Servicios Personalizados

Articulo

Inglés (pdf)

Inglés (pdf)

Articulo en XML

Articulo en XML Referencias del artículo

Referencias del artículo

Indicadores

Links relacionados

-

Citado por Google

Citado por Google -

Similares en Google

Similares en Google

Compartir

Permalink

PermalinkDe Jure Law Journal

versión On-line ISSN 2225-7160

versión impresa ISSN 1466-3597

De Jure (Pretoria) vol.50 no.2 Pretoria 2017

http://dx.doi.org/10.17159/2225-7160/2017/v50n2a2

ARTICLES

The protection of stakeholders: the South African social and ethics committee and the United Kingdom's enlightened shareholder value approach: Part 2*

Die beskerming van belanghebbendes: die Suid-Afrikaanse sosiaal en etiek komitee en die Verenigde Koninkryk se ingeligte aandeelhouer waarde benadering: Deel II

Irene-marié EsserI; Piet DelportII

ILLM, LLD. Senior Lecturer in Commercial law: University of Glasgow Professor Extraordinarius: University of South Africa Visiting Professor: The Open University, United Kingdom

IILLD, H DipTax Law. Professor of Mercantile Law: University of Pretoria

OPSOMMING

In hierdie tweede deel van die artikel word die toepassing van CSR in praktyk nagegaan, met die sosiaal en etiese komitee as Suid-Afrikaanse model en die statutêre sosiaal en etiese komitee wat gebruik word in die Verenigde Koninkryk. Ondersoek word ingestel of sodanige komitee, of 'n statutêre benadering, soos vervat in artikel 172 van die VK Maatskappyewet, verkieslik is.

1 The Social and Ethics Committee

Sections 72(4), (8), (9) and (10) of the 2008 Companies Act provide as follows:

72. Board committees. -

(4) The Minister, by regulation, may prescribe -

(a) a category of companies that must each have a social and ethics committee, if it is desirable in the public interest, having regard to -

(i) annual turnover;

(ii) workforce size; or

(iii) the nature and extent of the activities of such companies;

(b) the functions to be performed by social and ethics committees required by this subsection; and

(c) rules governing the composition and conduct of social and ethics committees.

(8) A social and ethics committee of a company is entitled to -

(a) require from any director or prescribed officer of the company any information or explanation necessary for the performance of the committee's functions;

(b) request from any employee of the company any information or explanation necessary for the performance of the committee's functions;

(c) attend any general shareholders meeting;

(d) receive all notices of and other communications relating to any general shareholders meeting; and

(e) be heard at any general shareholders meeting contemplated in this paragraph on any part of the business of the meeting that concerns the committee's functions.

(9) A company must pay all the expenses reasonably incurred by its social and ethics committee, including, if the social and ethics committee considers it appropriate, the costs or the fees of any consultant or specialist engaged by the social and ethics committee in the performance of its functions.

(10) Section 84 (6) and (7), read with the changes required by the context, apply with respect to a company that fails to appoint a social and ethics committee, as required by this section and the regulations.

1 1 Composition and Appointment

Regulation 431 deals with the social and ethics committee as referred to in section 72 of the Act.2

This regulation applies to all state-owned companies, public companies that are listed3 or any other company that complies with certain criteria.4 A public interest score of more than 500 points (in any 2 of the preceding 5 financial years) will be relevant in this regard. The 'public interest score' is calculated at the end of a financial year as the sum of a number of things. It is the aggregate of the number of points equal to the average number of employees of the company during the financial year (contract workers are annualised over the particular financial year); one point for every R1 million (or portion thereof) in third party liability of the company, at the financial year end; one point for every R1 million (or portion thereof) in turnover during the financial year; and one point for every individual who, at the end of the financial year, is known by the company, in the case of a profit company, to directly or indirectly have a beneficial interest in any of the company's issued securities; or, in the case of a non-profit company, to be a member of the company, or a member of an association that is a member of the company.5 The public interest score is thus a method used to determine whether a company must comply with enhanced accountability requirements based on its social and economic impact.

A minimum of three directors or prescribed officers6 must serve on a company's social and ethics committee. At least one must be a director who has, at least for the previous three financial years, not have been involved in the day-to-day management of the company's business.7

From the literature available it seems if there is some disagreement as to the exact legal status of this committee. In Henochsberg it is argued that the social and ethics committee is not a board committee, but a separate organ of the company.8 It is stated that, based on an interpretation of the Regulations, the committee is a company committee and not a board committee. Also, the social and ethics committee has a responsibility to report to the shareholders, but must only draw the attention of the board to certain matters.9 Furthermore, it is argued that the Act empowers the board to delegate additional functions to the audit committee, a provision that is not present in respect of the social and ethics committee.10 Joubert, on the other hand, argues that it is a board committee based on the short title of section 72 and the overall context of section 72 of the Companies Act.11 It is clearly of importance whether the social and ethics committee is a board committee or not. If it is a board committee then the board can delegate certain powers and authority to the committee. This will be in addition to those listed in the Act. If it is a company committee then it will only have the powers and authority as provided for in the Act and Regulations. This also has an impact on the standard of conduct and the liability of the members of this committee, as board committee members are, in the case of directors, subject to the same duties as directors, as will be discussed later.12

1 2 Functions

The division of power between the shareholders and the board of directors is relevant when considering the functions of the SEC. The two (main) organs of the modern company are the general meeting (meeting of shareholders) and the board of directors.13 The Act provides that the business and affairs of a company must be managed by or under the direction of its board, which has the authority to exercise all of the powers and perform any of the functions of the company, subject to the extent that the Act or the company's memorandum of incorporation14provides otherwise.15 The Act therefore introduced a shift in ultimate power in the company from the shareholders to the board.16 The board of directors now has the ultimate power in the company, subject to the Act and the MOI. Therefore where the Act provides that 'the company' must act, that would now be the board of directors and not the shareholders (collectively), unless the Act makes it clear that the opposite will apply.17 This provision on the shift in power from the shareholders to the board of directors has some serious consequences.

