Serviços Personalizados

Artigo

Inglês (pdf)

Inglês (pdf)

Artigo em XML

Artigo em XML Referências do artigo

Referências do artigo

Indicadores

Links relacionados

-

Citado por Google

Citado por Google -

Similares em Google

Similares em Google

Compartilhar

Permalink

PermalinkSouth African Journal of Economic and Management Sciences

versão On-line ISSN 2222-3436

versão impressa ISSN 1015-8812

S. Afr. j. econ. manag. sci. vol.17 no.5 Pretoria 2014

ARTICLES

Market barriers for voluntary climate change mitigation in the South African private sector

Derick de Jongh; Carmen M Möllmann

The Albert Luthuli Centre for Responsible Leadership, University of Pretoria

ABSTRACT

A key challenge in the twenty-first century is to enable economic growth and increase both environmental quality and social inclusiveness, while mitigating and adapting to the impacts of climate change. The need for a transition to more sustainable consumption and production patterns is undeniable and sustainable economic growth must be placed at the heart of future development for all citizens. The South African private sector is under enormous pressure to remain globally competitive while balancing the interests of society, the environment and its shareholders. It has been suggested that there are discrepancies between what companies say and what they actually do, as they are challenged to move from policy to action. This paper evaluates the extent to which the private sector in South Africa adheres to voluntary climate change mitigation mechanisms and identifies potential market barriers impeding the large-scale uptake of such mechanisms. The research findings suggest that the private sector in South Africa has adopted a "take position, wait and see approach" which places them in a position to take advantage of and influence the opportunities and risks associated with climate change without having a negative impact on the bottom line. The primary barrier to voluntary climate change action is the vagueness of local and international policy frameworks. The different rules and resultant uncertainty around local and international frameworks appear to impede consistent and meaningful action. Although this uncertainty does not prevent the private sector from taking voluntary action, it does appear to negatively affect the overall scale and type of climate change mitigation efforts. While companies are continually improving the quality of sustainability reporting and public disclosure, the challenge still lies in translating these strategies into daily operations and sustainable practice that goes beyond ad hoc mitigation actions.

Key words: sustainability, corporate governance, climate change, mitigation, South Africa, private sector, market barriers

1 Introduction

Climate change is the "greatest and widest ranging market failure ever seen". It will have an estimated potential cost of a minimum of 5 per cent of annual global GDP, if action is not taken (Stern, 2006:1). To remain competitive and profitable, companies will have to incorporate climate change and environmental awareness into their business strategies and operations or risk losing business from the growing number of environmentally concerned customers and consumers (KPMG, 2009:4). There are various factors that influence corporate response to climate change, ranging from economic opportunities to moral responsibility (Okereke, 2007:484; Reyers & Gouws, 2010:92). The scale and impact of corporate action are, however, limited, as action is voluntary. Although South Africa has a number of principle-based reporting mechanisms to ensure disclosure of economic, environmental and social impact, the onus lies on companies to implement climate change mitigation measures. A perception still exists within South African boardrooms that sustainability issues can be seen as an afterthought and generally "as little more than a peripheral, external issue" (Trialogue, 2007:11; Incite Sustainability, 2009:66).

This study aims to identify the market barriers preventing the private sector from voluntarily introducing climate change mitigation.

This was achieved by exploring the existence of market barriers in the climate change mitigation market through a literature review, test questionnaires, full questionnaires and follow up semi- structured interviews, with a focus on Johannesburg Stock Exchange (JSE) Sustainability Reporting Investment (SRI) Index 2010 companies.

This paper first reviews the relevant sustainable development, corporate governance and climate change literature. It then presents the research design and methods, followed by the research results, recommendations, future research, conclusions and references.

2 Sustainable development

We are witnessing the emergence of a new and very different world (WBCSD, 2011:6) - a world that is increasingly recognising the need to move towards sustainable development - to meet "the needs of the present without compromising the ability of future generations to meet their own needs" (WCED, 1987:51). According to the United Nations Population Fund, as the world's economies and populations continue to grow, the demand for finite natural resources is increasing unsustainably (UNFPA, 2011:2; Lloyd & Subbarao, 2009: 237). The social, environmental and economic pressures of the modern world are the result of developmental objectives which have required a drawdown of resources, primarily fossil fuels, since the 1850s (IPCC 2011:2-3; Lloyd & Subbarao, 2009:237). The world's population increased by 250 per cent between 1950 and 2000 alone (UNFPA, 2011:2), with sub-Saharan Africa's population expected to double or treble in the next 40 years (UNFPA, 2011:5). This will put increased pressure on natural resources, food, energy, and infrastructure, and on top of growing poverty, food insecurity and resource scarcity, climate change is expected to exacerbate the existing stresses; the need for collective global action is therefore growing (Bernstein et al., 2007:49).

The celebrated 1987 Brundtland Report (WCED, 1987:51) argued that the historical categorisation of economic, social and environmental issues as separate concerns was no longer valid, and that in order to move to a sustainable future, their interconnectedness needed to be acknowledged (WCED, 1987:20). It ignited a global realisation that the world's current consumption levels were not sustainable and that collective action needed to be taken, leading to the 1992 Rio Summit of the United Nations Conference on Environment and Development (UNCED, Earth Summit) and the adoption of Agenda 21, which stipulates a sustainable development plan of action to be taken globally, nationally and locally by organisations within the UN System, governments, and major groups (Kates, Parris & Leiserowitz, 2005:10). The increasing global commitment to move towards a common future resulted in the UN General Assembly's adopting the Millennium Development Goals (MDGs) in 2000 (Drexhage & Murphy, 2010:9).

