Servicios Personalizados

Articulo

Inglés (pdf)

Inglés (pdf)

Articulo en XML

Articulo en XML Referencias del artículo

Referencias del artículo

Indicadores

Links relacionados

-

Citado por Google

Citado por Google -

Similares en Google

Similares en Google

Compartir

Permalink

PermalinkSouth African Journal of Economic and Management Sciences

versión On-line ISSN 2222-3436

versión impresa ISSN 1015-8812

S. Afr. j. econ. manag. sci. vol.17 no.3 Pretoria jul. 2014

ARTICLES

The management accounting vocational fallacy

Christina Cornelia Shuttleworth

School of Accounting Sciences, University of South Africa

ABSTRACT

Rapid changes in highly competitive economic environments have created the need for sound financial management in organisations. In order to source sufficient numbers of skilled financial managers, specialised career guidance should be high on the agenda of educational and labour policy makers. While the chartered management accountant (CMA) enjoys international status, not many studies have been conducted to measure South African students' and accounting teachers' awareness of the CMA designation. This article reports on the results of first-year accounting students' perceptions of a career in management accounting as well as on the career guidance they received on how to become a CMA. It also reports on accounting teachers' awareness of the management accounting designation. This study found that first-year accounting students and accounting teachers do not possess sufficient knowledge of the career opportunities in the management accounting field and of the route to follow on how to become a CMA. Recommendations are made for tertiary institutions and professional bodies to alleviate this information gap by distributing brochures and posters to accounting and career guidance teachers and by providing information sessions to them as well as to first-year accounting students on career opportunities in the management accounting field.

Key words: management accounting, management accountant, chartered management accountant, management accounting career guidance

JEL: M490

Introduction

Career decisions are complicated and influenced by many determinants, including parental expectations, high earnings prospects, job-market considerations, perceived image of the profession and exposure to the subject field in high school. Although the number of enrolments at tertiary institutions has increased in the last decade, more graduates have become unemployed, suggesting that many graduates are not suitably qualified for the jobs that are available (Pauw, Oosthuizen & Van der Westhuizen, 2006:22). Owing to the fact that too many students are graduating in low employment areas, Pauw et al. (2006:22) suggest that guidance on study and career decisions is crucial and should be improved, especially at school level. Because there is a demand for qualified accountants in South Africa, career guidance pertaining to the various opportunities in this field should be up to standard. Students can, for instance, pursue a career as a chartered accountant (CA) and register with the South African Institute of Chartered Accountants (SAICA), from where they can either become an auditor or work as an accountant or financial manager in commerce and industry. They can, inter alia, also become a chartered management accountant (CMA) and register with the Chartered Institute of Management Accountants (CIMA) or they can become a professional accountant registered with the South African Institute of Professional Accountants (SAIPA).

Various international studies assessed the attractiveness of the accounting profession among students (Byrne, Willis & Burke, 2012; Chen, Jones & Mcintyre, 2008; Jackling & Keneley, 2009). According to Sugahara and Boland (2009:255), the number of tertiary students studying accounting as a degree major has dwindled worldwide. It is noted, for example, that the accounting profession in Malaysia is facing a major problem, namely to attract the 'best and brightest' students who have both ample accounting knowledge and strong communication, technical and analytical skills that are required in the increasingly complex business environment (Bolhan, Kassim, Jonathan & Atan, 2007:6-7). Research among first-year accounting students in South Africa (Myburgh, 2005:46; Van Zyl & De Villiers, 2011:68) concluded that respondents perceived, for instance, the difficulty of the accounting field, the cost and the number of years of study as constraints to pursue an accounting career. Since there is already a significant shortage of financial and accounting professionals in South Africa (Coetzee & Oberholzer, 2010) and of late fewer students elect to pursue an accounting career, it adds up to even fewer students majoring in management accounting or financial management. Burns, Hopper and Yazdifar (2004:3) support this view and point out that students are also less inclined to enrol for management accounting courses.

The evolving identity of management accountants (MAs) and their changing role in organisations call for a common understanding of the profession at occupational level (Ahrens & Chapman, 2000:479). To promote an MA profile and shape a professional brand, it is suggested in a CIMA research report that the current management accounting curriculum should be reviewed, MAs should demonstrate leadership and professional characteristics and become integrated into the business team (Kim, Hatcher & Newton, 2012:15). Even though professional management accounting bodies, such as CIMA in Britain and the Institute of Management Accountants (IMA) in the USA, as well as Management Accounting Departments at tertiary institutions, are continually constructing a common occupational identity for MAs, this study reveals that accounting teachers, school leavers and students do not necessarily possess this information.