Ultimate (indirect) control of a company is usually in the hands of the shareholders as they have the power to appoint and remove directors. The level of protection that shareholders receive in terms of the 2008 Companies Act is, however, different compared to the 1973 Companies Act as shareholders no longer have an original decision-making power. This is due to the enactment of section 66. Section 66(1) apparently creates a positive duty on the board of directors to manage the company as it provides that the business and affairs of the company must be managed by or under the direction of its board. It also means, due to the use of the words 'business and affairs', that the ultimate power is no longer with the shareholders in general meeting, unless otherwise stated in the Act or the MOI.18 The powers of the directors are now given by statute and not delegated or derived from an agreement between the shareholders and the directors. The ultimate responsibility for good corporate governance thus lies with the board of directors.19

The significance of the power to manage the business and affairs in terms of section 66 is twofold. The power is now original and no longer delegated from the shareholders. This shift from the previous position also happened in Canada, one of the models for the Act, and the significance thereof was summarised as follows: 'The directors' power is original, not delegated: as such, it is not subject to controls by the shareholders, except as specified in the applicable statute.'20 This is also true with regard to South Africa. This means, inter alia, that the shareholders no longer have the inherent residual power to take a decision in case of a deadlock. This principle was, however, not applied consistently in the Act, and section 81(1)(d) refers to the deadlock ground as a ground for the winding-up of a solvent company. In Henochsberg it is stated that 'if the directors are in deadlock, the power to take over the powers of the directors does not transfer to the shareholders as the 'highest' authority in the company'. The same principle applies if the MOI or Act does not provide who must exercise the power.21

Secondly, the ultimate power is now in the hands of the board of directors and no longer with the shareholders. Therefore, unless the qualifications of section 66 are complied with, the board of directors is now the ultimate organ of the company. The significance of this is that the shareholders, as erstwhile ultimate holders of authority and power, cannot at common law ratify any actions by the directors beyond their authority or in transgression of their duties in acting on authority of the shareholders, except to the extent that the Act or the MOI expressly provides otherwise.

Also, statutory provisions can provide that the 'company' can or may do certain things.22 It is thus important to determine whether the board or the shareholders will act as the company. Based on section 66(1) it seems that the default position is that 'the company' now refers to the board of directors and no longer to the shareholders. Thus, 'if the board acts, the company acts'.

The committee has reporting as well as monitoring duties. It has to monitor the company's activities, having regard to any relevant legislation, other legal requirements or prevailing codes of best practice23with regard to certain matters. These matters include social and economic development, good corporate citizenship, the environment, health and public safety, consumer relationships and labour and employment issues.

The committee has to consider matters relating to the company's social and economic development and this will include the company's standing relating to the goals and purposes as provided for in the United Nations' Global Compact Principles, the Organisation of Economic Cooperation recommendations on corruption, the Employment Equity Act24 as well as the Broad Based Black Economic Empowerment Act.25

Matters relating to good corporate citizenship also fall within their mandate and here reference is made to, inter alia, the promotion of equality, the prevention of unfair discrimination and the reduction of corruption. Further matters within their mandate include environmental, health and public safety issues as well as consumer relationships. Finally labour and employment is also listed and here reference is made to the International Labour Organization Protocol on decent work and working conditions.26

The committee is also entitled, but not obliged, to report annually to the shareholders at the company's annual general meeting on the matters within its mandate.27

The committee is also tasked with developing and monitoring a human rights management policy and system. On environmental, health and public safety the committee has a general duty to consider the impact of the company's activities and of its products and services. The committee is then also tasked to determine and monitor the company's standing in terms of the goals and purposes of the BBBEE Act. They should also monitor the company's activities relating to its consumer relations and this includes advertising, public relations and compliance with consumer protection legislation.28

A few remarks are appropriate with regard to the functions of the committee. First, the functions given to this committee are very wide and clear guidance on what is expected from this committee is not provided.29 Specific terms of reference are not provided.30 They can, for example, claim any costs or fees31 for appointing consultants and experts, but they do not have the power to make appointments.32 If the committee is a board committee, as discussed above, the board can give them this power. If not, the existence of this power is in doubt.

Secondly, as stated above, the committee should monitor the company's activities, having regard to all relevant legislation and codes as well as other legal requirements, and this is not just in relation to matters of a social nature as it extends to a wide range of issues like the environment, health and public safety. All relevant legislation, codes etc are not listed in the Regulations and a notable omission is King III.

Reference to national applicable instruments would have been preferred.33 Knowledge of the relevant legal position concerning these fields is thus necessary. It basically covers all dimensions of social responsibility, sustainability and corporate citizenship.34 The wider the scope of the duties of committee members the more unlikely that people will be willing to serve on such committees.35 Joubert36 argues that the task of identifying the relevant codes and legislation and performing the required monitoring and reporting functions in respect of the specific matters listed is quite an onerous task.

Thirdly, when considering the various matters that fall within the mandate of the committee it is abundantly apparent that the precise nature of these matters and the extent that the committee must pay attention to it is not clear. Herewith a few examples: The meaning of 'social and economic development' as one of the matters that the committee must monitor and report on, is unclear.37 Kloppers38 argues that the committee should focus more on social development as opposed to economic development, as the last mentioned is already dealt with by the audit committee.39 However, just because another committee already deals with an issue does not necessarily mean that the social and ethics committee does not have to pay attention to the issue if it falls within its statutory mandate. Also, reference is made to the Employment Equity Act40 in the context of 'social and economic development', but it is not clear whether the social and ethics committee should take responsibility for employment equity matters and the employment equity plan (as required by the Employment Equity Act). If it is argued that the social and ethics committee must take responsibility for these matters, and thus have more than a mere oversight function, then it can intrude with the functions of other board committees.41 Furthermore, a clearer definition of 'health' and 'public safety'42 would have been beneficial. It is not clear whether it only concerns occupational health, the health of consumers etc.

