Serviços Personalizados

Artigo

Inglês (pdf)

Inglês (pdf)

Artigo em XML

Artigo em XML Referências do artigo

Referências do artigo

Indicadores

Links relacionados

-

Citado por Google

Citado por Google -

Similares em Google

Similares em Google

Compartilhar

Permalink

PermalinkThe African Journal of Information and Communication

versão On-line ISSN 2077-7213

versão impressa ISSN 2077-7205

AJIC vol.28 Johannesburg 2021

http://dx.doi.org/10.23962/10539/32214

ARTICLES

User Perceptions of Mobile Banking Apps in Tanzania: Impact of Information Systems (IS) Factors and Customer Personality Traits

Daniel Ntabagi Koloseni

Lecturer, Faculty of Computing, Information Systems and Mathematics, Institute of Finance Management, Dar es Salaam; https://orcid.org/0000-0002-4104-2704

ABSTRACT

This study probes the roles that information systems (IS) success factors and user personality traits play in Tanzanian users' perceptions of their experiences with mobile banking apps. Based on a survey of 249 mobile banking customers, the study finds that users are being positively influenced by the apps' system quality and system service, but not by the apps' information quality. The study also finds that, with respect to user personality traits, openness, agreeableness, conscientiousness and extraversion are all traits that have a positive impact on customers' use of, and satisfaction with, mobile banking apps. The findings suggest that developers of mobile banking apps for the Tanzanian market need to both improve the quality of the information in the apps and continue to target a range of personality traits.

Keywords: mobile banking apps, adoption, personality traits, information systems (IS), IS success model, Tanzania

1. Introduction

Banks and financial institutions are investing heavily in the development of mobile applications (apps) to enhance their mobile banking service provision capacity. Mobile banking apps allow customers to use mobile devices (e.g., a smartphone or a tablet) to make money transfers within banks, across banks, and to/from mobile money platforms (e.g., M-Pesa and Tigo Pesa in Tanzania); to make in-app purchases; and to view balances and bank statements.

The mobile app provides a scalable platform for the provision of banking services and also serves as an advertisement platform through which banks can advertise their services and products. With mobile apps, banks can tailor their services based on the personal needs and/or locations of customers to retain them (Floh & Treiblmaier, 2006). Furthermore, mobile apps enable banks to reduce operational costs by changing the traditional service model to one of self-service, which also enhances customer engagement.

Mobile apps are mostly accessed via smartphones, and thus the proliferation of mobile apps has gone hand in hand with the exponential growth in smartphone usage. However, the use of mobile banking apps can be hampered by several factors, including security, privacy, reliability, information quality, e-services quality, and design issues such as response speed linked to sensor capabilities and small screens (Dukic et al., 2015; Fife & Orjuela, 2012; Gilbert et al., 2011; Godwin-Jones, 2011; Inukollu et al., 2014; Jain & Shanbhag, 2012; Zwass, 2003).

Furthermore, the use of mobile banking apps is affected by the personal characteristics of the user (Barnett et al., 2014; Bennett & Perrewé, 2002), as those personal characteristics interact with an app's system characteristics (Hong et al., 2002; Pituch & Lee, 2006; Ramayah et al., 2012). Because of the growing importance of user personal characteristics in the functioning of technologies, Bennett and Perrewé (2002) suggest incorporating personality traits into research frameworks to better understand technology adoption behaviour, specifically technology usage. There have been numerous studies of the adoption of mobile apps (see Alavi & Ahuja, 2016; Chmielarz & Luczak, 2015; Hepola et al., 2016; Kumar et al., 2018; Manuel & Veríssimo, 2016; Mufioz-Leiva et al., 2017; Sampaio et al., 2017; Sangar & Ras-tari, 2015; Vedadi & Warkentin, 2016; Yang, 2013). However, these studies have not given significant attention to the potential roles played by personality traits in the use of mobile banking apps, creating a knowledge gap for banks and their app developers.

Accordingly, the purpose of this study was to investigate the roles played by information systems (IS) factors and customers' personality traits in influencing customers' perceptions of the use of mobile banking apps in Tanzania. The study's data, generated via a survey questionnaire completed by Tanzanian mobile banking users, was analysed using the DeLone and McLean (2003) IS success model and the five factor model (FFM) of personality (Digman, 1990).

2. Context: Use of mobile banking apps

The Tanzanian financial services industry is growing exponentially(Were et al., 2021), triggering an increased need for easy, reliable, timely, and trustworthy access to financial services. To cope with this need, banks in Tanzania are, among other approaches, deploying mobile banking apps. The goal of such apps is to imitate the functions that are carried out by web-based mobile banking applications and make them accessible in a mobile setting, in an interactive and personalised manner, on a smartphone or tablet. Furthermore, mobile banking apps are used to enhance service reachability, position brands in the highly competitive market, and encourage impulse-buying behaviour among consumers (Alavi & Ahuja, 2016). Mobile banking apps add a new set of tools for marketing in the digital age (Alavi & Ahuja, 2016). The owners of the apps (i.e., banks) can easily map consumers' preferences and easily plan how best to meet consumers' preferences through personalised services and suggestions.

Recently, the functionality of mobile payment apps in Tanzania was extended through the integration of quick response (QR) codes. This integration allows customers to scan merchants' QR codes and make payments in real-time (ClickPesa, 2019). It is now common for QR codes, along with other mobile payment channels, to be made available by merchants in major stores in Tanzania. Therefore, due to the benefits offered by mobile financial apps, it is no surprise that banks are heavily and rapidly investing in using mobile apps to deliver selected banking services.

Meanwhile, user adoption of mobile banking apps is rapidly increasing. Several factors have been found to contribute to the adoption of such apps. For instance, Hepola et al. (2016) and Sampaio et al. (2017) find that cognitive processing, activation, perceived risks, and affection have a positive influence on the adoption of mobile banking apps, while Mufioz-Leiva et al. (2017) find that attitude is a strong predictor of intention to use mobile banking apps. Satisfaction and perceived usefulness (performance expectancy) have also featured in several studies as key predictors of the adoption of mobile banking apps, such as the studies by Vedadi and Warkentin (2016), Kumar et al. (2018) and Ahuja and Alavi (2016). Other factors found to influence the adoption of mobile banking apps are intrinsic regulation, identified regulation, external regulation and integrated regulation, perceived ease of use, perceived risk and cost, and need for information (Ahuja & Alavi, 2016; Kumar et al., 2018). Prominent theories used in previous studies investigating the adoption of mobile banking apps include the technology acceptance model (TAM) (Mufioz-Leiva et al., 2017), the expectation-confirmation theory (ECT) (Vedadi & Warkentin, 2016), the self-determination theory (Kumar et al., 2018), and service-dominant logic (Hepola et al., 2016).