Given the above background, the question arises as to how professional management accounting bodies and management accounting departments at tertiary educational institutions can recruit students to pursue a management accounting career. Before one can answer this question, the more significant question for this research project is whether accounting teachers and students have any knowledge of the MA designation.

The remainder of this article first delineates the objective of the study and the problem to be investigated. Secondly, a literature review examines prior studies conducted on the factors influencing accounting students' career choices, with specific reference to management accounting. Thirdly, the research methodology is described, followed by a discussion of the results. Finally, conclusions are drawn and recommendations made for further research.

2 Objective of the study and problem investigated

According to Maringe (2006:476-477), workplace career development places a great deal of emphasis on specialisation, and students select subjects that will ensure employment success. Taking into account the variety of management and accounting qualifications offered by universities, colleges and professional institutions, it became a problem finding a balance between the supply and demand of quality management accounting students. Many school leavers and students experience huge uncertainty and confusion when making a career choice and consider themselves to be a failure if they decide to change their field of study while studying (Bolhan et al., 2007:2).

The objective of this study is to determine empirically whether first-year accounting students have been introduced to the possibility of pursuing a management accounting career as opposed to becoming a CA, and if so, how they became aware of this. Subsequently the aim is also to determine if students are aware of the route they need to follow in order to qualify as a CMA.

Because students' perceptions of the profession are shaped during their final school years, it is crucial to also determine whether accounting teachers are equipped to enlighten school leavers about the career opportunities in the management accounting field. The purpose is therefore to interview accounting teachers and to determine if they believe that professional bodies, tertiary educational institutions and career guidance at school level can play a more active role in promoting the management accounting discipline.

Owing to the paucity of research on the management accounting career choice of school leavers and students, the theoretical framework for this study will include studies based on factors influencing students' choice to pursue a general accounting career.

3 Literature review

Unemployment in South Africa is a serious concern, even among graduates. Research has shown that inappropriate institutional and subject choices and poor career advice are some of the factors behind graduate unemployment (Kraak, 2010:85). The Organisation for Economic Co-operation and Development (OECD) and the World Bank conducted three overlapping reviews of national career guidance policies among 37 countries, including South Africa. In these reviews, the term 'career guidance' was defined as 'services intended to assist individuals, of any age and at any point throughout their lives, to make educational, training and occupational choices and to manage their careers' (Watts & Sultana, 2004:107). The review of the middle-income countries, which includes South Africa, found that these countries generally have less well-developed career guidance systems than high-income countries (Watts & Sultana, 2004:108). However, from these reviews it is evident that all countries need to expand access to career guidance in order to make it available, not only to selected groups like school leavers, but also to everyone throughout their lives. In this way, career guidance has the potential to contribute to national policies for the development of human capital (Watts & Sultana, 2004:110).

Factors influencing career choice can be widely classified as intrinsic (job satisfaction, personal interest and aspirations), extrinsic (availability of work, status and remuneration) and interpersonal factors (influence of parents, teachers and other roleplayers) (Agarwala, 2008:364; Ahmed, Alam & Alam, 1997:326327). A study among business students in 40 universities in the USA indicated that students majoring in accounting, ranked 'interested in this type of work', 'good job opportunities' and 'good fit with my abilities' as the three main reasons for choosing a business degree (Kim, Markham & Cangelosi, 2002:30). This study also revealed that career success depends on how well accounting students understand their major (Kim et al., 2002:31). It is therefore critical that in order to promote management accounting as students' business major, tertiary institutions should explore various ways of informing school leavers or first-year business students of the content of the management accounting syllabus, the job opportunities and the personal aptitudes required to become a management accountant.

A potential problem for recruitment into the accounting profession is the ensconced perception that accountants are dull and dreary (Jeacle, 2008:1296-1297). According to Jackling (2002: 66, 77) students' perceptions of the role of accountants are not aligned with the objectives of the profession and should be changed through marketing by professional bodies, career advice, and secondary and tertiary accounting curricula. Coetzee and Oberholzer (2010:458) contend that teachers' misunderstanding of the nature and importance of a career in accounting could contribute to students being misinformed about the profession.

In order to trace the reasons for embarking on training as MAs, Ahrens and Chapman (2000) interviewed 64 MAs from 12 British and 17 German firms. In most instances, the British interviewees offered purely pragmatic reasons for becoming MAs. These included reasons relating to the fact that there are relatively well-paid jobs in the field and that future promotion prospects are good. Although the German interviewees also emphasised pragmatic factors, they mostly regarded management accounting as an attractive option to develop an occupational identity and to fulfil various possible functions in an organisation (Ahrens & Chapman 2000:484-486).

