Services on Demand

Article

English (pdf)

English (pdf)

Article in xml format

Article in xml format Article references

Article references

Indicators

Related links

-

Cited by Google

Cited by Google -

Similars in Google

Similars in Google

Share

Permalink

PermalinkJournal of the Southern African Institute of Mining and Metallurgy

On-line version ISSN 2411-9717

Print version ISSN 2225-6253

J. S. Afr. Inst. Min. Metall. vol.119 n.2 Johannesburg Feb. 2019

http://dx.doi.org/10.17159/2411-9717/2019/v119n2a4

DIAMONDS - SOURCE TO USE 2018 CONFERENCE

Diamond exploration and mining in southern Africa: Some thoughts on past, current and possible future trends

W.F. McKechnie

Snowden Group, South Africa

SYNOPSIS

Southern Africa is generally thought to be well explored, with only limited potential for major new diamond discoveries. However, Chiadzwa in Zimbabwe and reports of a significant new kimberlite find in Angola are testimony to the dangers attached to an attitude that 'there is nothing left to find'.

Since the major discoveries in the central interior of South Africa in the 1870s, diamond exploration in the region has been led by market and political factors that influence the key exploration drivers of opportunity and value proposition. Unexpected new discoveries by new players always impact on existing producers and, from time to time, denial of opportunity through political or protectionist policies has inhibited investment in exploration.

Entrepreneurial exploration appetite in southern Africa will be tempered by the potential value equation and security of investment. Overlaid on this, developments in diamond recovery technologies provide opportunity to reinvigorate current mines and old prospects previously considered too difficult or costly to exploit. Position on the cost curve will remain a key factor for survival in an increasingly competitive environment.

Keywords: diamond exploration, production, trends, outlook.

Introduction

The diamond industry in southern Africa boasts a history of 150 years of discovery and mining, forming the cornerstone of development of the core, modern economies at the southern tip of Africa.

Since the discovery, in the 1860s and 1870s, of the secondary diamond placers and primary diamond-bearing kimberlite deposits in the central interior of the then Cape Colony and Orange Free State, southern Africa has endured as the pre-eminent diamond-producing region in the world. Notwithstanding periodic competition from significant new discoveries in other parts of the globe and the paucity of recent, new discoveries in the region, its ranking is unlikely to change in the short to medium term.

In a geological context the region contains the Kaapvaal-Zimbabwe and Angola-Kasai cratons, identified in terms of Clifford's rule as areas inherently prospective for diamonds, being underlain by portions of the Earth's crust that are tectonically stable and older than 1.5 billion years (Clifford, 1992). Although the Democratic Republic of Congo (DRC) would, in a geographic context, be considered to be part of Central Africa, for the purposes of this review it is included in southern Africa since northeast Angola and the adjacent parts of the DRC form part of the same geological terrane and diamond production from both countries needs to be considered together. Historical and current diamond production from the northeastern parts of the DRC around Kisangani is not considered to be significant and its inclusion in the overall numbers for the DRC does not materially affect the overall picture presented here.

Hence, in this review, the countries considered are South Africa, Zimbabwe, Namibia, Angola, the DRC, Lesotho, Botswana, and eSwatini (previously Swaziland), the first five of which each has a history of diamond production stretching back more than 100 years, and in the case of South Africa, 150 years (Table I).

Historical perspectives

The first wave of diamond exploration in southern Africa was initially driven by opportunistic, entrepreneurial spirit and endeavour but inevitably, and quite quickly, operational and market factors led to consolidation of the operating companies and lateral and vertical integration of the different industry components.

From 1870 until shortly before the start of the First World War the diamond mines of South Africa accounted for almost 100% of global diamond production. During the latter part of this period the main diamond-producing company of the time, De Beers, enjoyed a virtual monopoly in diamond supply from its kimberlite mines. This situation started to change shortly after the turn of the 19th century when the Premier Mine at Cullinan, east of Pretoria, came into production. Kimberlites had been discovered in 1897 at Rayton to the south, just before the South African War (Draper, 1898), but lay fallow until hostilities ended and economic conditions normalized.

Independent production from the Premier Mine led to increased market competition and volatility of diamond prices, but the situation worsened considerably in the following decade for the established producers (Innes, 1975). In the period between 1907 and 1912, massive secondary diamond deposits were discovered in German South West Africa (now Namibia), at Tshikapa in the Belgian Congo (now the DRC), and in the Lunda Provinces of Portuguese West Africa (now Angola).

Immediately following the end of the First World War, further new major diamond placers were found at Mbujimayi in the DRC, in the Gold Coast (now Ghana), in Namaqualand, and around Lichtenburg in South Africa, and other countries in West Africa, most notably Sierra Leone, (Levinson, Gurney, and Kirkley, 1992). The exceptional quality of the West African production had an enormous impact, with the result that, through to the 1960s, world diamond production was dominated by these major secondary diamond fields to the virtual exclusion, for a time, of the South African kimberlite mines, most of which either closed or drastically cut production in the inter-war period (Janse, 2007).