1 3 Appraisal

Some of the uncertainties with regards to this committee have already been touched upon above. The first issue concerns the appointment of this committee and whether or not it is a company committee or a board committee. We are of the view that the most convincing argument, in favour of the fact that it is a company committee and not a board committee, is the fact that the committee has the right, in its discretion, to report back to the shareholders. This is wider than their responsibility to simply draw certain matters to the attention of the board.43 It is clearly important how one classifies this committee. If it is a board committee then the members will have the same duties as directors. If it is a company committee then it is not the case and the members are only subject to the functions and powers as stated in the Act and the Regulations. The importance of this distinction is that if the committee is not a board committee, without any fiduciary duties as directors and/or prescribed officers in terms of the common law or the Companies Act, towards the company, it can make recommendations to the board, and also report to the shareholders, on matters and in a manner that is not in the interest of the company. In this sense the committee is in the same position as the shareholders who, as organ of the company, do not have fiduciary duties towards the company.44 Recommendations to the board for implementation would, obviously, be subject to the fiduciary duties of the board. However, if the board cannot or will not implement those recommendations, due to their fiduciary duties, a recommendation to the shareholders can result in removal of the board in terms of section 71, as neither the committee nor the shareholders have any fiduciary duties towards the company.

Secondly, on the functions of this committee, it was discussed above that clear terms of reference are not provided and that committee members will most probably be unclear as to what is precisely expected from them. Their functions will also, most definitely, overlap with some of the functions of the other committees, for example the remuneration committee, which is a board committee, in respect of employment issues. In this sense most of the duties and responsibilities of the social and ethics committee fall within the duties and responsibilities of the board in any case as the board has to take all the interests of stakeholders into account when acting for the benefit of the company.45 None of the 'stakeholders' as listed in regulation 43 can, directly or by implication, be excluded from the attention of the board in the exercise of its duties. To require the committee to merely report to the board on the matters as outlined in the regulations would be counter-productive, as the board would, in most if not all instances, already have knowledge thereof or will be alerted thereto by e.g. the company secretary or other management divisions within the company, such as labour developments by the human resources department, consumer issues by the legal and compliance department and so forth. Both the social and ethics committee and the audit committee also have an interest in sustainability disclosures and assurances.46 In addition, many of the risk issues that fall within the mandate of the audit committee, at least from a King III perspective and requirements, are also the responsibility of the social and ethics committee, such as the monitoring of and reporting on issues such as corruption. From a practical perspective this overlap is not effective. Two committees will thus report back to the board on the same issues. These committees may also have different views on the matters that they report on. From a cost perspective, the company has to remunerate members of different committees attending to the same matter. The different committees can, presumably, first talk to each other informally before they report back to the board to ensure that they do not provide conflicting views, but this will not solve the cost issues and this modus operandi is unacceptable per se from a corporate governance viewpoint due to, inter alia, lack of formal procedures and documentation. Also if the same members serve on both committees they will basically just meet once with two agendas. It is thus very important that a company provides, as far as it is practically possible, very clear terms of reference for each of its committees, within the ambit of the Act and the Regulations, and also taking into account the functions performed by the executive management and other divisions in the company. In practice the biggest danger has been shown here that the social and ethics committee may want to dictate to management and other divisions in the company as to the work to be done by the latter for the company or for the social and ethics committee. This is clearly untenable and should not be allowed. However, due to the uncertainties as to the exact role and function of the social and ethics committee, it is difficult, if not impossible, to manage this situation effectively in a company.47

Thirdly, the function of the social and ethics committee to report to the shareholders, as mentioned above, is most probably the biggest challenge. This can be explained as follows: In terms of Regulation 43(5)(c) the committee may report, through one of its members, to the shareholders at the company's annual general meeting on the matters within its mandate. If the committee brings a matter before the board, the board has to make a decision based on its duties towards the company. In other words they must act in the best interest of the company. If the committee is not a board committee, without any fiduciary duties, in terms of the common law or the Companies Act, towards the company as discussed above, it can make recommendations to the board, and also report to the shareholders, on matters and in a manner that is not in the interest of the company as defined above. If the board, however, does not implement the matter brought under their attention then the social and ethics committee can report back to the general meeting of shareholders as this is a matter that falls within their mandate. The shareholders can of course not implement the decision,48but they can remove a specific director or even all the directors elected by shareholders. This ultimate power of shareholders in respect of directors could affect the discretion of the board in respect of the implementation of a matter reported on by the social and ethics committee.49 In other words the shareholders can enforce CSR through the reporting function of the committee as they can determine the structure of the board. This can create tension between the board of directors and the general meeting and the committee. The reporting to the shareholders can also have the opposite effect from what is envisaged. This will be because the shareholders, in exercising their powers as shareholders, such as voting rights, have no duty, fiduciary or otherwise, towards the company or any other stakeholder for that matter. They will therefore, possibly, only take their own interests into account, and not even that of the company. This will therefore have the effect that the interests of the company as a separate entity, as well as that of the other stakeholders, are negated. If the shareholders are inclined to act in a manner that supports e.g. CSR or other interests, it may have a positive effect, but this is, at present at least, 'soft law' established and applied through codes.50

Locke states that the committee plays a supportive role to the board in addressing stakeholder issues as the committee has to draw matters within its mandate to the attention of the board.51 As stated above, most of these matters will be within the knowledge of the board in any case and this proposed function does not add anything. In view of the above it can be argued that the committee can have a bigger and more controversial role, possibly unplanned and hopefully unintended by the legislator.

The basic principle is, however, that all the functions that fall within the ambit of the committee are actually also matters that the board should take into account in complying with its fiduciary duties towards the company. If the intention with the committee was merely to act as a conduit to the board and to sensitize the board about these matters, so that the board can properly consider the matters in conjunction with other interests, it is submitted that it would have been an important addition to the governance structure of the company. The powers of the committee, as well as the composition thereof with the minimum representation of one director, coupled with the powers of the committee to approach the shareholders, clearly indicate that it was not the intention of the legislature for the committee to merely assist the board.