In 2002, a decade after the Rio Summit, countries met again and reaffirmed their commitment to sustainable development at the World Summit on Sustainable Development (WSSD), held in Johannesburg (Kates et al., 2005:10). As sustainable development is rapidly integrated into global thinking as a concept, goal and ideology (Kates et al., 2005:10), extensive dialogue and research have sought to further define the meaning of the term "sustainable development" (Ciegis Ramanauskiene & Martinkus, 2009:34; Kates et al., 2005:20). The ambiguity of the definition makes it unclear how much needs to be invested, which at times has led to an approach that varies from "sustain only" to "develop mostly" by global and national private and public sectors (Kates et al., 2005:12).

In the South African context, sustainable development is embedded in the Constitution of the Republic of South Africa, 1996, and formalised through the National Environmental Management Act 107 of 1998 as the "integration of social, economic and environmental factors into planning, implementation and decision making so as to ensure [that] development serves present and future generations" (South Africa, 1998). Since the Rio Summit in 1992, sustainable development as a discourse has been dominated by climate change. However, climate change forms only a part of the broader sustainable development discourse and challenge (Drexhage & Murphy, 2010:9).

3 Climate change

Sustainable development and climate change are not mutually exclusive terms, but rather have a two-way relationship, which can be mutually reinforcing (Drexhage & Murphy, 2010:9). Grist (2008:785) indicates that the management of climate change falls under the umbrella of sustainable development because of its long-term implications, in addition to its potential impact on the social, economic and environmental well-being of future generations.

As a developing country, South Africa is tackling a number of socio-economic challenges, ranging from job creation to the reduction of poverty and inequality. The Government recognises the need to reduce greenhouse gas emissions and mitigate the impact on climate change by weaning itself off its fossil fuel dependence (South Africa, 2011:9). In 2009, it was estimated that if South Africa continued with a "business as usual" approach, greenhouse gas emissions would quadruple by 2050 (Institute of Directors in Southern Africa, 2009:11).

South Africa is a fossil fuel dependent nation, with approximately 90 per cent of its energy derived from low-cost coal. In 2000 "the average energy use emissions for develop-ping countries constituted 49 per cent of total emissions, whereas South Africa's energy use emissions constituted just under 80% of total emissions" (South Africa, 2011:26). The Government has acknowledged that it must act to mitigate its emissions as it is one of the world's least energy-efficient economies (Incite Sustainability, 2011:18), and in 2011 the Government approved the National Climate Change Response White Paper, which sets out transition toward a climate-resilient and lower carbon economy and society, committing South Africa to making a "fair contribution to stabilising global Green House Gas (GHG) concentrations in the atmosphere and to protecting the country and its people from the impacts of inevitable climate change" (South Africa, 2011:10).

4 Climate change and the private sector

The Institute of Directors (2009:9) states: "Sustainability is the primary moral and economic imperative of the twenty first century," and is "one of the most important sources of both opportunities and risks for business". Sustainability in the private sector space can be defined as "meeting the needs of a firm's direct and indirect stakeholders (such as shareholders, employees, clients, pressure groups, communities) without compromising its ability to meet the needs of future stakeholders" (Dyllick & Hockerts, 2002:131). The aforementioned authors argue that a singleminded focus on economic stability can yield lucrative economic results in the short term, but to achieve long-term sustainability, all three sustainability dimensions (economic, environmental and social) must be satisfied simultaneously (Dyllick & Hockerts, 2002:132). The general failure to adopt a broader outlook on sustainable development within the implementation of company operations has resulted in a short-term economic perspective.

As stated by King (2009:13), "a key challenge for leadership is to make sustainability issues mainstream: the leadership must integrate strategy, sustainability and control (integrated governance), and establish the values and ethics that underpin sustainable practices". As such, governance, strategy and sustainability have become inseparable. King (2009:6) defines corporate governance as the "establishment of structures and processes, with appropriate checks and balances that enable directors to discharge their legal responsibilities and oversee compliance with legislation". However, the indications are that insufficient action is being taken (Incite Sustainability, 2009:4) and implementation is proving to be difficult (KPMG 2011a:3).

In reference to climate change, mitigatory action is broadly divided into compliance and voluntary action. Compliance actions stem from the Kyoto Protocol, where the primary motivation is regulatory compliance (UNFCCC 2011:1). The voluntary market, by contrast, is a demand-driven market impelled by voluntary action to reduce emissions (Reyers, 2009:21). Climate change as a global concern requires collective action from both the private and the public sector. This is crucial if the impact on the environment is to be mitigated, but the required action is not being taken because of the barriers that are inhibiting climate change mitigation from realising its full potential.

5 Market barriers to corporate climate change action

Market barriers within the mitigation market are defined as "conditions that prevent or impede the diffusion of cost-effective technologies or practices that would mitigate GHG emissions" (IPCC, 2008:817). Brown et al. (2007:xiii) identify barriers impeding the commercialisation of climate change mitigation technologies and suggest that these barriers are wide ranging, with the two biggest being the absence of a price on GHG emissions and issues relating to cost effectiveness.

