Services on Demand

Article

English (pdf)

English (pdf)

Article in xml format

Article in xml format Article references

Article references

Indicators

Related links

-

Cited by Google

Cited by Google -

Similars in Google

Similars in Google

Share

Permalink

PermalinkSouth African Journal of Economic and Management Sciences

On-line version ISSN 2222-3436

Print version ISSN 1015-8812

S. Afr. j. econ. manag. sci. vol.14 n.4 Pretoria Jan. 2011

A comparison of ethical perceptions of earnings management practices

Leonie Jooste

School of Accounting, Nelson Mandela Metropolitan University

ABSTRACT

In 1990, Bruns and Merchant (1990) surveyed earnings management practices and asked the readership of the Harvard Business Review to rate the acceptability of those practices. Prior to the Bruns and Merchant (1990) study, the morality of short-term earnings management was of little concern to researchers and accounting practitioners. However, in the light of increased financial frauds and failures, new and increased emphasis has been placed on the importance of the concepts of earnings quality and earnings management practices.

Despite increased research focusing on business ethics since 1990, there is little evidence that business schools and the profession are educating accountants about earnings management practices. Therefore, this study, similar to other studies, continues to use the Bruns and Merchant survey and compares the results of studies on students and business managers on earnings management practices. Students and business managers were surveyed at the Nelson Mandela Metropolitan University (NMMU) and these results were compared to four studies prior to the Sarbanes-Oxley Act 2002 in the US. The expectation will be of changes in attitudes towards earnings management since the financial scandals and passing the Act. Therefore, the aim of the study is to determine if there have been changes in attitudes towards earnings management practices. No surveys using the Bruns and Merchant (1990) questionnaire are available in SA. Therefore, the study in SA was compared to available studies in the US.

Keywords: Bruns and Merchant study, business managers, business schools, earnings management, ethics, students

JEL: M14, 41

1 Introduction

Bruns and Merchant (1990) was the first to conduct a survey of the readership of the Harvard Business Review on the acceptability of practices in earnings management. The survey required the readers to rate the acceptability of 13 earnings management practices. The authors were shocked by the results and observed that where a practice is not explicitly prohibited or where there is a slight deviation from the rules, it seems that it becomes an ethical practice regardless of who might be affected by the practice or the information that flows from it (Bruns & Merchant, 1990). This means that anyone who uses information on short-term earnings is vulnerable to misinterpretation, manipulation, or deliberate deception as some of the earnings management practices can be immoral and unethical (Bruns & Merchant, 1990).

In later years, companies like Enron and WorldCom that were once viewed as icons and symbols of success became images of greed and unethical behaviour. As a result of the financial scandals and fraud of these companies and the subsequent demise of Arthur Anderson, business ethics has become a much researched and discussed topic. Business ethics has not only revived academics' and accounting practitioners' interest in ethics and earnings management practices but it also supports the view that there is a lack of ethics and ethical behaviour on the part of businesses and management (Karassavidou & Glaveli, 2006). Rather, in many companies, there is a concern for the bottom line or 'making the numbers' which seems to override any concern for ethical values (Verschoor, 2002).

Public confidence in the accounting profession has been shaken by the financial frauds and failures in these companies and the fraud charges brought against management. For its 2002 Annual Meeting, the American Accounting Association chose the Quality of Earnings Project as its main theme and, in turn, academic journals have invited and published research articles that focus on earnings management practices (Giacomino & Akers, 2006). Following the scandals, the United States (US) Congress passed the Sarbanes-Oxley Act of 2002 (South Africa followed with Corporate Governance) that holds executives personally responsible and criminally liable for certifying financial statements (Elias, 2004).

Earnings management and business ethics also has implications for academia. Leading accounting associations, since the 1990s, have called for increased emphasis on ethics education in accounting curricula. They recommend that business and accounting curricula should emphasise ethical values by integrating their development with the acquisition of knowledge and skills to help prevent, detect, and deter fraudulent financial reporting (Fischer & Rosenzweig 1995). Therefore, the purpose of this study is to determine whether the ethical perceptions of a survey in South Africa (SA) differ from surveys in the USA that used the Bruns and Merchant (1990) study prior to the introduction of the Sarbanes-Oxley Act in the US and Corporate Governance in South Africa. The aim is to determine whether the demand for and introduction of courses in ethics in business schools changes the ethical perceptions of students and business managers.

2 The research problem

As scandals of public companies come more to the fore one realises that people, and not accounting, are responsible for the major losses suffered by innocent people. Business schools, which are considered a basic source of providing managers and entrepreneurs, seem to be blamed for much of the unethical behaviour in business (Karassavidou & Glaveli, 2006).