Following the Second World War De Beers, launched its 'A Diamond is Forever' marketing campaign to exploit an anticipated post-war economic boom in the USA and Europe. The company embarked on an ambitious investment programme to reopen and modernize its mines in South Africa and South West Africa, and also purchased the Williamson Mine in East Africa. New diamond production from major discoveries in Russia in the late 1950s threatened De Beers' market leader status, and this encouraged it to increase investment in diamond exploration throughout Africa, commencing in East Africa, extending southwards into Bechuanaland (now Botswana) and into Angola and Zaire (now the DRC). Newly independent Botswana was host to the fabulous discoveries at Orapa and Jwaneng. Smaller finds in Southern Rhodesia (now Zimbabwe) and Swaziland (now eSwatini) spurred renewed interest in South Africa, leading to the discovery of Venetia and other smaller mines in South Africa and Botswana.

Figure 1 shows a chart of diamond discovery and mining in southern Africa for all of the countries listed in Table I covering the period 1867 to present. Although the trend has the appearance of being fairly continuous, three definite discontinuities are noticeable, shown as A, B, and C.

'A' in Figure 1 represents the initial period of industry consolidation in Kimberley, which led to the formation of De Beers Consolidated Mines and its initial monopolization of the industry. Additional factors that diminished interest in diamond prospecting during that period were the discovery of the Witwatersrand goldfields in 1886 and political events leading up to the South African War of 1899 to 1903.

Period 'B' followed the discovery of the huge placer deposits in Namibia, Angola, the DRC, West Africa, and Namaqualand and Lichtenburg in South Africa. These had a devastating effect on the South African diamond mining industry. Investment in existing mines and exploration for, and development of, new kimberlite operations ceased in South Africa and exploration for primary deposits elsewhere was also deterred. The Great Depression of the 1930s undoubtedly played a part, but the greatest influence came from the low-cost production of high-quality, gem diamonds from West Africa, Angola, and other independent producers. In South Africa, the industry situation was so dire that in 1927, the Union government passed the Precious Stones Bill forbidding prospecting and digging for diamonds on state-owned land in the Cape Province. This restriction was only lifted in 1960 following the discovery of the diamond-bearing dykes at Bellsbank, followed shortly afterwards by the Finsch Mine discovery (Janse, 1995). Similar restrictions were in place elsewhere in the region. In Southern Rhodesia (now Zimbabwe) De Beers held exclusive rights to prospect for diamonds through the British South African Company (BSAC), founded by Cecil Rhodes, which were ceded to the government only in the 1940s. In Angola and the Congo, exclusive diamond rights were held by Diamang and Forminière respectively.

The main influence in period 'C' was the Angolan civil war, which affected the whole subcontinent from its commencement in 1975 to 2002. Although diamond mining continued in Angola throughout most of this period, exploration was not possible until the early 2000s and there were spillover effects into neighbouring countries. Zimbabwe was also not fully accessible between 1975 and the late 1980s. The effect of all of this was that, for an extended period in southern Africa, diamond exploration was restricted to South Africa and Botswana, both relatively mature exploration terranes by that time, and post-Venetia, the only significant new deposits found were small and short-lived operations. An additional factor was the significant exploration successes in in other parts of the world, such as Australia and Canada, which increased competition for exploration spend.

In recent years new diamond discoveries in southern Africa have been scarce, with most new production coming from re-examination of older mines and prospects. The two exceptions are the Luaxe kimberlite in Angola (Alrosa, 2017) and the Chiadzwa placer in Zimbabwe, which has had a significant influence on the industry for approximately 10 years (Kimberley Process Statistics, 2004-2016; Manenji, 2017).

Diamond production

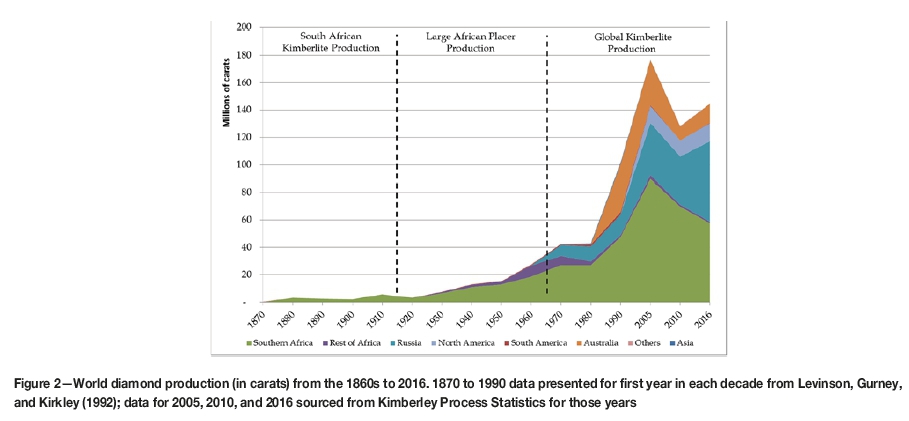

Figure 2 summarizes annual world diamond production in carats (ct) from 1870 through to 2016, showing the phenomenal growth since the 1950s. Three main production periods are shown. The period 1867 until 1910 was dominated by South African kimberlite mine production. Production from 1910 to about the mid-1960s was dominated by the large African secondary deposits which, for a considerable period, produced more than 50% of global production in value terms.

