Serviços Personalizados

Artigo

Inglês (pdf)

Inglês (pdf)

Artigo em XML

Artigo em XML Referências do artigo

Referências do artigo

Indicadores

Links relacionados

-

Citado por Google

Citado por Google -

Similares em Google

Similares em Google

Compartilhar

Permalink

PermalinkSouth African Journal of Economic and Management Sciences

versão On-line ISSN 2222-3436

versão impressa ISSN 1015-8812

S. Afr. j. econ. manag. sci. vol.20 no.1 Pretoria 2017

http://dx.doi.org/10.4102/sajems.v20i1.1247

ORIGINAL RESEARCH

Effect of earnings management on economic value added: G20 and African countries study

Zhen-Jia Liu; Yi-Shu Wang

Department of Accounting, School of Business, Changzhou University, China

ABSTRACT

BACKGROUND: Economic value added (EVA) may reflect true performance compared with other conventional accounting indices, it is still measured through financial statements. It is highly probable that EVA motivates managers to manipulate earnings.

AIM: The main contribution of this study is the analysis of the association between earnings management and EVA. This study provides shareholders, lenders and creditors (or other categories of investors) with a method for analysing the value of enterprises.

SETTING: We analyse the association between earnings management through real earnings management (REM) or discretionary accrual (DA) activities and the EVA by African and the Group of Twenty (G20) nations.

METHODS: The sample for this study was obtained from the COMPUSTAT database between 2009 and 2013. This study also adopted the ordinary least squares (OLS) method.

RESULTS: The results indicate that a significantly positive relationship exists between earnings management through DA items and EVA in African nations. In addition, a significantly negative relationship exists between earnings management through DA items or REM activities and EVA in G20 nations.

CONCLUSION: Our results provide critical implications for managers, researchers, investors and regulators of various nations; for example, managers may determine whether to increase the EVA through earnings management, researchers may analyse varying degrees of REM activities and DAs existing in the same nation groups or regulators may determine how to establish laws or rules to prevent earnings management because it is likely that differences in national development, culture or politics exist in these nations.

Introduction

Conventional accounting indices are used for measuring firm performance (Allgood & Farrell 2003; Bailey & Helfat 2003; Neumann & Voetmann 2005; Peng 2004; Shen & Cannella 2003). Such measurements are determined in accordance with Generally Accepted Accounting Principles (GAAP), requiring conservatism in preparing financial statements.

Economic value added (EVA) was proposed as an estimate of a firm's economic profit. The basic concept of EVA is that economic profit is created when the return on a firm is higher than the firm's capital cost (Mahdavi & Rastegari 2007). Therefore, EVA is used to calculate shareholder value (Kaur & Narang 2008).

Earnings management is when managers exercise judgement in financial reporting and in structuring transactions to adjust financial reports (Healy & Wahlen 1999). Several studies have focused on determining whether earnings management exists and on identifying the motive for managing earnings (e.g. Anjum et al. 2012; Brown & Higgins 2001; Caton et al. 2011; Chang, Hsin & Hou 2013; Chiu et al. 2013; Datta, Iskandar-Datta & Singh 2013; Degeorge et al. 2013; Essid 2012; Farrell, Unlu & Yu 2014; Francoeur, Amar & Rakoto 2012; Habib, Bhuiyan & Islam 2013; Hansen 2010; He, Yang & Guan 2011; Jha 2013; Kangarluei, Motavasse & Abodllahi 2011; Karampinis & Hevas 2013; Kim & Sohn 2013; Lin & Wu 2014; Nagata 2013; Salteh & Valipour 2012; Shu & Chiang 2014; Wu, Lin & Fang 2012; Zhang & He 2013).

Although EVA may reflect true performance compared with other conventional accounting indices, it is still measured through financial statements. Therefore, it is highly probable that EVA motivates managers to manipulate earnings. The main contribution of this study is the analysis of the association between earnings management and EVA. This study provides shareholders, lenders and creditors (or other categories of investors) with a method for analysing the value of enterprises.

The Group of Twenty (G20) is an international forum from 20 major economies. Collectively, the G20 economies account for approximately 85% of the gross world product (GWP), 75% of world trade (if all European Union intra-trade is excluded) and two-thirds of the world's population. Africa is the world's poorest and most underdeveloped continent. The 2003 United Nations Human Development Report indicated that the bottom 25 ranked nations were all African.

Because countries have relatively distinct governments, cultures, laws and economic conditions, enterprises operate in unique systems and environments; therefore, they cannot be considered equivalent. In this study, we developed a regression model and compared the relationship between earnings management and EVA among organisations in African1 and G202 nations.

Literature review

Economic value added

Stewart (1991) revised the computation of residual income and established a methodology for computing EVA. However, Parvaei and Farhadi (2013) reported that historical EVA offers low predictability for performance measured using return on equity (ROE), return on assets (ROA) or other metrics, and free cash flow has slightly superior predictability compared with other measures.

Huynh, Gong and Nguyen (2013) investigated the integration of activity-based costing (ABC) with EVA as an approach to measure firm performance. They proved that the EVA-ABC method is an innovation management accounting approach.

