Services on Demand

Article

English (pdf)

English (pdf)

Article in xml format

Article in xml format Article references

Article references

Indicators

Related links

-

Cited by Google

Cited by Google -

Similars in Google

Similars in Google

Share

Permalink

PermalinkJournal of the Southern African Institute of Mining and Metallurgy

On-line version ISSN 2411-9717

Print version ISSN 2225-6253

J. S. Afr. Inst. Min. Metall. vol.119 n.9 Johannesburg Sep. 2019

http://dx.doi.org/10.17159/2411-9717/2019/v119n9a4

PRESIDENTIAL ADRESS

The Southern African Institute Of Mining And Metallurgy - Annual Financial Statements For The Year Ended 30 June 2019

Statement of Office Bearers' responsibilities and approval

The Office Bearers are required by the Companies Act 71 of 2008, to maintain adequate accounting records and are responsible for the content and integrity of the annual financial statements and related financial information included in this report. It is their responsibility to ensure that the annual financial statements fairly present the state of affairs of the company as at the end of the financial year and the results of its operations and cash flows for the period then ended, in conformity with the International Financial Reporting Standard for Small and Medium-sized Entities. The external auditors are engaged to express an independent opinion on the annual financial statements.

The annual financial statements are prepared in accordance with the International Financial Reporting Standard for Small and Medium-sized Entities and are based upon appropriate accounting policies consistently applied and supported by reasonable and prudent judgements and estimates.

The Office Bearers acknowledge that they are ultimately responsible for the system of internal financial control established by the company and place considerable importance on maintaining a strong control environment. To enable the directors to meet these responsibilities, the members sets standards for internal control aimed at reducing the risk of error or loss in a cost effective manner. The standards include the proper delegation of responsibilities within a clearly defined framework, effective accounting procedures and adequate segregation of duties to ensure an acceptable level of risk. These controls are monitored throughout the company and all employees are required to maintain the highest ethical standards in ensuring the company's business is conducted in a manner that in all reasonable circumstances is above reproach. The focus of risk management in the company is on identifying, assessing, managing and monitoring all known forms of risk across the company. While operating risk cannot be fully eliminated, the company endeavours to minimize it by ensuring that appropriate infrastructure, controls, systems and ethical behaviour are applied and managed within predetermined procedures and constraints.

The Office Bearers are of the opinion, based on the information and explanations given by management, that the system of internal control provides reasonable assurance that the financial records may be relied on for the preparation of the annual financial statements. However, any system of internal financial control can provide only reasonable, and not absolute, assurance against material misstatement or loss.

The Office Bearers have reviewed the company's cash flow forecast for the year to 30 June 2020 and, in the light of this review and the current financial position, they are satisfied that the company has or has access to adequate resources to continue in operational existence for the foreseeable future.

The external auditors are responsible for independently auditing and reporting on the company's annual financial statements. The annual financial statements have been examined by the company's external auditors and their report is presented on page 748-749.

The annual financial statements set out on page 750-758, which have been prepared on the going concern basis, were approved by the Office Bearers on 12 August 2019 and were signed on their behalf by:

Office Bearers' Report

The Office Bearers have pleasure in submitting their report on the annual financial statements of The Southern African Institute of Mining and Metallurgy for the year ended 30 June 2019.

1. Nature of business

The Southern African Institute of Mining and Metallurgy was incorporated in South Africa with interests in the industry. The company operates in South Africa.

There have been no material changes to the nature of the company's business from the prior year.

2. Review of financial results and activities

The annual financial statements have been prepared in accordance with International Financial Reporting Standard for Small and Medium-sized Entities and the requirements of the Companies Act 71 of 2008. The accounting policies have been applied consistently compared to the prior year.

Full details of the financial position, results of operations and cash flows of the company are set out in these annual financial statements.