The period from the 1960s through to the present has again been dominated by large kimberlite and lamproite mines, with the result that, by the turn of the millennium, more than 75% of world production by volume and value came from primary deposits, a reversal of the situation that prevailed from 1920 through to 1960 (Janse, 2007). During the last 30 years, new kimberlite and lamproite primary deposits brought into production in Australia and Canada have further reduced southern Africa's market share in volume and value to an average of approximately 50% of total world diamond production (Kimberley Process statistics, 2004-2016).

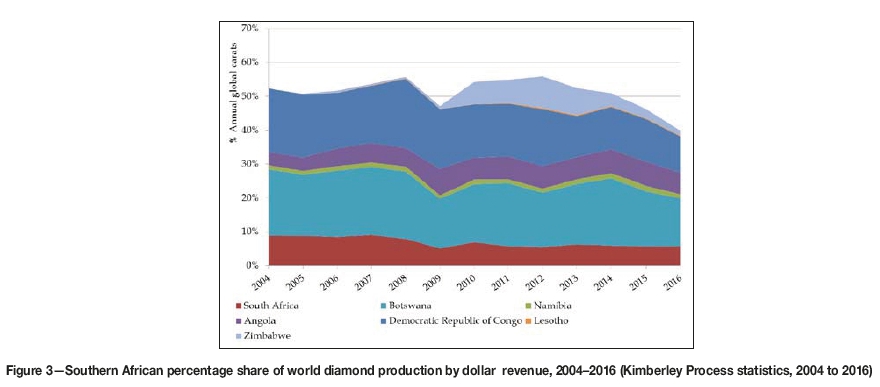

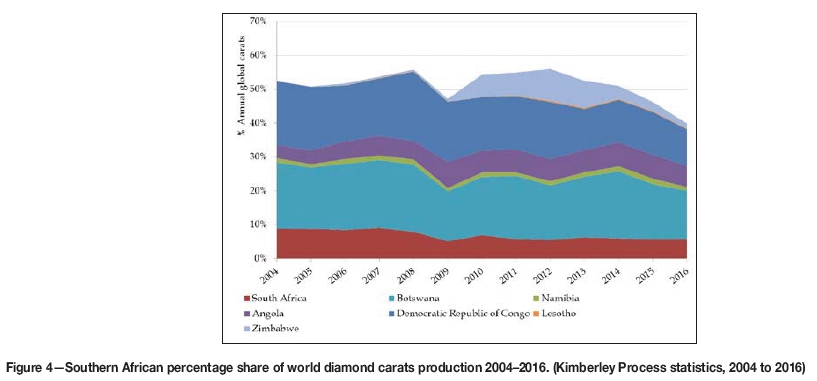

Annual production data reported by the Kimberley Process Certification Scheme since 2004 provides valuable insight into southern African diamond production. Records from 2004 to 2016 show that world diamond production peaked at almost 177 million carats in 2005, but reduced to an average of 125 million carats between 2009 and 2015, increasing again to almost 145 million carats in 2016, mainly on the back of significantly increased production from Russia. On average, for that period, southern Africa produced 51% of the world's diamonds in carats, representing 56% of global dollar revenue (Figure 3 and Figure 4).

Botswana is the dominant producer of the region in terms of volume and value, followed by South Africa, Angola, and Namibia. Lesotho is a relatively minor producer, notwithstanding the very high-value gems produced by its Letseng Mine. Since 2006, Zimbabwe has produced a significant volume of generally low-value diamonds, increasing the region's share of world production at times to almost 60% between 2010 and 2013. Zimbabwe's production is currently in decline and Botswana's mines have lowered production by approximately one-third since 2008 in response to challenging market conditions, causing southern Africa's share of global production to dip below 50% for the first time in 10 years. eSwatini's only diamond mine in closed in 1996 and is not included in Figure 2 or Figure 3.

Diamond values

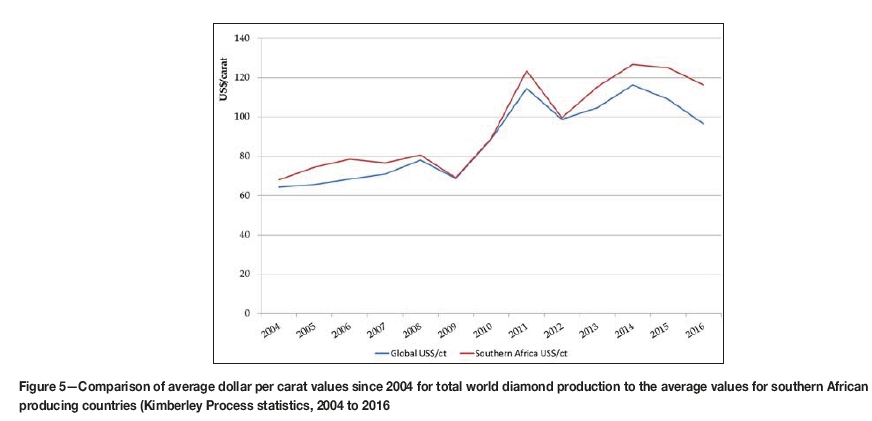

Figure 5 compares average dollar per carat values since 2004 for total world diamond production, as reported by the Kimberley Process, to the average values for southern African producing countries.