KPMG (2011a:4) found that companies globally are increasingly taking climate change mitigation more seriously. However, uncertainty is a still a barrier as the corporate value associated with responding to climate change is undetermined - companies require increased information and visibility on climate policy, carbon prices, and harmonisation within regulations to reduce the current risk (Pricewater-houseCoopers, 2008:iv), as well as an appropriate, robust and clear international framework of regulations within which companies can plan and invest with confidence (KPMG, 2011a:3; Okereke, 2007:483; Shu & Schroeder, 2010:299; WBCSD, 2011:20 KPMG (2011b:5) recommends strong and clear policy signals from the South African government, as well as information on how these policies will result in the transition to a low carbon economy. Reyers (2009:1-165) set out to determine what motivates voluntary climate change mitigation in South Africa and discovered three key motivational drivers: legitimacy, the financial business case and moral responsibility. Legitimacy refers to the impetus to take action because stakeholders expect (or will soon expect) the private sector to do so. Moral responsibility refers to the company's regarding voluntary climate change mitigation as the right thing to do, albeit with resource implications (time and/or money). Finally, the financial business case relates to actions taken by the companies that will either make or save them money (Reyers & Gouws, 2010:105). Climate change governance seems to be integrated and reported within governance activities. However, limited action is a common trend (PricewaterhouseCoopers, 2011:11; Unter-lerchner, 2007:50) despite an increased awareness of the risks and opportunities associated with climate change (Incite Sustain-ability, 2008: 64-65; Tyler, 2007:32). Shu & Schroeder (2010:299) argue that this lack of environmental stewardship action is due to managers' not being fully empowered to make changes as initiatives are often once-off projects that are not aligned with corporate strategy. Furthermore, a systemic market barrier exists relating to continuous corporate focus on short-term gains (KPMG, 2011a:4) as companies are motivated by a financially dominated paradigm and not by a legitimate one (Unterlerchner, 2007:50; Reyers, 2009:165), 2011:27). Peter and Swilling (2011:2) indicate that demand-side mitigation efforts alone will not be enough; what is required is normative change which will result in behavioural change as there are currently inadequate incentives for companies to act (United Nations Global Compact, 2011:7).

The next section will present the research design and methods used.

6 Research design and methods

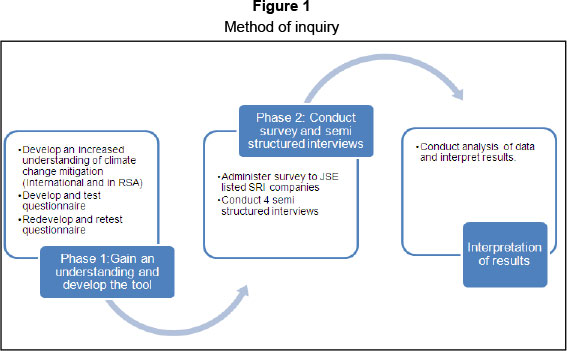

The research process employed a mixed method approach over two research phases, as represented in Figure 1. Phase 1 mainly used qualitative data, while Phase 2 used quantitative primary data - which both contributed to the findings.

In Phase 1, a draft questionnaire was developed to consult with climate change experts and suppliers, to explore the topic in depth, and to finalise a questionnaire to be used in Phase 2. The respondents were asked to review each of the 60 questions based on their experience, and to indicate whether the questions were clear and essential, and then state what suggested changes and additions to questions and themes should be included. The target population in Phase 1 included 40 experts and suppliers of climate change mitigation products in South Africa. Experts and suppliers were defined as persons who have been actively involved in climate change for more than six years. They represented academia, consultants, suppliers of renewable energy and public servants from the Government departments concerned. The group of respondents consisted of eight men and four women, nine of which had a Master's degree. The majority classified themselves as consultants in the sector. The predominant technique used in Phase 1 of the study was reviewing the "frequency of occurrence" on the basis of the quantifiable data of the draft questionnaire. The descriptive data were discussed and analysed.

The second phase involved using the questionnaire developed in Phase 1 to survey the population of the Johannesburg Stock Exchange (JSE) Sustainability Reporting Investment (SRI) Index 2010 companies, which comprises 74 companies from different industries. The only differentiating characteristic used in this study was their level of environmental impact (high versus low). This population was used in the study primarily on account of their knowledge and involvement in sustainability and because they represent some of the most influential and proactive companies in South Africa and Africa. The survey was selfadministered and was sent to each Chief Operating Officer (CEO), who either completed the questionnaire or sent it to the senior managers responsible for corporate climate change mitigation. In view of the sensitive nature of the questionnaire, it was completed in confidence and therefore further disaggregation is not possible.

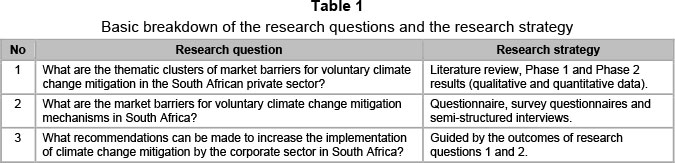

A total of 26 completed questionnaires were received, signifying a 35 per cent response rate. In addition, four semi-structured interviews were conducted after the survey. The interviewees were purposefully selected from the JSE SRI sample with the object of gaining further insight into the findings and thereby increasing the rigour of the study. Table 1 below provides a breakdown of the research questions and the research strategy employed per question.

Again, in Phase 2, the "frequency of occurrence" technique was used to make comparisons via the establishment of statistical relationships. Inductive reasoning - which is not underpinned by a predetermined theory - was used to draw conclusions about the sample. Ordinal data, collected by means of a logical, categorised questionnaire, allowed for the ranking of results based on scales or symbols. Measures of central tendency (mode, mean and median) were used extensively in the analysis, in combination with the standard deviation, to explain the results. In addition, a comparison of high and low environmental impact companies was performed to determine whether there was a correlation. The comparison was performed through the Wilcoxon matched pairs method and the Fisher method to establish relationships and frequencies. For related groups, this technique is considered to be the nonparametric alternative to the t-test, and it was specifically used to determine the magnitude of differences between the two groups. Where it was not possible to use the Wilcoxon matched pairs test the Fisher exact test method was used instead.

