Serviços Personalizados

Artigo

Inglês (pdf)

Inglês (pdf)

Artigo em XML

Artigo em XML Referências do artigo

Referências do artigo

Indicadores

Links relacionados

-

Citado por Google

Citado por Google -

Similares em Google

Similares em Google

Compartilhar

Permalink

PermalinkSouth African Journal of Economic and Management Sciences

versão On-line ISSN 2222-3436

versão impressa ISSN 1015-8812

S. Afr. j. econ. manag. sci. vol.20 no.1 Pretoria 2017

http://dx.doi.org/10.4102/sajems.v20i1.1703

ORIGINAL RESEARCH

Assessing the impact of macroeconomic variables on pension benefits in Ghana: A case of Social Security and National Insurance Trust

Grace Ofori-AbebreseI; Robert Becker PicksonII; Sherifatu AbubakariI

IDepartment of Economics, Kwame Nkrumah University of Science and Technology, Ghana

IICollege of Economics and Management, Sichuan Agricultural University, China

ABSTRACT

BACKGROUND: One of the most pressing phases for all economic agents is post-retirement standard of living. Irrespective of the higher returns on pension contribution and varied pension reforms, there are possible factors that can render these pension benefits inadequate, which can affect the longevity of retirees. Studies conducted in other countries have concluded that inflation deteriorates the value of pension benefits.

AIM: This study, thus, sought to assess the impact of some major economic indicators in the Ghanaian environment on pension benefits.

SETTING: This study was carried out in Ghana by obtaining quarterly data frequencies on pension benefits and economic indicators spanning the period 2000Q1 to 2014Q4.

METHOD: The Auto-regressive Distributed Lag Model was utilised to examine the long run and short run dynamics of some major economic indicators and pension benefits.

RESULTS: The empirical evidence indicated that inflation deteriorates total pension benefits. Increasing monetary policy rate and depreciation of the domestic currency should be an issue to contend with only in the short run rather than in the long run. The study also found the prominence of the implementation of the National Pension Reform in 2008.

CONCLUSION: The study concluded that if policy makers target the reduction in the monetary policy rate and the appreciation of the domestic currency in an effort to stabilise the value of total pension benefits in the long run, it would not be effective in the long run because of their insignificant nature. Policy makers should rather target inflation as the prime tool for stabilising the standard of living of retirees in the long run.

Introduction

One of the most pressing phases for all economic agents is post-retirement standards of living. This is justified because depending on the preparations made towards post-retirement, one is likely to live a life that can be either prolonged or shortened (Kumado & Gockel 2003). Prior to the rising of modern states in Africa, traditional societies saw the urgency to ensure measures are put in place to absorb major unforeseen contingencies via social and mutual help for one another in times of ageing. Originally, the family was the main institution recognised for the provision of support for their members in times of economic deprivation, social isolation or even disability. Nevertheless, with the world becoming a global village in this modern era coupled with the decline in the extended family system, there is gradual movement to the reliance on institutionalised forms and systems of social security (Kumado & Gockel 2003).

Across the globe, several sprouted pension systems are striving to deliver adequate retirement incomes coupled with financial sustainability because of the ageing population, which is characterised by increasing longevity and low fertility rates. Many countries have, thus, launched significant pension reforms including higher retirement ages, savings in pensions and changes in the calculation of pension entitlements amongst others (Organisation for Economic Co-operation and Development [OECD] 2015).

The urgency for pension schemes in Ghana dates back as far as the Second World War (1939-1945). The United Trading Company (UTC) of the then Gold Coast formed the first social institution for the welfare of the UTC employees. By 1946, the welfare of employees had expanded as a result of the adoption of the International Labor Convention, which catered for workers who were injured as well as those who passed on. This led to the enactment of the pension ordinance in 1946 (Appiah 1999). The expansion of the various schemes subsequently led to the addition of certified teachers when the Teachers' Pension Ordinance was passed in 1955 (Gockel 1996).

Also, with the increasing urbanisation caused by migration and the search for wage employment led to the high dependence on the magnanimity of the urban employers. The adverse socio-economic impact on the social welfare of migrants led to the establishment of a nationwide social security for migrants. The Social Security Act was passed in 1965 which laid the foundation of the National Social Security Scheme in the Ghanaian economy (Obiri-Yeboah & Obiri-Yeboah 2014).

Currently, in Ghana, Social Security and National Insurance Trust (SSNIT) is the prominent fund trustee set up to manage the pension schemes and social security systems for employers and employees. SSNIT is responsible for the administration of the Basic National Social Security Pension Scheme. It thus provides protection for workers in both public and private sectors. It sees to the investment of employees' contribution towards retirement, thus making the institution to be ranked amongst major stakeholders in the welfare of Ghanaians. However, the scheme was not without fault as it underperformed in the delivery of retirement income security for its members which led to several pension reform schemes in order to improve its performance (Gockel 1996).

The first step that was evident in the 2008 pension reform was when Ghana joined the league of Chileans by adopting a three-tier pension scheme. This pension scheme was enacted under the National Pensions Act, 2008 (Act 766) (Government of Ghana 2008) with its main purpose of being the provision of a universal pension scheme for all employers and employees in the country. Act 766 thereby resulted in the establishment of the National Pensions Regulatory Authority (NPRA) and Corporate Trustees amongst others, as part of the major efforts to bring to the barest minimum the inadequacies of pension benefits and the agitations about the low pension benefits received under the SSNIT pension fund (Kumado & Gockel 2003). It is thus evident that most governments recognise the essence of providing sustainable pension funds to cater for the ageing population to ensure an increased post-retirement well-being of all economic agents.