3. Office Bearers

The Office Bearers in office at the date of this report are as follows:

Office Bearers

A.S. Macfarlane

M.I. Mthenjane

Z. Botha

I.J. Geldenhuys

Professor S. Ndlovu

V.G. Duke

Professor R.T. Jones

4. Events after the reporting period

The Office Bearers are not aware of any material event which occurred after the reporting date and up to the date of this report.

5. Going concern

The Office Bearers believe that the company has adequate financial resources to continue in operation for the foreseeable future and accordingly the annual financial statements have been prepared on a going concern basis. The Office Bearers have satisfied themselves that the company is in a sound financial position and that it has access to sufficient borrowing facilities to meet its foreseeable cash requirements. The Office Bearers are not aware of any new material changes that may adversely impact the company. The Office Bearers are also not aware of any material noncompliance with statutory or regulatory requirements or of any pending changes to legislation which may affect the company.

6. Auditors

Genesis Chartered Accountants will continue in office in accordance with Section 90(1) of the Companies Act 71 of 2008.

7. Secretary

The company had no Secretary during the year.

Independent Auditor's Report

To the members of The Southern African Institute of Mining and Metallurgy

Opinion

We have audited the annual financial statements of The Southern African Institute of Mining and Metallurgy (the company) set out on pages 750-756, which comprise the statement of financial position as at 30 June 2019, and the statement of comprehensive income, statement of changes in equity and statement of cash flows for the year then ended, and notes to the annual financial statements, including a summary of significant accounting policies.

In our opinion, the annual financial statements present fairly, in all material respects, the financial position of The Southern African Institute of Mining and Metallurgy as at 30 June 2019, and its financial performance and cash flows for the year then ended in accordance with International Financial Reporting Standard for Small and Medium-sized Entities and the requirements of the Companies Act 71 of 2008.

Basis for opinion

We conducted our audit in accordance with International Standards on Auditing. Our responsibilities under those standards are further described in the Auditor's Responsibilities for the Audit of the annual financial statements section of our report. We are independent of the company in accordance with the sections 290 and 291 of the Independent Regulatory Board for Auditors' Code of Professional Conduct for Registered Auditors (Revised January 2018), parts 1 and 3 of the Independent Regulatory Board for Auditors' Code of Professional Conduct for Registered Auditors (Revised November 2018) (together the IRBA Codes) and other independence requirements applicable to performing audits of annual financial statements in South Africa. We have fulfilled our other ethical responsibilities, as applicable, in accordance with the IRBA Codes and in accordance with other ethical requirements applicable to performing audits in South Africa. The IRBA Codes are consistent with the International Ethics Standards Board for Accountants' Code of Ethics for Professional Accountants and the International Ethics Standards Board for Accountants' International Code of Ethics for Professional Accountants (including International Independence Standards) respectively. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our opinion.

Office Bearers' responsibilities for the Annual Financial Statements

The Institutes' Office Bearers are responsible for the preparation and fair presentation of the annual financial statements in accordance with International Financial Reporting Standard for Small and Medium-sized Entities and the requirements of the Companies Act 71 of 2008, and for such internal control as the council members determine is necessary to enable the preparation of annual financial statements that are free from material misstatement, whether due to fraud or error.

In preparing the annual financial statements, the Office Bearers are responsible for assessing the company's ability to continue as a going concern, disclosing, as applicable, matters related to going concern and using the going concern basis of accounting unless the Office Bearers either intend to liquidate the company or to cease operations, or have no realistic alternative but to do so.

Independent Auditor's Report

Auditor's responsibilities for the audit of the Annual Financial Statements

Our objectives are to obtain reasonable assurance about whether the annual financial statements as a whole are free from material misstatement, whether due to fraud or error, and to issue an auditor's report that includes our opinion. Reasonable assurance is a high level of assurance, but is not a guarantee that an audit conducted in accordance with International Standards on Auditing will always detect a material misstatement when it exists. Misstatements can arise from fraud or error and are considered material if, individually or in the aggregate, they could reasonably be expected to influence the economic decisions of users taken on the basis of these annual financial statements.

