Servicios Personalizados

Articulo

Inglés (pdf)

Inglés (pdf)

Articulo en XML

Articulo en XML Referencias del artículo

Referencias del artículo

Indicadores

Links relacionados

-

Citado por Google

Citado por Google -

Similares en Google

Similares en Google

Compartir

Permalink

PermalinkJournal of the Southern African Institute of Mining and Metallurgy

versión On-line ISSN 2411-9717

versión impresa ISSN 2225-6253

J. S. Afr. Inst. Min. Metall. vol.113 no.3 Johannesburg mar. 2013

PLATINUM CONFERENCE 2012

Metal accounting in the platinum industry: How effective is it?

P.G. GaylardI; N.G. RandolphII; C.M.G. Wortley

IUniversity of Cape Town, South Africa

IINSR Investments CC3, Consultant

SYNOPSIS

The AMIRA Code of Practice and Guidelines for Metal Accounting was developed in response to demand from a number of sponsor companies, including one major platinum producer. Since its publication in 2007, the Code has become widely accepted in the mining industry world-wide as a guide for best practice in metal accounting. With the changes in the structure of the platinum mining industry in South Africa over the last 10-15 years, in particular, the starting up of a number of small platinum producers who must have their concentrate smelted and the contained valuable metals refined by third parties, the need for metal accounting systems that are accurate and have an acceptable level of precision has become even more critical to the success of a platinum-producing operation. The current state of metal accounting in the industry is discussed, and possible areas for improved accounting and associated metallurgical efficiencies are identified.

Keywords: AMIRA Code, metallurgical accounting, platinum industry.

Introduction

The character of the South African platinum industry has changed significantly over the past ten to fifteen years. In the early 1990s, the industry was dominated by three major players, all of whom operated their own smelters, base metal refineries, and precious metal refineries. Since then, an additional smelter and base metal refinery have been commissioned, but the greatest change has been in the number of smaller mining operations that have been opened on both the western and the eastern limbs of the Bushveld Complex. In general, these smaller operations operate their own concentrator plants but have to ship their concentrate to one of the smelting plants in the industry locally or overseas for further processing and the extraction and refining of the valuable metals.

This has changed the way the established major players run their respective businesses. Previously, the smelting plants treated concentrates generated in-house and mine shafts or operations may have been unhappy at times with the metal quantities allocated to them, the income from the sale of the metals ended up in the hands of the owning company, and errors in metal allocation did not have a serious impact on the company's overall performance.

The smelting plants and their associated refineries have now become toll treatment operators, and it is vital that they are able to account as accurately and as reliably as possible for the metals received in the concentrate from these smaller producers. If their metal accounting systems are inadequate, the smelters and refiners are forced to reduce the metal recovery figures they quote to would-be concentrate suppliers, in order to protect their own production performance.

Another change in the platinum industry over the past twenty years has been the marked increase in the production of concentrate from UG2 ore with its associated smelting problems, to the extent where the existing smelter plants are beginning to compete for Merensky concentrate from the smaller suppliers, in order to provide sufficient diluent for the chrome-rich UG2 concentrates fed to the smelters. The smaller platinum producers will naturally enter into agreements with the smelter offering the most attractive treatment terms, and a smelting operation with a reliable metal accounting system will have a competitive advantage over an operation with a less reliable system.

Another, more recent, change in the South African platinum industry has been the impact of rapidly rising costs and falling metal prices over the past three years, which have had a serious impact on profits, to the point where at least three mining operations have been placed on a care-and-maintenance basis, while other operating shafts are reported to be running at a loss. This has affected all of the producing companies, but to the smaller producer it poses a much greater threat as smaller companies tend to have fewer production alternatives than the larger producers, as well as more fragile balance sheets.

From the point of view of these smaller platinum producers, an additional 1 per cent on the recoveries quoted to them for the treatment of their concentrates can make a significant difference to the valuation of their mining operation and to their ability to remain in production during periods of economic difficulty, as at present. They also need to be comfortable that the metal content of their concentrate and the metal recovery are being correctly measured and reported, and that they are not being adversely affected through inadequate metal accounting or through the effect of undetected mass measurement or analytical biases.