Regarding the factors influencing EVA, Burja and Burja (2010) revealed that EVA and resource management are interdependent. Moradi, Ghomian and Fard (2012) indicated that profitability, firm size, growth ability and intangible assets are significantly positively related to EVA, whereas capital structure is significantly negatively related to EVA. Nikbakht and Moghimi (2011) demonstrated that the active debt ratio is inversely related to EVA in manufacturers of non-metallic mineral products, construction machinery and industrial equipment. Altendorfer and Jodlbauer (2011) have indicated that fewer changes in a firm's operational personnel yield higher EVA. Haque et al. (2013) reported that dividend payout has a significantly negative relationship with EVA; this is because shareholder value theory discourages the distribution of earnings in the form of dividends because it implies management inefficiency towards maximising shareholder wealth.

Earnings management

The tools of earnings management are detailed as follows. Firstly, managers can make discretionary accrual (DA) item choices that are allowed under GAAP to reach a desired level of earnings. DAs are a component of accounting accruals and include items indicating a manager's forecasts of uncertain events. They can also be misleading when manipulated to distort public information for private gain. Dechow, Saloan and Sweeney (1995), Islam, Ali and Ahmad (2011) and Chang et al. (2013) have provided related models to measure DA items.

Secondly, managers can engage in earnings management by altering the time and scale of operating decisions. These actions deviate from normal business practices, with the primary objective of misleading stakeholders regarding a firm's economic performance. Researchers refer to the second type as real earnings management (REM) activities. On the basis of recent REM studies (e.g. Cohen, Dey & Lys 2008; Roychowdhury 2006), we considered the following three types of REM activities: (1) sales manipulation, (2) overproduction and (3) discretionary expense reduction.

The literature on accounting reports several motivations for earnings management; such motivations include mergers and acquisitions (M&A) (Francoeur et al. 2012), exchange rate exposure (Chang et al. 2013), R&D (Zhang & He 2013), product market pricing (Datta et al. 2013), distressed firm (Habib et al. 2013), board interlocks (Chiu et al. 2013), free cash flow (Kangarluei et al. 2011), investor stock returns (Wu et al. 2012), firm profitability (Anjum et al. 2012), initial public offerings (Nagata 2013), equity-based compensation (Essid 2012), seasoned bond offerings (Caton et al. 2011), private placement issuers (He et al. 2011), tax (Karampinis & Hevas 2013), seasoned equity offerings (Shu & Chiang 2014), debt covenant (Jha 2013), financing constraints (Farrell et al. 2014), analyst coverage (Degeorge et al. 2013), earnings benchmark (Hansen 2010) and corporate governance (Lin & Wu 2014).

Datta et al. (2013) revealed that firms with inferior product market pricing power in competitive industries frequently report discretionary earnings accruals. Habib et al. (2013) found that managers of distressed firms engage more in income-reducing earnings management practices than do managers of financially stable firms. Kangarluei et al. (2011) revealed a significantly positive relationship between earnings management and free cash flow, and they reported that the relationship is more significant for firms with high free cash flow, thus indicating that a firm's free cash flow can motivate managers to engage in earnings management behaviour. Wu et al. (2012) reported a negative relationship between earnings management and investor stock returns in Taiwanese firms; they attributed this phenomenon to the investment decisions made by Taiwanese stockholders, who are traditionally concerned about the quality of a firm's financial statements. Anjum et al. (2012) used a modified Jones model to calculate the DAs of companies in various sectors listed on the Karachi Stock Exchange. Their results showed that earnings management has a negative effect on firm profitability. Because they elucidated the manipulation of company profits, their study is of vital importance to managers, investors and analysts for decision-making and analysis.

Caton et al. (2011) showed that issuers tend to inflate earnings performance before an offering (seasoned bond offering). He et al. (2011) reported that earnings management serves as a likely source of investor over-optimism during private placements; moreover, they showed that income-increasing accounting accruals made during private placements predict post issue long-term stock underperformance. Degeorge et al. (2013) reported that in countries with high financial development, increased intra-firm analyst coverage engenders low earnings management.

Hansen (2010) reported that firms prefer to avoid a loss benchmark (i.e. managed earnings is above zero in time t); however, he did not consider firms just below the loss-avoidance benchmark that might be using DAs to avoid missing an alternative benchmark. Karampinis and Hevas (2013) reported that tax pressure is a significantly negative determinant of DAs in the pre-International Financial Reporting Standards (IFRS) period

Relationship between earnings management and capital costs

Salteh and Valipour (2012) indicated a significantly inverse relationship between DAs and the weighted average cost of capital. Managers attempting to avoid loss are likely to have stronger incentives to exaggerate their earnings to present a higher growth rate to generate a more positive picture of their business, which subsequently leads to diminished weighted average capital costs. Moreover, Wang, Jiang, Liu and Wang (2015) demonstrated that managers of listed firms consider that investors cannot identify earnings management through DAs; therefore, to generate a favourable image of businesses among investors, such as reduced capital cost, they are highly likely to attempt to adopt earnings management through DA items, inducing EVA to increase:

H1: Earnings management through DA manipulation of earnings has a significantly positive relationship with EVA.

