Services on Demand

Article

English (pdf)

English (pdf)

Article in xml format

Article in xml format Article references

Article references

Indicators

Related links

-

Cited by Google

Cited by Google -

Similars in Google

Similars in Google

Share

Permalink

PermalinkJournal of the Southern African Institute of Mining and Metallurgy

On-line version ISSN 2411-9717

Print version ISSN 2225-6253

J. S. Afr. Inst. Min. Metall. vol.113 n.1 Johannesburg Jan. 2013

MINERAL ECONOMICS

Nationalization: an analysis of the competing interests of capital, labour, and government

B. Sergeant

Freelance Mining Journalist/Writer

SYNOPSIS

Any study of the contentious subject of nationalization can ultimately be reduced to a sombre analysis of the simultaneous, and very different, interests of capital, labour, and government. Each of these interests attempts to maximize its objectives, subject to checks and balances provided, in an ideal system, by a country's executive government, legislature, and judiciary. Where even one of the three interests goes out of control, the consequences can be disastrous. The case histories show that when this occurs, the most common culprit is government, or its proxy, such as a dictator.

At the other extreme, the case studies indicate that the optimum outcome occurs when capital, labour, and government are 'ring fenced' from each other: each enjoys its rights, but is also subject to duties. 'Conflicts of interest' between the three entities are ideally avoided to the maximum possible extent.

The case studies include several salient instances from both the DRC (Gécamines, La Générale des Carrières et des Mines) and Zambia, along with Ghana and Chile. Further instances are examined in South Africa (gold), India (Coal of India), Brazil (Petrobras), Venezuela (Petróleos de Venezuela), Sweden(Luossavaara-Kiirunavaara Aktiebolag), Mauritania (Société Nationale Industrielle et Minière), Norway (Norsk Hydro), Botswana (Debswana), and Namibia (Namdeb).

The article concludes broadly that South Africa's minerals sector is not ready for nationalization.

Keywords: nationalization, sustainability, capital, labour, government.

Introduction

Any study of the contentious subject of nationalization can ultimately be reduced to a sombre analysis of the simultaneous, and very different, interests of capital, labour, and government. Each of these interests attempts to maximize its objectives, subject to checks and balances provided, in an ideal system, by a country's executive government, legislature and judiciary.

A country experiencing general prosperity is also a country where conflicts between the three interest groups are benign, if not 'healthy'. Where one of the three interests establishes itself as totally dominant, and the rule of law is suppressed, prosperity falters and eventually fails; misery sets in. In most cases of abuse, the culprit can be identified as executive government or one of its proxies, such as a dictator.

Case studies of nationalization are almost as varied as the number of countries found around the world. As such, there is no 'general case' of nationalization; similarly, there is no polemic for either extreme. It is more useful to consider the circumstances that are sometimes found where one or more of capital, labour, or government runs out of control.

Where the executive government establishes itself as dominant party, and checks and balances fail to counter excesses, capital and labour are forced into complete subservience. Capital, which is mobile, readily and quickly shifts to other jurisdictions. Labour, when it is unable to migrate, becomes impoverished and powerless. A country in such a situation can easily slide into the classification of a 'failed state'.

Prior to extraction and basic processing, the vast majority of mineral assets are immobile. For this reason, mineral assets have long ranked as favourite targets for predatory executive governments. It is far easier to spin the seizure of mineral assets than the seizure of an individual business genius, who anyway is likely to have long fled.

As a rule, nationalization of mineral assets eventually fails mainly because predatory executive governments resist, if not prevent, appropriate reinvestment in the formerly productive mining assets. In this scenario, the assets eventually fail. The long road to failure is accompanied by a steady exit of personnel, weighted towards the more highly paid, and skilled, executives and employees.

This period is most often followed, as seen from the early 1990s, by privatization, or reprivatization, aimed at attracting private sector capital in significant quantities. Such capital is most readily attracted, first and foremost, by high-quality and large mineral resource deposits, which are seen as mitigating other risks. The inward migration of capital is further encouraged by reforms, whether promised or real, aimed at guaranteeing the norms associated with private enterprise, such as security of tenure.

However, where previous elites, typically members of the former predatory executive government, are not held in check, the privatization process itself may be severely undermined by corruption. One such practice involves selling potentially valuable assets more than once.

Mining enterprises majority-owned and operated by private enterprise tend to be efficient, espousing, and practicing business models aimed at optimizing profits. In the majority of cases, private enterprise robustly follows a strategy of expansion, usually nationally, if not also internationally.

In countries where private enterprise is allowed to thrive, labour and government always benefit. If the general environment is conductive to prosperity, finer checks and balances often flow from the ventilation of issues by the likes of NGOs and other interest groups. In contrast, state-owned companies of any kind are by definition immune from takeover. This characteristic tends to spawn complacency, which in turn creates many ills.

In practice, mining companies contribute significantly to stakeholders other than shareholders and financial institutions (which provide debt finance). The value chain generated by mining enterprises is often understated and misunderstood. Beyond the societal benefits for communities, and the long value chains in and around mineral extraction enterprises, deeper analysis also shows that mining companies contribute significant imposts, either directly through company tax or indirectly through excise and customs duties.

Close examination shows that the only additional benefit available to a government after nationalization of a profitable mining enterprise would be the dividends that the entity would otherwise have paid to its shareholders. The cost of acquiring such assets, at market values, can be impressive. Over the past few years, there have been occasions when the market capitalization (value) of BHP Billiton, the world's biggest diversified resources stock, has comfortably exceeded US$200 billion. Few governments in the world could afford that. In terms of forward dividend receipts, based on BHP Billiton's current dividend yield, it would take decades for the outlay to be recouped. Factoring in the time value of money, even at today's rates which are around historic lows, it would take more than a century - in other words, forever.

Since the start of the so-called commodities supercycle during 2001, both private enterprise and governments have expressed and shown increasing interest in claiming larger chunks of an apparent new-found bounty which seems, certainly to the uninitiated, to be as easy to harvest as proverbial low-hanging fruit. A closer examination of the subsectors within the overall minerals complex indicates, however, that above-trend profit margins have only been produced by enterprises in oil and gas, iron ore, copper, and coking (metallurgical) coal. Over the past five years, however, the hydrocarbons complex has been heavily impacted by the commercialization of new-found deposits through the combined techniques used in what is generally referred to as 'fracking'.

