Servicios Personalizados

Articulo

Inglés (pdf)

Inglés (pdf)

Articulo en XML

Articulo en XML Referencias del artículo

Referencias del artículo

Indicadores

Links relacionados

-

Citado por Google

Citado por Google -

Similares en Google

Similares en Google

Compartir

Permalink

PermalinkThe African Journal of Information and Communication

versión On-line ISSN 2077-7213

versión impresa ISSN 2077-7205

AJIC vol.31 Johannesburg 2023

http://dx.doi.org/10.23962/ajic.i31.16013

RESEARCH ARTICLES

Competition regulation for digital markets: The South African experience

Simphiwe GumedeI; Phathutshedzo ManenzheII

ILegal Counsel, Competition Commission South Africa, Pretoria. https://orcid.org/0009-0002-0158-2455

IIAnalyst, Competition Commission South Africa, Pretoria. https://orcid.org/0009-0007-8781-112X

ABSTRACT

The study examines the recent experiences of South Africa's competition authorities in engaging with competition matters in the country's digital markets. Specifically, the authors examine engagements by the Competition Commission South Africa (CCSA), the Competition Tribunal of South Africa, and the Competition Appeal Court (CAC) with three regulatory elements: (1) mergers, examined through the MIH and WeBuyCars and Google and Fitbit cases; (2) abuse of dominance, examined through the GovChat v Facebook case; and (3) cartel conduct, examined through the Competition Commission v Bank of America Merrill Lynch International Limited & Others case. In reviewing the decisions made in these cases, the authors highlight regulatory considerations that are coming to the fore in response to competition matters in digital markets.

Keywords: digital markets, competition, regulation, mergers, abuse of dominance, cartel conduct, South Africa

1. Introduction

Since the introduction of internet connectivity, the digital economy has been growing rapidly throughout the world. It provides businesses in digital markets with an unprecedentedly large geographic reach with which to access customers and intermediaries. This digital economy has brought with it challenges that have necessitated appropriate competition regulation. Traditional competition tools, which have been successfully applied to prevent elevated levels of concentration and the establishment of monopolies within the traditional economy, have come under great scrutiny given the potential difference in the dynamics of digital markets (Maihaniemi, 2020). These tools appear to have fallen short in some respects, given the high concentration levels in digital markets, leading to calls for differences in approach when regulating certain elements of competition in the digital economy (Maihaniemi, 2020).

The economics that drive digital markets provide significant challenges for competition law and regulation (Ademuyiwa & Adeniran, 2020). These challenges include defining markets through the use of the SSNIP (small but significant non-transitory increase in price) test, as the price arrived at must, in most digital markets, also take into account the multi-sided nature of the market and thus the need to balance the effect that a price on one side of the market has on the other side of the market (OECD, 2018). For example, in the Google LLC and Alphabet Inc v European Commission case, the General Court acknowledged that competition can take place in terms of quality and innovation, and found that the small but significant non-transitory deterioration in quality (SSNDQ) test, rather than an SSNIP test, constituted relevant evidence for the purpose of defining a market (Google LLC and Alphabet Inc v European Commission, 2018). Furthermore, the traditional tools used to establish market power (such as elasticities, diversion ratios, and market shares) now need to also take into account the effect on consumer behaviour on one side of the market, contrasted with the effect on the other side of the market (OECD, 2018). At the same time, evaluation of the effect of high market share on one side of the market is unlikely to assist in understanding why a digital firm is also able to command dominance on the other side of the market where it does not have high market share (OECD, 2018).

The provisions of the South African Competition Act No. 89 of 1998, as amended (the Act), and the decisions of the Competition Commission South Africa (CCSA), the Competition Tribunal of South Africa, and the Competition Appeal Court (CAC), have come into sharp focus with respect to their ability to effectively regulate competition in South Africa's digital markets. This article examines recent decisions by the CCSA, the Tribunal, and the CAC with respect to three areas of competition regulation that have taken on new complexities in the digital dispensation: (1) merger control, which we examine through consideration of the MIH and WeBuyCars and Google and Fitbit cases; (2) preventing abuse of dominance, which we examine through consideration of the GovChat v Facebook case; and (3) preventing cartel conduct, which we examine through consideration of the Competition Commission v Bank of America Merrill Lynch International Limited & Others case. In examining these cases, we seek to highlight some of the regulatory elements that have gained increased prominence in the digital dispensation.

2. Background: Competition in digital markets Global context

The proliferation of digital platforms has caused significant disruptions to the traditional economy, through prioritisation of the growth of platforms, in the short and medium term, over profit-making (UNCTAD, 2019). Digital platforms undertake this growth by focusing on the collection of large amounts of user data and using this data to improve their algorithms for more effective attraction of new users to the platform.

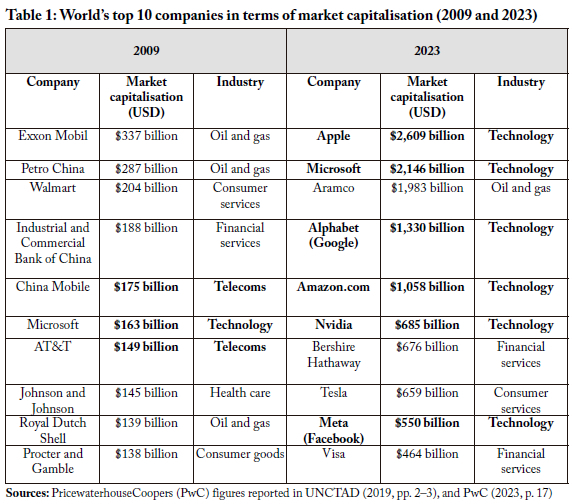

A comparison (see Table 1) of the industries of the top 10 companies in the world (by market capitalisation) in 2009 with the industries of the top 10 companies in 2023 reveals just how far the digital economy has grown and increased its impact on our lives (PwC, 2023; UNCTAD, 2019).