Despite these pension reforms, employees argue that irrespective or regardless of their years of service to the country coupled with the contributions they make towards the scheme, they are normally given menial sums, which they feel do not match what they have contributed. It brings to question the relevance of these economic reforms in respect of pension benefits such that economic agents continue to battle with standards of living after retirement (Agyeman 2011). Pension schemes should provide adequate income for pensioners; nevertheless, in the midst of unfavourable economic factors, these increased benefits may not serve the intended purpose rendering it less useful. With the increasing level of volatility in the rates of inflation, the fast and unstable depreciation of the domestic currency as well as the unstable rates of interest amongst other major macroeconomic variables can serve as threat to pension benefits and thus the paltry sum pensioners receive. Bulow (1982) stresses that, in the absence of post-retirement adjustments, the real value of pension benefits tends to fall in the presence of inflation and the rates of interest. This tends to affect the sustainability of households' welfare, thus analysing pension benefits in the midst of major macroeconomic factors cannot be overemphasised as it would ensure the efficient allocation of resources by economic agents towards retirement as well as economic growth.

The possible remedy lies in how to ensure that these pension reforms in the midst of other economic reforms remain financially sustainable by providing citizens adequate income for the retirement periods. Much attention over the years has been given to the impact of macroeconomic forces on the returns that are earned from investing pension contributions. Obiri-Yeboah and Obiri-Yeboah (2014), Kumado and Gockel (2003) and Agyeman (2011) in the Ghanaian context have broadened our understanding about Pension reforms, SSNIT and returns on pension funds' investments in the midst of macroeconomic forces. However, what is not well understood and completely ignored in the Ghanaian context is the effect of these macroeconomic forces on the take-home pension benefits of economic agents. In other words, irrespective of the higher returns on pension contribution and varied pension reforms, there are possible factors that can render these pension benefits inadequate, which can affect the longevity of retirees.

This study thus seeks to assess the impact of some major economic indicators in the Ghanaian environment on pension benefits spanning 2000Q1 to 2014Q4. Specifically, this study attempts to evaluate the impact of macroeconomic variables on pension benefits, and eventually analyse how well the 2008 Pension Reform has been able to improve pension benefits in Ghana.

The rest of the paper is organised as follows: the second section presents the related literature reviewed, the third section describes the study methodology, the fourth section uncovers the empirical results and analysis and the fifth section considers the conclusion and policy implications.

Review of related literature

Historical development of pension scheme and social security in Ghana

The urgency for pension schemes in Ghana dates back as far as the Second World War (1939-1945). The UTC of the then Gold Coast formed the first social institution for the welfare of the UTC employees. The UTC was a multinational corporation formed by the Basel Mission in 1921. This development of the UTC led to the formation of the African Pension Fund, which was the first social institution meant to cater for the welfare of the indigenous populations of the then Gold Coast. Irrespective of this, it was not a national social security but specifically for employees of the UTC.

By 1946, the welfare of employees had expanded as a result of the adoption of the International Labour Convention, which catered for workers who are injured as well as those who passed on. This led to the enactment of the pension ordinance in 1946 after the Second World War (Appiah 1999). The main purpose of this pension ordinance was to provide a non-contributory scheme for the African senior civil servants, their widows as well as orphans. Furthermore, the expansion of the various schemes subsequently led to the addition of certified teachers when the Teachers' Pension Ordinance was passed in 1955 (Gockel 1996).

Also, increasing urbanisation caused by migration and the search for wage employment led to a high dependence on the magnanimity of the urban employers. The adverse socio-economic impact on the social welfare of migrants led to the establishment of a nationwide social security for migrants. In 1960, a compulsory savings scheme was established by the Convention Peoples Party for all formal sector workers. The savings scheme was maintained through the deduction of monthly contributions from the wages and salaries of all formal sector employees, which was paid into a consolidated fund.

By 1965, this savings scheme had failed because of the mismanagement of the consolidated funds. The Social Security Act was then passed in 1965, which laid the foundation of the National Social Security Scheme in the Ghanaian economy. The Social Security Act aimed at the provision of a provident fund of 22.5% contribution to be made each month by the employee and employers. 7.5% and 15% contributions were made by the employee and employer, respectively, each month (Obiri-Yeboah & Obiri-Yeboah 2014).

Currently, in Ghana, SSNIT is the prominent fund trustee set up to manage the pension schemes and social security systems for employers and employees. It was established under the National Redemption Council Decree (NRCD) 127 in 1972. SSNIT is responsible for the administration of the Basic National Social Security pension scheme. It thus provides protection for workers in both public and private sectors. SSNIT sees to the investment of employees' contribution towards retirement, thus ranking the institution amongst major shareholders in the Ghanaian economy.

The Social Security and National Insurance Trust of Ghana

Amongst the varied efforts made to provide social security in Ghana for all employees, the passage of the NRCD 127 in 1972 was the major social security scheme in the Ghanaian economy (Kumado & Gockel 2003). In an attempt to rectify the shortfalls of the 1965 Parliamentary Act 279, the NRCD 127 established an independent corporate body known as the Social Security and National Insurance Trust (SSNIT) in 1972.