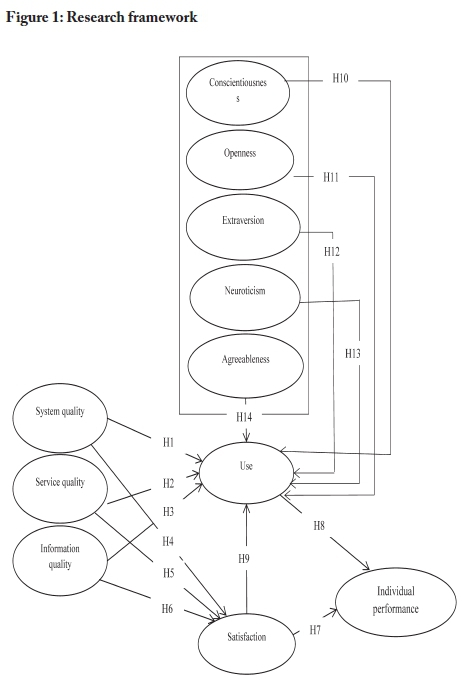

3. Hypothesis development and research framework IS success model

For measuring users' perceptions of the success or effectiveness of an information system, the DeLone and McLean (2003) IS success model is one of the dominant models. However, as seen in the previous section of this article, the IS success model is not prominent in published studies of the adoption of mobile banking apps. The model focuses on how three quality measures-system quality, service quality, and information quality-interact with system use (or intention to use) and user satisfaction in ways that, if the influences are positive, will generate net benefits for the user (DeLone & McLean, 2003).

Previous studies, such as those by Barnett et al. (2014), Camadan et al. (2018), De-varaj et al. (2008), Krishnan et al. (2010), McElroy et al. (2007), Panda and Jain (2018) and Svendsen et al. (2013), have already examined the influence of personal characteristics on technology use in various contexts. However, studies of the influence of personality elements on technology adoption through the lens of the De-Lone and McLean (2003) information systems (IS) success model are limited, thus presenting another knowledge gap that this study seeks to address.

Relationships between the IS success model's three quality measures and use have been empirically validated in previous studies. For example, Mohammadi (2015) finds that all three quality measures influence the use of e-learning; and Rana et al. (2015) find that the three quality measures influence the use of online public grievance redress systems. Accordingly, for this study, it was expected that each of the three quality measures would influence the use of the mobile banking app. Hence, the following hypotheses were tested:

H1: System quality has a positive influence on the use of mobile banking apps.

H2: Service quality has a positive influence on the use of mobile banking apps.

H3: Information quality has a positive influence on the use of mobile banking apps.

Relationships between the IS success model's three quality measures and user satisfaction are also well-documented in previous studies, including the aforementioned Mohammadi (2015) and Rana et al. (2015) studies, and in the work of Freeze et al. (2019) and Gao and Park (2017). In connection with the above findings, the following hypotheses emerged:

H4: System quality has a positive influence on user satisfaction with mobile banking apps.

H5: Service quality has a positive influence on user satisfaction with mobile banking apps.

H6: Information quality has a positive influence on user satisfaction with mobile banking apps.

Furthermore, the consequent effects of both actual use and user satisfaction could ultimately impact user individual performance based on the net benefits of using mobile banking apps. The user could continue using the mobile banking app if the net benefits are positive or, in other words, if the mobile banking app continues to help the customer or user to achieve individual performance.

User satisfaction is defined as a sum of feelings or an affective response regarding the effectiveness of a particular technology to accomplish a given task (Gatian, 1994; Melone, 1990). In the context of this study, user satisfaction is achieved if the user feels that the mobile banking apps have effectively helped him or her to accomplish banking-related tasks. The relationship between user satisfaction and individual performance is also demonstrated in previous studies such as those of Gelderman (1998) and Isaac et al. (2017). The influence of a user's actual use of information systems on individual performance is reported in studies such as Tam and Oliveira (2016). Furthermore, literature strikes a close relationship between perceived user satisfaction and actual use of information systems or ICT in general. It has been demonstrated that as the perceived satisfaction of using information systems increases, the desire to use mobile banking apps could also shoot up. Examples of empirical findings demonstrating this relationship include those generated by AL Athmay et al. (2016) and Byun and Finnie (2011). Based on the findings of previous studies, the following hypotheses were developed:

H7: User satisfaction with mobile banking apps has a positive influence on individual performance.

H8: Use of the mobile banking apps has a positive influence on individual performance.

H9: User satisfaction with mobile banking apps has a positive influence on the use of the apps.

Thefive-factor model

Personality characteristics refer to cognitive behaviour patterns in facets of general tendencies that govern an individual's thoughts, feelings, and actions (Krishnan et al., 2010; Maddi, 1996). These personality traits play an important role in IS adoption as they affect how information systems are used (Halko & Kientz, 2010; Rosen & Kluemper, 2008). There are many personal characteristics in the psychology literature, however, the current study investigates the direct effects of the "big five" personality traits on the use of mobile banking apps. These five traits are: conscientiousness, openness, extraversion, neuroticism, and agreeableness (taken from Digman, 1990). Previous studies suggest that the five-factor model (FFM) is effective in explorations of the effects of personal characteristics, with a good predictive ability (Chang et al., 2012). The influence of the big five personality traits has been rarely studied in the mobile banking apps context, despite their potential importance in understanding differences in user behaviour.

Conscientiousness encompasses an individual's predisposition to be cautious, organised, hardworking, abiding by rules, and reliable. Thus, conscientious individuals organise themselves to perform tasks with a high level of discipline, and do so cautiously and reliably. Since this group of individuals is self-disciplined, cautious and reliable, they are likely to use mobile banking apps productively to perform banking-related tasks. The empirical finding also indicates that conscientiousness influences the productive use of internet resources (Landers & Lounsbury, 2006) and IT system usage (Barnett et al., 2014). Therefore, the resulting hypothesis was:

H10: Conscientiousness has a positive influence on the use of mobile banking apps.

Openness includes an individual's inquisitiveness, willingness to experiment, and inclination to engage and to explore new ideas and the surrounding world (McCrae, 1993; McCrae & Terracciano, 2005). These individuals are likely to try new technology in pursuit of a better way to accomplish the tasks at hand. Similarly, it is expected that open-minded individuals are likely to use mobile banking apps in an attempt to explore the bank-related functions and services offered through mobile banking apps. The association between an individual's openness and eagerness to use technology is reported in various IS studies such as Tuten and Bosnjak (2001) and Kim and Jeong (2015). Hence, consistent with such previous studies, it was hypothesised that:

H11: Openness has a positive influence on the use of mobile banking apps.

Extraversion refers to individuals who are social, affectionate, cheerful, and optimistic. They easily get themselves involved in seeking affiliation in the social environment in a quest to achieve a particular goal. Hence, they are more likely to use technology that will help them to achieve goals (Shambare, 2013). For this reason, extroverts are likely to use mobile banking apps to achieve socially related goals. The connection between extraversion and technology use is well reported in the works of Loiacono (2015) and Leonidas et al. (2019). Therefore, it was hypothesised that:

H12: Extraversion has a positive influence on the use of mobile banking apps.