As depicted in Table 1, in 2009 the top 10 companies included one technology company and two telecommunications companies. By 2023, the majority of the top 10 companies were technology-driven entities. The economic power of the "GAFAM" companies-Google (Alphabet), Apple, Facebook (Meta), Amazon, and Microsoft-achieved through intensive investment in their digital platforms and the deployment of user data collected via these platforms, is evident in their presence in the top 10 companies of 2023. These firms together provide digital infrastructure and software for, inter alia, applications, search engines, social networking sites, social media, e-commerce, marketplaces, personal computers, and cloud computing. These firms control the largest digital platforms-a position that enables them to dominate both sides of a market and leverage their dominance for their own benefit (US House of Representatives, 2022).

One characteristic of the digital economy is the two-sided or multi-sided nature of the digital platforms that operate in various markets (UNCTAD, 2019). In such markets, firms simultaneously interact with two or more separate customer groupings. These can include users, content providers, and advertisers (OECD, 2018). The effects of what is done on one side of the market can also influence what happens on the other side(s). For example, a price increase for users may have a negative impact not just on the user side but also on the advertising side and the content creation side (OECD, 2018). The underlying business model of these firms is predicated on the collection of large amounts of data (Maihaniemi, 2020). On the one hand, digital platforms offer free services to consumers while gaining their attention and data, and, on the other, they monetise this attention and data by selling advertising opportunities to advertisers and allowing business users to sell goods and services to consumers through the platforms (ACCC, 2020; Maihaniemi, 2020). The consumer data that digital platforms collect is often seen as a commodity, valuable enough to influence big data companies' ability to "make decisions with economic impacts, environmental impacts or effects on health, education or society in general" (Coyle et al., 2020, as cited in UNCTAD, 2021, p. 5). The role of data is paramount for digital platforms because it often becomes the tool through which market power is established (UNCTAD, 2019).

The digital economy has brought with it some unique features that have facilitated high levels of market concentration. The control of big data, and use of machine-learning algorithms and analytics, generates enormous digital intelligence for the data controller. The high and increasing returns available through the use of big data entrenches the dominance of the data controllers. For instance, digital platform companies collect data on their users, and on their users' online behaviour, and sell the data to third parties who in turn use this data to develop their online businesses (Maihaniemi, 2020). Digital platform companies also use the data they collect for targeted/personalised marketing and to improve their consumer offerings, thus attracting more use on, and more users of, their platforms (Maihaniemi, 2020). The economic power of the collected data is further intensified by the digital platforms' low distribution costs, which facilitate global reach.

Today's most powerful digital platform companies have links to pioneering players in the digital economy, who continue to benefit from first-mover advantages. The pioneers were able to amass the first large collections of user data and to deploy this data (in the ways described above) in order to grow their digital platforms and market power, thus providing access to ever-larger pools of user data (UNCTAD, 2021). The largest digital platform companies have also been able to implement deliberate strategies to retain their early leadership, such as acquiring start-up entities that could potentially pose a competitive threat (UNCTAD, 2019) and imposing restrictive terms and conditions on business users that are not imposed on the businesses or business units within the platform company's conglomerate. Most of the core competition matters present in digital markets include elements of abuse of market power by large digital platforms-i.e., exploitation of their ability to behave, to an appreciable extent, in a manner independent from the behaviour of their competitors, customers, and/or consumers, usually resulting in anti-competitive effects.

Smaller digital platforms struggle to compete effectively with the large platforms. In addition to up-front investment costs, new entrants are faced with incumbent digital platforms that enjoy substantial economies of scale wherein the marginal cost of acquiring large numbers of additional users is close to zero. The incumbent platforms also benefit from substantial network effects. Business users seek strategies to grow their consumer base, and this rewards digital platforms which have strong network effects. The platforms' network effects allow businesses users to rapidly increase their user base, thus building business user dependence on the platforms. Such network effects can result in virtuous cycles where growing users on the business user side drives the growth of consumers on the other side, which then repeats itself.

A number of theories of harm are relevant to competition in digital markets. These include forced free-riding, which arises from digital platforms' use of business users' competitively sensitive information, concerning both sellers and consumers. Forced free-riding is defined by Shelanski (2013, p. 1699) as occurring "when a platform appropriates innovation by other firms that depend on the platform for access to consumers". In the e-commerce context, Khan (2017) explains that forced free-riding can, for instance, arise when a digital platform operator copies the design of popular goods sold by third-party retailers on its platform. Also, digital platform operators can easily identify which goods are bestsellers on their platforms and, potentially, favour their own products in advertising efforts and search rankings (OECD, 2018). The threat of free-riding on digital platforms is afflictive as it cannot be easily identified or proven.

Another practice identified and characterised as abusive or discriminatory leveraging is when a dominant digital platform that is active in numerous related markets leverages its dominance in one market for the benefit of its products in a related market (OECD, 2020). While the leveraging of dominance by a firm in one market to an adjacent market is not unique to digital markets, this type of conduct can be particularly egregious in digital markets where the dominant firm is a digital platform owner. The dominant firm can, through self-preferencing, treat business users and third-party users in a discriminatory manner and favour its own products or services over competing goods or services. The prevalence of this type of conduct in the digital economy is of concern because large platforms provide an important gateway into the broader market.