In respect of its coverage, the Act 279 of 1965 was amended by the NRCD 127 of 1972 to ensure the coverage of employees in any institution that employs a minimum of five workers by compulsion. Establishments with less than five employees were given the choice to either join the scheme or not with no compulsion to do so. Nevertheless, the following institutions and workforce were exempted by law from joining the SSNIT pension scheme:

-

The Armed Forces, the Police Service and the Prison Service

-

Foreigners in the Diplomatic Missions

-

Senior members of the university and research institutions

According to the International Labour Organization Convention 102 of 1952, a country is mandated to provide a minimum of nine basic social security services for its contributors. Nevertheless, the provident fund operated by the SSNIT has managed to ensure the provision of five major direct contingencies including:

-

Unemployment

-

Emigration

-

Invalidity

-

Sickness

-

Death or Survivors

The above-mentioned benefits enjoyed by contributors come in the form of lump sum payments made up of their actual contributions and up to a 3% compounded rate of interest.

SSNIT's inability to provide the other four contingencies which include medical care benefit, employment injury benefit, family benefit and maternity benefits could be attributed to the developing state of the economy because of the low contributions made by contributors. Given the bulk sum SSNIT receives monthly as contributions, it remains one of the biggest shareholders in the country.

The scheme defaulted because it underperformed in the delivery of retirement income security for its members, which led to several pension reform schemes to improve its performance (Gockel 1996).

Overview of pension reforms

According to Whiteford and Whitehouse (2006), the majority of OECD countries over the last 25 years have changed their retirement income systems. While some countries have undertaken single 'big-bang' pension reforms, others, on the other hand, have maintained a regular but increasing pension system. Furthermore, countries such as Australia and Japan are the only countries that have reduced the accrual rate of public pension benefits. The usual expectation of pension benefits is its ability to increase to ensure a decent post-retirement standard of living. Nevertheless, the justification for a reduction in pension benefits as demonstrated by Japan and Australia is to ensure the affordability of pension plans by the citizens of their countries. The higher the contribution made, the higher the benefits accrued upon retirement.

The major motivation for all these efforts (either to increase or decrease) made under the pension schemes is to ensure a much more sustainable financial public pension system. The cut in pension benefits, however, has the tendency to result in the increase of inadequate income in retirement and consequently to lead to old-age poverty (Whiteford & Whitehouse 2006).

Irrespective of this, most of the reforms are geared towards the encouragement of low-income older people to take public pension plans while the middle- and high-income earners embark on voluntary and private pension schemes. Some of the significant changes that can be viewed under the pension reforms include the following:

-

Changing the valorisation of past benefits: In most OECD countries, past earnings are re-valued to take into account changes in the level of standard of living between the time pension benefits accrue and the time they are claimed.

-

Changing the indexation of pension benefits: In recent years, most developed and developing countries are moving away from a system of indexation of pension benefits to earnings towards an indexation with prices. The main purpose is to preserve the purchasing power of retirees and maintain financial sustainability of the benefits earned.

-

Linking pension benefits to higher life expectancy: The accrued benefits for pension are mostly related to the life expectancy in most countries, such that increasing life expectancy reflects a reduction in pension benefits. For example, Japan, Austria and Germany aim to reduce pension benefits as life expectancy increases; however, it is accompanied by a reflection in financial sustainability.

-

Increasing eligibility age: Most countries' pension reforms equalise ages between men and women. Thus, the implementation of age for pension tends to affect only or mainly women. Some countries such as the United States, Greece, Japan and Australia amongst others have increased the pension age that affects both men and women. In Australia for example the pensionable age is 65 years or older for both men and women. It is further projected to hit 67 years by 2023 as the pensionable age increases by 6 months every 2 years.

-

Increasing the reward of continuing to work: Most pension reforms across the globe have put measures in place to cater for early and late retirement ages. The number of years required to receive the full entitlement for any pension benefit has been increased by most countries such as the United States and the United Kingdom. To this effect, penalties have been introduced for people opting for early retirement, while bonuses and incremental packages are available to those employees who retire after the normal retirement age.

Overview of the National Pensions Act, 2008 of Ghana

In December 2008, Ghana joined the league of Chileans by adopting a three-tier contributory pension scheme. This pension scheme was enacted under the National Pensions Act, 2008 (Act 766) (Government of Ghana 2008) with its main purpose being the provision of a universal pension scheme for all employees in the country. The Act further led to the formation of the NPRA to oversee the management and administration of registered pension schemes and trustees. These were part of the major efforts to bring to the barest minimum the inadequacies of the current pension benefits and the agitations about the low pension benefits received under the SSNIT pension fund (Kumado & Gockel 2003).

Aside from the establishment of the three-tier contributory body of the National Pensions Act, there were three additional parts that fully made the Pension Act a whole. The second part of the Act entailed the basic national security scheme, with part three composed of occupational pension schemes, provident fund and personal pension schemes as well as management of the scheme. The last part entailed the general provisions.

