Serviços Personalizados

Artigo

Inglês (pdf)

Inglês (pdf)

Artigo em XML

Artigo em XML Referências do artigo

Referências do artigo

Indicadores

Links relacionados

-

Citado por Google

Citado por Google -

Similares em Google

Similares em Google

Compartilhar

Permalink

PermalinkSouth African Journal of Economic and Management Sciences

versão On-line ISSN 2222-3436

versão impressa ISSN 1015-8812

S. Afr. j. econ. manag. sci. vol.15 no.3 Pretoria Jan. 2012

ARTICLES

Corruption and multinational companies' Entry Modes - do linguistic and historical ties matter?

Mariene GrandeI; Aurora AC TeixeiraII

IFaculdade de Economia, Universidade do Porto

IICEF. UP, Faculdade de Economia, Universidade do Porto; INESC Porto; OBEGEF

ABSTRACT

The literature on FDI entry modes and corruption tends to convey the idea that corruption leads to a choice between low equity modes, i.e. joint ventures with local partners, and non-equity modes, namely exports and contracting, in order to avoid contact with corrupt state officials. Recently, some studies have argued that despite corruption, linguistic and historical ties between home and host countries lead MNCs to prefer high-equity modes. Focusing on a rather unexplored setting, the African countries, most specifically the Portuguese-speaking ones (PALOP - Países Africanos de Língua Oficial Portuguesa), which include countries where levels of corruption are very high (e.g., Guinea-Bissau and Angola), high (e.g., Mozambique, Sao Tome and Principe), and intermediate (e.g., Cape Verde), maintaining also close linguistic and historical ties with Portugal, we found that the FDI entry mode is associated with the less corrupt markets. Thus, our results do not support the recent contention that cultural and historical links are likely to perform a mediating role, by fostering foreign direct investment, in supporting African countries to overcome the dismal growth some have been facing in the last few decades. On the contrary, our findings highlight the pressing need for these countries to combat corruption if higher economic growth via FDI attraction is envisioned.

Key words: corruption, emerging economies, entry mode

1 Introduction

Africa is becoming the new frontier for emerging-market investors (Santiso, 2007). An analysis by The Economist (2011) finds that over the last decade, no fewer than six of the world's ten fastest-growing economies are in sub-saharan Africa, including Angola in first place in the ranking and Mozambique in eighth. This evolution of formerly underdeveloped markets makes it increasingly more difficult for foreign investors to ignore these markets, despite their (justified) reputation as a tough place for business owing to political uncertainty, corruption, weak infrastructure and consistent regulation (The Economist, 2010).

Multinational companies (MNCs) are in-creaseingly influenced by institutional instability, perceived risk and uncertainty in their process of investing in emerging economies (Uhlenbruck, Rodriguez, Doh & Eden, 2006). In corrupt and risky contexts, there is evidence that firms prefer joint ventures to wholly-owned subsidiaries (Rodriguez, Uhlenbruck & Eden, 2005; Uhlenbruck et al., 2006; Straub, 2007; Javorcik & Wei, 2009; Demirbag, McGuinness & Altay, 2010). Regardless of whether firms face petty bureaucratic or high-level political corruption (Straub, 2007) and of the level of the pervasiveness and arbitrariness of corruption (Rodriguez et al., 2005; Uhlenbruck et al., 2006), existing empirical studies suggest that corruption influences the entry mode, particularly in the choice of non-equity modes or partnering.

According to some more recent studies (e.g., Cuervo-Cazurra, 2008; Demirbag et al., 2010; Jimenez, Durban & De la Fuente, 2011), the growing attractiveness of emergent regions allied to strong cultural and historical ties between home and some host countries have progressively led to a higher propensity for FDI despite the existence of corruption.

Studies that analyse the relationship between corruption and its impact on the MNCs' choice of entry mode have focused mainly on Eastern Europe (Javorcik & Wei, 2009) and Asia (Demirbag et al., 2010), or provide a general overview based on cross-country compositions (Uhlenbruck et al., 2006; Straub, 2007). Similar analyses focusing on African countries have been rather neglected in this regard.

Aiming to test the role of corruption in the firms' choice of entry mode in contexts where there are significant historical and cultural linkages, our analysis is focused on the Portuguese MNCs investing in the PAL OP, a set of countries characterised by levels of corruption which are very high (e.g., Guinea-Bissau, and Angola), high (e.g., Mozambique, Sao Tome and Principe) and intermediate (e.g., Cape Verde) (Transparency International, 2009). Given the close ties between Portugal and the PALOP based on linguistic and historical factors, and following the reasoning of Cuervo-Cazurra (2008), Demirbag et al. (2010) and Jiménez et al. (2011), it would be scientifically pertinent to analyse the extent to which the PALOP's corruption levels influence the entry modes of Portuguese MNCs in these countries. To this end, a direct questionnaire was built and applied to 562 Portuguese firms that have internationalised to the PALOP, from which we obtained 147 responses representing 334 firm-market observations. The empirical analysis undertaken contributes to the lack of literature on corruption and the MNCs' entry modes by analysing an under-explored context, the PALOP countries.

This paper is structured as follows. In Section 2 we review the literature on the theories and determinants of MNCs' entry modes and on corruption, broadening the analysis of existing articles on the impact of corruption on MNCs' entry modes. Section 3 details the study's methodological considerations: data gathering procedures, questionnaire, target firms (Portuguese firms that have internationalised to the PALOP), and the specification of the econometric model which aims to quantify the net impact of corruption on entry mode choice. In Section 4, the results of the econometric estimations are discussed and, finally, Conclusions summarises the main points of the research.