Leaving hydrocarbons aside, mineral extraction margins over the past decade have been poor, and even abysmal, in a number of subsectors, not least aluminium, the number two base metal after copper. On this score, it can be noted that a long-term positive price trend does not automatically translate into above-trend margins. Thus, the gold bullion price may have performed magnificently since 2001, but average margins at gold miners have risen at a lower rate, mainly because gold mining is more vulnerable to input cost increases, compared to bulk commodities such as iron ore.

As such, each minerals subsector can be regarded as idiosyncratic, subject to varying and often erratic and unpredictable changes in both supply and demand, and as subject to varying outcomes stemming from exogenous input-cost price increases. Governments, however, are wont to see these differentiations as unimportant, and even as no obstacle, when viewing extractors of mineral resources as targets for various agendas. In the private sector, enterprises that have suffered the ignominy of 'being in the wrong commodity at the wrong time' are weeded out; marginal cases, given some luck, are taken over by entities with larger capital and skills resources.

Examples of value added and wealth distribution

For firms occupying the private enterprise space, is there anything such as 'business as usual?' For BHP Billiton, the world's biggest diversified resources group (involved in extraction of both minerals, and oil and gas), it can be described as 'business unusual'. In its most recent annual 20-F filing with the Securities and Exchange Commission in Washington, BHP Billiton stated that 'as at 30 June 2012, we had a market capitalisation of approximately US$160.6 billion (2011: US$233.9 billion)'. This ranks the group as one of the ten most valuable listed business enterprises, of any kind, in the world. BHP Billiton reported a net operating cash flow for fiscal 2011 of US$24.4 billion (US$30.1 billion), profit attributable to shareholders of US$15.4 billion (US$23.6 billion), and revenue of US$72.2 billion (US$71.7 billion). Referring to its 2012 financial year, BHP Billiton reported that it had 'approximately 125 000 employees and contractors working in more than100 locations worldwide'.

The biggest and most successful mineral extractors can be regarded as custodians of low-cost, long-life, high-grade, world-class assets, but again, idiosyncrasies are never far away. BHP Billiton's remarkable geographical and commodity diversification belies the significant variations between bottom-line contributors. Aluminium, reflecting the experience of the broad global subsector, has been disappointing. A substantial portion of BHP Billiton's profits and operating cash flows are contributed by four subsectors: iron ore, oil and gas, copper, and coking coal. The majority of the group's iron ore and coking coal is produced in Australia.

In theory, BHP Billiton can be regarded as an attractive target for nationalization, whether as a whole, or as to subsectors, or, more likely, geographic subsectors. Nationalization has been shown to stand on two main pillars. The first is the status and prestige, whether perceived or actual, that goes with government ownership of mineral extraction firms. Second, the attraction of the additional monies, real or imagined, that government can appropriate from mineral extractive firms.

An examination of nationalization across the world over the past century or so suggests that reinvestment, and capital expenditure more generally, are the most abused factors in cases where nationalization fails. Given its highly successful business model, and a leading position in the world's most profitable mineral subsectors, BHP Billiton provides a useful base case for examining the use of cash flow for reinvestment and capital expenditure. Over the past five calendar years, including 2010, BHP Billiton produced operating cash flows of approximately US$100 billion.

It can be noted that, like any other private sector enterprise, BHP Billiton has three basic options for sourcing cash. First, operational cash flow is produced from day-today operations. Second, cash can be raised by securing debt, mainly from banks but also sometimes by way of issuing corporate bonds. Third, capital can be raised by issuing fresh shares to investors, in the form of a rights issue. Asset sales provide a fourth potential source of cash. Of these four classifications, there is no question that in the longer run, the most attractive enterprises are those which produce sustainable growth in operating cash flows.

Of the approximately US$100 billion operating cash flow produced by BHP Billiton over the past five years, nearly half was spent on capital expenditure, viz., stay-in-business capital expenditure (reinvestment), and also capital expenditure at new ventures. Most of the balance was paid directly to shareholders as dividends, or indirectly awarded to shareholders through the mechanism of stock buybacks.

Capital expenditure at appropriate levels is crucial to sustainability in minerals extraction. Stay-in-business capital expenditure aims at ensuring optimal working conditions for employees, and at maximizing efficiencies. Capital expenditure on new ventures aims at replacing depletion, and also at generally expanding group production. Minerals extraction is highly capital intensive, creating and sustaining a very substantial value added across multiple supply industries.

Sasol, the Johannesburg-based energy company, provides a useful example of how stakeholders in a mineral extraction enterprise carve out monetary benefits. The group, which mines coal, is far better known for its production of synthetic liquid fuels. Sasol is a particularly important example of a mining company that also 'beneficiates', or 'adds value' to an extracted mineral. The majority of mining companies prefer to remain 'upstream'; among the exceptions, Alcoa can be found all along the value chain from mining of bauxite to producing highly specialized fabricated aluminium products.

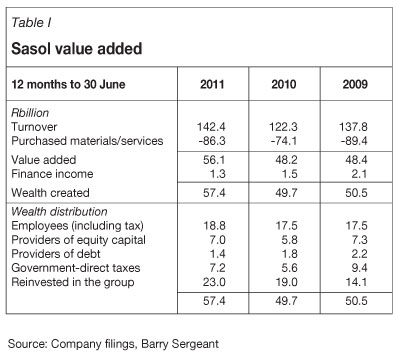

Sasol, originally founded as a state-sponsored enterprise in 1950, published a 'value added' statement for fiscal 2011 which indicates wealth creation of R57.4 billion. Of this, nearly R19 billion was paid to employees; R23 billion was reinvested in the group. (Table I)

At the end of its 2011 financial year, Sasol had 33 708 employees on its payroll. These employees generated average per capita turnover of R4.2 million, added value of R1.7 million each, and created also R1.7 million of measurable wealth.