However, earnings management is not a new phenomenon and has been used for many years. Since the seventies researchers stressed the importance of ethics in accounting. Bernstein and Siegel (1979) agree that earnings figures should have integrity and should not be the product of manipulations designed purely to increase the reported income of an entity. Earnings should also be reliable and provide a good indication of the earning power of the company. Since then, many cases of financial fraud and failure in companies have come to light throughout the world. The failure of a company is not simply a matter of accounting and auditing but the involvement of a convergence of factors including personal values, integrity and ethics (Akers, Eaton & Giacomino, 2004).

The problem with earnings management practice is that it also has consequences for accounting educators. They are the main suppliers of business managers. Educators should attempt to minimise the difference between students and business managers as conflicting opinions begin to develop during undergraduate business education. This results in students often adopting the attitudes of their professional reference groups before they even commence their professional careers (Giacomino & Akers, 2006).

This study therefore compares a recent survey on the ethical perceptions of students and business managers and compares it to four similar surveys (Clikeman, Greiger & O'Connell, 2001; Fischer & Rosenzweig, 1995; Rozenzweig & Fisher, 1994; Merchant & Rockness, 1994) performed in the US prior to the introduction of the Sarbanes-Oxley Act. The aim is to determine whether the introduction of the Act and educational interventions in business ethics courses effectively improved the ethical perceptions and skills of accounting students and practitioners.

3 Purpose of the study

Research has focused on detecting earnings management practices but the ethical perceptions of students and business managers are also important. The question is how a student will react when confronted with an ethical conflict in the business world. Therefore, the purpose of this study is to compare a survey on ethical perceptions of selected earnings management practices in SA with surveys performed in US prior to the introduction of the Sarbanes-Oxley Act in 2002. Sufficient time has passed since the publicity of cases such as Enron and WorldCom that changes in the views on the morality of earnings management may be expected throughout the world.

4 Literature study

Defining earnings management

Earnings management has been practiced for many years. It occurs when managers use judgement in financial reporting and in structuring transactions to alter financial reports either to mislead some stakeholders about the underlying economic performance of the company or to influence contractual outcomes that depend on reported accounting numbers (Healy & Wahlen, 1999).

This definition focuses on the exercise of judgement in financial reports to mislead stakeholders who either do not or cannot do earnings management and also to make financial reports more informative to users. There is therefore a good and a bad side to earnings management. The bad side is the cost created by misallocation of resources and the good side is the potential improvements in management's credible communication of private information to external stakeholders, improving resources allocation decisions.

Belkaoui (2004) agrees that various definitions have been offered to explain earnings management as a special form of 'designed' rather than 'principled' accounting. Earnings management may be seen as a purposeful intervention in the external reporting process with the intent of obtaining some private gain by either a selection of accounting methods within GAAP or by applying given methods in particular ways (Belkaoui, 2004).

Earnings management may also be seen from either an economic (or true) income perspective or an informational perspective. The true income perspective assumes firstly the existence of a true economic income which is distributed by a deliberate earnings management and/or by measurement errors embedded in accounting rules, and secondly as noisy unmanaged earnings acquire through earnings management of new properties in terms of amount, bias or variance. However, the informational perspective assumes that earnings is one of the signals used for decisions and judgements, and furthermore that managers have private information which they can use when they choose elements within GAAP under different sets of contracts which determine their conversation and behaviour (Belkaoui, 2004).

Managers manage earnings through their choices of accounting policies, judgements, or their timing or selection of operating decisions. Furthermore, managers' actions are related to a number of their incentives. In this regard, an association was found between accounting accruals and the incentives managers received from earnings-related bonus plans. Managers also have a tendency to decrease earnings when earnings are extreme in either direction, or to overstate earnings because they have not been performing well, or to boost earnings by squeezing reserves (Merchant & Rockness, 1994).

Earnings management activities include accounting-based activities or operating-based activities. As an example of an accounting method, a manager may unjustifiably adjust the amount of a reserve thereby changing income. On the other hand, when a manager postpones discretionary expenses into the future in order to improve current income, it will be an example of an operating method (Kaplan, 2001).

Not all earnings management actions are illegal and many are within the manager's prerogatives. The ethical perspective, however, raises the question as to whether it is the right thing to do. Although an individual's moral code should prevent earnings management actions, if it does not, the individuals engaging in these actions are acting in a socially unacceptable way (Merchant & Rockness, 1994).

Ethics in the accounting curriculum

The Treadway Commission (Cohen & Pant, 1989), called for changes in accounting education that would increase the extent to which ethical issues are incorporated into classroom practices. The Commission argued that the responsibility of the accounting profession and their accountability to the public requires a much broader exposure to ethics. Business schools should include ethics discussions in every accounting course and, ideally, it should be part of all business courses. Business and accounting curricula should emphasise ethical values by integrating their development with the acquisition of knowledge and skills to help prevent, detect and deter fraudulent financial reporting (Cohen & Pant, 1989).