2 Corruption and MNC entry modes - literature review

International entry modes represent the third most-researched field in international management, being directly related to the international activity of MNCs (Canabal & White, 2008). Entry modes vary largely in their scale of entry (Peng, 2009), and are generally divided into two categories: equity and non-equity (Tian, 2007).

Equity entry modes include joint ventures and wholly-owned subsidiaries. The former consist in a sharing arrangement between a foreign MNC and a local firm, where resources, risk and operational control are divided between the partners (Julian, 2005), whereas the latter may involve both greenfield investments, which include establishing a new firm, and acquisitions of already existing firms (Razin & Sadka, 2007). Equity modes require a very high resource commitment, i.e. the scale of entry, because direct establishment takes place in the foreign market (Hill & Jones, 2009).

Non-equity modes include exports and contractual agreements like licensing, franchising, turnkey projects and R&D contracts. In this case, the scale of entry is lower because relations with the foreign market do not imply direct establishment (Peng, 2009).

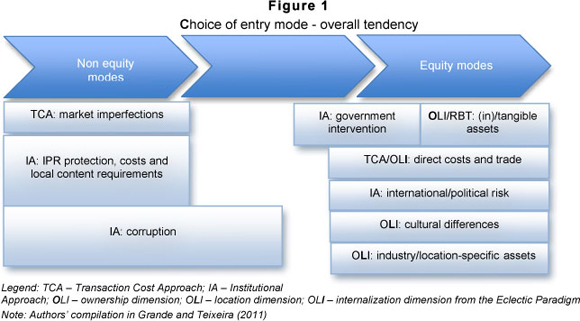

A MNC's choice of market entry mode depends on several determinants. It is thus important to review the theories on FDI and MNCs that intend to explain why firms become involved in several types of internationali-sation processes. In general, the highly diversified theoretical approaches (e.g. early studies on FDI; the neoclassical trade theory; ownership (O), location (L) and internalization (I) framework - cf. Faeth, 2009), do not directly and explicitly aim to explain MNC entry modes but they focus instead on highlighting key determinants of foreign direct investment.1

By adapting the existing theoretical approaches to FDI and internationalisation, we intend to provide a distinct approach, mixing existing contributions with Transaction Cost Analysis (TCA) and Dunning's Eclectic Paradigm or OLI model. The latter is an integrated internationalisation model that draws inspiration from three different strands of business theory, namely competitive theory, in terms of ownership of strategic assets, international business theory, in terms of location advantages, and finally, TCA, in terms of internalisation issues. According to Dunning's Eclectic Paradigm, only by integrating the three perspectives can the international activities of MNCs be fully understood (Aspelund & Butsko, 2010) and their choice of entry mode rationalised (cf. Figure 1).

Based on the firms' abilities, it may be possible to connect the firm's competences, skills and assets from the resource-based theory (Hill & Jones, 2009) to Dunning's Eclectic Paradigm or the OLI framework (Luo, 1999). Accordingly, to take advantage of firm-specific assets (Madok, 1998; Sreenivas & Pangarkar, 2000), such as technology-intensive resources (Sun, 1999; Javorcik & Wei, 2009) and inventive/R&D-intensive activities (Bhaumik & Gelb, 2005; Chung, 2009), the most common entry mode is the establishment of wholly-owned subsidiaries (WOS). This is justified on the basis that firm-specific resources and activities need a high level of control (Edwards & Buckley, 1998; Chen & Hu, 2002), which would not be possible in a joint venture (JV), where knowledge has to be transferred to the partner (Chiao, Lo & Yo, 2010; Yiu & Makino, 2002; Martin & Salomon, 2003). Therefore, we put forward that:

Hypothesis 1: The higher the MNC's R&D intensity, the higher the likelihood of entry via FDI.

In line with Garcia and Fernandez (2009), who found a positive correlation between service-providing companies and entry through FDI, we maintain that service-related companies, as opposed to manufacturing ones, would be more inclined to opt for the FDI entry mode, given the nature of services -- immaterial, often information-intensive; hard to separate production from consumption; consumer-intensive, hard to store or transport (Toivonen & Tuominen, 2009).

Hypothesis 2: MNCs from the services sector are more likely to enter a foreign host country through FDI rather than through other nonequity modes.

MNCs with accumulated experience in inter-nationalisation are less likely to rely on the support of a joint venture partner, because they already have the required know-how to conduct business abroad (Mutinelli and Piscitello, 1998). In contrast, when MNCs do not have any experience, JVs can be used to complement internal R&D resources and to exchange knowledge on an inter-firm basis (Mutinelli & Piscitello, 1998). Consequently, we put forward that:

Hypothesis 3: The higher the MNCs ' international experience, the more likely the choice for FDI entry modes.

Although some studies did not find a statistically significant relationship between firm size and entry mode choices (Evans, 2002; Esperança, Hill & Valente, 2006), Demirbag et al. (2010) found that the larger the size of the operation, measured by the number of employees, the more likely the foreign investor will choose wholly-owned subsidiaries to enter a foreign market. According to Mutinelli and Piscitello (1998), small firms with a lack of resources, experience and information face a high level of uncertainty, which can be mitigated by lower levels of involvement in the host market, such as, for example, through non-equity modes. On the contrary, larger firms, usually possessing a higher amount of valuable tangible or intangible assets, may attract opportunistic joint venture partners or intermediaries, which may lead them to establish on their own. To test this argument, we put forward that:

Hypothesis 4: The larger the MNC, the more likely it will opt for FDI entry modes.