Although the CA profession in South Africa places considerable emphasis on management accounting and financial management training, especially for those who follow the route to train outside public practice (in commerce and industry-TOPP programme) (Barac 2009:8890), little research has been conducted in South Africa on students' awareness of the different entry routes into the MA profession. One option is to follow the TOPP programme as part of the CA route and then work as a management accountant in commerce and industry, without necessarily registering as a chartered or certified management accountant (CMA). To clarify, CIMA refers to its qualified members as 'chartered management accountants', while IMA uses the term 'certified management accountant'. As a rule, students first obtain a relevant accredited degree and/or postgraduate degree, after which they may follow various gateway routes to become a CMA.

Of late, the prestigious American Institute of Certified Public Accountants (AICPA) and CIMA have formed a joint venture to establish the Chartered Global Management Accountant (CGMA) designation. The CGMA label now elevates the management accountancy profession to one of the most respected and recognised international MA designations (CIMA 2011). Against this background, this study endeavours to establish just how recognised and well known the management accounting profession is among a subsection of South African accounting teachers and first-year accounting students.

4 Research methodology

A concurrent mixed-method research study was conducted, collecting quantitative and qualitative data by means of questionnaires and interviews respectively. This concurrent mixed-method approach converges the qualitative and quantitative data in order to triangulate data sources and ensure a comprehensive analysis of the research problem (Creswell, 2011:15-16).

4.1 Questionnaire

A questionnaire aimed at first-year accounting students at both the University of South Africa (Unisa) and the University of Pretoria (UP) investigated students' perceptions and knowledge of a prospective career in management accounting. A pilot study was conducted to test the content, user-friendliness and time taken to complete the questionnaire. The questionnaire was presented to the Unisa students as a web-based Lime survey soon after registrations for the first semester had closed. Although the questionnaire consisted of a number of different sections, only those sections relevant to this paper will be discussed.

Section A of the questionnaire was used to determine the students' demographic background with regard to the Institution (Unisa or UP) they attend, their gender, age and language of learning. The purpose of section B was to ascertain whether they were aware of the fact that they could become a CA and/or a CMA. If they were aware that they could become a CMA, they had to indicate how they had obtained this knowledge. They were also asked if they were considering becoming an MA. In the last section of the questionnaire, the respondents rated on a five-point Likert scale the extent to which they agreed with the given statements on the route to follow in order to qualify as a CMA.

The Unisa students were invited by email to complete the questionnaire and submit it to the dedicated uniform reference locator (URL) hosted on the Unisa ICT server. The questionnaire was sent to all students (14 522) with email addresses registered for the FAC 1502 accounting module. A reminder was sent to students after two weeks, and on the due date, 899 completed questionnaires had been submitted, of which 724 were considered valid. The UP Accounting I students completed the exact same questionnaire on campus during their first week of class. Questionnaires were handed out to 1000 students who attended the Accounting I lectures during their first week of enrolment and 798 questionnaires were completed, of which 757 were valid. A high response rate (79.8 per cent) was achieved because lecturers in the various classes helped to administer the questionnaires. The Unisa sample was elevated with a weight of 15.18 to ensure a correct proportional presentation in the sample that correlates with the population proportions (see Table 1). When population subgroups are sampled with unequal probability it is in some instances necessary to give them correspondingly unequal weights to compensate for bias due to difference in response rates across population subgroups (Kish 1990; Lumley 2004:2; Pike 2008:154). According to Vaske, Jacobs, Sijtsma and Beaman (2011:210), weighting strategies are commonly used to compensate for sampling issues, especially where internet surveys are concerned.

First-year students registered for the first semester were chosen for the quantitative survey because they could still reflect on the career guidance received before entering a tertiary educational institution. Accounting students were chosen because they had already demonstrated a preference to pursue a career in a financial discipline.

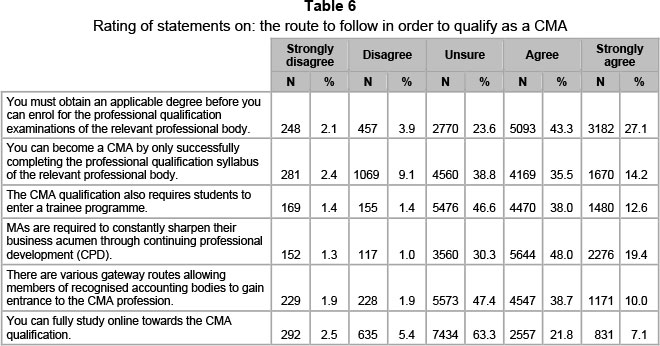

Reliability in quantitative research encompasses the consistency of a set of measurements of a measuring instrument. The Cronbach alpha value was used as a measure of the reliability of the items measuring the construct on 'the route to follow in order to qualify as a CMA' (see Table 2). The individual six statements that were grouped together in order to measure this particular construct (route to follow) are depicted in Table 6.

