Servicios Personalizados

Articulo

Inglés (pdf)

Inglés (pdf)

Articulo en XML

Articulo en XML Referencias del artículo

Referencias del artículo

Indicadores

Links relacionados

-

Citado por Google

Citado por Google -

Similares en Google

Similares en Google

Compartir

Permalink

PermalinkJournal of the Southern African Institute of Mining and Metallurgy

versión On-line ISSN 2411-9717

versión impresa ISSN 2225-6253

J. S. Afr. Inst. Min. Metall. vol.122 no.1 Johannesburg ene. 2022

http://dx.doi.org/10.17159/2411-9717/1556/2022

PROFESSIONAL TECHNICAL AND SCIENTIFIC PAPERS

Mine-impacted water: From waste to resource

A.N. Clay; S. Joubert; N.N. Moeketsi

EY Minvest

SYNOPSIS

For many years, mine-impacted water has been regarded as a problem and linked to long-term environmental liabilities. However, this water can be a renewable and a sustainable resource, provided that it is managed in a responsible and sensible manner.

South Africa's National Water Resource Strategy (NWRS, 2013) considers water that can be used to contribute to economic activity to be a water resource. Although all water resources are considered as belonging to the State, government does not appear to have meaningfully explored the use of mineimpacted water to contribute to the country's economic activity.

Africa is blessed with more sunshine than anywhere else, apart from Australia, yet we see no rollout of vast quantities of solar panels to ensure every African family has access to affordable power. This suggests that governments are incapable of managing such a free resource. At the same time, apart from the equatorial areas, water is a seriously constrained resource and yet we expect the same entities to manage a commodity none of us can live without.

This paper explores the conversion of mine-impacted water from waste to a resource and how the inclusion of other stakeholders (such as water users, landowners, and ordinary South Africans) could benefit the process.

Keywords: mine-impacted water, water balance, water resources.

Introduction

Mining activities have been accompanied by a legacy of environmental issues resulting from the discharge of mine-impacted water from old mine operations. For many years, this mine-impacted water has been regarded as a residual problem and linked to long term environmental liabilities. Reclamation activities are governed by widespread national and international regulatory structures. In this regard, assuring compliance with national legislation and related regulations and following best practice international guidelines on mine closure and rehabilitation is vital.

Waste water and its treatment account for the biggest portion of the closure and rehabilitation liability of a mine. The National Environmental Management Act No. 107 of 1998 (NEMA) requires that this liability, including the responsibility for extraneous or polluted water, continues after closure. The inclusion of this requirement, setting out how to calculate the financial provision, is a clear indication that the quantum of the provision will necessarily increase over time. As a consequence, this will reflect as a significant liability on the balance sheet.

Mining as a polluter

The historical management of mine rehabilitation in South Africa by the main mining companies has been perfunctory to say the least, hence the current situation of many abandoned sites. The mining industry has developed a bad reputation in this regard, with few examples of successfully rehabilitated sites. The creation of 'rehabilitation trust funds' was a concept and practical approach to ensuring companies contributed to the financial provisioning of the closure costs and was incorporated into Section 37A of the Income Tax Act No. 62 of 1968 (the ITA). This meant that contributions to the fund should be provided evenly by taking the terminal liability and dividing it by the life of mine.

During times when metal prices were high and companies were generating profits, the preferred option was to contribute more, and when profits were low, to decrease contributions. This was counterintuitive, since during times of high prices the pay limits should go down and the life of mine would increase, meaning that the denominator increased and so contributions should also decrease. In some instances, companies would make provisions which were not 'cash', and so when a mining company was no longer profitable the provision disappeared as well. The accounting process also posed challenges in that, in a high inflationary economic climate, the rehabilitation liabilities were escalated at inflation and then discounted at the company's cost of capital, which was generally more than the inflation rate. The resulting present value of the liability was less than the original estimate.

The government has since stepped in to ensure that this situation doesn't persist, but the intervention is clearly too late. Consequently, it is nigh impossible for any mining company to obtain a closure certificate. The obvious result is that mine owners will simply go into insolvency and then we are back to square one. It should be remembered that during the process of State capture and takeover of Optimum Coal Mine the then Minister of Mineral Resources, Mosebenzi Zwane, authorized the transfer of the R1.4 billion rehabilitation trust fund (all trust funds need ministerial permission for expenditure) to an offshore Gupta-based business, never to be seen again.

The identification and quantification of rehabilitation liabilities is a fairly reliable process, and most companies take this matter seriously as part of their commitments to environmental, social, and corporate governance (ESG). These amounts are embedded in the financial statements under IAS 37 (Provisions, Contingent Liabilities and Contingent Assets) and scrutinized by activist bodies.