Kim and Sohn (2013) determined that cost per capita is positively associated with the extent of REM activities aimed at earnings manipulation. Specifically, they argued that REM activities increase the cost of equity because of two major reasons. Firstly, REM introduces noise into reported earnings because it affects accruals in addition to distorting the cash flow through real operation-manipulating activities. Secondly, REM is more difficult to detect than Accrual earnings management (AEM) and REM activities are typically less subject to external monitoring or scrutiny. Moreover, REM is more difficult to detect using internal monitors such as the board or audit committee. Because REM might not be curtailed by effective governance mechanisms, external investors experience difficulty when evaluating firm performance. Brown and Higgins (2001) also observed that REM is positively associated with capital costs because REM distorts the fundamentals of a business. Furthermore, it increases noise or errors in earnings and reduces investor expectations on future cash flow levels. Therefore, managers of listed firms attempt to adopt earnings management through REM, which may increase the capital cost and then reduce EVA:

H2: Earnings management through REM activity manipulation has a significantly negative relationship with EVA.

Methodology

The sample for this study was obtained from the COMPUSTAT database between 2009 and 2013. This study also adopted the ordinary least squares (OLS) method. The variables and model of this study are discussed in the subsequent sections.

Independent variables: Earnings management

Discretionary accruals

Discretionary accruals has been used as a proxy for earnings management, where the absolute value of εit was adopted to measure

Where MACCit denotes the total accruals calculated as the change in non-cash current assets minus the change in current liabilities minus the depreciation expense for year t, ASSETit-1 denotes the assets for year t−eno ΔNETREVit denotes the change in net revenue for year t and PPEit denotes the gross fixed assets for year t (Wang et al. 2015). The absolute value of εit for Equation 1 denotes the Jones (1991) model for year t.

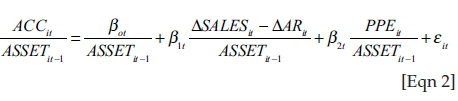

Where ACCit represents the total accruals calculated as the continuing operating net profit minus the cash flow from operations for year t, ASSETit-1 represents the assets for year t−ep ΔSALESit and represents the change in sales for year t, ΔARit represents the change in account receivables for year t and PPEit represents the gross fixed assets for year t. The absolute value of εit for the results of Equation 2 denotes the modified Jones model (Dechow et al. 1995) for year t.

Where CACit is the change in income before extraordinary items minus operating cash flow minus depreciation and amortisation expenses, ASSETit-1 is the assets for year t−s ΔREVit is the change in the net revenue for year t and ΔRECit is the change in account receivables for year t. The absolute value of εit for Equation 3 denotes the current accruals model (Louis 2004) for year t.

Real earnings management

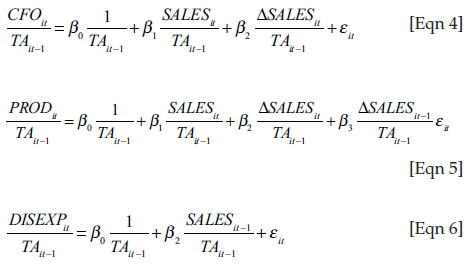

Roychowdhury (2006) developed empirical models for estimating the typical levels of real business activities, as reflected in the cash flow from operations, production costs and discretionary expenditures. We used Models 5-7 to estimate the absolute value of εit to measure the abnormal level (namely, REM).

Where CFOit is the cash flow from operations for year t; PRODit is the sum of the cost of goods for sale and change in inventory for year t; DISEXPit is the discretionary expenses according to the sum of advertising, R&D and sales, as well as general and administrative expenses for year t; TAit-1 is the assets for year t−s t SALESit is the sales for year t; ΔSALESit is the change in sales for year t; ΔSALESit-1 is the change in sales for year t−s the SALESit-1 is the sales for year t−s t The absolute value of εit for Equation 4 denotes the abnormal level of cash flow from operations for year t, the absolute value of εit for Equation 5 denotes the abnormal level of production costs for year t and the absolute value of εit for Equation 6 denotes the abnormal level of discretionary expenditures for year t.

Dependent variables: Economic value added

EVAit,1 (Unadjusted EVA): NOPATit-(WACCit×ICit)

NOPATit = Net operating profit after tax for year t= PRETAXOIit × (1-CTRit)

WACCit = weight average capital cost for year t

ICit= invest capital for year t = ASSETit - APit - NPit - AEit - PERit - OAPit - ATPit - OCLit - SSIit - CIPit

where PRETAXOIit is pre-tax operating income for year t, CTRit is the cash tax rate for year t, ASSETit is the assets for year t, APit is the account payable for year t, NPit is the notes payable for year t, AEit is the accrued expense for year t, PERit is the pre-earned revenue for year t, OAPit is the other account payable for year t, ATPit is the account tax payable for year t, OCLit is the other current liabilities for year t, SSIit is the short securities investment for year t and CIPit is the construction in process for year t (Huang & Liu 2010; Wang et al. 2015).