7 Research results

The literature study (Phase 1) provided a broad framework for the study and revealed five thematic clusters of market barriers that inhibit the uptake of voluntary climate change mitigation mechanisms in the South African private sector. Firstly, there are sustainability values, which concern the commitment of the managements of organisations to the triple bottom line based on abstract sustainability ideals. The second is legislation, which refers to the regulatory framework within which climate change initiatives operate and outlines the legal requirements which have to be met. The third thematic cluster is knowledge of GHG mitigation instruments; this represents the expertise, skills and experience which organisations use to take steps to mitigate their impact on climate change. The fourth cluster represents organisational strategy, which is the corporate will and action required to implement corporate climate change action. Finally, there is finance, which relates to cost, productivity, efficiency and risk and their relationship with climate change mitigation action.

The feedback from the questionnaire indicated that the questions and thematic clusters tested were clear and essential. The major changes involved combining questions, rewording and clarifying terminology. This process validated the research conducted in the literature review by identifying themes acting as a market barrier to corporate voluntary climate change mitigation, which was further tested in Phase 2.

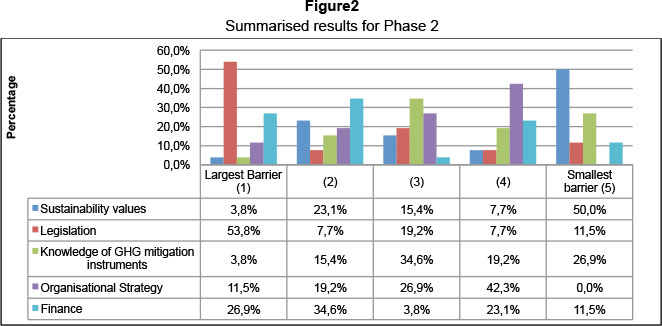

The JSE SRI listed respondents who participated in the primary survey research in Phase 2 ranked the five market barrier clusters based on their level of significance in inhibiting the uptake of voluntary climate change mitigation as represented in Figure 2. In addition, the survey reviewed corporate motivations, perceptions and rationale for climate change mitigation; the findings are discussed in greater detail in the research results.

The respondents indicated that the biggest barrier, in ranked order, is the lack of existing legislation. This was followed by finance and the lack of internal knowledge of GHG mitigation instruments within the private sector. This fourth barrier was organisational strategy and the smallest barrier was considered to be sustainability values. These findings were further supported by the informal interviews.

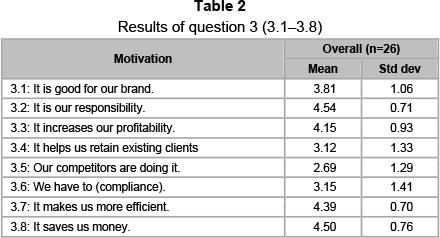

Questions 3, 4, 6 and 7 probed the rationale, motivation and important characteristics of voluntary climate change mitigation products. The significant results of these questions are discussed below. Questions 3, 4 and 6 used a five-point scale, with participants being asked to indicate what their company's view was, based on the particular statement, with 1 representing "strongly disagree" and 5 representing "strongly agree". Question 7 used a slightly different scale, with 1 representing "not important" and 5 representing "very important".

Question 3 (3.1-3.8) asked participants what motivation there was for companies to take action on climate change; the results are represented in Table 2 below and reflect the mean response, with 5 representing "strongly agree" and 1 being "strongly disagree".

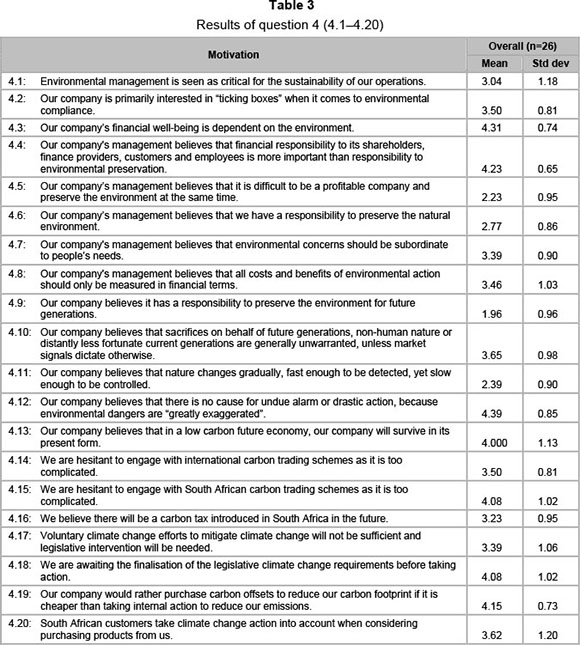

The fourth question (comprising 20 statements as represented in Table 3 below) indicates the companies' opinions and motivations regarding the environment. Table 3 reflects the mean response, with 5 representing "strongly agree" and 1 being "strongly disagree". In comparing companies with different levels of environmental impact, using the Wilcoxon p-value test, a significant difference between high- and low-impact companies was found for questions 4.5, and 4.11.