2 Conclusions on the South African Social and Ethics Committee

We are of the view that provision for the social and ethics committee is, in principle, a good initiative to give effect to the interests of stakeholders. As stated before, the role of directors is to make a profit for the company. When doing this they need to have regard to the interests of various stakeholders. In the end they need to make a decision that is best for the company as a separate legal entity. By having a committee that addresses the board on issues that are relevant when making business decisions should place directors in a better position to make the best decision for the company. However, as discussed above, there are various shortcomings and uncertainties with this committee. Its terms of reference are not clear enough. There is uncertainty as to whether this is a board committee or a company committee and this have various implications, for example, with regard to the liability of the members of this committee. The tension that can be created between the board and the shareholders is also problematic based on the fact that the committee should report back to the shareholders, as explained above. We are, however, still of the view that a committee like this is preferred to a legislative pluralist approach. But then it should be drafted with more certainty and its shortcomings should be addressed.

Joubert states that listed companies have already showed an awareness of social and sustainability issues in their public reporting.52Empirical research is obviously not available on how effective this committee is, but when considering the top 10 listed companies on the JSE it is clear that all of these companies have a social and ethics committee, as required by the Act, in place.53 Procedurally it therefore seems if companies are starting to comply. Substantially, only time will tell whether this monitoring and reporting role on a wide selection of matters will actually result in better corporate socially responsible behavior and companies that are sustainable and good corporate citizens. It is, however submitted, that although the aims and functions of the social and ethics committee should at least, as argued above, sensitize the board in respect of the interests and importance of other shareholders, there are a substantial number of material legal issues, as discussed above, that will impact negatively on the ultimate effect of this committee.

3 A Comparison with the Stakeholder Approach in the United Kingdom

3 1 Introduction

In 1998 the Secretary of State for Trade and Industry announced a three-year fundamental review of core company law in the United Kingdom. This review was led by an independent steering group. Their aim was to develop a simple, modern, efficient and cost-effective framework to carry out business activity in Britain for the twenty-first century.54

In the course of the review process, various consultation documents were drafted.55 A detailed discussion of the review process is not within the scope of this article. The aim is to discuss the stakeholder approach taken in the United Kingdom with the intention to compare it with the South African approach, discussed in Part 1 of this article.56 The protection of stakeholders is one of the issues that received considerable attention during the United Kingdom company law review process.57The Steering Group, 'for ease of reference', referred to two basic approaches as far as company interests and the stakeholder debate are concerned, namely the so-called enlightened shareholder value approach and the pluralist approach.58 They summarised the two different approaches as follows:

A distinction is drawn between the enlightened shareholder value approach, which asserts that [productive relationships] can be achieved within present principles, but ensuring that directors pursue shareholders' interests in an enlightened and inclusive way, and the 'pluralistic' approach, which asserts that co-operative and productive relationships will only be optimised where directors are permitted (or required) to balance shareholders' interests with those of others committed to the company.59

The Steering Group seems to strongly favour the so-called enlightened shareholder value approach.60

The Companies Act of 2006 provides for a comprehensive code of directors' duties and sections 171-177 set out their general duties. The scope of the general duties is listed in section 170 which states that the duties specified in sections 171-177 are owed to the company by the directors. The general duties are based on certain common law rules and equitable principles. These duties should be interpreted and applied in the same manner as common law rules and equitable principles.61Section 172 concerns the duty to promote the success of the company and is of importance for purposes of this article. These factors include that directors should have regard to the likely consequence of any decision in the long-term; the interests of the employees; the need to foster the company's business relationships with suppliers, customers and others; the impact of the company's operations on the community and the environment; the desirability of the company maintaining a reputation for high standards of business conduct; and the need to act fairly as between members of the company.

3 2 Section 172 of the Companies Act of 2006

Section 172 of the United Kingdom Companies Act of 2006 provides as follows:

172. Duty to promote the success of the company

(1) A director of a company must act in the way he considers, in good faith, would be most likely to promote the success of the company for the benefit of its members as a whole, and in doing so have regard (amongst other matters) to -

(a) the likely consequences of any decision in the long term,

(b) the interests of the company's employees,

(c) the need to foster the company's business relationships with suppliers, customers and others,

(d) the impact of the company's operations on the community and the environment,

(e) the desirability of the company maintaining a reputation for high standards of business conduct, and

(f) the need to act fairly as between members of the company.

(2) Where or to the extent that the purposes of the company consist of or include purposes other than the benefit of its members, subsection (1) has effect as if the reference to promoting the success of the company for the benefit of its members were to achieving those purposes.

(3) The duty imposed by this section has effect subject to any enactment or rule of law requiring directors, in certain circumstances, to consider or act in the interests of creditors of the company.

3 2 1 Explanation of Section 172

It is stated in the Explanatory Notes on the Act that this section enshrines in statute the enlightened shareholder value approach by stating that a director must promote the success of the company with reference to a number of important factors. With regard to subsection (1) it is explained that the list of factors is not exhaustive, but highlights areas of particular importance, which reflect wider expectations of responsible business behaviour, such as the interests of the company's employees. Directors have to determine, with the necessary care and skill, which factors are relevant at what stage of the existence of a company. Subsections (2) and (3) are explained as follows in the Explanatory Notes:

Subsection (2) addresses the question of altruistic, or partly altruistic, companies. Examples of such companies include charitable companies and community interest companies, but it is possible for any company to have 'unselfish' objectives which prevail over the 'selfish' interests of members. Where the purpose of the company is something other than the benefit of its members, the directors must act in the way they consider, in good faith, would be most likely to achieve that purpose. It is a matter for the good faith judgment of the director as to what those purposes are, and, where the company is partially for the benefit of its members and partly for other purposes, the extent to which those other purposes apply in place of the benefit of the members. Subsection (3) recognises that the duty to promote the success of the company is displaced when the company is insolvent. Section 214 of the Insolvency Act 1986 provides a mechanism under which the liquidator can require the directors to contribute towards the funds available to creditors in an insolvent winding up, where they ought to have recognised that the company had no reasonable prospect of avoiding insolvent liquidation and then failed to take all reasonable steps to minimise the loss to creditors. It has been suggested that the duty to promote the success of the company may also be modified by an obligation to have regard to the interests of creditors as the company nears insolvency. Subsection (3) will leave the law to develop in this area.62