Neuroticism reflects emotional instability, negativity, sadness, and difficulty with dealing with all sorts of stress. Since neurotic individuals are inclined to negative perceptions and emotional instability, they tend to perceive technology as stressful and difficult to use, and as a result they tend to avoid and oppose using it (Rosen & Klue-mper, 2008). Similar findings which support the relationship between neuroticism and information systems usage include those of Loiacono (2015) and Barnett et al. (2014). Hence, it was hypothesised that:

H13: Neuroticism has a negative influence on the use of mobile banking apps.

Agreeableness embodies the tendency of individuals to be compassionate, tolerant, good-natured, forgiving, and cooperative. IS literature indicates that agreeableness is positively linked to technology use. It has been found that agreeable individuals patiently use technology that is slightly difficult to use, such as a website that is onerous to navigate (Landers & Lounsbury, 2006). Loiacono (2015) reports that agreeable people are more likely to use the internet and social networking sites. Accordingly, it was hypothesised that:

H14: Agreeableness has a positive influence on the use of mobile banking apps.

The research framework for the study, based on the 14 hypotheses, is illustrated in Figure 1.

4. Methodology

Instrument development

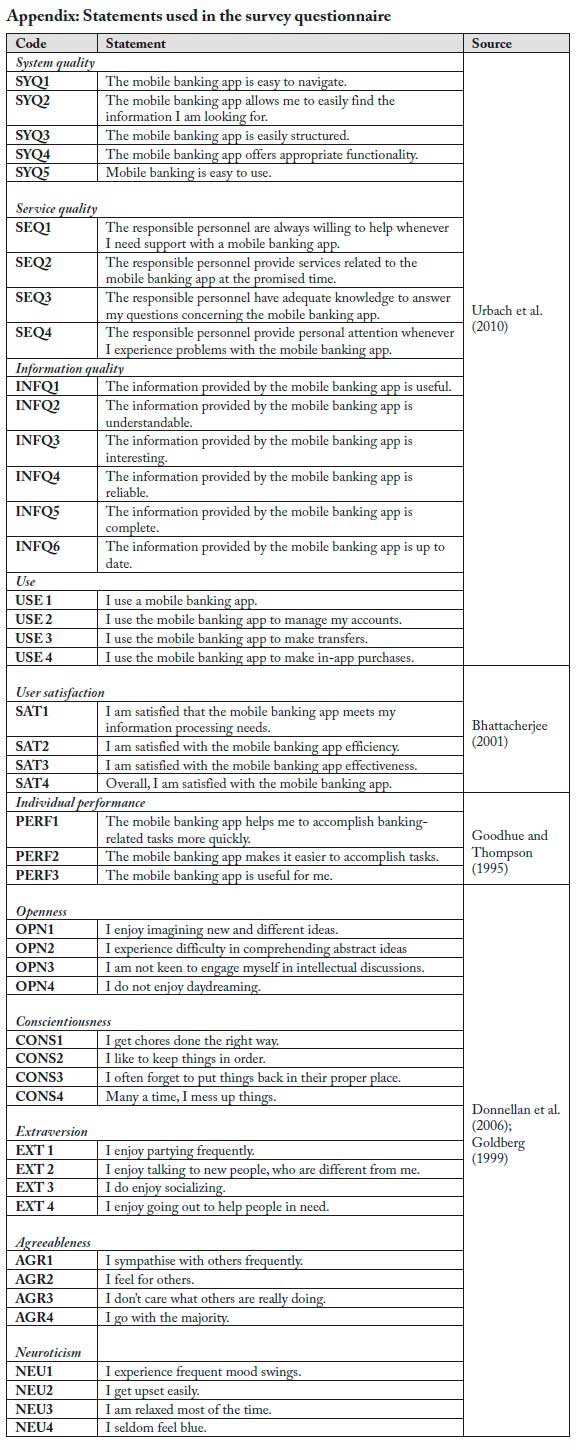

The data collection questionnaire had two parts. The first part consisted of items for measuring respondent perceptions of the use of mobile banking apps, and the second part consisted of items aimed at gathering demographic information. Items on the perceptions of respondents (see Appendix) were borrowed from previous studies and adjusted to match the setting of this study. Items for measuring user perceptions of system quality, service quality, information quality and use were based on those used by Urbach et al. (2010); items for measuring a user's performance were based on those used by Goodhue and Thompson (1995); items for measuring user satisfaction were based on those used by Bhattacherjee (2001), and items for measuring conscientiousness, openness, agreeableness, extraversion, and neuroticism were based on those used by Donnellan et al. (2006) and Goldberg (1999).

All the items for measuring respondent perceptions consisted of statements (see Appendix), each of which respondents rated via a five-point Likert scale ranging from 1 (strongly disagree) to 5 (strongly agree). Prior to its use with respondents, the questionnaire was sent to five information system experts and five experienced banking services personnel to check content validity. The comments provided by these individuals informed the finalisation of the questionnaire.

Study sample, data collection

The study sample consisted of Tanzanian users of mobile banking apps from five regions: Dar es Salaam, Arusha, Mwanza, Dodoma, and Kilimanjaro. These regions host the majority of the country's bank branches. A judgmental sampling method was employed during the selection of respondents. Respondents were selected based on two criteria: (1) experience of using mobile banking apps for six months or more; and (2) habit of using mobile banking apps at least once per week.

The population of respondents who met the selection criteria for this study is large and unknown. In this situation, it is recommended that the Cochran formula for the unknown population be applied to determine the appropriate sample size for

the study (Cochran, 1977). Using the Cochran formula, IMAGEMAQUI (where Z is the confidence level,p = expected proportion, and e = margin error), the sample size of the study was 384 respondents. This study set Z = 1.96 at 95% confidence level, margin error in a proportion of one, if 5%, e = 0.05 and expected proportion in a proportion of one, p = 0.5.

The questionnaire was self-administered to the targeted respondents. Out of 384 questionnaires, 249 questionnaires were completed. Before data analysis, the collected questionnaires were checked for missing data using the missing completely at random (MCAR) test (Little, 1988). The test result was not significant (x2= 178.733, df = 160, p = 0.148), indicating that there were randomly missing data. Missing data were replaced by estimating maximum likelihood using the expectation-maximisation (EM) approach.

5. Results

Descriptive findings

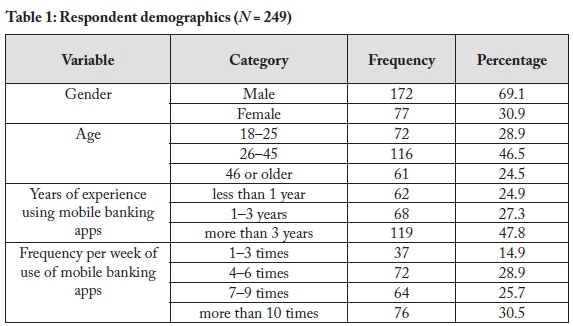

Table 1 provides demographic information-gender, age, years of experience using mobile banking apps, and frequency per week of use of the apps-for the 249 respondents.

