Servicios Personalizados

Articulo

Inglés (pdf)

Inglés (pdf)

Articulo en XML

Articulo en XML Referencias del artículo

Referencias del artículo

Indicadores

Links relacionados

-

Citado por Google

Citado por Google -

Similares en Google

Similares en Google

Compartir

Permalink

PermalinkSouth African Journal of Economic and Management Sciences

versión On-line ISSN 2222-3436

versión impresa ISSN 1015-8812

S. Afr. j. econ. manag. sci. vol.24 no.1 Pretoria 2021

http://dx.doi.org/10.4102/sajems.v24i1.3764

ORIGINAL RESEARCH

Household saving and wealth in South Africa

Fanie Joubert; Theo Van der Merwe

Department of Economics, College of Economic and Management Sciences, University of South Africa, Pretoria, South Africa

ABSTRACT

BACKGROUND: A detailed picture of the saving behaviour of South African households would enable researchers to determine whether households are proactively attempting to safeguard themselves financially.

AIM: Of this article is to analyse household saving(s), using both an income-statement (saving) and a balance-sheet (savings or wealth) approach, while investigating the link between the two as well.

SETTING: The perception that households are 'dis-savers' without really delving into the details, definitions, or reasons why this may or may not be the case. This notion is proven superficial as it ignores various interacting definitional and measurement issues

METHODS: A descriptive analytical methodology is applied to household saving (flow) and savings (stock or wealth) in the period 1995 to 2018, with the focus on macro-economics, while data are sourced from the South African System of National Accounts (SNA).

RESULTS: Findings include a long-term decline in net household saving to Gross Domestic Product (GDP), which turned negative in 2006, so that dissaving occurred. In contrast, household wealth recorded an average nominal increase of 10.3% in the period 1995 to 2018. Focusing on the link between the two concepts, it is confirmed that net revaluation of assets plays a prominent role to support the rise in wealth, while the role of saving diminishes over time. Therefore, the need for additional methodological updates is highlighted. More research is required on the various possible factors driving household income and expenditure trends, and their sustainability. The contribution of household saving to total saving should be evaluated in detail.

Keywords: household saving; household wealth; theories on saving; South African System of National Accounts.

Introduction1

Saving, specifically household saving, is a complex subject as theoretical (definitional) differences could lead to diverse conclusions regarding the state of saving in a country. This creates confusion to users of the data, such as politicians, analysts and academics, and impacts directly on the appropriateness of research findings and policy recommendations. The confusion stems, inter alia, from the (erroneous) interchangeable use of terms such as saving and savings (or wealth). The aim of this paper is to analyse household saving(s), using both an income-statement, or flow (saving) approach, and a balance-sheet, or stock (savings or wealth) approach. The link between the two is also highlighted. The paper has a macro-economic focus and data are sourced from the South African System of National Accounts (SNA).

To define, delineate and measure household saving and savings; as indicated earlier, theoretical concepts that are often blurred in the literature. It further highlights and quantifies the link between the two concepts, an important empirical exercise often neglected in related research.

It is key to note that the South African Reserve Bank (SARB) is in the process of a significant methodological overhaul of data for various sectors of the economy (including households), especially regarding their national income and product accounts (NIPA), as well as financial account data. The current data, therefore, need to be interpreted with caution. This also means that the 'elusive' link between the various accounts should become clearer in future (for example, household saving measurements, as observed in the production, distribution and accumulation accounts; the household balance sheet; and the national financial account [NFA]). At the time of writing, the SARB confirmed that the figures used in this article are based on the best (most relevant) data publicly available.

The rest of the article is structured as follows: In Section 2: Definitions and appropriate literature is discussed, while an overview of the Systems of National Accounts (SNA) is provided in section 3: This is followed by 4: The income-statement approach, with detailed definitions and measurements of South African household saving from the flow perspective. Section 5: The balance-sheet approach, with definitions and measurements of household wealth. The link between these two measures is analysed in Section 6, and followed by Section 7, the Conclusion.

Literature review and definitions

As far as the distinction between saving and savings is concerned, Hodgetts, Briggs and Smith (2006:3) mention that 'the topic of saving is muddied by the tendency for "saving" to mean different things to different people' and that a clear distinction needs to be made between the verb saving and the accumulated stock of savings (the noun, also referred to as wealth or net worth). Looking at the period 1985 to 2005, they found that New Zealand households had been dissaving since the early 1990's, while household wealth increased rapidly, driven strongly by positive house- price revaluations. They warn that a low or negative household saving rate, even when accompanied by strong rises in savings (or wealth), still carries various 'adverse economic implications', including more pressure on current account deficits, rising external debt and higher household indebtedness that may lead to increased financial vulnerability.