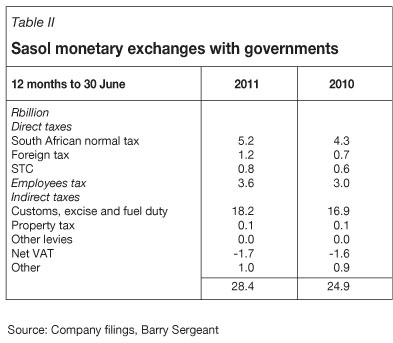

During 2011, an amount of R7 billion was paid to 'providers of equity capital', that is, cash dividends paid to shareholders. In the event of nationalization, this is the only additional amount that government would extract from Sasol. It is noteworthy that Sasol paid R7.2 billion in direct (income) tax, slightly more than the amount returned to shareholders. It is equally noteworthy that during fiscal 2011, Sasol's enterprise and products generated R28.4 billion in taxes of various kinds. The biggest contributor, at R18.2 billion, was appropriated from consumers by way of customs duty, excise, and fuel duty. If Sasol was nationalized, all else being equal, Sasol would not per se generate any further imposts for government. (Table II)

Sasol also provides South Africa with an enormous 'hidden' benefit, by way of its liquid fuels substituting for the import of further liquid fuels. This means that the country's foreign exchange reserves benefit to the tune of tens of billions of rand a year. South Africa produces no crude oil of its own.

Cyclicality

Mineral extraction firms, whether owned by private enterprise or governments, are subject to the vagaries of cycles, most directly in the form of changes in the pricing levels of commodities. The issue of input costs is also subject to cyclicality: where commodity prices rise, the general case for the past decade, most of the capital costs for building and running a mineral extraction enterprise also increase.

In the private sector, mineral extraction firms that are unable to survive a downcycle are either taken over, or closed down. Where mineral extraction firms are government-owned, downcycles are typically countered by injections of government-sponsored debt, which can sometimes lead to heavy calls on taxpayers. Experience has also shown that employees of government-owned mineral extraction firms enjoy more bargaining power than their counterparts in the private sector. This dynamic typically translates to yet further calls on taxpayers: private sector enterprises are better able to optimize risks and costs.

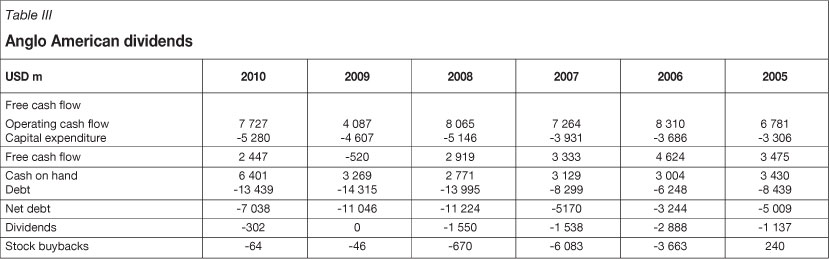

Cyclicality can produce dramatic results, whether welcome or otherwise. In the case of Anglo American, a medium-sized transnational miner, operating cash flow nearly halved to US$4.1 billion during 2009, in the aftermath of the crisis that gripped markets during 2008. For the first time in the nine decades of its history, Anglo American passed its dividend during 2009. Just two years before, Anglo American had paid cash dividends of US$1.5 billion, and simultaneously expended US$6.1 billion on stock buybacks. The group resumed dividends during 2010, after devoting substantial chunks of its operating cash flows to reducing debt (Table III).

Nationalization in action

The Democratic Republic of Congo

The République démocratique du Congo (DRC), previously Zaïre, provides one of the most extreme examples of nationalization. In 1965, Joseph-Désiré Mobutu, known by other names, most commonly Mobutu Seso Seko, assumed the presidency. In May 1997, he fled the country and was replaced by Laurent-Désiré Kabila, who was later assassinated by one of his own bodyguards in 2001, and replaced in turn by his son, Joseph, who has remained in power.

In 1966, Union Miniere du Haut Katanga, the private enterprise mining company that operated in the DRC's Katanga Province from 1906, was nationalized and replaced by the state-owned Gécamines, La Générale des Carrières et des Mines. Even after nationalization, however, the mines were managed by contracted foreign nationals. Between 1975 and 1990, copper production in the DRC ranged broadly between 355 000 and 480 000 tons a year. As time went by, Mobutu's demands for cash from the mines increased. The major casualty was reinvestment capital expenditure, mainly for maintenance. The mines were stretched to the point where production could only occur at the margin. By 1996, production had plummeted to less than 30 000 tons a year.

Mobutu's 'defences' in every sense of the word became increasingly fragile and within years, particularly from 1998, the country was engulfed in a regional war that would claim the lives of millions. The DRC's collapse into a failed state, mainly at the hands of Mobutu, was accelerated by the mine collapse in 1992 at Kamoto (which can today be found in the stable of Katanga Mining, listed in Toronto and London). Gécamines had suffered a 'brain drain' for decades, and was persistently raided by Mobutu to the point where capital expenditure was no longer available from internal cash generation. By the early 1990s, Gécamines was gasping under net debt running into billions of dollars. Despite a number of privatization deals, starting with certain actions taken by Laurent-Désiré Kabila, Gécamines continues to struggle with a mountain of debt.

The DRC is a specific country example where an executive government, mainly in the form of Mobutu, a dictator, exhibited absolutely no respect for capital or labour. It took many years to ruin the copper-cobalt mines. This was less a gradual process than a tribute to the legacy that was created by Union Minière, which had built world-class mines, and operated a giant enterprise of magnificent efficiency. If anything, the mines were over-capitalized, as if built to counter decades of mismanagement. Earlier in this decade, the Kamoto operations and the adjacent KOV (Kamoto East, Oliveira, Virgule, and FNSR orebodies) operations, now housed within Katanga Mining, resembled one of the largest scrapyards in the world, and, certainly, the world's largest scrapyard without any customers.

Beyond mining, Union Minière had been at the forefront of building Africa's most extensive rail network, centred on Katanga junction. Railways ran to the west coast of Africa, to two ports on the east coast, and to South Africa. A line was also built to the north in the DRC. The rail network was also ruined, though various sections have benefited from refurbishment over the past few years.

