Serviços Personalizados

Artigo

Inglês (pdf)

Inglês (pdf)

Artigo em XML

Artigo em XML Referências do artigo

Referências do artigo

Indicadores

Links relacionados

-

Citado por Google

Citado por Google -

Similares em Google

Similares em Google

Compartilhar

Permalink

PermalinkSouth African Journal of Economic and Management Sciences

versão On-line ISSN 2222-3436

versão impressa ISSN 1015-8812

S. Afr. j. econ. manag. sci. vol.16 no.2 Pretoria Jan. 2013

ARTICLES

Performance satisfaction, shareholder and stakeholder orientations: managers' perceptions in three countries across continents

Georgios Angelopoulos; John A Parnell; Gregory J Scott

CENTRUM Católica, Pontificia Universidad Católica del Perú

ABSTRACT

Managers working in South Africa, Peru and the United States were classified as stakeholder- and/or shareholder-oriented along the Perceived Role of Ethics and Social Responsibility (PRESOR) scale. The relationship between stakeholder/shareholder orientation and perceptions of organisational performance was further explored. In South Africa and overall, respondents with both high stakeholder and low shareholder orientations reported the greatest performance satisfaction. In Peru, managers with a high stakeholder orientation reported the greatest satisfaction with organisational performance. A significant link between stakeholder or shareholder orientation and performance satisfaction was not found in the United States, however. Directions for future research are outlined.

Key words: PRESOR, shareholder, stakeholder, stockholder, ethics, corporate social responsibility, Peru, South Africa, United States

1 Introduction

Increased globalisation in recent years has led to considerable discussion and debate regarding the fundamental purpose of the modern firm and the requirements for managerial success in today's business environment (Handy, 2002; Pienaar, 2010; Scherer, Palazzo & Matten, 2009; Sen, 2009). Essentially two distinct perspectives have emerged on the nature of the pursuit of sustainable high firm performance. These perspectives constitute what is commonly viewed as two competing viewpoints, the stakeholder and shareholder perspectives on firm governance (Crilly, 2011; Garcia-Castro, Arino & Canela, 2011). Proponents of the shareholder or shareholder primacy view argue that aside from ethical obligations-engaging in moral and legal transactions-firms should be managed in the sole interest of their shareholders or owners, and to that end seek to maximise profits. Firms are best equipped to serve their interests and ultimately those of society by meeting the demand for goods and services in such a way that they maximise both financial returns and client satisfaction in the process. Business organisations should engage in social endeavours only to the extent that in doing so they enhance the prospects of higher short- or long-term financial returns. Social considerations not linked to shareholder considerations are seen as matters of personal initiative, private charities and foundations, or the responsibility of government. As con-ceptuallised in this paper and in others, we refer to this as the shareholder or shareholder primacy view (see Prahalad, 1994; Armour, Deakin & Konzelmann, 2003; Rodin, 2005; Reberioux, 2007; Schwartz, 2007; Keay, 2008), but it may also be termed the stockholder view (see Freeman & Reed, 1983; Bierema & D'Abundo, 2004; Charron, 2007; Dias & Goncalves, 2007; Strine, 2008; Matwijkiw & Matwijkiw, 2010).

Proponents of the stakeholder view focus on a different set of priorities. They recognise the growing influence of individuals and entities that are directly affected by a firm's actions- employees, governments, suppliers, distributers, clients, consumers and others-and suggest that business success has evolved to include more than just traditional objectives like profit maximisation, but other concerns such as environmental sustainability as well (Goodpaster, 1993; Kay & Popkin, 1998; Moura-Leite, Padgett & Galan, 2011; Orlitzky, Siegel & Waldman, 2011). Proponents of the stakeholder perspective argue that this evolution is substantial, to the extent that financial returns are often tied directly to the social and sustainability concerns inherent in the perspective (Schwalb, Ortega, García & Soldevilla, 2003; Schwalb, García & Soldevilla, 2005; Flores & Ickis, 2007; Gil, 2009). Given recent attention to factors such as carbon emissions, energy prices and increased public pressure for greater corporate transparency and consultation, business success would depend on a firm's ability to satisfy the needs of an array of stakeholders other than shareholders alone. As such, the modern business enterprise should develop partnerships with a broader range of relevant stakeholders to achieve and sustain the highest financial performance possible for shareholders, and in so doing address the needs of a much broader group of constituents on whom the firm's continued success depends as well.

Efforts to link or debunk notions of managerial ethics and social responsibility with organisational performance have been pervasive over the past few decades (Quinn & Rohrbaugh, 1983; Zahra & LaTour, 1987; Vitell & Hunt, 1990; Aquilar, 1994; GarciaCastro et al., 2011). Different measurement tools have been developed that help contribute to our understanding of the relationship between performance and the ethical and social responsibility orientations of organisational decision makers (Singhapakdi, Vitell, Rallapalli & Kraft, 1996). Most have been developed in western industrialised countries, and the majority of these in the United States. While substantial progress has been made in that regard, competing conceptualisations of and measurement schemes for ethics, social responsibility, and performance have heightened the challenge (Shafer, Fukukawa & Lee, 2007; Vitell, Ramos & Nishihara, 2010).

However, there remains a dearth of published work assessing ethical orientations and their prospective links with organisational performance in the developing world (Robertson, Olson, Gilley & Bao, 2007). Several cross-cultural applications of specific measurement tools such as those of Axinn, Blair, Heorhiadi and Thach (2004), Vitell and Paolillo (2004), Shafer et al. (2007) and Vitell et al. (2010) have been conducted, but additional work is needed. This study explores the interrelated perceptions of business performance, ethics and corporate social responsibility (CSR) in a comparative, cross-continental study of South Africa, Peru and the United States. More specifically, this study seeks to determine whether managers in these disparate nations hold similar or contrasting views on the importance of stakeholder and shareholder considerations with regard to their decision-making, and to gain insights into managers' appreciation of the relative importance of shareholder and stakeholder well-being in defining organisational success.

2 Global and country contexts

The overwhelming majority of scholarly work on ethics and CSR focuses on developed western societies, particularly the United States. Given the long history of CSR in the United States (Bowen, 1953) and its growing importance among United States multinational firms (e.g. Porter & Kramer, 2002) one would expect American preference for a stakeholder orientation. Nonetheless, the United States has also had noteworthy advocates (Friedman, 1993) and more recent proponents (Karnani, 2011) of the shareholder perspective. In practice, United States corporations and their chief executives offer many examples of both points of view, from the days of Hewlett Packard (Handy, 2002) to the recent period of Wall Street excess (Kliksberg, 2009).

Interest in the interaction between CSR and entrepreneurial activity outside North America and Europe has increased recently (Lenartowicz & Johnson, 2003; Belausteguigoitia & Portilla, 2004; Jain & Pisani, 2008; Parnell, 2008), in large part because of four developments. The first was the publication of the Brundtland Report, titled 'Our Common Future' in 1987 (WCED, 1987). The report highlighted the importance of focusing global attention on the needs of the poor in developing countries and calling for a more inclusive notion of economic development. Furthermore, it christened the notion of sustainable development in which the needs of the future were not to be compromised in meeting the needs of the present, and put the concept of intergenerational equity on the agenda of governments and multinational companies in industrialised and developing countries.