As part of an audit in accordance with International Standards on Auditing, we exercise professional judgement and maintain professional scepticism throughout the audit. We also:

• Identify and assess the risks of material misstatement of the annual financial statements, whether due to fraud or error, design and perform audit procedures responsive to those risks, and obtain audit evidence that is sufficient and appropriate to provide a basis for our opinion. The risk of not detecting a material misstatement resulting from fraud is higher than for one resulting from error, as fraud may involve collusion, forgery, intentional omissions, misrepresentations, or the override of internal control.

• Obtain an understanding of internal control relevant to the audit in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the company's internal control.

• Evaluate the appropriateness of accounting policies used and the reasonableness of accounting estimates and related disclosures made by the Office Bearers.

• Conclude on the appropriateness of the Office Bearers' use of the going concern basis of accounting and based on the audit evidence obtained, whether a material uncertainty exists related to events or conditions that may cast significant doubt on the company's ability to continue as a going concern. If we conclude that a material uncertainty exists, we are required to draw attention in our auditor's report to the related disclosures in the annual financial statements or, if such disclosures are inadequate, to modify our opinion. Our conclusions are based on the audit evidence obtained up to the date of our auditor's report. However, future events or conditions may cause the company to cease to continue as a going concern.

• Evaluate the overall presentation, structure and content of the annual financial statements, including the disclosures, and whether the annual financial statements represent the underlying transactions and events in a manner that achieves fair presentation.

We communicate with the Office Bearers regarding, among other matters, the planned scope and timing of the audit and significant audit findings, including any significant deficiencies in internal control that we identify during our audit.