EVAit,2 (adjusted EVA, join adjusted items): NOPATit-(WACCit×ICit)

NOPATit = Net operating profit after tax for year t = PRETAXOIit × (1-CTRit) + UNARDit + UNAMEit + ALARit + ALLINVit + ALLSSIit

WACCit = weight average capital cost for year t

ICit = invest capital for year t = ASSETit-APit-NPit-AEit-PERit-OAPit-ATPit-OCLit-SSIit-CIPit+UNARDit+UNAMEit+ALARit+ALLINVit+ALLSSIit

Where PRETAXOIit is pre-tax operating income for year t, CTRit is the cash tax rate for year t, UNARDit is un-amortisation research and development expense3 for year t, UNAMEit is un-amortisation marketing expense for year t,4ALARit is the allowance for account receivable for year t, ALLINVit is the allowance for loss on inventory for year t and ALLSSIit is the allowance for loss on short-term investment securities for year t. ASSETit is the assets for year t, APit is the account payable for year t, NPit is the notes payable for year t, AEit is the accrued expense for year t, PERit is the pre-earned revenue for year t, OAPit is the other account payable for year t, ATPit is the account tax payable for year t, OCLit is the other current liabilities for year t, SSIit is the short securities investment for year t and CIPit is the construction in process for year t.

EVAit,3 (adjusted EVA, (join adjusted items and economic depreciation adjusted items): NOPATit-(WACCit×ICit)

NOPATit = Net operating profit after tax for year t = PRETAXOIit × (1-CTRit) + UNARDit + UNAMEit + ALARit + ALLINVit + ALLSSIit ± ECONDEPRit

WACCit = weight average capital cost for year t

ICit = invest capital for year t = ASSETit - APit - NPit - AEit - PERit - OAPit - ATPit - OCLit - SSIit - CIPit + UNARDit + UNAMEit + ALARit + ALLINVit + ALLSSIit

Where PRETAXOIit is pre-tax operating income for year t, CTRit is the cash tax rate for year t, UNARDit is un-amortisation research and development expense for year t, UNAMEit is un-amortisation marketing expense for year t, ALARit is the allowance for account receivable for year t, ALLINVit is the allowance for loss on inventory for year t and ALLSSIit is the allowance for loss on short-term investment securities for year t. ECONDEPRit is the economic deprecation adjusted items for year t,5ASSETit is the assets for year t, APit is the account payable for year t, NPit is the notes payable for year t, AEit is the accrued expense for year t, PERit is the pre-earned revenue for year t, OAPit is the other account payable for year t, ATPit is the account tax payable for year t, OCLit is the other current liabilities for year t, SSIit is the short securities investment for year t and CIPit is the construction in process for year t.

In addition, weight average capital cost for year t:

where IEit is the interest expense for year t, DEBTit is the liabilities for year t, ASSETit is the assets for year t, TAXit is the tax rate for year t and EQUITYit is the equity for year t. COEit is the cost of equity measured using the capital asset price model for year t through Rf +β(Rm-Rf), Rf is the risk-free fixed deposit interest rate in 1 year for year t, β is the risk coefficient for year t and Rm is the return of market portfolio for year t (i.e. a section of the stock market index).

Control variables

Moradi et al. (2012) demonstrated that capital structure, profitability, firm size, firm growth and intangible assets have significantly effect on EVA. We used debt ratio (i.e. capital structure), ROE (i.e. profitability), sales (i.e. firm size), asset growth (i.e. firm growth) and intangible assets (i.e. firm innovation) to measure control variables.

Empirical model

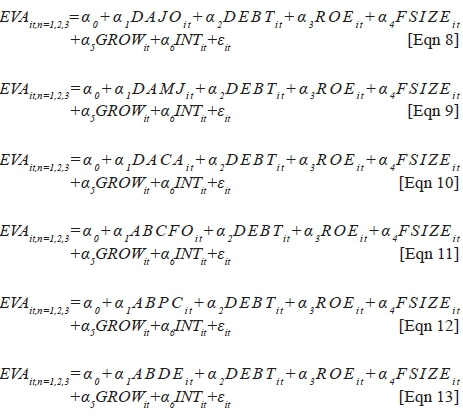

where DAJOit denotes the Jones model for year t (Equation 1), DAMJit denotes the modified Jones model for year t (Equation 2), DACAit denotes the current DAs for year t (Equation 3), ABCFOit denotes the abnormal level of cash flow from operations for year t (Equation 4), ABPCit denotes the abnormal level of production costs for year t (Equation 5), ABDEit denotes the abnormal level of discretionary expenditures for year t (Equation 6), EVAit,n = 1,2,3 denotes the EVA (n = 1 for unadjusted EVA; n = 2 for adjusted EVA, join adjusted items and n = 3 for adjusted EVA, join adjusted items and economic deprecation adjusted items), DEBTit denotes a firm's debt ratio for year t, ROEit denotes the equity of average assets for year t, FSIZEit denotes the sales for year t, GROWit denotes the asset growth rate for year t and INTit denotes the intangible assets for year t.

Robustness test

To avoid possible bias from extreme values, this study adopted the sample data of each variable from the 5th percentile to the 95th percentile (Huang & Liu 2011).