A more established issue identified in digital markets is tying or bundling, which refers to sales practices whereby customers (business users) are either required or incentivised to buy two or more distinct products as a combined sales package. Tying or bundling can harm competition through the exertion of market power from one market segment to another, thereby foreclosing the latter. For instance, where dominant platform operators offer multiple services-such as online marketplaces providing both retail listing and delivery services or price comparison-the platform can engage in tying or bundling to foreclose rival sellers (OECD, 2018). However, it has also been found that tying or bundling practices may generate significant welfare-enhancing efficiencies, and therefore an outright prohibition may not be the most appropriate response (OECD, 2018).

Envelopment strategies have also been identified as potential causes of harm to competition in digital markets. Such strategies concern the imposition of unfair data collection terms by dominant firms. These terms allow dominant firms to collect the data of consumers and use it beyond the limited instances prescribed in the firms' privacy policies. These firms subsequently use this data to enter a new but related market with an overlapping user base, while entrenching their position in their original market (OECD, 2020). This form of strategy has also been referred to as privacy-tying (OECD, 2020).

Potential competitive harms relating to commissions, access conditions, and trading terms have also caused great concern in respect of digital markets. Several jurisdictions, including the US, the EU, Germany, and India, have recorded concerns regarding exploitative practices by large platforms in the form of high commission fees, unfair terms and conditions of access to platforms, and the treatment of smaller suppliers on digital platforms.

A clear understanding, by competition authorities, of how digital markets operate is imperative if such authorities are to be effective in achieving their fundamental purpose of ensuring competition. South Africa's approach to some of the challenges highlighted above will be considered next. Specifically, consideration will be given to specific cases-involving proposed mergers, potential abuse of dominance, and potential cartel conduct-in order to examine the functioning of South African competition regulation on, and the Act's ability to deal with, digital markets.

South African context

In September 2020, the CCSA published its strategic review, Competition in the Digital Economy (CCSA, 2020a). The report identifies four features of the digital economy in South Africa, namely: (1) the dynamic and innovative nature of digital markets; (2) concentration in digital markets, often created by first-mover advantages, data accumulation, and network effects; (3) the ease of entry in some secondary and tertiary levels of digital markets; and (4) the rapid pace of change (CCSA, 2020a). The report concludes that market inquiries are among the most effective mechanisms for addressing practices that may limit or prevent competition, and reduce barriers to entry, or expansion, in digital markets.

Based on the recommendation of the 2020 strategic review, the CCSA launched, in May 2021, an Online Intermediation Platforms Market Inquiry (OIPMI). The OIPMI Terms of Reference stated that the Inquiry stemmed from a "general recognition that normal enforcement tools may be inadequate on their own to prevent initial market leaders from durably entrenching their position [...]" (Department of Economic Development, 2021). Of specific concern were: the lack of competition enforcement tools to regulate data and data's ability to lead to market power; and the inability to define conduct which distorts and/or impedes competition and thus prosecute big data firms.

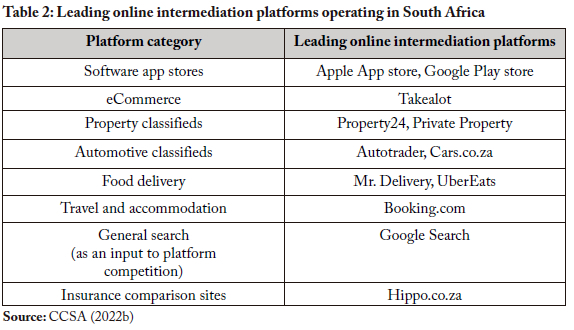

The initial scope of the OIPMI, which is nearing its conclusion as this article is being finalised in May 2023, included e-commerce marketplaces, online classifieds (in property and automotive), food delivery services, software application stores, as well as travel and accommodation services (CCSA, 2021). The OIPMI subsequently identified a need to include price comparator services in its scope, including insurance price comparator sites. In its July 2022 OIPMI Provisional Summary Report, the CCSA identified (see Table 2) the leading online intermediation platforms operating in eight South African platform categories that may require remedial action.

The identification of these platforms as leading was not premised on their dominance (as it is not necessary to establish dominance in a market inquiry), but rather on their exhibition of characteristics of a dominant firm in a particular market. The OIPMI is focused on market features that: inhibit platform competition and business user competition; lead to the exploitation of business users; and/or hinder the ability of small businesses and historically disadvantaged firms to participate in the markets (CCSA, 2022b).

We now turn to an examination of recent decisions taken by South African competition authorities in respect of three types of market behaviour-mergers, abuse of dominance, and cartel conduct-that have taken on significant new dimensions in the digital dispensation.

3. Mergers

Of the 87 proposed mergers in South African digital markets between 2011 and 2018, 82 were approved without conditions and the remaining five were approved with public interest conditions (CCSA, 2020a). As a consequence of the dynamic nature of digital markets and the difficulty in regulating them because of unmet merger thresholds, the CCSA was not able to impose any substantive conditions or prohibit any of these mergers (CCSA, 2020a). It is important to note that this data does not indicate the number of mergers that did not meet the merger notification thresholds. Section 13(3) of the Act allows the CCSA to require parties to a "small merger" to file their merger at the request of the CCSA-provided that the CCSA is of the view that the merger may result in a lessening of competition in a market or that the merger cannot be justified on public interest grounds. However, in some cases the small-merger threshold fails to capture high-potential-value "killer acquisitions", which occur when a big data firm acquires a small firm still at an early stage of its operations and prior to the small firm acquiring assets or generating turnover that is sufficient to meet the merger notification thresholds.