The three-tier pension scheme

The established three-tier scheme under the Pension Reform Act of 2008 in Ghana consists of:

-

A mandatory basic national security scheme: This first tier incorporates an improved system of SSNIT benefits and it is mandatory for all private and public sector employees. It involves the contribution of 13.5% of gross monthly salary of employees while the benefits from the contribution would be presented to pensioners in the form of monthly income. Furthermore, in the event of death before retirement or unforeseen circumstances such as disability or death, disability benefits are given to the contributors or their dependents.

-

A mandatory fully funded and privately managed occupational pension scheme: The second tier being a mandatory occupational scheme is originally to be managed by private fund managers and it involves the contribution of 5% of employee's gross monthly salary. Nevertheless, as opposed to the SSNIT benefits, the benefits under this tier would be a lump sum payment to beneficiaries, which is projected to be higher than the benefits currently under the SSNIT and Cap 30 schemes.

-

A voluntary fully funded and privately managed provident fund and personal pension scheme: The third tier enables every employee in the formal and informal sectors who voluntarily wants to enhance their pension benefits by making additional contributions. It is privately managed and supported by tax benefits incentives.

Empirical literature

Empirical literature that links the impact of economic variables on the pension benefits in Ghana and across the globe is not expansive. Amongst the earlier studies include Grubbs (1979), Bulow (1982), Munnell and Muldoon (2008), and Karam et al. (2010). Feldstein (1981) examined private pension and inflation in the United States. The study found retiree's pension benefits to be continually on the decline with the rising price levels. Also, in order to cater for the negative impact of inflation on these benefits, the study found it to be costly as a 6% adjustment of inflation on an annuity of a 65 year old pensioner would lead to a rise in the cost on pension by approximately 50%. This outcome he recommended could be financed by reducing wages and salaries or indexation of pension benefits. It thus concluded that inflation can be costly from both the trustees and pensioners perspective.

Also, Clark and McDermed (1982) further looked at inflation, pension benefits at retirement and found increasing rates of inflation to lower the present value of pension benefits and hence the accumulated pension compensations in the long run. The study was based on employee retirement decision as a function of the expected value of pension benefits; the study thus concluded work life could be prolonged because of the low value of pension benefits as a result of inflation.

Bulow (1982) evaluated the effects of inflation on the private pension system in the United States. According to the study, an increase in inflation causes the nominal interest rates (IRs) to increase. He found inflation not to directly affect pension benefits but can do so through the channel of higher IRs. Using a three-period scenario and Pension Benefit Guarantee Corporation in the United States, the study found a change in either inflation or IRs to significantly alter the value of the claims given to households, firms, and governments. An increase in IRs tends to reduce both the pension benefits accrued and the benefits that are guaranteed to be paid by the pension trustees per the outcome of the study.

United Nations Joint Staff Pension Board (2008) explored the impact of currency fluctuations on the United Nations Joint Staff Pension Board and pension benefits across the globe. Making use of the data from United States, France, Italy, Switzerland, United Kingdom and Austria and on the basis of a 36-month average local currency exchange as a measure of exchange rate and income replacement ratio (I/R) as a measure staff pension benefits, the study found in the United States a constant I/R with respect to the US dollar, indicating a no-currency effect on such benefits. However, the rest of the countries outside the base found their I/R values to be declining during the period reviewed.

Munnell and Muldoon (2008) also explored the impact of inflation on social benefits in the United States and found inflation to negatively impact the benefits enjoyed by retirees. According to their study, two major factors undermine much of the inflation protection that is offered by social security. Increasing medical care premiums and the personal income tax for benefits, increasing medical care meant a greater portion of benefits goes into medical insurance while taxation reduces the benefits compelling purchasing ability at retirement to decline. The study thus recommended inflation protection for retirees (Center for Retirement Research at Boston College).

Karam et al. (2010) assessed the macroeconomic effects of public pension reforms using the Global International Monetary and Fiscal dynamic stochastic equilibrium model. The study's pension reform was limited to increasing retirement age, reduction in benefits paid to retirees and increasing contributions. The study then revealed pension reforms to greatly impact positively on economic growth in both the short and long run. The long run impact they established was because of the declining government debt while the rising consumption propelled the short run economic growth. Nevertheless, the increasing retirement age yielded the most impact on economic growth because of the increasing demand effects from labour income.

The present literature differs from these existing studies in a number of ways. Whereas the previous literature limits the number of macroeconomic factors that may possibly affect pension benefits, the current literature takes into account multiple macroeconomic factors when it comes to the value of pension benefits. Secondly, because of the scarcity or virtually no literature from the Ghanaian perspective, the present study contributes to the body of knowledge in the Ghana's pension experience and possibly many developing countries with similar economic setting.

Study methodology

Theoretical model specification

To uncover a robust and reliable model that captures the impact of macroeconomic variables on pension benefits in Ghana, the study followed the Structural Hedonic model of compensating differential framework as a baseline model. This framework suggests that jobs are often seen to have non-wage benefits, which workers value differently from wage benefits. These benefits are largely identified to be pension benefits according to Whiteford and Whitehouse (2006). Thus, emphasis is placed on the value of these benefits received.