Results and analyses

Descriptive statistics

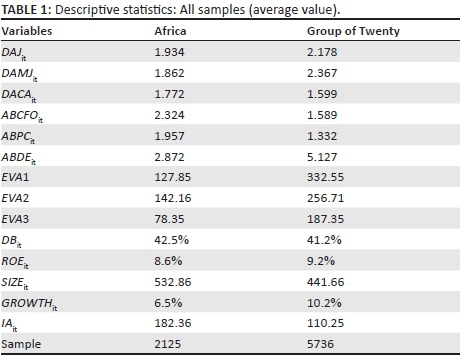

The mean DAs in African and G20 nations are positive, indicating that nations use DA items to manage earnings to increase their adjusted income (Table 1) because a positive εit denotes income-increasing, performance-adjusted items (Chen et al. 2011). Overall, the DAs of the Jones model are higher in African nations, whereas those of the modified Jones model are higher in G20 nations. The mean of REM activities in African and G20 nations is also positive. The African and G20 nations thus adopt REM activities to manage earnings to increase their adjusted income. Consequently, the difference in earnings management is manifested through DAs or REM activities in these nations.6

According to the performance index (US$ billion), EVA2 is higher and EVA3 is lower in African nations, whereas EVA1 is higher and EVA3 is lower in G20 nations. The proportion of debt and equity return shows that financial conditions have been conservative in these nations since the 2008 global financial crisis.

Empirical test

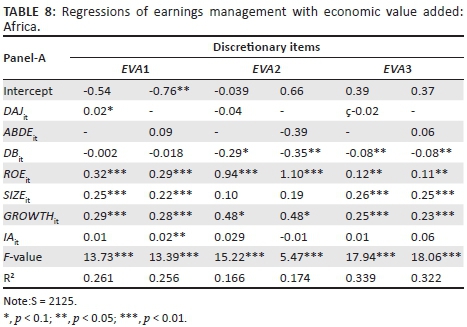

Tables 2-7 showed that the discretionary accruals (DAs) of the Jones model, modified Jones model, discretionary current accruals of Louis model and discretionary expenditures model of G20 and African countries. DAs (Jones model) have a significantly positive relationship with EVA1 and a non-significant relationship with EVA2 and EVA3 for all firms in African nations (Table 8). These findings support Hypothesis 1. Compared with the DA items, an abnormal level of discretionary expenditures has a non-significant relationship with EVA. These findings do not support Hypothesis 2. The absolute value of εit was obtained using the Jones model, and the value indicated that African nations use DA items to increase their income because the market structure or government policies (e.g. related rules or external monitoring) are not completely capital markets in these nations; therefore, investors cannot identify earnings management behaviour. Outside investors may then consider that enterprises have generated a favourable image of businesses, such as higher performance, and may willingly provide more funds to enterprises or accept a lower return of funds (i.e. corporates acquire external funds easily or at cheaper rates), which subsequently, leads to a reduction in the weighted average cost of capital and an increase in EVA. Moreover, a high likelihood exists that managers in African nations attempt to adopt earnings manipulation through discretionary expenditures; however, this type of behaviour does not affect investors' willingness to provide funds; therefore, capital cost and EVA are unchanged.

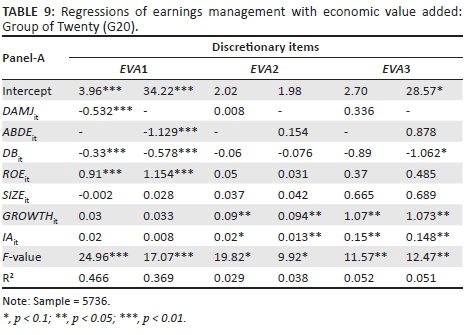

DAs (modified Jones) have a significantly negative relationship with EVA1 and a non-significant relationship with EVA2 and EVA3 in G20 nations (Table 9). These findings do not support Hypothesis 1. Compared with the DA items, an abnormal level of discretionary expenditures exhibit a significantly negative relationship with EVA1 and a non-significant relationship with EVA2 and EVA3; these findings support Hypothesis 2. Compared with African nations, the market structure or government policies (e.g. related rules or external monitoring) are more completely capital markets in G20 nations; therefore, investors can identify earnings management.

Furthermore, the absolute value of εit was obtained using the discretionary expenditures model, and this value indicated that G20 nations use discretionary expenditures to increase their income. Investors may consider that the financial statements are false because earnings management has distorted the real performance; hence, investors may be unwilling to provide additional funds to the enterprise or accept a lower return of funds (i.e. corporates acquire external funds at higher rates), which subsequently leads to an increase in the weighted average cost of capital and reduction in EVA. Moreover, it is likely that the listed firms in G20 nations (most samples in nations are significant partners of the United States) were affected by the 2008 global financial crisis; since then, outside investors have focused more on the true value of enterprises. Therefore, managers have attempted to adopt earnings management through DA items or REM activities, which generates an unfavourable image of businesses.