Besides the fact that most of the studies in this literature stream did not obtain a statistically significant correlation between the openness of the host economy and a specific entry mode (e.g. Javorcik & Wei, 2009), there are studies that suggest a positive correlation between openness and FDI (Chang & Rosenzweig, 2001). They argue that trade barriers (i.e. a low level of economic openness) should lead to a lower share of exports in the market, and consequently, the market share of imports in a host country can be seen as a factor that encourages high resource-commitment modes. Therefore, we put forward that:

Hypothesis 5: The more open the host economy, the more likely the MNC's choice for FDI entry modes.

Some studies on the determinants of MNCs' entry modes find a positive correlation between the host market size and FDI inflows. Cuervo-Cazurra (2008) obtained high levels of correlation among the variables related to the characteristics of a country (such as GDP and population). In line with these results, Uhlenbruck et al. (2006), when analysing 220 telecommunication projects in 64 emerging economies, also controlled for GDP per capita and obtained a positive correlation with FDI inflows. Accordingly, we put forward that:

Hypothesis 6: The larger the host market, the more likely the MNC will opt for FDI entry modes.

Cultural distance is a dominant determinant of entry mode choice. According to Chen and Hu (2002:196) "[c]ulture is shared values and beliefs. Cultural distance is the difference in these values and beliefs shared between home and host countries. Large cultural distances lead to high transaction costs for multinationals investing overseas".

Studies focusing on FDI flows and/or entry mode choices often obtain a statistically significant correlation when it comes to culture-measuring variables. Cornelius (2005) attempted to shed some light on the quality of governance practices in a large sample of countries and the extent to which that quality could offset perceived weaknesses in the institutional framework in which companies operate. And indeed the perceptions of the quality of corporate governance appear to be consistent with his assumptions. Most importantly, though, he identified important outliers, suggesting that other factors such as political, cultural and historical roots also play an important role. Moreover, Strange, Filatotchev, Lien & Piesse (2009), when examining the FDI location strategies of firms from Taiwan in a rapidly emerging market (China), found that the efficacy of firms' external linkages varies according to the strength of the cultural and historical ties between the location of the foreign affiliate and the home country.

Hypothesis 7: When the home and host country share linguistic and historical ties, the more likely foreign investors are to enter via FDI rather than through non-equity modes.

Jiménez et al. (2011) aimed to analyse the impact of political risk variables in the location strategy of Spanish Multinational Enterprises (MNEs) in Europe. In this study, they collected evidence on the relevance of lower political constraints to attract investments. However, the results also highlighted the importance of cultural and geographical proximity, which may serve to overcome obstacles derived from higher corruption or lower economic freedom levels. In line with these findings, which suggest that the effect of cultural links may exceed the impact of other determinants, such as corruption, Cuervo-Cazurra (2008), when controlling for cultural similarities, found a positive correlation between a common language in host and home countries and FDI inflows, even when there is corruption in the host country. The findings of Demirbag et al. (2010) confirmed this correlation, when analysing 104 Turkish MNCs which invest in the culturally close Republics of Central Asia. They found that even in the presence of corruption, foreign MNCs reveal a preference for high levels of involvement in the host market, which they enter by means of wholly-owned subsidiaries. Thus, we put forward that:

Hypothesis 8: The higher the importance MNCs attribute to institutionally-related factors (e.g. legal restrictions and political stability), the higher its FDI propensity tends to be.

Since corruption is one of the most pervasive political problems worldwide, there has been considerable empirical research on its causes and effects in recent years (Frischmann, 2010; Goel & Nelson, 2010).2 The World Bank has estimated that more than 1 trillion USD is paid in bribes each year and that countries that fight corruption, improve governance and the rule of law, potentially increase per capita incomes by 400 per cent (Dreher, Kotsogiannis & McCorriston, 2007).

A large amount of research on the impact of corruption on the MNCs' choice of entry mode has found that corruption discourages the establishment of wholly-owned subsidiaries (WOS). The analysis by Uhlenbruck et al. (2006) of 220 telecommunications development projects in 64 emerging economies found that firms adapt to the pressures of corruption via short-term contracting and joint ventures, avoiding WOS. Javorcik and Wei (2009) studied how entry modes were affected by the extent of corruption in 22 Eastern and Central European countries and found that corruption reduces inward FDI and shifts the ownership structure towards joint ventures, to avoid excessive transaction costs related to corrupt government officials. Rodriguez et al. (2005) confirm this tendency arguing that, in the presence of both arbitrary and pervasive corruption, MNCs tend to enter by means of non-equity modes or joint ventures to avoid direct contact with corrupt government officials and to achieve legitimacy through networking activities. Furthermore, Demirbag et al. (2010), when analysing 104 Turkish MNCs investing in Central Asian countries, found that corruption generally leads to entry through joint ventures with local partners. An analysis of 231 entries by Dutch MNEs in 48 countries by Slangen and van Tulder (2009) offers support for these findings, arguing that MNCs often choose joint ventures over WOS to protect themselves from external uncertainties. This assumption is supported by Straub (2007) who state that countries with high political corruption are most frequently entered via non-equity modes.

