Services on Demand

Article

English (pdf)

English (pdf)

Article in xml format

Article in xml format Article references

Article references

Indicators

Related links

-

Cited by Google

Cited by Google -

Similars in Google

Similars in Google

Share

Permalink

PermalinkJournal of the Southern African Institute of Mining and Metallurgy

On-line version ISSN 2411-9717

Print version ISSN 2225-6253

J. S. Afr. Inst. Min. Metall. vol.111 n.9 Johannesburg Sep. 2011

PRESIDENTIAL ADDRESS

Future of the South African mining industry and the roles of the SAIMM and the Universities

J.N. van der Merwe

School of Mining Engineering, University of the Witwatersrand, Johannesburg, South Africa

SYNOPSIS

The current state of the South African mining industry is briefly reviewed from the point of view of an engineer not schooled in the finer details of predictive economics. Based on the assumption that current world exploration targets are indicative of which commodities the world will want in the future, it is concluded that the South African mining industry will continue to be viable and growing well into the future. South Africa holds the minerals the world wants and needs, and as long as the world has people, the demand for those, including gold, will continue to grow. There still is a growing demand for 'vanity commodities' and even the demand for platinum as a jewellery material displays significant growth.

Mine safety still needs to improve, but significant improvement has already been made although the industry is not always acknowledged for the effort in this field. The safety target set for 2013 is within reach but will require sustained effort.

The physical mining conditions for the main revenue earners, coal, platinum, and gold, will change substantially in the near future. Research in mining has declined alarmingly and it is urgently necessary for that to be revitalized to generate the knowledge that will be required.

In order to streamline the transfer of knowledge to the mining engineers of the future, research needs to be conducted with the full involvement of the universities. It will also be necessary for the universities to continually review curricula to incorporate the latest knowledge and to embark on a campaign of knowledge transfer to the older generation of mining engineers.

The mining industry is well supported by the universities, who have done their duty with regard to societal transformation, and the universities are in turn supported by the industry through vehicles like the METF. Industry is also strongly supported by a number of professional and vocational societies.

The SAIMM will continue to play its vital role as the meeting point of the mining technical sciences, and will continue to disseminate knowledge via the Journal, schools, and conferences. In the future, it will review its modus operandi to support the needs of growing membership in the remote branches. It will enter the research arena in an appropriate manner and give effect to the developing integration of mining and society.

The most important threat to the future of the mining industry is the recurrent mention of nationalization. While interaction between the mining industry and political and economic development of South Africa has always been characteristic, the current debate is emotional more than rational, and engineers are not well equipped to participate. This matter needs to be finalized before it becomes a popular force that politicians cannot control.

Keywords: wealth generation, mineral resources, mineral export, mineral production, mining skills, mining future, political interference.

Introduction

Southern Africa hosts the oldest known mine in the world, the 40 000 year old Ngwenya mine in Swaziland, where haematite was mined, presumably for use as a cosmetic. Due to the lack of documented history of the early stages of mining in the region, we today know only that of which scars or relics are still visible or which is still contained in folklore. It is, however, known that coal was mined by indigenous people in KwaZulu Natal. Mining has always been an integral activity of the region.

The discovery of gold and diamonds and the subsequent related industries, supported by coal mining to provide energy and followed by several other mining industries, is well known and documented. The role that mining played in the social and economic development of the country cannot be denied. Mining was pivotal in the political development of the country.

Now, in 2011, we have a well developed, mature industry facing serious challenges, and it is perhaps opportune to reflect on the way forward and to examine whether the bright past of the industry is reflected in the future. A number of indicators will be briefly reviewed in this paper, including the need for the products of mining, the availability of resources, the political environment, scientific support to the industry, and the provision of the necessary skills to operate the mines.

This will be done from the point of view of an engineer, not a political scientist, economist, or whatever other form of analyst. The Encyclopaedia Britannica defines engineering as 'The application of science to the optimum conversion of the resources of nature to the uses of humankind.' In this sense, the branches of mining and agricultural engineering can perhaps lay claim to being the core engineering professions. In developing society, there is a continuous need for wealth generation and protection. While the social and political sciences are necessary to protect and regulate the use of the wealth by the people, and the medical and other sciences to protect the health of the people, all of those would be useless without the generation of wealth which is primarily provided by the engineering professions.

It is thus not out of place for an engineer to intrude briefly on the terrain of other experts.

The opinions expressed in this paper are those of the author, and do not reflect the views of the SAIMM or the University of the Witwatersrand.

Current state of the industry

In this section, the demand for the most common minerals and the supply and availability thereof in South Africa are briefly described.

World exploration trends

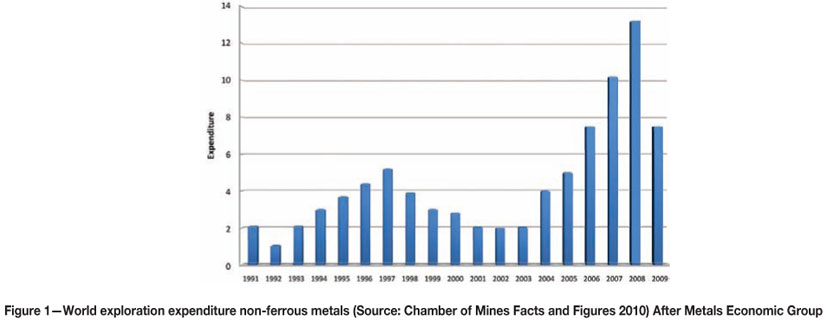

To reflect on the future of mining, it is necessary to know what people will want and need in the future, and this is best demonstrated by what the world is exploring for today. Figure 1 shows the trend of world exploration expenditure for non-ferrous metals for the past two decades. The dramatic increase since 2003 is clear, as is the sharp decline in 2009 following the 2008 economic crisis. This does not necessarily reflect a short-term view on the side of the mining financiers, rather that the world went into survival mode—without shortterm survival, there is no long-term to be concerned about.