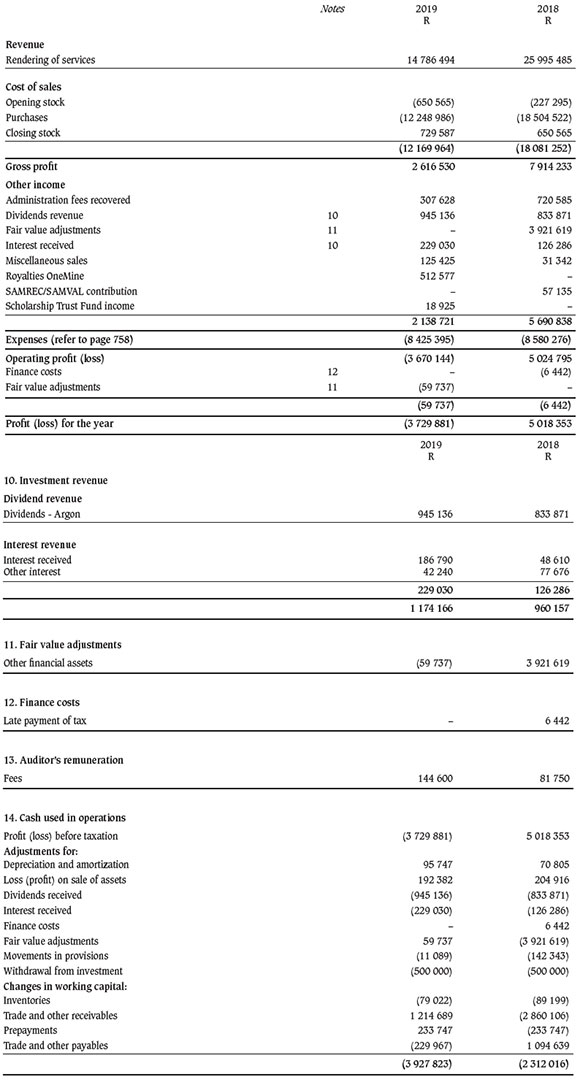

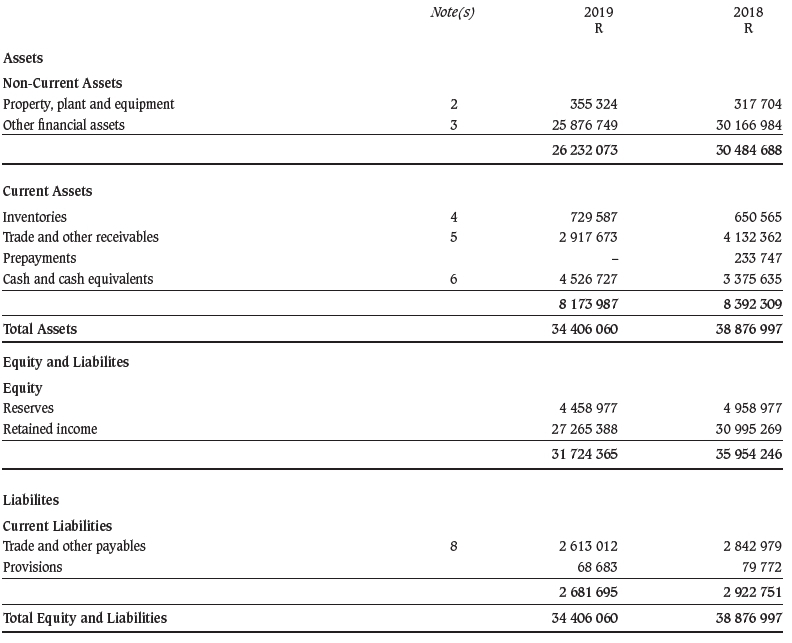

Statement of Financial Position as at 30 June 2019

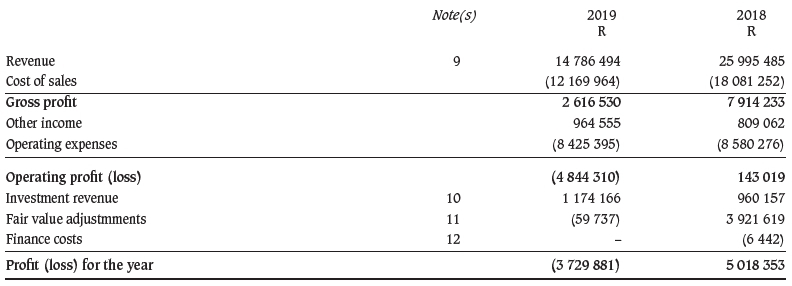

Statement of Comprehensive Income

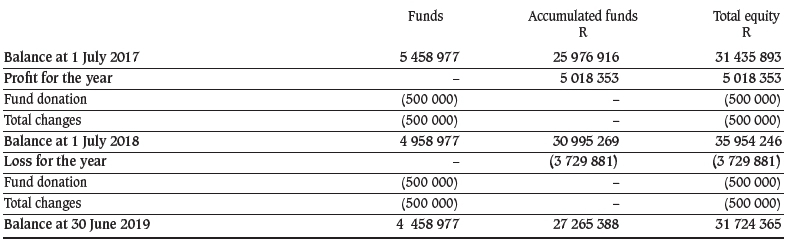

Statement of Changes in Equity

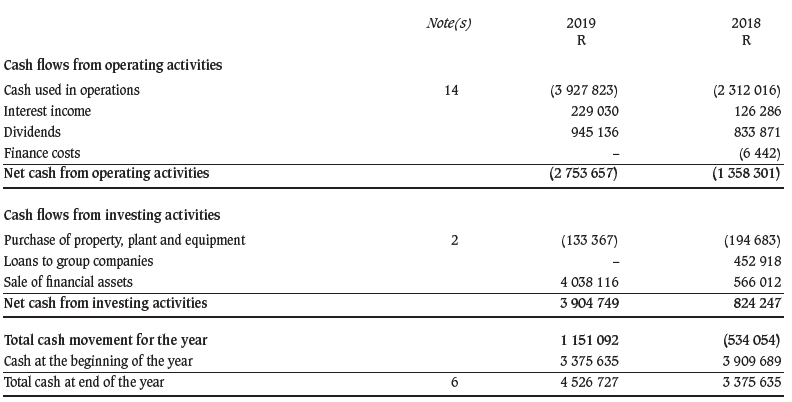

Statement of Cash Flows

Accounting Policies

1. Basis of preparation and summary of significant accounting policies

The annual financial statements have been prepared on a going concern basis in accordance with International Financial Reporting Standard for Small and Medium-sized Entities, and the Companies Act 71 of 2008. The annual financial statements have been prepared on the historical cost basis, and incorporate the principal accounting policies set out below. They are presented in South African rands.

