Serviços Personalizados

Artigo

Inglês (pdf)

Inglês (pdf)

Artigo em XML

Artigo em XML Referências do artigo

Referências do artigo

Indicadores

Links relacionados

-

Citado por Google

Citado por Google -

Similares em Google

Similares em Google

Compartilhar

Permalink

PermalinkLaw, Democracy and Development

versão On-line ISSN 2077-4907

versão impressa ISSN 1028-1053

Law democr. Dev. vol.26 Cape Town 2022

http://dx.doi.org/10.17159/2077-4907/2021/ldd.v26.5

ARTICLES

Examining the interpretation of section 115(2)(a) of the Companies Act of 2008

Simphiwe S Bidie

Senior Lecturer, Nelson R Mandela School of Law, University of Fort Hare; https://orcid.org/0000-0002-5022-2715?Iang=en

ABSTRACT

For the purposes of protecting the rights and interests of sharehoIders, section 115(2)(a) of the Companies Act 71 of 2008 is imperative and essential. The section and its concomitant provisions are beginning to find their footing before South African courts. One of the occasions when the imperative nature of the section is seen is when directors take part in decision-making where companies intend to enter into share buy-back schemes of arrangement. In that respect, the clarity and precision of the section has so far received Iimited scrutiny. To compound matters, even before the roIe shareholders are expected to play has been thoroughIy scrutinised, the sections relating to shareholders' exercise of power are currently the subject of a proposed repeaI. FortunateIy, recent judgments have begun to provide insight into the interpretation of section 115(2)(a), and the same can be said with respect to simiIar sections from other jurisdictions. This contribution examines these Iatter sections. It chiefIy shows that the judgments consuIted regard shareholder protection, not as a straight-jacket; the protection has its pitfalls. Meritoriously, it shows how courts interpret section 115(2)(a) to protect shareholders from the pitfalls by promoting/advancing shareholder protection. The judgments also speak with one voice in their interpretation of provisions aimed at maintaining the necessary balance between the rights and interests of company stakeholders. Essentially, the judgments admirably show that the process of finding that balance is a delicate exercise.

Keywords: Majority and minority shareholders; shareholder protection; re-acquisition of shares; share buy-back; duties of directors; company law; distribution.

1 INTRODUCTION

The protection of a company's capital is historical and fundamental. Company capital occupies a key position within the operations of a company, so scrutiny of the role that shareholders play vis-à-vis company directors in the protection of that capital is essential.1 The importance of a company's capital has always been seen through the lens that it is meant for the satisfaction of creditors' claims. In Re Exchange Banking Co, the court said:

"The creditor has no debtor but that impalpable thing, the corporation, which has no property except the assets of the business. The creditor gives credit to that capital and he has therefore a right to say the corporation shall keep its capital and not return it to the shareholders."2

Since 2011, the Companies Act 71 of 2008 (2008 Act),3 has prohibited certain transactions from being carried out by directors except with the approval of shareholders. The transactions were mostly those which had an effect on shareholder's rights, or whose aims were to change a company's capital structure. From the recent judgments, four factors need highlighting. These provide insight into the important role of shareholders within companies, and they confirm several propositions about the role that section 115(2)(a) of the 2008 Act plays, namely: (i) the section's centrality in maintaining share capital where a company engages in distribution of its money or property; (ii) that the mechanism is used by the legislature as a policy to maintain the existence of companies as a mode of doing business;4 (iii) that, as a rule, section 115(2)(a) must be satisfied by companies; and (iv) that shareholders of a disposing company have an obligation, just as much as its subsidiary company/s have where it is the subsidiary that makes a disposal.5

The rule creating the obligation has recently been affirmed in Cooper NO v Myburg.6It is curious that initially for buy-backs, the Companies Bill, 2008, the Explanatory Guidelines to the 2008 Companies Act, and eventually the 2008 Act, did not require shareholder approval in their respective provisions, despite this mechanism's having been part of the Companies Act 61 of 1973 (1973 Act). For the 2008 Act to be repealed, it took several commentators to heavily criticise the initial lacklustre approach the Act adopted to shareholder protection. For example, some authors considered the Act's approach to be a diminution of shareholder rights.7 Wainer opined that, by failing to mention shareholder approval, the 2008 Act omitted one of the most important protections afforded to shareholders against unscrupulous actions by directors, as was the case under the 1973 Act.8 Cassim decried the approach of not recognising the fact that the initial protection of shareholders lay in the requirement that the acquisition of shares had to be authorised by special resolution. He reasoned that such an approach not only ensured prevention of abuse of the share repurchase power, but also prevented discrimination against shareholders holding the same class of shares.9