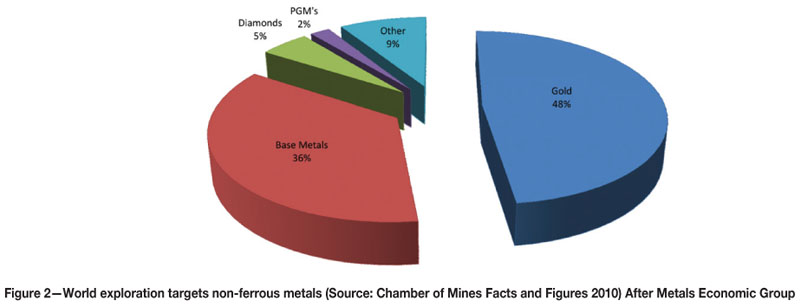

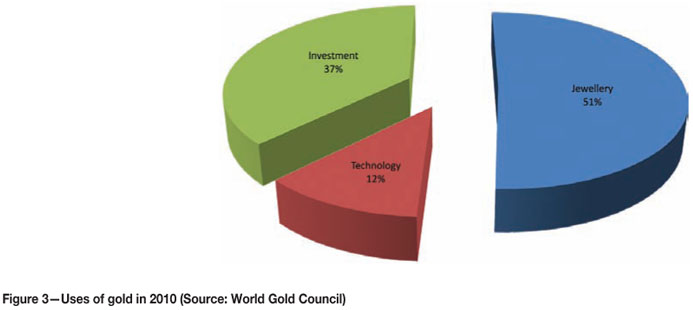

The first surprise is shown in Figure 2, containing a breakdown of 2009 world expenditure into exploration targets. Gold still dominates. The uses of gold in 2009, according to the World Gold Council (2011), are shown in Figure 3. Jewellery still dominates. This leads to the conclusion that the world as a whole is still in luxury mode, and we will continue to mine what people want, not necessarily what they need.

General overview of the South African mining industry

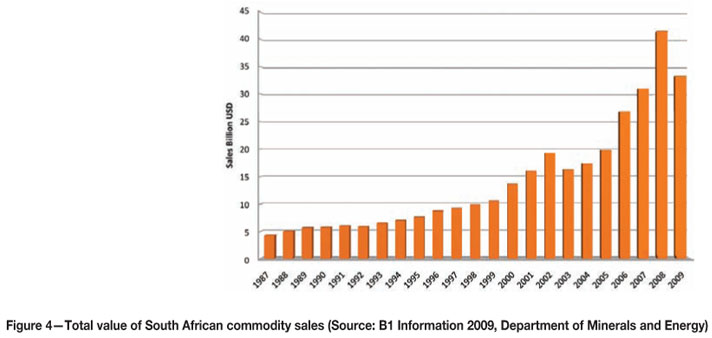

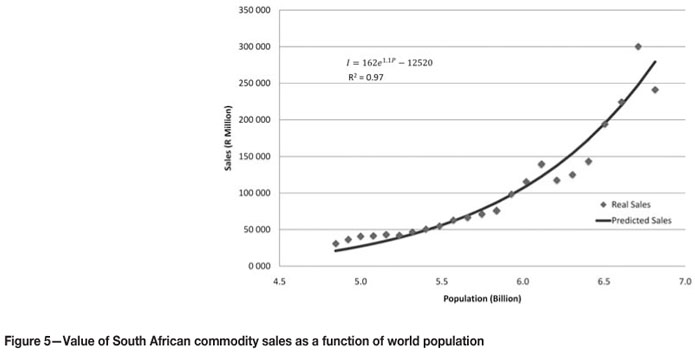

The growth in sales volume of South African mining products is shown in Figure 4. The growth is clearly exponential (correlation coefficient 0.96), in line with the growth of world population, which is also exponential.

In fact, there is a direct relationship between world population (P ) in billions and the total sales of the South African mining industry (I ) in million rand over the longterm, expressed by the equation

I =162e1.1P−12520

(see Figure 5). The correlation coefficient is 0.97. The relationship is valid only if viewed over a long time span, and is not accurate at predicting short-term (annual) fluctuations. Neither does it claim to be the result of in-depth economic analysis, it is an observation.

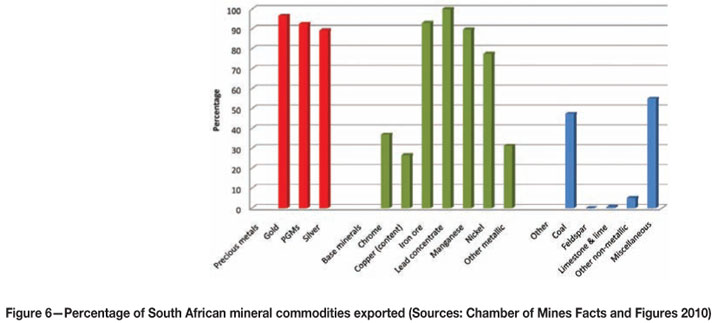

The reason for the correlation with world population growth, is shown in Figure 6, which indicates the percentage of exports of local mining products. Almost all the precious metals, and more than half of the base metal mine production, are exported. Our mine production links us to the world and exposes us to the economic trends of the globe. We produce greatly in excess of what we can ever consume locally, and the mining industry in this manner brings in much-needed foreign exchange. In short, the world needs our minerals and we get the world's money in return.