However, not all empirical studies have found a clear-cut negative relationship between corruption and entry through WOS. For example, Taylor, Zou and Osland (2000) and Ahmed, Mohamad, Tan and Johnson (2002) argue that MNCs tend to opt for high control modes (WOS) when the risk of doing business in the host country is high. Henisz (2000) also found that in the presence of political risks, MNCs tend to choose WOSs to protect themselves from potentially manipulative joint venture partners. Another approach by Li and Rugman (2007) showed that MNCs prefer to enter markets with high uncertainty levels through WOSs because they contribute to reducing uncertainty. Therefore, we put forward that:

Hypothesis 9: The higher the host country's corruption level, the more likely foreign investors will opt for entry through non-equity modes.

3 Methodological considerations

Similarly to other studies which analyze the role of the several determinants of the MNCs' choice of entry mode (e.g. Uhlenbruck et al., 2006; Straub, 2007; Slangen & van Tulder, 2009), our study makes use of a multivariate econometric model, more specifically, a logistic regression to assess how corruption affects the firms' entry modes in countries characterised by widespread levels of corruption (the PALOP), and which maintain historical and linguistic affinities with the MNCs' home country (Portugal).

Based on the literature, the MNCs' choice of entry mode depends on four main groups of determinants, namely on the three dimensions of Dunning's Eclectic Paradigm (or OLI model) and the institutional approach.

Our 'dependent' variable, MNC entry mode, is a dummy which assumes the value 1 in cases where the firm opts for entry (in a given market) through FDI and 0 otherwise (nonequity modes).3

Given the nature of the dependent variable (binary), the empirical assessment of the MNCs' FDI propensity is based on the estimation of the general logistic regression, which in turn is based on the existing literature on the determinants of entry modes, surveyed in Section 2. In order to obtain a more straightforward interpretation of the logistic coefficients, a rearrangement of the logistic model's equation has to be considered, and it is rewritten in terms of the odds of an event occurring. Writing the logistic model in terms of the log odds, we obtain the following logit model:

The logistic coefficient can be interpreted as a change in the log odds associated with a one-unit change in the independent variable. Then, e raised to the power β is the factor by which the odds change when the ith independent variable increases by one unit. If β is positive, this factor will be greater than 1, which means that the odds are increased; if β is negative, the factor will be less than one, which means that the odds are decreased. When β is 0, the factor equals 1, which leaves the odds unchanged. In the case where the estimate of β emerges as positive and significant for the conventional levels of statistical significance (that is, 1 per cent, 5 per cent or 10 per cent), this means that, on average, all other factors remaining constant, the 'preferred' entry mode by Portuguese MNCs in countries/markets with higher perceived corruption levels is FDI, which would be in line with Hypothesis 9.

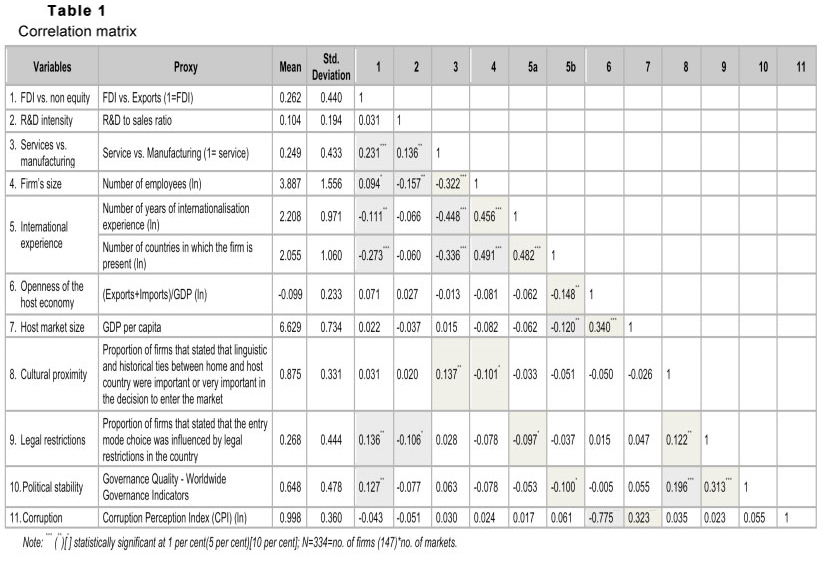

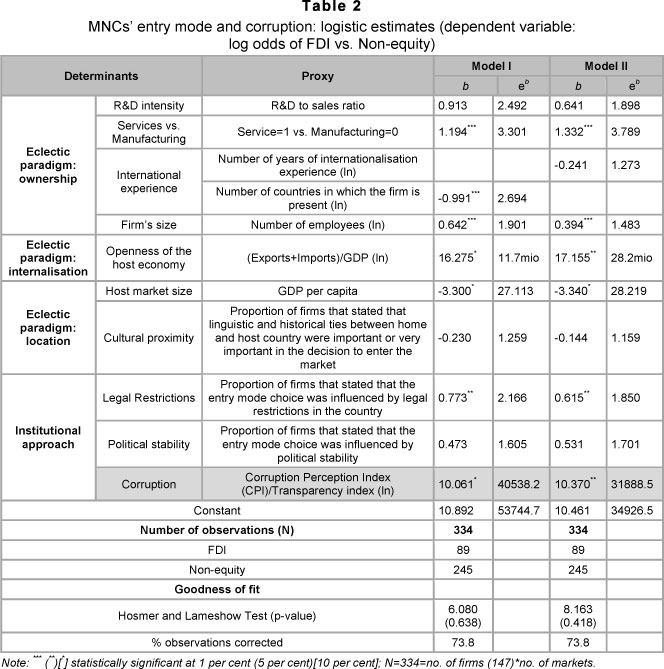

The descriptive statistics of the variables model and the matrix of correlations are presented in Table 1. The estimates of the β are given in Table 2.