After the criticisms, the Act swiftly improved its protection prowess in favour of shareholders.10 Under Part A of chapter 5 of the 2008 Act, section 115(1) provides that a proposed scheme of arrangement (scheme) shall be approved in terms of section 115.11 As a result, this contribution is intended to interpret and unpack section 115(2)(a) of the Act. It intends to adopt a comparative approach with like provisions from Australia in order to gain insight into the strengths and weaknesses of section 115(2)(a). The analysis is undertaken in the context of formation of schemes of arrangement that, in the main, involve share buy-backs. To that extent, the first task is to highlight the regulatory framework and the rationale underlying section 115(2)(a) in Part 2. The second step, in Part 3, is a pertinent examination of the adoption of a buy-back special resolution under a scheme together with its ancillary provisions. Next, in Part 4, is a critical examination of the adoption of a buy-back special resolution in Australia. Finally, Part 5 provides comments, observations and the conclusion.

2 THE REGULATORY FRAMEWORK AND THE RATIONALE UNDERLYING SECTION 115(2)04) OF THE 2008 ACT

Section 115(2)(a) of the Act gives effect to section 115(1), and, as far as is relevant, provides that a proposed transaction contemplated in section 115(1) must be approved "by a special resolution adopted by persons entitled to exercise voting rights on such a matter ...".12 Generally, the provisions of section 115(2) of the 2008 Act provide the substantive part to approve all schemes listed under section 114(1) of the 2008 Act, and those which are not listed but that parties may agree to. In the author's view, a buy-back scheme of arrangement involves give and take.13 The element "give and take" in the context of a buy-back could be a misnomer, as the shares which the company receives for the capital it distributes to its members are not necessarily valuable upon reacquisition. Instead, a company depletes its capital.14 Because capital is an essential component of a company, it is this depletion that the law guards against15 through the shareholder-approval mechanism under section 115(2)(a) of the 2008 Act. The section is therefore in place as the last element to protect shareholder interests where a reduction of a company's capital is proposed through a buy-back scheme under section 114(1) and section 48 of the 2008 Act, by setting out how a proposed buy-back and its approval ought to be carried out.

The 2008 Act follows in the footsteps of several contemporary statutes regulating company affairs which empower company directors, when discharging their duties, to determine what change a company should make to its capital structure.16 Thus, section 115(2)(a), and other like sections in statutes from other jurisdictions, empower the shareholders to take part in decision-making alongside directors. The power embodied in a shareholder's vote to approve carries more weight where proposed changes are to a company's capital structure.17 Broadly, section 115(2)(a) is the sine qua non which provides the glue between the powers of the shareholder and the director with respect to how the management of the affairs of their companies ought to evolve.18 The relationship is abetted by policy imperatives. Hence, and as has been confirmed in Myburg, the obligation imposed by section 115(2)(a) on companies cannot be seen outside the parameters that approval of a buy-back is approval of the reduction of a company's share capital.19

Having observed the judgments that arose from challenges made against the conduct of companies and/or directors over the period of the operation of the 2008 Act, what is manifest is that the inclusion of section 115(2)(a), regulating the approval of proposed buy-backs, was not simply a window-dressing exercise.20 In Cilliers,21the court held that the purpose of the approval underpinning section 115(2)(a) is to ensure that the interests and views of all shareholders are considered before a company disposes of its assets, or where a company contemplates re-acquiring its own shares. In Reezen, the court acknowledged that, in requiring shareholder approval for various transactions, the objective of the legislation appears to be two-fold. On the one hand, it is to protect shareholders. On the other, it is to restrict directors' powers either to issue shares or to make a decision for a company to re-acquire its own shares without shareholder approval.22 The same sentiments were expressed in Moraitis.23In that case, the court held that the purpose of sections 112 and 115 of the 2008 Act was to ensure that the interests and views of all shareholders are taken into account before the company disposes of the whole or greater part of its assets or the undertaking itself.