Average values for southern Africa are slightly higher than the global average, which is considered to be due to the low average values reported for Russia as a result of the low bottom size cut-offs used in Russian operations, often as low as 0.5 mm compared to 1.25 mm or 1.5 mm for other producers. Another feature of this chart is the general long-term upward dollars per carat trend in average diamond values since 2004. The strong initial post-GFC price recovery was short-lived and average diamond values have been variable but effectively flat since 2011, and negative the in last two years.

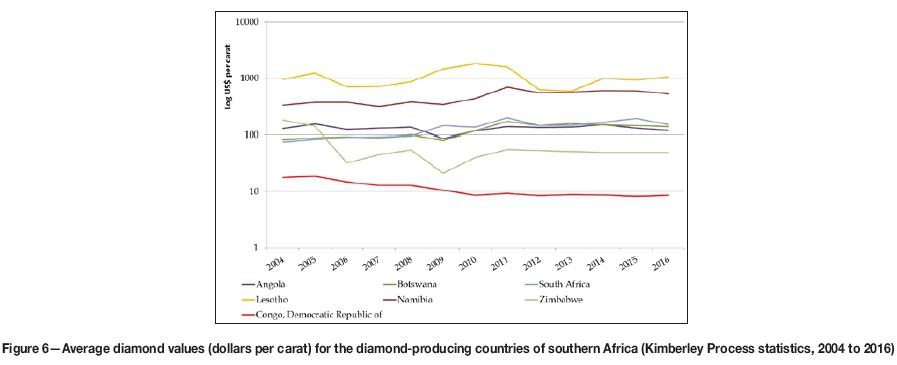

Average diamond values for the different countries in southern Africa are compared in Figure 6 on a logarithmic scale, which allows visual separation of the different country production profiles.

Average values for South Africa, Botswana, and Angola cluster together around the $100 per carat line. Diamond values for Lesotho and Namibia are considerably higher, being influenced by the unusually high-value production from the Letseng kimberlite in the case of Lesotho, and the gem-quality diamonds typical of the Namibian west coast placer deposits. Lower value production separates out towards the lower end of the value scale, representing the Zimbabwe secondary Chiadzwa operations and DRC production, the latter mainly influenced by the diamond population typical of the Mbujimayi area.

Future production and exploration trends

In the medium term (5 to 10 years), given the time needed to develop any new discoveries, the diamond production profile of southern Africa is not expected to change significantly. However, Botswana, having reduced output in recent years, is expected to be able to ramp up supply again should market circumstances change. In the longer term South Africa's and Botswana's share of global and regional production will eventually trend downwards as open pit mines go deeper or move underground. The new Luaxe discovery in Angola, announced recently by the Endiama/Alrosa JV, will increase that country's share of production significantly in due course (Alrosa, 2017; Rough Polished, 2017). Diamond production in the other countries in the region is not expected to change much from current levels and, for the foreseeable future, southern Africa is expected to comfortably maintain its approximately 50% production share in carat and value terms.

The diamond discovery and production history of southern Africa bears testimony to the inherent prospectivity of the region, which justifies continued interest in exploration for new diamond deposits. Previously remote parts of the region and areas inaccessible due to conflict or other reasons are now more accessible. The region's geology is now better understood compared to when the first kimberlite discoveries were made in Angola and Botswana in the middle of the last century. Cover sequences younger than the last phase of kimberlite intrusion in the region are also better mapped and understood, although these continue to present challenges to kimberlite exploration that are not yet fully overcome. Other parts of the region, such as South Africa, Zimbabwe, Lesotho, and eSwatini, where young cover is generally not considered a problem, have been more intensively explored. This lowers the residual prospectivity and leads some to believe that there remains only limited potential for discovery of new large, long-life deposits in these areas.

Diamond placer exploration

It is generally accepted that the potential for the discovery of new mega-placer deposits of the type exploited in southern Africa for the last 100 years is very low. A mega-placer is a diamond deposit that holds at least 50 million carats with 95% or higher of gem quality (Bluck, Ward, and de Wit, 2005), acknowledged examples being the west coast diamond deposits of Namibia and South Africa. The combined inland diamond fields of Angola and the adjoining portion of the DRC would also meet this definition. The diamond-bearing conglomerates of the Umkondo Series sediments in Zimbabwe might narrowly fit the definition in carat terms, but not in terms of gem diamond content.

The potential for significant new placer discoveries seems therefore to be limited to extensions of known occurrences in Namibia, Angola, and elsewhere in the region. The feasibility of exploiting the in-situ conglomerates at Chiadzwa in Zimbabwe is yet to be proven, but extensions of this field may still be found. Other potential placer targets might be surficial deposits proximal to new kimberlite discoveries, such as those being exploited at the Krone-Endora deposit adjacent to Venetia. Such small deposits are unlikely to be of interest to major mining companies but would be suitable for exploitation by juniors.

Kimberlite exploration

It is evident therefore that most future diamond exploration in southern Africa must be directed towards the discovery of as yet undiscovered kimberlite deposits. The parts of Angola and Botswana covered by younger strata appear to hold promise for new opportunity, with Angola, as result of having been inaccessible during its civil war years, holding pole position in terms of potential.