The Mobutu legacy permeated everything in the DRC, a country the size of Western Europe. In a specialist report1 dated May 2008, the World Bank captured a long timeline in the DRC:

'Throughout its modern history, the people of the Congo have been exploited by slave traders, King Leopold of Belgium, mining companies in colonial times, and, most of all, the kleptocracy of the Mobutu years. Taking inspirationfrom this history and leadership, a culture of rent seeking, corruption, and impunity are deeply engrained in DRC. Rent seeking takes many forms, including offers or solicitations of bribes and illicit payments to or by government officials; fraudulent declarations to the tax authorities; embezzlement of state funds; conflicts of interest of officials who have an ownership stake in companies doing business with the government; inappropriate use of position to influence government decisions; and others. The pervasive culture of corruption exists at every echelon of Congolese politics and government administrative services. For those lowest in the hierarchy, such as a customs official who has not been paidfor months, taking a bribe is a matter of survival. For more senior members of the hierarchy, vast sums are said to find their way to offshore bank accounts or property investments in South Africa, Europe, or elsewhere'.

As mentioned, the DRC exhibited an extreme form of nationalization, one that provided the rotten foundations for a system that developed into a form of extreme corruption that could take decades to 'fix'.

Zambia

In 1968, the-then president of Zambia, Kenneth Kaunda, complained heavily that from Zambia's independence in 1964, the two private sector miners, Roan Selection Trust and Anglo American, had underinvested in the country's copper mines. In turn, the companies complained that Zambia's royalty system had developed to the point where it dissuaded investment.

This dispute, which was never resolved, graphically demonstrates the classic government vs. capital conundrum. In 1969, the Zambian government responded by announcing nationalization of the mines. At this time, Zambia was classified as a middle-income country, with one of the highest GDPs in Africa, three times that found in Kenya, twice the level in Egypt, and higher than any of the GDPs of Brazil, Malaysia, Turkey, and South Korea. This was a time when Zambia was exceptionally prosperous.

In terms of the nationalization in Zambia, all rights of ownership of minerals as well as exclusive prospecting and mining licenses reverted to the state. Mining companies were forced to surrender 51 per cent of equity in all existing mines to the state, albeit in return for a determined quantum of compensation. This was used by Anglo American to establish its secretive offshore operation, Minorco, which joined De Beers as part of Anglo American's tripartite family of top companies.

In 1982, the two nationalized Zambian copper companies were merged to form Zambia Consolidated Copper Mines (ZCCM). On the issue of cyclicality, it can be noted that copper prices collapsed after the first oil crisis in 1974, and again after the second oil crisis in 1979. As the relationship between government, capital, and labour steadily broke down, copper production in Zambia collapsed from a high of 750 000 tons in 1973 to 257 000 tons in 2000.

By the early 1990s, in line with most countries across Africa, Zambia recognized the potential benefits of revitalizing collapsed mining extraction enterprises. London-and Toronto-listed First Quantum Minerals acquired Bwana Mkubwa in 1996. The mine's state of dereliction and apparently hopeless future left it outside the mandate of the copper industry privatization initiated by the Zambian government. The government did not want so much as a single share in Bwana Mkubwa. Located in the far north of Zambia, Bwana Mkubwa exhausted the last of its own ore reserves in mid-2002; those 'reserves' in any event were poor-quality tailings from previous operations; the mine had been worked on and off since its discovery in 1902.

During 2000, mindful that Bwana Mkubwa would soon exhaust its ore reserves, First Quantum 'rediscovered' Lonshi, just across the Zambian border in the DRC. Lonshi had first been found by Belgian geologists in the 1930s, but had never been worked. First Quantum sunk the first modern drill holes into Lonshi in November 2000, and commissioned the US$25 million mine just eight months later. It was a relatively small, but high-grade, surface deposit that extended underground. Lonshi was the first greenfield copper mine built on the Copperbelt in 33 years. Nationalization on both sides of the Copperbelt, in Zambia and the DRC, had effectively terminated all potential initiatives to build new mines; strenuous efforts were instead focused on ruining existing mines.

First Quantum started mining at Lonshi in August 2001; a 36 kilometre laterite road, built by the company, was used to haul ore from Lonshi to the established processing facilities at Bwana Mkubwa. First Quantum also built the first big new Zambian mine at Kansanshi, at a deposit known since 1899. Copper prices were not assisting. In 2002, Anglo American quit Zambia Copper Investments (ZCI) and its main interest, Konkola Copper Mines, at a cost of US$34 million, in addition to a US$353million write-off taken during 2001. After Anglo American quit Zambia for the second time, this time voluntarily, the copper price kicked up in the early stages of what would prove to be a longer term sustainable bull market.

Over the past decade, boom times have once again returned to Zambia, fuelled by significant private sector investment in the mining sector. There have been a number of heated debates over taxation and royalty levels, but the word 'nationalization' has apparently been banished from the national vocabulary.

Ghana

Ghana's first commercial mining event can be traced to March 1890, when two merchants from the country's Cape Coast, Joseph Ellis and Chief Joseph Biney, and their accountant, Joseph Brown, secured mining concessions of over 25 900 hectares in and around Obuasi. In due course this would emerge in what has long been known as Ashanti Goldfields, listed for the first time in London in 1897.

In 1968, Lonrho, listed in London and Johannesburg, acquired Ashanti Goldfields and took the entity private. In 1972, the independent government of Ghana seized a 55 per cent stake in the main Ashanti Goldfields asset, Obuasi, after a coup d'etat led by Colonel Ignatius Acheampong toppled K.A. Busia's democratically elected regime. Amid comprehensive nationalization of assets of every kind, the state nationalized 55 per cent of all mining companies, but Lonrho retained an equity stake in Obuasi and remained, by and large, in control of day-to-day operations.

Ashanti Goldfields was listed for the second time, again in London, during 1994. The Ghanaian government effectively re-privatized Ashanti Goldfields by selling 25 per cent, reducing its equity stake in Ashanti Goldfields to 30 per cent while, at the same time retaining a 'golden vote' in the equity of the company. Ashanti Goldfields later merged into AngloGold, already one of the world's biggest gold miners, creating AngloGold Ashanti.