Fisher and Rosenzweig (1995) also supported the Treadway Commission to address their concerns by identifying specific topics in ethics and accounting for curricular development. Earnings management practices are one such topic to be included because of ethical ambiguities associated with these practices. If the educational curricula of accountants and managers can inculcate ethical sensitivity to earnings management, then perhaps it can help to reduce the tendency to engage in these practices (Fischer & Rosenzweig, 1995).

It is therefore important for educators to be familiar with current attitudes of students towards earnings management practices if they are interested in integrating ethical concerns into accounting programs. In response to this concern, many business schools have begun to review the role of ethics in their curricula and many have initiated new business ethics courses, developed cases, conducted workshops and seminars to put the spotlight on the need for principled leadership. Woo (2003) stresses that one of the primary goals of educators should be to help students understand how they might react when presented with an ethical conflict, no matter how big or small.

Karassavidou and Glaveli (2006) believe that a lack of ethics and ethical behaviour on the part of businesses, leaders and managers seems to pervade the societies universally having a direct outcome on leadership and organizational effectiveness, employees' job satisfaction and turnover, orginisational justice and in general on businesses' ability to compete, create jobs and contribute to a country's economic development and social prosperity. Furthermore, the authors blame business schools for much of the unethical behaviour in business because they are considered the basic source of providing leaders, managers and entrepreneurs. Therefore, many universities and business schools are increasingly requiring form their students to take courses in business ethics (Karassavidou & Glaveli, 2006).

Chang and Leung (2006) agree that whilst much research has concentrated on ethical reasoning and ethics education to enhance the ethical conduct of accountants, it is also important that the profession and researchers also direct their attention and efforts to cultivating the ethical sensitivity of accountants.

Surveys in earnings management

In response to corporate scandals and the loss of confidence in the accounting profession, researchers embarked upon similar research as Bruns and Merchant (1990) in earnings management practice and corporate-ethical values. Bruns and Merchant (1990) prepared a 13-action questionnaire that consisted of practices that the authors considered short-term earnings management practices. This questionnaire was used by Merchant and Rockness (1994) where general managers, staff managers, operation-unit controllers, and internal auditors were sampled in two entities. In their study, accounting manipulations were judged more harshly.

Rosenzweig and Fischer (1994) found that respondents with more years of experience and higher levels of responsibility (partners) judged practices less harshly than accountants with less than six years experience and at the entry and junior levels.

Fischer and Rosenzweig (1995) surveyed undergraduate students, MBA students, and practicing accountants on their attitudes on the ethical acceptability of earnings management practices and found that operating manipulations were judged less ethically by accounting practitioners. Clikeman et al. (2001) surveyed students and made comparisons by culture, based on national origin and gender. However, in their study, no significant differences were found. Furthermore, Elias (2004) surveyed certified public accountants (CPAs) and reported on their low perceptions of corporate ethical values.

Kaplan (2001) did not utilise the Bruns and Merchant (1990) questionnaire. He presented two groups of respondents, managers and shareholders, with only three earnings management actions. It involved an operating activity gain through deferral of discretionary expenses, an accounting activity gain by requesting an invoice from a consulting firm to be delayed, and an accounting activity loss through an unnecessary increase in the obsolescence reserve. The results indicated that managers rated operating manipulations more ethically than accounting manipulations, whereas the shareholders rated both as unethical.

Another survey was performed by Karassavidou and Glaveli (2006). They investigated the ethical orientation of undergraduate business students in Greece. The researchers found that academic dishonesty is positively related to students' attitudes towards unethical managers' behaviour in the business context.

Chang and Leun (2006) surveyed 156 accounting undergraduates to investigate the ethical sensitivity of accounting students and the effects of their ethical reasoning and personal factors on their ethical sensitivity. They found no significant relationship between accounting students' ethical sensitivity and their ethical reasoning. Their survey also indicated that an accounting ethics intervention may have positive effect on accounting students' ethical sensitivity development.

Giacomino and Akers (2006) surveyed students and business managers to measure their perception of specific earnings management actions. The questionnaire was similar to that used by Bruns and Merchant (1990) but an additional seven practices were included, totaling 20 items relating to ten earnings management practices. Their results showed no significant difference between students and business managers and also between genders. The findings of the 13 practices similar to the Bruns and Merchant (1990) study were used to compare their study with four studies using the Bruns and Merchant (1990) questionnaire prior to 2002. The average of the prior studies was determined and the comparison indicated that the respondents in their study had stricter views.