Variance inflation factors can be calculated to explain the correlation of variables. Therefore, a correlation problem did not exist in this study (variance inflation factors < 10).7

Debt ratio has a significantly negative relationship with EVA in the African and G20 nations, profitability (ROE) has a significantly positive relationship with EVA in the African and G20 nations, size (sales) has a significantly positive relationship with EVA in the African nations, growth (asset growth rate) has a significantly positive relationship with EVA in the African and G20 nations and intangible assets has a significantly positive relationship with EVA in the African and G20 nations. These results are consistent with those reported by Moradi et al. (2012). However, size (sales) has a non-significant relationship with EVA in G20 nations. Overall, earnings management (through DA items or REM activities) has a significantly positive or negative relationship with EVA in the African and G20 nations because of the 2008 global financial crisis. Moreover, earnings management (through DA items) has a significantly positive relationship with EVA in the African nations because of the lack of government policies or immature market structures. Consequently, earnings management (through DA items or REM activities) has a significantly negative relationship with EVA in the G20 nations because the market structure or government policies are completely the capital markets in these nations.

Conclusion

Several nations have incurred severe losses since the 2008 global financial crisis. Managers attempting to adopt earnings management through DA items or REM activities for generating a more unfavourable or favourable image of businesses and acquiring external funds at cheaper (easier) or more expensive rates may have affected business capital costs and EVA.

There is a lack of related literature on the association between earnings management and EVA. The results indicate that a significantly positive relationship exists between earnings management through DAs and EVA in African nations. We conclude that the enterprises operate in environments that lack government policy and have an immature market structure. Comparing the aforementioned nations reveals a significantly positive relationship between earnings management through DAs and EVA in African nations. On the basis of our analysis results, we conclude that a significantly negative relationship exists between earnings management through DAs or REM activities and EVA in G20 nations. The enterprises in these nations were affected by the 2008 global financial crisis.

Managers in African nations should increase EVA through earnings management; however, EVA can be reduced in G20 nations through earnings management. The differences in national development, culture or the magnitude of losses possibly result from the financial tsunami in these nations.

For researchers, our empirical findings show that REM activities and DAs are substitutes. Investors can analyse the true value of enterprises. In addition, researchers may consider refining the measurements of earnings manipulation. Governments must establish stricter security laws and rules for listed firms to prevent earnings management. Future studies may consider establishing a theory for examining the relationship between earnings manipulation and EVA.

Acknowledgements

Competing interests

The authors declare that they have no financial or personal relationships that may have inappropriately influenced them in writing this article.

Authors' contributions

Z-J.L. was the project leader, Y-S.W. performed some of the experiments. Z-J-L. prepared the samples and calculations were performed by Y-S.W.

References

Allgood, S. & Farrell, K.A., 2003, 'The match between CEO and firm', Journal of Business 76(2), 317-340. https://doi.org/10.1086/367752 [ Links ]

Altendorfer, K. & Jodlbauer, H., 2011, 'Which utilization and service level lead to the maximum EVA?', International Journal of Production Economics 130(1), 16-26. https://doi.org/10.1016/j.ijpe.2010.10.008 [ Links ]

Anjum, N., Saif, M.I., Malik, Q.A. & Hassan, S., 2012, 'Earnings management and firms' profitability evidence from Pakistan', European Journal of Economics, Finance and Administrative Sciences 47, 13-18. [ Links ]

Bailey, E.E. & Helfat, C.E., 2003, 'External management succession, human capital and firm performance: An integrative analysis', Managerial and Decision Economics 24, 347-369. https://doi.org/10.1002/mde.1119 [ Links ]

Brown, L. & Higgins, H., 2001, 'Managing earnings surprises in the US versus 12 other countries', Journal of Accounting and Public Policy 20, 373-398. https://doi.org/10.1016/S0278-4254(01)00039-4 [ Links ]

Burja, V. & Burja, C., 2010, 'Patrimonial resources' management and effects on the economic value added', Annales Universitatis Apulensis Series Oeconomica 12(2), 608-615. [ Links ]

Caton, G.L., Chiyachantana, C.N., Chua, C.T. & Goh, J., 2011, 'Earnings management surrounding seasoned bond offerings: Do managers mislead ratings agencies and the bond market?', Journal of Financial and Quantitative Analysis 46(3), 687-708. https://doi.org/10.1017/S0022109011000147 [ Links ]

Chang, F.Y., Hsin, C.W. & Hou, S.S., 2013, 'A re-examination of exposure to exchange rate risk: The impact of earnings management and currency derivative usage', Journal of Banking and Finance 37, 3243-3257. https://doi.org/10.1016/j.jbankfin.2013.03.007 [ Links ]

Chen, H., Chen, J.Z., Lobo, G.J. & Wang, Y., 2011, 'Effects of audit quality on earnings management and cost of equity capital: Evidence from China', Contemporary Accounting Research 28(3), 892-925. https://doi.org/10.1111/j.1911-3846.2011.01088.x [ Links ]

Chiu, P.C., Teoh, S.H. & Tian, F., 2013, 'Board interlocks and earnings management contagion', The Accounting Review 88(3), 915-944. [ Links ]