Metal accounting - the AMIRA Code

In 2003 AMIRA initiated their P754 research project: Improving Metal Accounting. The primary objective of the project was to provide tools for improving the auditability and transparency of metal accounting from mine to product, and to facilitate good corporate governance. The planned deliverables of the project included a Code of Practice for Metal Accounting (AMIRA, 2007), and a textbook on the subject that could serve as a guide for metal accounting practitioners and students studying the topic. The development of the Code of Practice for Metal Accounting and its application are discussed in Gaylard et al. (2009), and its main features are summarized here.

The Code is based on a set of ten Principles of Metal Accounting, which were agreed by the development team in consultation with the accounting profession and the sponsors of the project and which cover accurate measurements of mass and metal content, transparency, documentation and calculation procedures, internal and external audits, reporting, procedures and levels of authorization for the replacement of provisional or rogue data, data verification and reconciliation, target mass measurement and sampling and analysis accuracies, physical stock-takes and the treatment of unaccounted losses or gains, and the rapid identification of any bias that may occur.

The basic philosophy behind the Code is that it prescribes standards and best practices for mass measurement, sampling, sample preparation, analysis, data management, and metal balancing, to enable compliance with the basic principles. However, where an operation cannot comply with these prescribed standards an exception report must be prepared, setting out the reasons for non-compliance (cost, risk, etc.). The exception report must be signed off by a competent person and submitted to the company's audit committee for approval. In this way, decisions related to metal accounting that could have a significant impact on the company's reported results and on its metallurgical efficiencies are brought to the attention of senior management and, where appropriate, to the board of directors. Such decisions are therefore handled in a transparent manner, subject to review by the company's financial auditors, and incorporate a formal review of the risks associated with non-compliance with the Code.

The Code makes provision for a 'Competent Person', who must be a member of the relevant local professional registration authority, or any other statutory local or international body that is recognized by the relevant Code administrators, and that person should have a minimum of five years' experience relevant to the type of metal or mineral under consideration and to the type of operation involved. The Competent Person must be independent of the operation concerned, and be formally appointed by the management of the company or the operation concerned to recommend standards for the setting up and auditing of metal accounting systems. He will be required to accept responsibility for the final approval of the design of the metal accounting systems and to conduct periodic reviews and audits of the system, to ensure continued compliance and, as required, to investigate problems that may occur, submitting reports to management. For large or complex operations, the Competent Person is likely to lead a small team of experts. However, only the Competent Person will have sign-off responsibility.

Since Release 3 of the Code and Guidelines was distributed in February 2007, the Code has been adopted by numerous mining companies, in addition to the companies that sponsored the AMIRA project, in South Africa, Australia, and in North and South America. Requests for copies of the Code have been received from mining companies, and from people providing services to these companies, in a wide range of countries on every continent.

In addition, members of the Code Development Team have been asked to conduct audits of various aspects of metal accounting at a variety of operations ranging from base metal concentrators and smelting plants to precious metal refineries.

Errors and biases in metal accounting

Sampling, sample management and analysis

Introduction

Because of the very high intrinsic values of the platinum group metals (PGMs), the need for accurate metal accounting has been recognized by the platinum industry for many years. For example, Pierre Gy, the 'godfather' of correctly designed samplers, was brought to South Africa as a consultant for Rustenburg Platinum Mines as long ago as 1980, and his book 'Sampling of Particulate Materials -Theory and Practice' published in 1979 became compulsory, but very difficult, reading for the technical staff employed in evaluation. In addition, six-monthly or annual stocktakes have always been part of the platinum refinery's metal accounting arsenal, but these are now being applied as early in the process chain as the concentrators.

In spite of this, because the industry was starting from a poor position, it has taken many years of effort to arrive at the current situation where, in many cases, we can say that we have almost achieved the goal of accurate metal accounting in the platinum sector.

Sampling

When the AMIRA Code was in its initial stages of preparation, the only stated requirement for a sampling system was that it must be correctly designed. This is in respect of the well-known factors such as minimum cutter gap, maximum speed, retention of the total sample etc. This was very quickly expanded to include correct installation and correct maintenance, because without the combination of all three, an unbiased sample with an acceptable precision will not be obtained. This is probably especially true for correct maintenance in terms of making sure that the sampling system is regularly inspected, at least once per shift, to ensure that it is operating correctly and is clean. Unfortunately, the occurrence of fully or partially blocked sample cutters observed during the audits of plants is still far too high: the figure should be zero.