Second, the United Nations Development Program's 1992 global conference on the environment in Rio de Janeiro led to the launch of World Earth Day, which raised global awareness of environmental protection. In business circles this increased an awareness of the link between a sustainable environment and sustainable business.

Third, many nations in Africa, Asia and Latin America adopted policies to reduce the size and influence of the public sector, ceding greater influence to private firms through programs of privatisation, liberalisation of domestic markets and free trade agreements (Robles, Simon & Haar, 2003; Casanova, 2005).

At the same time governments' and civil society's expectations of the private sector's contribution to economic growth and social progress took on greater importance (Reficco & Ogliastri, 2009).

Fourth, many businesses operating in developing countries saw their growth prospects adversely affected by the recent financial crisis in the industrialised nations (Kliksberg, 2009).

In short, firms today are confronted with the multiple challenges of achieving greater competitiveness in light of trade liberalisation, sustainability, civil society's expectations and the added pressure of the global financial crisis. These have resulted in the awareness of a responsibility towards a broader constituency than simply shareholders, and a more detailed set of performance indicators than simply maximising profits (Casanova, 2005; Reficco & Ogliastri, 2009; Scherer et al., 2009). Hence, the notion of business success and what it means from a societal perspective has in recent years received considerable attention around the globe.

South Africa is a middle-income emerging economy. While its economy is no longer defined by race as it was in the apartheid years before 1994, inequality remains and its Gini coefficient is amongst the world's highest (Bosch, Rossouw, Claassens & du Plessis, 2010). Its economy is the largest and most competitive in Africa although the economic gap between South Africa and some of its neighbours is narrowing. In certain areas such as financial market development and private institution accountability it is globally competitive. In areas such as labour market efficiency, crime prevention, health and education, however, it ranks very poorly (WEF, 2011). CSR and business ethics are prominent concerns in South Africa with the institutionalisation of standards of corporate governance through, for example, wide adoption in the early 1990s of the codes of conduct of the King Committee's Report on Corporate Governance and their revisions in 2002 and 2009 (Rossouw, van der Watt & Malan, 2002; Rossouw, 2005). Firms are expected to supply information on their CSR programs and to have them independently assured (Institute of Directors, 2009), and the degree of assurance in South Africa compares favourably with that in developed countries (Marta, Singhapakdi & Higgs-Kleyn, 2001; Ackers, 2009).

One may, therefore, expect South Africans to demonstrate a high stakeholder orientation. South Africans would not see profits as the exclusive objective of business activity; moral values would probably be seen as central to success in business. 'Good' business people tend to be successful, and business ethics are not merely a public relations concept (Moore & Radloff, 1996; Sims & Gegez, 2004). The prominence given to the King Committee's codes (Rossouw & Van Vuuren, 2003) and their wide adoption would suggest that great value is placed on ethics and social responsibility. The importance of business ethics has increased in South Africa, in part because of legislative requirements (Edwards, 2007; Johnston, 2011). Pienaar and Roodt (2001), for example, found no demand for business ethics training among industrial psychologists, but within five years Barnard and Fourie (2007) found a significant call for such training.

Certain South African managers may, on the other hand, exhibit a shareholder orientation or indeed a pure profit motive that extends beyond the shareholder view. Historically, South Africa has tended to follow the US business model (Rossouw & Van Vuuren, 2003; Goosen & Van Vuuren, 2005); and while business formally endorses good governance and ethical conduct, ethics training in organisations is generally brief (Malan & Smit, 2001; Nicolaides, 2009) and unethical conduct is rife (Erasmus & Wordsworth, 2004; Lloyd & Mey, 2010), suggesting that the pure profit motive remains paramount, and for some that goal overrides ethical considerations.

Peru experienced drastic changes in government economic policy, social and political upheaval, and bust-to-boom shifts in its business environment over the last four decades (Jaramillo & Silva-Jauregui, 2011). The country survived a military dictatorship from the late 1960s through the 1970s, intense terrorist activity in the 1980s, and hyperinflation exceeding 7000 percent in the early 1990s (Murakami, 2007). In 1991, the government responded with efforts geared toward aggressive privatisation and the pursuit of free trade (ADEX, 2005; Gonzalez Vigil, 2009). An influx of foreign investment followed and has continued up to the present (De Althaus, 2007; Dube, 2011). Political stability, macro-economic caution and the aggressive pursuit of free trade enabled the nation to emerge as one of the fastest growing economies in Latin America (Tello & Tavara, 2010). This economic expansion created heightened interest in the link between corporate activity and society (De Althaus, 2007; Flores & Ickis, 2007; Qmroz, 2008; Gil, 2009; Jaramillo & Silva-Jauregui, 2011).

In the case of Peru, a predominant stakeholder orientation would be plausible because of its Roman Catholic tradition, the growing influence of civil society (Caravedo, 1998; Peru 2021, 2010; Tromben, 2011), repudiation of corruption (Quiroz, 2008) and increased interest in social equity and inclusion (Jaramillo & Silva-Jauregui, 2011). Indeed, Peruvian managers appear to have a greater tendency towards idealism than their counterparts in other nations (Robertson et al., 2007). The recent, sustained economic boom, however, brought conspicuous tangible benefits, with corporate success receiving wide publicity and admiration in the media (De Althaus, 2007 Anon., 2008; Parnell, 2008; Anon., 2009; Tello & Tavara, 2010), suggesting that a shareholder orientation may also be plausible in Peru.

CSR has been discussed in various business, political, and academic circles in Peru (Schwalb et al., 2003; Schwalb et al., 2005) but research suggests that the concept is still in its operational infancy (Burton & Goldsby, 2009; Tromben, 2011; Marquina, Goñi, Rizo-Patrón, Castelo, Castro, Morice, Velasquez & Villaseca, 2011). While many firms engage in philanthropy or public image initiatives, the relatively few that consider CSR to be something more have focused on community relations and the environment (Schwalb et al., 2003; Portocarrero, Sanborn & Camacho, 2007; Caravedo, 2009) rather than labour or other internal issues (Garavito, 2008).

3 The perceived role of ethics and social responsibility

Numerous scholars and practitioners argue that decision-makers should incorporate ethical and social responsibility considerations into their strategic decision-making processes (Velasquez, 1996; Shafer et al., 2007; Vitell et al., 2010). Singhapakdi et al. (1996) developed the Perceived Role of Ethics and Social Responsibility (PRESOR) scale to measure individual orientations toward ethics, social responsibility and profits. Three PRESOR factors were included in their original work, including social responsibility and profitability, long-term gains, and short-term gains. The PRESOR scale is appropriate for international comparison because national culture is a significant factor in ethical decision-making (Buller, Kohls & Anderson, 2000; Sims & Gegez, 2004; Singhapakdi, Vitell & Leelakulthanit, 1994).