3 2 2 Shareholder Primacy Retained

In terms of this duty embedded in section 172, directors are primarily expected to act in good faith to promote the success of the company for the benefit of its members as a whole.63 In other words, shareholder primacy has been retained. However, the directors may also have regard to other matters, including and primarily those listed in section 172(1)(a)-(f). As was mentioned above, this list is not exhaustive.64 The list provided in section 172(1) is probably the most comprehensive list of factors that directors should consider when managing a company contained in any modern company legislation. It is also, probably, the clearest recognition in modern company legislation of the importance of interests apart from the interests of shareholders, namely those of other stakeholders such as employees, suppliers, customers and others.

3 2 3 The Practical Application of Section 172

The practical application of this section is, however, unclear. This uncertainty can be explained as follows: firstly, directors are provided with an unfettered (or unlimited) discretion in terms of this provision. They should manage a company in a way they consider would promote the success of the company, for the benefit of its members. But there are no objective criteria indicating how they should exercise this important discretion. According to the Ministerial Statements of June 2007, there are two ways of looking at the statutory statement of directors' duties. On the one hand, it codifies the existing common law obligations of company directors. On the other hand, it marks a radical departure in 'articulating the connection between what is good for a company and what is good for society at large'.65

Secondly, it is stated that the new statutory statement of directors' duties captures a cultural change in the way in which companies conduct their business. The Act is based on a new approach to pursue the interests of shareholders and considering the interests of stakeholders. These approaches are complementary approaches and not contradicting ones. It is stated in a 'Corporate Update' by Ashurst 66 that section 172(1) will at least have the effect of making directors think harder about their duties.

Thirdly, the list of issues directors need to have regard to is also not exhaustive. It is specifically stated that directors need to consider these issues 'amongst other matters'. There is no indication of what these 'other matters' entail. Fourthly, there is no definition concerning 'the success of the company'.67

Fifthly, none of the stakeholders other than shareholders will have standing to compel directors to take their interests into consideration, unless it can be established that the interest of the company itself was contravened. This will have to be done by way of a shareholder derivative action (in terms of the derivative action in sections 260-264 of the United Kingdom Companies Act of 2006).68

The extent of the protection afforded in section 172(1) is therefore uncertain. It would seem that the only practical consequence of recognising these other interests in the legislation is that the actions of directors would not be open for any challenge if they have not only taken the interests of the company as a whole (defined as the collective interest of the current and future shareholders) into consideration in making decisions, but also other interests. Under the common law, other interests, such as employees' interests, were considered to be pertinent only when they coincided with the company's best interests.69

3 2 4 Conclusions on Section 172

The drafters can be commended for clearly stating which approach they prefer regarding the stakeholder debate. The Act seems to provide a theoretical answer to the stakeholder debate, but its practical application is far from clear. It may well be that over time guidelines on its practical application may be provided.70 The Strategic Report is another method of ensuring that directors comply with their duties. During 2013 regulations were issued relating to the Strategic Report and Directors' Report. Section 414A of the Companies Act now requires all companies that are not small71 to prepare a Strategic Report. The Report must, to the extent necessary for an understanding of the development, performance or position of the company's business, include- (a) analysis using financial key performance indicators, and (b) where appropriate, analysis using other key performance indicators, including information relating to environmental matters and employee matters.72Section 415 of the Act requires all companies to prepare a directors' report.73 Section 418 deals with the contents of the Directors' Report relating to a statement as to disclosure to auditors. Both the Strategic Report and the Directors' Report are integral parts of the annual report. The purpose of the strategic report is to inform members of the company and help them to assess how the directors have performed their duty under section 172 of the Act.74

The Act clearly refers to the interests of other stakeholders and to the fact that directors should have regard to the interests of other stakeholders when promoting the success of the company for the benefit of its members.75 Thus the Act is very clear on the preferred approach to stakeholders' protection. Shareholders should still be seen as the primary beneficiaries of company's management in comparison to other stakeholders. But directors have a discretion in this regard.76 Directors should only consider the interests of these stakeholders when it would be in the interests of the shareholders collectively to do so.

The Australian and Market Advisory Committee77 stated that a non-exhaustive list of stakeholder interests provides directors with little guidance as how to balance these competing interests. They argued that in the interest of certainty it would be more beneficial if the 'best interests of the company' is interpreted to include the interests of stakeholders. Others argue that section 172 provides more clarity on the determination of what directors may consider as being the interests of stakeholders.78 They argue that the section provides directors with general and structural guidance on how to balance the interests of stakeholders.

In short the advantages of the broad nature of section 172 are that it is adaptable and flexible. The disadvantage is that it does not give meaningful indications to directors as to what these interests entail.79

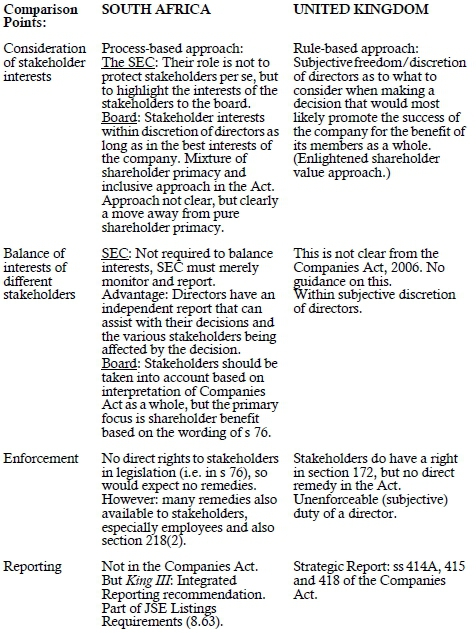

4 Conclusions

Based on the above analysis, the position in the United Kingdom and South Africa can thus be compared as follows:80

It is clear from the literature that the common law shareholder supremacy doctrine is being questioned. A movement away from that doctrine will change the roots of company law fundamentally. However, it must also be accepted that the doctrine cannot remain absolute and that its reach should be tempered but it should also be recognised that a pluralist approach would, for all intents and purposes, make managing companies by directors virtually impossible. Using 'soft law', such as codes, to at least shift the focus of the management of the company to also recognise other interests more clearly will work, but only in respect of socially responsible companies, but the enforcement thereof is problematic and lies in the hands of a secondary 'regulator' like a stock exchange, the investors in that company and the shareholders voting with their feet. There are, however, many companies that have an effect on a wide range of stakeholders, where these 'duties' cannot be enforced as above due to the fact that the shares are not listed.