Cohen, D.A., Dey, A. & Lys, T.Z., 2008, 'Real and accrual-based earnings management in the pre- and post-Sarbanes Oxley periods', The Accounting Review 82(3), 757-787. https://doi.org/10.2308/accr.2008.83.3.757 [ Links ]

Datta, S., Iskandar-Datta, M. & Singh, V., 2013, 'Product market power, industry structure, and corporate earnings management', Journal of Banking and Finance 37(8), 3273-3285. https://doi.org/10.1016/j.jbankfin.2013.03.012 [ Links ]

Dechow, P., Saloan, R. & Sweeney, A., 1995, 'Detecting earning management', The Accounting Review 70, 193-225. [ Links ]

Degeorge, F., Ding Y., Jean T. & Stolowy, H., 2013, 'Analyst coverage, earnings management and financial development: An international study', Journal of Accounting and Public Policy 32, 1-25. https://doi.org/10.1016/j.jaccpubpol.2012.10.003 [ Links ]

Essid, W., 2012, 'Executive stock options and earnings management: Is there an option level dependence?', Corporate Governance 12(1), 54-70. https://doi.org/10.1108/14720701211191337 [ Links ]

Farrell, K., Unlu, E. & Yu, J., 2014, 'Stock repurchases as an earnings management mechanism: The impact of financing constraints', Journal of Corporate Finance 25, 1-15. https://doi.org/10.1016/j.jcorpfin.2013.10.004 [ Links ]

Francoeur, C., Amar, W.B. & Rakoto, P., 2012, 'Ownership structure, earnings management and acquiring firm post-merger market performance evidence from Canada', International Journal of Managerial Finance 8(2), 100-119. https://doi.org/10.1108/17439131211216594 [ Links ]

Habib, A., Bhuiyan, B.U. & Islam, A., 2013, 'Financial distress, earnings management and market pricing of accruals during the global financial crisis', Managerial Finance 39(2), 155-180. https://doi.org/10.1108/03074351311294007 [ Links ]

Hansen, J.C., 2010, 'The effect of alternative goals on earnings management studies: An earnings benchmark examination', Journal of Accounting and Public Policy 29, 459-480. https://doi.org/10.1016/j.jaccpubpol.2010.06.002 [ Links ]

Haque, R., Siddikee, J.A., Hossain, S., Chowdhury, S.P. & Rahman, M., 2013, 'Relationship between dividend payout and economic value added: A case of square pharmaceuticals limited, Bangladesh', International Journal of Innovation and Applied Studies 3(1), 98-104. [ Links ]

He, D., Yang, D.C. & Guan, L., 2011, 'Earnings management and long-run stock underperformance of private placements', Academy of Accounting and Financial Studies Journal 15(1), 31-58. [ Links ]

Healy, P.M. & Wahlen, J.M., 1999, 'A review of the earnings management literature and its implications for standard setting', Accounting Horizons 13(4), 365-383. https://doi.org/10.2308/acch.1999.13.4.365 [ Links ]

Huang, D.T. & Liu, Z.C., 2010, 'Board composition and corporate value in high technology firms of Taiwan', International Journal of Organizational Innovation 2(4), 126-138. [ Links ]

Huang, D.T. & Liu, Z.C., 2011, 'The relationships among governance and earnings management: An empirical study on non-profit hospitals in Taiwan', African Journal of Business Management 5(14), 5468-5476. [ Links ]

Huynh, T., Gong, G. & Nguyen, A., 2013, 'Integrating activity-based costing with economic value added', Journal of Investment and Management 2(3), 34-40. https://doi.org/10.11648/j.jim.20130203.11 [ Links ]

Islam, A., Ali, R. & Ahmad, Z., 2011, 'Is modified Jones model effective in detecting earnings management? Evidence from a developing economy', International Journal of Economics and Finance 3(2), 116-125. https://doi.org/10.5539/ijef.v3n2p116 [ Links ]

Jha, A., 2013, 'Earnings management around debt-covenant violations - An empirical investigation using a large sample of quarterly data', Journal of Accounting, Auditing and Finance 28(4), 369-396. https://doi.org/10.1177/0148558X13505597 [ Links ]

Jones, J.J., 1991, 'Earnings management during import relief investigations', Journal of Accounting Research 29, 193-228. https://doi.org/10.2307/2491047 [ Links ]

Kangarluei, S.J., Motavasse, M. & Abodllahi, T., 2011, 'The investigation and comparison of free cash flows in the firms listed in Tehran Stock Exchange (TSE) with an emphasis on earnings management', International Journal of Economics and Business Modeling 2(2), 118-123. [ Links ]

Karampinis, N.I. & Hevas, D.L., 2013, 'Effects of IFRS adoption on tax-induced incentives for financial earnings management: Evidence from Greece', The International Journal of Accounting 48, 218-247. https://doi.org/10.1016/j.intacc.2013.04.003 [ Links ]

Kaur, M. & Narang, S., 2008, 'Economic value added reporting and corporate performance: A study of Satyam Computer Services Ltd.', The ICFAI Journal of Accounting Research 7(2), 40-52. [ Links ]