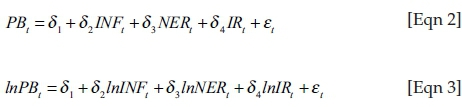

Because of the value placed on pension benefits, the study posited the value of pension benefits could be influenced by major macroeconomic variables, which may either increase or decrease the value depending on the state of the economy. Therefore, taking into account inflation, exchange rate and interest rate, the following baseline model was specified in Equation 1 as:

where PB denotes pension benefits, which is the dependent variable for the study. INF, NER and IR are inflation, nominal exchange rate and interest rate respectively. The function of the pension benefit in Equation 2 was transformed into a parametric model in the form:

It becomes prudent to introduce the log of the variables of interest to enable the interpretation of the partial elasticities, which looks at the degree of responsiveness of pension benefits to the respective economic variables as depicted in Equation 3.

Data types and sources

Secondary sources of data were employed for this study. Quarterly data frequencies on pension benefits and economic indicators spanning the period 2000Q1 to 2014Q4 were used. The time period for the study was chosen based on the accessibility and availability of data on pension benefits, which is the main point of focus for the study. The selected macroeconomic variables include the NER, IR and INF. The data on the pension benefits were obtained from the research department of SSNIT, Ghana. The macroeconomic indicators including inflation, exchange rate and the IR were obtained from two major sources made up of the International Financial Service of the International Monetary Fund and from the research department of the Bank of Ghana.

Measurement and a priori expectation of the variables

Pension benefits: being the dependent variable per the study is defined to mean the total amount of money paid by trustees to the various retirees.

Inflation: is defined as the sustained increase in the general prices of goods and services over a given period of time. INF was measured by the consumer price index. Pension benefits are expected to be inversely related to the rates of inflation such that an increasing INF would cause a decline in the value of pension benefits. According to Clark and McDermed (1982) and Thompson (1978), the general increasing price of goods and services affects the purchasing ability of retirees because the value of their benefits would decline and thus should be compensated by higher benefits. Thus, inflation is expected to have a negative influence on pension benefits (i.e. δ2 < 0).

Nominal exchange rate: is seen as the actual rate of exchange on the foreign currency market. The study uses Ghanaian cedi against the US dollar as its measure. An increase in the nominal exchange rate signals the depreciation of the domestic currency, whilst its decrease indicates appreciation of the Ghana cedi. The depreciation of the domestic currency is also posited to cause a decline in the value of the benefits received by pensioners because it becomes expensive to undertake any international trading activity. The exchange rate is thus expected to have a positive relationship with pension benefit of retirees. Therefore, the expected impact of NER on pension benefits is positive (i.e. δ3 > 0).

Interest rate: The return earned on a given amount invested is called the IR. The study made use of the monetary policy rate (MPR) as a measure of IR. The MPR is the rate at which the central bank lends to commercial banks. An increase in MPR by Bank of Ghana means an increase in the lending rates by the commercial banks to their clients. IRs are also expected to be positively related to pension benefits. The higher the rates of interest, the higher the returns that would be earned on the benefits invested. Hence, there exists a positive relationship between IR and pension benefits (i.e. δ4 > 0).

Estimation techniques

Cointegration test

Subsequent to the test for cointegration, the Augmented Dickey-Fuller (ADF) and the Phillips-Perron (PP) tests were deployed to examine the stationarity of the variables. The term cointegration mimics the existence of a long-run equilibrium to which an economic system converges over time. The study applied the auto-regressive distributed lag (ARDL) bounds test to cointegration to test the existence of a long-run relationship amongst the variables of interest. The bounds test is an estimation procedure that is used to test the long-run relationship given the fact that the time series is strictly I(0) or I(1) or a combination of both. It makes use of the F- and t-statistics to test for the significance of the lagged variables when there is uncertainty if the time series exhibits a trend or it is stationary at first difference.

From the above-mentioned equation, we perform an overall F-test of the null hypothesis that there is no cointegration between the variables X and Z as against the alternative that it is not true. The rejection of the null hypothesis implies that there exists a long-run relationship between the variables. The ARDL bounds test gives an upper and lower boundary with which the overall F-statistic is to be compared. If the F-test score is greater than the upper boundary, we reject the null hypothesis while an F-test score lower than the lower boundary moots for the acceptance of the null hypothesis. The outcome is inconclusive because the F-test falls in between these two boundaries.

The Auto-regressive Distributed Lag Model

The case where the unit root properties of the data are uncertain applying the ARDL procedure is the more appropriate model for empirical work. Applying the ADF and the PP tests for unit root, one may incorrectly conclude that a unit root is present in a series that is actually stationary around a one-time structural break. The ARDL approach is useful because it avoids these problems. The ARDL model specifies both the long run and short run impact of the independent variables on the dependent variable.

The researchers considered the model of the form ARDL(p,q,k). The long run ARDL model was specified as

The short run dynamics of the coefficient from the regression process was expressed by finding the error correction model associated with the long run estimates.

where Et-i represents the error correction factor and τ is the speed of adjustment. The error correction tells the speed of adjustment of the variables to the long run, should there be any deviation. The error correction factor should be negative and significant. The negative state spells out the fact that with any deviation from the long run, the variables would turn back to equilibrium. However, a positive error correction term tells the explosive state of the variables, an indication of no return back to its equilibrium.

Structural break analysis

One of the main objectives of the study was to assess the significance of the 2008 pension reform introduced to cater for inconveniences and the lapses of social security systems, particularly pension benefits. The study considered this reform as a major structural change that can highly impact positively or inversely on the benefits received by retirees. To this effect, the researchers introduced dummy variables to capture this structural change.