In December 2022, in response to concerns regarding such "killer acquisitions", the CCSA published revised Guidelines on Small Merger Notification. The Guidelines require that the CCSA be notified before the implementation of a small merger where: (1) the acquiring firm's turnover or asset value (irrespective of the turnover or asset value of the target firm) exceeds the large-merger threshold (currently set at ZAR6.6 billion); and one of two additional conditions is met: (a) the acquisition or investment in the target firm exceeds the intermediate-merger threshold (currently set at ZAR190 million); or (b) the effective valuation of the target firm exceeds the intermediate-merger threshold (CCSA, 2022c).

The 2018 amendments to the Act have increased the CCSA's powers of scrutiny when considering mergers, by allowing for the examination of previous mergers that either of the parties may have engaged in over a period determined by the CCSA. This affords the CCSA the ability to consider a firm's previous merger activity and the potential impact it may have in a proposed merger. This is important for the CCSA when assessing potential mergers in the digital economy, given the ease with which firms can make new acquisitions, and enter new markets, within a short space of time.

MIH eCommerce Holdings (Pty) Ltd (t/a OLX) and WeBuyCars

This proposed merger involved the acquisition, by MIH eCommerce (Pty) Ltd (MIH) t/a OLX South Africa (OLX), of 60% of the shares in WeBuyCars (Pty) Ltd (WeBuyCars). OLX is an online classified advertising platform that "carries advertisements for a broad range of goods and services for purchase and sale, including used cars" (MIHand WeBuyCars, 2020). OLX is a wholly owned subsidiary of South African technology and media holding company Naspers, which operates The Car Trader (Pty) Ltd, t/a AutoTrader, an online specialised classified advertising platform for the purchase and sale of used and new vehicles. WeBuyCars, on the other hand, operates as a guaranteed buyer and seller of used cars.

Following the CCSA's investigation of the proposed merger, the CCSA was required, in terms of section 14A of the Act, to refer the merger (because of its size) to the Tribunal, along with a recommendation as to whether it should be approved or prohibited. In this case, the CCSA recommended to the Tribunal that the proposed transaction be prohibited. The theories of harm examined by the Tribunal were: (1) unilateral effects, specifically the removal of a potential entrant (Frontier Care Group (FCG)) into the market; and (2) conglomerate or portfolio effects, specifically the likelihood that the merger would entrench Naspers' dominance in the market.

During the investigation, it emerged that Naspers had already acquired a controlling interest in FCG, a German-based online car-buying and -selling company that was understood be on the verge of entering the South African market to compete with WeBuyCars. FCG buys used vehicles from private individuals and from car rental companies, and then sells the used vehicles to dealers (it does not sell to individual consumers).

The Tribunal identified a narrow South African market for car-buying services, and pointed out that the merging parties' own strategic documents stated that "traditional dealers do not exert any meaningful constraint upon car-buying services such as WeBuyCars" (MIH and WeBuyCars, 2020). Evidence presented during the hearing, including a survey done by AutoTrader, confirmed that traditional car dealers were customers of WeBuyCars rather than competitors. The Tribunal pointed out that online car-buying services are different from traditional dealers because an online car-buying service (such as WeBuyCars) focuses on: (1) the provision of immediate cash for a high volume of used cars; (2) a strong reputation coupled with a strong marketing strategy; (3) an online platform that eliminates geographic constraints, allowing private sellers to approach dealers on the platform without having to travel from one dealer to another; (4) a more rapid and convenient method of selling a car than that provided by traditional offline dealers; and (5) a greater scale for buying and storing cars than traditional car dealers are able to achieve.

In assessing the likelihood of the removal of a potential entrant from the market, the Tribunal pointed out that in terms of the merging parties' strategic documents and those of FCG,1 FCG was "poised to enter the market in South Africa but for the proposed merger" (MIH and WeBuyCars, 2020). The Tribunal further pointed out that FCG would have been a formidable entrant in South Africa, in competition with WeBuyCars, because it had been able to achieve success in other developing-world markets.

The Tribunal then examined the second theory of harm: conglomerate or portfolio effects. This theory of harm analysed whether, post-merger, Naspers' complementary businesses, including OLX and AutoTrader (as well as its broader portfolio of businesses, including its media and technology assets) could be leveraged to entrench WeBuyCars' dominance in the car-buying services market. The Tribunal found that WeBuyCars would be able to leverage OLX's market position in private listing offerings as customers would be able to receive a quote from WeBuyCars automatically when listing their vehicle on the OLX website.

With no competitor in the market to constrain WeBuyCars, the Tribunal concluded that the competition harm identified was likely to arise. Furthermore, the Tribunal highlighted that AutoTrader would be provided with "over 30 years of WeBuyCars' intricate data on both the cars and consumer behaviour" (MIH and WeBuyCars, 2020), and that this would enable it to set purchase and sale prices of vehicles coupled with an established dealership network to on-sell vehicles to.

The Tribunal prohibited the merger in 2020, and its decision was grounded in the identification of two crucial elements of digital markets: (1) the centrality of an online platform in the market; and (2) the increasing importance of data access in this market. The Tribunal's assessment of portfolio or conglomerate effects focused on the data that WeBuyCars would have access to post-merger and how this would effectively entrench WeBuyCars' dominant position in the market. Here we see a fundamental change from a traditional portfolio effects assessment, which would consider the products that the merged entity would have access to post-merger. When it comes to digital markets, the wealth of data that the merged entity would have access to has become a central assessment metric.