As far as South Africa is concerned, Prinsloo (2000) looked at trends in saving between 1960 and 1999 and found a decreasing trend in gross household saving as a percentage of household disposable income, notably from the mid-1980s. Unfortunately, his definition does not explicitly address the difference between saving and wealth (savings); however, he states that 'in terms of standard accounting practice, the saving of a household will be equivalent to the increase in (its) net asset value' (Prinsloo 2000:21). He identified 'rising marginal personal-tax rates' and 'persistent high inflation' to be disincentives to saving. Combining these with changes in the real after-tax interest rate, he arrived at a '3-sides-of-the-same-coin' argument; and it followed that an increase in interest rates alone is unlikely to incentivise South African households to save, if the impact of taxes and inflation is not sufficiently addressed (Prinsloo 2000:16-17).

Seminal works related to the theoretical underpinnings of household savings in South Africa, include those by Aron and Muellbauer (2006), as well as Aron, Muellbauer and Prinsloo (2006a, 2006b); these provided the first estimates of household sector balance sheets (or wealth), covering the period 1975 to 2005 (see, Aron et al. 2006a). Kuhn (2010) provided further important refinements to the work of Aron et al. (2006a), and supplied a detailed analysis of the trends for the period 2005 to 2009.

As far as empirical literature is concerned, Orthofer (2015, 2017) made important contributions, and lamented the lack of focus on and attention to what exactly is measured as saving in the national accounts. Her findings for South Africa mirror those of Hodgetts et al. (2006), in the sense that a steady decline in household saving rates is observed, while household net worth had simultaneously risen strongly, driven to a large extent by the appreciation of asset valuations, notably domestic corporate equities. She remarked that 'the full integration of the South African national accounts will contribute to our understanding of aggregate saving and wealth dynamics in future' (Orthofer 2017:239). She also raised an important warning, related to the distribution of wealth in South Africa, specifically the highly concentrated nature of equity ownership.

As mentioned earlier, and also revealed in literature, the definition of saving is very important. This section, therefore, is concluded with some definitions focusing on the important, yet easily confusing distinction between the terms saving and savings.

Grammatically, saving is usually seen as a verb, such as 'saving money when buying an item on special' or 'saving for a special occasion'. Savings is used as a noun, such as 'I'm going to put some of my savings into a down payment on a car', or, 'I asked my financial advisor for a summary of my retirement savings' (Oxford learner's dictionary; examples adjusted by authors). Use of both words evidently stem from the same origin, save, and are, therefore, often explained together in dictionaries.

Conceptually, in economics saving is usually regarded as a flow concept, for example 'the part of your monthly income left over after paying all your bills'. In contrast, savings could be regarded as a stock concept, referring to an individual's 'net worth calculated by subtracting liabilities from assets' or it could be used in reference to 'savings institutions' (Poole 2007:2-3). Poole (2007) further makes the important statement that 'you may use your saving to pay down debt or add to your assets', hinting on the theoretical link between the two words.

As far as possible, it will be indicated whether the flow or the stock concept is referred to. This approach is supported by literature, typically differentiating between household saving (as measured by using the income-statement approach or the flow measure), and household wealth (as measured by a balance-sheet method or the stock measure).

Overview of the System of National Accounts

Similar to the way in which organisations are required to record their business activities according to a set of generally accepted accounting principles, so too a system was developed allowing countries to record their macro-economic activity according to a standard internationally accepted statistical framework. According to the United Nations (UN) website, the SNA is defined as a: 'statistical framework that provides a comprehensive, consistent and flexible set of macroeconomic accounts for policymaking, analysis and research purposes'. The SNA is a joint project produced and released under the auspices of the UN, the European Commission (EC), the Organisation for Economic Coordination and Development (OECD), the International Monetary Fund (IMF) and the World Bank Group (WBG) (United Nations, 2009: iii).

For most countries, this official framework of reporting economic activity began during or after World War II. For example, the first official National Accounts for the United States were published in 1942 (Mohr 2016:18). South African National Accounts data are available from 1946, and the latest version of the accounts is the 2008 SNA, which replaced the 1993 version (SARB 2015). The full set of national accounts includes various items such as NIPA, input-output tables, the NFA, national balance sheets and the Balance of Payments (BoP). The responsibility for compiling these accounts was traditionally divided between Statistics South Africa (production and income) and the SARB (expenditure, as well as institutional sector accounts, balance sheets and accumulation accounts) (Orthofer 2015:16), but Statistics South Africa now also prepares the expenditure accounts.

In defining the household sector in South Africa, it is important to note that, not only are private households included in the SNA, but also unincorporated business enterprises of households, non-profit institutions serving households (NPISHs), as well as private trusts and friendly societies. The justification for including unincorporated businesses is based on the unlimited liability of owners, meaning that household assets are at risk in the case of bankruptcy. NPISH, private trusts and friendly societies are included because the boundaries between them and private households are not always clear (Orthofer 2015:11).