These accounting policies are consistent with the previous period.

1.1 Significant judgements and sources of estimation uncertainty

Critical judgements in applying accounting policies

Management did not make critical judgements in the application of accounting policies, apart from those involving estimations, which would significantly affect the annual financial statements.

Key sources of estimation uncertainty

The financial statements do not include assets or liabilities whose carrying amounts were determined based on estimations for which there is a significant risk of material adjustments in the following financial year as a result of the key estimation assumptions.

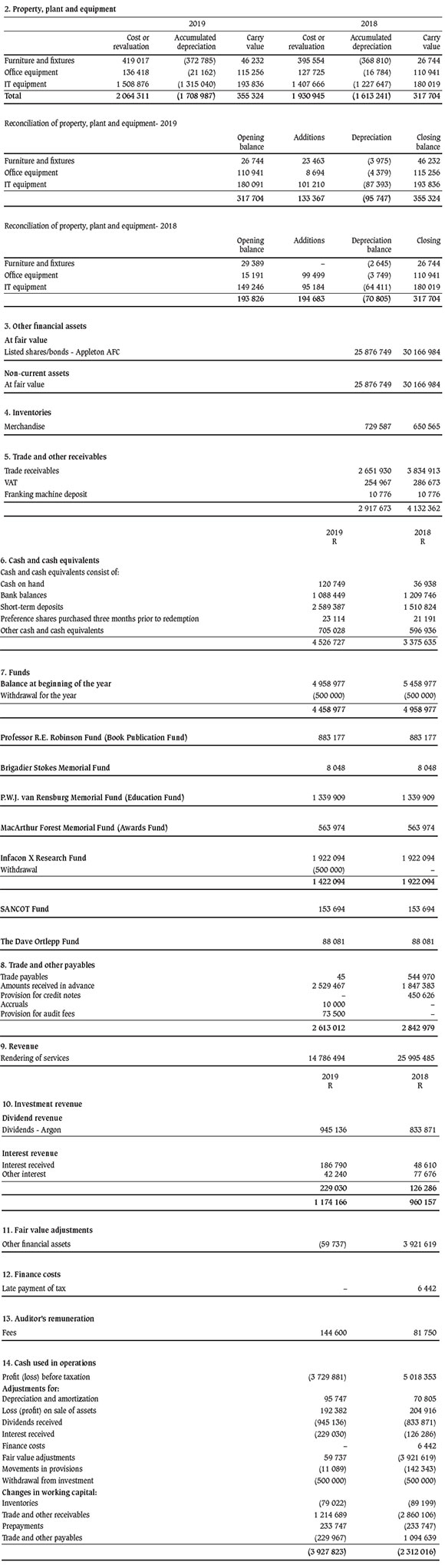

1.2 Property, plant and equipment

Property, plant and equipment are tangible assets which the company holds for its own use or for rental to others and which are expected to be used for more than one period.

Property, plant and equipment is initially measured at cost.

Cost includes costs incurred initially to acquire or construct an item of property, plant and equipment and costs incurred subsequently to add to, replace part of, or service it. If a replacement cost is recognized in the carrying amount of an item of property, plant and equipment, the carrying amount of the replaced part is derecognized.

Expenditure incurred subsequently for major services, additions to or replacements of parts of property, plant and equipment are capitalized if it is probable that future economic benefits associated with the expenditure will flow to the company and the cost can be measured reliably. Day-to-day servicing costs are included in profit or loss in the period in which they are incurred.

Property, plant and equipment is subsequently stated at cost less accumulated depreciation and any accumulated impairment losses, except for land which is stated at cost less any accumulated impairment losses.