Kim, J.B. & Sohn, B.C., 2013, 'Real earnings management and cost of capital', Journal of Accounting and Public Policy 32, 518-543. https://doi.org/10.1016/j.jaccpubpol.2013.08.002 [ Links ]

Lin, F.Y. & Wu, S.F., 2014, 'Comparison of cosmetic earnings management for the developed markets and emerging markets: Some empirical evidence from the United States and Taiwan', Economic Modelling 36, 466-473. https://doi.org/10.1016/j.econmod.2013.10.002 [ Links ]

Louis, H., 2004, 'Earnings management and the market performance of acquiring firms', Journal of Financial Economics 74, 121-148. https://doi.org/10.1016/j.jfineco.2003.08.004 [ Links ]

Mahdavi, Q. & Rastegari, N., 2007, 'Information content of economic value for the profit forecast', Journal of Social Sciences and Humanities of Shiraz University 26(1), 137-156. [ Links ]

Moradi, M., Ghomian, M.M. & Fard, M.G., 2012, 'The relationship between particular features of a firm and the economic value added', World Applied Sciences Journal 19(11), 1640-1648. [ Links ]

Nagata, K., 2013, 'Does earnings management lead to favorable IPO price formation or further underpricing? Evidence from Japan', Journal of Multinational Financial Management 23, 301-313. https://doi.org/10.1016/j.mulfin.2013.05.002 [ Links ]

Neumann, R. & Voetmann, T., 2005, 'Top executive turnovers: Separating decision and control rights', Managerial and Decision Economics 26(1), 25-37. https://doi.org/10.1002/mde.1187 [ Links ]

Nikbakht, M.R. & Moghimi, A.A., 2011, 'The relationship between economic value and capital structure', Journal of Auditor 56, 1-4. [ Links ]

Parvaei, A. & Farhadi, S., 2013, 'The ability of explaining and predicting of economic value added (EVA) versus net income (NI), residual income (RI) & free cash flow (FCF) in Tehran Stock Exchange (TSE)', International Journal of Economics and Finance 5(2), 67-77. https://doi.org/10.5539/ijef.v5n2p67 [ Links ]

Peng, M.W., 2004, 'Outside directors and firm performance during institutional transitions', Strategic Management Journal 25, 453-471. https://doi.org/10.1002/smj.390 [ Links ]

Roychowdhury, S., 2006, 'Earnings management through real activities manipulation', Journal of Accounting and Economics 42(3), 335-370. https://doi.org/10.1016/j.jacceco.2006.01.002 [ Links ]

Salteh, H.M. & Valipour, H., 2012, 'Investigating the relationship between earnings management and weighted average cost of capital (WACC)', Business and Management Review 1(12), 28-38. [ Links ]

Shen, W. & Cannella, A.A., Jr, 2003, 'Will succession planning increase shareholder wealth? Evidence from investor reactions to relay CEO successions', Strategic Management Journal 24, 191-198. https://doi.org/10.1002/smj.280 [ Links ]

Shu, P.G. & Chiang, S.J., 2014, 'Firm size, timing, and earnings management of seasoned equity offerings. International Review of Economics and Finance 29, 177-194. [ Links ]

Stewart, G. B., 1991, The quest for value, Harperbusiness, New York. [ Links ]

Wang, Y.S., Jiang, X., Liu, Z.J. & Wang, W.X., 2015, 'Effect of earnings management on economic value added: A China study', Accounting and Finance Research 4(3), 9-19. https://doi.org/10.5430/afr.v4n3p9 [ Links ]

Wu, S.W., Lin, F.Y. & Fang, W.C., 2012, 'Earnings management and investor's stock return', Emerging Markets Finance & Trade 48(3), 129-140. https://doi.org/10.2753/REE1540-496X4805S308 [ Links ]

Zhang, X. & He, Y., 2013, 'R&D-based earnings management, accounting performance and market return evidence from national-recognized enterprise technology centers in China', Chinese Management Studies 7(4), 572-585. https://doi.org/10.1108/CMS-09-2013-0176 [ Links ]

Correspondence:

Correspondence:

Yi-Shu Wang

wys124@163.com

Received: 31 Oct. 2014

Accepted: 13 July 2016

Published: 25 Oct. 2017

1. We considered Egypt, Nigeria and South Africa because these nations have the top three gross domestic products and largest stock exchanges (i.e. Egyptian, Nigerian and Johannesburg Stock Exchanges) in Africa.

2. We only selected Argentina, Japan, Korea, Russia and Saudi Arabia because these nations do not belong to other groups such as the NAFTA, ASEAN, EU and Newly Industrialised Country nations.

3. It is based on R&D expenses in each business, every year, and is used as a straight-line method for 5 years; thus, we can calculate un-amortisation in the next 5 years.

4. It is based on marketing expense in each business, every year, and is used as a straight-line method for 5 years; thus, we can calculate 'un-amortisation' in the next 5 years.

5. Economic depreciation adjusted items are measured using the funds method because it is superior to all other methods.

6. All of the εit was measured using Equations 1-6 and passed the t-test.

7. In order to shorten the tables, we omit the solution.