There is a possibility that the SARB in future may exclude all, or at least some of these four additional items mentioned, thus focusing on households only. Such an approach should be welcomed, as various items currently included (e.g. depreciation or rent on subsoil assets), are linked to the related enterprises and institutions, which creates confusion.

The income-statement approach

The flow measure of household saving relates to the concept that saving is the part of income not consumed, and is sometimes described as 'abstinence' or 'postponed consumption'. In accounting terms, it is a flow measure typically found in the income statement of entities. An example often used to illustrate the term relates to changes in the water level of a dam, where the flow of water in and out of a dam is measured over a specific period of time, expressed as a rate. The flow concept dominated the saving literature in most countries after World War II, predominantly due to the availability of data.

From a theoretical perspective, saving in the household sector, in its most basic form, is represented by:

Where:

S: Household saving (gross saving)

Y: Household disposable income2

C: Household consumption expenditure

(Hodgetts et al. 2006:9).

However, provision is also made for the consumption of fixed capital (CFK, depreciation of the household sector's capital stock; or housing stock). This reflects the amount that households need to invest annually to maintain their stocks' productivity. From this, net saving (SN) can be calculated as follows:

Where CFK is the depreciation in the housing stock.3

Household saving is recorded in the production, distribution and accumulation accounts for households and NPISHs (see Table 1). It includes six accounts, namely the production account, generation of income account, allocation of primary income account, secondary distribution of income account, use of disposable income account and capital account.4 The first five of these accounts enable the calculation of the gross (and net) saving of households, and is discussed further below.

The first account, the production account, shows the net output of production when production is defined as an activity that 'uses inputs of labour, capital, and goods and services to produce outputs of goods and services' (United Nations 2009:95). An example is subsistence agriculture or other forms of agricultural production, part of which is consumed by the household itself (intermediate production). As this is often part of the informal sector, it provides various measurement challenges (United Nations 2009:466). Output, less intermediate consumption, is stated as gross value added at basic prices (see Table 1).

The second account, the generation of income accounts, is merely an extension of the production account as more production costs and subsidies are taken into consideration. It views households in their capacity as producers, whose activities generate primary incomes (United Nations 2009:131).5 The costs include labour costs (compensation of employees6) and taxes on production. This gives the gross operating surplus of household production. In 2018, the gross operating surplus contributed 21.2% to the gross disposable income of households.

The third account, the allocation of primary income account, shifts the focus from households as producers to their capacity as recipients of primary incomes. Included in this account is the most prominent source of household income, namely the compensation of employees. The account also includes property income received and paid. Compensation of employees equalled 79.1% of the gross disposable income of households in 2018. Compared over time to the size of the economy, compensation of employees dropped from just below 50.0% in 1998 to 43.5% in 2002. It remained at, or close to this level, until 2007, after which it started to recover. By 2018, it was 47.6% of GDP.

Property income received, reached a high of 18.2% of GDP in 1998. It declined with a noticeable drop of 4.0 percentage points from 2008 to 2010, linked to the slump during the 2008 and 2009 Global Financial Crisis (GFC) also causing an economic recession in South Africa. The slowdown narrowed the gap between property income received and paid, thus placing pressure on household income.

The fourth account is the secondary distribution of income which deals with current transfers or instances in which income is received, without any goods exchanging hands or services rendered (United Nations 2009:157). This differs from the primary income account in which actual goods or services are provided by households in exchange for compensation. Prominent items in this account include social assistance payments, as well as taxes on income and wealth.

Social benefits received, include current transfers to households by government. This item equalled 14.8% of gross disposable income in 2018. Compared to the size of the economy, social benefits received, rose sharply from 6.8% of GDP in 2005 to 9.8% in 2015. Of important is that although social assistance payments7 are included here, social benefits received are defined more broadly and also include, for example, payments made in respect of sickness, unemployment, housing, education or family circumstances (United Nations 2009:172).

Also evident from this account is the impact of taxes on income and wealth, measuring 17.2% of gross disposable income during 2018. Looking at the trend over time, it rose from 7.6% of GDP in 2005 to 10.3% in 2018. Personal income tax (PIT) has been contributing a relatively larger share of total government revenue over time, while the highest marginal tax rate of PIT was increased to 41.0% in 2016, and to 45.0% again in 2017.

Social contributions paid, should not be regarded as the counterpart of social benefits received, and are defined as 'actual or imputed payments to social insurance schemes', which also include voluntary contributions, or those made by employers on behalf of their employees (United Nations 2009:158).

Gross disposable income of households forms the last line item in the secondary distribution of income account and decreased from 62.8% of GDP in 1998 to 56.4% of GDP in 2008. Thereafter it improved again to 60.1% of GDP in 2018. Income usually has an important impact on saving which the World Bank (2011:27-28) refers to as the 'income channel of saving'. The Bank notes that the size of the impact depends on the level of a country's development and whether economic agents view movements in income of a transitory nature, or regard it as a permanent change. In its analysis, the World Bank concluded that the role of household income growth in South Africa was insufficient ('it did not play as major a role, as it could have') to support household saving.