From Table 2 it is evident that the Cronbach alpha was between 0.60 and 0.95 overall, which falls within the accepted level of reliability (Tredoux & Durrheim, 2002:216). It also indicated that the individual items pertaining to the route to follow in order to qualify as a CMA, measured the same concept in the same manner.

4.2 Interviews

Semistructured interviews were conducted with Grade 11 and 12 accounting teachers in the Tshwane South District of the Gauteng province. The researcher needed to select interviewees who could enlighten the issue under investigation (Henning, Van Rensburg & Smit, 2004:71). Based on the researcher's judgement and advice from the Senior Education Specialist for Accounting in the Tshwane South District, nonprobability purposive sampling was used to interview a sufficient number of accounting teachers from eight schools in the Tshwane South District. Purposive sampling refers to a sample based on the judgement of the researcher and encompassing typical attributes or characteristics of the population (De Vos et al., 2005:202). This sampling method is also useful for the purpose of triangulation (Sandelowski, 2000: 248). These interviews were conducted at the schools and knowledge of management accounting was not a prerequisite. To include different socioeconomic population groups, the site sample consisted of independent (private) schools as well as public schools. The public schools included former model C schools, a school in the Pretoria CBD and township schools. Two accounting teachers per school were interviewed, except for one independent school that had only one accounting teacher, resulting in 15 interviewees. Since data saturation was achieved, these interviewees were found to be sufficient. According to De Vos et al. (2005:294), data saturation is reached when the researcher begins to hear the same information repeatedly and learns nothing new.

Operational measures to ensure trustworthiness, as demonstrated by Lincoln and Guba's (1985) seminal work, included the following:

- Credibility

All the interviews were conducted by the primary researcher with previous interview experience. The researcher built trust by honouring anonymity, honesty and openness during the interview. By conducting the interviews at a place and time of the interviewees' convenience, prolonged engagement was achieved which enhanced the trust relationship between the parties (Shenton, 2004:65). The same questions were put to all the interviewees, who provided informed written consent. This consent form acknowledged that participants' rights have been protected during the interview process and that they could withdraw at any time (Creswell, 2003:73).

- Transferability

Although the respondents came from different demographic backgrounds and worked with learners from various demographic groups, they were representative of the phenomenon under study (Krefting, 1991:220; Sandelowski, 2000:248). Transferability was thus achieved through purposive sampling and by conducting the same interview methods in different school environments (Shenton, 2004:70). The interviews were professionally transcribed and the results were discussed and substantiated with direct quotations from the interviewees.

- Dependability

All aspects of the research were fully described, including the methodology, sampling process and data analysis. The process was thus clearly documented. A code-recode procedure was followed to increase the dependability of the study (Krefting, 1991:221). The same themes occurred in each of the interview questions when the data was recoded after two weeks.

- Authenticity

Specific groups were not excluded from the project based on race, sex or any other social or financial criteria.

Ethical clearance for the questionnaire and interviews was granted by the CEMS Ethics committee and the Unisa Senate Research and Innovation Committee (SENRIC). Permission to conduct the survey and interviews was obtained from the following institutions:

- Unisa: Director of the School for Accounting Sciences (2012), Prof C Cronje and SENRIC

- UP: Head of Department, Accounting and CA Programme Manager, Prof JGI Oberholster and the Registrar, Prof NJ Grove

- Gauteng province, Department of Education.

5 Results and discussion

The quantitative and qualitative results will be discussed independently before any conclusions are drawn.

5.1 Questionnaire results

- Descriptive results

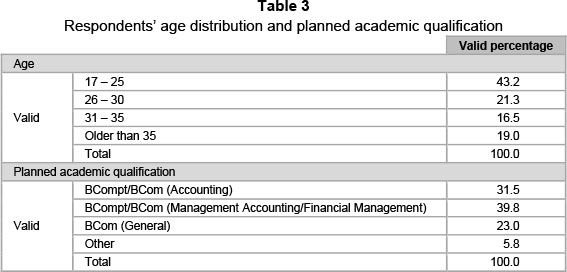

Based on the fact that the Unisa sample was elevated to the weight depicted in Table 1, the demographics of both the Unisa and UP students who participated in the survey revealed that 58.9 per cent were female and 41.1 per cent male. An overwhelming percentage of respondents indicated their language of learning as English (92.4 per cent), followed by Afrikaans (6.9 per cent), an African language (0.7 per cent) and other (0.1 per cent). Table 3 shows the respondents' age distribution and their planned academic qualification.

Students were also asked if they were aware of the fact that they can become a CA or a CMA and if they received any career guidance while at school on how to qualify as either a CA or a CMA (see Table 4).