3 EXAMINATION OF THE ADOPTION OF SPECIAL RESOLUTION

It is submitted that, in the main, section 115(2)(a) of the Companies Act 2008 presents two criteria that companies must satisfy before a proposed buy-back scheme can be lawfully adopted.24 In this part, the discussion is limited to part of the first criteria, namely, "a special resolution be adopted by persons entitled to exercise voting rights on that matter". Concentration on this isolated part is deliberate and is informed by the fact that, in the opinion of the author, if a company's approved proposal falls short of satisfying the latter requirement, a court may possibly declare that proposed scheme unlawful even before proceeding to the next stage and consider other requirements.25For ease of discussion the criterion is divided into two: (i) voting by persons who are entitled to exercise voting rights on the matter; and (ii) adoption of a special resolution, first, under sections 48(8)(a), and, secondly, under 115(2)(a).26

At this stage, it makes sense, to begin with a reference to various judgments which have set out principles interpreting documents or statutes, and explain the trite position with which provisions or documents have to be engaged. Paramount in this regard is the Constitutional Court judgment in PFE International v Industrial Department Corporation of South Africa Ltd.27In the case, the Constitutional Court recently affirmed the principle that rules of procedure are no longer to follow the orthodox approach to interpretation, to first read the text, and thereafter consider the context. The Court reasoned that from the onset courts must apply rules of procedure contextually and flexibly. In National African Federated Chamber of Commerce and Industry v Mkhize,28Majiedt JA held that it was trite that a constitution or document must be interpreted in accordance with ordinary rules of construction applied to contracts generally. Effect must be given to the plain language of that document, objectively ascertained within its context. Preference should be given to a sensible meaning over one that leads to nonsensical or unbusinesslike results, or undermines the apparent purpose of that document.29 In Butler v Van ZyI,30Van Zyl AJA followed this approach to the letter. The acting judge held that a court order should not be interpreted such that it literally has undesirable consequences. Particularly, the court said court orders should not be read to put a hold on shareholder voting in a general meeting, otherwise that would render a company moribund. Thus, it was not proper to adopt an interpretation of the court order in that case as interdicting a vote.31 With the above underlying principles in mind, it suffices to examine the two criteria identified above.

3.1 Dissecting persons entitled to exercise voting rights on a buy-back

Adoption of special resolutions and the exercise of voting rights32 are inseparable from each other when a company decides on a matter. Therefore, in the author's view, before engaging in the interpretation of the adoption of special resolutions by shareholders it makes sense first to dissect the persons on whom sections 48(8) and 115(2)(a) of the 2008 Act bestow the right to exercise voting rights. For an understanding of who is empowered to exercise voting rights as holders of a company's issued securities, the definition of "shareholders meeting" under section 1 of the 2008 Act is determinative. The section provides that, with respect to any particular matter concerning a company, a shareholders' meeting means: "a meeting of those holders of that company's issued securities who are entitled to exercise voting rights in relation to that matter".33 So the requirement that only those securities holders entitled to exercise voting rights are permitted to attend is consistent with this definition. The question which then arises is: What test does the 2008 Act envisage?

3.1.1 The test to attend shareholder meetings

In the writer's view, the manner in which a meeting of security holders must be organised and who must attend appears to be in line with the decision in Verimark, which previously set out the guiding principles on who may attend meetings to approve a proposed scheme.34 From the judgment, the first principle with which the court underpinned its decision referred to the foundational test for class members, which remains that of:

"whether the impact of the scheme on the legal rights of each particular group (as opposed to their commercial interests arising out of the scheme) is sufficiently similar to make it not impossible for them to consult together "with a view to their common interests."35

From the passage, what was determinative for courts was how they viewed shareholder class formations. For courts, class formations were informed by the impact of a scheme on the legal rights of each group. Thus, courts were influenced to ascertain how sufficient the similarity of each particular group and/or person's interests were to the other. Two stages on how the test operated are identified. The first stage had two phases: first, it looked at the proximity of the impact of the scheme on the rights or interests of the class which gave a sense of to which class a person belonged; secondly, it looked at the sufficiency in similarity or otherwise that would then direct whether or not it was impossible for two groups and/or persons within that group to consult together "with a view to their common interests". The latter phrase is significant because, obviously, where either group or those person's interests were impacted on by a scheme dissimilarly "no common interests" would arise.36Verimark and other similar judgments seem to agree that the test used to determine class members applied once there was certainty as to their identity. In other words, the test functioned to ascertain whether the persons within a class should in fact be part of that class.