Accurate metal accounting requires that:

The specification and design of a sampling system, even from a reputable OEM, be carefully inspected to ensure that it complies with the requirements of an accurate sampler. Mistakes such as minimum cutter gaps being < 10 mm, parallel cutters in a radial sampler, and cutter speeds >> 0.6 m/s are still regular occurrences

The authors have found that, in those platinum producers with whom they are regularly associated, sampling of materials is undergoing continuing improvement.

Sample management

The trend is to remove the responsibility for the initial preparation of a sample from the central laboratory to a facility on the plant that is managed either by production or by a dedicated evaluation department, the latter being the preferred option.

In a number of cases, the samples are delivered to the analytical laboratory in a 'ready to analyse' form, i.e. they have been filtered, dried, split, and the particle size reduced, so that they are ready for the analytical aliquot to be weighed out.

There are now numerous examples of where the following requirements of best practice are being applied:

However, an area still requiring attention is the storage of samples that require moisture determination. Too often these samples are collected into 'open' containers and left for periods of up to 8 hours in ambient temperatures that can easily exceed 30°C.

Analysis

Virtually all of the laboratories in the platinum Industry that are well managed are either accredited to ISO 17025 or operating fairly close to these requirements. In fact, in most cases, the full move to ISO 17025 simply formalizes the way the laboratory is operating, but accreditation of those analytical methods that provide the data required for metal accounting is highly recommended.

The following are suggested as the minimum requirements of a laboratory:

- Proof of method validation and adequate staff training

- Twin-stream analysis, which is the analysis of samples by different analysts or repeat analysis of

- the samples by the same analyst at different times. In those laboratories where this is not done, the usual reaction is to say that it is too much effort, but this is only a different form of duplicate analysis. As all analyses for metallurgical accounting should be done in at least duplicate, there is no increase in effort, and knowledge of the true precision of the analytical method is a major advantage. In addition, the improvement in analytical precision from analysing a greater number of replicates is not warranted

- Shewhart (control) graphs, which are used to plot the results of QC samples to provide a visual representation of the results in relation to the ± 2*SD (standard deviation) and ± 3*SD limits

- CUSUM graphs, which are extremely good at detecting and measuring bias in an analytical procedure.

If all of these steps are carried out, the question of 'How reliable is your laboratory?' can be answered positively and proof supplied almost instantly.

Mass measurement

Introduction

During the preparation of the AMIRA Code of Practice and from observations during visits, surveys, and audits conducted subsequently on various plants throughout the mining industry, it was apparent that accurate measurement of mass was often the most neglected of the procedures required for accurate metal accounting i.e. mass measurement, sampling, sample preparation, and analysis.

Sampling and analytical procedures had received a great deal of attention but the same could not be said for mass measurement, especially for measurement of mass in motion. Thus, often the mass is the largest error in the calculation of the metal content and, by the nature of the errors, the most prone to bias.

As the nature of the industry has changed and reporting requirements have become more stringent, the priority for more accurate measurement has increased. It is pleasing to be able to say that, in the platinum companies with which the author has been involved, the management of mass measurement has improved considerably during the past few years, in some part due to application of the AMIRA Code. However, the consistent application of a few basic principles could assist in reducing errors further.

In the platinum industry, the materials requiring mass measurement for metal accounting vary from:

Each of the above stages constitutes a custody transfer, even if all the plants and material belong to one company, and thus all the inputs and outputs are applicable for primary accounting. This means that, even if the plants are in the same operating company, the material transferred should be weighed, sampled, and analysed on the 'Home and Away' system i.e. at both ends of the transfer, especially if this involves transport across security boundaries. In addition, it is now common practice for materials to be toll treated. These can be ore from a joint venture, concentrate, matte, or other materials. Here, errors in mass measurement and metal accounting will affect a company's earnings directly and can even result in toll materials, in reality, being treated at a loss. The range of quantities, material types, and value means virtually all the techniques applicable for mass measurement need to be applied in the industry to suitable standards for primary accounting.

As the material proceeds through the process, the accuracy of the mass measurement improves as the methodology changes from the measurement of mass in motion to static weighing. At the same time, the value increases and the stocks and material in process become increasingly significant as sources of error. These vary from large stockpiles of ore, stocks of concentrate and matte, and higher grade material (slurry, solution, melt, or solid) in process. Often the areas where the greatest errors in metal accounting occur are in the measurement/estimation of the quantity and content of the material in these stocks.

Requirements for mass measurement

Mass measurement for metal accounting requires that the measurement must be:

To achieve the accuracy required for metal accounting requires:

It is important to note that there is an extensive list of standards, regulations, and legal requirements that cover all aspects of the equipment, installation, and calibration, which are often unknown or not utilized.