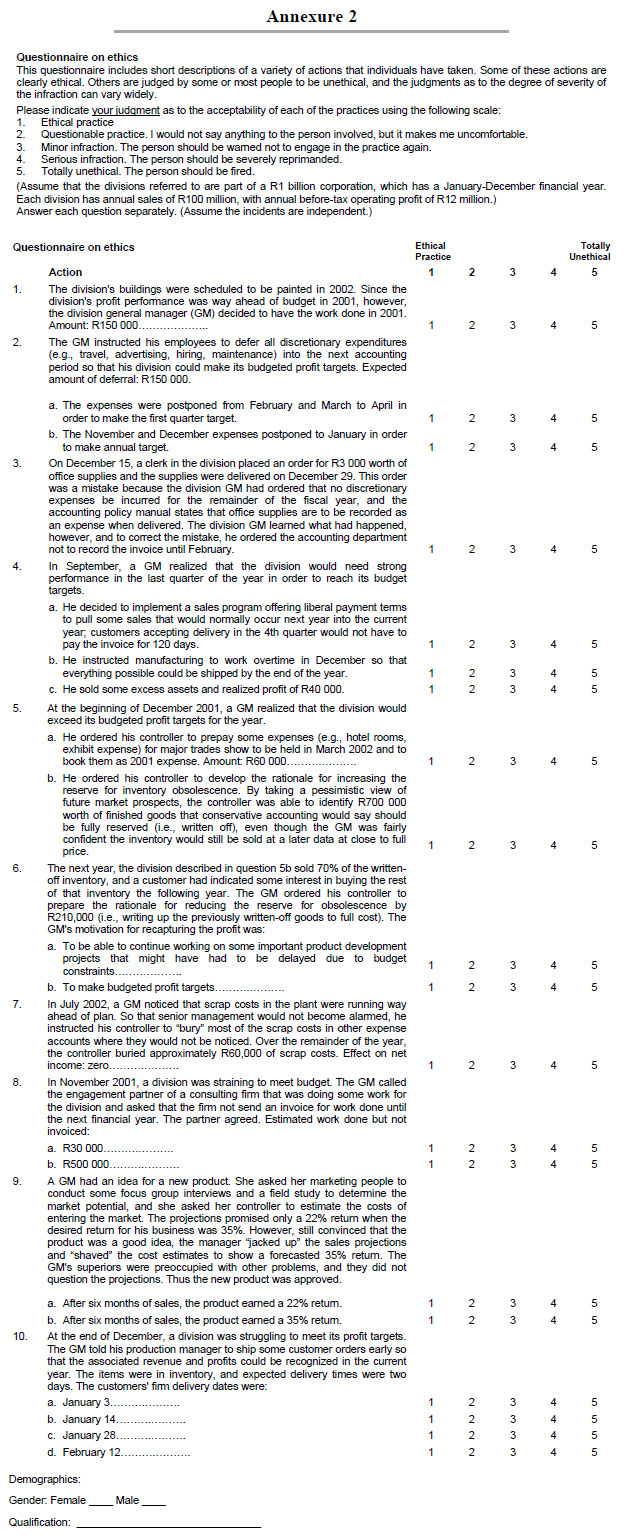

Jooste (2010) proceeds with a similar study as Giacomino and Akers (2006) and surveys the ethical perceptions of students, business managers and gender on 20 short-term earnings management practices. The results indicated no significant difference between genders but found a significant difference between students and business managers. Business managers rated the practices less ethically than students. See Annexure 2 for the actual questionnaire the respondents completed.

5 Methodology

This study is similar to the study by Giacomino and Akers (2006) where the authors compare a 2006 survey of students and business managers from Marquette University, Milwaukee, USA, with four US studies (Clikeman et al., 2001; Fischer & Rosenzweig, 1995; Rozenzweig & Fisher, 1994; Merchant & Rockness, 1994) prior to 2002 (hereafter referred to as prior studies). The objective, given the publicity of cases such as Enron and WorldCom, was to determine if there have been changes in attitudes towards earningsmanagement practices. The authors argued that sufficient time has passed since the fraud cases and the issuance of the Sarbanes-Oxley Act in 2002, that they might expect some change in the views on the morality of earnings management.

The fraud cases in the US received worldwide publicity, even in SA. Furthermore, the King report and Corporate Governance in SA followed the Sarbanes-Oxley Act in the US. SA universities also introduced ethics courses in business studies. Therefore, this study aims to determine if perceptions changed towards earnings management practices. Due to a lack of similar studies in SA, this study, similar to that of Giacomino and Akers (2006), compares a survey from NMMU in SA with the four US studies (Clikeman et al., 2001; Fischer & Rosenzweig, 1995; Rozenzweig & Fisher, 1994; Merchant & Rockness, 1994) prior to 2002.