According to the Chamber of Mines (2010), more than 50% of the country's export value arises from mining products. The mining industry is responsible for approximately 19% of the GDP and employs half a million people directly, with another half million employed in directly related industries. It is the second largest employer in South Africa, second only to agriculture.

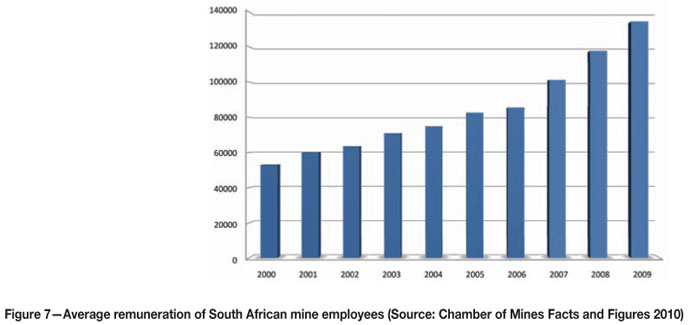

The growth average income of mineworkers in real terms (2009 base) is shown in Figure 7, using information from Chamber of Mines (2010). The current average income is more than 20% more than the minimum wage prescribed by the Department of Labour for the top category of workers in the civil engineering sector.

Selected minerals

In this section, a brief overview of the current state of selected minerals will be given. The four selected ones, in order of revenue generation, are coal (R65 billion), platinum (R58 billion), gold (R49 billion), and iron ore (R27 billion).

Coal

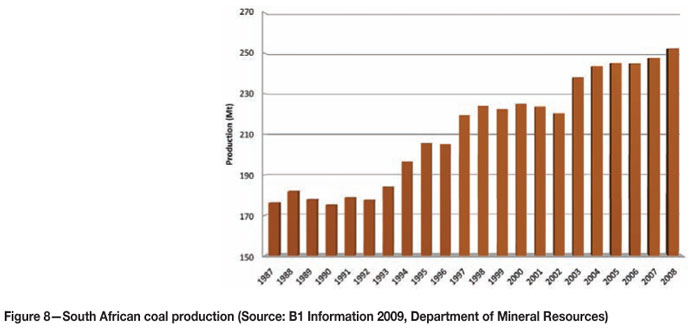

Of all the mined commodities (coal is not classified as a mineral), coal has historically been the most stable in terms of production growth, (Figure 8). Current production is just over 250 million tons per year.

It is estimated that at current production levels and known reserves, the world will deplete its coal reserves in 67 years' time, i.e. by 2078. This is not an accurate prediction, as it assumes constant demand and no additional resources, but serves to illustrate that coal resources are finite. Based on the same assumptions, South Africa will be the third last country in the world to cease production, outlived only by Russia and Kazakhstan (Chamber of Mines 2010).

South Africa's coal resource is the subject of recurrent debate, as it is more complex to define than commonly believed. It is not just a matter of quality and volume, as mining technical issues are often the determining factor in transforming the resource into a reserve. Factors like mining depth and seam thickness are just two that give rise to serious technical issues that influence the mineability of a resource.

The most important challenge in coal mining for the next decade is to meet the demand for electricity generation. At current coal qualities, it is estimated that production will have to increase by 100 million tons per year between now and 2020. That is an increase of 40%, which will require constant growth of 3.5% per year, every year. It is known that the reserve in the Witbank field is approaching the end of its life, and that the elements of infrastructure in the next major resource fields, Limpopo and the Waterberg, are nowhere near the state that will support the industry. Merely increasing the rate of production of the existing mines will not solve the problem; it will actually aggravate it as the existing reserves will be depleted even sooner and replacement mines will also have to be established quicker.

While the mining engineers may be able to meet the challenge (growth in the period 1992 to 1997 was close to what will be required for the next decade), the supporting infrastructure will have to be provided very quickly. It also estimated that R100 billion of investment will be required, which assumes great importance against the background of the nationalization debate.

By whatever means and against whatever ideological background, the coal will simply have to be provided and thus the outlook for mining as mining, is positive. If supplies are inadequote, the electricity will simply not be there to sustain the growth or even maintain the current level of activity of the country, and then the entire debate has to take place at a different level.

Substitute sources of energy have been shown to simply not be viable yet on the required scale; we will thus rely on coal for a long time to come.

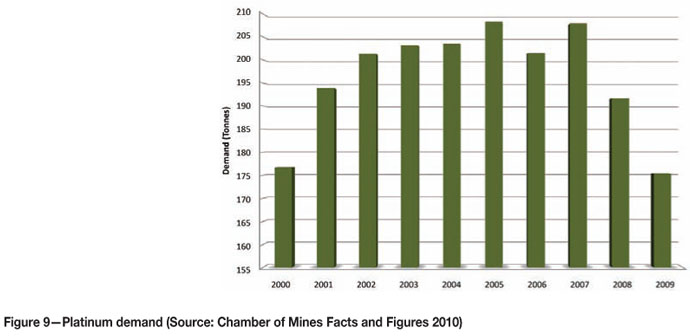

Platinum

The platinum market was hard hit by the world economic crisis, due mainly to the slump in automotive manufacturing. The decrease in demand is shown in Figure 9. As the world economy improves, so will the demand for platinum, leading to optimism for the future. To some extent at least, the carbon energy and platinum mining industries are interdependent. The more cars, the more fuel is required, the more platinum is required to combat the negative effects of carbon energy generation.