3.1.2 The nature of the test regarding the future: Does it promote certainty?

The second stage is that the test is formulated to give direction as to who may form part of a particular class or group of persons at the time a matter is proposed. The words "with a view to their common interests" speak to the formulation of a class at the present, while anticipating future implications. One of the implications is that a person is part of a class or group with common interests on which persons in that class or group may consult or negotiate. Otherwise, if the persons in that class or group have no common interests, the question would be: On what basis could they possibly consult?37

Read in context, the words "with a view" reveal the element of the future. This element has an effect on, and is connected to, the first stage, as it requires that it is certain that, from the outset, persons who are part of a class be only those who would at a later stage be entitled to consult on the buy-back and eventually exercise voting rights. By implication, the manner in which the phrase "with a view" appears in the test recognises the next stage in the ladder of events that shall ensue: (i) that shareholder interests had already converged before the directors of that company determined the proposed buy-back of shares from that class; and (ii) that groups or class members are expected to still negotiate or consult between themselves before exercising their voting rights. The phrase "with a view" is not contrary to and/or distant from an interpretation suggesting "in the hope of or aiming towards". The phrase recognises that at times it might be unclear whether or not holders of that company's securities agree on the proposed buy-back. So, at the time of the meeting, some negotiation or consultation might still be necessary to determine whether or not to approve a proposal. The test recognises the different steps that are foundational to the ultimate approval of a buy-back by that company's security holders, by having regard to the different stages which occur before the exercise of voting rights. Therefore, the test does promote certainty.

3.1.3 The test contemplated under the 2008 Act

The question which arises is: Does the 2008 Act contemplate the use of the same test? This question should be answered in the affirmative because, from the definition of "shareholder meeting" put forward earlier, the Act appears to do so. To this day, the principles Verimark set out remain the example and, analogously, provide a practical demonstration of what sections 48(8) and 115(2)(a) of the 2008 Act contemplate in the context of who should be invited to take part in the subject matter of a meeting to re-acquire own shares by a company. This is despite the fact that Verimark was decided under a different statutory regime. However, Verimark can only serve as a point of departure and/or point of reference, subject to any changes the 2008 Act aims to make to improve on the previous position, if any. In terms of section 48(2)(a), the 2008 Act contemplates that at the time when company directors determine that the company must buy-back its own shares, and at the same time recommend from which class that repurchase be made, the shareholders would have already been categorised. From that point, there could hardly be doubt in which class each shareholder belongs.38 This requirement, and the permission given by the Act in sections 36 and 37 for formation of classes by companies, appears aimed at the reduction or elimination of like contestations.

In Verimark, the respondents opposed the sanctioning of the scheme on two grounds: that Verimark, as directed by the Van Straaten Family Trust (VSFT) as the majority shareholder, and the "excluded members" were not "scheme participants" and should not have been permitted to vote; and VSFT and the "excluded members" were a class of ordinary shareholders different from the remaining 37% of the shareholders and should not have been permitted to vote.39 Conversely, and as is relevant in the context of section 115(2)(a) of the 2008 Act, it can be argued that effectively what the challenge was based on was the fact that VSFT and the "excluded members" should not have been invited to the meeting, since the manner in which the proposed scheme was designed was for the parties not to have voting rights on the matter - and not necessarily that the excluded parties had no voting rights per se. Besides, in the definition of "scheme participants" in the offer to the invitees, these parties were not included at all.40 In response, the court first acknowledged and made it clear that a "proposer", the "excluded members" and "minorities" may all be ordinary shareholders, thereby causing their rights or the bundle or conglomerate of personal rights to entitle the holder thereof to a certain interest in the company, being the company's assets and its dividends; by virtue of this entitlement, the parties may be identical and all may belong to the same class of shareholders.