Introduction of dummy variables: Dummy variables are fictional variables created to represent the attributes of two or more distinct categories of things. They are proxy variables for a qualitative fact in a regression model. It usually takes binary forms of 0 or 1 to indicate the absence or presence of some intrinsic categorical effect that has the tendency to shift an outcome, in this case the 2008 pension reform. When the dummy takes 0, it is an indication that the explanatory variable's coefficient has no role in influencing the dependent variables while when the dummy takes on the value of 1, its coefficient acts to alter the intercept and thus the dependent variables.

Dummy for Pension Reform 2008 = 1 for periods when the 2008 Pension Reform was effected 0 for periods prior to the 2008 Pension Reform.

Empirical results and analysis

Stationarity test

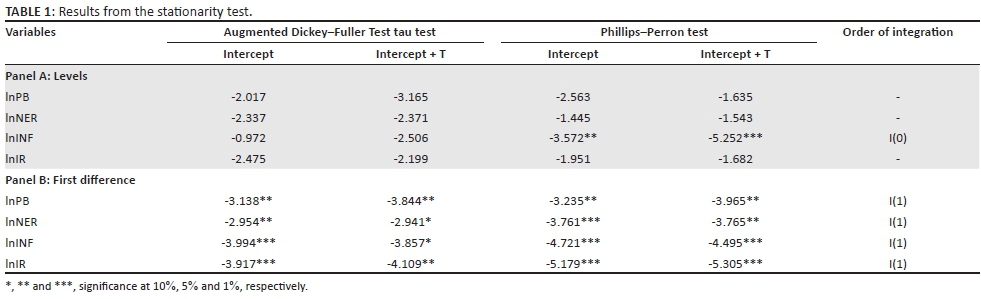

Table 1 presents the results of using ADF and the PP tests for the stationarity of the variables concerned.

From Panel A of Table 1, only the null hypothesis of unit root for inflation was rejected at 5% and 1% level of significance using ADF and PP tests, respectively. This implies that inflation is stationary at the levels, hence integrated of order zero [I(0)].The other variables were further first differenced in an attempt to ensure stationarity of the variables. From the outcomes in Panel B of Table 1, total pension benefits, exchange rate and IR were all statistically significant after their first difference, hence integrated of order one [I(1)]. It is, therefore, appropriate to estimate the model using the ARDL bounds test specification.

Cointegration analysis

The prime purpose of the cointegration analysis is to determine whether a group of time series variables has some form of long run relationships. Table 2 presents the results of the ARDL bounds test to cointegration.

The results in Table 2 present two different models' outcomes, the first model does not take into account the structural break of the National Pension Reform in 2008 while the second model does. The study considered the lower and upper bounds of the bounds tests at 1% and 5% level of statistical significance. The F-statistics of 14.64514 and 11.91449 from both models were found to be greater than their respective upper boundary at a 1% level of significance. Hence, there exists a long running relationship amongst the variables with or without a structural break. There would have been no cointegration should the F-statistic fall below the lower boundary and become undetermined should it have fallen in between the upper and lower boundary.

Results from the Auto-regressive Distributed Lag Model

This section of the empirical analysis presents the estimates of both the long and short run results from the ARDL. The first part takes into account the long- and short run estimates without a structural break pertaining to the National Pension Reform in 2008 while the second aspect factors the structural break as shown in Tables 3 and 4, respectively.

Short and long run analyses without structural break

This section of the analysis presents model 1 and model 2, which are the results of both the short and long run results, respectively, without the incorporation of a structural break. This section thus underscores the impact of inflation, IR and exchange rate on total pension benefits without incorporating major pension reforms.

Model 1 presents the short-run results when the National Pension Reform is excluded. From the model, it was determined that inflation, the NER and IR were all inversely related to total pension benefits paid to retirees. This implies that inflation tends to negatively affect the total amount of benefits paid out. An increase in INF by a percentage results in a decline in the value of pension benefits by approximately 18% in the short run. Also, a depreciation of the domestic currency (an increase in exchange rate) and an increase in the rate at which the central bank lends money to the commercial banks cause a decline in the value of pension benefits by approximately 9% and 8%, respectively. In the short run, however, inflation and IR were the only statistically significant determinants of the benefits paid out by the trustees of the fund all at 5% significance level. Exchange rate proved otherwise but economically tends to decrease the value of pension benefits by about 9%. The insignificant nature of the local currency could be associated with low direct investments by the trustees and beneficiaries in the foreign financial market and thus fluctuations in the domestic currency could not affect pension benefits directly but perhaps indirectly.

The sustained increase in the general prices of goods and services which tends to diminish the value of pension benefits paid out was expected to reduce the purchasing ability of pensioners. This tends to be detrimental to their post-retirement standard of living; the outcome of the study is consistent with the finding of Munnell and Muldoon (2008). They argued that most of the inflationary pressures come from varied medical care pertaining to hospital expenses and attempts to adopt healthy lifestyles associated with old-age eventually eat away the value of their post-retirement benefits.

The study adds to the body of literature considering the IR, the recent frequent increase in the rate at which commercial banks borrow from the central bank has rather reduced the post-retirement investments of retirees (in order to make efficient use of their pension benefits). The study found such rates of interest to contemporaneously reduce the value of pension benefits by 8%. It is argued that, with an increase in IR, the cost of borrowing from commercial banks to undertake major investments becomes very expensive with its accompanying high interests on loans. These high interests in comparison to post-retirement benefit tend to trivialise the benefits.