Google LLC and Fitbit Inc

This was classified as a small merger, due to the low turnover and asset value of Fitbit, which was filed at the request of the CCSA. Section 13(1)(a) of the South African Act states that "a party to a small merger is not required to notify the Competition Commission of that merger unless the Commission requires it to do so". The merger was also notified in the EU, the UK, and Australia. The theories of harm considered by the CCSA were: (1) the removal of potential competition in the production and supply of wearable devices (fitness trackers and/or smart watches); (2) input foreclosure (leveraging of Google's dominance in the provision of operating systems (OS) for Android mobile devices into the market for the production and supply of wrist-worn wearable devices); (3) using Fitbit data or data collected from wrist-worn wearable devices to enter the market for the provision of digital health; and (4) preventing future competition in the provision of digital health.

In assessing these theories, the CCSA did not conclude on a relevant market. However, it did consider the national upstream market for: (1) the production and supply of OS for wrist-worn wearable devices; (2) the production and supply of OS for smart mobile devices; and (3) the national downstream market for the production and supply of wrist-worn wearable devices. The CCSA found that Google's entry into the market for the supply of wearable devices through this transaction would lead to the removal of Fitbit as a non-vertically-integrated competitor in the market. The Commission also found that this transaction would raise the barriers to entry in the market and would enhance Google's already existing data, which would allow Google to enhance its dominance in the advertising market. However, the CCSA found that it was unlikely that Google would be able to foreclose Fitbit's competitors, because Google's Wear OS was not a significant input in the production and supply of wrist-worn wearable devices.

The CCSA also found that ownership of Fitbit's existing health data, when combined with Google's individualised non-health data, could result in Google entering markets (and tipping them in its favour) for the provision of health and health insurance. Thus, in its own words, the CCSA "found that the proposed transaction is likely to result in a substantial prevention or lessening of competition" (CCSA, 2020b).

Accordingly, though the Commission approved the merger in 2020, it made the approval conditional on Google committing to several behavioural conditions for a period of 10 years, with the conditions to be monitored "by an independent Trustee who will have the necessary skills, competencies, and technical abilities to monitor these conditions" (CCSA, 2020b). The conditions comprised Google's commitments to:

• make access to the Android OS available for free, without discrimination, and with unchanged licence conditions, to competing makers of wrist-worn-wearables;

• keep Fitbit data separate from existing Google data, to not automatically use Fitbit data in any Google services, and to allow South African users to decide whether or not to allow storage of their "measured body data" in their Google or Fitbit accounts; and

• to allow third parties currently accessing users' Fitbit data to continue to have that access, without a charge from Google and provided the user gives consent (CCSA, 2020b).

This case demonstrates the utility of imposing conditions as a regulatory tool for regulating the conduct of firms operating in digital markets. The case also shows that, as with some traditional markets, mergers in digital markets can be assessed without a concluded market definition. The identification of the perimeters of competition were sufficient for the assessment of the transaction. It is also significant that this merger revealed that the effects of a merger in digital markets can have an impact on a number of other markets. In addition to its identification of the three aforementioned broad markets, the CCSA also identified the potential impact of the merger in adjacent markets, namely the markets for the provision of health, and health insurance. The CCSA's imposition of a 10-year monitoring period provides it with the opportunity to examine and consider the impact of the merger on these adjacent markets. Setting behavioural conditions and monitoring behavioural compliance are important mechanisms for competition authorities seeking to control and assess the impact of data collection and use in digital markets. This is due to such markets being dynamic, rapidly-evolving, and double- or multi-sided in nature.

4. Abuse of dominance

In its Competition in the Digital Economy report (CCSA, 2020a), the Commission highlights several challenges for abuse-of-dominance prevention in digital markets, including: (1) jurisdiction-due to the globalised nature of digital markets, firms that operate in them often have a limited presence in South Africa, and holding them to account may therefore be difficult; (2) meeting the evidentiary burden for effects (often challenging in digital markets); and (3) assessing market power with an increased focus on competitive relationships and strategies as opposed to market shares, and assessing new types of market power, such as "gatekeeper" market power. The challenges faced by competition authorities around the world in seeking to prevent abuse of dominance in digital markets have prompted specific focus in international fora (see, for example, OECD, 2020).

GovChat v Facebook

This was an application for interim relief brought, before the Competition Tribunal, by GovChat, a South African government online services platform. GovChat requested that the Tribunal prevent Facebook (the owner of WhatsApp) from "off-boarding" GovChat from WhatsApp Business (WhatsApp's paid business messaging platform). GovChat argued that WhatsApp is dominant and that its conduct amounted to a prohibited practice, namely a contravention of section 8(1) (d)(ii) and section 8(1)(c) of the Act. Section 8(1)(d)(ii) prohibits a dominant firm from "refusing to supply scarce goods or services to a competitor or customer when supplying those goods or services is economically feasible". Section 8(1)(c), in the alternative, prohibits a dominant firm from engaging "in an exclusionary act, other than an act listed in paragraph (d), if the anti-competitive effect of that act outweighs its technological, efficiency or other pro-competitive gain".