The focus shifts in the fifth account to how households utilise their income, aptly named the use of disposable income in the households' accounts. The account consolidates three important concepts namely household income, consumption and saving (United Nations 2009:179). Household income (line item total available household resources8) declined from 67.3% of GDP in 1997 to 61.3% in 2018 while consumption (final consumption expenditure of households) declined from 63.3% of GDP in 1997 to 59.9% in 2018 (see Figure 1). Therefore, disposable income of households, as measured against the size of the economy, decreased at a faster pace. This means that the financial buffer (or gap) that existed between households' income and spending during the 1990s and early 2000s, was wiped out by 2006.

Possible reasons for the disappearance of the buffer are provided by the BANKSERV Disposable Salary Index (BDSI), which mentions that although gross salary increases in general have been above the rate of inflation since the early 2000s, expenditure pressures were also severe, especially those related to income tax, medical aid and Unemployment Insurance Fund (UIF) contributions (Bankserv Africa 2016). A further detailed analysis of these and other possible drivers of household income and expenditure remain important research objectives, but fall outside the immediate scope of this paper.

The gap between consumption expenditure and household resources increased somewhat during 2008 to 2010 and again towards the end of the analysis period. However, the size of the gap remains less than half the size it was during the late 1990s (see Figure 1).

Household saving (gross saving) is calculated as the difference between income and consumption. In nominal terms, it amounted to R18.1 billion and R67.1 bn., in 1995 and 2018 respectively, with an average of R28.4 bn. recorded during the period. Compared to the size of the economy, gross saving declined notably after 1995, but has been recovering somewhat since 2014 (see Figure 2).

To determine net saving, depreciation (or the CFK, at replacement value) has to be factored in. Depreciation remained very stable from 1995 to 2018, averaging around 1.6% of GDP.

The net saving of households declined from 2.4% of GDP in 1997 to a negative (dissaving) −1.4% in 2007; that is at the height of the strong economic growth spurt South Africa experienced at the time.9 It seems likely that the GFC imparted some caution to both banks (limiting their credit extension) and consumers (more prudent management of their household finances), as net saving 'improved' to −0.3% of GDP by 2009. Evidence of this improvement is revealed by domestic private sector credit extension which declined from an average rise of 21.3% in 2008, to merely 6.8% in 2009 (in addition, actual negative year-over-year figures were recorded during the first quarter of 2010) (SARB 2021). However, as soon as the economy regained traction (around 2010), net saving again declined to −1.4% in 2013. It did improve somewhat towards the end of the analysis period, albeit mostly in negative territory still.

The balance-sheet approach

The balance-sheet approach views household savings as the accumulation of wealth, and is therefore a stock concept measured at a specific point in time. Formal (or standardised) measures and accounting practices related to the household balance sheet have been lacking in the national accounts (both globally and in South Africa), and evidence of research aimed at reliable estimating techniques for South Africa could only be found from the mid-2000s onwards. Still, South Africa remains one of the first emerging market countries to have incorporated household balance-sheet estimates into its SNA. These figures have since been recalculated (backdated) to 1975 (Aron & Muellbauer 2006; Orthofer 2015:1-3, 16, 33). In this article the figures of the SARB for the period 1995 to 2018 are used.

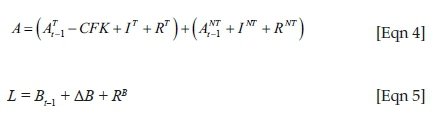

Household wealth (W) is calculated as the market value of assets (A), less liabilities (L), or in mathematical terms:

Household assets can be defined as:

[A] store of value representing a benefit or series of benefits accruing to the economic owner by holding or using the entity over a period of time. It is a means of carrying forward value from one accounting period to another. (United Nations 2009:39)

For most assets, there is a corresponding liability, defined as being established when:

[O]ne unit (the debtor) is obliged, under specific circumstances, to provide a payment or series of payments to another unit (the creditor). (United Nations 2009:39)

From a theoretical perspective, strong emphasis is placed on the distinction between tangible (e.g. residential property) and non-tangible (financial) assets. Using these concepts, the determinants of Equation 3 can be further refined as follows:

Where:

A: The value of tangible and non-tangible assets (AT + ANT)

: The value of tangible assets (capital stock) in the previous period

: The value of tangible assets (capital stock) in the previous period

: The value of non-tangible assets in the previous period

: The value of non-tangible assets in the previous period

CFK: Consumption of fixed capital

IT: Investment in tangible assets

INT: Investment in non-tangible assets

RT: Revaluation of tangible assets

RNT: Revaluation of non-tangible assets

RB: Revaluation of borrowed amount

Bt−1: Level of borrowing in the previous period

(Hodgetts et al. 2006:25-26).