There is a conundrum facing stakeholders - how to make sure the rehabilitation or decommissioning costs are clearly identified and defined as a 'liability' while at the same time creating a financing process to concert the supposed 'liability' into an 'asset' in an orderly and responsible manner. So, where does water fit into the problem? In general, water inflows and outflows can be readily identified for a mine in the water balance, which is crucial during operations in order to ensure the mine is dewatered and has enough pumping capacity to meet routine and exceptional circumstances such as a flood. Once mining operations have ceased, the mine is usually sealed up and the water in the workings left to decant via natural watercourses or aquifers flow.

That issue should be nothing more than restoring the situation to the pre-mining position, except that the mine void, which is now a new 'reservoir', connects to the natural aquifers. The water is often polluted as a result of exposure to minerals such as pyrite and other sulphides that generate acidic solutions with iron as a major pollutant. This is commonly called 'acid mine drainage' (AMD) (Simate and Ndlovu 2014).

An example of AMD is the decanting of polluted water from the coal mines in the Witbank coalfield and surroundings into the Crocodile River ecosystem, creating significant downstream problems. One could say that this was inevitable, but the question is what can be done about it now?

Legalities and regulatory issues

Closure and remediation activities are governed by widespread legislative structures in various countries. Inclusive within the framework are international treaties and protocols, national acts, regulations, standards, and guidelines that address the management and financial accounting requirements. These requirements inform the input parameters that influence the Asset Retirement Obligation (ARO) as recognized in the International Accounting Standard (IAS) 37. The consideration of all aspects that have the potential to influence the ARO quantum is essential in understanding current ARO requirements, engineering solutions, and remediation liability.

In the South African context, the promulgation of the new Financial Provision Regulations (GNR1147) on 20 November 2015 in terms of NEMA resulted in a significant shift from Regulations 53 and 54 of the Mineral and Petroleum Resources Development Act No. 28 of 2002 (MPRDA). The purpose was to regulate the creation of financial provisions as contemplated in the Act for the costs associated with management, rehabilitation, and remediation of environmental impacts from prospecting, exploration, mining, or mineral production. Regulation 6 of GNR1147 requires that 'An applicant must determine the financial provision through a detailed itemisation of all activities and costs, calculated based on the actual costs of implementation of the measures required for:

> Annual rehabilitation, as reflected in the annual rehabilitation plan

> Final rehabilitation, decommissioning and closure of the prospecting, exploration, mining or production operations at the end of the life of operations, as reflected in a final rehabilitation, decommissioning and mine closure plan and

> Remediation of latent or residual environmental impacts which may become known in the future, including the pumping and treatment of polluted or extraneous water, as reflected in an environmental risk assessment report.'

The current legislative requirements revolve around providing for water-related liabilities during operations and post closure, and no allowance is made for converting waste water into a resource that can ultimately be regarded as an asset. We believe that water can be a renewable and sustainable resource provided that it is managed in a responsible and sensible manner. If it isn't, it is likely that water scarcity will lead to next round of global conflict if government is not on board. In recent years, many countries have been experiencing serious drought and water shortages, a good case in point being Cape Town in South Africa.

The authors have identified a specific need to classify water beyond the limits of that which would be required for national strategic planning. In this regard, the commercial imperative is to link the human right of access to water to the efficient utilization of various water resources. To this end, the very principle and philosophy of ownership is at the heart of the classification system, which in itself is intimately related to the cost of producing various types of water and the price at which it can be sold.

Many approaches have been taken to planning water management, primarily driven by government agencies. However, in many ways this is similar to other national planning issues including road, rail, health, retirement planning, farming, and air pollution. As a result, the governmental process is invariably in conflict with the realities of commerce, since the concept that 'nothing is for free' is an increasing global human population problem.

Tranformation from liability to asset

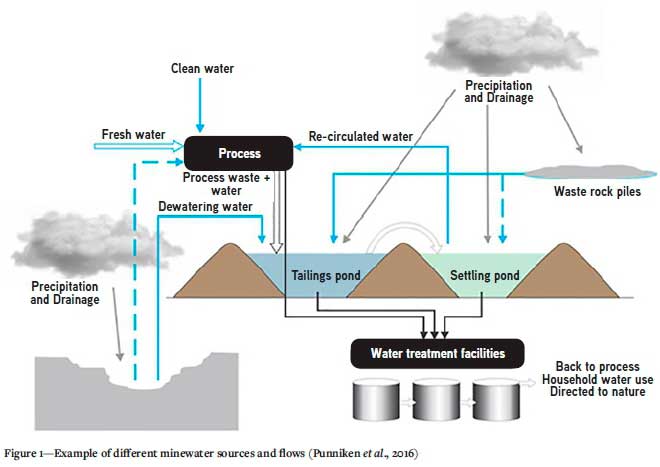

The purpose of this paper is to outline a simple solution to the problem of mine-impacted water and the management of the long-term effects, technically and financially. To begin with, all mines must have a 'water balance' that accurately identifies and quantifies the inflows and outflows of water and a pumping capacity that maintains the appropriate water level for operating the mine.