Although their initial analysis supported the existence of these factors, additional work suggested that modifications were appropriate, while the cross-cultural context of many of the studies suggests their validity in diverse national settings. Etheredge (1999) applied the PRESOR scale to part-time Chinese MBA students in Hong Kong and identified only two factors, 'importance of ethics and social responsibility' and 'subordination of ethics and ; social responsibility.' Axinn et al. (2004) assessed the original data of Singhapakdi, Kraft, Vitell and Rallapalli (1995) as applied to MBA students in Malaysia and the Ukraine, with results also coalescing along two themes-stakeholder and shareholder views- with the former further divided into two subdimensions. The cross-cultural study by Axinn et al. (2004) lends credence to the instrument in Malaysia and Ukraine. The Spanish application in Vitell et al. (2010) supported the instrument's general structure as well. Research in the United States and China reported by Shafer et al. (2007) supports a two-factor solution with five shareholder view items and eight stakeholder view items.

From these studies and less formal operational observations, two different characterisations of managers' perceptions have emerged. Some managers possess a predominantly shareholder orientation, emphasising the fiduciary responsibility of a firm to its owners. Others are more stakeholder-oriented, giving more credence to the interests of multiple organisational stakeholders rather than emphasising just shareholders. Broadly speaking, a stakeholder orientation reflects a general thrust in CSR literature (see Orlitzky et al., 2011). More specifically, it is consistent with Sen's (2009) notion of heightened concern for ethics and social responsibility as an integral part of managing the firm.

4 Hypotheses

This paper tests the extent to which an individual's responses along the PRESOR scale are associated with perceptions of organisational performance. Four hypotheses are proposed and tested in South Africa, Peru and the United States.

The relationship between PRESOR category and organisational performance is intriguing. Prima facie, one might expect individuals with a shareholder orientation to outperform their counterparts on traditional measures of performance, that is, to demonstrate greater satisfaction with performance as defined by their satisfaction with firm profits.

H1a: In the United States, respondents with a high stakeholder orientation will report greater satisfaction with performance than respondents with a low stakeholder orientation.

This hypothesis postulates a link between organisational performance, ethics and CSR. As previously suggested, one might initially expect a stakeholder orientation when traditional measures of organisational performance are employed in the United States. The next hypothesis postulates a link between performance satisfaction and an approach that is more narrowly focused on profit and benefits to shareholders. This assertion assumes that ethics may be traded for profits in many decisions, and that individual predilections are associated with perceptions of performance (i.e. profitability) at the organisational level.

H1b: In the United States, respondents with a high shareholder orientation will report greater satisfaction with performance than respondents with a low shareholder orientation.

In Peru, the case for stakeholder and shareholder orientations could be supported by recent organisational performance and economic success (De Althaus, 2007), on the one hand, and the growing interest in ethical issues related to the operations of public and private organisations on the other (Quiroz, 2008; Caravedo, 2009). The picture is clouded, however, given the limited track record and awareness of such initiatives (Marquina et al., 2011) and the expectation that they would be more evident in developed countries with deeper traditions of CSR and formalised ethical approaches to business (Garavito, 2008; D'Alessio & Marquina, 2009). Nevertheless, the business environment in Peru is evolving and expectations regarding organisational behaviour are changing (Tromben, 2011; Jaramillo & Silva-Jauregui, 2011). Select case studies documenting the practice of CSR refute the notion that such practices are not undertaken or are impractical in Peru (Schwalb et al., 2003, 2005; Sanborn, Del Castillo & Chavez, 2006; Flores & Ickis, 2007; Portocarrero, Sanborn, Del Castillo & Chavez, 2007). In some instances these studies quantify the contribution of CSR to firms' financial success rather than confirming a popular notion that they represent only a cost with little net positive impact on the firm's financial performance. The following hypothesis postulates a link between performance satisfaction and a broader ethical approach to business in Peru.

H2a: In Peru, respondents with a high stakeholder orientation will report greater satisfaction with performance than respondents with a low stakeholder orientation.

A link between a shareholder orientation and stronger performance outcomes seems consistent with two factors in Peru: recent rapid growth of the economy, despite growth being concentrated in traditional sectors such as mining and agribusiness (Tello & Tavara, 2010); and the absence of widespread initiatives linking business performance to CSR (Garavito, 2008; Marquma et al., 2011). This is postulated in the following hypothesis and a broader ethical.

H2b: In Peru, respondents with a high shareholder orientation will report greater satisfaction with performance than respondents with a low shareholder orientation.

In the case of South Africa, there is support for the view that managers reporting a stakeholder orientation would report greater satisfaction with performance. It is widely held that ethics and organisational success are linked (Rossouw et al., 2002; Van Vuuren, 2002; Rossouw & Van Vuuren, 2003). The following hypothesis postulates a positive link between performance satisfaction, ethics and CSR.

H3a: In South Africa, respondents with a high stakeholder orientation will report greater satisfaction with performance than respondents with a low stakeholder orientation.

However, opposition to this perspective is also evident. Some believe that directors focus too heavily on CSR, that 'codes of behaviour have been driven to such a degree that they now derogate from the essential requirement... to run successful businesses' (Johnston, 2011: 62). The idea that a preoccupation with ethics hinders business is not uncommon. In South Africa, it could also be expected that a shareholder orientation would correspond with greater satisfaction than would the stakeholder orientation. A lack of morality is not the equivalent of a shareholder orientation, although both may share a profit focus. Coldwell (2010) identifies 'amoral' management as a profit-driven approach with little sensitivity to ethics, but recognises that such an orientation and its prevalence is unmeasured. The following hypothesis postulates a link between satisfaction with organisational performance and a shareholder orientation in South Africa.

H3b: In South Africa, respondents with a high shareholder orientation will report greater satisfaction with performance than respondents with a low shareholder orientation.

One's management perspective can change when one progresses through an organisation's hierarchy. Indeed, top managers often view strategic and other considerations differently from their counterparts at other management levels (Parnell, 2005). The extent to which stakeholder or shareholder orientation might differ is unclear, however. The final hypothesis postulates no difference in orientation by level of management.

H4: There will be no significant differences in stakeholder or shareholder orientation across management levels.

5 Methods

This study utilised the previously validated PRESOR scale of Singhapakdi et al. (1996) as the theoretical frame for the further measurement of subjective perceptions of organisational performance. Qualitative measures of organisational performance have been utilised in a number of studies to assess subjective areas of performance such as the satisfaction of managers, customers and other stakeholders. Invoking a qualitative perspective of performance can provide insight into organisational processes and outcomes that cannot be seen via financial measures (Ayadi, Dufrene & Obi, 1996; Parnell, O'Regan & Ghobadian, 2006). Hence, self-reporting scales that assess relative competitive and objective performance in the present study were adopted from Ramanujam and Venkatraman (1987).

The present study employed these scales in South Africa, Peru and the United States. Targeting a minimum of 60 respondents in each country for a multi-nation comparison is consistent with the protocol suggested by Malhotra, Agarwal and Peterson (1996). The questionnaire was presented in USA English in the United States, in UK English in South Africa, and in Peru it was translated into Spanish and checked for accuracy.were graduate business students and working professionals across professions and industries, and all Respondents were practising managers.

6 Findings

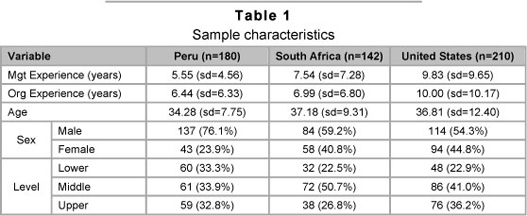

A total of 532 usable responses were collected, including 180, 142, and 210 from Peru, South Africa, and the United States respectively. A summary of the national samples appears in Table 1.