In Angola, Diamang, the original state-owned diamond mining company, discovered and developed the Angolan diamond deposits over a period of 60 years. Until 1971, Diamang was the only company authorized to explore for and mine diamonds in Angola. It exploited alluvial deposits with great success and, starting in the 1950s, its exploration work led to the discovery of kimberlite deposits such as Catoca, Camatchia, and Camútue (Chambel, Caetano, and Reis, 2013). More than 40 years after Diamang's replacement by the new state company Endiama, the recent discovery at Luaxe by the Endiama/Alrosa joint venture appears to be the only kimberlite deposit capable of being exploited in Angola so far not found by Diamang.

Study of any map of the distribution of kimberlites in northeast Angola leads to the inescapable conclusion that most of the known kimberlites occur in, or proximal to, river valleys, suggesting that these have been found as a result of having been exposed by erosion and that others lie undiscovered under younger cover (Chambel, Caetano, and Reis, 2013). A number of companies have undertaken airborne geophysical exploration on the uneroded interfluves and some new kimberlites have been found, notably the Mulepe cluster by De Beers, but until the Luaxe discovery nothing of significance had emerged. In 2015 the government of Angola embarked on an ambitious geophysical survey of large parts of the country, the results of which were expected by the end of 2017 (Ponce de Leâo, 2015). It is not clear how the Angolan government intends dealing with the results from these surveys but, once available, new exploration targets are likely to be generated.

In Botswana, some greenfield work continues but most recent diamond exploration interest is being generated around existing mines and reinvestigation of old prospects, mainly as result of the Karowe experience and the idea that the application of new diamond recovery technologies and different processing flow sheets may revitalize some of these (Sasman, Deetlefs, and van der Westhuyzen, 2018). Despite improved geophysical technologies, the Kalahari cover in Botswana continues to hamper exploration, making the discovery process difficult; however, potential for new finds remains.

South Africa was considered a mature area for diamond exploration potential even in the 1950s, but this did not prevent two major new discoveries 100 years after the original Kimberley and Free State finds; at Finsch, only 150 km from Kimberley, and 20 years later at Venetia in the far north of the country. Since then, other smaller, but nevertheless economic discoveries have also been made, with small mines developed at The Oaks, Klipspringer, and Marsfontein. Many new kimberlites were found in the Northern Cape Province from airborne geophysical surveys, but to date the only deposit being exploited as a result of that work is the Kareevlei kimberlite, owned by BlueRock Diamonds.

Similarly, in Zimbabwe, also considered a relatively well explored part of the region, the Murowa kimberlites and the Chiadzwa placer deposits lay hidden for almost a hundred years after the first alluvial diamonds and kimberlites were found. Factors discouraging diamond exploration historically were the same economic factors applicable in South Africa, combined with exclusive rights to prospect and mine for diamonds being restricted for various reasons and, to some extent, perceptions that there was nothing new to be found

Current diamond exploration activity in Lesotho is mainly restricted to investigation of old prospects, also using new diamond recovery technologies to improve efficiencies and reduce costs. A countrywide diamond exploration programme was reported to have been carried out in eSwatini in the early 2000s but nothing new appears to have come from this work.

Diamond-bearing kimberlite deposits are not easy to find and, generally having a limited surface expression, require painstaking and diligent work to ensure discovery. Traditional methods of exploration based on soil and drainage sampling for indicator minerals have proven very effective in the past and will continue to be the most important exploration tool. In areas where the effects of unusual geomorphology or younger cover further inhibit direct discovery, it will be necessary to supplement sampling programmes using geophysical technologies. Airborne magnetics has generally been the method of choice, sometimes combined with electromagnetic systems, but the results from airborne gravity systems have been unfulfilling to date.

Exploration expenditure trends

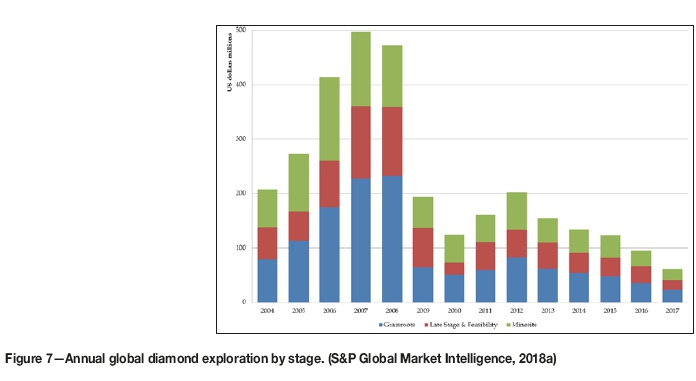

Estimates of annual exploration spend are prepared each year by S&P Global Market Intelligence (S&P GMI) based on surveys of a large number of mining and exploration companies throughout the world. Data retrieved from S&P GMI in April 2018 has been used in the analysis of diamond exploration data presented here.

Figure 7 shows that almost $1 billion was spent cumulatively in 2007 and 2008 on diamond exploration throughout the world, with almost half of that being spent in Africa. For the three-year period from 2006 to 2008, over $400 million was spent annually on African diamond exploration.