Ashanti Goldfields had remained intact after nationalization due mainly to the professional management administered by Lonrho. By the early 1990s, all other gold mines, less able to resist government meddling, had been comprehensively run into the ground. During 1993, Gold Fields, one of the world's largest gold miners, acquired a 71 per cent stake in Tarkwa for the relative pittance of US$10 million. Tarkwa was producing a few thousand ounces of gold a year. The mine was in effect rediscovered as Gold Fields established a mineable surface resource holding significant quantities of gold.

Today Tarkwa ranks as one of the world's biggest open-cut gold ventures, producing a sustainable 750 000 ounces of gold a year. Private sector gold mines re-emerged elsewhere across Ghana, initially with brownfield startups such as Tarkwa, and progressing to greenfield developments, such as the Ahafo cluster, under the considerable balance sheet and expertise of Newmont, one of the world's biggest gold miners. For some years now, Ghana has ranked as Africa's second-largest gold producer, after South Africa, and ranks among the top ten in the world.

There has also been strong interest in developing other types of mines in Ghana, but the country's limited infrastructure remains a constraint. Among miners, those digging for gold are best able to operate in such country environments, mainly because the final product can be sent to market by helicopter.

Chile

During an interview in November 2010, South African minister for economic development Ebrahim Patel stated that:

'We've looked to the example of Chile, it's a very, very interesting example because Codelco, which is the Chilean state-owned mining company, is a significant player in the copper market and not only do they run a very efficient operation but the resources that they generate is important to the fiscus and it's also helped to manage their sovereign wealth fund.. That has been an instrument that the Chilean state could use to help manage their currency. I think the important thing is that whilst we raise the issue of a state-owned mining company, we're also very, very clear in the growth path that we see a large and very important private sector in mining and that the state has a role but the critical jobs, the large number of jobs, most of the investment will in fact be in the private part of the mining sector. We see partnerships that can be built between a state-owned company and private mining houses'. With respect to the minister's selective analysis, several issues are conflated. Codelco, or Corporation Nacional del Cobre de Chile, which has for many years ranked as the world's biggest copper miner, was 'nationalized' in 1971 under extraordinary circumstances. During the excessively repressive regime of president Salvador Allende's government, it was agreed that Codelco would part-fund the country's military.

This agreement was formalized, and remains an impediment to any fundamental changes to Codelco's business model. A month or so before the interview with Minister Patel, the London-based newspaper The Economist reported, in essence, that Codelco was bound for change that would lead it away from its nationalized state. During the 2009 election campaign, Sebastian Pinera, who ended up as Chile's president in March 2010, often criticised Codelco, 'for its inefficiency, griping over its stagnant output and climbing costs', echoing concerns that have been directed at so many nationalized mining extraction firms around the world.

Codelco's share of Chile's copper output had dwindled from 75 per cent in 1990 to 32 per cent in 2009, as private sector mining enterprises boomed across the country. Pinera told The Economist that 'we need to create a new Codelco . . . It needs funds, new organisation and new management'. He favoured Codelco's partial listing on the stock markets. Diego Hernandez, Codelco's new chief executive, announced objectives that included the implementation of a proposed five-year US$15 billion investment plan, including a new mine and the expansion of El Teniente and Chuquicamata. Some of Codelco's mines have been in production for more than a century.

Hernandez was previously an executive at BHP Billiton, which is the major shareholder in Chile's Escondida, the world's biggest copper mine; the other main shareholder here is Rio Tinto, another transnational miner. In line with so many other nationalized mining extraction companies, Codelco has accumulated a substantial legacy of jobs unlikely to be tolerated by a competitive private sector enterprise. Codelco's official employee count cannot disguise more than 20 000 people it employs under a special 'subcontracts' law, and a remarkable 25 000 or so who work as 'investment company contractors'.

Over the past few years, Codelco has raised several billion dollars by selling corporate bonds into private sector markets.

Some other countries

In South Africa, the ANC Youth League, which has promoted the notion of the nationalization of mines and other industries, faded heavily after the ANC's Mangaung elective conference in December 2012. Not only did the conference remove the notion of nationalization, but the very future, if any, of the ANC Youth League itself was put in balance. During a lengthy period of promoting the notion of nationalization, the ANC Youth League had focused heavily on a purported optimal outcome for nationalization, without explaining what means would be used to achieve that end. The empirical evidence shows, certainly in the South African case, that a lack of nationalization has delivered many benefits over many decades.

The tripartite meeting of the three factors of capital (both monetary and human), government, and labour itself is well represented by examining Johannesburg, where gold was first commercially discovered in 1886, close to the present-day central business district. As it turned out, the Witwatersrand continues to rank as the world's biggest goldfield, albeit that production has declined since peaking in 1970 at 1 000 tons. Production in 2012 is unlikely to exceed 200 tons.

Within months of the discovery of the goldfields, the abundant riches of the Witwatersrand attracted some of the darker forces of human nature. In 1891, the Land en Volk, an opposition newspaper, accused President Paul Kruger of trying to divert the railway line from Pretoria to Delagoa Bay over land owned by his relatives and friends. The newspaper complained that 'The friends of the President are becoming rich while the burghers sweat'. Even the pro-government Pretoria Press conceded 'widespread corruption in the civil service'. Money talks, for good or ill; within years, war would break out.

Today, Johannesburg ranks as Africa's financial powerhouse. It ranks as the biggest city in the world absent a position on a major river, alongside a large lake, or on a seacoast. It boasts the world's biggest non-commercial manmade forest. Above all, perhaps, Johannesburg is diversified in every sense. It stands as a tribute to the possibilities of the long-term survival of the conflicts of capital, government, and labour.

Royal Bafokeng Platinum

The broader South African economy continues to face many challenges, not least the debilitating and deepening crisis of stubborn unemployment. Along with other negative features, not least the perception of endemic corruption, the country is vulnerable to populist agendas. Within this context, the nationalism 'debate' has seeded many unhelpful exchanges. In November 2010, Zoli Diliza, CEO of the South African Chamber of Mines, reacted to an ANC Youth League statement by in turn stating that 'the contribution that the League makes to sensible and enlightened debate on issues of national importance is lamentable and is consistently characterised by a crude proclivity to descend into abusive and intimidatory rhetoric'. This, during a week when the black-controlled Royal Bafokeng Platinum published a prelisting statement ahead of it joining the listings on the Johannesburg bourse.