On whether VSFT and "excluded members" should have been allowed in the meeting and to vote, the court held that the enquiry as to whether separate meetings should have been held arose only after the determination of the identity of the offeree, the relevant question being, "Between whom is it proposed that a compromise or arrangement is to be made?".41 In the author's view, the latter question has been the hallmark of the formation of class meetings over time, and wiII continue to do so. It clarifies the classification of shareholders entitled to vote where a buy-back scheme between them and their company is proposed. In simple terms, the question asks, "Who is invited in terms of the proposal?", suggesting that persons with interests in the matter have already been identified or established. What remains at this stage is further talks on the proposed buy-back. In the author's view, and based on what has been suggested in the discussion of the test above, the question tells us something else, namely, that even within a class of ordinary shareholders it is possible that an offer might not have been made to all, but rather to a certain category of shares held by holders whose shares occupy a certain status within the classes of shares of that company.

In response to the question of who is invited, the court in Verimark referred to three relevant possible scenarios that might arise and for which clarification might be needed.42 With respect to the first scenario, what the court appears to have had in mind is a situation where a company makes an offer to buy-back from all shareholders. In the context of the 2008 Act, this would mean repurchase from both persons under section 48(8)(a) and those under section 48(2)(a) who are expected to approve the proposed buy-back based on section 115(2)(a). (The two sections are discussed below.) In the second, it would be where the company proposes to buy-back from shareholders who hold shares under a special scheme for a certain period based on an agreement between them and the company, for example an employee scheme. The third category is where an offer is made to what appears to be a single class of shareholders, but on closer scrutiny it is realised that the shareholders should have been classified differently because they hold dissimilar and distinct interests. The first and the last scenarios appear to be what could be determined under section 48(2)(a) and be voted for as directed under section 48(8)(a) and (b), thus also invoking section 115(2)(a), as the case may be. The second scenario may fall to be voted for by all shareholders with voting rights on the matter in terms of section 48(8)(a) since it appears to be directed at an employee scheme, these being directors, prescribed officers or their related persons or another class of employees. What the three scenarios prove, as the court said in Verimark, is that the correct answer would depend on the circumstances peculiar to that case. Amongst the three, one considers the first and the third instances as are the more relevant and the ones that could arise in the context of the proposed buy-back schemes discussed in this article.

If the approach suggested in Verimark finds support from courts under the current regime, analogously it suggests that sufficiency of similarity of interests will on the one hand, rest on the determination made by directors under section 48(2)(a) in regard to the question of with whom they determined the company should propose to enter into a buy-back scheme. The question will be whether the proposal is made to directors, prescribed officers and their related persons regulated under section 48(8)(a), or also with shareholders generally whose approval shall only be adopted under section 115(2)(a), or only to one of the class of shareholders falling within the respective sections. It will also depend, on the other hand, on whether or not the directors intend to create a scheme. Once the category of persons to whom a proposal shall be made is identified, the formation of a scheme will then depend on how the persons have negotiated to vote and/or have voted, and in the latter instance, whether based on individual interests or those of the group/class generally.

In sum, from the discussion above, the holding of meetings depends on four issues: (i) classes, where these are created; (ii) common interests of shareholders; (iii) whether or not holder's interests are sufficiently similar; and (iv) voting rights. It was upon the four that in Verimark the court classified the offer in question made in the case to have been made only to minority shareholders who were "scheme participants" as defined. The proposal was not made to the "proposer", nor was it made to the "excluded members".43 As a result, the court held that only the "scheme participants" were entitled to accept or reject the offer; only they should have been permitted to vote on the matter.

The court held as it did despite the fact that holders of shares were all ordinary shareholders. In the latter respect, it reasoned that the same ordinary shareholders may be from a single class, but the same class may be divided into different classes based on what the proposer intended. Thus, the two approaches by which an offer may be made from the category of persons specified in the Act, and for that offer to gain an approval either as contemplated under section 48(8)(a) or contemplated from shareholders determined in terms of section 48(2)(a), is not far-fetched from the Verimark judgment. The latter decision shows that simply because the persons from whom shares are proposed to be bought back are all ordinary shareholders, that in itself is not determinant that all shareholders shall belong to the same class in terms of the purpose of the proposed scheme. Within the one class there might still be further categorisation or classification of members. What will be paramount is how the participants are defined, for example by a published circular making the offer.