This study will use the average of the prior studies determined by Giacomino and Akers (2006) to compare 13 earnings management practices actions (the same 13 as in the Bruns and Merchant study). The aim of this comparison is to determine whether there have been changes in the attitudes of respondents in SA since the highly-publicised cases of Enron and WorldCom and the issuance of Sarbanes-Oxley Act 2002 and Corporate Governance in SA.

6 Research design

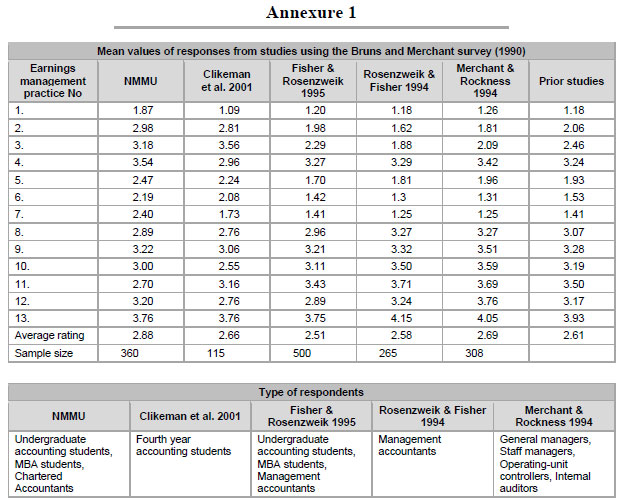

The average of the studies from the study by Giacomino and Akers (2006) will be used (see Annexure 1). The means of the NMMU survey (Jooste 2010) will then be compared with the average of the prior studies. The findings will be analysed to determine if there are changes in perceptions on earnings management practices.

Sample

Two groups were surveyed, undergraduate accounting students at the NMMU and business managers. The business managers were students in an MBA course at the NMMU and qualified accountants employed by accounting firms.

Demographic data

| Students | 259 |

| Business managers (BM) | 94 |

| Not answered (5 students; 2 BM) | 7 |

| Total : | 360 |

Prior studies

Four studies (Clikeman et al., 2001; Fischer & Rosenzweig, 1995; Rozenzweig & Fisher, 1994; Merchant & Rockness, 1994) subsequent to the Bruns and Merchant (1990) study have utilised the Bruns and Merchant questionnaire.

Annexure 1 lists the mean values from the four studies' responses and the study at NMMU for 13 practices. The 13 practices correspond with the original Bruns and Merchant questionnaire. The average of the prior study for each of the 13 actions is also provided in Annexure 1.

The questionnaire

Bruns and Merchant (HBR, 1989) study prepared a 13-action questionnaire based on practices that the authors considered short-term earnings management practices. The practices involve the choice and timing of operating events and the choice and timing of recognition of specific revenues and expenses, therefore covering operating manipulations and accounting manipulations. The respondents were informed that the questionnaire referred to a $1 billion company consisting of different divisions which has a January-December fiscal year. Each division has a turnover of $100 million and net profits before taxation of $12 million. The respondents were required to rate each question on a five-point Likert scale ranging from 1 to 5 as follows:

| 1 | = | Ethical Practice (mean below 1.5). |

| 2 | = | Questionable Practice. I would not say anything to the person involved, but it makes me uncomfortable (mean between 1.5 and 2.5). |

| 3 | = | Minor Practice. The person should be warned not to engage in the practice again (mean between 2.5 and 3.5). |

| 4 | = | Serious Infraction. The person should be severely reprimanded (mean between 3.5 and 4.5). |

| 5 | = | Totally Unethical. The person should be fired (mean between 4.5 and 5). |

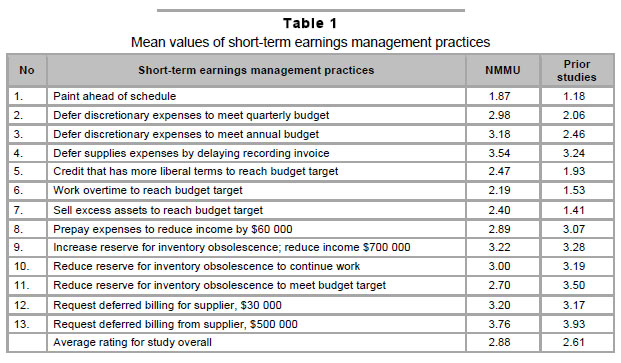

On the questionnaire's first page the respondents were informed that the questionnaire consists of a short description of a variety of actions that individuals have taken. Some of these actions are clearly ethical. Others are judged by some or most people to be unethical, and the judgments as to the degree of severity of the infraction may vary (HBR, 1989). In Table 1, the 13 earnings management practices are listed as well as the averages of the mean values from prior studies and the mean value from the NMMU study.