The global financial crisis (GFC) of 2008-2009 caused significant disruption to the diamond industry and this translated through to significantly reduced expenditure on exploration, which has flowed through to the present (S&P GMI, 2018a). Post-GFC, world diamond exploration budgets more than halved in 2009 compared to the previous year, and similar or greater reductions carried through to African exploration budgets. Budgets reduced further in 2010 and recovered in 2011 and 2012; but this was short-lived, and a steady and continuous decline in global annual budgets is noted, from $520 million in 2012 to $208 million in 2017 (S&P GMI, 2018a).

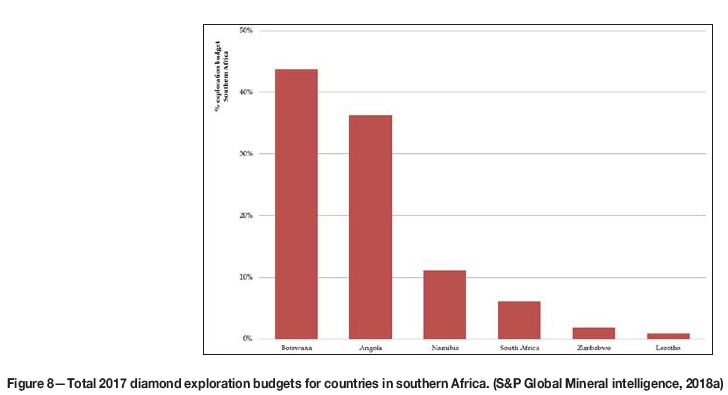

This downward trend in budgets is not confined to diamonds, but has been general across all mineral commodities since 2012. A slight up-kick in overall exploration budgets was reported for 2017 (S&P GMI, 2018b) but did not appear to carry through to diamond exploration. S&P GMI (2018b) estimated the total global, non-ferrous metal exploration budget at $8.4 billion for 2017, but only $208 million (2.5%) was allocated to diamond exploration (S&P GMI, 2018a). Current estimates indicate that the total diamond exploration budget for southern Africa in 2017 was approximately $56 million, with 80% split fairly evenly between Angola and Botswana (Figure 8) (S&P GMI, 2018a).

The immediate reasons for the post-GFC trends were most likely the inherent risks associated with exploration and the need for companies to conserve cash, especially smaller companies. As the recovery in diamond prices has been slower than hoped for and the long-promised upward price drive has not been forthcoming, the level of annual budgets allocated to diamond exploration has also diminished.

Based on analysis of S&P GMI data, supported by a review of company annual reports, more than half of the global diamond exploration budget is spent by just two companies, Alrosa and De Beers. Alrosa in particular has become increasingly active outside Russia and in southern Africa is undertaking exploration in Angola, Botswana, Namibia, and Zimbabwe. Alrosa's JV with Endiama in the Catoca mine appears to be successful and is a strong pillar of the Angolan diamond mining industry. The new Luaxe discovery will add to that success, and according to recent reports will double Angola's annual diamond production once mine development is completed (Rough Polished, 2017).

Outlook for diamond exploration in Southern Africa

Key factors to be considered in undertaking diamond exploration are the inherent prospectivity of the target area, especially if there is a proven track record of production, ease of access, security of tenure and investment, political stability, and an open and transparent operating and fiscal regime. The foregoing has shown that southern Africa scores very highly on the first factor but, as reported in the Fraser Institute Annual Survey of Mining Companies 2017 (Fraser Institute, 2018) and evidenced by prevailing legislation applicable to diamond exploration and mining, the region is a mixed bag as regards the other factors. However, this is not always a deterrent for explorers and investors operating in the African diamond exploration and mining field, some of whom are prepared to operate under high levels of uncertainty.

Gem diamond production

An important consideration for investors is the potential value of the prize that might be obtained as a result of the exploration investment. All things being equal, areas with potential for higher value diamonds will usually attract higher levels of interest than others, as mines that produce better quality diamonds, especially if the diamond grade is also high, tend to be more robust in market downturns than those that produce poorer quality diamonds.

All diamonds are not equal, and a number of factors influence the desirability and value of individual rough stones. These are the size or weight of the diamond in carats, morphology (or shape), colour (shades of white through to yellow and other colour varieties, described as 'fancies'), and clarity (the impact of inclusions, cracks, or other impurities).

Levinson, Gurney, and Kirkley (1992) commented that rough diamonds that yield good-quality polished gems, especially 0.5 ct or larger, are not common, and that stones over 1.5 ct are particularly rare. The reduced output of secondary diamond sources over time, which tend by their nature to contain larger and better quality stones than kimberlite sources, also means that relatively fewer of these better quality stones are being produced than in the past. Also, although 50% of the world's rough diamonds were classified as cuttable at that time, only about 2% to 2.5% were expected to yield good-quality stones of 1 ct or larger. In the author's experience, these estimates are considered reasonable on average, although diamond qualities vary according to the source area. For instance Siberian and Canadian kimberlite pipes generally contain a higher proportion of better quality diamonds than southern African sources, and variations exist within each region.