Because this was an application for interim relief, the standard of proof for success was a prima facie standard. The Tribunal identified a market for over-the-top (OTT) messaging applications, in which WhatsApp was active, and distinguished the WhatsApp platform from other services (these included SMS, MMS, USSD) based on the fact that WhatsApp's users only required internet connection on a suitable phone and because the app was capable of sending and receiving a variety of media, including "photos, music, videos, voice memos, animated GIFs and even documents like MS Word or PDF files" (GovChat v Facebook, 2020, p. 10). Another important distinguishing feature that the Tribunal identified was WhatsApp's end-to-end encryption. Based on these distinguishing technological features, the Tribunal categorised WhatsApp in a narrowed OTT messaging apps market along with WeChat, Facebook Messenger, and Snapchat. The Tribunal established that WhatsApp was dominant in this market on the grounds that: (1) 89% of all internet users in South Africa between the ages of16 and 64 reported having used WhatsApp; (2) at least 58% of all mobile phone users in South Africa had downloaded WhatsApp; (3) WhatsApp comes pre-loaded on almost all Android smartphones; and (4) mobile networks in South Africa offer WhatsApp data bundles (GovChat v Facebook, 2020).

In assessing the contravention (off-boarding) alleged by GovChat, the Tribunal observed that it is very difficult to duplicate OTT apps without extensive capital investment, and thus such apps fall within the meaning of "scarce goods or services". The Tribunal found, on a prima facie standard, that WhatsApp was selectively applying its terms and conditions in support of its own business service providers (BSPs), and that WhatsApp was rendering services directly to government departments and its direct approach to GovChat's government clients indicated that WhatsApp sought to foreclose GovChat from the market. The Tribunal further found that GovChat had established a prima facie case of anticompetitive conduct on the part of WhatsApp because of WhatsApp's threats to off-board GovChat from the WhatsApp Business platform in favour of its own BSPs.

After concluding that GovChat had prima facie met the requirements of section 8(1) (d)(ii), the Tribunal ordered interim relief. We are of the view that this case opened an important door in South Africa for the interpretation and application of abuse-of-dominance provisions to digital markets. By making the crucial finding that the WhatsApp platform was scarce and could not be easily duplicated, and by showing the effects of Facebook's conduct (through the selective application of its terms), this case broadened the application of section 8(1)(d)(ii) for application to digital markets, confirming that the abuse-of-dominance provisions of the Act are able to apply to more than just brick-and-mortar markets.

With respect to the Tribunal's application of the concept of scarcity, it can be argued that the reason why the Tribunal could apply this concept in this case was because of the popularity and the significant start-up costs involved in establishing a platform such as WhatsApp. It remains to be seen whether the same will be true in an instance where the start-up costs are not high.

5. Cartel conduct

The proliferation of algorithms as tools used by firms to participate in digital markets has provided firms with greater efficiencies in their efforts to compete. Algorithms have also facilitated advanced mechanisms for collusion (CCSA, 2020a). Globally, the use of big data by firms has been found to enable collusion where firms can share identical pricing algorithms and use real-time data analysis to monitor compliance with a collusive agreement. The multi-country or globalised nature of many digital platforms also means that the prosecution of cartels in a single country will often be met by jurisdictional challenges.

Competition Commission v Bank of America Merrill Lynch International Limited & Others

In February 2017, the CCSA referred to the Tribunal allegations of price-fixing and dividing markets, concerning the South African Rand, against 17 local and international banks operating in South Africa.2 The CCSA alleged that the 17 banks had, in part, divided markets through the allocation of "customers in the USD/ZAR currency pair" (CCSA, 2020c, p. 1). The CCSA pointed out in its media statement that the investigation of this conduct stemmed from the identification of an agreement between the banks to collude, in 2007, on prices for "bids, offers and bid-offer spreads for the spot trades in relation to currency trading involving US Dollar / Rand currency pair" (CCSA, 2020c, p. 1). In investigating this alleged cartel, the CCSA had relied on traditional and familiar tools of investigation such as the identification of the agreement between the banks and the examination of online chats between bank employees held in chatrooms and on trading platforms.

This potential cartel had been detected in 2007 but only referred to the Tribunal in 2017, after a CCSA investigation that started in 2015. Following the CCSA's referral of this case, many of the internationally based banks raised jurisdictional challenges before the Tribunal. The Tribunal concluded that it did not have personal jurisdiction over the foreign-based banks. The Tribunal determined that both personal jurisdiction and subject-matter jurisdiction were necessary for it to have jurisdiction over the foreign-based banks (Competition Commission v Bank of America Merrill Lynch International Limited & Others, 2019). The Tribunal reasoned that section 3(1) of the Act established only subject-matter jurisdiction, with the lack of physical presence in South Africa meaning that no personal jurisdiction could be established.

The matter was ultimately appealed by the CCSA to the CAC, whose 2020 ruling in this case provided the CCSA with the opportunity to set out a clearer case against the foreign-based banks in respect of their conduct and its impact on South Africa. The CAC held that this opportunity would ensure that the CCSA was able to show that the Act and the Tribunal had jurisdiction over the foreign-based banks. The CAC, crucially, held that cartel conduct involving a foreign firm and impacting South Africa can be subject to the jurisdiction of the Act. The CAC further asserted that "courts should examine whether the forum which is sought to be employed has a real and substantial connection with the action; and whether the relevant connecting factors tie the action to the forum in question" (Competition Commission v Bank of America Merrill Lynch International Limited & Others, 2020, p. 22).

This assertion by the CAC was crucial in buttressing the point that anticompetitive conduct that has an effect on the South African economy would be in danger of falling outside of the scope of domestic enforcement if courts did not carefully examine and consider the merits of the case and jurisdiction (Competition Commission v Bank of America Merrill Lynch International Limited & Others, 2020). The CAC thus adopted a broader interpretation of section 3(1) of the Act than that which had been adopted by the Tribunal, which afforded the CCSA the opportunity to set out a clearer case against the foreign-based banks, particularly on the question of jurisdiction.