Research method

This descriptive study compares surveys to determine the changes in ethical perceptions subsequent to the Enron and WorldCom scandals and the Sarbanes-Oxley Act in 2002, followed by Corporate Governance in SA. The results on how the respondents rated 13 earnings management actions at NMMU and the average of four studies prior to 2002 were compared. Table 1 provides a breakdown of the survey groups.

Findings

The mean values of NMMU are above the average of the prior studies for eight of the 13 actions (1, 2, 3, 4, 5, 6, 7 and 12). This indicates that the respondents in the NMMU study have stricter views than the respondents in the prior studies for these actions. In five of the 13 actions (8, 9, 10, 11 and 13) the respondents in the prior studies had stricter views. The greatest difference in the mean values is 0.99 (action 7), namely, Sell excess assets to reach budget target. The smallest difference is 0.03 (action 12), namely, Request deferred billing from supplier for $30 000. The overall average rating for all 13 actions for the NMMU was 2.88, which is 0.27 higher than the overall average of the prior studies.

In the comparison by Giacomino and Akers (2006), such a small difference is not rated as a substantial difference, which indicates that the perceptions regarding earnings management have not changed substantially since 2002. According to Giacomino and Akers (2006), small differences in mean values suggest that the results are consistent with the findings of the Bruns and Merchant study conducted in 1990 and the prior studies. This indicates that perceptions regarding earnings management practices have changed, but they have not changed significantly owing to events such as the issuance of the Sarbanes-Oxley Act of 2002 and the financial frauds and failures of Enron and WorldCom.

The overall response showed a significant lack of agreement and the dispersion of ratings varied considerably. The surveys suggest that the 13 earnings management practices are not acceptable, since only two practices (1, Paint ahead of schedule, and 7, Sell excess assets to reach budget target) were rated as ethical practices by prior studies. Although NMMU has the stricter view, the following similarities were found:

• Totally Unethical: The person should be fired (mean between 4.5 and 5)

No practice was rated as totally unethical by both groups.

• Serious Infraction: The person should be severely reprimanded (mean between 3.5 and 4.5)

Two practices were rated as a serious infraction by NMMU of which one was rated the same by the prior studies. The practice is:

Request deferred billing from supplier, $500 000 (13)

NMMU rated one more practice as a serious infraction, whereas the prior studies rated it as a minor infraction, which is:

| | Defer supplies expense by delaying recording invoice (4) |

• Minor Infraction: The person should be warned not to engage in the practice again (mean between 2.5 and 3.5)

Five of the seven practices rated by NMMU were also rated by the prior studies as a minor infraction, namely:

| | Prepay expenses to reduce income by $60 000 (8) |

| | Increase reserve for obsolescence, reduce income $700 000 (9) |

| | Reduce reserve for obsolescence to continue work (10) |

| | Reduce reserve for obsolescence to meet budget target (11) |

| | Request deferred billing for supplier, $30 000 (12) |

NMMU rated one more practice as a serious infraction, whereas the prior studies rated it as a minor infraction, which is:

| | Defer supplies expense by delaying recording invoice (4) |

• Questionable Practice: I would not say anything to the person involved, but it makes me uncomfortable (mean between 1.5 and 2.5).

Two of the four practices rated as a questionable practice by NMMU received the same rating by the prior studies, namely:

| | More liberal credit terms to reach budget target (5) |

| | Work overtime to reach budget target (4b) |

The NMMU also rated Paint ahead of schedule (1) and Sell excess assets to reach budget target (7) as a questionable practice. Both these actions were rated by the prior studies as an ethical practice. The prior studies rated the following actions as a questionable practice:

| | Defer expenses to meet quarterly budget (2) |

| | Defer expenses to meet annual budget (3) |

• Ethical Practice: (mean below 1.5)

Paint ahead of schedule (1), and Sell excess assets to reach budget target (7), were rated by the prior studies as an ethical practice.

In this comparison, further interesting earnings management findings were evident. It was found that for some of the practices, the dollar amount, timing of the action, the method used, and the extent of the budgets affected the respondent's views.

• Dollar amount

Both actions 12 and 13 request the supplier to defer a bill, for $30 000 and $500 000 respectively. Where the dollar amount is $500 000 both the NMMU and the prior studies rated the action more serious. This is also consistent with those of Giacomino and Akers ((2006). The prior studies also reported that materiality was a factor and that large amounts were judged more seriously than small amounts.