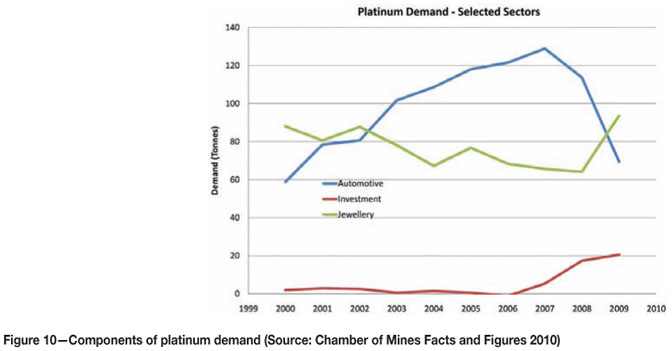

However, there is even more reason for optimism. Figure 10 shows the components of platinum demand. When the demand from the automotive sector dropped, the demand for investment purposes increased, indication that the optimism of the miners is at least shared by significant financiers. The other interesting trend is the increase in demand for jewellery, complementing the earlier conclusion that the world still indulges in luxury. If the link between platinum and vanity can be cemented, the platinum mining outlook will indeed be positive to the extreme. It is not by chance that the SAIMM's premier award, the Brigadier Stokes Award, consists of a platinum medal.

South Africa holds just less than 90% of the world's known platinum reserves, with Russia in a distant second place with 8%.

Gold

The world has been mining gold for over 6 000 years. The value of the metal is perhaps illustrated by the fact that in all that time, only approximately 165 000 tons has been mined, which would occupy a volume of 8 500 m3, or a cube measuring just more than 20 m in all directions. A medium sized coal mine produces an equivalent mass of coal in less than two weeks. As an illustration of the effort required to produce that amount of gold, consider that at a high grade of 10 grams per ton, 16.5 billion tons of ore (more than 6 billion cubic metres, almost three times the volume of the Vaal dam) has had to be mined to produce the world's gold.

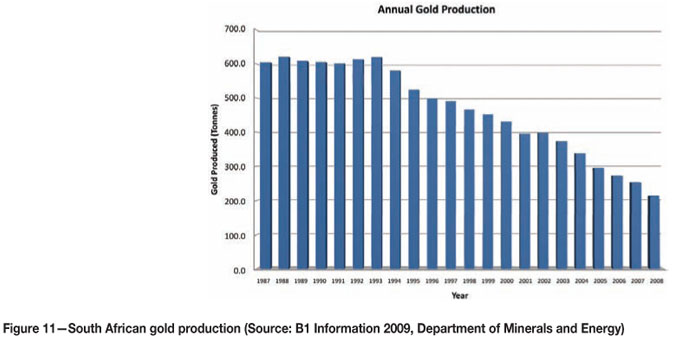

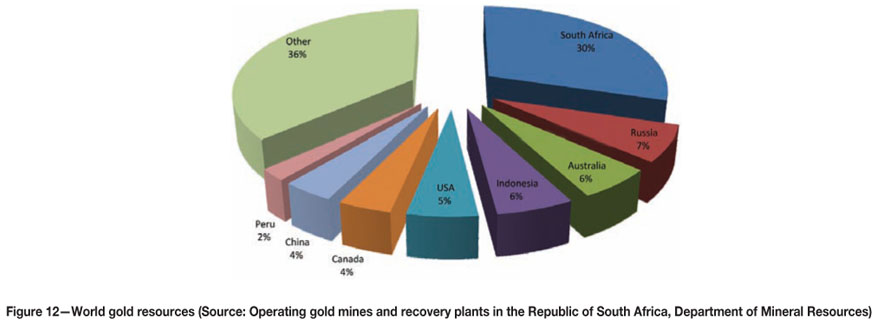

Over the past few decades, South Africa has grown used to the idea of not being the world's largest gold producer. However, we are still on the list of top producers, and gold mining continues to be a major revenue earner and employer. While the linear decline in production since 1993 from approximately 600 tons per year to 200 tons per year is shown in Figure 10 and Figure 11 compares the resource bases of the countries of the world.

We are still the country with the largest gold resource. It is conceded that there are severe challenges in mining our abundant resource at competitive costs, especially in the immediate future, but as has been shown, investment will go the way of what the world wants, not needs. It is difficult to imagine that mankind's desire for gold will decrease when the supply is under threat. If anything, it will drive the price up.

At the current rate of gold consumption of around 2 500 tons per year, if South Africa were to stop producing now all the currently known gold reserves in the world will have been mined in 20 years' time. With the South African resources and production included, the production can be stretched to 35 years.

While this simplistic argument is by no means claimed to be accurate in terms of real production and consumption, it nonetheless serves to indicate that South Africa is still in a very favourable position in world gold terms. The world will not stop wanting gold. When other resources run out, the price will merely increase and we will be able to mine our expensive resource economically.

Where we have failed is to generate the knowledge and methods we need to mine our very difficult resources safely and economically under current conditions. We simply fell behind in research, and if we are to have any hope of turning our gold resource into benefit for the country, the research effort has to be revived. Fortunately, there are serious efforts at doing just that under investigation at the moment, and if successful, there is no reason to believe that the country's scientists will not deliver, even if it requires a repetition of the short-term import of expertise that we experienced after the Coalbrook mine disaster.

Iron ore

Although world demand for iron ore was severely affected by the economic crisis of 2008, South African iron ore production continued to grow during that period to a new high of 55 million tons in 2009. Global steel production fell by over 15% in 2009, but South Africa was still able to increase exports during that period, no doubt assisted by the growth of more than 13% in Chinese steel production and, importantly, improved export infrastructure between Sishen and Saldanha.