Assessment of the measurement and structural models

The study used covariance-based structural equation modelling (CB-SEM) to assess both the measurement model and the structural model. The study followed a two-stage approach, as recommended by Anderson and Gerbing (1988): (1) assessment of the measurement model; and (2) assessment of the structural model.

Assessment of the measurement model

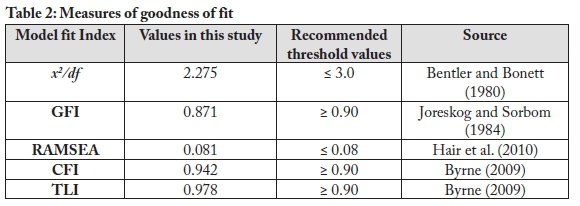

To assess the measurement model, the study used model fit indices from each category of model fit indices as defined by Hair et al. (2010). Specifically, the study used Root Mean Square of Error Approximation (RAMSEA) and Goodness of Fit Index (GFI) from the absolute fit category, Comparative Fit Index (CFI) and Tucker-Lewis index (TLI) from the incremental fit category, and x2/df (Chi-square/f from the parsimonious fit category. In the first stage, the study found that the measurement model demonstrated adequate psychometric properties after dropping INFOQ3 and INFOQ5 from information quality and EXT2 from extraversion constructs due to low factor loadings. The results of the goodness of fit for the entire model and acceptable thresholds are reported in Table 2.

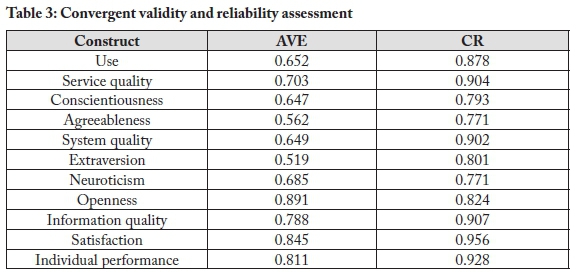

Convergent and discriminant validity was used to assess the measurement model and composite reliability (CR) was used to assess reliability. Table 3 indicates the results of convergent validity and reliability assessment. The results of convergent validity indicate that the average variance extracted (AVE) values for the constructs are great than 0.5, implying that the measurement items for each construct are theoretically related to each other (Fornell & Larcker, 1981) and the values for composite reliability are all above 0.7, implying that the measurement items have met the reliability threshold (Nunnally & Bernstein, 1994).

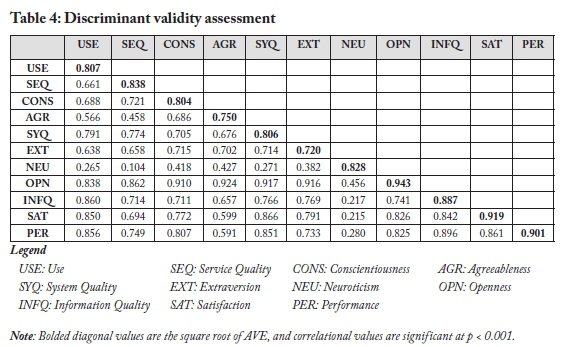

Concerning discriminant validity, the results confirm that the constructs of the study were distinct from each other since the intercorrelations of the constructs did not exceed the square root of the AVE of the constructs. Results of discriminant validity are reported in Table 4.

Assessment of the structural model, and hypothesis testing

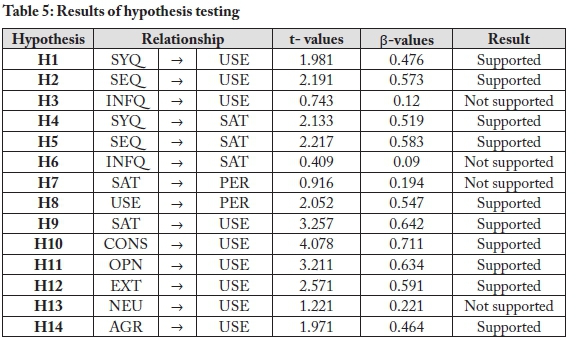

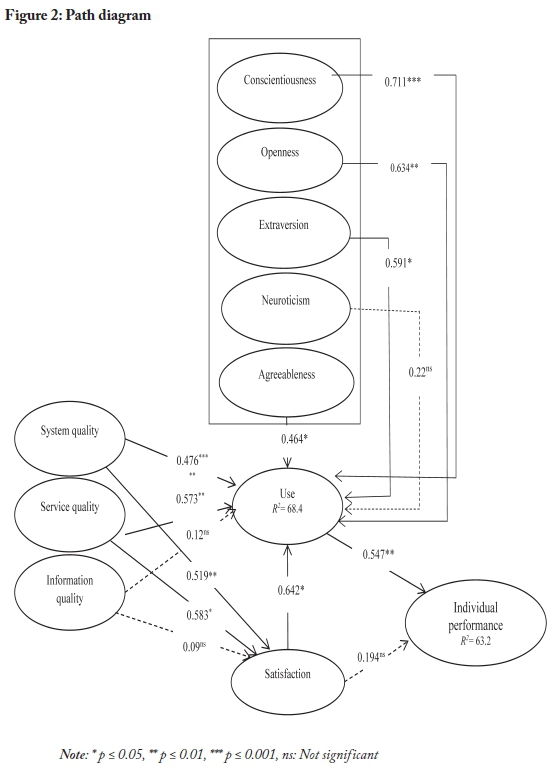

In the second stage, the study assessed the structural model using the same model fit indices used in the assessment of the measurement model. The assessment of the structural model yielded the following goodness of fit: x?/df = 2.267, RAMSEA = 0.083, GFI = 0.870, CFI = 0.940, and TLI = 0.976. The model fit indices indicate that there is an adequate structural fit between the hypothesised model and the observed data. The explained variance (R2) in use is 63.2% and in individual performance is 68.4%, suggesting that the model has good explanatory power as compared to similar studies and is good enough to produce substantial effects (Cohen, 1988). Results of hypothesis testing and the resulting path diagram are provided in Table 5 and Figure 2, respectively.

6. Discussion

Unsupported hypotheses

Four of the 10 hypotheses were not supported by the findings:

• H3: Information quality positively influences the use of mobile banking apps.

• H6: Information quality positively influences user satisfaction with mobile banking apps.

• H7: User satisfaction with mobile banking apps has a positive influence on individual performance.

• H13: Neuroticism has a negative influence on the use of mobile banking apps.

Information quality and use (H3), information quality and user satisfaction (H6) One of the three DeLone and McLean (2003) quality measures-information quality-was found to not have a positive influence on either use or user satisfaction with the use of mobile banking apps. (Under information quality, the survey (see Appendix) probed the extent to which users found the information in the apps useful, understandable, interesting, reliable, complete, and up to date).This finding, which suggests that the surveyed users perceived the quality of the information provided by the mobile banking apps as being unsatisfactory and thus a disincentive to using the apps, appears to resonate with the findings of Chiu et al. (2016) on the adoption of mobile banking services in Philippines. Also, the study by Franque et al. (2021) in Mozambique finds that information quality had a positive influence on the use of mobile banking services, and the study by Kumar and Sharma (2019) in Oman finds that information quality had a positive influence on user satisfaction with such services.