Although Table 3 shows that only 31.5 per cent of the respondents indicated that they had planned to study BCom/BCompt (Accounting), Table 4 shows that 65.9 per cent of them indicated that they had been aware of the fact that they could become a CA before entering tertiary education and 26.5 per cent revealed that they had received career guidance on how to qualify as a CA. However, while 39.8 per cent of the respondents (see Table 3) indicated that they had planned to study BCom/BCompt Management Accounting/Financial Management, Table 4 shows that 39.7 per cent had been aware of the fact that they could become a CMA, but only 10.0 per cent had received career guidance at school on how to qualify as a CMA.

Table 5 indicates how those respondents who were aware of the fact that they could become a CMA had obtained this information.

From Table 5 it is clear that career guidance teachers (9.5 per cent) were either non-existent in most schools or did not play a major role in advising students that they could become CMAs. It is also evident that accounting teachers (18.1 per cent) played a prominent role in advising prospective accounting students on becoming a CMA. Although not specifically applicable to CMAs, these results concur with the findings of Myburgh (2005), namely that performance in Accounting at school and the influence of school teachers were important factors that influenced students to become CAs. Although respondents could specify any other source of information on how to become a CMA, no one indicated visits by tertiary educational institutions or any other source not included in the list (see Table 5).

Table 6 shows how students rated the extent to which they agreed with statements on the route they had to follow to qualify as a CMA.

Although 70.4 per cent of the students agreed (see Table 6) that one must obtain an applicable degree before one can enrol for the professional qualification examinations of the relevant professional body, only 49.7 per cent agreed that one can become a CMA only by successfully completing the professional qualification syllabus of the relevant professional body. Students who take the CIMA route can become a CMA without having obtained a degree or any other qualification prior to entering their programme (CIMA 2013; Cory & Huttenhoff, 2011:3). However, IMA requires students to first obtain an accredited bachelor's degree.

From Table 6 it is evident that 50.6 per cent of the students agreed that the CMA qualification also requires students to enter a trainee programme. It is important to note that both CIMA and IMA require three and two years respectively of continuous professional experience in management accounting or financial management. Of the respondents, 67.4 per cent agreed that management accountants have to engage in continuing professional development (CPD) programmes. Both CIMA and IMA offer CPD programmes and expect qualified CMAs to stay abreast of new developments.

Although 48.7 per cent of respondents (see Table 6) agreed that there are various gateway routes to the MA profession, 47.4 per cent of them were unsure. By the same token, only 28.9 per cent of the students agreed and strongly agreed that they could fully study online towards the CMA qualification, while 63.3 per cent were unsure. Notably, CIMA offers fully online study programmes from their entry-level Certificate programme to their Test of Professional Competence in Management Accounting (TOPCIMA) case study examination (CIMA 2013). IMA also offers online courses with interactive study material, but their gateway route requires a bachelor's degree before entering the programme.

- Inferential results

A Pearson chi-square test was conducted to examine whether there was a relationship between two nominal variables, posted as statements or questions in the questionnaire (see Table 7) and to test for independence of association. Only those variables with a significant relationship (p<0.05) prior to and after the weighting of the data will be discussed in Table 7.

From the first association depicted in Table 7, only 21.2 per cent of those respondents who were aware of the fact that they could become a CMA, had received any career guidance on how to qualify as a CMA while at school. Notably, the majority of students (88.6 per cent) who had received career guidance on how to qualify as a CMA, indicated English as their language of learning. Furthermore, an equitable 65.7 per cent of those respondents, who had received any career guidance on how to qualify as a CMA, had considered becoming one. From Table 7, it became evident that only 39.2 per cent of those who were aware that they could become a CMA had actually planned to study BCompt/BCom (Management Accounting/Financial Management). The last association in Table 7 revealed that 57.0 per cent of those respondents who received career guidance while at school on how to qualify as a CMA were between the ages of 17-25, whereas 15.7 per cent were between the ages of 26 and 30 years and 27.4 per cent were older than 30 years.

As indicated in tables 6 and 7, there is an apparent lack of career guidance at school level on how to become a CMA. If 65.7 per cent of those who had received career guidance while at school on how to qualify as a CMA considered becoming one, it is questionable why only 39.2 per cent had currently planned to study the applicable BCompt/Bcom Management Accounting degree. Interviews with accounting teachers provided some answers to these and other questions.

5.2 Interview results

In order to determine whether accounting teachers are equipped to enlighten school leavers on the career opportunities in the management accounting field and the route to follow towards becoming a CMA, data were interpreted according to the following themes that emerged during the interviews and then cumulated in a theory on accounting teachers' ability to provide guidance to school leavers on a career in management accounting:

1 Participants ' knowledge of the career opportunities in the management accounting field.

Two of the interviewees reflected that an MA would do human resource management, one interviewee said that they manage information systems and another that they analyse financial statements. One of them specifically mentioned that MAs work with budgets and projected income statements, while another mentioned that they can be financial advisors. Although some of the interviewees indicated that MAs are involved in decision-making activities, two interviewees said that they had no idea what MAs do. The verbatim comment of one respondent clearly highlights this: 'I honestly have no idea. Management accounting would entail what? I don't even know what the management accounting umbrella would cover.'