The DRC is therefore unlikely to attract explorers except for small-scale alluvial operations in the Kasai. Botswana will continue to attract exploration investment due its discovery track history and the ease of doing business there. Zimbabwe has recently announced changes to its mining investment regime, but the picture for diamonds is not yet clear, with the Zimbabwe Consolidated Diamond Company enjoying what appear to be exclusive diamond rights, at least in the Chiadzwa area. The situation for South Africa is also unclear, given current uncertainty concerning amended mining legislation (which is still to be put in place) and the time taken to process prospecting right applications. In Angola all rights to explore for diamond deposits are vested in the state company Endiama, and private companies may obtain prospecting rights only by virtue of a concession contract approved by the Angolan Council of Ministers. This is often a lengthy and expensive undertaking, which generally means that only well-equipped and well-financed exploration companies can go through this process.

As shown earlier in this paper, in southern Africa the diamond exploration playing field has never been level, with various countries effectively closed off to exploration at times due to legislation or exclusive rights awarded to preferred companies, or conflict. One reason for this is certainly because governments often regarded diamond mining as being of strategic interest, requiring special oversight and protection. This situation still prevails in parts of southern Africa, and indeed other parts of the world, limiting areas easily accessible to private or listed exploration entities. In southern Africa, with the exception of Botswana and Namibia, the right to undertake diamond exploration and mining is not an open door for prospective explorers and investors.

Market factors

Price stability of the product is a key factor to be considered in developing a diamond mine, and from the very early days, producers and marketers recognized this need. The rationale for restrictive practices in the past was provision of market support to ensure price stability and surety of mining investments already made, as well as revenues going forward (Innes, 1975). In the post-Second World War years, De Beers' dominance brought a semblance of stability to the diamond market, interrupted at times by new independent discoveries such as in Russia, Australia, and later in Canada. This situation prevailed for some decades but increasing antitrust and competition law pressures, initially from the USA and later from the European Community, forced a policy rethink. Consequently, De Beers relinquished its policy of market dominance, with the result that its market share has fallen from more than 90% in the 1980s to less than 40% today, and it might be argued that the industry has paid for this in terms of increased price volatility.

Most market commentators report a stable and positive outlook for the diamond industry going forward and predict that for the period through to 2030, rough diamond demand will grow at average rates of 1% to 4% (Bain and Company, 2017). Industry fundamentals also suggest a supply-demand shortfall going forward, which is expected to influence prices positively. However, this is predicated on normal business continuing as it has in the recent past. In the past, new discoveries, especially large finds, have always impacted on existing producers. The impact of the new discovery in Angola is still to be seen but, if it is as important as implied in recent press articles, then the overall balance of the industry may be affected, and more so if further exploration success is achieved.

A further external factor confronting the natural diamond industry is competition from laboratory-grown gem diamonds. A report by Frost and Sullivan (2014) postulated that the predicted developing supply-demand gap for natural gem diamonds could, at least partly, be taken up by synthetic gem diamonds. A key constraint for such a scenario is the cost of building production facilities and consumer resistance, but the report argues that, as natural gems become scarcer and more expensive, the barriers to market entry for grown diamonds may reduce. In a 2017 report ABN AMRO (2017) suggested that, in the coming decades, laboratory capacity for production of laboratory-grown gem diamonds could exceed the mined production of gem-quality diamonds. However, it is considered that laboratory-grown diamonds are more likely to impact on the market for diamonds below 0.5 ct in size, as described earlier, than the larger and rarer categories of gem diamonds. The recent foray by De Beers into this field is an interesting development that will be closely watched (De Beers, 2018).

Conclusions

Southern Africa is inherently prospective for diamonds and has the potential to continue as the pre-eminent producer of natural diamonds for the foreseeable future. This has been confirmed by recent discoveries in Angola and Zimbabwe, but some parts of the subcontinent have greater exploration potential than others. Entrepreneurial exploration appetite in southern Africa will be tempered by perceptions of the potential value equation and security of investment in diamond exploration. The uneven investment climate that prevails in the region will also affect levels of exploration investment, but recent changes in the political environment may provide potential for new exploration opportunities.

References

ABN AMRO. 2016. Diamond sector outlook, nothing is forever ... 19 January 2016. https://insights.abnamro.nl/en/2016/01/diamond-sector-outlook-nothing-is-forever/ [ Links ]

ABN AMRO. 2017. Diamond sector outlook, nothing is forever - part 2... 8 December 2017. https://insights.abnamro.nl/en/.../diamond-sector-outlook-nothing-is-forever-part-2/ [ Links ]

Alrosa. 2017. ALROSA to participate in the development of the largest deposit in Angola. http://eng.alrosa.ru/alrosa-to-participate-in-the-development-of-the-largest-deposit-in-angola/ [ Links ]

Bain and Company Inc. 2017. The global diamond industry 2017. The enduring story in a changing world. 33 pp. http://www.bain.com/publications/articles/global-diamond-industry-report-2017.aspx [ Links ]

Bluck, B.J., Ward, J.D., and de Wit, M.C.J. 2005. Diamond mega-placers: southern Africa and the Kaapvaal craton in a global context. Special Publication 248. Geological Society, London. pp. 213-245. https://doi.org/10.1144/GSL.SP.2005.248.01.12 [ Links ]