User satisfaction and individual performance (H7)

Contrary to the study's expectations and the literature, user satisfaction was not found to positively influence individual performance-though it does, as seen later in this section, positively influence the use of mobile banking apps.

Neuroticism and use (H13)

Neuroticism was found to have no significant influence on the respondents' use of mobile banking apps. This finding appears to contrast with findings from several other studies. For example, studies by Loiacono (2015) in Italy and Ashraf (2019) in Lebanon find that neuroticism had a significant influence on, respectively, the intention to use social networking websites and the intention to use mobile banking. An earlier study, by Rosen and Kluemper (2008) in the US, finds that neurotics often perceive new technology negatively.

Supported hypotheses

Ten of the hypotheses-all except the four hypotheses discussed in the previous sub-section-were supported by the research findings.

Openness

The study found that openness has a positive influence on the use of Tanzanian mobile banking apps. It is plausible that mobile banking users consider the use of the apps to be a new experience and therefore they are attracted to using them. This finding would appear to be consistent with findings in studies by Kim and Jeong (2015) in South Korea and by McElroy et al. (2007) in the US, which find openness to be positively related to internet use, but the finding appears to contrast with the Barnett et al. (2014) finding that openness is unrelated to technology acceptance.

Conscientiousness

Similar to findings by Moslehpour et al. (2018) on the intention of Taiwanese to purchase goods and services online, this study found that conscientiousness positively influences Tanzanians' use of mobile banking apps. It is possible that this finding stems from a belief that using mobile banking apps can improve financial management discipline and offer greater reliability in making business transactions.

Extraversion

Extraversion was also found to have a positive influence on the use of mobile banking apps, a finding that appears to be consistent with findings from several previous studies, such as the Panda and Jain (2018) study of the obsessive use of smartphones among young Indians, and the Lissitsa and Kol (2021) study of mobile shopping among members of the so-called "generation Y" (i.e., people reaching adulthood at the turn of the millennium) in Israel. Devaraj et al. (2008) find that because extraverts are socially inclined, outgoing, and like to create connections, they are amenable to the use of advanced technology to achieve socially oriented goals.

Agreeableness

The core of agreeableness behaviour is maintaining a positive relationship with others (Graziano & Eisenberg, 1997). Given the importance of one's relationship with one's bank, the respondents could reasonably be expected to choose to use the mobile banking apps, upon being introduced to them by their respective banks, to maintain their relationship with their banks. This finding appears to be consistent with that of Khan et al. (2019) on the use of mobile payment systems in China.

System quality and use, service quality and use

Two of the three DeLone and McLean (2003) IS quality measures-system quality and service quality-were found to positively influence the use of mobile banking apps. These findings appear to be in line with previous studies in technology acceptance literature. For example, Mohammadi (2015) finds that these two factors influenced the use of e-learning in Iran.

System quality and user satisfaction, service quality and user satisfaction Two of the three DeLone and McLean (2003) IS quality measures-system quality and service quality-were also found to positively influence user satisfaction with the use of mobile banking apps. This finding apparently aligns with that of Veeramootoo et al. (2018) on the use of e-government services in Mauritius.

User satisfaction and use

Unsurprisingly, user satisfaction was found to positively influence use, a finding that appears to be consistent with the findings of Shim and Jo (2020), who investigated the use of health informatics sites in South Korea.

Limitations and further studies

This study was conducted with respondents living in a single country, Tanzania. Future studies would benefit from involving respondents from more than one country, so as to account for the effects of national and cultural differences on the final results. Also, some of the studied constructs, particularly those used to measure personality traits, may have been perceived by some respondents as carrying a negative meaning. Hence, their responses could have been influenced by notions of social acceptability. Future studies could supplement questionnaire data with an additional data source in using a combination of data collection methods to overcome the potential common methods biases.

7. Conclusions

The study offers a research framework which combines the consideration of personality traits and IS success factors in influencing Tanzanians' use of, and satisfaction with, mobile banking apps. This model enhances our understanding of the influence of personality traits on the acceptance of mobile banking apps. Studies which have studied these traits in the context of the IS success model, particularly in the African context, are limited. This study's identification of strong positive relationships between four personality traits-openness, agreeableness, conscientiousness, and extra-version-and both use and user satisfaction suggests that banks can benefit from ensuring that users can give full expression to their personalities when using the apps. If developers can design mobile banking apps which allow each customer to have a sense of expressing their unique personality traits, the customer's use and user satisfaction can be expected to increase.

Also of potential value to developers is the finding that one of the three IS success factors-information quality-is not at present positively influencing Tanzanian mobile banking users. This is an apparent indication that developers of mobile banking apps for the Tanzanian market need to place greater emphasis on ensuring that the information provided is, according to the terms used in the survey, useful, understandable, interesting, reliable, complete, and up to date.

References

AL Athmay, A. A. A., Fantazy, K., & Kumar, V. (2016). E-government adoption and user's satisfaction: An empirical investigation. EuroMedJournal of Business, 11(1), 57-83. https://doi.org/10.1108/EMJB-05-2014-0016 [ Links ]

Alavi, S., & Ahuja, V. (2016). An empirical segmentation of users of mobile banking apps. Journal of Internet Commerce, 15(4), 390-407. https://doi.org/10.1080/15332861.2016.1252653 [ Links ]

Anderson, J. C., & Gerbing, D. W. (1988). Structural equation modelling in practice: A review and recommended two-step approach. Psychological Bulletin, 103(3), 411-423. https://doi.org/10.1037/0033-2909.103.3.411 [ Links ]

Ashraf, H. (2019). Factors that Influence the use of Mobile Banking in Lebanon: Integration of UTAUT2 and 3MModel. Universidade de Santiago de Compostela.

Barnett, T., Allison, W., Pearson, R., & Kellermanns, F. W. (2014). Five-factor model personality traits as predictors of perceived and actual usage of technology. European Journal of Information Systems, 24(4), 374-390. https://doi.org/10.1057/ejis.2014.10 [ Links ]

Bennett, J., & Perrewé, P. L. (2002). An empirical examination of individual traits as antecedents to computer anxiety and computer self-efficacy. MIS Quarterly, 26(4), 381-396. https://doi.org/10.2307/4132314 [ Links ]

Bentler, P. M., & Bonett, D. G. (1980). Significance tests and goodness of fit in the analysis of covariance structures. Psychological Bulletin, 88(3), 588-606. https://doi.org/10.1037/0033-2909.88.3.588 [ Links ]

Bhattacherjee, A. (2001). Understanding information systems continuance: An expectation-confirmation model. MIS Quarterly, 25(3), 351-370. https://doi.org/10.2307/3250921 [ Links ]

Bond, M. H. (1983). Linking person perception dimensions to behavioral intention dimensions: The Chinese connection. Journal of Cross-Cultural Psychology, 14(1), 41-63. https://doi.org/10.1177/0022002183014001004 [ Links ]

Bond, M. H., & Forgas, J. P. (1984). Linking person perception to behavior intention across cultures: The role of cultural collectivism. Journal of Cross-Cultural Psychology, 15(3), 337-352. https://doi.org/10.1177/0022002184015003006 [ Links ]

Byrne, B. M. (2009). Structural equation modeling with AMOS: Basic concepts, applications, and programming (2nd ed.). Routledge.