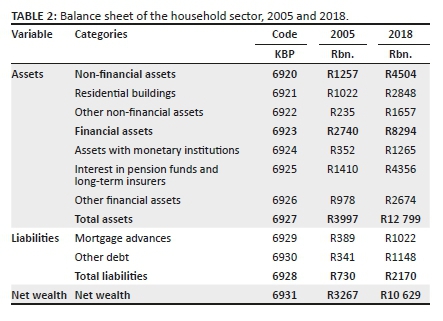

The SARB uses the same concepts to present the household balance sheet, but refers to non-tangible assets as financial assets, while tangible assets are called non-financial assets. Non-financial assets include items such as residential buildings, while financial assets include various bank deposits, interest in pension funds and long-term insurers, and even foreign assets. On the liability side of the household balance sheet, mortgage advances and other debt (including instalment sale and leasing, as well as personal loans) are listed (for a detailed list of all household assets and liabilities included by the SARB see Kuhn 2010).

Table 2 provides the balance sheet data of the household sector for 2005 and 2018 respectively. Over time, and compared to the size of the economy, total household assets performed strongly during the early 2000s as it rose from 217.5% of GDP in 2002 to 295.7% in 2006. It declined during the GFC but by 2018 it had again recovered slightly to 262.6% of GDP (see Figure 3). The category for financial assets, is the largest household asset category and contributed two-thirds (64.8%) to total assets in 2018, while non-financial assets contributed only 35.2%.

Interest in pension funds and long-term insurers is the largest financial asset class and contributed 52.5% to financial assets for 2018 (it is also the largest of all asset classes, both non-financial and financial). Looking at this item's performance over time, a distinctive 'W' pattern is evident, as interim high points were reached during 2006 (96.7% of GDP) and 2014 (100.0% of GDP) respectively. This is most likely linked to strong bull runs in local equities, experienced in both these periods. After 2014, the item decreased notably to 89.4% of GDP in 2018.

Non-financial assets are driven strongly by the residential property market, and the housing boom experienced during the early 2000s in the South African economy is clearly visible in the data. Residential property assets almost tripled from R528 bn. in 2002 to R1.5 trillion in 2008. Compared to the size of the economy, residential buildings peaked at 68.5% of GDP in 2007. Following the GFC, this item decreased to 58.0% of GDP in 2012, after which it again increased marginally, but remained well below its previous peak.

On the liability side, mortgage advances to households contributed roughly half (47.1%) to total liabilities, while the other half is made up of other debt items, including instalment sale and leasing, as well as personal loans (see Table 2). Mortgage advances rose especially strongly around the residential property boom of 2003 to 2007. Thereafter the demand for mortgages had been muted, as the item dropped from 32.4% of GDP in 2007 to 21.0% in 2018.

In contrast to this, the demand for other debt items (such as instalment and leasing credit, personal loans and open accounts) showed an upward trend and caught up with mortgages in 2014, after which it remained the main household liability. Prinsloo (2000:21) noted that an inverse relationship could be expected between consumer credit and saving. Various researchers tested this empirically and found evidence of a negative (inverse) correlation between the liberalisation (expansion) of credit markets and household saving in South Africa (see, for instance, Aron & Meullbauer 2000, 2012; Harjes & Ricci 2005; Viegi 2014:134-136).

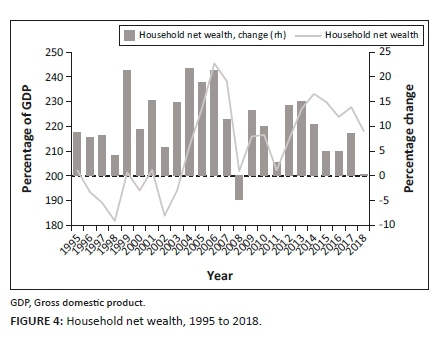

The focus now falls on net wealth that is calculated as assets less liabilities. Compared to the size of the economy, net wealth in South Africa peaked in 2006 at 245.4% of GDP. It dropped to 201.9% of GDP in 2008, as the GFC impacted on asset valuations. A distinctive 'W' pattern is evident again between 2007 and 2014 as wealth fluctuated in accordance with economic growth and financial market trends during the period. A notable improvement is evident during 2012 to 2014. However, after 2014 net wealth shows mostly a declining trend and in 2018 it measured 218.1% of GDP, or roughly the same level as it was during 2012 (see Figure 4).

Another measure is to look at how household net wealth changed on an annual basis. This indicates an average annual nominal increase of 10.3% for the period 1995 to 2018. The strongest performances were measured during 1999, 2004 and 2006, all of which recorded rises above 20.0% year over year. The only negative value was recorded in 2008, which measured −4.8%, while in 2018 a rise of merely 0.3% was recorded (see Figure 4).