The prelisting statement said in part that 'a faction of the ruling political party in South Africa, the youth league of the African National Congress, has recently called for the nation- alization of all mines in South Africa. The government of South Africa has publicly stated, in response to these calls, that there is no present intention to consider nationalization or to change the existing government policy on this issue in the short, medium or long-term'.

Coal of India

For its part, government has failed to reassure investors, if only by declaring - for example - that it will support any private enterprise in any way possible. The ANC Youth League defiantly stated that it has 'made public many case studies of countries that have greatly succeeded with nationalization across the world'. No such case studies were, in fact, made available. As 2010 drew to a close, Coal of India, the world's biggest coal producer (with about 400 000 employees), listed, as the Indian government moved yet another asset towards privatization.

Petrobras

Also towards the end of 2010, Petrobras, in which the Brazilian government effectively holds a controlling stake, raised US$70 billion in cash from private investors: Petrobras is listed. The event ranked as the biggest single capital raising in the history of world stock markets, places where governments, as such, are not welcomed. Where, however, investors in stock markets are satisfied that appropriate safeguards are built into a listed entity, the reaction is generally supportive. The advisors to Petrobras would have toiled no end to ensure that the capital raising was enthusiastically received; the keynote is that Petrobras is independently managed, and as such, follows a business model associated with a competitive private sector enterprise.

Venezuela

The ANC Youth League has often cited Venezuela as a supportive example of nationalization. Petróleos de Venezuela (PDVSA) was nationalized - not for the first time - in 1976. Hugo Rafael Chavez Frias, elected country president in February 1999 and survivor of a coup d'etat in 2002, 're-nationalized' PDVSA after a crippling strike across December 2002 to February 2003. Since the first nationalization of PDVSA, Venezuela's oil output has steadily fallen, despite a sustained bull market in dollar oil prices over the past decade. PDVSA has persistently and increasingly failed to address overall skills challenges within the group. In line with so many other nationalized mineral extraction firms, PDVSA has been milked of profits at the expense of reinvestment, never mind expansion. In 2010 Venezuela accepted a US$20 billion loan from China to recapitalize its oil sector. The sector continues to labour under an inefficient business model, and technical challenges presented by its oil fields it wishes to move towards production.

In recent years, the country's president has been seen nationalizing anything from iron and aluminium plants to transportation firms and food companies. In most surveys of Latin America, Venezuela ranks as the most unstable country, and amongst the most disturbed in the world. The country harbours one of the highest murder rates on the planet. The inflation rate is amongst the highest anywhere, and the country's multi-tier currency system has collapsed.

Substantial oil assets across the world, not least in Saudi Arabia, the leading producer, are state-owned, but professionally managed. Successful state-owned oil producers readily accept, and professionally manage, the competing interests of capital, government, and labour. Countries as different, as to history, as Norway and Angola have shown a willingness and ability to manage oil-producing assets on a long-term sustainable basis, optimizing production while at the same time taking specific action on underlying efficiency factors such as reinvestment and expansion.

LKAB and SNIM

Another example of vastly differing countries with successful histories in state-owned mineral extraction companies can be found in Sweden and Mauritania. In Sweden, LKAB (Luossavaara-Kiirunavaara Aktiebolag) has mined iron ore since its establishment in 1890. The firm has been 100 per cent state owned since 1950, after it virtually collapsed owing to falling prices following the end of the Second World War.

In Mauritania, SNIM (SociétéNationale Industrielle et Minière) was established, under another name, in 1952. SNIM has been state-owned from 1974, but changed its legal status in 1978, becoming semi-public, with the intention of attracting capital from the private sector. Today, the government of Mauritania continues to hold the majority of equity in SNIM, to the tune of 78 per cent.

In the cases of both LKAB and SNIM, governments over very long periods have respected the imperatives of capital and labour as different but essentially equal. These may be clichéd cases of 'all parties win', but neither case proves a general case that can be applied indiscriminately to nationalization as a whole, in all countries, at all times. The more valuable lesson from both LKAB and SNIM is that where executive government regards itself as accountable, and is seen to act accordingly, mineral extraction enterprises have more than a chance of long-term sustainable existence. There may be historic reasons, as in the case of LKAB, for nationalization, but government should constantly re-examine whether it wants to retain control of assets that may eventually become moribund, compared to the possibilities under private enterprise management.

Norsk Hydro

Norway's Norsk Hydro, the aluminium maker, has also been cited as an example of successful nationalization. Once again, the specifics paint a different picture. Norsk Hydro's biggest cost input, electricity, benefits from state-owned hydroelectric facilities in Norway. In effect, the benefits of low-cost electricity are recycled back to Norwegians via the government's stake in Norsk Hydro.

Most of Norsk Hydro's baseline material input, bauxite, is mined in Brazil, Jamaica, and Australia, rather than Norway. The Norwegian government holds directly and indirectly about half the issued shares in Norsk Hydro. 'The state', declares Norsk Hydro, 'has never taken an active role in the day-to-day management of Hydro and has for several decades not disposed of any of the ordinary shares owned by it, except when participating in the share buyback programs'.

Once again, here is an example of an independently managed and professional firm. There is no general objection to government-sponsored investment, as seen in the growth over recent decades in sovereign funds. These are often associated with countries that have produced substantial cash surpluses from state investment in the mineral resources sector. Most of the oil-rich Middle Eastern nations own substantial sovereign funds, financed principally from boom time oil profits. As a rule, sovereign funds seek passive investments, preferring the role of a sleeping partner, in order to avoid conflicts, real or perceived. Sovereign funds aim, broadly, to enhance a nation's wealth, as opposed to scoring political points of any kind.