The stakeholder position in the United Kingdom is still very much based on shareholder primacy. The interests of stakeholders will really only be attended to if it coincides with those of the shareholders collectively and is, it is submitted, an imperfect system and solution as it does not change the common law, but merely affirms it.

South Africa's legislative approach to the protection of stakeholders is not clear but a move away from shareholder primacy can, however, not be denied. A committee such as the social and ethics committee is therefore in line with this approach and, in principle, a welcome move. The social and ethics committee therefore seems to be an attempt to ensure that the interests of other stakeholders are directly recognised by the company and by the board, but in a manner that shies away from the amendment of the relevant common law rules which influences its efficacy. It will, however, only be successful and be able to protect the interests of stakeholders (in line with an inclusive approach) if the material legal deficiencies, uncertainties and shortcomings, discussed above, are addressed. Failure to do so will have the effect that the impact of the social and ethics committee will not only be negated, but that it will also cause tensions in the management of a company, and between different stakeholders, that can paralyse the company. We are nevertheless of the view that a structure like the social and ethics committee is perhaps the more sensible process to protect stakeholder interests and to assist directors to consider these interests when they make business decisions, but then the terms of reference and the duties and functions of this committee should be drafted in much clearer terms. The matters that fall within the mandate of the committee are most probably issues that the board would consider in any event, but to have a committee reporting back to the board and not just the board merely 'going through the list' is arguably a better way to make sure that all interests are adequately addressed. A properly constituted social and ethics committee and the proper functioning of such a committee will also indicate the possible pitfalls and dangers if and when a legislative move towards a pluralist approach is contemplated or deemed necessary.

* Continued from 2017 De Jure 17(1).

1 In terms of section 223 and Item 14 of Schedule 5 of the 2008 Companies Act the Minister of Trade and Industry publishes regulations relating to the functions of the Companies and Intellectual Property Commission, the Takeover Regulation Panel and the Companies Tribunal, and other matters relating to the regulation of companies.

2 This requirement is in line with King III recommendations. Principle 1.1 of King III states that the board should provide effective leadership with an ethical foundation, which includes the responsibility to promote the stakeholder-inclusive model of corporate governance. Principle 8 of King IV concerns committees of the governing body and Recommended Practices 68-70 deal with the social and ethics committee. Paragraph 50 deals with disclosure in relation to this committee. King IV especially expands on the ethics role of this committee. It recommends that this committee should expand beyond mere compliance to contribute to the creation of value (page 29).

3 Reg 43(1). The fact that state-owned companies and public companies that are listed must, automatically, have social and ethics committees seems to imply that it is accepted that these companies comply with the criteria in s 72(4)(a)-(c). While this may be true in respect of listed public companies, it does not follow logically in respect of state-owned companies. Section 72(4) requires expressly that the three criteria (or one of them) must be present and the type of company is irrelevant. To apply the section, by way of regulations, automatically to certain types of companies does not seem to comply with the powers to make those regulations as in s 72(4): See Henochsberg 277 but also De Lange 'The social and ethics committee in terms of the 2008 Companies Act: Some observations regarding the exemptions and the role of the Companies Tribunal' 2015 SA MercLJ 507-539. [ Links ]

4 Reg 43(1)(c).

5 Regulation 26(2). Certain companies are exempted, such as when the company is required in terms of other legislation to have, and does have, some form of formal mechanism within its structures that substantially performs the function that would otherwise be performed by the social and ethics committee (section 72(5)(a)) and if it is a subsidiary of another company (as defined in section 3 of the Companies Act) and if the holding company has a social and ethics committee that will perform the functions of the social and ethics committee for the (subsidiary) company (Regulation 43(2)(a)). If a company is required to appoint a social and ethics committee, it may apply to the Companies Tribunal in the prescribed manner and form for an exemption and the Tribunal can give such an exemption for five years if it is satisfied that it is not reasonably necessary in the public interest to require the company to have a social and ethics committee, having regard to the nature and extent of the activities of the company (section 72(5)(b)). This exemption is problematic as the same criteria (quantitatively) that require a company to appoint a social and ethics committee must be used to determine whether it is not necessary, in the public interest, to do so. It is suggested that the nature of the activities (i.e. a qualitative criterion) should be applied in the exercise of the discretion by the Tribunal, as the quantitative criteria are fixed by the public interest formula: See Henochsberg 278.

6 As defined in ss 1, 66(1) and Regulation 38.

7 See Reg 43(4).

8 See Henochsberg 276.

9 Henochsberg 276; Regulation 43(5)(b).

10 See s 94(7) (i) of the 2008 Companies Act.

11 Joubert 190, footnote 33, or at best a 'hybrid' committee. See also Locke 109, footnote 371 where she argues that Regulations 43(2) and 43(3) must be read together to mean that the board has the power to appoint members of the social and ethics committee and Cassim (man ed) Contemporary Company Law 417. This view is shared by Wixley and Everingham Corporate Governance (2015) 79.

12 See section 76 on the partial codification of directors' duties. This section is equally applicable to prescribed officers or members of board committees: s 76(1) (a) and (b).