Summary of current position with regard to resources and production

South Africa's position in the world with regard to resources and production of selected commodities is shown in Figure 13.

It is clear that we are ranked in the world top 5 with regard to resources of 10 important commodities: platinum, manganese, vermiculite, vanadium, gold, zirconium, fluorspar, titanium, uranium, and nickel. We are ranked in the top 5 producers of 9 commodities.

As long as humankind needs minerals, there will be mining and the resources are here. Importantly, we have the resources of the world's most sought after minerals. A point first raised by Agricola (1455) is that several other industries are dependent on mining. That argument can today be extended – try to imagine any object in the immediate vicinity of a house or place of work that would have been there in its present form without mining. Even plants use fertilizer, planks are made of wood from trees that were fertilized, and are formed by saws and other tools made of steel, etc.

Mine safety

It is an ironical twist of terminology that when we mention mine safety, we really discuss mine accidents. In this regard, we do not yet have much to be proud of. It is well known that we lag behind the important world players' safety records.

Experts argue about the reasons for our poor performance, citing reasons ranging from a low regard for human life in our society to the inherently dangerous nature of our gold mines, flavouring the arguments with a reluctance to implement new technology, etc. Anyone with an axe to grind will find reason to attach an argument to the unacceptable fatality and injury rates of our mining industry.

But looking at the facts coldly, our mines are at least an order of magnitude safer than our roads. The probability of losing one's life in a car accident is more than 10 times as high as it is underground in a mine, based on the comparison of fatalities per million hours worked to the number of fatalities per million hours travelled. Even the murder rate per capita, at approximately 38 per 100 000 people per year, is higher than the mining industry fatality rate of around 26 per 100 000 workers per year.

However, this in no way softens our accident performance. One just feels that it would be so much better for all concerned if we paid the same attention to road safety (to mention but one dangerous activity in our society) as we do to mine safety.

But, on the positive side, our re-entry into the world after the democratization of society has also meant a new approach to mine safety. Suddenly, we were exposed and shown to be far behind the rest of the world. Financiers were no longer prepared to invest in a dangerous industry, and the State followed by being less forgiving than in times gone by.

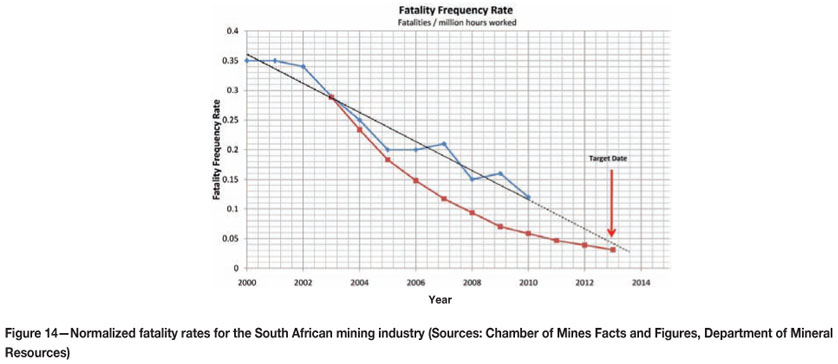

Miners reacted by changing attitudes. 'Acts of God' were seen in a new light and accidents were no longer acceptable. Figure 14 shows the current overall fatality rate compared with the agreed target. This year started off badly, but all is not lost. Linear extrapolation of the trend exhibited over the past decade indicates that the target of 0.03 fatalities per million hours worked is still achievable by 2013. Detractors will argue that a linear extrapolation is not valid, as it becomes exponentially more difficult to reduce accidents at the low levels. This is a valid argument, but examination of past performance indicates that there were periods of almost linear decrease as recent as 2002 to 2005. If it could be done before, it can be done again.

Our deep level gold mining conditions are the most severe in the world, and if we can match the rest of the world in terms of safety performance, it will be a remarkable achievement, comparable to that of a barefoot athlete matching Hussein Bolt's time in a hundred metre race.

When the time arrives—as it will—to mine at even greater depth and under even more difficult conditions, we will need the technology to back up the mining industry. In this respect, we are sadly lacking but, as mentioned before, there are plans to redress the situation. If one considers that the estimated cost associated with a fatal accident amounts to between R10 million and R20 million, then the total cost associated with fatalities is more than R2 billion per annum. Safety research under these conditions cannot but be a worthwhile investment.

Political background

One has to wonder whether it is coincidence that South Africa's Foreign Direct Investment (FDI) decreased by a staggering 70% in the year (2010) that nationalization of inter alia the mining industry was first called for from political platforms, albeit junior ones. In the same period, the FDI of the African continent also decreased, but by only 9%.

The denial of nationalization being government policy, expressed by more senior cabinet ministers, was outweighed by the silence from the State President.

Yet, interaction between mining and politics is nothing new. The history of South Africa largely revolved around the interplay between mining and politics, see inter alia Cameron (1986).

The first major occurrence was when Nicolaas Waterboer claimed the area including the Kimberley diamond fields as tribal heritage land from the Orange Free State government. His claim was adjudicated by a judge appointed by the British, Keate, who decided in favour of Waterboer in 1871. He was then offered and accepted British citizenship as protection against the Boer republics, whereupon the diamond mines became Crown property. The border of the Cape Colony, then in British hands, was adjusted to include Kimberley.

The outbreak of the Second War of Independence (South African War) in 1899 was set against the mining background, when the British government acted to protect the rights of foreign mineworkers (British citizens) who were denied voting rights by the Zuid Afrikaanse Republic, while the real aim was to gain control of the goldfields.