Compared on a pre- and post-GFC basis, it is evident that the nominal rise in household wealth had been weaker post-GFC, as it averaged 8.4% (2009 to 2018), compared to an average of 11.7% before the crisis (inflation did average around 1.0 percentage point higher during the pre-GFC period). Interestingly, the weakness post-GFC has been more prominent in the non-financial asset category as it rose by an average of 6.4% (2009 to 2018), while financial assets rose 8.9% during the same period. Pre-GFC, non-financial assets recorded exceptionally strong rises on an average of 14.8%, while financial assets rose with 11.1%. The next section determines whether or not any 'flow through' occurred by linking household saving to wealth.

The link between household saving and wealth

The link between the income-statement and the balance-sheet approaches is important because it enables analysts to determine the extent to which households' decisions in one time period effect their financial circumstances in another time period, or more specifically, to identify how saving decisions effect the accumulation of wealth.

Given that saving is a flow concept and wealth a stock concept, the link between these two concepts only becomes evident when time (e.g. change in wealth over a given period) is factored into the analysis. An identity may be used to assist in this regard. It relates to the fact that investment is financed from one of three sources, namely from current income, by borrowing or by capital transfers,10 which equals:

Where:

IT: Investment in tangible assets11

INT: Investment in non-tangible assets12

S: Gross saving

ΔB: Net change in household borrowing

CT: Capital transfers (including those from overseas)

(Hodgetts et al. 2006:25).

By subtracting liabilities from assets (that is subtract Equation 5 from Equation 4), and using the identity provided in Equation 6, it can be shown that:

W = W-1 + RNET + SN + CT

Or stated differently:

Where:

ΔW: Change in wealth (Wt - Wt-1)

RNET = RT + RNT - RB (net revaluations)

SN = Y - C - CFK

(Hodgetts et al. 2006:26).

The three theoretical factors contributing to the change in household wealth are: net revaluations, net saving and capital transfers. Alternatively, yet similar to this, Orthofer (2015:5) defines the change in household wealth in more detail as:

Where:

SS,t: Stock of savings (changes in wealth)

SF,t: Flow of saving ('saving-induced wealth')

: Asset revaluations

: Asset revaluations

Kt: Capital transfers

Ot: Other13 factors

Both Hodgetts et al. (2006) (see Equation 7) and Orthofer (2015) (see Equation 8) list the three factors contributing to the changes in household wealth as net revaluations, net saving and capital transfers; however, Orthofer (2015) also explicitly includes a fourth, namely 'other factors' (e.g. destruction or a discovery).

Net saving represents the part of disposable income that is not spent on consumption expenditure. When positive, it can be used 'to acquire non-financial or financial assets of one kind or another, including cash, or to repay liabilities'. But when negative, 'the excess must be financed by disposing of assets, or incurring new liabilities' (United Nations 2009:197). Stated differently, a high level of saving should mean that net worth and assets could be acquired without increasing debt. Conversely, in a situation of low savings (or dissaving), wealth should be reduced, ceteris paribus, and existing assets be decreased and/or liabilities will have to be increased (Hodgetts et al. 2006).

Using the methodology of Hodgetts et al. (2006), the change in South African households' net wealth is calculated using three factors, namely net saving, revaluations and capital transfers. Net-saving and capital-transfer data are available from the SARB; however, the revaluation of assets is treated as a balancing14 item.

The contribution of net saving to the acquisition of wealth peaked in 1998 at 24.0%, after which the contribution of saving declined to the point where it turned negative in 2006 (see Table 3). In other words, households were increasing their borrowing and/or utilising existing wealth. In 2017, saving again made a small positive contribution, but this turned negative once more in 2018.

The prominence of the net revaluation of assets (treated as the balancing item in the calculation) is evident as it alone explains almost all the movements in the change of wealth, especially from the mid-2000s onwards. It is very likely that the stellar rise in residential property prices and equity markets are responsible for the bulk of the revaluation adjustments.

The contribution of capital transfers remains rather insignificant throughout the respective time, with exceptions in 2008, 2011 and 2018, during which the contribution was almost half (49.0%). This was, however, due to weak or negative changes in net wealth recorded during these periods. The 2018 value clearly indicated how sensitive this type of analysis is and confirmed the need for an improved (or a more insightful) methodology and data linking saving to wealth.

International evidence supports these findings and suggest that asset revaluations are often the most important driving factor for household wealth. Hodgetts et al. (2006) analysed data for New Zealand and indicated how the revaluation effect completely 'swamped' other factors between 2002 and 2005. The problem is that this could fluctuate significantly according to, among other factors, different accounting principles (e.g. book or market values), to the point where it could be regarded as merely 'paper profits'. Orthofer (2015:4) ran a similar test and found that between 1975 and 2014, South African real net household saving accounted for merely 15.0% of the increase in real household wealth.