2 Participant's opinion of the role played by professional bodies, such as CIMA, to promote their profession among school leavers.

Some interviewees remarked that they knew a little about SAICA and SAIPA, albeit more about SAIPA because it sponsors the Accounting Olympiad. However, the majority of interviewees had never heard of CIMA and pointed out that members of the institution should visit schools and explain what the institution stands for and what MAs do. Workshops by PriceWaterhouse Coopers (PWC) were mentioned by more than one teacher as the only contact with the accounting profession. They also expressed a need for brochures or posters to display in their classes and that the educators should at least obtain the necessary information to be able to impart such knowledge to their learners. One interviewee contended that 'these institutions can play a more vital role in our institutions, especially in our township schools where knowledge, rather information, is coming in drips and drabs'.

3 Participants ' view of the role played by tertiary institutions to promote the management accounting discipline among school leavers.

All the interviewees arrived at a similar conclusion that tertiary institutions need to visit schools and inform both the learners and the teachers of the different career opportunities in the accounting field. They reflected that there is currently no contact and that they would welcome lecturers or even students in the management accounting field visiting schools and explaining to learners what MAs do and the possible career opportunities for qualified MAs. Some even mentioned that learners should be informed before they make their final subject choice during their Grade 9 year. One interviewee also mentioned that the number of accounting learners is declining and one should therefore motivate them to take accounting as a subject from Grade 10 onwards. Although some acknowledged that it would be impractical to visit all the schools, they still felt strongly that the learners would benefit from face-to-face contact with lecturers or students. Information workshops with accounting teachers were suggested as a more practical possibility to disseminate information at schools.

4 Participants ' perception of the route that students need to follow in order to qualify as a CMA.

Although the interviewees generally indicated that they were not familiar with the route, the majority of them said that students would at least have to do a BCom in order to become an MA. Only one suggested that they would do a BCom specialising in management accounting. Although some interviewees stated that students would have to do honours, it became clear that they were unaware of the fact that certain universities, such as Unisa, are now offering postgraduate diplomas and that these diplomas are at the same level as an honours degree. However, it was evident that all the interviewees had a more informed idea on how to become a CA, as opposed to the route to follow on how to become a CMA.

5 Participants ' view of time spent on career guidance at school level.

The overall response was that more time should be spent on career guidance at school. One interviewee exclaimed: 'Yes, definitely because there is actually no career guidance here!' Interviewees from one private school and one former model C school stated that they did have adequate career guidance teachers, but admitted that they were not sure if these teachers were knowledgeable about the management accounting designation. One interviewee suggested that the subject teachers should do research on the careers pertaining to their subject in order to inform and motivate students about the various opportunities in the specific field. It was also mentioned that career guidance should start from Grades 8 and 9, instead of in Grades 11 and 12.

The literature recognises the fact that top-quality career information and some form of personal support are essential for satisfactory career guidance and effective career decision making (Watts & Sultana, 2004:114-115). However, a bleak picture of management accounting career guidance emerged from the interviews, as discussed above. In theory, although some of the accounting teachers who participated in the survey mentioned one or two career opportunities, they were mostly uninformed of the career prospects in the management accounting field. They generally expressed a need for professional bodies and tertiary institutions to play a more active role in promoting the management accounting designation at schools. Regarding the route that students need to follow to qualify as a CMA, most interviewees posited that students would have to enrol for a BCom degree. Except for one interviewee, they did not specify the specialisation field for the BCom degree or the postgraduate qualifications that students should attain; nor did they indicate that students could study directly through CIMA without first obtaining a degree. Interviewees reiterated that more time should be spent on career guidance at school level, especially before choosing their final subjects.

6 Conclusions

The literature review underscored the importance of career guidance for students, but specifically for school leavers. According to Kraak (2010:100), in order to overcome the problem of increasing graduate unemployment, the South African government needs to look at several labour market policy interventions with clear structured pathways into work. Hence focused career guidance is necessary to ensure the availability of skills relevant to the business world. Because of the diverse roles played by MAs in organisations and the different routes that students can follow in order to become a CMA, the South African youth should be informed about this. Job opportunities for management accountants in organisations are increasing and there seems to be a need for graduates specialising in this field.