Factor analyses were conducted to assess the integrity of both PRESOR subscales (see Table 2). Results were generally supportive, including coefficient alphas above .70 and solid factor loadings, with only one below .500 and four below .600.

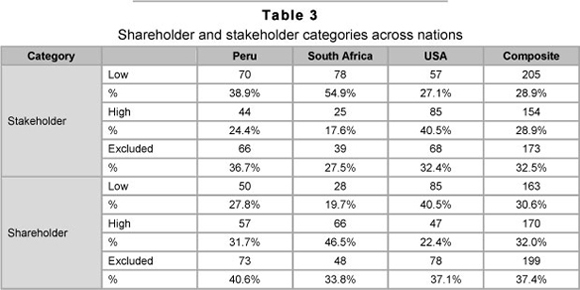

The national samples were categorised along the PRESOR scale. Following the distinction in Shafer et al. (2007) between shareholder and stakeholder views, each respondent was classified as high or low in shareholder and stakeholder orientations if the factor score for each measure was one-half of one standard deviation or greater from the mean. Those with factor scores within one-half of one standard deviation from the mean were not classified. In other words, respondents with factor scores greater than 0.5 were considered high, those less than -0.5 were considered low, and those between -0.5 and 0.5 were excluded from the test. Table 3 provides category membership by nation.

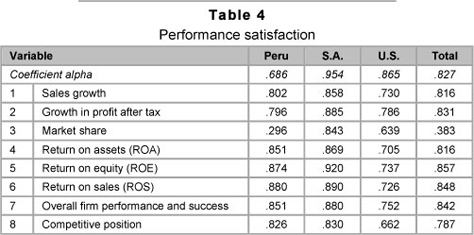

The performance satisfaction scale was also factor analysed to assess integrity (see Table 4). One item in the performance satisfaction scale (item 3) did not load well in the Peruvian and composite samples but the coefficient alpha statistics were acceptable across all national samples, so no items were removed from the analysis.

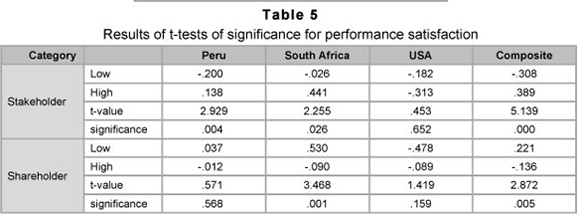

H1a and H1b were not supported. While high stakeholder and shareholder orientations were associated with performance satisfaction in the United States, the differences were not significant (see Table 5) and the hypotheses were not supported.

H2a was supported. Managers in Peru with a high stakeholder orientation reported a greater satisfaction with performance than did those with a low stakeholder orientation.

H2b was not supported. In Peru, managers with low and high shareholder orientations reported performance satisfaction levels near the mean; the difference was therefore not significant. The view that a high shareholder orientation is associated with greater performance in Peru was not supported.

H3a was supported. Managers in South Africa with a high stakeholder orientation reported significantly greater satisfaction with performance than did those with a low stakeholder orientation.

H3b was not supported. Managers with a high shareholder orientation did not reflect greater performance satisfaction. In fact, South African managers with a low shareholder orientation reported the greatest satisfaction with performance with over one-half of one standard deviation below the mean.

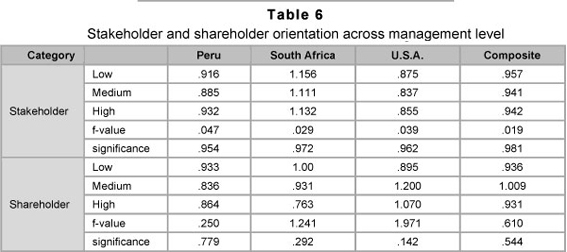

H4 was supported. None of the differences in stakeholder or shareholder orientation across management level were significant (see Table 6).

7 Discussion

The data presented in this paper suggests several key differences in stakeholder and shareholder orientations. Indeed, results were mixed, suggesting differences across nations. A number of findings warrant elaboration. In Peru - unlike South Africa and the United States - there is a long history of business corruption which is a significant hindrance to business (Lopez-Claros, Porter & Schwab, 2005; Lopez-Claros, Porter, Sala-i-Martin & Schwab, 2006; Porter & Sala-i-Martin, 2007; Quiroz, 2008). Hojman and Perez (2005) have identified the tumultuous influence of multiple cultures in neighbouring Chile that result in ambiguity, inconsistency and contradiction. Peru has similarly experienced a mosaic of sharply contrasting cultural perspectives that go with the visible, outward embrace of market capitalism that may not reflect many Peruvians' true position. While the view was not corroborated in this study, previous research also suggests that significant differences exist in the attitudes of middle and lower managers and those at senior executive level (Parnell, 2008) while expatriate professionals with whom Peruvians work may also affect perceptions (Delmestri, 2006).

When compared to both Peru and the United States, the percentage of South African managers categorised as stakeholder-oriented was lower, and the percentage categorised as shareholder-oriented was substantially higher (see Table 3). On close examination the percentage of South African managers with a low stakeholder orientation was far greater than the percentage with a high stakeholder orientation; and the percentage with a high shareholder orientation was far greater than the percentage with a low shareholder orientation. While South African stakeholder and shareholder orientations were originally considered as a possibility, their extremity was unexpected, and particularly so when compared to Peru and the United States. It is surprising given the overt attention paid to CSR in South African business, legislation and research, and in the light of earlier cross-national studies such as those of Moore and Radloff (1996) or Sims and Gegez (2004). The finding may also point to the possibility that there is a degree of 'CSR fatigue' amongst South African managers, as expressed in Johnston (2011).

A key shortcoming of the PRESOR scale is noted. Ethics is an individual construct associated with moral decision-making. Social responsibility is an organisational construct and refers to the notion that firms have an obligation to society beyond that of producing profits for their shareholders. The PRESOR scale includes social responsibility considerations as part of a broader ethics orientation. Rejection of social responsibility appears as rejection of managerial ethics, which is not necessarily the case. Moreover, in some nations high degrees of CSR can co-exist with low or varying degrees of individual honesty, morality and fairness, and vice-versa. Hence, the scale may measure the perceived importance of CSR for the business enterprise more than it does the individual's imperative for managerial ethics. Moreover, there is the assumption that managers are willing to sacrifice ethics in their pursuit of shareholder profit. For example, the item, 'The most important concern for a firm is making a profit, even if it means bending or breaking the rules,' is two-dimensional, assessing both shareholder orientation and a willingness to compromise ethics. PRESOR presupposes that ethical concerns underpin a shareholder orientation. Hence, additional scale modifications might be necessary to categorise managers with greater precision.

The links between stakeholder/shareholder categories and organisational performance are not causal and should not be interpreted literally. Greater satisfaction with firm performance in one category does not mean that alignment to that category always results in higher performance, especially at firm level. Given the influence of organisational culture, one's ethical perspective is often shared - at least to some extent - by other members of an organisation, but this is not always the case (Parnell & Dent, 2009). Moreover, ethical views are assessed at the individual level, whereas performance is assessed at the organisational level. Hence, the findings reported here are promising, but additional work is warranted.