An example of a water balance is shown in Figure 1. In general, a qualified person should be responsible for preparing this and a geohydrologist should be involved. At the centre of the process is the ability to create a stochastic link between the aquifers, which are generally recharged from rainfall, and the climatic conditions as well as the open volumes constituting the underground workings or open pits. Essentially the mine void is the 'reservoir".

It is the latter which forms the basis of the definition of an asset. The mine void has been created by the mining company, and is therefore an asset of the mine, but where do you ever see it booked as an asset? The nearest you may get is the accounting treatment of 'deferred stripping', whereby the cost of creating the pit is capitalized onto the balance sheet as an asset and then written off as the mine extracts ore (mineable reserves) in the production plan on an annual basis. When the void is exhausted it is seldom possible to completely backfill it, and so another 'reservoir' has been created as an asset.

The fact that the pit or underground workings can fill with water becomes a sustainability opportunity. It is quite ironic that the historical view is that a mine is a wasting asset, and once the mineral resources have been depleted there is nothing left of value. The approach suggested here challenges this philosophy, especially when the water balance demonstrates that a reliable, sustainable water volume is available for exploitation.

Estimating volumes

The water balance allows water volumes to be accurately quantified as inflows and outflows. This can be cross-referenced to the survey estimates of the volume of the mine working void from mine plans and production records. These three sources of information, namely the inflows, outflows, and reservoir volume, can be reconciled to a high level of accuracy. It is normal to estimate the water volumes in megalitres per day and then to annualise this quantity.

For recharge, annual rainfall statistics can be used from weather records and in this example, we used @RISK to calculate probabilities in the same manner as in the oil and gas industry. The probability function can then be used to calculate the 10%, 50%, and 90% confidence limits for the best, mean, and least confident estimates of volumes, and a water resource declared.

In mineral resource estimation it is a fundamental principle to ensure that there are 'reasonable and realistic prospects for eventual economic extraction' as a prerequisite to signing off a resource. Therefore, understanding the pumping and water reticulation structure is crucial in the case of a water resource. This information is generally available from the mine engineer, with records of pumps, pipe network, and power within the mine infrastructure.

After considering recharge, the ability to confidently define water volumes ,with a high level of confidence is relatively easy.

Financial engineering

Once the water balance and the volumes have been estimated using probabilistic methods, the next question is how to obtain an asset value for the water. The first course of action is to seek a 'value in use' method where the sustainable volume of water can be pumped into a user network and distributed for sale, just like any other mineral. The quality of the water is a key factor governing the ability to sell the water but, in the case of polluted water, constructing a water purification plant of an appropriate nature is a simple engineering process.

For financial engineering, all that is needed is the cost of pumping, treatment, and distribution, and determination of the sales price. If these elements are incorporated into a cash flow model with escalation and taxation, the discounted cash flow method allows one to estimate the value of the project.

A key issue here is that the government regulates the mine's responsibility for the rehabilitation and closure costs, and water has generally been regarded as a legacy issue that essentially never goes away. So, in fact, with the concept of 'matching', the use of the water resource in a sustainable financial solution should at least mitigate the monetary aspect of the rehabilitation liability, let's say on a defined timescale such as ten years. If the net effect is to zero that out, then the sale price of water can be calculated.

Although not dealing with minewater, many countries licence private water utilities so that the efficient and sustainable use and distribution of water is financially sustainable.

Accounting recognition

As many of the decommissioning and closure activities of mining operations have the potential to vary on a year-on-year basis, the International Financial Reporting Standards (IFRS) require that an Asset Retirement Obligation (ARO) is recognized within the auspices of IAS 37.

The scope of IAS 37 requires that a provision be recognized if:

> A present obligation (legal or constructive) has arisen as a result of a past event (the obligating event)

> Payment is probable ('more likely than not')

> The quantum can be estimated reliably.

When determining the ARO for a mining entity, the following aspects must therefore be considered:

> Legal obligations for decommissioning and demolition

> Legal obligations for closure and post-closure

> Legal obligations for meeting environmental and social rehabilitation commitments

> Constructive obligations for decommissioning and closure (for example, company policy, lender requirements, or similar obligations).