When the Chamber of Mines attempted to promote black workers to more senior positions on the mines in an effort to reduce costs, it resulted in the major strike of 1921, which developed into a full scale revolt that was ended only after the government used the air force against the strikers. This was one of the reasons why General Smuts, then Prime Minister, resigned before the end of his term in 1924. Some were dissatisfied with his use of the air force against his own people, while others blamed him for not acting sooner to end the strike.

The Mines and Works Act of 1911 contained the first job reservation clauses in South Africa, reserving certain categories of work for white people.

Mining was used as the catalyst to introduce Afrikaner people into the higher level of economic activity of South Africa, the so called 'Afrikaner Empowerment' movement. Anglo American in the 1950s felt that the country needed more of the skills of the Afrikaner at higher levels, and assisted the Federale Mynbou group to purchase two coal mines. These were operated successfully and the group ventured into gold mining with the takeover of General Mining, retaining the latter name. Success followed upon success, General Mining later merged with Union Corporation to form Gencor, and the final result today is the international mining giant, BHP Billton, which resulted from Gencor's take-over of the BHP group and the eventual merger with Billiton.

Throughout South African history, mining has been an instrument that was used to shape boundaries as well as society and financial structure. It is an integral part of our society, not a stand-alone entity on the side. Whatever happens in South African society will echo in the mining industry.

It is thus no surprise that mining was one of the targets to assist with societal reform when the country officially became a democracy in 1994. That it is now used by politicians for their own purposes is neither strange nor unique. This is the way it has always been.

The threat of nationalization overshadows all other threats to the industry, and given the importance of the industry to society, to the country as a whole.

It is tempting for politicians to promise riches to the poor of the country. Sharing an industry with an income of around R250 billion to R300 billion per year sounds wonderful. However, what is not stated is that far more than 80% of that income is already in the hands of the people, (see Figure 15). Of the income, 48% is spent on procurement, the vast majority from South African BEE companies. Salaries and wages, paid to South Africans, account for another 18%. All the money, except for the 6% paid out as dividends, is spent in order to remain operative.

It even sounds tempting to distribute only the amount paid out on dividends, amounting to roughly R18 billion per year, to the people of the country. However, dividends are rewards to shareholders for taking the risk to invest in the industry in the first place, to provide the capital to create the mines. If the dividends go to the people, then the capital to create the next mines must also come from the people. Nationalization will result in a total withholding of foreign capital investment in the industry, leading to the collapse of the industry and with it, delivering a blow to the nation which could well be fatal.

Nationalization makes no rational sense, but the debate is not a rational one, it is emotional. As engineers we too often believe that people will be convinced by rational argument, but that is not the case. We operate rationally inside a political system that is far more emotionally based. The argument needs to be driven on a level with which we are not familiar and for which we are ill equipped.

The decision makers need to be convinced. We cannot compete with them for the hearts and the minds of the people, it is not our terrain.

At the same time, the abject poverty of people in the rich mining districts of South Africa is all too apparent. As an industry, we are fulfilling our role of unearthing the minerals and thereby creating wealth, but the regulators need to review the mechanisms to channel that wealth to where it is needed. This is perhaps a more urgent aspect to be investigated.

All the political interferences of the past had the central goal of controlling the industry with a view to long-term sustainability. It is to be hoped that sanity will again prevail and that the industry will survive once more. It is too important for the future of the country to harm it. Fortunately, politicians are not known for consistency of viewpoint and in this case, politicians may well save the industry by that very inconsistency.

Role of the universities

In addition to the classical university roles of providing skilled manpower and knowledge by conducting research, universities in South Africa also have a vital role to play in the broader transformation of society. According to Cruise (2011) the South African universities produced exclusively white male mining graduates until 1981, when an Indian man graduated from the University of the Witwatersrand. This was seven years before the racially discriminating clause in the Mines and works Act was repealed.

The first female mining engineer graduated from the University of the Witwatersrand in 1994, two years before the sex discrimination clause was repealed from the Act. Since then, transformation has gathered momentum, with 100% of the University of the Witwatersrand mining graduates in 2010 being black and 70% of the class of the University of Pretoria. Female mining graduates from the two universities combined accounted for 30% of the total.

The universities have transformed to supply the needs for the future in terms of societal demands.

From an engineering perspective, the universities now have to produce engineers that will be able to handle the technical challenges of the future.

Gold mines will be deeper, as will platinum mines. Coal will be mined in new coalfields, requiring perhaps new methods of mining. The external environment will be different.

Not only will there be natural hazards such as high rock stress and temperature to contend with, there will be severe organizational challenges. Attitudes toward safety and wellbeing will be different, there will be more community involvement, there will be logistical challenges—how to get workers and material to working places quickly and efficiently if mining is done 5 000 m below surface? How will new mining methods be introduced?

Mining engineers are taught by older, experienced mining engineers. The new graduates will require at least ten years after graduation before they are in decision-making positions. The challenge before the universities now is to address the curricula to ensure that the foundations of the skills that will be required in 2025 are taught in 2011 by lecturers who were themselves trained in the 1980s and 1990s.

There will have be some element at least of 'training the trainers'. The trainers will have to be intimately familiar with new trends, new methods, new mining. The best—perhaps the only—way to achieve this is to generate the new knowledge that is required at the institutions where the students are educated. In other words, mining research will have to be done by the mining universities and with the involvement of the staff responsible for education. The universities will have to be involved in all aspects of mining research.