Question 6 (6.1-6.20) asked whether respondents' companies have measured their carbon emissions, to which 100 per cent of companies indicated "Yes" (Question 6.8), while 85 per cent (22/26) indicated that they have a detailed understanding of their carbon emissions footprint and have set realistic and achievable carbon reduction targets (Question 6.15). However, 62 per cent (15/26) have not allocated sufficient resources to achieve their carbon reduction target (Question 6.9), even though 92 per cent (24/26) believe that they can reduce their environmental footprint while increasing their productivity in a sustainable way (Question 6.10, reverse scored). The results showed that 69 per cent (15/26) of respondents indicated that climate change is clearly featured at a strategic planning level within their company (Question 6.11) and 77 per cent (20/26) indicated that it is clearly featured at an operational planning level within the company (Question 6.12). Only 46 per cent (12/26) of respondents factor the costs for greenhouse gas mitigation into major investment and operational decisions (Question 6.16). When conducting a comparison test based on environmental impact for Question 6.16 using the Fisher p-value test, a statistical difference was found between the two groups, with a confidence level of 5 per cent (p-value 0.0246). The results indicate that high-impact companies do factor the costs for greenhouse mitigation into investment decisions (75 per cent (9/12)) while low-impact companies do not (65 per cent (9/14)). The findings do, however, show that 65 per cent (17/26) of companies believe climate change will have a fundamental impact on their business model (Question 6.18), while 62 per cent (16/26) perceive carbon management as a business asset which can create new opportunities (Question 6.14). Question 6.19 asked respondents if their "company's chairperson clearly articulates the company's views on climate change and greenhouse gas control measures".

To this question, 69 per cent (18/26) indicated "Yes". To add to this, 85 per cent (22/26) indicated that their board conducts periodic reviews on climate change and monitors progress in implementing strategies (Question 6.20). The majority (62 per cent (16/26)) of companies believe they have sufficient skills in their company to account for and administer greenhouse gas mitigation products internally (Question 6.13). The companies seemed generally uncertain whether investors take climate change action into account when deciding to invest in their company (Question 6.17), with 54 per cent (14/26) indicating that they do take it into account, 35 per cent (9/26) indicating that they do not, and 11 per cent (3/26) being undecided.

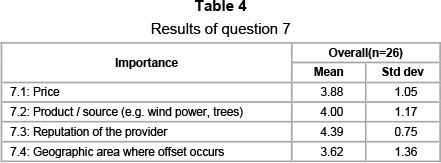

In Question 7, the survey reviewed perceptions about the importance of certain "product" characteristics of voluntary climate change mitigation products (see Table 4). The table reflects the mean response, with 5 representing "strongly agree" and 1 being "strongly disagree". The Wilcoxon p-value test was used to compare companies with different levels of environmental impact and a significant difference between high- and low-impact companies was found for questions 7.2, 7.3 and 7.4.

8 Research findings

The results indicate that the themed clusters, in rank order, are legislation, followed by finance, knowledge of the GHG mitigation instruments, organisational strategy and lastly sustainability values. The themed clusters are not mutually exclusive nor are they exhaustive, rather they provide a framework of theme-based market barriers. Inaction (or limited action) does not lie with one barrier alone as the barriers are complex and multidimensional; and thematic market barriers are often mutually reinforcing. Further specific findings from the study are discussed below, as they relate to policy, level of environmental impact, the utilisation of mitigation instruments, sustainability values and the corporate challenges imposed by moving from strategy to action.

a Legislative and policy frameworks

The primary barrier to voluntary climate change action concerns the vague local and international policy frameworks. The different rules and resultant uncertainty around local and international frameworks appear to impede consistent and meaningful action. While this uncertainty does not prevent the private sector from taking voluntary action, it does appear to negatively affect the overall scale and type of climate change mitigation efforts.

The study found that the South African private sector believes that voluntary climate change efforts alone will not be sufficient and that additional legislative intervention will be required. Companies indicate that future legislation will act as a catalyst to expand the climate change mitigation market, which in the absence of clear rules encourages a "wait and see" approach. In a challenging economic climate, companies are obliged to balance economic, social and environmental interests while remaining globally competitive. The private sector may therefore be positioning itself, ready to take action once legislation has been clarified and implemented. Until such time, internal energy efficiency will be the primary action taken. The study found that actions are largely motivated by the financial business case and driven by an increase in efficiency, profitability and money saving.

Those companies that have already implemented voluntary action to reduce their GHG emissions are generally motivated by a financial business case with short-term payback periods. Currently, there are no financial penalties for those companies that do not act, and limited financial incentives for those who do act beyond the business case. It could therefore be argued that the relative lack of legal requirements concerning corporate climate change presents a significant barrier by creating a competitive disadvantage for those companies that take action in the present.

The possible implementation of a South African carbon tax was included as a question in the research questionnaire to ascertain whether the private sector is expecting to see it introduced in the near future. The majority of respondents expected the implementation of this tax. In February 2012 the National Treasury announced that a tax will be imposed in 2013 or 2014 to limit GHG emissions based on industry sector, thereby making companies responsible for their external environmental costs. At the time of writing, full and final details of the tax law remain unclear.

b Low versus high environmental impacts

Companies with a high environmental impact seem to be more price-sensitive than low environmental impact companies when taking action to mitigate climate change. Price sensitivity is related to factors such as the level of emission reductions required and the subsequent cost and scale of action required from companies with a higher environmental footprint. Compared to low-impact companies, high environmental impact companies indicate that it is more difficult to be profitable while simultaneously preserving the environment.