In light of the above, we believe that the Accounting Standards can be improved such that a water resource can be recognized on the balance sheet as an asset instead of a liability.

Definitions

Aguzfers-Underground rock strata that are saturated with water that can be brought to the surface through natural springs or by pumping (Oskin, 2018).

Asset-A resource controlled by [an] entity as a result of past events and from which future economic benefits are expected to flow to the entity (International Financial Reporting Standards, 2008).

Mine Closure-A period of time when the operational stage of a mine is ending or has ended, and the final decommissioning and mine rehabilitation is being undertaken (Australian Government: Department of Industry, Tourism and Resources, 2006).

Liability-The future sacrifices of economic benefits that the entity is obliged to make to other entities as a result of past transactions or other past events, the settlement of which may result in the transfer or use of assets, provision of services or other yielding of economic benefits in the future. (International Financial Reporting Standards, 2008).

Provision-A liability of uncertain timing or amount. (International Financial Reporting Standards, 2008).

Rehabilitation-The restoration of the post-mined landscape to the intended post-mining land use (Mine Closure and Completion, 2006).

Reservoir-An enclosed area for the storage of water to be used at a later date.

Water resource-Water that can be used to contribute to economic activity, including a watercourse, surface water, estuary, and groundwater in an aquifer (NWRS, 2013).

Water balance-The regulation or rationalization of human activity to match the sustainable local water supply, rather than base, or a process of balancing water supply and demand to ensure that water use does not exceed supply (NWRS, 2013).

Conclusion

This paper is intended to serve as a transformation initiative for one of the most critical resources in Africa and the world in general. In the past, mine tailings were considered to be a pollutant and historical tailings with their associated dust and pollution issues were never viewed as an asset. However, that changed in the 1970s when commodity prices rose significantly and mining operations expanded, and with the recognition of retreatment liabilities the retreatment of tailings dams became possible, especially in South Africa.

Mining creates a number of underground water reservoirs. This paper outlines an opportunity to transform reservoir volumes, through an acceptable water balance, into an asset that can be booked onto the balance sheet.

This is a work in progress for which the concept is clear and the mechanism of defining the quantities and qualities of water is relatively simple. A water resources and reserves standard is in preparation and will be reported upon as a follow-up to this paper in the near future.

In the meantime, creating financial engineering solutions that link the water quantities as assets with the rehabilitation liabilities still remains to be completed.

References

Australian Government 2006. Mine Closure and Completion. Department of Industry, Tourism and Resources. https://www.im4dc.org/wp-content/uploads/2014/01/Mine-closure-and-completion.pdf [accessed 11 November.2020]. [ Links ]

Department of Water Affairs. 2013. National Water Resource Strategy. http://www.dwa.gov.za/documents/Other/Strategic%20Plan/NWRS2-Final-email-version.pdf. [accessed 11 November.2020]. [ Links ]

International Financial Reporting Standards. 2008. https://www.ifrs.org/issuedstandards/list-of-standards/ [accessed 11 November.2020]. [ Links ]

Responsible Jewellery Council. 2006. Leading Practice Sustainable Development Program for the Mining Industry (Australia). Mine Closure and Completion. https://www.responsiblejewellery.com/wp-content/uploads/Mine-Rehabilitation-and-Closure-RJC-Guidance-draftv1.pdf [accessed 11 November.2020]. [ Links ]

Oskin, B. 2018. Aquifers: Underground stores of freshwater. https://www.livescience.com/39625-aquifers.html [accessed 11 November.2020]. [ Links ]

Punkkinen, H., Räsänen, L., Mroueh U., Korkealaakso, J., Luoma, S., Kaipainen. Backnäs, S., Turune, K., Hentinen K., Pasanen, A., Kauppi, S., Vehviläinen, B., and Krogerus, K. 2016. Guidelines for mine water management. https://www.vttresearch.com/sites/default/files/pdf/technology/2016/T266.pdf [accessed 11 November.2020]. [ Links ]

Simate, G.S. and Ndlovu, S. 2014. Acid mine drainage: Challenges and opportunities. Journal of Environmental Chemical Engineering. doi: 10.1016/j.jece.2014.07.021 [ Links ]

Votruba, L. and Broza, V. 1989. Basic function of water reservoirs. Developments in Water Science, vol. 33. pp. 19-60. [ Links ]

Correspondence:

Correspondence:

N.N. Moekets

Email: naledi.n.moeketsi@za.ey.com

Received: 3 Mar. 2021

Revised: 23 Nov. 2021

Accepted: 1 Dec. 2021

Published: January 2022

{kind=link}