Stakeholder and shareholder orientations are, in addition, not mutually exclusive. Put another way, some managers may be oriented toward a stakeholder or a shareholder orientation, but others might be oriented toward both, or possibly neither; trade-offs between the two extremes are not inherent. Indeed, the extent to which choices must be made between ethics and profits has been widely debated (Parnell & Dent, 2009; Vitell et al., 2010). Some scholars and practitioners emphasise the maxim that 'good ethics is good business' - a perspective also reflected in PRESOR item 13 - while others highlight the myriad decisions executives face whereby profits can be maximised at the expense of ethical considerations. Managers with both stakeholder and shareholder orientations eschew the notion that interests in ethics and profits are mutually exclusive.

The notion of a combined stakeholder/ shareholder orientation may be more common in some nations than in others. For example, such a combination may not be as pervasive in Peru because of the relatively few examples of firms embodying such a perspective (Schwalb et al., 2003; Schwalb, 2010; Marquina et al., 2011). In a sense, respondents are probably less likely to opt for something that is practised on a limited scale and hence not readily seen.

Another distinction warrants clarification -the examination of short- and long-term perspectives on performance. Although a shareholder orientation might lead to high profits in the short run, one could argue that maximising long-term shareholder returns only occurs when the needs of all stakeholders are considered (Jones & Wicks, 1999). In this regard, individuals with stakeholder and shareholder orientations appear to focus on the convergence of both sets of interests in the long run.

8 Conclusions and future directions

The evidence presented in this paper supports the notion that many, albeit not all, business professionals in the United States, Peru and South Africa tend to see beyond a narrow profits-only orientation in their quest for high organisational performance. Although there is evidence of a range of perceptions amongst managers and differences in and across countries, the study's findings dispel the notion that outside of industrialised countries managers do not link firm performance to questions of ethics and social responsibility. It also suggests that trade-offs do not necessarily exist between concerns for ethics and profits.

There are similarities and differences across nations with respect to the link between stakeholder and shareholder orientations and organisational performance. The composite results presented in Table 5 underscore the reality that relationships differ markedly across nations.

A re-examination of the conceptual foundation for a high orientation in both stakeholder and shareholder orientations is germane. If all stakeholders benefit in the long run from superior firm performance and shareholders benefit from attention given to the needs of other stakeholders (see Jones & Wicks, 1999), then such a perspective is the most rational. The distinction between a high stakeholder orientation alone and combined high stakeholder and shareholder orientations categories is therefore modest at best. Given these considerations, it would follow that organisations should consider social obligations within the context of long-term performance and 'manage' CSR as they do other business considerations.

On the other hand, if the needs of shareholders and other stakeholders do not converge over the long term, then proclaiming both orientations simultaneously is naive. Only those with stakeholder and shareholder orientations understand the necessary short-term and long-term trade-offs that must be made with regard to myriad conflicting stakeholder interests (see Asher, Mahoney & Mahoney, 2005; Jacoby, 2005).

Most scholars and practitioners occupy a middle ground between these two extremes, assuming partial convergence of shareholder and other stakeholder interests (Garcia-Castro et al., 2011). Numerous positions between these two extremes can be identified, however, each accepting a different degree of possible convergence and favouring one extreme over the other. Additional scholarly work is needed to clarify this conundrum.

A number of opportunities for future research have been identified. First, the blending of managerial ethics and social responsibility in the shareholder portion of the PRESOR presents a challenge to scholars attempting to categorise managers on various ethical, CSR, or profit orientations. Additional research on the prospective combinations of stakeholder and shareholder orientations would be fruitful. Individuals possessing mixed orientations reject an either/or perspective on profits and ethics. Embracing the two perspectives simultaneously is plausible and can be associated with high organisational performance.

Replications of the present study in other emerging and newly industrialised countries (NICs) may identify factors that are associated with economic development status. The need to understand the cultural impact of the relationships among behavioural variables in organisations has never been more important (Hutchings, Metcalfe, & Cooper, 2010). Whereas scholars have typically viewed findings in western industrialised organisations as generalisable (Boyacigiller & Adler, 1991), research highlighting the influence of culture and other factors suggests that is not always the case (Lenartowicz & Johnson, 2003). Additional scholarly work investigating the role of culture and other factors in organisational processes and performance in developing nations is needed (Elbanna, 2007; El-Amir & Burt, 2008).

The relationship between managers' performance satisfaction, shareholder and stakeholder orientations in developing countries bears monitoring. Perceptions are affected by the pace and nature of development and current economic conditions, hence, managers should be assessed to establish whether more unanimous perceptions emerge over time. This is particularly significant in countries such as South Africa and Peru where economic transition is rapid and management ethos in a greater state of flux than is the case in more established economies.

Individuals aligning along specific PRESOR categories across national boundaries could have more in common than they would with those in other categories within their own countries. Following this logic, exploring the differential construction of the categories across national boundaries, and the degree of similarity of those aligning along particular categories across national boundaries in terms of management variables other than ethics, represent fruitful endeavours for further study.

Problems arise when constructs and surveys are modified or translated to suit samples in other cultures (Punnett & Shenkar, 1994; Parnell & Hatem, 1999), while the universality, hegemony and cultural encroachment of theory, methodology and practice based exclusively on experience in western industrialised economies is increasingly resisted and challenged (McDonald, 2010; Sams, Khan & Ospina, 2011). While methodological consistency is desirable, many western management constructs are inappropriate in emerging economies and NICs, including those in Latin America and Africa. Existing theory should be applied with allowance made for theoretical modifications when findings cannot be readily explained by prevailing approaches.

REFERENCES

ACKERS, B. 2009. Corporate social responsibility assurance: how do South African publicly listed companies compare? Meditari Accountancy Research, 17(2):1-17. [ Links ]

ADEX (ASOCIACIÓN DE EXPORTADORES). 2005. TLC con Tailandia se suscribirá en mayo del 2006. Perú Exporta, 324:28-29. [ Links ]

ANON. 2008. Country Report: Peru. London: The Economist Intelligence Unit. [ Links ]

ANON. 2009. Peru's economy has shrunk but it should escape recession. The Economist, London, September 2:23. [ Links ]

ARMOUR, J., DEAKIN, S. & KONZELMANN, S.J. 2003. Shareholder primacy and the trajectory of UK corporate governance. British Journal of Industrial Relations, 41(3):531-555. [ Links ]

ASHER, C., MAHONEY, J. & MAHONEY, J. 2005. Towards a property rights foundation for a stakeholder theory of the firm. Journal of Management & Governance, 9(1):5-32. [ Links ]

AQUILAR, F.J. 1994. Managing Corporate Ethics. New York: Oxford University Press. [ Links ]

AXINN, C.N., BLAIR, M.E., HEORHIADI, A. & THACH, S.V. 2004. Comparing ethical ideologies across cultures. Journal of Business Ethics, 54(2):103-119. [ Links ]

AYADI, O.G., DUFRENE, U.B. & OBI, C.P. 1996. Firm performance measures: Temporal roadblocks to innovation? Managerial Finance, 22(8): 18-22. [ Links ]