In March 2023, the Tribunal ruled that the CCSA had now satisfactorily set out the evidence of cartel conduct, and that the Tribunal had determined that it did indeed have jurisdiction to hear the case, on the grounds that "[t]he Respondents are accused of engaging in conduct considered the most egregious in competition law. Furthermore, the alleged conduct relates to fixing and manipulating the rand/dollar exchange rate, which has a central and crucial role in the South African economy" (Competition Tribunal, 2023). This ruling by the Tribunal, and the earlier ruling by the CAC, provide an important gateway for the CCSA to prosecute, where appropriate, conduct which involves firms that are based outside of South Africa. Given the global nature of digital markets, this is an important gateway.

We submit that this case reveals that the current legal framework is capable of prosecuting cartel activity even when digital firms located globally use quite novel means to collude. The CAC's wide interpretation of section 3(1) of the Act means that digital platforms that provide services or goods in South Africa need not necessarily have a physical presence in South Africa for the Act's jurisdiction to apply. While this discussion relating to jurisdiction has taken place within the context of cartel conduct, it is important to point out that the principles expressed by the CAC can find equal resonance within an abuse-of-dominance matter.

6. Conclusion

The cases examined in this study illustrate the ways in which South Africa's competition authorities are grappling with competition issues in the context of digital markets. In the cases outlined above, we have seen examples of: identifying the importance of the accumulation of data post-merger; preventing a merged digital platform firm from limiting the ability of competitors and new entrants to compete with it; requiring several behavioural conditions, with a 10-year monitoring period, in order to approve a merger of two global digital platform firms; and broadening the interpretation of the Act's provisions on scarce goods and services in order to account for some of the unique dynamics of scarcity in digital markets and in the strategies of digital firms.

We have also seen confirmation that the Act's jurisdiction clause can be interpreted such that the Act applies to the conduct of digital firms based outside of South Africa when the firms' actions have clear negative impacts on the South African economy.

The actions of the South African competition authorities in addressing merger, abuse-of-dominance, and cartel cases in digital markets have shown that, to date, the Act-and the bodies interpreting and conducting enforcement in terms of the Act-are capable of adapting it to digital markets. The final OIPMI report will, it is assumed, bolster the existing capabilities through its focused recommendations on how to address the competition dynamics at play in and among online intermediation platforms. It will also be important to track, in the years to come, how the public interest considerations in the Act (e.g., the impact on small and medium enterprises, and the impact on ownership by historically disadvantaged individuals) are interpreted by the South African competition authorities as they relate to digital markets.

References

Australian Competition and Consumer Commission (ACCC). (2019). Digital Platforms Inquiry: Finalreport. https://www.accc.gov.au/system/files/Digital%20platforms%20inquiry%20-%20final%20report.pdf

Ademuyiwa, I. & Adeniran, A. (2020). Assessing digitalisation and data governance issues in Africa. Centre for International Governance Innovation (CIGI). https://www.cigionline.org/documents/1767/no244_0.pdf

Competition Commission South Africa (CCSA). (2017, February 15). Competition Commission prosecutes banks (currency traders) for collusion. [Press release.] http://www.compcom.co.za/wp-content/uploads/2017/01/Competition-Commission-prosecutes-banks-currency-traders-for-collusion-15-Feb-2016.pdf

CCSA. (2020a). Competition in the digital economy: Version 2. http://www.compcorn.co.za/wp-content/uploads/2021/03/Digital-Markets-Paper-2021-002-1.pdf

CCSA. (2020b, December 22). Competition Commission conditionally approves the Google/Fitbit merger. [Media release.] http://www.compcom.co.za/wp-content/uploads/2020/12/Competition-Commission-conditionally-approves-the-Google-Fitbit-merger.pdf

CCSA. (2020c, June 2). Competition Commission refers its case against banks for Rand manipulation to the Tribunal for prosecution. [Media release.] https://www.compcom.co.za/wp-content/uploads/2020/06/Competition-commission-refers-its-case-against-banks-for-rand-manipulation-to-the-tribunal-for-prosecution.pdf

CCSA. (2021a). Online Intermediation Platforms Market Inquiry: Statement of issues. https://www.compcom.co.za/wp-content/uploads/2021/05/OIPMI-Statement-of-Issues_May-2021.pdf

CCSA. (2021b). Notification to approve with conditions the transaction involving: Google LLC (USA) and Fitbit Inc. (USA). Case Number: 2020sep0045. https://www.gov.za/sites/default/files/gcis_document/202110/45250gon968.pdf

CCSA. (2022a, March 14). Facebook prosecuted for abusing its dominance. [Media release.] https://www.compcom.co.za/wp-content/uploads/2022/03/FACEBOOK-PROSECUTED-FOR-ABUSING-ITS-DOMINANCE.pdf

CCSA. (2022b). Online Intermediation Platforms Market Inquiry: Provisional summary report. https://www.compcom.co.za/wp-content/uploads/2022/07/OIPMI-Provisional-Summary-Report.pdf

CCSA. (2022c). Final Guidelines on Small Merger Notification. https://www.compcom.co.za/wp-content/uploads/2022/09/Guidelines-on-small-merger-notification.pdf

Competition Commission of South Africa v Bank of America Merrill Lynch International Limited and Others (CR121Feb17) [2019] ZACT 50; [2020] 1 CPLR 205 (CT) (12 June 2019).

