money from sandstone to cyberspace. Crown Press.

World Commission on Environment and Development. (1987). Our common future: Report of the World Commission on Environment and Development. Oxford University Press.

Received: 7 June 2016

Accepted: 20 December 2016

Available online: 9 July 2017

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}