13 See Henochsberg 276 on the arguments in favour of the social and ethics committee being a company committee and not a board committee. The audit committee is also appointed by the shareholders and therefore also an organ of the company. See s 94 and Henochsberg 277, 356 and on board meetings see s 73 and Henochsberg 280. See Cilliers et al Cilliers and Benade Corporate law (2000) 83 for the significance of the distinction between organs and agents.

14 Hereafter the MOI.

15 See s 66(1).

16 See s 66(1). See Henochsberg 250(1) for a detailed discussion of s 66. It is uncertain to what an extent management functions can be excluded in the MOI or transferred to the shareholders to perform. See s 15(1) that provides that the provisions in the MOI must be in line with the Act; otherwise it would be void in so far as it is inconsistent. Also the directors owe the fiduciary duties to the company, and it will not make sense to give the shareholders the majority or all of the managerial powers because the directors can transfer their powers to the shareholders, or anybody else for that matter, but not their duties. It is also unclear how the shareholders will give effect to the full managerial function, as they will not have access to all the company records and accounts. See the discussion in Henochsberg 250(4).

17 See s 75, as one example, where the ultimate power is with the shareholders.

18 Henochsberg 250(5); Delport 'The division of powers in a company' in: Visser and Pretorius (eds) Essays in Honour of Frans Malan (2014) 81-92 91. [ Links ]

19 This is different from the position in the United Kingdom, which is more in line with the position of the 1973 Companies Act. See Cilliers et al 88.

20 Welling Corporate Law in Canada: The Governing Principles (2006) 315.

21 Henochsberg 332.

22 See e.g. s 78.

23 Monitoring a company's standing in respect of the codes and legislation expressly listed is, however, not enough. Full compliance will only be attained if the company's standing is monitored with reference to all relevant codes and legislation. Joubert 189. See also Stoop 2013 Stellenbosch Law Review 562-582 and Havenga 'The social and ethics committee in South African Company law' 2015 Journal of Contemporary Roman Dutch Law 285-292 in respect of the functions of the social and ethics committee. [ Links ]

24 Act 55 of 1998.

25 Act 53 of 2003.

26 For a detailed discussion on 'labour' and the Protocol in this context see Locke 111-112.

27 Section 72(8)(e). This may be an additional indication that the committee is a company committee rather than a board committee, because if it's the latter, reporting should be only to the board.

28 See Locke 109 -118 for a detailed discussion of the function and duties of the committee with reference to the aspects mentioned in the Regulations.

29 See Kloppers 166, 1 87 and Joubert 1 88.

30 Kloppers 166, 188.

31 Section 72(9)

32 Section 72(8).

33 Kloppers 2013 PER 166 187.

34 Kloppers 180 argues that it is not unusual to include matters like these under 'social and ethics', but then clear guidance is needed of what exactly is required from the committee. This is not the case.

35 Kloppers 183.

36 Joubert 188.

37 Regulation 43(5)(a)(i).

38 Kloppers 172.

39 Kloppers 172 and footnote 22.

40 Act 53 of 2003.

41 Kloppers 178.

42 Regulation 43(5)(a)(iii).

43 Henochsberg 276.

44 See Henochsberg 276 and Cilliers et al Cilliers and Benade Corporate law (2000) 83.

45 See discussion under para 4.1 supra.

46 Joubert 194, footnote 55.

47 A cursory study of arbitrarily chosen companies such as Steinhoff International Ltd and Sanlam Ltd and the reports by the chairmen of these companies in the annual reports, show that there is no consistent application in respect of the social and ethics committee.

48 Section 66.

49 Henochsberg 279.

50 It is beyond the scope of this article to give an exposition of these codes and the effect thereof. See in respect of institutional investors the Code for Responsible Investment in South Africa and a discussion thereof in Esser and Delport 2016 Journal of Contemporary Roman Dutch Law 27-28.

51 As per Regulation 43(5)(b). See Locke 110.

52 According to a KPMG study the percentage of the hundred largest companies listed on the JSE reporting on corporate responsibility increased from 18% in 2005 to 97% in 2011. See Joubert 183, footnote 1. See https://www.kpmg.com/PT/pt/IssuesAndInsights/Documents/corporate-responsibility2011.pdf for the study (accessed 2017-11-07).

53 For the Top 40 listed companies see https://www.jse.co.za/current-companies/companies-and-financial-instruments.

54 See Attenborough 'The Company Law Reform Bill: an analysis of directors' duties and the objective of the company' 2006 Company Lawyer 162-169 where he discusses the company law reform of the United Kingdom as undertaken by the Steering Group. For a discussion of the company law review in the UK, see: Rickford 'A history of the company law review' in De Lacy (ed) The Reform of United Kingdom Company Law (2002) 3-37,10.

55 The Strategic Framework; Developing the Framework; Completing the Structure; the Final Report and the White Paper of 2005. See also Modern Company Law for a Competitive Economy: Reforming the Law concerning Overseas Companies (October 1999); Company Formation and Capital Maintenance (October 1999); Company General Meetings and Shareholder Communication (October 1999); Capital Maintenance Other Issues (June 2000); Registration of Company Charges (October 2000); Trading Disclosures (October 2000).

56 See De Jure 17(1). See Lombard and Joubert 'The legislative response to the shareholders v stakeholders debate: a comparative overview' 2014 Journal of Corporate Law Studies 211-240, 211 for a discussion of different models, legislative and otherwise, in various jurisdictions.

57 The interests of the employees as stakeholders have received legislative attention by the Labour government as early as 1980, when the Companies Act of 1980 in s 46 provided that the directors shall have regard to the interests of employees, but that such employees will not be able to enforce those duties directly. See Gower, Prentice and Pettet Gower's Principles of Modern Company Law (1992) 73. This movement was also attempted in South Africa, albeit it with a somewhat different modus operandi, but with the same lack of success. See Botha Employee Participation and Voice in Companies: A Legal Perspective (LLD Thesis 2015 North-West University) for a detail discussion of the development in South Africa.

58 See the Strategic Framework p 37, par 5.1.11. It has been stated that the enlightened shareholder value approach has a strong emphasis on shareholder primacy and the pluralist approach on the protection of stakeholders.