Competition Commission v Bank of America Merrill Lynch International Limited and Others (175/CAC/Jul19) [2020] ZACAC 1; 2020 (4) SA 105 (CAC); [2020] 1 CPLR 26 (cAC) (28 February 2020).

Competition Tribunal of South Africa. (2021, March 25). Tribunal grants GovChat, #Letstalk interim relief against WhatsApp and Facebook. [Press release.] https://www.comptrib.co.za/info-library/case-press-releases/tribunal-grants-govchat-letstalk-interim-relief-against-whatsapp-and-facebook

Competition Tribunal of South Africa. (2023, March 30). Tribunal rules that it has jurisdiction to hear the "forex cartel case" against foreign and local banks. [Press release.] https://www.comptrib.co.za/info-library/case-press-releases/tribunal-rules-that-it-has-jurisdiction-to-hear-the-forex-cartel-case-against-foreign-and-local-banks

Coyle, D., Diepeveen, S., Wdowin, J., Kay, L., & Tennison, J. (2020). The value of data - Policy implications. Bennett Institute for Public Policy, University of Cambridge; and Open Data Institute. https://www.bennettinstitute.cam.ac.uk/publications/value-data-policy-implications/

Da Silva, F., & Nunez, G. (2021). Free competition in the post-pandemic digital era: The impact on SMEs. Economic Commission for Latin America and the Caribbean (ECLAC), United Nations.

Department of Economic Development. (2021). Online Intermediation Platforms Market Inquiry: Terms of reference. Government Gazette No. 44432. https://www.gov.za/sites/default/files/gcisdocument/202104/44432gon330.pdf

Google and Alphabet v Commission (Google Shopping) (2021). T-612/17.

Google LLC and Alphabet Inc v European Commission (2018). T-604/18.

Google LLC and Fitbit Inc (2020). 2020Sep0045.

GovChat (Pty) Ltd, Hashtag Letstalk (Pty) Ltd v Facebook Inc., WhatsApp Inc., Facebook SA (Pty) Ltd (2020). Order IR165Nov20. Competition Tribunal of South Africa.

Kelly, L., Unterhalter, D., Goodman, I., Smith, P., & Youens, P. (2016). Principles of competition law in South Africa. (1st ed.). Oxford University Press.

Khan, L. M. (2017). Amazon's antitrust paradox. Yale Law Journal, 126(3), 710-805. [ Links ]

Maihaniemi, B. (2020). Competition law and big data: Imposing access to information in digital markets. Edward Elgar. https://doi.org/10.4337/9781788974264

MIH eCommerce Holdings Pty Ltd t/a OLX South Africa and WeBuyCars Pty Ltd (2020): Reasons for decision. Case No. LM183Sep18. Competition Tribunal of South Africa. https://www.comptrib.co.za/case-detail/8539

Organisation for Economic Co-operation and Development (OECD). (2018) Implications of e-commerce for competition policy. https://www.oecd.org/daf/competition/implications-of-e-commerce-for-competition-policy-2018.pdf

OECD. (2020). Abuse of dominance in digital markets. https://www.oecd.org/daf/competition/abuse-of-dominance-in-digital-markets-2020.pdf

PricewaterhouseCoopers (PwC). (2023). Global top 100 companies - by market capitalisation. https://www.pwc.com/gx/en/audit-services/publications/top100/pwc-global-top-100-companies-2023.pdf

Shelanski, H. A. (2013). Information, innovation and competition policy for the internet. University of Pennsylvania Law Review, 161(6), 1663-1705. [ Links ]

UN Conference on Trade and Development (UNCTAD). (2019). Competition issues in the digital economy. TD/B/C.I/CLP/54. https://unctad.org/system/files/offirial-document/ciclpd54_en.pdf

UNCTAD. (2021). Digital economy report 2021: Cross-border dataflows and development: For whom the dataflow. UNCTAD/DER/2021. https://unctad.org/publication/digital-economy-report-2021

US House of Representatives. (2022). Subcommittee on Antitrust, Commercial and Administrative Law of the Committee on the Judiciary of the House of Representatives. Investigation of Competition in Digital Markets. Majority Staff Report and Recommendations (117 Congress 2d Session). U.S. Government Publishing Office.

Acknowledgements

This article draws on content from the authors' paper presented to the 7th Annual Competition and Economic Regulation (ACER) Week conference, 15-16 September 2022 in Senga Bay, Malawi. ACER Week 2022 was convened by the COMESA Competition Commission, the Competition and Fair Trading Commission of Malawi, and the University of Johannesburg's Centre for Competition, Regulation and Economic Development (CCRED). AJIC is grateful for the reviewing support provided for this article by CCRED Research Fellow Sha'ista Goga, who is Director of Acacia Economics, Johannesburg.

1 These included FCG's public statements and email exchanges between WeBuyCars and OLX FCG.

2 The initial group of 17 banks comprised Bank of America Merrill Lynch International Limited, BNP Paribas, JP Morgan Chase & Co, JP Morgan Chase Bank NA, Investec Ltd, Standard New York Securities Inc, HSBC Bank Plc, Standard Chartered Bank, Credit Suisse Group, Standard Bank of South Africa Ltd, Commerzbank AG, Australia and New Zealand Banking Group Limited, Nomura International Plc, Macquarie Bank Limited, ABSA Bank Limited (ABSA), Barclays Capital Inc, and Barclays Bank plc. The number later increased to 28 when the CCSA, in June 2020, filed a new referral.