• Timing of the transaction

In both actions 2 and 3 discretionary expenses were deferred to meet different budgets. Where the action was to meet the annual budget both the NMMU and the prior studies judged the action more harshly than where the action was to defer discretionary expenses to meet quarterly budgets.

Totally Unethical:

• Method used

The prior studies also reported that the methods used to reach budget targets affected the views of the respondents even though the result turned out the same. Action 5 called for more liberal terms to reach the budget target, whereas action 6 required working overtime, and action 7, to selling excess assets to reach the budget target. Both the prior studies and the NMMU study rated more liberal credit terms as less acceptable than working overtime or the selling of excess assets.

• Quarterly or annual budgets

In actions 2 and 3 the deferral to meet the annual budget is viewed as more serious by the NMMU than the deferral to meet the quarterly budget. These findings are also consistent with those of the prior studies and the studies by Bruns and Merchant (1990) and Giacomino and Akers (2006).

Overall, these results seem to be consistent with the findings of the Bruns and Merchant (1990) study as well as the prior studies by Merchant and Rockness (1994), Rozenzweig and Fisher (1994), Fischer and Rosenzweig (1995), and Clikeman et al. (2001). This similarity was also found in a survey by Giacomino and Akers (2006).

This study also found that the respondents do not support the acceptability of these earnings management practices, since only two (by the prior studies) were rated as an Ethical Practice. However, the greatest concern of the findings was the total lack of agreement as no action was unanimously rated as unethical.

7 Implications for academia

Although this study shows that there have been some changes in perceptions regarding earnings-management practices since 2002, the changes seems to be insignificant. This means that business students still need more exposure and an understanding of methods used to manage earnings, as was suggested by Fischer and Rosenzweig (1995). Therefore, this has implications for academia and becomes the responsibility of universities and business schools. They are the basic source of providing leaders and managers and also seem to be blamed for much of the unethical behaviour in business (Karassavidou & Glaveli, 2006).

Giacomino and Akers (2006) suggest that business publications should continue to report fraudulent financial reporting in the media and academic journals on a regular basis. Fraudulent reporting is often the result of earnings management. Fisher and Rosenzweig (1995) suggest that greater emphasis be placed on earnings management practices in the accounting curricula. Although difficult, it should be integrated into business courses, or be a separate business ethics course or an accounting course taught by accounting and business ethics academia.

Furthermore, Giacomino and Akers (2006) suggest that the 'real-world' aspects of earnings management practices be enhanced and that experienced business professionals become an integral part of accounting courses. In addition, differences between business managers and students should be minimised as conflicting opinions begin to develop during undergraduate business education. Students appear to adopt the attitudes of their professional reference groups before they even commence their professional careers. Therefore, by using experienced business professionals during lectures and making discussions of earnings more realistic, the differences between students and business managers may be reduced with reference to perceptions of earnings management practices.

8 Conclusions

Ethics in accounting has been an issue for many years. In earlier years, the Treadway Commission (Cohen & Pant, 1989) called for changes in accounting education and called on business schools to include ethics in every accounting and business course.

Furthermore, Bruns and Merchant (1990) did a survey on earnings management that revealed unfavourable results. Therefore they suggest that the key to moral behaviour is the obligation to look beyond self-interest and to focus on the concerns of others. They regard the morality of doing otherwise questionable and the ethical perspective therefore raises the question as to whether earnings management practices are moral. This followed with the bankruptcy of Enron and WorldCom in 2001 that shocked the business world and resulted in serious harm to all stakeholders.

As a result, the Sarbanes-Oxley Act was introduced in 2002 (followed in SA by Corporate Governance). The concept of earnings management practices has received considerable attention in the accounting literature, and sufficient time has passed since the financial scandals and the passage of the Sarbanes-Oxley Act so that one would expect some change in the ethical perceptions towards earnings management. Therefore the question to be raised, in the light of all the research, is whether the ethical perceptions of accounting students and practitioners have changed since 2002.

Many accounting practitioners and students think that ethics is a list of rules, such as the Ten Commandments or explicit organisational codes of ethics. Hence, the assumption is that if something is not expressly prohibited, there is no need to worry about ethics (Giacomino & Akers, 2006). Based on this view, earningsmanagement practices are not problematic if no rules are broken by engaging in it. However, if a respondent has this rule-based view of ethics, he or she would judge accounting manipulations (a violation of accepted accounting practice) as more unethical, since they violate explicit rules, while operating manipulations do not (Fischer & Rosenzweig, 1995). It seems from the surveys in the study that ethics is still viewed in this light.