Based on the perceptions of students who completed the questionnaire, it can be deduced that although many students were aware that they could become a CA, not many of them were aware of the fact that they could become a CMA and even fewer had received any career guidance on how to qualify as one. Evidently, only a small percentage of the respondents had received advice from career guidance teachers on the CMA designation, although accounting teachers had played a more significant role in informing them about the CMA designation. Most of the responding students lacked information on the various entry routes into the profession as well as the prerequisites to register as a CMA.

Regarding the noteworthy role of accounting teachers in informing school leavers of career opportunities in the accounting field, it is imperative that these teachers are informed of the career opportunities for MAs and their role in organisations as well as the route they need to take in order to qualify as one. However, in the interviews it became evident that accounting teachers are not as informed on the career possibilities in the MA field as in the CA field.

The findings of this study could have implications for promoting vocational guidance and counselling among school leavers and students aspiring to a career in management accounting. It could also have significant implications for the recruitment strategies of management accounting faculties at tertiary educational institutions and the applicable professional bodies.

7 Recommendations and limitations

This study suggests that professional bodies such as CIMA and tertiary institutions need to consider innovative ways for promoting the management accounting profession to the recruitment market, specifically school leavers and first-year accounting students. Brochures explaining the international status, career opportunities, entry routes and prerequisites for qualifying as a CMA could be distributed to career guidance teachers, accounting teachers, school leavers and first-year accounting students. Social media could be used to promote the profession and discussion forums with qualified CMAs could inspire prospective management accounting students. Accounting teachers can be invited to tertiary institutions for workshops or information sessions on the career opportunities for their students and the routes they could follow in order to qualify as CMAs.

The fact that this study did not also include interviews with career guidance teachers appears to be a limitation, but it is also an opportunity for further research. Only three out of the eight schools represented in the interviews had dedicated career guidance teachers. It might be informative to assess the knowledge they have of the management accounting profession. Future research could also involve administering a questionnaire to champions of industry on their perceptions of the career opportunities of MAs in their organisations.

Since accounting students from only two South African universities were surveyed and only accounting teachers in the Tshwane South District were interviewed, sample bias can be seen as a limitation of this study. Therefore the results of this study cannot be used to make generalised assumptions about all first-year accounting students and all the accounting teachers in the country. However, the data gathered in this study provide insight into students from diverse backgrounds in a residential and an open distance learning institution, as well as teachers from both private and public schools.

References

AGARWALA, T. 2008. Factors influencing career choice of management students in India. Career Development International, 13(4):362-376. [ Links ]

AHMED, K., ALAM, K.F. & ALAM, M. 1997. An empirical study of factors affecting accounting students' career choice in New Zealand. Accounting Education: An International Journal, 6(4):325-335. [ Links ]

AHRENS, T. & CHAPMAN, C.S. 2000. Occupational identity of management accountants in Britain and Germany. The European Accounting Review, 9(4):477-498. [ Links ]

BARAC, K. 2009. Management accounting and financial management knowledge requirements for South African entry-level trainee accountants. South African Journal of Accounting Research, 23(1):87-111. [ Links ]

BOLHAN, D.R.H.J.A., KASSIM, H.J., JONATHAN, L. & ATAN, P. 2007. Is accounting profession the right career choice? A case of first-year accounting students in Universiti Teknologi Mara Sarawak. 5 December, Universiti Teknologi Mara (UiTM). [ Links ]

BURNS, J., HOPPER, T. & YAZDIFAR, H. 2004. Management accounting education and training: putting management in and taking accounting out. Qualitative Research in Accounting and Management, 1(1):1-29. [ Links ]

BYRNE, M., WILLIS, P. & BURKE, J. 2012. Influences on school leavers' career decisions: implications for the accounting profession. The International Journal ofManagement Education, 10:101-111. [ Links ]

CHARTERED INSTITUTE OF MANAGEMENT ACCOUNTANTS. 2013. Management Accounting: a career advantage. Available at: http://www.cimaglobal.com/entryroutes [accessed 2013-02-01]. [ Links ]

CHARTERED INSTITUTE OF MANAGEMENT ACCOUNTANTS. 2011. How management accounting drives sustainable success. London: CIMA. [ Links ]

CHEN, C., JONES, K.T. & MCINTYRE, D.D. 2008. Analyzing the factors relevant to students' estimations of the benefits and costs of pursuing an accounting career. Accounting Education: An International Journal, 17(3):313-326. [ Links ]

CIMA, vide Chartered Institute of Management Accountants. [ Links ]

COETZEE, S. & OBERHOLZER, R. 2010. South African career guidance counsellors' and mathematics teachers' perception of the accounting profession. Accounting Education: An International Journal, 19(5):457-472. [ Links ]

CORY, S. & HUTTENHOFF, T. 2011. Perspectives of non-public accountants about accounting education and certifications: an exploratory investigation. Journal of Finance and Accountancy. Available at: http://aabri.com/manuscripts/10688.pdf [accessed on 2013-03-19]. [ Links ]