During a discussion with employees of the SARB, they also expressed caution about the various assumptions and estimates included in the calculation. However, they simultaneously confirmed that for the time being these calculations are based on the best available data. They also indicated that they are in the process of a major overhaul regarding various aspects of the household-sector data. Hopefully, future data from the SARB will enable analysts to 'close the elusive loop' between household saving and household wealth.

Conclusion

A descriptive analytical methodology is used to highlight the trends in household saving and wealth (savings) in South Africa for the period 1995 to 2018. It further links the two concepts by providing empirical estimates of the 'flow-through' effects, in the form of a decomposition of wealth.

Household saving, as measured by the income statement approach, indicates a long-term declining trend in net household saving to GDP. Since 2006 it turned negative (dissaving). This decline stabilised around 2008, as net household saving fluctuated around the −1.0% to GDP level since then, and actually improved to record a small positive value of 0.1% of GDP in 2017. However, the latest available value for 2018 indicates a small dissaving again.

There are two major determinants of this trend, namely disposable income of households and final consumption expenditure of households. Compared to GDP, both of these have been trending downwards, but over time the difference or buffer that existed between them had been eroded to the point where it disappeared in 2006. However, after 2010 the downward trend in both the disposable income of households and final consumption expenditure of households stabilised somewhat, which also explains the stabilisation in the saving rate.

Compared to the size of the economy, household wealth in South Africa peaked in 2006 at 245.4% of GDP. The GFC had a significant impact, and household wealth dropped to 201.9% of GDP in 2008. Some recovery occurred around 2012 to 2014; however, net wealth had been mostly on a declining trend since then and in 2018 measured 218.1% of GDP. As far as annual performance, households' wealth rose by an average nominal increase of 10.3% for the period 1995 to 2018.

Lastly, an analysis of the link between saving and wealth shows that the contribution of net saving to the acquisition of wealth peaked in 1998, after which it declined and turned negative in 2006. The prominence of the net revaluation of assets in the change of wealth is confirmed as it explains almost all the movements, especially from the mid-2000s onwards. Drivers for the revaluations include a strong rise in the valuations of residential property values and equities.

Future research should focus in more detail on the factors driving household income and expenditure trends in South Africa, and whether they are sustainable. Also important is the role that household saving plays (or should play) in total saving in the economy, as well as what an optimal mix between the major saving categories (including households, businesses and government) should be.

Acknowledgements

Competing interests

The authors have declared that no competing interest exists.

Authors' contributions

All authors contributed equally to this work.

Ethical considerations

Ethical clearance was obtained from Unisa, School of Economic Sciences, Research Ethics Review Committee. Ethical clearance number: 2016_CEMS_SES_001.

Funding information

This research received no specific grant from any funding agency in the public, commercial, or not-for-profit sectors.

Data availability

Data sharing is not applicable to this article as no new data were created or analysed.

Disclaimer

The views and opinions expressed in this article are those of the authors and do not necessarily reflect the official policy or positions of any affiliated agency of the authors.

References

Aron, J. & Muellbauer, J., 2000, 'Personal and corporate savings in South Africa', World Bank Economic Review 14(3), 509-544. https://doi.org/10.1093/wber/14.3.509 [ Links ]

Aron, J. & Muellbauer, J., 2006, 'Estimates of household sector wealth for South Africa. 1970-2003', Review of Income and Wealth 52(2), 285-307. https://doi.org/10.1111/j.1475-4991.2006.00188.x [ Links ]

Aron, J. & Muellbauer, J., 2012, 'Wealth, credit conditions and consumption: Evidence from South Africa', CEPR Discussion paper No. 8800. [ Links ]

Aron, J., Muellbauer, J. & Prinsloo, J., 2006a, 'Estimating household-sector wealth in South Africa', South African Reserve Bank, Quarterly Bulletin 2006, 61-72. [ Links ]

Aron, J., Muellbauer, J. & Prinsloo, J., 2006b, 'Estimating the balance sheet of the personal sector in an emerging market country', United Nations University working paper No. 2006/99, September 2006. [ Links ]

Bankserv Africa, 2016, Average salaries, pensions barely grow above inflation, viewed 07 September 2017, from https://www.bankservafrica.com/Press-Office/ArticleId/118/average-salaries-pensions-barely-grow-above-inflation?category=\bdsi [ Links ]

Harjes, T. & Ricci, L., 2005, 'What drives savings in South Africa?' in M. Nowak & L.A. Ricci (eds.), Post-apartheid South Africa: The first ten years, International Monetary Fund, Washington, DC. [ Links ]

Hodgetts, B., Briggs, P. & Smith, M., 2006, 'Household saving and wealth. Reserve Bank of New Zealand', paper prepared for Reserve Bank Workshop titled 'Housing, Savings and the Household Balance Sheet', Wellington, 14th November, viewed 10 May 2017, from https://www.rbnz.govt.nz/research-and-publications/speeches/2006/speech2006-09-27 [ Links ]