Our unit of analysis is not the firm or the market but rather the firm and the market - the same firm can internationalise to a single country or to all the (5) countries (Angola, Cape Verde, Guinea Bissau, Mozambique, and Sao Tome Principe) in analysis.

The population surveyed included all (562) the Portuguese firms that have internationalised to the 5 PALOP countries, according to AICEP Portugal Global (a government business entity focused on FDI and the inter-nationalisation of Portuguese companies).4

A direct email questionnaire was built and sent to all these firms. Questions covered not only the firms' main characteristics but also aspects regarding their entry modes in each market under analysis (depending on whether they had in fact entered) and their perceptions of some key institutional factors (specifically, the importance of legal restrictions, linguistic and historical ties, and the impact of corruption in the choice of entry mode).

Around a quarter of the surveyed firms answered the questionnaire and, considering that 65 per cent had internationalised to more than one PALOP country, 321 valid responses were obtained.

The descriptive results (cf. Table 1) based on the survey's sample suggest that the Portuguese MNCs' 'propensity' for FDI as the 'preferred' entry mode in PALOP countries is positively and significantly related to firm size and the importance attributed to legal restrictions and political stability. That is, in a bivariate statistical analysis, larger MNCs and those that perceive legal restrictions and political stability as key factors when choosing their entry mode, tend on average to opt for equity-based entry modes (i.e. FDI), instead of exports and/or contracting. In contrast, firms with higher international experience, as measured by the number of countries to which they have internationalised or the number of years since they first internationalised, tend to opt for non-equity entry modes, namely exports.

Regarding the relationship between the independent variables, the results show that the years of internationalisation experience and number of countries to which the firm has internationalised are positively and significantly related, revealing that firms which have internationalised to a larger number of countries tend to have started their internationalisation processes much earlier. Given this high correlation, it was advisable to estimate the 'theoretical' model using one of the two proxies of internationalisation experience. Thus, we estimated Model I (cf. Table 2) using 'number of countries in which the firm is present' as the proxy for internationalization experience, whereas in Model II, the 'number of years of internationalisation experience' was used.

Although some correlations between the independent variables are strong (namely, between the corruption perception index and the openness indicator - see Table 1), these are not high enough to undermine the estimation of the proposed model.

4 Econometric results

According to the goodness-of-fit measures (Hosmer & Lameshow test and percentage corrected), the two estimated models represent 'reality' quite well. Table 2 presents the results of our logistic estimates.

Considering the results related to the control variables included in our models, statistical evidence was not found to sustain a correlation between the MNCs' R&D intensity and a specific entry mode (i.e. Hypothesis 1 is not corroborated). In contrast, sector dimension emerged as a statistically significant variable. Thus, our results support Hypothesis 2. Specifically, estimates indicate that MNCs from the Services sector tend to present an odds for FDI 3 times higher (e1.194=3.301) than that of their Manufacturing counterparts.

Quite unexpectedly, and in contrast to the literature (e.g., Mutinelli & Piscitello, 1998; Chiao et al., 2010), Hypothesis 3 was not supported. The international experience of Portuguese MNCs is negatively related with the (log odds of) FDI 'propensity', meaning that firms with higher international experience tend to enter the PALOP markets mainly by way of exports. As noted by Slangen and van Tulder (2009) in their study, this may be due to the fact that MNCs tend to enter new markets by the same method/mode with which they entered other markets previously - i.e. when a firm has experience in entering markets via exports, it is more likely that subsequent internationalisation processes will take the same path.

As expected, the larger Portuguese MNCs tend, on average, ceteris paribus, to choose FDI as their preferred entry mode in the PALOP. Thus, Hypothesis 4 is corroborated, which reflects the finding of Demirbag et al. (2010) that the higher the number of employees (in their case, as a proxy for the size of operation), the more likely the foreign investor will choose an equity entry mode.

In contrast to some of the existing literature (e.g. Javorcik & Wei, 2009) where the economy's openness does not appear to have a statistically significant effect on the choice of entry mode, in this study, the country's openness indicator emerges as quite relevant. The estimate coefficient of market openness, which stands as a proxy for the host countries' reception of trade and commerce, reveals that, on average, all other factors remaining constant, markets which are relatively more open (reflecting lower transaction costs) tend to be associated with FDI modes of entry. Summing up, Hypothesis 5 holds.

The location dimension received median support from our data. Indeed the size of the market, proxied by the host country's GDP per capita, emerged as negatively and significantly related with FDI propensity, which contradicts Hypothesis 6. This suggests that, on average, Portuguese MNCs entering larger markets tend to fall back on non-equity modes (namely exports). Such results contradict findings in the existing literature (Horstmann & Markusen, 1996; Eicher & Kang, 2005), which in general claim that the larger the market size the higher the probability of entering via high equity modes. Cultural proximity (Hypothesis 7), reflected by the proportion of MNCs that stated that linguistic and historical ties between home and host country were important or very important in the decision to enter the market, failed to emerge as significant.

The estimations put forward highlight the crucial role of institutional factors (Hypothesis 8) in explaining the MNCs' entry modes. Indeed, legal restrictions and, most importantly, the host country's level of corruption are statistically significant elements related with the MNC's choice of entry mode. In effect, the Portuguese MNCs that perceive legal restrictions as very important in their choices regarding the entry mode in the PALOP tend, on average, to have a higher propensity for FDI entry modes.