c Mitigation instruments

The private sector has a limited appetite for purchasing GHG mitigation instruments such as carbon offsets. Despite the importance of factors such as price, reputation of the supplier, product source and geographic location, the private sector indicates that it would rather take internal action to reduce emissions than purchase carbon offsets - even if the former is more expensive. Half of the respondents indicated that GHG mitigation instruments were not too expensive and 35 per cent indicated that they did not know the costs involved. This result therefore reflects the fact that only 15 per cent of respondents believe that these instruments are too expensive. It could be argued that the private sector has had limited active engagement with GHG mitigation instrument providers, despite knowing how and where to access these products. Furthermore, the results indicate that companies have a narrow perspective on climate change actions, as the majority have not considered purchasing offsets on the carbon market or South African renewable energy certificates.

d Sustainability values

Company sustainability values reflect the commitment by management towards environmental preservation and their inherent responsibility to help mitigate climate change. Companies are finding it difficult to translate these values into climate change mitigation behaviour and manage the expectations of all stakeholders. The challenge lies in putting such commitments into practice. Companies believe that environmental management is critical for the sustainability of their operations. They further believe their financial well-being is dependent on the environment and that it is their responsibility to take action as corporate citizens to preserve the natural environment for future generations. The corporate sector is primarily motivated by financial benefits associated with increased efficiency, productivity and profits. A secondary motivation for companies to take action is to align themselves with the perceived positive branding opportunities related with climate change activities. South African companies indicate that they are not motivated by their competitors' climate change actions. This is probably due to the fact that the majority see themselves as leaders (or fast followers) in climate change mitigation efforts and assume their competitors to be lagging behind in such efforts. Interestingly, the research shows that more than a third of the companies are uncertain whether their South African and/or international customers take climate change into account when purchasing their products. When comparing local with international customers, there is a tendency to think that international customers are more influenced by climate change action than their South African counter parts. The cost benefit of corporate climate change action beyond the obvious business case has yet to be determined as the private sector is generally uncertain of the true drivers for their investors' and customers' decisions.

e Implications: Moving from strategy to action

The companies indicated that they have a detailed understanding of their carbon emissions footprint and have set realistic and achievable carbon reduction targets. However, when reviewed in detail, many companies seem to be reporting one thing while doing another. All of the companies who participated in the study indicated that they had measured their carbon emissions, while 85 per cent indicated that they have set realistic and achievable carbon reduction targets. However, only 38 per cent allocated sufficient resources to actually achieve said targets. This irregularity in the setting of "seemingly" realistic targets and thereafter failing to assign sufficient resources to achieve the targets leads to the perception that falling short of targets is not of great consequence, nor is meeting targets a priority.

Companies regularly include climate change considerations at the strategic and operational planning level, but less than half of these factor GHG costs into the actual major investment and operational decisions. Significant statistical differences which were found based on the level of a company's environmental impact need to be taken into consideration. The majority of high-impact companies do factor such costs into investment decisions, whereas 65 per cent of low-impact companies do not. The majority of corporate actions are short term, once-off initiatives without any seemingly large-scale impacts. In this context, motivation to take action on climate change is again based on a financial business case, as found by Reyers (2009:165).

The research shows that although companies recognise that they can reduce their environmental footprint while increasing their productivity in a sustainable manner, this is seemingly not being put into practice. These discrepancies raise the question of how seriously the corporate sector is taking action on climate change, and the perceived importance of being "seen" to be involved in climate change action from a political and/or strategic viewpoint. It could be argued that the scale and level of action required may demotivate companies as they attempt to balance a number of priorities but fail to assign similar priority levels and resource expenditure to climate change action.

In general the findings suggest that the private sector is politically and ethically committed to environmental stewardship. They recognise their inherent responsibilities and impacts on the environment and are dedicated in principle to mitigating their impacts on climate change. The challenge lies in remaining globally competitive and maximising shareholder returns while balancing social and environmental ideals and interests. The private sector has adopted a "take position, wait and see approach" which places them in a position to take advantage of and influence the opportunities and risks associated with climate change without having a negative impact on the bottom line.

9 Recommendations

It is recommended that legislative and regulatory bodies negotiate and implement a simple, clear and effective policy framework, both nationally and internationally. The lack of clarity regarding regulations and growing uncertainty in the private sector impede the utilisation and growth of voluntary climate change mitigation mechanisms. It is recommended that such regulations prescribe penalties to companies with excess emissions and reward companies which take steps to mitigate their impacts. Stakeholders and specifically the private sector should be consulted in the development of these regulations to ensure that implementation progresses beyond once-off, short-term projects in favour of mainstream programmes that produce long-term change.

Given that corporate action in terms of disclosure seems to be a growing trend, it is recommended that clear measureable actions be reported alongside targets that go beyond disclosure. Both actions and targets should be tracked in order for companies to be held accountable. It is further recommended that the King Committee review its King Code to include a form of regulation that moves beyond motivating companies on a purely voluntary basis.

It is recommended that the regulatory focus shift towards enabling factors in order to encourage the private sector to participate more meaningfully and quantitatively in mitigating their impacts. These enabling factors should incentivise companies and not competitively disadvantage them for being progressive.

Although the findings suggest that for reasons which remain ambiguous the corporate sector has little or no appetite for external GHG mitigation instruments, it is recommended that the suppliers of external GHG mitigation instruments further engage with the private sector to better understand their needs, requirements and motivations in adopting climate change action. It is further recommended that suppliers communicate collectively and effectively with the private sector and demonstrate the benefits of their instruments. The research indicates that corporate branding is an important motivator for companies to take action. It is therefore recommended that suppliers of GHG mitigation instruments align themselves further with branding opportunities as an entry point into the private sector.