This study compared a survey performed at NMMU with US studies prior to 2002 using the Bruns and Merchant (1990) questionnaire. The results indicated that since 2002 there has not been a substantial change in the views of students and business managers regarding earnings management practices. The US studies were used in the comparison as no SA studies using the Bruns and Merchant (1990) survey exist.

This still has implications for educators and business schools to increase changes in accounting curricula and to include greater ethics discussions. Therefore, it is suggested that the survey should also be repeated in the future to determine if there are changes in the ethical views of accounting students. The results may enable accounting educators to understand what students feel and how they may react to earnings management practices when in practice. Furthermore, if courses are introduced to address aspects of earningsmanagement practices, a further survey can determine whether it contributed towards changing the ethical views of the students or if the attitudes of students towards earnings management practices can be improved. Akers et al. (2004) found that very little research and few curricular activities have been done with respect to the role of personal values in accounting. Their study (Akers et al., 2004) includes a step-by-step discussion of how accounting programmes can apply intervention methods to change students' personal values toward a desired end. The intervention methods include programmatic, curriculum and classroom activities. These intervention methods were introduced at a comprehensive, private university in the Midwest of the US. Their aim was to introduce an effective tool that can be used by accounting educators to positively influence the next generation of accountants. To date no further studies have been published by the authors in this regard.

The results of this NMMU study need to be interpreted in the light of possible weaknesses. The respondents in the study may not be representative of students and business managers of the local country. Overall, business managers were found to view the earnings-management practices less favourably than the students. This may be due to the fact that students have fewer risks than business managers and also the possibility that students may not fully understand the wording of the questionnaire on earnings management.

It is suggested that a follow-up survey be performed in SA using similar respondents. This could indicate, amongst others, whether the introduction of King 111 in South Africa has contributed towards changing the ethical perceptions of students and business managers.

References

AKERS, M.D., EATON, T.V. & GIACOMINO, D.E. 2004. Measuring and changing the personal values of accounting students. Journal of College Teaching & Learning, 1(4):63-70.

BELKAOUI, A. 2004. Accounting Theory (5th ed.) Singapore: Thompson Learning.

BERNSTEIN L.A. & SIEGEL, J.G. 1979. The concept of earnings quality. Financial Analysts Journal, 35: 72-75.

BRUNS, W.J. & MERCHANT, K.A. 1990. The dangerous morality of managing earnings. Management Accounting, 72(2):22-25.

CHANG, S.Y.S. & LEUNG, P. 2006. The effects of accounting students' ethical reasoning and personal factors on their ethical sensitivity. Managerial Auditing Journal, 21(4):436-457.

COHEN, J.R. & PANT, L.W. 1989. Accounting educators' perceptions of ethics in the curriculum. Issues in Accounting Education, 4(1):70-81.

CLIKEMAN, P., GREIGER, M. & O'Connell, B. 2001. Student perceptions of earnings management: the effects of national origin and gender. Teaching Business Ethics, 5(4):389-410.

ELIAS, R. 2004. The impact of corporate ethical values on perceptions of earnings management. Managerial Accounting Journal, 19(1):84-98.

FISCHER, M. & ROSENZWEIG, K. 1995. Attitudes of students and accounting practitioners concerning the ethical acceptability of earnings management. Journal of Business Ethics, 14(6):433-444.

GIACOMINO, D.E. & AKERS, M. 2006. The ethics of managing short-term earnings: business managers and business students have few problems with earnings management practices. Journal of College Teaching & Learning, July:57-71.

HEALY, P.M. & WAHLEN, J.M. 1999. A review of the earnings management literature and its implications for standard setting. Accounting Horizons, 13(4):365-383.

HARVARD BUSINESS REVIEW. 1989. Ethics test for everyday managers. Harvard Business Review, March-April:220-221.

JOOSTE, L. 2010. Accounting ethics -an empirical investigation of managing short-term earnings. South African Journal of Economic and Management Sciences, 13(1):98-111.

KAPLAN, S.E. 2001. Ethically related judgments by observers of earnings management. Journal of Business Ethics, 32:285-298.

KARASSAVIDOU, E. & GLAVELI, N. 2006. Towards the ethical or the unethical side? International Journal of Educational Management, 20(5):348-364.

MERCHANT, K.A. & ROCKNESS, J. 1994. The ethics of managing earnings: an empirical investigation. Journal of Accounting and Public Policy, 13:79-94.

ROSENZWEIG, K. & FISCHER, M. 1994. Is managing earnings ethically acceptable? Management Accounting, 75(9):31-34.

VERSCHOOR, C. 2002. It isn't enough to just have a code of ethics. Strategic Finance, December:22-24.

WOO, C.J. 2003. Personally responsible. BizEd. May/June:22-27 .

Accepted: Septemer 2011

{kind=link}

{kind=link}

{kind=link}