The jabbering of politicians

That can be contrasted, sharply, with the potentially harsh world of nationalization, where politicians have been known to manipulate situations, usually under the banner of 'national interest'. Where nationalizations proceed in the wake of an exogenous commodity price collapse, as in the case of LKAB, successful government can be recognized when it respects its own discrete interests as separate to those of capital and labour. Populist political interests that promote nationalization for political gain, or other hidden agendas, tend to conflate the situation at hand. When lobbying, such interest groups will always find reasons to explain away nationalization cases that failed.

The ANC Youth League, for example, claims to have 'scientific evidence on why nationalized mines in Zambia could not succeed', referring to price cyclicality. At the same time, there was no explanation for why Codelco managed to weather periods of poor copper prices, and likewise no reference to significant private sector producers, such as Freeport McMoRan, the world's biggest listed copper miner, which, in its own right, separately survived nationalization of its mining interests in Cuba in 1960.

Debswana

There is also an important distinction to be drawn between the nationalization of full-blown mineral extraction enterprises, and mineral extraction enterprises formed initially as joint ventures.

Botswana has over several decades produced substantial surplus profits from its investment in the country's diamond mines, in conjunction with De Beers. Botswana has invested its surpluses principally in a diversified basket of low-risk global government bonds. The country is also cited as an example of successful nationalization. Debswana, the joint venture between the Botswana government and De Beers, has from inception resembled a public-private partnership (PPP). The joint venture's first big investment was made at the Orapa diamond mine, which opened in 1971. At the time, Botswana ranked as one of the poorest countries in the world. It was a time when South Africa's gold mines were so profitable that the government legislated a super-tax which raised funds sufficient to build the most sophisticated infrastructure in Africa. There was a prolonged period during which South Africa's gold mines could have been regarded as part-nationalized, certainly from a cash flow viewpoint. This quaint feature of South Africa's history is neither appreciated nor discussed.

In Botswana in 1982, the Debswana partnership opened the Jwaneng mine, which exploits the world's richest diamond pipe. The two partners have enjoyed equal interests at the equity level, but the Botswana government has benefited additionally from societal and other gains associated with the opportunities created by a major world-class mining enterprise. Taxes paid by Debswana, its suppliers, and its employees are excluded from the joint venture. In other words, the Botswana government's stake in Debswana is substantially understated at 50 per cent.

There is also an important distinction to be drawn regarding the 'nationalization' of mineral extraction companies where production has long peaked. On this score, Namibia's diamond sector is often baldly cited as a successful example of nationalization. Diamonds were discovered in 1908, and mined for decades by De Beers. The 1994 equity agreement between De Beers and the government was lacking in any form of expropriation without compensation, and took place well after Namibia's diamond production had peaked.

There has also been no alteration in the practice of running Namdeb on a professional basis. Given the stages in the long life cycle of Namibia's diamond sector, De Beers could be seen as executing an exit strategy, as later partially implemented in South Africa, where it sold off five mines in the three years to 2011. In November 2011, De Beers declared that it would increase spending at its Venetia asset from R5 billion to R15 billion, taking the mine underground. This is De Beers' major South African diamond mine; it also operates Voerspoed, near Kroonstad, and a retreatment works (TRP) at Kimberley.

The costs of nationalization

On 2 November 2011, Johannesburg-based Sasol had a market capitalization, or market value, of R226 billion. Leaving aside the notion of nationalizing Sasol as a form of expropriation without any compensation for its shareholders, a purchase of Sasol, with a reasonable premium for control of, say, 20 per cent, would have required (at the time) an outlay of R271 billion. As discussed, the only additional monetary gain government would secure from such a move would be the Sasol dividend, which amounted to R7 billion for 2011. Ignoring the carrying cost of the capital outlay of R271 billion, on this basis, it would take government just under 40 years to recoup its investment in Sasol. Again, factoring in the time value of money, by applying interest, typically at the rate displayed by South Africa's long-dated government bonds, the capital outlay required to purchase Sasol would never be recovered.

Many governments around the world are facing the challenges of managing significant national budget deficits. The South African government faces very expensive social programmes in the years ahead, and rising national deficits, never mind the pressing issue of a seemingly intractable swelling of the trade deficit. The country simply does not have access to the kind of capital that would be required to buy even Sasol, a single asset. In a speech on 25 October 2011, Trevor Manuel, the National Planning Minister, argued that

'this country desperately needs investment, more specifically, investment in that which we know we have - and that is our rich mineral endowment. And, if for no other reason than we need investment, we must declare repeatedly that the nationalisation of the mines is a seriously bad idea. Even reading the MTBPS [medium term budget policy statement] with half a brain will confirm that there are no fiscal resources available through taxes or borrowing to pay for mines or invest in them, even if government were to get these mines gratis'.

Much as this confidently summarizes the realities, the minister was especially alert when he specifically referred to the lack of funds to 'invest in them'. This refers to the broad category of capital investment, including stay-in-business capital expenditure and capital expenditure allocated for new projects.

Mega capital expenditure budgets

Seen from a global viewpoint, successful and competitive mineral extraction requires enormous capital expenditure. Brazil's Vale, the world's number two mining company, has announced proposed 2013 capital expenditures of US$10.1 billion for project execution and US$5.1 billion dedicated to sustaining existing operations, as well as US$1.1 billion for research and development expenditures.

Despite advances in technology, covering everything from exploration to extraction and processing, and the depth and width of global capital markets, led by New York, London, Toronto, and Hong Kong, big new mining projects are sometimes beyond the individual reach of even the largest mining companies. Vale has long ranked as the major player in seaborne iron ore, the world's most profitable mining franchise. It is no coincidence that Rio Tinto, the world's third-largest miner, ranks as number two in seaborne iron ore, and that BHP Billiton ranks third.

Vale owns and operates the world's biggest iron ore province, the Carajäs system, in northern Brazil. During 2007, Vale announced the effective go-ahead for a new mine in the system, known as Serra Sul, flagged as 'the largest greenfield site in our history and the largest iron ore project in the world'. The estimated budget was initially stated as US$10 billion. This would have been significantly higher without the proposed mine's automatic access to the substantial infrastructure Vale has developed in the region over a period of decades, including railroads to the coast, a company-owned port with company-owned handling facilities, and, to boot, company-owned supertankers.