With global competition at its keenest, companies require a detailed understanding of the purchasing habits and motivators of their consumers and investors. It is recommended that companies include climate change purchasing and investment indicators within their market research frameworks, to determine whether consumers' and investors' habits and trends are influenced by corporate climate change action.

10 Conclusions

The findings of the study highlight the market barriers that are impeding the uptake of voluntary climate change mitigation mechanisms by the private sector. Furthermore, the research indicates that the lack of uptake does not lie with one barrier alone but rather that barriers are complex and mutually reinforcing; therefore potential strategies to remove barriers should view the barriers as an interconnected system rather than as separate components. The research identifies the need for simple, clear and effective policy or a regulatory framework to be implemented nationally and internationally. This framework should stipulate that companies with excess emissions should be penalised while companies taking decisive action to mitigate their impacts should be rewarded. Corporate climate change actions should be integrated within the entire organisation and should be mainstreamed, not only into policy, but also into sustained practice. Companies are continually improving the quality of reporting and public disclosure, but this is not enough if we are to successfully tackle global climate change and ensure a sustainable future for generations to come. The time has come for business, government and civil society to translate their values into behaviours and actions and to share the responsibility of climate change.

References

BERNSTEIN, L., BOSCH, P., CANZIANI, O., CHEN, Z., CHRIST, R., DAVIDSON, O., HARE, W., HUQ, S., KAROLY, D., KATTSOV, V., KUNDZEWICZ, Z., LIU, J., LOHMANN, U., MANNING, M., TAROH, M., MENNE, B., METZ, B., MIRZA, M., NICHOLLS, N., NURSE, L., PACHAURI, R., PALUTIKOF, J, PARRY, M., QIN, D., RAVINDRANATH, N., REISINGER, A., REN, J., RIAHI, K., ROSENZWEIG, C., RUSTICUCCI, M., SCHNEIDER, S., SOKONA, Y., SOLOMON, S., STOTT, P., STOUFFER, R., SUGIYAMA, T., SWART, R., TIRPAK, D., VOGEL, C., & YOHE, G. 2007. Climate change: synthesis report. Intergovernmental Panel on Climate Change, Valentia, Spain. [ Links ]

CIEGIS, R., RAMANAUSKIENE, J. & MARTINKUS, B. 2009. The concept of sustainable development and its use for sustainability scenarios. Engineering Economics, 62(2):28-37. [ Links ]

CORINA, G. & ROXANA, S. 2011. Comparative study on corporate governance. Economic Science Series, 20(2):674-680. [ Links ]

DEPARTMENT OF ENVIRONMENTAL AFFAIRS AND TOURISM. 2009. National climate change response policy: Discussion document for the 2009 National climate change response policy development summit. Available at: www.ccsummit2009.co.za/framework.html [accessed 2010-07-15]. [ Links ]

DREXHAGE, J. & MURPHY, D. 2010. Sustainable development: From Brundtland to Rio 2012. Available at: http://www.un.org/wcm/webdav/site/climatechange/shared/gsp/docs/GSP1-6_Background%20on%20Sustainable%20Devt.pdf [accessed 2012-09-10]. [ Links ]

DYLLICK, T. & HOCKERTS, K. 2002. Beyond the business case for corporate sustainability. Business Strategy and the Environment, 11(2):130-141. [ Links ]

GRIST, N. 2008. Positioning climate change in sustainable development discourse. Journal of International Development, 20(6):783-803. [ Links ]

INCITE SUSTAINABILITY. 2008. Carbon disclosure project report 2008: JSE Top 100. Available at: http://www.cdproject.net/reports.asp [accessed 2009-10-01]. [ Links ]

INCITE SUSTAINABILITY. 2009. Carbon disclosure project 2009: South Africa JSE 100. Available at: http://www.nbi.org.za/welcome.php?pg=2&pgm=M&id=11046 [accessed 2009-07-10]. [ Links ]

INCITE SUSTAINABILITY. 2011. CDP South Africa JSE 100 Report 2011: Partnering for a low carbon future. Available at: https://www.cdproject.net/CDPResults/CDP-2011-South-Africa-JSE-100-Report.pdf [accessed 2012-05-10]. [ Links ]

INTERGOVERNMENTAL PANEL ON CLIMATE CHANGE (IPCC). 2008. IPCCFourth assessment report: Annex 1 glossary, Aviel Verbruggen (ed.) Belgium. [ Links ]

IPCC. 2011. Summary for policymakers. In: O. Edenhofer, R. Pichs-Madruga, Y. Sokona, K. Seyboth, P. Matschoss, S. Kadner, T. Zwickel, P. Eickemeier, G. Hansen, S. Schlvmer, C. von Stechow (eds.) IPCC special report on renewable energy sources and climate change mitigation. Cambridge, UK and New York, NY: Cambridge University Press, [ Links ]

INSTITUTE OF DIRECTORS SOUTHERN AFRICA. 2009. King code of governance for South Africa 2009. [ Links ]

KATES, R., PARRIS, T. & LEISEROWITZ, A. 2005. What is sustainable development? Goals, indicators, values and practice. Environment: Science and Policy for Sustainable Development, 47(3):8-21. Available at: http://www.heldref.org/env.php [accessed 2012-04-10]. [ Links ]

KING, M.E. 2006. The corporate citizen. South Africa: Penguin. [ Links ]