CRESWELL, J.W. 2003. Research design: qualitative, quantitative and mixed methods approaches. London: Sage. [ Links ]

CRESWELL, J.W. 2011. Research design: qualitative, quantitative, and mixed methods approaches (2n ed.) London: Sage. [ Links ]

DE VOS, A.S., STRYDOM, H., FOUCHE, C.B. & DELPORT, C.S.L. 2005. Research at grass roots for the social sciences and human service professions (3rd ed.) Pretoria: Van Schaik. [ Links ]

HENNING, E., VAN RENSBURG, W. & SMIT, B. 2004. Finding your way in qualitative research. Pretoria: Van Schaik. [ Links ]

JACKLING, B & KENELEY, M. 2009. Influences on the supply of accounting graduates in Australia: a focus on international students. Accounting and Finance, 49:141-159. [ Links ]

JACKLING, B. 2002. Are negative perceptions of the accounting profession perpetuated by the introductory accounting course? - an Australian study. Asian Review of Accounting, 10(2):62-80. [ Links ]

JEACLE, I. 2008. Beyond the boring grey: the construction of the colourful accountant. Critical Perspectives on Accounting, 19:1296-1320. [ Links ]

KIM, D., MARKHAM, F.S. & CANGELOSi J.D. 2002. Why students pursue the business degree: a comparison of business majors across universities. Journal of Education for Business, 78(1):28-32. [ Links ]

KIM, J., HATCHER, C. & NEWTON, C. 2012. Professional identity of management accountants: leadership in changing environments. Research executive summary series, 8(1). London: Chartered Institute of Management Accountants. [ Links ]

KISH, L. 1990. Weighting: Why, when, and how? In Proceedings of the Survey Research Methods Section, 121-130, Alexandria, VA. [ Links ]

KRAAK, A. 2010. The collapse of the graduate labour market in South Africa: evidence from recent studies. Research in Post-Compulsory Education, 15(1):81-102. [ Links ]

KREFTING, L. 1991. Rigor in qualitative research: the assessment of trustworthiness. The American Journal of Occupational Therapy, 45(3):214-222. [ Links ]

LINCOLN, Y.S. & GUBA, E. 1985. Naturalistic Inquiry. Beverly Hills, CA: Sage. [ Links ]

LUMLEY, T. 2004. Analysis of complex survey samples. April 15, University of Washington: Washington. [ Links ] MARINGE, F. 2006. University and course choice: implications for positioning, recruitment and marketing. International Journal of Educational Management, 20(6):466-479. [ Links ]

MYBURGH, J.E. 2005. An empirical analysis of career choice factors that influence first-year accounting students at the University of Pretoria: a cross-racial study. Meditari Accounting Research, 13(2):35-48. [ Links ]

PAUW, K., OOSTHUIZEN, M. & VAN DER WESTHUIZEN, C. 2006. Graduate unemployment in the face of skills shortages: a labour market paradox. Accelerated and Shared Growth in South Africa: Determinants, Constraints and Opportunities Conference. The Birchwood Hotel and Conference Centre, Johannesburg: 18-20 October. [ Links ]

PIKE, G.R. 2008. Using weighting adjustments to compensate for survey nonresponse. Research in Higher Education, 49:153-171. [ Links ]

SANDELOWSKI, M. 2000. Focus on research methods: combining qualitative and quantitative sampling, data collection, and analysis techniques in mixed-method studies. Research in Nursing & Health, 23:246-255. [ Links ]

SHENTON, A.K. 2004. Strategies for ensuring trustworthiness in qualitative research projects. Education for Information, 22:63-75. [ Links ]

SUGAHARA, S. & BOLAND, G. 2009. The accounting profession as a career choice for tertiary business students in Japan: a factor analysis. Accounting Education: An International Journal, 18(3):255-272. [ Links ]

TREDOUX, C. & DURRHEIM, K. 2002. Numbers, hypotheses and conclusions: a course in statistics for the social sciences. Cape Town: UCT Press. [ Links ]

VAN ZYL, C. & DE VILLIERS, C. 2011. Why some students choose to become chartered accountants (and others do not). Meditari Accountancy Research, 19(1/2):56-74. [ Links ]

VASKE, J.J., JACOBS, M.H., SIJTSMA, M.T.J. & BEAMAN, J. 2011. Can weighting compensate for sampling issues in internet surveys? Human Dimensions of Wildlife, 16:200-215. [ Links ]

WATTS, A.G. & SULTANA, R.G. 2004. Career guidance policies in 37 countries: contrasts and common themes. International Journal for Educational and Vocational Guidance, 4:105-122. [ Links ]

Accepted: January 2014

{kind=link}

{kind=link}