Byun, D. H., & Finnie, G. (2011). Evaluating usability, user satisfaction and intention to revisit for successful e-government websites. Electronic Government, 8(1), 1-19. https://doi.org/10.1504/EG.2011.037694 [ Links ]

Camadan, F., Reisoglu, I., Faruk, U. Ö., & Mcilroy, D. (2018). How teachers['] personality affect on their behavioral intention to use tablet PC. The International Journal of Information and Learning Technology Article Information, 35(1), 12-28. https://doi.org/10.1108/IJILT-06-2017-0055 [ Links ]

Chang, L., Connelly, B. S., & Geeza, A. A. (2012). Separating method factors and higher order traits of the big five: A meta-analytic multitrait-multimethod approach. Journal of Personality and Social Psychology, 102(2), 408-427. https://doi.org/10.1037/a0025559 [ Links ]

Chiu, P. S., Chao, I. C., Kao, C. C., Pu, Y. H., & Huang, Y. M. (2016). Implementation and evaluation of mobile e-books in a cloud bookcase using the information system success model. Library Hi Tech, 34(2), 207-223. https://doi.org/10.1108/LHT-12-2015-0113 [ Links ]

Chmielarz, W., & tuczak, K. (2015). Mobile banking in the opinion of users of banking applications in Poland. Applied Mechanics and Materials, 795, 31-38. https://doi.org/10.4028/www.scientific.net/AMM.795.31 [ Links ]

Clickpesa. (2019). An overview of Consumer Financial Apps in Tanzania. https://clickpesa. com/financial-apps-tanzania/

Cochran, W. (1977). Sampling techniques (3rd ed.). John Wiley & Sons.

Cohen, J. (1988). Statistical power analysis for the behavioral sciences (2nd ed.). Hillsdale.

DeLone, W. H., & McLean, E. R. (2003). The DeLone and McLean model of information systems success: A ten-year update. Journal of Management Information Systems, 19(4), 9-30. https://doi.org/10.1080/07421222.2003.11045748 [ Links ]

Devaraj, S., Easley, R. F., & Crant, J. M. (2008). How does personality matter? Relating the five-factor model to technology acceptance and use. Information Systems Research, 19(1), 93-105. https://doi.org/10.1287/isre.1070.0153 [ Links ]

Digman, J. M. (1990). Personality structure: Emergence of the five-factor model. Annual Review of Psychology, 41(1), 417-440. https://doi.org/10.1146/annurev.ps.41.020190.002221 [ Links ]

Donnellan, M. B., Oswald, F. L., Baird, B. M., & Lucas, R. E. (2006). The mini-IPIP scales: Tiny-yet-effective measures of the big five factors of personality. Psychological Assessment, 18(2), 192-203. https://doi.org/10.1037/1040-3590.18.2.192 [ Links ]

Dudley, N. M., Orvis, K. A., Lebiecki, J. E., & Cortina, J. M. (2006). A meta-analytic investigation of conscientiousness in the prediction of job performance: Examining the intercorrelations and the incremental validity of narrow traits. Journal of Applied Psychology, 91(1), 40-57. https://doi.org/10.1037/0021-9010.91.L40 [ Links ]

Dukic, Z., Chiu, D., & Lo, P. (2015). How useful are smartphones for learning? Perceptions and practices of Library and Information Science students from Hong Kong and Japan. Library Hi Tech, 33(4), 545-561. https://doi.org/10.1108/LHT-02-2015-0015 [ Links ]

Fife, E., & Orjuela, J. (2012). The privacy calculus: Mobile apps and user perceptions of privacy and security regular paper. International Journal of Engineering Business, 4(11), 1-10. https://doi.org/10.5772/51645 [ Links ]

Floh, A., & Treiblmaier, H. (2006). What keeps the e-banking customer loyal? A multigroup analysis of the moderating role of consumer characteristics on e-loyalty in the financial service industry. Journal of Electronic Commerce Research, 7(2), 97-110. https://doi.org/10.2139/ssrn.2585491 [ Links ]

Fornell, C., & Larcker, D. (1981). Evaluating structural equation models with unobservable variables and measurement error. Journal of Marketing Research, 18(1), 39-50. https://doi.org/10.1177/002224378101800104 [ Links ]

Franque, F. B., Oliveira, T., & Tam, C. (2021). Understanding the factors of mobile payment continuance intention: empirical test in an African context. Heliyon, 7(8), 1-12. [ Links ]

Freeze, R. D., Lane, P. L., & Wen, H. J. (2019). IS success model in e-learning context based on students' perceptions. Journal of Information Systems Education, 21(2), 173-185. [ Links ]

Gaardboe, R., Nyvang, T., & Sandalgaard, N. (2017). Business intelligence success applied to healthcare information systems. Procedia Computer Science, 121, 483-490. https://doi.org/10.1016/j.procs.2017.11.065 [ Links ]

Gao, L., & Park, A. T. (2017). Understanding sustained participation in virtual travel communities from the perspectives of IS success model and flow theory. Journal of Hospitality and Tourism Research, 41(4), 475-509. https://doi.org/10.1177/1096348014563397 [ Links ]

Gatian, A. W. (1994). Is user satisfaction a valid measure of system effectiveness? Information & Management, 26(3), 119-131. https://doi.org/10.1016/0378-7206(94)90036-1 [ Links ]

Gelderman, M. (1998). The relation between user satisfaction, usage of information systems and performance. Information & Management, 34(1), 11-18. https://doi.org/10.1016/S0378-7206(98)00044-5 [ Links ]

Gilbert, P., Cox, L. P., Chun, B.-G., & Jung, J. (2011). Vision: Automated security validation of mobile apps at app markets. In Proceedings of the Second International Workshop on Mobile Cloud Computing and Services (pp. 21-26). https://doi.org/10.1145/1999732.1999740

Godwin-Jones, R. (2011). Emerging technologies mobile apps for language learning. Language Learning & Technology, 15(2), 2-11. [ Links ]

Goldberg, L. (1999). A broad-bandwidth, public-domain, personality inventory measuring the lower-level facets of several five-factor models. In I. Mervielde, I. Deary, F. De Fruyt, & F. Ostendorf (Eds.), Personality psychology in Europe (Vol. 7) (pp. 7-28). Tilburg University Press.