Furthermore, the Error Correction Model (ECM) term is statistically significant at the 10% significance level and the sign of its coefficient is also negative. The coefficient for the ECM is approximately -0.066 implying that, when there is a percentage shock or deviation of the variables from equilibrium, the long-run equilibrium relationship is restored at the rate of approximately 6.6%. In other words, the error correction suggests that just about 6.6% of the disequilibrium caused by the shocks in the current year is corrected in the long run. The speed of adjustment, though very low, spells the exact situation in the Ghanaian economy because it takes a long time for overall pension benefits to be adjusted to fit the current economic situation.

In the long run, however, it was inflation that remained a significant determinant of pension benefits; the rest of the macroeconomic variables did not matter in the long run. The negative consequence of inflation on pension benefits increased more elastically reducing pension benefits by more than 100%. This stresses the long-run effect of an uncontrolled fluctuation in the rates of inflation on the pensioners' standard of living and the economy as a whole.

Structural break analysis

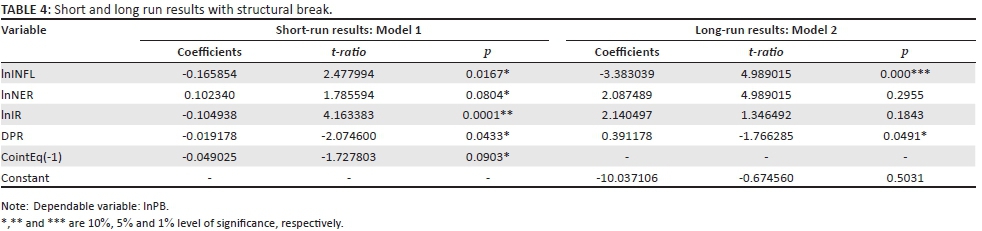

One major objective was to assess the significance of the pension reform undertaken by Ghana to make social security a better one. The study took into account the 2008 pension reform that brought into existence the NPRA with major efforts to bring to the barest minimum the inadequacies of the current pension benefits and the agitations about the low pension benefits received under the SSNIT pension fund. The study, therefore, introduced a dummy variable denoted DPR in an attempt to capture the National Pension Reform as a structural break in the social security administration. The results are presented in Table 4.

Model 1 in this second part of the analysis presents the short-run results when the National Pension Reform is included. From the model, inflation together with IR were all inversely related to total pension benefits paid to retirees just as in the previous analysis. This implies that inflation tends to negatively affect the total amount of benefits paid to pensioners. An increase in INF by a percentage results in a decline in the value of pension benefits by approximately 16% in the short run. The increase in the rate at which the central bank lends to the commercial banks also results in a decline in the value of pension benefits by approximately 10%. However, an appreciation of the domestic currency (a decrease in exchange rate) impacted positively on pension benefits. This implies that an appreciation of the local currency tends to increase the value of pension benefits by a 10% margin. The study also found the pension reform of 2008 to negatively affect pension benefits in the short run but merely by about 1.9%. All macroeconomic variables including inflation, NER and IRs as well as pension reforms in Ghana were all statistically significant determinants of the benefits paid out by the trustees of the fund all at 10% significance level with the exception of MPR, which was significant at 5%. In the long run, inflation and pension reform were the only statistically significant determinants of total pension benefits. Pension reform impacted positively on pension benefits in the long run compared to its inverse relation in the short run.

With the introduction of this structural break, about three major significant changes were observed in comparison to the model without the structural break.

Firstly, the study found the NER to be a significant determinant of pension benefit in the short run in the model with pension reforms. This brings to prominence that with the introduction of the pension reform, the NER tends to positively relate to pension benefits. This means that with efforts to make the pension benefits universal to include all employers and voluntary contributors around the globe, the investments made by the trustees in the foreign market tend to increase with the aim of improving the incomes and interest earned on the contributions.

Secondly, inflation and IR remained negative and significant just as in the model without the National Pension Reform. However, the magnitude of impact of the forces on pension benefits in the short run increased in value compared to the former analysis. The impact of IR increased from 8% to 10% and inflation declined from 18% to 16%. The decision to launch significant pension reform systems brings into light the exact magnitude of economic impact of these forces.

Above all, the study found the National Pension Reform itself to be a significant determinant in both the long and short run. The study underscores its negative impact in the short run, but tends to have a positive impact in the long run. The inverse relation of the National Pension Reform on pension benefits contemporaneously implies that the launch of the scheme with its positive intended purpose does not immediately take effect. This can be as a result of administrative and other adjustments of the scheme before it becomes effective in the long run.

In the long run, however, consistent with the first model, inflation was the only highly significant economic variable that mattered.

The speed of adjustment is much slower from about 6.6% to about 4% with the consideration of the structural break. The introduction of the National Pension Reform in 2008 meant a slower adjustment to the long-run equilibrium of pension benefits should there be any deviation.

Conclusions and policy implications

The main objective of the study was to assess the impacts of some macroeconomic forces on total pension benefits paid out to retirees by the SSNIT. Specifically, the study sought to find out the impact of inflation, the IR and the NER on total pension benefits in Ghana. Also, the study sought to investigate how well the National Pension Reform of 2008 has been able to improve pension benefits on the average pensioner since it was launched.