Chambel, L., Caetano, L., and Reis, M. 2013. One century of Angolan diamonds. Report prepared by Sinese - Consultoria Lda and Eaglestone Advisory Limited. [ Links ]

Clifford, T.N. (1966. Tectono-metallogenic units and metallogenic provinces of Africa. Earth and Planetary Science Letters, vol. 1. pp. 421-434. [ Links ]

Damaruparshad, A. 2007. Historical diamond production (South Africa). Report R61/2007. Department of Minerals and Energy, Pretoria. [ Links ]

De Beers Group of Companies. 2018. De Beers to launch new fashion jewelry brand with laboratory grown diamonds. Media release, 29 May. https://www.debeersgroup.com/en/news/company-news/company-news/de-beers-group-to-launch-new-fashion-jewelry-brand-with-laborato.html [ Links ]

De Wit, M.C.J. 2010. Identification of global diamond metallogenic clusters to assist exploration. Proceedings of Diamonds Source to use, Gaborone, Botswana, 1-3 March 2010. Southern African Institute of Mining and Metallurgy, Johannesburg. http://www.saimm.co.za/Conferences/DiamondsSourceToUse2010/015-deWit.pdf [ Links ]

De Wit, M.C.J., Bhebhe, Z., Davidson, J., Haggerty, S.E., Hundt, P., Jacob, J., Lynn, M., Marshall, T., Skinner, C., Smithson, K., Stiefenhofer, J., Robert, M., Revitt, A., Spaggiarri, R., and Ward, J. 2016. Overview of diamond resources in Africa. Episodes, vol. 39, no. 2. pp. 199-237. [ Links ]

Draper, D. 1898. On the diamond pipes of the South African Republic. Transactions of the Geological Society of South Africa, vol. iV. p. 5. [ Links ]

Fraser Institute. 2018. Annual Survey of Mining Companies 2017. https://www.fraserinstitute.org/studies/annual-survey-of-mining-companies-201 [ Links ]

Frost and Sullivan. 2014. Grown diamonds: Unlocking future of diamond industry by 2050. https://ww2.frost.com/news/press-releases/grown-diamonds-key-unlocking-future-diamond-industry-finds-frost-sullivan/ [ Links ]

Innes, D. 1975. The exercise of control in the diamond industry of South Africa: Some preliminary remarks. African Studies institute, university of the Witwatersrand. African Studies Seminar Paper, March 1975. [ Links ]

Janse, A.J.A. 1995. A history of diamond sources in Africa: Part I. Gems and Gemology, vol. 34, no. 4. pp. 228-255. [ Links ]

Janse, A.J.A. 1996. A history of diamond sources in Africa: Part II. Gems and Gemology, vol. 35, no.1. pp. 2-30. [ Links ]

Janse, A.J.A. 2007. Global diamond production since 1870. Gems and Gemology, vol. 43, no. 2. pp. 98-119. [ Links ]

Kimberley Process Rough Diamond Statistics, 2004 to 2016. https://kimberleyprocessstatistics.org/public_statistics [ Links ]

Levinson A.A., Gurney J.J., and Kirkley M.B. 1992. Diamond sources and productivity: Past, present and future. Gems and Gemology, vol. 28, no. 4. pp. 234-254. [ Links ]

Manenji, T. 2017. The trajectory of Zimbabwean Marange diamond revenue remittances from 2016 to 2013. Scholedge International Journal of Business Policy and Governance, vol. 4, no. 6. doi: 10.19085/journal.sijbpg040601 [ Links ]

Ponce de Leäo, T. 2015. Geological mapping of Angola; An example of knowledge share between GeoSurveys of Europe and Africa. Proceedings of the EGS-ASGMI Director's Joint Workshop, October 2015. EuroGeoSurveys, Brussels, Belgium. [ Links ]

Rough Polished. 2017. Luaxe kimberlite to help Angola double output by 2022. 10 February 2017. http://www.rough-polished.com/en/news/105846.html [ Links ]

S&P Global Market Intelligence. 2018a. User platform. [ Links ]

S&P Global Market Intelligence. 2018b. World Exploration Trends. A Special Report from S&P Global Market Intelligence for the PDAC International Convention. March 2018 [ Links ]

Stocklmayer, V. and Stocklmayer, S. 2015. A review of diamonds in Zimbabwe - a century on - part 1, Geological Society of Zimbabwe Newsletter, October 2015. pp. 4-11. [ Links ]

Sasman F., Deetlefs B., and van der Westhuyzen, P. 2018. Application of diamond size frequency distribution and XRT technology at a large diamond producer. Journal of the Southern African Institute of Mining and Metallurgy, vol. 118. pp. 1-6. [ Links ]

Wilson, A.N. 1982. Diamonds: From Birth to Eternity. Gemmological Society of America, Santa Monica, CA. [ Links ]

Zimnisky, P. 2014. The state of the global rough supply 2014. Paul Zimnisky Diamond Analytics. 8 pp. http://www.paulzimnisky.com/the-state-of-global-rough-diamond-supply-2014 ♦ [ Links ]

This paper was first presented at the Diamonds - Source to Use 2018 Conference, 11-13 June 2018, Birchwood Hotel and OR Tambo Conference Centre, JetPark, Johannesburg, South Africa.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}