BARNARD, G. & FOURIE, L. 2007. Exploring the roles and contributions of industrial psychologists in South Africa against a multi-dimensional conceptual framework. South African Journal of Industrial Psychology, 33(2):45-53. [ Links ]

BELAUSTEGUIGOITIA, I. & PORTILLA, S. 2004. The family business in Chile and Mexico: organisational climate as an antecedent of entrepreneurial orientation. In S. Tiffin (ed.) Entrepreneurship in Latin America. London: Praeger. [ Links ]

BIEREMA, L.L. & D'ABUNDO, M.L. 2004. HRD with a conscience: practicing socially responsible HRD. International Journal of Lifelong Education, 23(5):443-458. [ Links ]

BOSCH, A., ROSSOUW, J., CLAASSENS, T. & DU PLESSIS, B. 2010. A second look at measuring inequality in South Africa: A modified Gini coefficient. Working Paper No 58. School of Development Studies, University of KwaZulu-Natal. [ Links ]

BOWEN, H.R. 1953. Social responsibilities of the businessman. New York: Harper Business. [ Links ]

BOYACIGILLER, N. & ADLER, N.J. 1991. The parochial dinosaur: Organizational science in a global context. Academy of Management Review, 16(2):262-290. [ Links ]

BULLER, P.F., KOHLS, J.J. & ANDERSON, K.S. 2000. When ethics collide: Managing conflict across cultures. Organizational Dynamics, 28(4):52-66. [ Links ]

BURTON, B.K. & GOLDSBY, M. 2009. Corporate social responsibility orientation, goals, and behavior: A study of small business owners. Business & Society, 48(1):88-104. [ Links ]

CARAVEDO, B. 1998. La responsabilidad social de las empresas privadas n el Perú. Lima: SASE (Servicios para el desarrollo) y Perú 2021-Una nueva visión. [ Links ]

CARAVEDO, B. (ed.) 2009. Responsabilidad social: Todos. La voz de lasregiones: La Libertad. Lima, PUND (Programa de las Naciones Unidaspara el Desarrollo). [ Links ]

CASANOVA, L. 2005. Latin America: Economic and business context. International Journal of Human Resource Management, 16(12):2173-2188. [ Links ]

CHARRON, D. 2007. Stockholders and stakeholders: The battle for control of the corporation. CATO Journal, 27(1):1-22. [ Links ]

COLDWELL, D.A.L. 2010. A road to organizational perdition? Business, ethics and corporate social responsibility. South African Journal of Economic and Management Sciences, 13(2):190-202. [ Links ]

CRILLY, D. 2011. Cognitive scope of the firm: Explaining stakeholder orientation from the inside-out. Business & Society, 50(3):518-530. [ Links ]

D'ALESSIO, F. & MARQUINA, P. 2009. Evolución del concepto de responsabilidad social. Revista Brújula, 9(16). [ Links ]

DE ALTHAUS, J. 2007. La revolución capitalista en el Perú. Lima: Fondo de Cultura Económica. [ Links ]

DELMESTRI, G. 2006. Streams of inconsistent institutional influences: Middle managers as carriers of multiple identities. Human Relations, 59(11):1515-1541. [ Links ]

DIAS, A.T. & GONÇALVES, C.A. 2007. Macroeconomic context, relationships with stockholders and strategic factors in the determination of Brazilian corporations' performance. Latin American Business Review, 8(3):1-23. [ Links ]

DUBE, R. 2011. Peru's May GDP expands 7.1% versus year ago. Wall Street Journal, 15 July:2. [ Links ]

EDWARDS, T. 2007. Ethical fitness for accountable public officials: An imperative for good governance. Journal of Public Administration, 42(5):28-34. [ Links ]

EL-AMIR, A. & BURT, S. 2008. Sainsbury's in Egypt: The strategic case of Dr. Jekyll and Mr. Hyde? International Journal of Retail Distribution Management, 36(4):300-322. [ Links ]

ELBANNA, S. 2007. The nature and practice of strategic planning in Egypt. Strategic Change, 16(5):227-243. [ Links ]

ERASMUS, B.J. & WORDSWORTH, R. 2004. Aspects of business ethics in South Africa. South African Journal of Labour Relations, 28(2):77-112. [ Links ]

ETHEREDGE, J.M. 1999. The perceived role of ethics and social responsibility: An alternative scale structure. Journal of Business Ethics, 18(1):51-64. [ Links ]

FLORES, J. & ICKIS, J. 2007. La responsabilidad social en Cementos Lima, y susefectos en la creación de valor para el negocio y en la gestión de riesgo. In J. Flores, E. Ogliastri, E. Peinado-Vara & I. Petry (eds.) El argument empresarial de la RSE: 9 casos de America Latina y el Caribe. Washington D.C.: BID (Banco Interamericano de Desarrollo) y INCAE Business School. [ Links ]

FREEMAN, R.E. & REED, D.L. 1983. Stockholders and stakeholders: A new perspective on corporate governance. California Management Review, 25(3):88-106. [ Links ]

FRIEDMAN, M. 1993. The social responsibility of business is to increase its profits. In T.I. White (ed.) Business ethics: A philosophical reader. New York: Macmillan. [ Links ]

GARAVITO, C. 2008. Responsabilidad social empresarial y mercado de trabajo. Economía, XXXI(61):81-104. [ Links ]

GARCIA-CASTRO, R., ARINO, M.A. & CANELA, M.A. 2011. Over the long-run? Short-run impact and long-run consequences of stakeholder management. Business & Society, 50(3):428-455. [ Links ]

GIL, V. 2009. Aterrizajeminera. Cultura, conflicto, negociaciones y leccionespara el desarrollodesde la minería en Ancash, Perú. Lima: Instituto de Estudios Peruanos (IEP). [ Links ]

GONZÁLEZ VIGIL, F. 2009. El TLC China-Perú: Una negociación ejemplar. Punto de Equilibrio, 18(101):30-31. [ Links ]

GOODPASTER, K.E. 1993. Business ethics and stakeholder analysis. In T.I. White (ed.) Business ethics: A philosophical reader. New York: Macmillan. [ Links ]

GOOSEN, X. & VAN VUUREN, L.J. 2005. Institutionalising ethics in organisations: The role of mentoring. SA Journal of Human Resource Management, 3(3):61-71. [ Links ]

HANDY, C. 2002. What's a business for? Harvard Business Review, 80(12):49-56. [ Links ]

HOJMAN, D. & PÉREZ, G. 2005. Culturanacional y culturaorganizacional en tiempos de cambio: La experiencia chilena. Revista Latinoamericana de Administración, 35:87-105. [ Links ]

HUTCHINGS, K., METCALFE, B.D. & COOPER, B. 2010. Exploring Arab Middle Eastern women's perceptions of barriers to, and facilitators of, international management opportunities. International Journal of Human Resource Management, 21(1):61-83. [ Links ]

INSTITUTE OF DIRECTORS. 2009. King Report on corporate governance. Johannesburg: IOD. [ Links ]

JACOBY, S.M. 2005. The embedded corporation. New Jersey: Princeton University Press. [ Links ]