The demise of mining research in South Africa has been described before Van der Merwe, (2006), and it is vital for the future of the industry that it be revived. It should be revived with the involvement of the universities.

However, simply training students will not be enough either. It is wrong to believe that we will be successful by implanting all the new knowledge in eager young graduates who will join the mines at the lowest level. There will also have to be emphasis on training the existing old-school personnel on the mines. The sooner the professional registration of mining engineers is made compulsory, the better, so that continuing professional development can be enforced.

There is a shortage of mining engineers the world over. Cruise (2011) reported that the average age of mining engineers in the English-speaking world was approaching 60. South Africa produces high quality mining engineers, while mining engineering education elsewhere is declining. There will be increasing demand from other countries for South African engineers. The current mining schools are overcrowded, therefore provision will have to be made to train even greater numbers to ensure that we have sufficient supply for our own needs.

The mining schools in South Africa are fortunate to have the full support of the mining industry. Without the support offered by institutions such as the Minerals Education Trust Fund (METF) that supplements the salaries of teaching staff, it will not be possible for the universities to attract and retain vital training skills. This is a two-way affair: it is of critical importance for this support to continue and for the universities to remain worthy of this support.

The role of the Southern African Institute of Mining and Metallurgy

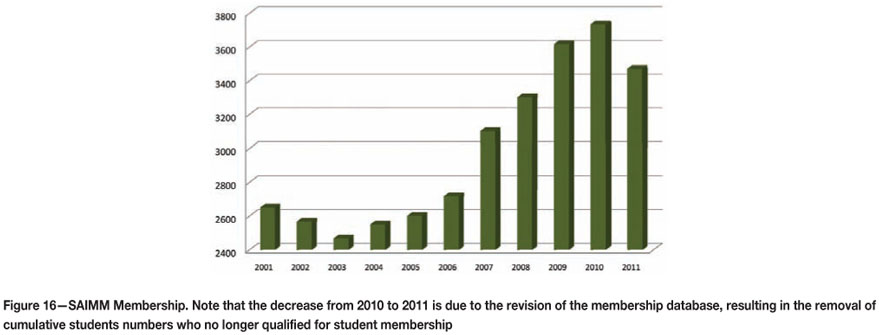

The SAIMM, created in 1894, is the only organization in the southern African region that offers a home to all the technical disciplines in mining. It supports the mining industry by serving its members and has a vital role to play in the dissemination of new knowledge that has been tested and reviewed. It has just over 3 400 members (Figure 16), and publishes an accredited journal that has been the communication vehicle for world renowned mining scientists. The Institute organizes conferences, symposia, and schools on a variety of subjects each year. On average, there are between 12 and 15 such events per year, attended by approximately 2 500 to 3 000 delegates.

The website contains all the information regarding conferences and makes all the papers published in the Journal available free for download by anyone. Papers made available by OneMine, the world's leading online mining library, are accessible free of charge to SAIMM members, including students who benefit from free membership.

The SAIMM has branches not only in South Africa, but also in neighbouring countries including Namibia, Zimbabwe, and Zambia, with more in the pipeline. Interest has been expressed from countries like Ghana and Tanzania. There is a policy to formalize ties with similar organizations in the BRICS countries, with India already in place and Russia, Brazil, and China to follow. We will continue to enhance our role as the conduit of mining technical knowledge and experience.

The SAIMM is recognized as a Voluntary Association for mining by the Engineering Council of South Africa, assisting with the registration of professional engineers and overseeing the quality of mining and metallurgical engineering education in South Africa. It is also the custodian of the SAMREC and SAMVAL reporting codes of the Johannesburg Stock Exchange.

Recently, in recognition of the importance of mineral economics to the mining industry, it branched into that field with the creation of the Mineral Economics Committee which is due to host its first major international conference next year.

A non-profit organization, the SAIMM is now financially strong, having survived through difficult periods where its existence was in jeopardy. It now has an annual turnover in the region of R20 million.

The SAIMM is well placed to support the mining industry, and has developed the necessary structure to do so. It should now look to the future and ensure that it continues to do so.

Certain changes will be required, such as transforming the operation of Council to cater for the needs of the growing number of members in the distant branches. The position of Council is also planned to be elevated by leaving only important decisions on policy matters to Council, while Office Bearers will assume full responsibility for the more mundane management matters. These changes have been approved by Council, and the next step will be to put the matter to a member vote as required by the constitution if changes are required.

A feasibility study is also under way to investigate the application of the 'Green Mine' concept, based on a similar venture in China. A 'Green Mine' is defined as one that complies fully with legal, environmental, safety, and societal requirements, but also implements the most appropriate new technology and transparent management processes. If the outcome is positive, the exact specifications for the classification will be drawn up by consultation with all the role players. If the project is approved for implementation, the SAIMM Green Mine classification will become the benchmark for the top mines in the country. It will be a classification, not a competition.

The SAIMM is now in a position to invest in the future needs of its members, and the research field has been identified as the most appropriate one to become active in. It is not foreseen that the SAIMM will be able to afford to fund research projects directly, but it has a role to play in providing the means whereby research in mining can be stimulated or perhaps coordinated between the various funders and suppliers. This is still under discussion.

Conclusions

The first fact at hand is that South Africa has the resources the world wants and needs. Current exploration expenditure, used as an indicator for expected future demand, is dominated by gold. Although South Africa has the world's largest gold resource, local production is declining due to high costs brought about by the physical conditions under which our resources exist. The lower cost resources located in other parts of the world are finite and the long-term outlook for gold remains positive. The challenge for the immediate future is to maintain a presence in gold mining until the price increases to levels that will improve the viability of local gold mining. Gold is gold, and there is no reason to believe that the demand will decrease once the lower cost resources have been depleted or approach the end of their lives. Rather, the price will just increase.