It is surprising that, even in relatively new plants, the first two criteria are ignored or compromised in the plant design, and inadequate provision made for the installation of suitable equipment for calibration. This is sometimes done as part of capital cost reduction. Sometimes suppliers fail to meet the required standards for the equipment or location. All the other factors necessary to achieve good results are part of best practice and good housekeeping and are entirely under the control of current plant management.

Mass measurement of ore

Custody transfer between the mines and the plants is the most difficult to measure and is often the source of much argument and conflict. The method used by the different producers varies depending on the type of mining, the site and plant layouts, the number of sources, and initial design philosophy.

Mass measurement of tailings

In very few cases are the mass of tailings measured and magnetic flow meters installed. Where they are, the values are often suspect as calibration facilities do not exist. Accurate measurement of large slurry flows is difficult. Thus the mass and content is usually calculated by difference and use of the two-product formula, as is common in many concentrators across the world. Therefore, it is especially important that a suitable sample of the tailings is taken to provide the value to use in the calculation.

Mass measurement of concentrate

Only four platinum operations in South Africa have their own smelters, whereas there are numerous concentrators. Thus there are very few integrated concentrator/smelter complexes and a great deal of the concentrate is transported relatively long distances and toll smelted. A great deal of effort has gone into improving these mass measurements as a necessity for efficient, economic treatment.

For the integrated plants, the concentrate produced is thickened, sometimes filtered, and then dried for feeding to the furnaces. One of these streams usually provides the concentrate mass for primary accounting, which may be wet filter cake on a belt or dry concentrate. The stock in the thickeners can be relatively high and is difficult to measure, which introduces errors on a monthly basis (which should self-correct). Moisture content also contributes errors as the filter cake may be too wet, or alternatively for flash drying, dry and dusty. Sometimes furnace weigh bins are used a check on the tonnage to the furnaces.

In some plants the concentrate produced is measured by flow meter (electromagnetic or Coriolis) and/or the use of weigh tanks. However, these measurements have tended to be inaccurate because of the lack of calibration facilities for the flow meters and the effect of different ores (e.g. Merensky/UG2) on the meters.

Concentrate is often transported between concentrators and smelters in the same company by tanker as a slurry. The material is sampled during loading for analysis and moisture content, and the truck weighed on a weighbridge on dispatch and usually on delivery. It may also be sampled on delivery. The material settles during transport and it is important to ensure that tankers are empty and that the tares of the vehicles are checked and are within the permitted range.

Providing the weighbridges are calibrated and maintained adequately and procedures are followed, they should give a wet mass within ±0.25 per cent, and the major errors usually occur in the calculation of the dry mass contained, as the moisture content of the concentrate can differ considerably, depending on the mineralogy.

The custody transfer for toll treated materials is governed by the commercial contract. This will specify which weight and analysis is used. The concentrate is weighed and sampled at loading/dispatch and upon receipt. It may be filter cake, which is dumped and stored in a shed (sampled by auger) or slurry which is pumped into storage tanks, usually using a dedicated sampling facility. Again, as far as the mass is concerned the major errors will be determining the dry mass.

Mass measurement of matte/intermediates

Converter matte is usually granulated and weighed on a platform scale into tote bags containing one to two tons each. These are transported in trucks to the BMR and are weighed on a weighbridge on dispatch and upon delivery weighed, offloaded, and each bag weighed to provide the 'Home and Away' figures. These checks should be within ± 0.2 per cent. However, the major error is likely to be moisture content as sometimes free water will seep from the bag, especially during transport, which will cause larger variances to be observed. Thus it is important that moisture samples are taken to reflect the material weighed.

Mass measurement of base metal products

These comprise nickel, copper, cobalt, and/or nickel sulphate or cobalt salts. The metals are weighed on platform scales and drummed, and the salts weighed and loaded into bags.

These procedures are usually well supervised as the material value is significant, and the weights should be accurate providing the correct procedures are followed, the scales checked regularly with certified check weights, and kept clean and in good condition. In the case of the metal salts, the same problems with the free moisture content are encountered as for the matte.

The mass accepted for payment will often be that of the customer and will be specified in the commercial sale agreement, as will procedures for settlement of differences.

Mass measurement of precious metal concentrate

Precious metal concentrate filter cake from the BMR is sampled and accurately weighed on small platform scales, usually after drying, in lots of about 20-30 kg, and weighed and sampled again in the PMR.