The empirical evidence supported conclusions that inflation reduces the value of total pension benefits. Increasing IR and depreciation of the domestic currency should be an issue to contend with only in the short run rather than in the long run. The study revealed that the prominence of the implementation of varied pension reforms in the Ghanaian economy, specifically the National Pension Reform of 2008, has significantly impacted on total pension benefits. However, it started by contemporaneously having a negative effect but in the long run it was worthy of its implementation as it positively affected pension benefits with a high magnitude of impact.

It should be noted that for policy purposes, the distinction between short and long run is justified. The variables that are relevant in the short run and long run as opposed to those which are not relevant should be distinguished to enable effective policy implementations.

In the short run, the behaviour of pension benefit is explained by inflation, IR, and the NER. Inflation was further the only relevant variable in the long run as well. If policy makers target the reduction in the IR and the appreciation of the domestic currency in an effort to stabilise the value of total pension benefits in the long run, it would not be effective in the long run because of their insignificant nature. Policy makers should rather target inflation as the prime tool for stabilising the standard of living of retirees in the long run.

In line with the findings of the study, policy makers are recommended to ensure the reduction and stabilisation of INF to be the paramount policy option in order to increase the standard of post-retirement living. This would be effective when medical expenses related to old-age are gradually subsidised or reduced to the barest minimum to ensure a prolonged life after retirement because inflation in that direction tends to really affect retirees.

Also, gradual increase in the IR by the central bank of the economy at the initial stages rather than the outright increase in it would be useful to stabilise the value of pension benefits. Furthermore, IRs on loans are recommended to be moderately fixed rather than increasing it at a fast rate in order to attract and encourage investment by pensioners.

Lastly, the various pension reforms should be reviewed periodically, and implementation of more such reforms year after year should be done as it tends to positively impact total pension benefits paid out in the long run.

Acknowledgements

The authors wish to acknowledge the comments and the helpful suggestions from the editor and the anonymous reviewers which gave shape to this article.

Competing interests

The authors have declared that no competing interests exist.

Authors' contributions

This work was carried out in collaboration between all authors. All authors read and approved the final manuscript.

References

Agyeman, A., 2011, 'An assessment of the returns on employee pension fund investments and their impact on future benefit payments; a case study of Social Security and National Insurance Trust (SSNIT)', An Unpublished master's thesis, Kwame Nkrumah University of Science and Technology, Kumasi. [ Links ]

Appiah, P., 1999, 'UTC as an off shoot of the Basel Mission in the Daily Graphic', A Ghanaian Daily Newspaper, 04 January, 1999, p. 15. [ Links ]

Bulow, J., 1982, The effects of inflation on the private pension system, University of Chicago Press, viewed 23 February 2016, from www.nber.org/chapters/c11455 [ Links ]

Clark, R.L. & McDermed, A.A., 1982, 'Inflation, pension benefits and retirement', The Journal of Risk and Insurance 49(1), 19-38. https://doi.org/10.2307/252574 [ Links ]

Gockel, A.F., 1996, The formal social security system in Ghana, Freiderich Ebert foundation, Accra. [ Links ]

Government of Ghana, 2008, National Pensions Act 766, Ghana Publishing, Accra. [ Links ]

Grubbs, D.S., 1979, 'The impact of inflation on pension plans', Record of Society of Actuaries 5, 983-1014. [ Links ]

Karam, P., Muir, D., Pereira, J. & Tudlashar, A., 2010, Macroeconomic effects of public pension reform, International Monetary Fund Working Paper WP/10/97, International Monetary Fund, Washington, DC. [ Links ]

Kumado, K. & Gockel, A.F., 2003, A study on social security in Ghana, Unpublished manuscript, University of Ghana, Legon. [ Links ]

Feldstein, M., 1981, 'Private pensions and inflation', The American Economic Review 71(2), 424-428. [ Links ]

Munnell, A.H. & Muldoon, D., 2008, 'The impact of inflation on social security benefits', Centre for Retirement Research 2, 8-15. [ Links ]

Obiri-Yeboah, D.A. & Obiri-Yeboah, H., 2014, 'Ghana's pension reforms in perspective: Can the pension benefits provide a house a real need of the retiree?', European Journal of Business and Management 6(32), 121-133. [ Links ]

Organisation for Economic Co-operation and Development (OECD), 2015, Pension at a glance: OECD and G20 indicators, OECD Publishing, Paris. [ Links ]

Thompson, G.B., 1978, 'Impact of inflation on private pensions of retirees, 1970-74: Findings from the Retirement History Study', Social Security Bulletin 41(11), 16-25. [ Links ]

United Nations Joint Staff Pension Board, 2008, Study on the impact of currency fluctuations on UNJSPF pension benefits, JSPB/55/R.39, United Nations, New York. [ Links ]

Whiteford, P. & Whitehouse, E., 2006, 'Pension challenges and pension reforms in OECD countries', Oxford Review of Economic Policy 22, 78-94. https://doi.org/10.1093/oxrep/grj006 [ Links ]

Correspondence:

Correspondence:

Robert Becker Pickson

myselfpickson@yahoo.com

Received: 18 Nov. 2016

Accepted: 10 July 2017

Published: 24 Oct. 2017

{kind=link}

{kind=link}

{kind=link}

{kind=link}