Kuhn, K., 2010, 'Note on household wealth in South Africa', South African Reserve Bank, Quarterly Bulletin 2010, 66-73. [ Links ]

Mohr, P., 2016, Economic indicators, 5th edn., Van Schaik Publishers, Pretoria. [ Links ]

Orthofer, A., 2015, 'What we talk about when we talk about savings: Concepts and measures of household saving and their application to South Africa, Economic Research Southern Africa', ERSA working paper No 530, Claremont, Cape Town, July 2015, viewed 16 September 2021, from https://www.econrsa.org/system/files/publications/working_papers/working_paper_530.pdf [ Links ]

Orthofer, A., 2017, 'Concepts and measures of saving: Selected issues for South Africa', South African Journal of Economics 85(2), 222-241. https://doi.org/10.1111/saje.12129 [ Links ]

Oxford Learners Dictionaries, 2020, Oxford Advanced Learner's Dictionary, viewed 06 July 2020, from https://www.oxfordlearnersdictionaries.com/ [ Links ]

Poole, W., 2007, 'U.S. Saving. Federal Reserve Bank of St. Louis, Speech 111', Presented to the CFA Society of Nebraska, Omaha, Nebraska, 15th February 2007, viewed 06 July 2020, from https://ideas.repec.org/e/ppo114.html [ Links ]

Prinsloo, J.W., 2000, The saving behaviour of the South African economy, South African Reserve Bank, Pretoria, Occasional Paper No.14, November 2000. [ Links ]

South African Reserve Bank (SARB), 2015, 'South Africa's national accounts 1946-2014: An overview of sources and methods', Supplement to the South African Reserve Bank Quarterly Bulletin, March 2015. [ Links ]

South African Reserve Bank (SARB), 2016, Quarterly bulletin, No 280, June, South African Reserve Bank, Pretoria. [ Links ]

South African Reserve Bank (SARB), 2021, Statistical releases, viewed 12 August 2021, from https://www.resbank.co.za/en/home/what-we-do/statistics/releases/selected-statistics [ Links ]

United Nations, 2009, System of National Accounts 2008-2008 SNA, United Nations, viewed 26 January 2017, from http://unstats.un.org/unsd/nationalaccount/sna2008.asp [ Links ]

Viegi, N., 2014, '(Dis)saving in South Africa', in H. Bhorat, A. Hirsch, R. Kanbur & M. Ncube (eds.), The Oxford companion to the economics of South Africa, pp. 134-139, Oxford University Press, Oxford. [ Links ]

World Bank, 2011, 'South Africa economic update: Focus on savings, investment and inclusive growth', Issue 1, July 2011, viewed 20 October 2016, from http://documents.worldbank.org/curated/en/115621468115472034/South-Africa-economic-update-focus-on-savings-investment-and-inclusive-growth [ Links ]

Correspondence:

Correspondence:

Stephanus Joubert

sjjoube@unisa.ac.za

Received: 15 July 2020

Accepted: 30 Aug. 2021

Published: 26 Oct. 2021

1 . Findings in this article form part of a doctoral thesis, which was shared by one of the authors with the South African Reserve Bank, during a meeting on 26 July 2017. Feedback from this meeting has been incorporated into the thesis and this article. The authors thank the members of the SARB for their inputs.

2 . Also referred to as 'total available household's resources', (SARB 2016:S-132, KBP6847).

3 . Also referred to as 'consumption of fixed capital at replacement value' (see SARB 2016:S-132, KBP6849).

4 . The capital account looks at the changes in assets held by households, specifically the 'values of non-financial assets that are acquired, or disposed of' (United Nations 2009:195).

5 . Households and non-profit institutions serving households.

6 . This item relates to the compensation of employees by unincorporated enterprises owned by households (United Nations 2009:131). It should not be confused with the compensation of employee's item, recorded in the primary income account.

7 . Social assistance payments rose from around 2.5% of GDP in 2005 to 3.0% in 2015.

8 . Total available household resources is calculated by adjusting gross disposable income with two items namely the change in the net equity of households in pension fund reserves and a residual (a statistical discrepancy between the expenditure components of GDP [SARB 2016]).

9 . South Africa's GDP rose on average by more than 5.0 per cent per year during the period 2004-2007 (SARB).

10 . Capital transfers are cash injections into the household sector, which is not part of current income, for example, capital transfers by immigrants (Hodgetts et al. 2006:9).

11 . This item includes houses and flats (Hodgetts et al. 2006:9).

12 . This includes financial assets (Hodgetts et al. 2006:9).

13 . Examples of other factors can be the 'result of the discovery of a subsoil resource or the destruction of assets as a result of war or a natural disaster' (United Nations 2009:330).

14 . Orthofer (2015:21) encountered a similar challenge and lamented the fact that a fully integrated set of national accounts (from which this type of data could simply be read) had not yet been published by the SARB.