However, even after drying, it may contain small amounts of moisture or salts, which can cause the material to become sticky and difficult to sample. Handling of the concentrate occurs under continuous high security and multiple observers to reduce theft. However, this is still the major risk affecting the metal accounting in this area.

Mass measurement of precious metal products

These are all weighed very accurately under close supervision during packaging, again on dispatch, and at the customer, and the risk of errors occurring is very low.

Mass measurement of residues/dust losses/effluent streams

There is a wide range of materials (residues), especially from the BMR and PMR, that are sold, sent to specialist firms for toll recovery of the PGMs and base metals, or recycled internally to the appropriate plant in the processing chain. These can be relatively high in PGM grade, often contain toxic undesirable elements, and are difficult to sample to obtain the moisture content. A prime example is smelter reverts, where the stock and content are very inaccurate and can hide a multitude of sins. In addition, it can be a lengthy process before the recovered metal content is established, leading to significant quantities of metal 'in limbo'. If the material is circulated internally care must be taken that the mass accounting is consistent and that double accounting does not occur.

Measurement of relative density and moisture content

In the author's experience these are among the greatest sources of error in mass measurement for metal accounting, as they are often not measured but are assumed, especially in the case of ore feed and the estimation of stocks.

Mass measurement of stocks/in-process inventory

This is often the largest error in the mass measured for the metal balance, for the reasons pointed out above and the fact that it is virtually impossible to sample large stockpiles or materials such as reverts.

Although these errors are self-correcting and will emerge when the stocks are run to zero, they have been known to cause major write-offs or adjustments and to affect companies' annual financial statements. There have been improvements in these measurements but the ongoing management of these stocks is an area for further attention.

Stocktakes

Stocktakes, which periodically measure all material that is in a plant, are used to set the clock back to zero and confirm the comparison between actual and theoretical stocks. Stocktakes have a significant cost, due to their disruption of production, the involvement of technical teams, including outside consultants and auditors, and the large number of samples that are generated. The greatest disruption to production is usually in the PMR, where a so-called 'bubble' stocktake is carried out. This involves stopping the feed into the plant for a number of days to create the 'bubble', and then taking the opportunity to empty and clean as many of the reaction vessels as possible. This has the major advantage of satisfying the requirement of taking stock levels to zero, because the only truly accurate measure of stock is zero.

In the AMIRA Code, it is recommended that stocktakes are conducted at least annually, but on some operations they are conducted every six months and at others either annually or once every three years. The latter period has not been set only on cost or production factors but, because of careful measurements in previous stocktakes, it has been established that the criteria for the differences between the actual and theoretical stocks being within the required confidence intervals have consistently been met.

This highlights the necessity of establishing the actual variances of all components of the evaluation chain, namely mass measurement, sampling, and sample preparation and analysis, so that accurate confidence intervals can be calculated.

Toll smelting and refining

Standard commercial terms for concentrate toll treatment are based on the receiver's mass, moisture determination, and sample, with the sample being split and analysed at both the receiver's (toll smelter's) and the shipper's laboratories. On a prearranged date, the analytical results recorded by the two laboratories are exchanged and compared. If there is satisfactory agreement between the laboratories for each metal, settlement is reached for that particular lot. If the analytical results do not agree within specified limits, settlement will be delayed until the two parties have agreed a final value for each metal, either by negotiation or following analyses of the same sample by an independent umpire laboratory.

Are you getting the best possible value for your concentrate?

In the case of a junior platinum producer shipping concentrate to a smelter operated by one of the major producers, the shipper relies on the sample and mass measurement of the receiving smelter.

In order to eliminate bias or errors in the mass measurement, the concentrate producer must be entitled to inspect the receiving smelter's sampling equipment and procedures at any time and should have its own, similar sampling and mass measurement facility so that each dispatch can be sampled and weighed by the concentrate producer for checking purposes and to identify possible biases in mass measurement or sampling and sample preparation. This also provides protection to the concentrate producer, as it has been known for concentrate trucks to deliver their load to a smelter without the mass being measured, or without an accounting sample being taken, or with the accounting sample being contaminated or lost during the handling and preparation process. In this unlikely event, both parties can use the shipper's sample and mass measurement for settlement purposes.