Vale has persistently delayed the full go-ahead for Serra Sul. The reasons for this are not clear. Vale generated just short of US$20 billion in operating cash flow during 2010; US$12.7 billion of that was spent on capital expenditure.

Guinea

It could be that Vale's attention had been distracted by the Simandou system, in Guinea. This has been characterized by Vale as 'one of the best undeveloped iron ore deposits in the world in terms of size and quality'.

Rio Tinto, which discovered Simandou in 2004, initially claimed a 95 per cent stake in all four Simandou blocks. After Guinea was taken over by soldiers, not for the first time, in December 2008, Rio Tinto found itself accused of dragging its feet on the development of Simandou. On 19 March 2010 Rio Tinto announced a non-binding MOU with China's Chinalco, Rio Tinto's largest shareholder, to establish a Simandou joint venture, where the new partner would acquire a 47 per cent interest by providing a US$1.35 billion earn-in over two to three years. Chinalco, it can be noted, is a state-owned mining company.

Guinea has long ranked as an important mining nation, principally for its deposits of bauxite, the base material for the production of alumina, which is smelted into aluminium. It was on 2 October 1958 that Guinea proclaimed itself a sovereign and independent republic. Ahmed Sékou Touré, who was declared president, instituted a dictatorship which included the broad implementation of socialism. These policies did not, however, include full scale nationalization of mineral extracting companies. On the contrary, in 1964, the Compagnie des Bauxites de Guinea (CBG) was established as the main force in the country's bauxite industry, and has since retained a global leadership role in the mining of bauxite. The Guinea government has always held 45 per cent of CBG; the balance is held by Alcoa and Rio Tinto-Alcan, leading private sector players in the global aluminium sector. CBG holds its mineral rights, over some 10 000 square kilometres, until 2038.

The Compagnie des Bauxites de Kindia (CBK) is likewise a joint venture; here, the government's partner is Russki Alumina, better known as Rusal. The Alumina Compagnie de Guinee (ACG), latterly a subsidiary of Rusal, mines bauxite and also produces alumina in Guinea. Dian Dian, an upcoming bauxite miner, is a joint venture between the government and certain Ukrainian interests. Recent policy in Guinea has promoted investment in alumina refineries, to further add value to bauxite within the country. Contracts to build new alumina refineries have been signed by two consortia, the first involving existing players in the form of Alcoa and Rio Tinto-Alcan. The second consortium, the Guinea Alumina Corporation (GAC), is held by shareholders that include BHP Billiton, the Global Alumina Corporation, the Dubai Alumina Corporation, and the Mubadala Development Company.

Guinea has for decades followed a joint venture approach to mining of the country's bauxite. It has been less strident in insisting on such a role in other subsectors, including iron ore, diamonds, and gold. Operation of the country's bauxite mines has for decades been characterized by government's apparent recognition that it can work together and alongside capital and labour. The partnerships have been able to function successfully under executive governments that can be regarded as anything but ideal, certainly from a political viewpoint.

Conclusion

South Africa's mineral extraction sector is recognized as continuing to hold unexploited resources which, once mined and processed, would be worth hundreds of billions of dollars. The extraction and processing of these minerals requires an enormous effort, a combination of significant capital expenditure, a supportive regulatory and legal system, and a prosperous and cooperative labour force, which includes professional management and the presence of requisite skills.

The country's prevailing investment climate is characterized by reluctant capital, which has found any number of other destinations, a hostile government environment, and a generally unsettled workforce.

Regulatory uncertainty is proving to be an increasingly worrying factor for a number of mining executives. During a speech in Johannesburg on 4 December 2012, Cynthia Carroll, outgoing CEO of Anglo American, said, inter alia, that:

'When making investments, mining companies have to think decades ahead. They need certainty as to the rules under which they will operate. They will not invest if there is a fear of arbitrary and unpredictable regulatory change. The regulatory debate in South Africa has been going on for a very long time. And it is still not completely resolved. The spectre of nationalisation has been laid to rest. But the need to guard against damaging regulatory changes remains.'

Carroll identified what she named as 'four truths':

There is no future for any society without law and order

There is no future for any society without law and order

Anarchy in the workplace ultimately benefits no one

None of us can defy economic reality, and

Like any other nation, South Africa will succeed only if it fosters an environment that is conducive to business and attractive to international investors.

Mindful of mounting criticism, the ANC at its recent Mangaung conference announced that 'strategic nationalization' would no longer be discussed; instead, a policy of 'strategic state ownership where deemed appropriate' would be followed. The ANC also toned down its interventionist approach to the economy. It also promised policy certainty for the next five years. At the same time, there would be a new tax regime for the mining industry; this may include export taxes on 'strategic minerals', should miners decline to cooperate with government's developmental aims, particularly in the pricing. According to anecdotal information, certain volumes of iron ore and platinum would be expected to be offered at discount prices to South African users, to promote 'beneficiation'.

The bottom line is that South Africa simply cannot afford to nationalize its mines. Even if the capital was available, there are any number of mines, notably in the gold and platinum sectors, where returns on capital are suboptimal, despite the benefits of a decade's worth of rising dollar commodity prices.

There are other significant obstacles to more extensive development of South Africa's minerals sector. Input costs, principally electricity, water, and labour, have been rising above trend lines for some years. There are major infrastructural impediments, occasioned by suboptimal management of parastatals such as Transnet. Government insists on remaining stubbornly in control of dozens of parastatals, echoing the intentions of malevolent executive governments which have pursued nationalization of mineral extraction firms for all the wrong reasons.

It is clear that South Africa's public and private sectors need to 'reconcile' interests that are not only different, but which remain in many ways in conflict. The level of distrust remains unacceptably high and labour, both organized and contract, has become a collateral victim, as witnessed by the tragic events in and around Marikana on 16 August 2012. It is time, surely, for the various parties to develop a bonafide respect for each other, and prepare for the launch of a positive future.

© The Southern African Institute of Mining and Metallurgy, 2013. ISSN2225-6253. Paper received, 1-2 August 2012.

1 World Bank Democratic Republic of Congo: Growth with Governance in the Mining Sector. Report No. 43402-ZR Washington DC May 2008 [ Links ]

{kind=link}