Finally, the estimations support Hypothesis 9, indicating a positive correlation between the CPI (transparency index) and an FDI entry. This means that, controlling for all the other factors which are likely to affect entry mode choices, Portuguese MNCs tend to opt for direct investment in the more transparent/less corrupted markets. Thus, our results are in line with the general tendency conveyed in the literature (e.g., Rodriguez et al., 2005; Uhlenbruck et al., 2006; Straub, 2007; Paul & Wooster, 2008), which contends that MNCs should prefer non-equity entry modes in corrupt contexts.

5 Conclusions

The present paper intended to analyse how Portuguese MNCs' choice of the most appropriate entry mode is affected by the level of corruption in host countries, namely with regard to the PALOP countries.

Based on a multivariate econometric model, we found that services and larger firms have a preference for high-equity entry modes, which contrasts with the size dimension in the study of Esperança et al.'s (2006), and may be explained by the fact that they analyzed a set of different host countries. While Esperança et al. (2006) focused on Portuguese MNCs which invest in Spain, our study analysed firms from the same home country but which have internationalised to emerging African countries with very different characteristics, namely the levels of corruption, political restrictions, and economic and political instability. These and other factors, such as physical proximity, may explain why the results point in different directions.

Additionally, we found that the openness of the host market favours entry via FDI, which is somewhat surprising, since this determinant did not appear to have a statistically significant effect in previous studies focusing on other (central and eastern European) emerging markets like, for exemple, Javorcik and Wei (2009). Also in contrast with the existing literature (e.g. Horstmann and Markusen, 1996), the host market size emerged as negatively related to the equity mode propensity, such that a (Portuguese) MNC is more likely to enter via exports in larger (PALOP) markets. Finally, we found that international experience is not, as would be expected, associated with high equity modes. As noted by Slangen and van Tulder (2009), this may be due to the fact that MNCs tend to enter new markets by the same method/mode with which they entered other markets previously - i.e. firms with experience in entering markets via exports are more likely to follow the same path in subsequent internationalisation processes.

In line with prior studies that point out the firms' general preference for non-equity modes when entering corrupt markets (e.g. Rodriguez et al., 2005; Uhlenbruck et al., 2006; Straub, 2007; Paul & Wooster, 2008), our results show that, on average, Portuguese firms opt for nonequity modes, most specifically exports, when entering more corrupted countries. Recall that, according to Uhlenbruck et al. (2006), MNCs use non-equity modes as an adaptive strategy because this entry mode provides an opportunity to participate in economies where corruption is high while avoiding some of the costs related to corruption. Non-equity modes also enable the MNCs to avoid direct contact with corrupt practices, such as bribes (Rodriguez et al., 2005). Apart from bribes and extra taxes, direct establishment in a corrupt market may affect the MNCs' investment through their interaction with corrupt state officials. This increases the risk of expropriation and reduces the informational advantage a firm entering via FDI may have (Straub, 2007).

Based on these results, we failed to corroborate the arguments put forward in the studies mentioned previously. Indeed, despite the fact that the vast majority of the firms (about 90 per cent of our sample) underlined the importance of cultural ties with the PALOP countries, perceived corruption emerged negatively and significantly correlated with the FDI propensity. In other words, the PALOP countries characterised by a lower level of perceived corruption tend to be the most successful in attracting foreign direct investment. Thus, we have shown that in the PALOP too, high levels of institutional quality tend to foster economic growth and development through its positive effects on FDI attraction.

Summing up, our findings highlight that, despite the existence of strong cultural ties between home (Portugal) and host countries (PALOP), corruption stands as a critical obstacle to foreign direct investment. Recall that, with the exception of Cape Verde, all the other PALOP countries present very low levels of transparency (with a CPI below 3 out a maximum of 10). Given the perceived widespread corruption among the PALOP, our findings reflect a rather troubling scenario for these countries' prospects for future growth.

Our study clearly emphasises that historical and cultural ties are not sufficient to overcome the costs of institutional weaknesses, namely the perceived widespread corruption. We draw on Lawal's (2007) words when she maintains that corruption has been an impediment to the true and real development of African society. Thus, in order to benefit from the potential benefits of foreign capital, which contributes to economic development and integration in the global economy (Shrestha, Smith & Evans, 2010), African countries in general, and the PALOP in particular, should implement serious measures to combat corruption, building a strong political system that inspires confidence and attracts foreign investors.

Endnotes

1 In an earlier research proposal from the authors (Grande and Teixeira, 2011) these literature approaches are surveyed and presented with further detail and scope. Although in this paper no empirical tests are pursued, the authors provide an in-depth account of the determinants of MNC's entry mode choices according to each theoretical approach (Transaction Cost Approach, Ecletic Paradigm - Ownership, Location, Internalisation, Institutional) which help to support/rationalise Figure 1.

2 There are many definitions of this phenomenon (Detzer, 2010). However, there is relative consensus among authors (Dey, 1989; Mauro, 1998; Treisman, 2000; Dietrich, 2010; Reiter & Steensma , 2010) that corruption refers to acts in which the power of public office is used for personal gain in a manner that contravenes the rules of the game (Jain, 2002).

3 We opted to compare FDI versus non-equity modes instead of considering each entry mode (acquisition, greenfield investment, joint venture, etc.) given that the majority of the firms surveyed had very few observations for each specific equity-entry mode.