The concentrate producer must also either have its own in-house laboratory, capable of analysing each payable metal in the concentrate to an acceptable level of accuracy, or enter into an agreement with a suitably qualified commercial laboratory to provide this analytical service. This is not always as simple as it appears, as many laboratories claim to be able to provide a reliable analytical service but, in fact, those that provide the best service are usually those already providing a routine analytical service to other platinum metals producers, so that their analytical procedures are correctly calibrated and set up to handle the type of sample delivered by the concentrate supplier.

Experience of round-robin analysis comparative exercises conducted amongst the platinum producers has shown this, whereas laboratories new to the industry have difficulty in matching the analytical accuracy and precision achieved by those serving the existing producers. A new producer setting up its own laboratory needs to be aware of this potential difficulty.

A similar problem relates to the identification of a suitable umpire laboratory. The most reliable laboratories will be those already engaged in the industry, usually operated by an existing producer, with little spare capacity for handling umpire analyses for third parties.

As a precursor to entering into a toll treatment agreement for their concentrate, it is essential that the smaller producers devote sufficient attention to setting up a metal accounting system. The system must be capable not only of measuring, sampling, and analysing their concentrate to be dispatched, but also of carrying out checks on weighing, sampling, and analytical precision and accuracy, both of their own system as well as that of the toll treatment operator, to ensure that, at all times, the accounting issues described in the previous sections are adequately covered. By doing this, producers will be able to ensure that they are obtaining a fair payment for their metal shipped and that they are receiving the maximum possible value for each shipment in terms of their toll treatment contract.

Splitting limits

The analytical splitting limits set out in the commercial toll treatment terms are usually based on accepted practice elsewhere in the industry. Obviously, to minimize the analytical and sampling risk associated with each concentrate dispatch, these limits must be kept as low as possible. However, in a normal distribution of analytical results, 95 per cent of all results should fall within two standard deviations of the true analytical value, and splitting limits are normally set to meet this criterion. Making them tighter than this results in too many analyses being disputed, causing delays in settlement, re-analyses, and the use of umpire analyses. It follows that the tightest splitting limits are achieved by laboratories that deliver accurate and precise analyses consistently.

In a toll treatment contractual arrangement, the contract will set down initial splitting limits, based on accepted practice elsewhere, but these should be reviewed on an ongoing basis, as analytical data from the laboratories becomes available. If the laboratories are performing well, it should be possible to reduce the splitting limits applied to the critical value metals, thus reducing the analytical risk associated with each metal dispatch. Conversely, if one of the laboratories is performing badly, it may become necessary to widen the splitting limits, increasing the analytical risk.

A simple example

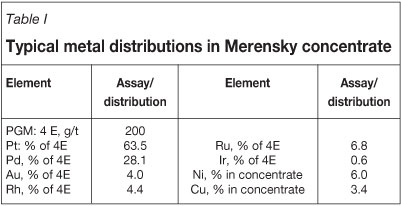

Consider the case of a small platinum metals producer producing 120 000 ounces of platinum per year in Merensky concentrate. Cramer (2008) quoted the figures in Table I as being typical for the metal distribution in such a concentrate.

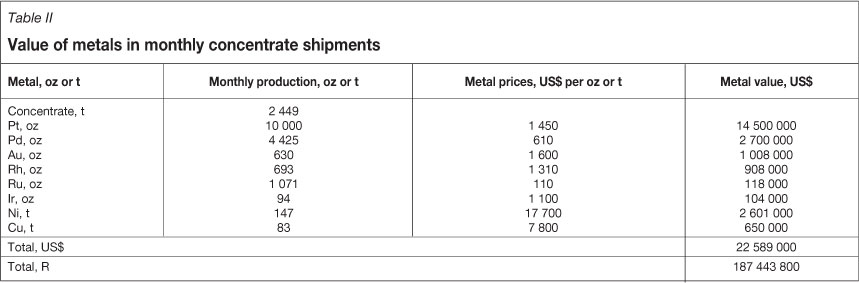

Table II shows the quantities and values of these metals in monthly concentrate shipments, obtained by applying the distributions in Table I and the metal prices shown in the Table.

As can be seen from Table II, the value of metal in the total monthly concentrate shipments is R187 million, using an exchange rate of US$1 = R8.20. However, Cramer (2008) also indicates typical smelting and refining commercial terms to give a net metal return of 83 per cent, so that the recoverable metal value in the concentrate would be R155.6 million per month, or R1 867 million per year.