Goodhue, D. L., & Thompson, R. L. (1995). Task-technology fit and individual. MIS Quarterly, 19(2), 213-236. https://doi.org/10.2307/249689 [ Links ]

Graziano, W. G., & Eisenberg, N. (1997). Agreeableness: A dimension of personality. In R. Hogan, J. Johnson, & S. Briggs (Eds.), Handbook of personality psychology (pp. 795-824). Elsevier. https://doi.org/10.1016/B978-012134645-4/50031-7

GSMA. (2021). The mobile economy 2021. https://www.gsma.com/mobileeconomy/wp-con-tent/uploads/2021/07/GSMAMobileEconomy20213.pdf

Hair, J., Black, W. C., Babin, B. J., & Anderson, R. E. (2010). Multivariate data analysis: A global perspective (7th ed.). Prentice-Hall.

Halko, S., & Kientz, J. A. (2010). Personality and persuasive technology: An exploratory study on health-promoting mobile applications. In T. Ploug, P. Hasle, & H. Oinas-Kuk- konen (Eds.), Persuasive technology: 5th International Conference, PERSUASIVE 2010, Copenhagen, Denmark, June 7-10, 2010:Proceedings (pp. 150-161). https://doi.org/10.1007/978-3-642-13226-1 16

Hepola, J., Karjaluoto, H., & Shaikh, A. A. (2016). Consumer engagement and behavioral intention toward continuous use of innovative mobile banking applications-A case study of Finland. In Thirty Seventh International Conference on Information Systems, Dublin (pp. 1-20).

Hong, W., Thong, J. Y. L., & Wai-Man Wong, K.-Y. T. (2002). Determinants of user acceptance of digital libraries: An empirical examination of individual differences and system characteristics. Journal of Management Information Systems, 18(3), 97-124. https://doi.org/10.1080/07421222.2002.11045692 [ Links ]

Hu, P.-H. (2003). Evaluating telemedicine systems success: A revised model. In 36th Annual Hawaii International Conference on System Sciences, 2003. https://doi.org/10.1109/HICSS.2003.1174379

Inukollu, V. N., Keshamoni, D. D., Kang, T., & Inukollu, M. (2014). Factors influencing quality of mobile apps: Role of mobile app development life cycle. International Journal of Software Engineering & Applications (IJSEA), 5(5), 15-34. https://doi.org/10.5121/ijsea.2014.5502 [ Links ]

Isaac, O., Abdullah, Z., Ramayah, T., & Mutahar, A. M. (2017). Internet usage, user satisfaction, task-technology fit, and performance impact among public sector employees in Yemen. The International Journal of Information and Learning Technology, 34(3), 210-241. https://doi.org/10.1108/IJILT-11-2016-0051 [ Links ]

Jain, A. K., & Shanbhag, D. (2012). Addressing security and privacy risks in mobile applications. IT Professional, 14(5), 28-33. https://doi.org/10.1109/MITP.2012.72 [ Links ]

Joreskog, K., & Sorbom, D. (1984). LISREL VI user's guide (3rd ed.). Scientific Software.

Keyes, D. (2019, July 2). WhatsApp Pay is on the verge of launching in India. Business Insider. https://www.businessinsider.com/whatsapp-pay-ready-for-india-launch-2019-7?IR=T

Khan, A. N., Xiongfei, C. & Pitafi, H. (2019). Personality traits as predictor of m-payment systems: A SEM-neural networks approach. Journal of Organizational and End User Computing, 31(4), 89-110. https://doi.org/10.4018/JOEUC.2019100105 [ Links ]

Kim, M., Chang, Y., Park, M., & Lee, J. (2015). The effects of quality on the satisfaction and the loyalty of smartphone users. Telematics and Informatics, 32(4), 949-960. https://doi.org/10.1016/j.tele.2015.05.003 [ Links ]

Kim, Y., & Jeong, J. S. (2015). Personality predictors for the use of multiple internet functions. Internet Research, 25(3), 399-415. https://doi.org/10.1108/IntR-11-2013-0250 [ Links ]

Krishnan, S., Lim, V. K. G., & Tao, T. S. H. (2010). How does personality matter? Investigating the impact of big-five personality traits on cyberloafing. In International Conference on Information Systems (pp. 1-16). https://scholarbank.nus.edu.sg/han-dle/10635/44246

Kumar, R. R., Israel, D., & Malik, G. (2018). Explaining customer's continuance intention to use mobile banking apps with an integrative perspective of ECT and self-determination theory. Pacific Asia Journal of the Association for Information Systems, 10(2). https://doi.org/10.17705/1pais.10204 [ Links ]

Kumar, S., & Sharma, M. (2019). Examining the role of trust and quality dimensions in the actual usage of mobile banking services : An empirical investigation. International Journal of Information Management, 44, 65-75. https://doi.org/10.1016/jijinfomgt.2018.09.013 [ Links ]

Landers, R. N., & Lounsbury, J. W. (2006). An investigation of big five and narrow personality traits in relation to internet usage. Computers in Human Behavior, 22(2), 283-293. https://doi.org/10.1016/jxhb.2004.06.001 [ Links ]

Leonidas, H., Misirlis, N., Arnhem, H., Boutsouki, C., & Vlachopoulou, M. (2019). Understanding the role of personality traits on Facebook intensity. International Journal of Internet Marketing and Advertising, 13(2), 99-119. https://doi.org/10.1504/IJIMA.2019.099494 [ Links ]

Lissitsa, S., & Kol, O. (2021). Four generational cohorts and hedonic m-shopping: association between personality traits and purchase intention. Electronic Commerce Research, 21(2), 545-570. [ Links ]

Little, R. J. A. (1988). A test of missing completely at random for multivariate data with missing values. Journal of the American Statistical Association, #3(404), 1198-1202. https://doi.org/10.1080/01621459.1988.10478722 [ Links ]

Loiacono, E. T. (2015). Self-disclosure behavior on social networking web sites. International Journal of Electronic Commerce, 19(2), 66-94. [ Links ]

Luo, X., Li, H., Zhang, J., & Shim, J. P. (2010). Examining multi-dimensional trust and multi-faceted risk in initial acceptance of emerging technologies: An empirical study of mobile banking services. Decision Support Systems, 49, 222-234. https://doi.org/10.1016/j.dss.2010.02.008 [ Links ]

Maddi, S. R. (1996). Personality theories: A comparative analysis. Brooks/Cole.