4 The original database had 653 firms but 46 firms claimed they did not have any presence in the PALOP countries, and in 45 cases the email did not reached the recipient. Thus, our 'effective' population is 562 firms.

References

AHMED, Z.U., MOHAMAD, O., TAN, B. & JOHNSON, J.P. 2002. International risk perceptions and mode of entry: a case study of Malaysian multinational firms. Journal of Business Research, 55(10):805-813. [ Links ]

ASPELUND, A. & BUTSKO, V. 2010. Small and middle-sized enterprises' offshoring production: a study of firm decisions and consequences. Tijdschrift voor Economische en Sociale Geografie, 101(3):262-275. [ Links ]

BHAUMIK, S.K. & GELB, S. 2005. Determinants of entry mode choice of MNCs in emerging markets: evidence from South Africa and Egypt. Emerging Markets Finance and Trade, 41(2):5-24. [ Links ]

CANABAL, A. & WHITE, G.O. 2008. Entry mode research: past and future. International Business Review, 17(3):267-284. [ Links ]

CHANG, S.-J. & ROSENZWEIG, P. 2001. The choice of entry mode in sequential foreign direct investment. Strategic Management Journal, 22(8):747-776. [ Links ]

CHEN, H. & HU, M.Y. 2002. An analysis of determinants of entry mode and its impact on performance. International Business Review, 11(2): 193-210. [ Links ]

CHIAO, Y.-C., LO, F.-Y. & YU, C.-M. 2010. Choosing between wholly-owned subsidiaries and joint ventures of MNCs from an emerging market. International Marketing Review, 27(3):338-365. [ Links ]

CHUNG, M.-F. 2009. Multinational firms' entry mode: technology spillovers in an intra-industry differentiated product market. International Research Journal of Finance and Economics, 1(28):187-197. [ Links ]

CORNELIUS, P. 2005. Good corporate practices in poor corporate governance systems: Some evidence from the Global Competitiveness Report, Corporate Governance, 5(3):12-13. [ Links ]

CUERVO-CAZURRA, A. 2008. Better the devil you don't know: Types of corruption and FDI in transition economies, Journal of International Management, 14(1):12-27. [ Links ]

DEMIRBAG, M., MCGUINNESS, M. & ALTAY, H. 2010. Perceptions of institutional environment and entry mode, FDI from an emerging country. Management International Review, 50(2):207-240. [ Links ]

DEY, H.K. 1989. The genesis and spread of economic corruption: a microtheoretic interpretation. World Development, 17(4):503-511. [ Links ]

DETZER, D. 2010. The impact of corruption on development and economic performance. Norderstedt: GRIN Verlag. [ Links ]

DIETRICH, S. 2010. The politics of public health aid: why corrupt governments have incentives to implement aid effectively. World Development, 39(1):55-63. [ Links ]

DREHER, A., KOTSOGIANNIS, C. & MCCORRISTON, S. 2007). Corruption around the world: Evidence from a structural model. Journal of Comparative Economics, 35(3):443-466. [ Links ]

EDWARDS, R.W. & BUCKLEY, P.J. 1998. Choice of location and mode: the case of Australian investors in the UK. International Business Review, 7(5):503-520. [ Links ]

EICHER, T. & KANG, J.W. 2005. Trade, foreign direct investment or acquisition: optimal entry modes for multinationals. Journal of Development Economics, 77(1):207-228. [ Links ]

ESPERANÇA, J.P., HILL, M.M. & VALENTE, A.C. 2006. Entry mode and HRM strategies of emerging multinationals: an empirical analysis of Portuguese firms entering the Spanish market. International Journal of Organizational Analysis, 14(4):260-276. [ Links ]

EVANS, J. 2002. Internal determinants of foreign market entry strategy. Manchester: Manchester Metropolitan University Business School. [ Links ]

FAETH, I. 2009. Determinants of foreign direct investment . A tale of nine theoretical models. Journal of Economic Surveys, 23(1):165-196. [ Links ]

FRISCHMANN, E. 2010. Decentralization and corruption: a cross-country analysis. Norderstedt: GRIN Verlag. [ Links ]

GARCÍA, V.B. & FERNANDEZ, J.C. 2009. La internalización de la franquicia espanola y sus formas de penetración de mercados. Cuadernos de Economia y Dirección de la Empresa, 40:47-82. [ Links ]

GOEL, R.K. & NELSON M.A. 2010. Causes of corruption: History, geography and government. Journal of Policy Modeling, 32(4):433-447. [ Links ]

GRANDE, M. & TEIXEIRA, A.A.C. 2011. Corruption and MNCs' entry mode. An empirical econometric study of Portuguese firms investing in PALOPs. Economics and Management Research Projects: An International Journal, 1(1):36-52. [ Links ]

HENISZ, W.J. 2000. The institutional environment for multinational investment. Journal of Law, Economics, and Organization, 16(2):34-364. [ Links ]

HILL, C. & JONES, G. 2009. Foreign direct investment: analysis of aggregate flows. Mason: South Western Cengage Learning. [ Links ]

HORSTMANN, I.J. & MARKUSEN, J.R. 1996. Exploring new markets: direct investment, contractual relations and the multinational enterprise. International Economic Review, 37(1):1-19. JAIN, A.K. 2002. Corruption: a review. Journal of Economic Surveys, 15(1):71-121. [ Links ] [ Links ]