KING. M.E. 2009. King report on governance for South Africa 2009. Institute of Directors Southern Africa 2009. Available at: http://www.iodsa.co.za/downloads/documents/King_Code_of_Govemance_for_SA_2009.pdf [accessed 2012-05-10]. [ Links ]

KPMG. 2009. Sustainable IT, finding your shade of green. Available from: http://www.iodsa.co.za/king.asp#King%20III%20Report%20-%202009 [accessed 2009-03-12]. [ Links ]

KPMG. 2011a. Corporate sustainability: A progress report. KPMG International, Switzerland. [ Links ]

KPMG. 2011b. South Africa's carbon chasm based on carbon disclosure project 2010 responses from the JSE 100 companies. Available at: https://www.cdproject.net/CDPResults/south-africa-carbon-chasm.pdf [accessed 2012-10-10]. [ Links ]

LLOYD, B. & SUBBARAO, S. 2009. Development challenges under the clean development mechanism (CDM) - Can renewable energy initiatives be put in place before peak oil? Energy Policy, 37(1)237:245. [ Links ]

NAIDOO, R. 2009. Corporate governance: An essential guide for South African companies. Pietermaritzburg: Juta. [ Links ]

OKEREKE, C. 2007. An exploration of motivations, drivers and barriers to carbon management: The UK FTSE 10. European Management Journal, 25(6):475-486. [ Links ]

PRICEWATERHOUSECOOPERS. 2008. Global disclosure report 2008: Global 500. Available at: http://www.cdproject.net/reports.asp [accessed 2009-04-13]. [ Links ]

PRICEWATERHOUSECOOPERS. 2009. King's council: Understanding and unlocking the benefits of sound corporate governance. Executive guide to King III, South Africa: PricewaterhouseCoopers Inc. [ Links ]

PRICEWATERHOUSECOOPERS. 2011. CDP global 500 report 2011: Accelerating low carbon growth. Available at: https://www.cdproject.net/CDPResults/CDP-G500-2011-Report [accessed 2012-04-20]. [ Links ]

REEEP. 2010. Corporate clean energy investment trends in Brazil, China, India and South Africa. Available at: https://www.cdproject.net/CDPResults/CDP-G500-2011-Report [accessed 2012-02-20]. [ Links ]

REYERS, M. 2009. Corporate sustainability consciousness: A climate change perspective. Published MCom thesis, University of Pretoria. [ Links ]

REYERS, M. & GOUWS, D. 2010. An exploratory study of motivations driving corporate investment in voluntary climate change mitigation in South Africa. South African Journal of Economic and Management Sciences, 14(1)92-108. [ Links ]

SHU, C. & SCHROEDER, H. 2010. Private governance of climate change in Hong Kong: An analysis of drivers and barriers to corporate action. Asian Studies Review, 34(3):287-308. [ Links ]

SOUTH AFRICA. 1998. National Environmental Management Act 107 of 1998. Government Gazette 401(19519):1-72. Available at: http://www.info.gov.za/view/DownloadFileAction?id=70641 [accessed 2009-10-15]. [ Links ]

SOUTH AFRICA. 2011. National climate change response - White paper. Available at: http://www.info.gov.za/view/DownloadFileAction?id=152834 [accessed 2011-07-10]. [ Links ]

STERN, N. 2006. The economics of climate change: Summary of conclusions. Available at: http://www.hmtreasury.gov.uk/d/CLOSED_SHORT_executive_summary.pdf [accessed 2009-04-10]. [ Links ]

TRIALOGUE. 2007. The sustainable business handbook: Smart strategies for responsible companies. (4th ed.) Cape Town: Trialogue. [ Links ]

TYLER, E. 2007. Carbon disclosure project South Africa report 2007: JSE Top 40. Available at: http://www.cdproject.net/cdp5reports.asp [accessed 2010-04-18]. [ Links ]

United Nations Environment Programme (UNEP). 2011. Towards a green economy: Pathways to sustainable development and poverty eradication - A synthesis for policy makers. Available at: www.unep.org/greeneconomy [accessed 2011-08-12]. [ Links ]

UNITED NATIONS FRAMEWORK CONVENTION ON CLIMATE CHANGE (UNFCC). 2011. [ Links ]

UNITED NATIONS POPULATION FUND (UNFPA). 2011. The state of world population. New York. USA. [ Links ]

UNITED NATIONS INDUSTRIAL DEVELOPMENT ORGANIZATION (UNIDO). 2003. Clean development mechanism (CDM) investor guide. Vienna, Austria. [ Links ]

UNTERLERCHNER, J. 2007. Survey of integrated sustainability reporting In South Africa: An investigative study of the companies listed on the JSE securities exchange all share index. Unpublished thesis, University of Stellenbosh. [ Links ]

UNTERLERCHNER, J. & MALAN, D. 2008. The corporate response to sustainability reporting. USB Leaders Lab Magazine, August 2008:22-25. Available at: http://www.usb.sun.ac.za/USB/discover/LeadersLab/August%202008/Corporate_response _sustainability_reporting.pdf [accessed 2009-03-12]. [ Links ]

WORLD BUSINESS COUNCIL FOR SUSTAINABLE DEVELOPMENT (WBCSD). 2011. Transformation in the turbulent teens. Geneva, Switzerland. [ Links ]

WORLD COMMISSION ON ENVIRONMENT AND DEVELOPMENT (WCED). 1987. Our common future. New York: Oxford University Press. [ Links ]

Accepted: May 2014

{kind=link}

{kind=link}