Depreciation of an asset commences when the asset is available for use as intended by management. Depreciation is charged to write off the asset's carrying amount over its estimated useful life to its estimated residual value, using a method that best reflects the pattern in which the asset's economic benefits are consumed by the entity.

The useful lives of items of property, plant and equipment have been assessed as follows:

The depreciation charge for each period is recognized in profit or loss unless it is included in the carrying amount of another asset.

Impairment tests are performed on property, plant and equipment when there is an indicator that they may be impaired. When the carrying amount of an item of property, plant and equipment is assessed to be higher than the estimated recoverable amount, an impairment loss is recognized immediately in profit or loss to bring the carrying amount in line with the recoverable amount.

Accounting Policies

1.3 Financial instruments

Initial measurement

Financial instruments are initially measured at the transaction price (including transaction costs except in the initial measurement of financial assets and liabilities that are measured at fair value through profit or loss) unless the arrangement constitutes, in effect, a financing transaction in which case it is measured at the present value of the future payments discounted at a market rate of interest for a similar debt instrument.

Financial instruments at amortized cost

These include loans, trade receivables and trade payables. Those debt instruments which meet the criteria in section 11.8(b) of the standard, are subsequently measured at amortized cost using the effective interest method. Debt instruments which are classified as current assets or current liabilities are measured at the undiscounted amount of the cash expected to be received or paid, unless the arrangement effectively constitutes a financing transaction.

At each reporting date, the carrying amounts of assets held in this category are reviewed to determine whether there is any objective evidence of impairment. If there is objective evidence, the recoverable amount is estimated and compared with the carrying amount. If the estimated recoverable amount is lower, the carrying amount is reduced to its estimated recoverable amount, and an impairment loss is recognized immediately in profit or loss.

Financial instruments at cost

Commitments to receive a loan are measured at cost less impairment.

Equity instruments that are not publicly traded and whose fair value cannot otherwise be measured reliably without undue cost or effort are measured at cost less impairment.

Financial instruments at fair value

All other financial instruments, including equity instruments that are publicly traded or whose fair value can otherwise be measured reliably, without undue cost or effort, are measured at fair value through profit and loss.

If a reliable measure of fair value is no longer available without undue cost or effort, then the fair value at the last date that such a reliable measure was available is treated as the cost of the instrument. The instrument is then measured at cost less impairment until management are able to measure fair value without undue cost or effort.

1.4 Inventories

Inventories are measured at the lower of cost and estimated selling price less costs to complete and sell, on the weighted average cost basis.

1.5 Impairment of assets

The company assesses at each reporting date whether there is any indication that property, plant and equipment or intangible assets or goodwill may be impaired.

If there is any such indication, the recoverable amount of any affected asset (or group of related assets) is estimated and compared with its carrying amount. If the estimated recoverable amount is lower, the carrying amount is reduced to its estimated recoverable amount, and an impairment loss is recognized immmediately in profit or loss.

1.6 Provisions and contingencies

Provisions are recognized when the Institute has an obligation at the reporting date as a result of a past event; it is probable that the Institute will be required to transfer economic benefits in settlement; and the amount of the obligation can be estimated reliably.

Provisions are measured at the present value of the amount expected to be required to settle the obligation using a pre-tax rate that reflects current market assessments of the time value of money and the risks specific to the obligation. The increase in the provision due to the passage of time is recognized as interest expense.

Provisions are not recognized for future operating losses.

1.7 Revenue

Revenue is recognized to the extent that the company has transferred the significant risks and rewards of ownership of goods to the buyer, or has rendered services under an agreement provided the amount of revenue can be measured reliably and it is probable that economic benefits associated with the transaction will flow to the company. Revenue is measured at the fair value of the consideration received or receivable, excluding sales taxes and discounts.

Interest is recognized, in profit or loss, using the effective interest rate method.

Dividends are recognized, in profit or loss, when the company's right to receive payment has been established.

Notes to the Annual Financial Statements

Detailed Income Statements