The effect of an undetected bias of 1 per cent in the concentrate mass measurement would, therefore, be R1.56 million per month, or R18.7 million per year, either in favour of the concentrate producer or of the toll treatment operator.

A platinum producer operating at this level of production would be expected to dispatch between 80 and 90 tons of concentrate per day, typically in three 30-ton road trucks. Each truck would be weighed and sampled at the dispatching concentrator and at the receiving smelter and, to optimize analytical costs, the three truck batches would be combined to form an accounting lot for the day. Table III sets out the quantities and values of the metals in a 90 ton daily lot, and applies typical analytical splitting limits to show the effective risk associated with each dispatch.

Table III shows that the value of the typical daily concentrate shipment for a producer shipping 120 000 ounces of platinum per year would be US$831 000, or R6.814 million, using the metal prices and exchange rate quoted in Table II. The analytical splitting limits quoted are typical values used in toll treatment contracts and, as can be seen, vary according to the metal concerned, and the difficulty associated with the analysis of that particular metal.

The value at risk, due to the splitting limits, is divided equally between the two parties, so the total risk value for each metal would be double that shown in the last two columns of the table. It can be seen that the total value to each party of the risk associated with the analytical splitting limits of all the metals in the example used is R220 000, or 3 per cent of the total value dispatched.

As the table shows, the risk values vary from metal to metal depending on the quantity, price, and splitting limit for each metal, with platinum providing the largest component of the risk value. The amount of time and money devoted to reducing the splitting limits (and the associated risk) will depend on the priorities of the companies involved. An alternative approach would be to sample and analyse each truckload individually, to reduce the associated risk, and this would have to be compared with the additional analytical costs.

The purpose of this simple example is to illustrate the potential for significant financial losses through inadequate attention to the metal accounting aspects of toll treatment contracts and to the mass measurement, sampling and analysis highlighted previously.

Through the correct design and implementation of every aspect of the metal accounting system, these potential losses can be minimized and the risks associated with the transfer of concentrate to a toll treatment operation can be quantified and managed.

Applying the AMIRA Code

In general there has been good acceptance of the principles of the AMIRA Code by the established platinum producers, and where any shortcomings are noted efforts are made to either remove them or minimize their effects.

In sampling, sample preparation, and analysis:

In mass measurement:

![]() Conveyer belt weighers are 4- or 6-idler

Conveyer belt weighers are 4- or 6-idler

There are, however, still some notable aspects that need improving:

Thus, although there has been general acceptance of most of the principles of the Code, there are areas which have not been adopted. However, the real challenge for the smaller producers is to use the Code to ensure their metal accounting systems and procedures are in line with best practice and that the smelters receiving their concentrate also follow best metal accounting practices.

Summary and conclusions

Even before the development of the AMIRA Code, the platinum industry had, from necessity, developed their metal accounting systems to a high degree. But, rather like the ISO 17025 standard in the laboratories, the Code has provided a basis for the formalization of the metal accounting system and for indicating what the best practices are.

However, as in virtually all areas of the mining business, it is an area requiring continuous improvement, which the platinum industry has recognized and is pursuing. As stated in the previous section, some aspects of the Code have not yet been adopted by the major producers, while for the smaller producers, application of the Code can only benefit them in terms of improved accounting of the metals in their concentrate dispatches and operating efficiencies.

Acknowledgements

The authors would like to acknowledge that the basis of this paper has been derived from the consulting work they have conducted for a number of the platinum producers.

References

AMIRA International. P754: Metal Accounting; Code of Practice and Guidelines: Release 3. Melbourne, Australia, Feb. 2007. [ Links ]

Cramer, L.A. What is your PGM concentrate worth? Third International Platinum Conference, 'Platinum in Transformation', Sun City, South Africa, 5-9 October 2008. Southern African Institute of Mining and Metallurgy, Johannesburg, 2008. pp. 387-393. [ Links ]

Gaylard, P.G., Morrison, R.D., Randolph, N.G., Wortley, C.M.G., and Beck, R.D. Extending the application of the AMIRA P754 Code of Practice for metal accounting. Fifth Southern African Base Metals Conference, Kasane, Botswana, 27-31 July 2009. Southern African Institute of Mining and Metallurgy, Johannesburg, 2009. pp. 16-38.

© The Southern African Institute of Mining and Metallurgy, 2013. ISSN 2225-6253.

This paper was first presented at the 5th International Platinum Conference 2012, 18-20 September 2012, Sun City, South Africa.

{kind=link}

{kind=link}