JAIN, A. & PISANI, M.J. 2008. Small- and microenterprise business development in Costa Rica: an examination of domestic and foreign born entrepreneurs. Latin American Business Review, 9(2): 149-167. [ Links ]

JARAMILLO, F. C. & SILVA-JÁUREGUI, C. (eds.) 2011. Peru en el umbral de una nueva era. Lecciones y desafíos para consolidar el crecimiento económico y un desarrollo más incluyente. Notas de política Vol. 1. Lima: Banco Mundial. [ Links ]

JOHNSTON, A. 2011. A matter of ethics. Without Prejudice, 11(6):62-64. [ Links ]

JONES, T.M. & WICKS, A.C. 1999. Convergent stakeholder theory. Academy of Management Review, 24(2):206-211. [ Links ]

KARNANI, A. 2011. 'Doing well by doing good': The grand illusion. California Management Review, 53(2):69-86. [ Links ]

KAY, S. & POPKIN, S.J. 1998. Integrating ethics into the strategic management process: Doing well by doing good. Management Decision, 36(5):331-338. [ Links ]

KEAY, A. 2008. Ascertaining the corporate objective: An entity maximisation and sustainability model. Modern Law Review, 71(5):663-698. [ Links ]

KLIKSBERG, B. 2009. Una agenda renovada de responsabilidad empresarial para América Latina en la era de la crisis. In Ministerio de Trabajo, Empleo y Seguridad Social. RSE y trabajo decente en la Argentina. Contexto, desafíos y oportunidades. Buenos Aires: Ministerio de Trabajo, Empleo y Seguridad Social. [ Links ]

LENARTOWICZ, T. & JOHNSON, J.P. 2003. A cross-national assessment of the values of Latin American managers: contrasting hues or shades of gray. Journal of International Business Studies, 34(3):266-281. [ Links ]

LLOYD, H.R. & MEY, M.R. 2010. An ethics model to develop an ethical organisation. SA Journal of Human Resource Management/SA Tydskrif vir Menslike Hulpbronbestuur, 8(1), Art. #218, 12 pages. DOI:10.4102/sajhrm.v8i1.218. [ Links ]

LOPEZ-CLAROS, A., PORTER, M.E. & SCHWAB, K. 2005. The Global Competitiveness Report 2005-06. New York: Palgrave Macmillan. [ Links ]

LOPEZ-CLAROS, A., PORTER, M.E., SALA-I-MARTIN, X. & SCHWAB, K. 2006. The Global Competitiveness Report 2006-07. New York: Palgrave Macmillan. [ Links ]

MALAN, F. & SMIT, B. 2001. Ethics and leadership in business and politics. Lansdowne: Juta. [ Links ]

MALHOTRA, N.K., AGARWAL, J. & PETERSON, M. 1996. Methodological issues in cross-cultural marketing research: A state-of-the-art review. International Marketing Review, 13(5):7-43. [ Links ]

MARQUINA, P., GOÑI, N., RIZO-PATRÓN, C., CASTELO, L., CASTRO, R., MORICE, J., VELASQUEZ, I. & VILLASECA, M. 2011. Diagnóstico de la Reponsabilidad Social en Organizaciones Peruanas. Una Aproximación Interinstitucional y Multidisciplinaria. Lima: CENTRUM Centro de Negocios de la Pontificia Universidad Católica del Perú [ Links ].

MARTA, J.M., SINGHAPAKDI, A. & HIGGS-KLEYN, N. 2001.Corporate ethical values in South Africa. Thunderbird International Business Review, 43(6):755-772. [ Links ]

MATWIJKIW, A. & MATWIJKIW, B. 2010. Stakeholder theory and justice issues: The leap from business management to contemporary international law. International Criminal Law Review, 10(2010):143-180. [ Links ]

MCDONALD, G. 2010. Ethical relativism vs. absolutism: Research implications. European Business Review, 22(4):446-464. [ Links ]

MOORE, R.S. & RADLOFF, S.E. 1996. Attitudes toward business ethics held by South African students. Journal of Business Ethics, 15(8):863-869. [ Links ]

MOURA-LEITE, R.C., PADGETT, R.C. & GALAN, J.I. 2011. Stakeholder management and nonparticipation in controversial business. Business & Society, forthcoming. [ Links ]

MURAKAMI, Y. 2007. Perú en la Era del Chino. Kyoto: Instituto de EstudiosPeruanos and the Center for Integrated Area Studies, Kyoto University. [ Links ]

NICOLAIDES, A. 2009. Business ethics in Africa. Journal of Contemporary Management, 6:490-501. [ Links ]

ORLITZKY, M., SIEGEL, D.S. & WALDMAN, D.A. 2011. Strategic corporate social responsibility and environmental sustainability. Business & Society, 50(1):6-27. [ Links ]

PARNELL, J.A. 2005. Strategic philosophy and management level. Management Decision, 43(2):157-170. [ Links ]

PARNELL. J.A. 2008. Strategy execution in emerging economies: Assessing strategic diffusion in Mexico and Peru. Management Decision, 46(9):1277-1298. [ Links ]

PARNELL, J.A. & DENT, E.L. 2009. Philosophy, ethics and capitalism: An interview with BB&T CEO John Allison. Academy of Management Learning & Education, 8(4):587-596. [ Links ]

PARNELL, J.A. & HATEM, T. 1999. Cultural antecedents of behavioral differences between American and Egyptian managers. Journal of Management Studies, 36(3):399-418. [ Links ]

PARNELL, J. A., O'REGAN, N. & GHOBADIAN, A. 2006. Measuring performance in competitive strategy research. International Journal of Management and Decision Making, 7(4):408-417. [ Links ]

PIENAAR, J. 2010. Ethics in economic and management sciences: A researcher's resource. South African Journal of Economic and Management Sciences, 13(2):177-189. [ Links ]

PIENAAR, Y. & ROODT, G. 2001. Die teenwoordige en toekomstige rolle van bedryfsielkundiges in Suid-Afrika [The present and future roles of Industrial Psychologists in South Africa]. Journal of Industrial Psychology, 27(4):25-33. [ Links ]

PERÚ 2021. 2010. Indicadores ETHOS-Perú 2021 de Responsabilidad Social Empresarial. Lima: Perú 2021. [ Links ]

PORTER. M. E. & KRAMER, M.R. 2002. The competitive advantage of corporate philanthropy. Harvard Business Review, 80(12):56-69. [ Links ]

PORTER, M. & SALA-I-MARTIN, K. 2007.The Global Competitiveness Report 2007-08. New York: Palgrave Macmillan. [ Links ]

PORTOCARRERO, F. S., SANBORN, C.A. & CAMACHO, L.A. (eds.) 2007. Moviendomontañas: Empresas, comunidades y ONG en las industrias extractivas. Lima: CIUP (Centro de Investigación de la Universidad del Pacífico). [ Links ]

PORTOCARRERO, F. S., SANBORN, C.A., DEL CASTILLO, E. & CHÁVEZ, M. 2007. Moviendomontañas: El caso de la Compañia Minera Antamina. Social Enterprise Knowledge Network. Case #SKS-086. Lima: Universidad del Pacifico. [ Links ]

PRAHALAD, C.K. 1994. Corporate governance or corporate value added?: Rethinking the primacy of shareholder value. Journal of Applied Corporate Finance, 6(4):40-50. [ Links ]