JAVORCIK, B.S. & WEI, S.-J. 2009. Corruption and cross-border investment in emerging markets: firm-level evidence. Journal of International Money and Finance, 28(4):605-624. [ Links ]

JIMENEZ, A., DURÁN, J.J. & DE LA FUENTE, J.M. 2011. Political risk as a determinant of investment by Spanish multinational firms in Europe. Applied Economics Letters, 18(8):789-793. [ Links ]

JULIAN, C.C. 2005. International joint venture performance in South East Asia. Northampton: Edward Elgar Publishing Limited. [ Links ]

LAWAL, C. 2007. Corruption and development in Africa: challenges for political and economic change. Humanity and Social Sciences Journal, 2(1): 1-7. [ Links ]

LI, J. & RUGMAN, A.M. 2007. Real options and the theory of foreign direct investment. International Business Review, 16(6):687-712. [ Links ]

LUO, Y. 1999. Entry and cooperative strategies in international business expansion. Westport: Greenwood Publishing Group. [ Links ]

MADOK, A. 1998. The nature of multinational firm boundaries: Transaction costs, firm capabilities and foreign market entry mode. International Business Review, 7(3):259-290. [ Links ]

MARTIN, X. & SALOMON, R. 2003. Knowledge transfer capacity and its implications for the theory of the multinational corporation. Journal of International Business Studies, 34(4):356-373. [ Links ]

MAURO, P. 1998. Corruption and the composition of government expenditure. Journal of Public Economics, 69(2):263-279. [ Links ]

MUTINELLI, M. & PISCITELLO, L. 1998. The influence of firm's size and international experience on the ownership structure of Italian FDI in manufacturing. Small Business Economics, 11(1):43-56. [ Links ]

PAUL, D.L. & WOOSTER, R.B. 2008. Strategic investments by US firms in transition economies. Journal of International Business Studies, 39(2):249-266. [ Links ]

PENG, M.W. 2009. Global strategy. Mason: South Western Cengage Learning. [ Links ]

RAZIN, A. & SADKA, E. 2007. Foreign direct investment: analysis of aggregate flows. New Jersey: Princeton University Press. [ Links ]

REITER, S.L. & STEENSMA, H.K. 2010. Human development and foreign direct investment in developing countries: the Influence of FDI policy and corruption. World Development, 38(12):1678-1691. [ Links ]

RODRIGUEZ, P. UHLENBRUCK, K. & EDEN, L. 2005. Government corruption and the entry strategies of multinationals. Academy of Management Review, 30(2):383-396. [ Links ]

SANTISO, J. 2007. Africa: an emerging markets frontier. OECD Observer, 21st December. Available at: http://www.oecdobserver.org/news/ullstory.php/aid/2350/Africa:_an_emerging_markets_frontier_.html [accessed 2011-04-19]. [ Links ]

SHRESTHA, N.R., SMITH, W.I. & EVANS, C.E. 2010. Africa's global economic integration and national development: a management framework for attracting FDI. Journal of Management Policy and Practice, 11(5):34-48. [ Links ]

SLANGEN, A.H.L. & VAN TULDER, R.J.M. 2009. Cultural distance, political risk, or governance quality? Towards a more accurate conceptualization and measurement of external uncertainty in foreign entry mode research. International Business Review, 18(3):276-291. [ Links ]

SREENIVAS RAJAN, K. & PANGARKAR, N. 2000. Mode of entry choice: an empirical study of Singaporean multinationals. Asia Pacific Journal of Management, 17(1):49-66. [ Links ]

STRANGE, R., FILATOTCHEV, I., LIEN, Y.-C. & PIESSE, J. 2009. Insider control and the FDI location decision evidence from firms investing in an emerging market. Management International Review, 49(4): 433-454. [ Links ]

STRAUB, S. 2007. Opportunism, corruption and the multinational firm's mode of entry. Journal of International Economics, 74(2):245-263. [ Links ]

SUN, H. 1999. Entry modes of multinational corporations into China's market: a socioeconomic analysis. International Journal of Social Economics, 26(5-6):642-659. [ Links ]

TAYLOR, C.R., ZOU, S. & OSLAND, G.E. 2000. Foreign market entry strategies of Japanese MNCs. International Marketing Review, 17(2):146-163. [ Links ]

THE ECONOMIST 2010. South of the Sahara 22nd November. Available at: http://www.economist.com/node/17493372?story_id=17493372 [accessed 2011-4-19]. [ Links ]

TIAN, X. 2007. Managing international business in China. Cambridge: Cambridge University Press. [ Links ]

TOIVONEN, M. & TUOMINEN, T. 2009. Emergence of innovations in services. The Service Industries Journal, 29(7):887-902. [ Links ]

TRANSPARENCY INTERNATIONAL 2009. Corruption perceptions index 2009. Available at: http://www.transparency.org/policy_research/surveys_indices/cpi/2009/cpi_2009_table, [accessed 2010-10-16]. [ Links ]

TREISMAN, D. 2000. The causes of corruption: a cross-national study. Journal of Public Economics, 76(3):399-457. [ Links ]

UHLENBRUCK, K., RODRIGUEZ, P., DOH, J. & EDEN, L. 2006. The impact of corruption on entry strategy: evidence from telecommunication projects in emerging economies. Organization Science, 17(3):402-414. [ Links ]

YIU, D. & MAKINO, S. 2002. The choice between joint venture and wholly owned subsidiary: an institutional perspective. Organization Science, 13(6):667-68. [ Links ]

Accepted: November 2011

{kind=link}

{kind=link}