There is an encouraging shift in the demand pattern for platinum, which is now also entering the 'vanity' category. The industrial demand is a function of the state of the world economy, and once the economic recovery is complete demand will also recover. A major threat for platinum as an industrial material is the potential development of alternative methods of reducing harmful gas emissions or even switching to cleaner types of automotive fuel.

The outlook for coal and iron ore remains positive. Indeed, the major challenge facing the coal mining industry is to increase production to the required levels for electricity generation and at the same time to relocate the industry to new fields as the Witbank resources are approaching depletion.

Mine safety is improving. While it may be stated that the safest place a miner in South Africa can be is underground, there is ample room for improvement, and the performance over the last decade is sufficiently encouraging to believe that the internationally benchmarked target set for 2013 can be met.

It has also been shown that due to the fact that the bulk of mining products are exported, there is a close link between world population and the income of the South African mining industry. This link will continue to hold for as long as the world GDP also increases, which means that as the population grows, the relative number of rich people must also grow.

Purely from the mechanical point of view, i.e. considering availability of resources, demand, and the ability to mine, the future outlook is very positive indeed. Coupled to this is the fact that the mining industry is at the core of the South African economy. The country needs a strong mining industry, the world needs the minerals, and we have both the resources and the proven ability to produce.

However, mining is conducted in a society, and society is governed by politics. Uninformed and irresponsible political statements for the sake of personal popularity can have a devastating effect on the mining industry and could change the entire landscape. South Africa simply has too many minerals the world needs to allow total collapse, and should the situation deteriorate to critical levels, external intervention to prevent a collapse cannot be ruled out. However, this type of scenario development is beyond the scope of this paper.

The universities supply graduates of world quality to serve the industry in the coming decades. This is where the future is created, and with strong mining departments that have successfully transformed to meet the requirements of South African society, there is no reason to fear the future. The strong support from the mining industry has been a characteristic of mining education in South Africa, and with continued support from organizations like the METF this can only improve further.

In coming decades, the face of mining will undergo substantial change. We will mine in new environments and our current methods may not be suited. Research is required and urgently so, but there are plans to redress the situation. It is vital for the future of the industry that those attempts succeed.

The SAIMM is well placed to continue with its role of supporting the industry on a nonprofit basis by providing a vocational home to the technical disciplines in mining and to assist with the ECSA committee on mining. It will continue to disseminate technical knowledge by publication of the Journal and presenting schools and conferences. It is set now for the next level of activity, to broaden its network by strengthening links with the SADC countries as well as the BRICS alliance. It will also enhance the service to the industry by involvement in research.

There is a single dark cloud on the horizon for mining in South Africa, and that is that the political environment—the mere threat of nationalization, to be specific—will cause much-needed foreign investment to be withheld. This spectre needs to be publicly cancelled by the highest authority in the country to restore confidence. It needs to be done before the call for nationalization develops into a popular movement that can perhaps not be controlled by the politicians.

Bibliography

The following publications were used to source the information contained in the address. In several cases, information from different sources has been combined to produce diagrams and single references were thus not made in all cases. Readers are encouraged to view the material in the publications below as they contain a wealth of information on the South African mining industry.

References

WORLD GOLD COUNCIL. Gold Demand Trends. Downloaded from www.gold.org. [ Links ]

CHAMBER OF MINES OF SOUTH AFRICA. Chamber of Mines Facts and Figures. www.bullion.org.za. 2010. [ Links ]

CHAMBER OF MINES OF SOUTH AFRICA. Annual Report. www.bullion.org.za. 2010 [ Links ]

AGRICOLA, G. (1455) De Re Metallica. Transl. Herbert Clark Hoover and Lou Henry Hoover. Dover Publications Inc., New York, 1950. [ Links ]

CAMERON, T. New History of South Africa. Human & Rosseau, Cape Town. 1986. [ Links ]

CRUISE, J.A. The gender and racial transformation of mining engineering in South Africa. Journal of the Southern African Institute of Mining and Metallurgy, vol. 111, no. 4, April 2011. pp. 217–224.

VAN DER MERWE, J.N. Beyond Coalbrook: what did we really learn? Journal of the Southern African Institute of Mining and Metallurgy, vol. 106, no. 12, December 2006. pp. 857–868.

DEPARTMENT OF MINERAL RESOURCES. Operating gold mines and recovery plants in the Republic of South Africa, 2010. www.dmr.gov.za/Mineral_Information/Mineral_Directories.html. 2011. [ Links ]

DEPARTMENT OF MINERAL RESOURCES. Platinum-group metal mines in South Africa, 2009. www.dmr.gov.za/Mineral_Information/Mineral_Directories.html. 2011a [ Links ]

DEPARTMENT OF MINERAL RESOURCES. Ferrous mineral commodities produced in the Republic of South Africa, 2009. www.dmr.gov.za/Mineral_Information/Mineral_Directories.html. 2011b. [ Links ]

DEPARTMENT OF MINERAL RESOURCES. B1 Information 2009. www.dmr.gov.za/Mineral_Information/Mineral_Directories.html. 2011c. [ Links ]

DEPARTMENT OF FOREIGN AFFAIRS (2011) South Africa Yearbook: Section 16, Mineral Resources. www.southafrica-newyork.net. 2011. [ Links ]

© The Southern African Institute of Mining and Metallurgy, 2005. SA ISSN 0038–223X/3.00 + 0.00. Address presented at the Annual General Meeting on 11 August 2011.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}