59 The Strategic Framework p iv, par 5.

60 The Strategic Framework p 39, par 39; p 42, par 5.1.23; pp 43, par 5.1.25 ff.

61 Section 170(4).

62 See pars 325-322 of the Explanatory Notes on the Act. The Steering Group was against the inclusion of creditors as beneficiaries of directors' duties.

63 See Esser and Du Plessis 'The stakeholder debate and directors' fiduciary duties' 2007 SA MercLJ 346, 353 and Richardson 'The Companies Act 2006, directors' duties and the onset of insolvency' 2007 Insolvency Law & Practice 138. See further Wesley-Key 'Companies Act 2006: are cracks showing in the glass ceiling' 2007 International Company and Commercial Law Review 422-429 arguing that s 172(1) does not provide stakeholders with sufficient protection. The duty to consider the interests of stakeholders is still subjective. Miles 'Company stakeholders' 2003 The Company Lawyer 56-59 also argues that it is within the discretion of the directors whether to consider other stakeholders or not. See also Attenborough 'Recent developments in Australian corporate law and their implications for directors' duties: lessons to be learned from the UK perspective' 2007 International Company and Commercial Law Review 312 317 stating that s 172(1) does not appear to represent a great movement away from shareholder value. Section 172(1) places merely a general obligation on directors to consider the interests of other stakeholders. Shareholders are still the primary beneficiaries of directors' duties. See further on s 172: Cerioni 'The success of the company in s. 172(1) of the UK Companies Act 2006: towards an 'enlightened directors' primacy?'' 2008 OLR 1 17; Fisher 2009 ICCLR 12; Keay 'Moving towards stakeholderism? Enlightened shareholder value, constituency statutes and more: much ado about little?' 2011 EBLR 1, 33-36; Lynch 'Section 172: A ground-breaking reform of director's duties, or the emperor's new clothes?' 2012 CoLaw 196 201.

64 See Nakajima 'Whither 'enlightened shareholder value'?' 2007 The Company Lawyer 353-354 stating that the statement of directors' duties is not an exhaustive list.

65 See the introduction to the Ministerial Statements of June 2007 available at http://uk.practicallaw.com/4-369-5991?q=&qp=&qo=&qe= (accessed 2017-11-07).

66 See the 'Corporate update' of Ashurst of November 2006 on the Companies Act of 2006.

67 Keay 'Section 172(1) of the Companies Act 2006: an interpretation and assessment' 2007 The Company Lawyer 106 109.

68 In England and Wales referred to as 'derivative claims' (s 260 CA 2006ff) and in Scotland as 'derivative proceedings' (s 265 CA 2006ff). This was one of the dilemmas employees faced under s 309 of the United Kingdom Companies Act of 1985. See Du Plessis & Dine 'The fate of the draft fifth directive on company law: accommodation instead of harmonisation' 1997 Journal of Business Law 23, 46; Roach 'The paradox of the traditional justifications for exclusive shareholder governance protection: expanding the pluralist approach' 2001 The Company Lawyer 12, 15. It has been said that one effect of s 309 was to dilute directors' accountability to shareholders rather than to strengthen their accountability to employees. Section 260 sets out the key aspects of a derivative claim. There are three elements to a derivative action: (1) the action must be brought by a member of the company; (2) the cause of action is vested in the company; and (3) relief is sought on the company's behalf. Section 260(3) provides that a derivative claim 'may be brought only in respect of a cause of action arising from an actual or proposed act or omission involving negligence, default, breach of duty or breach of trust by a director of the company'.

69 Hampson v Price's Patent Candle Co (1876) 45 LJ Ch 437; Hutton v West Cork Railway Co (1883) 23 Ch D 654.

70 Section 172(1) CA 2006 has thus far mainly been mentioned in the context of the application for permission to bring judicial review proceedings and shareholder's remedies, e.g. unfair prejudice petitions (s 994) and derivative (shareholder) actions on behalf of the company. See for a detailed discussion on case law referring to s 172: Chataczkiewicz-tadna The Relevance of Long-term Interests in the Decision-Making Processes of Company Directors in the UK, Delaware and Germany: a Critical Evaluation (PhD Thesis 2016 University of Edinburgh) para 4. [ Links ]2. E.g. Lesini v Westrip Holdings [2010] BCC 420 421 where the court held that in most cases courts will not challenge directors' subjective judgments.

71 A company is entitled to small companies exemption in relation to the strategic report for a financial year if - (a) it is entitled to prepare accounts for the year in accordance with the small companies regime, or (b) it would be so entitled but for being or having been a member of an ineligible group. See s 414B of the Companies Act, 2006.

72 Section 414C (4).

73 Section 416 deals with the general contents of the Report.

74 Section 414C (4).

75 Section 172(1) of the Companies Act of 2006.

76 Richmond Pharmacology Ltd v Chester Overseas Ltd [2014] EWHC 2692 (Ch) para 66-68 (Stephen Jourdan QC) confirms that the test in s 172 is a subjective one. See also Re Southern Countries Fresh Foods Ltd [2008] EWHC 2810 (Ch) para 53 (Mr Justice Warren) confirming that it is a task for the directors, and not for the court, to decide what constitutes the best interest of the company. The case also stresses the subjectivity of the duty to promote the success of the company.

77 CAMAC Report on Social Responsibility of Corporations (2006) available at http://www.asx.com.au/resources/newsletters/listed_at_asx/20070221_camac_ repor t_the_social_responsibility_of_corporati.htm (assessed on 2016-11-01).

78 Horrigan CSR in the 21st Century (2010) 232ff.

79 Wilkinson Will Social and Ethics Committees Enlighten Shareholders? A Comparison of the South African provisions relating to Social and Ethics Committees with the Enlightened Shareholder Value Approach in the United Kingdom Companies Act 2006 (LLM Dissertation 2011 University of Johannesburg) at 67.

80 The headings used for this comparison are based, but adapted, on those used by Wilkinson.