Manuel, J., & Veríssimo, C. (2016). Enablers and restrictors of mobile banking app use: A fuzzy set qualitative comparative analysis (fsQCA). Journal of Business Research, 69(11), 5456-5460. https://doi.org/10.1016/j.jbusres.2016.04.155 [ Links ]

McCrae, R. R. (1993). Openness to experience as a basic dimension of personality. Imagination, Cognition and Personality, 13(1), 39-55. https://doi.org/10.2190/H8H6-QYKR-KEU8-GAQ0 [ Links ]

McCrae, R. R., & Terracciano, A. (2005). Universal features of personality traits from the observer's perspective: Data from 50 cultures. Journal of Personality and Social Psychology, 88(3), 547. https://doi.org/10.1037/0022-3514.88.3.547 ' [ Links ]

McElroy, J. C., Hendrickson, A. R., Townsend, A. M., & DeMarie, S. M. (2007). Dispositional factors in internet use: Personality versus cognitive style. MIS Quarterly, 31(4), 809-820. https://doi.org/10.2307/25148821 [ Links ]

Melone, N. P. (1990). A theoretical assessment of the user-satisfaction construct in information systems research. Management Science, 36(1), 76-91. https://doi.org/10.1287/mnsc.36.L76 [ Links ]

Mohammadi, H. (2015). Investigating users' perspectives on e-learning: An integration of TAM and IS success model. Computers in Human Behavior, 45, 359-374. https://doi.org/10.10167j.chb.2014.07.044 [ Links ]

Moslehpour, M., Thi Thanh, H. Le, & Van Kien, P. (2018). Technology perception, personality traits and online purchase intention of Taiwanese consumers. In International Conference of the Thailand Econometrics Society (pp. 392-407). https://doi.org/10.1007/978-3-319-70942-028

Munoz-Leiva, F., Climent-Climent, S., & Liébana-Cabanillas, F. (2017). Determinants of intention to use the mobile banking apps: An extension of the classic TAM model. Spanish Journal of Marketing, 21(1), 25-38. https://doi.org/10.1016/j.sjme.2016.12.001 [ Links ]

Njoroge, C. N., & Koloseni, D. (2015). Adoption of social media as full-fledged banking channel: An analysis of retail banking customers in Kenya. International Journal of Information and Communication Technology Research, 5(2), 1-12. [ Links ]

Nunnally, J. C., & Bernstein, I. (1994). Psychometric theory. McGraw-Hill.

Ones, D. S., & Viswesvaran, C. (1996). Bandwidth-fidelity dilemma in personality measurement for personnel selection. Journal of Organizational Behavior, 17(6), 609-626.https://doi.org/10.1002/(SICI)1099-1379(199611)17:6<609::AID-JOB1828>3.0.CO;2-K [ Links ]

Panda, A., & Jain, N. K. (2018). Compulsive smartphone usage and users' ill-being among young Indians: Does personality matter? Telematics and Informatics, 35(5), 13551372. https://doi.org/10.1016/j.tele.2018.03.006 [ Links ]

Pituch, K. A., & Lee, Y. (2006). The influence of system characteristics on e-learning use. Computers & Education, 47, 222-244. https://doi.org/10.1016/jxompedu.2004.10.007 [ Links ]

Podsakoff, P. M., MacKenzie, S. B., & Podsakoff, N. P. (2012). Sources of method bias in social science research and recommendations on how to control it. Annual Review of Psychology, 63, 539-569. https://doi.org/10.1146/annurev-psych-120710-100452 [ Links ]

Ramayah, T., Wai, J., & Lee, C. (2012). System characteristics, satisfaction and e-learning usage: A structural equation model. The Turkish Online Journal of Educational Technology, 11(2), 26-28. [ Links ]

Rana, N., Dwivedi, Y., Williams, M., & Weerakkody, V. (2015). Investigating success of an e-government initiative: Validation of an integrated IS success model. Information Systems Frontiers, 17(1), 127-142. https://doi.org/10.1007/s10796-014-9504-7 [ Links ]

Rosen, P. A., & Kluemper, D. H. (2008). The impact of the big five personality traits on the acceptance of social networking website. In AMCIS 2008 Proceedings (pp. 1-10). https://citeseerx.ist.psu.edu/viewdoc/download?doi=10.1.1.909.2632&rep=rep1&-type=pdf

Sampaio, C. H., Ladeira, W. J., & Santini, F. D. O. (2017). Apps for mobile banking and customer satisfaction: A cross-cultural study. International Journal of Bank Marketing, 35(7), 1133-1153. https://doi.org/10.n08/ITBM-09-2015-0146 [ Links ]

Sangar, A. B., & Rastari, S. (2015). A model for increasing usability of mobile banking apps on smart phones. Indian Journal of Science and Technology, 8(30), 1-9. https://doi.org/10.17485/ijst/2015/v8i30/85690 [ Links ]

Shambare, N. (2013). Examining the influence of personality traits on intranet portal adoption by faculty in higher education. PhD dissertation, Northcentral University, San Diego, CA. [ Links ]

Shim, M., & Jo, H. S. (2020). What quality factors matter in enhancing the perceived benefits of online health information sites? Application of the updated DeLone and McLean information systems success model. International Journal of Medical Informatics, 137. https://doi.org/10.1016/j.ijmedinf.2020.104093 [ Links ]

Svendsen, G. B., Johnsen, J. A. K., Almâs-S0rensen, L., & Vitters0, J. (2013). Personality and technology acceptance: The influence of personality factors on the core constructs of the technology acceptance model. Behaviour and Information Technology, 32(4), 323-334. https://doi.org/10.1080/0144929X.2011.553740 [ Links ]

Tam, C., & Oliveira, T. (2016). Understanding the impact of m-banking on individual performance: DeLone & McLean and TTF perspective. Computers in Human Behavior, 61, 233-244. https://doi.org/10.1016/j.chb.2016.03.016 [ Links ]

Tuten, T., & Bosnjak, M. (2001). Understanding differences in web usage: The role of need for cognition and the five factor model of personality. Social Behaviour and Personality, 29(4), 391-398. https://doi.org/10.2224/sbp.2001.29.4.391 [ Links ]

Urbach, N., & Ahlemann, F. (2010). Structural Equation Modeling in Information Systems Research Using Partial Least Squares. JITTA:Journal of Information Technology Theory and Application, 11(2), 5. [ Links ]

Vedadi, A., & Warkentin, M. (2016). Continuance intention on using mobile banking applications - A replication study of information systems continuance model. AIS Transactions on Replication Research, 2, 1-11. https://doi.org/10.17705/1atrr.00014 [ Links ]

Veeramootoo, N., Nunkoo, R., & Dwivedi, Y. K. (2018). What determines success of an e-government service? Validation of an integrative model of e-filing continuance usage. Government Information Quarterly, 35(2), 161-174. https://doi.org/10.1016/j.giq.2018.03.004 [ Links ]

Were, M., Odongo, M., & Israel, C. (2021). Gender disparities in financial inclusion in Tanzania. World Institute for Development Economic Research (UNU-WIDER).

Yang, H. C. (2013). Bon appétit for apps: Young American consumers' acceptance of mobile applications. Journal of Computer Information Systems, 53(3), 85-96. https://doi.org/10.1080/08874417.2013.11645635 [ Links ]

Zwass, V. (2003). Electronic commerce and organizational innovation: Aspects and opportunities. International Journal of Electronic Commerce, 7(3), 7-37. https://doi.org/10.1080/10864415.2003.11044273 [ Links ]

Appendix: Statements used in the survey questionnaire