PUNNETT, B.J. & SHENKAR, O. 1994. International management research: Toward a contingency approach. Advances in International Comparative Management, 9:39-55. [ Links ]

QUINN, R.E. & ROHRBAUGH, J. 1983. A spatial model of effectiveness criteria: Towards a competing values approach to organizational analysis. Management Science, 29(3):363-377. [ Links ]

QUIROZ, A. 2008. Corrupt circles: A history of unbound graft in Peru. Washington, D. C.: Woodrow Wilson Center. [ Links ]

RAMANUJAM, V. & VENKATRAMAN, N. 1987. Planning system characteristics and planning effectiveness. Strategic Management Journal, 8(5):453-468. [ Links ]

REBÉRIOUX, A. 2007. Does shareholder primacy lead to a decline in managerial accountability? Cambridge Journal of Economics, 31(4):507-524. [ Links ]

REFICCO, E. & OGLIASTRI, E. 2009. Empresa y sociedad en America Latina: Una introducción. Academia, Revista Latinoamericana de Administración, 43:1-25. [ Links ]

ROBERTSON, C.J., OLSON, B.J., GILLEY, K.M. & BAO, Y. 2007. A cross-cultural comparison of ethical orientations and willingness to sacrifice ethical standards: China versus Peru. Journal of Business Ethics, 81(2):413-425. [ Links ]

ROBLES, F., SIMON, F. & HAAR, J. 2003. Winning Strategies for the New Latin Markets. Upper Saddle River, NJ: Financial Times. [ Links ]

RODIN, D. 2005. The ownership model of business ethics. Metaphilosophy, 36(1/2):163-181. [ Links ]

ROSSOUW, G.J. 2005. Business ethics and corporate governance in Africa. Business & Society, 44(1):94-106. [ Links ]

ROSSOUW, G.J., VAN DER WATT, A. & MALAN, D.P. 2002. Corporate governance in South Africa. Journal of Business Ethics, 37(3):289-302. [ Links ]

ROSSOUW, G.J. & VAN VUUREN, L.J. 2003. The business case for business ethics. Management Dynamics, 12(1):2-11. [ Links ]

SAMS, D., KHAN, M.A. & OSPINA, M. 2011. Across the great divide: Management, culture, and sustainability across NAFTA region. Journal of Academic and Business Ethics, 4(1): 1-13. [ Links ]

SANBORN, C, DEL CASTILLO, E. & CHÁVEZ, M. 2006. Cementos Lima: Construyendo los cimientos de una visión de responsabilidad social. Social Enterprise Knowledge Network. Case #SKS-069. Lima: Universidad del Pacifico. [ Links ]

SCHERER, A.G., PALAZZO, G. & MATTEN, D. 2009. Introduction to the special issue: Globalization as a challenge for business responsibilities. Business Ethics Quarterly, 19(3):327-347. [ Links ]

SCHWALB, M. M. (ed.) 2010. Experiencias exitosas de responsabilidad social empresarial. Apuntes de estudio 72. Lima, CIUP. [ Links ]

SCHWALB, M. M., ORTEGA, C. & GARCÍA, E., & SOLDEVILLA, V. (eds.) 2003. Casos de responsabilidad social. Apuntes de estudio 53. Lima: CIUP. [ Links ]

SCHWALB, M. M., GARCÍA, E. & SOLDEVILLA, V. (eds.) 2005. Buenaspractícasperuanas de responsabilidadempresarial: colleción 2005. Apuntes de estudio 63. Lima: CIUP. [ Links ]

SCHWARTZ, M. 2007. Corporate responsibility and Australian business: Identifying the issue. Australian Journal of Social Issues, 42(3):419-426. [ Links ]

SEN, A. 2009. "El papel de la éticaempresarial en el mundocontemporáneo, " Selected extracts of a speech delivered at Harvard University August 24, 2009 at the opening of the II Program for Trainers in Corporate Social Responsibility in Latin America. Boston: Harvard University. [ Links ]

SHAFER, W.E., FUKUKAWA, K. & LEE, G.M. 2007. Values and the perceived importance of ethics and social responsibility: The U.S. versus China. Journal of Business Ethics, 70(3):265-284. [ Links ]

SIMS, R.L. & GEGEZ, A.E. 2004. Attitudes towards business ethics: A five nation comparative study. Journal of Business Ethics, 50(3):253-265. [ Links ]

SINGHAPAKDI, A., KRAFT, K.L., VITELL, S.J. & RALLAPALLI, K.C. 1995. The perceived importance of ethics and social responsibility on organizational effectiveness: A survey of marketers. Journal of the Academy of Marketing Science, 23(1):49-56. [ Links ]

SINGHAPAKDI, A., VITELL, S.J. & LEELAKULTHANIT, O. 1994. A cross-cultural study of moral philosophies. Ethical perceptions and judgments: A comparison of American and Thai marketers. International Marketing Review, 11(6):65-7. [ Links ]

SINGHAPAKDI, A., VITELL, S.J., RALLAPALLI, K.C. & KRAFT, K.L. 1996. The perceived role of ethics and social responsibility: A scale development. Journal of Business Ethics, 15(11):1131-1140. [ Links ]

STRINE, L.E. 2008. Human freedom and two Friedmen: Musings on the implications of globalization for the effective regulation of corporate behaviour. University of Toronto Law Journal, 58(3):241-274. [ Links ]

TELLO, M.D. & TAVARA, J. 2010. Productive development policies in Latin American countries: The case of Perú, 1990-2007. IDB Working Paper Series No. IDB-WP 129. Washington, D.C.: Inter-American Development Bank. [ Links ]

TROMBEN, C. 2011. Capitalismo 3.0. Américaeconomía Perú, Feb:68-78. [ Links ]

VAN VUUREN, L.J. 2002. Institutionalising business ethics: A multi-level ethics strategy. Management Dynamics, 11(2):21-27. [ Links ]

VELASQUEZ, M. 1996. Why ethics matters: A defense of ethics in business organizations. Business Ethics Quarterly, 6(2):201-222. [ Links ]

VITELL, S.J. & HUNT, S.D. 1990. The general theory of marketing ethics: A partial test of the model. In N. Sheth (ed.) Research in Marketing, vol. 10 (pp. 237-265). Greenwich, CT: JAI Press. [ Links ]

VITELL, S.J. & PAOLILLO, J.G.P. 2004. A cross-cultural study of the antecedents of the perceived role of ethics and social responsibility. Business Ethics, 13(2-3):185-1999. [ Links ]

VITELL, S.J., RAMOS, E. & NISHIHARA, C.M. 2010. The role of ethics and social responsibility in organizational success: A Spanish perspective. Journal of Business Ethics, 91(4):467-483. WCED 1987. Report of the World Commission on environment and development: our common future. New York, NY: United Nations. [ Links ]

WEF 2011. The global competitiveness report 2011-2012. Geneva: World Economic Forum. [ Links ]

ZAHRA, S.A. & LATOUR, M.S. 1987. Corporate social responsibility and organizational effectiveness: A multivariate approach, Journal of Business Ethics, 6(6):459-467. [ Links ]

Accepted: September 2012

{kind=link}