Therefore, the court in Verimark agreed with the respondents to the effect that VSFT and the "excluded members" should not have been permitted to vote on the matter, as these parties were not part of the class of holders envisioned under the proposed scheme of arrangement; thus, the court refused to sanction the scheme.44

3.2 Dissecting the adoption of special resolution

It is apt to note that to approve a transaction, courts favour that a company follow the procedure set out in that specific legislation.45 Approval of fundamental transactions either to dispose of or to acquire shares are governed by the same procedural rules under section 115(1) of the 2008 Act.46 For shareholders to approve or adopt a board decision, first section 65(11) of the 2008 Act prescribes transactions which are subject to special resolution.47 Under that part, section 65(11)(g) with (l) is particularly relevant when companies re-acquire own shares in circumstances contemplated under section 48(8) and any fundamental transaction. Moreover, section 115 is sequentially interrelated with other sections of the Act cascading from each other, these being sections 48, 65, 112, 113 and 114, which also bear relevance to the regulation of the disposal by a company of its assets,48 or where the company re-acquires its own shares, as the case may be. This part interprets the adoption of a special resolution by shareholders of a company under sections 48(8) and 115(2).

3.2.1 Adoption of a special resolution under section 48(8)(a)

The operation of the sections on buy-backs was recently dealt with in First National Nominees (Pty) Ltd v Capital Appreciation Ltd.49In that case, Windell J's interpretation of section 48 arrangements implicitly confirmed that the adoption of proposed schemes through buy-back of own shares may be directly activated by a company by following the procedure in section 114(1) and (4). Section 114(1) provides as follows:

"Unless it is in liquidation or in the course of business rescue proceedings in terms of Chapter 6, the board of a company may propose and, subject to subsection (4) and approval in terms of this Part, implement any arrangement between the company and holders of any class of its securities by way of, among other things ... a re-acquisition by the company of its securities."50

As the preceding paragraph illustrates, a board of a company is empowered to propose and implement any arrangement. Because a proposed scheme in terms of section 114(1)(e) results in an acquisition,51 section 114(4) activates the formal procedure provided for under section 48 for companies to follow to approve a proposed share buy-back scheme.52 So, to have a proposed scheme approved, the route must pass through section 114(4) of the 2008 Act, which supplements section 114(1) by being the bridge through which section 48 is activated. Section 114(4) provides that:

"[s]ection 48 applies to a proposed arrangement contemplated in this section to the extent that the arrangement would result in any re-acquisition by a company of any of its previously issued securities."53

Once section 48 of the 2008 Act is activated, section 48(2)(a) of the same Act empowers a company's board of directors to determine a buy-back that a company proposes to make. Section 48(2)(a) of the 2008 Act does not at first sight specify from whom the board must determine to buy-back shares. Nevertheless, the latter section goes on to subject a board's determination to section 48(8) of the same Act. Consequently, in section 48(8)(a) the Act specifies persons from whom shares may be acquired by a company for which shareholder approval is required. These are directors, prescribed officers or their related persons.54 There is no provision in section 48(8) which makes mention of buy-backs from shareholders themselves.

This is surprising because not all shareholders become company directors, prescribed officers or become related to the two. Perhaps, section 48(2)(a) is designed to play the determinative role when a company repurchases shares from its shareholders, since section 48(8) of the Act is silent. This is so because the opening words of section 48(2)(a) are open-ended, namely: "a board of a company may determine that the company will acquire a number of its own shares ...".55 The latter wording is not directed at any particular person; implicitly, the wording refers generally to all shares of that company held by a person irrespective of the holder. The silent posture the Act has adopted under section 48(8) to refer specifically to shareholders is puzzling, especially when compared to section 114(1). The latter section authorises implementation of any arrangement between the "company and hoIders of any cIass of its securities". Obviously, the section refers to holders who might not necessarily be directors, prescribed officers or their related persons as articulated or stipulated under section 48(8)(a).

In Capprec, the court's judgment partially agreed with the approval proposition expected to unfold to pass a special resolution under section 48(8)(a) of the 2008 Act, and that approval is consistent with the inference that one draws from the preceding different wording. The court did not expressly acknowledge, but indeed, it seemed to agree that companies may at times aim to buy-back shares only from persons mentioned in section 48(8)(a), or alternatively from those expressly determined by directors under section 48(2)(a) or section 114(1), but whose rights shall eventually be subjected only to the section 48(8)(b) and section 115(2)(a) procedures.56

The question which arises is whether the Act aims to have all shareholders of a company approve a buy-back under section 48(8)(a). Section 48(8)(a) appears to respond adequately to the question.57 The relevant words from the latter section responding to the question are that approval must be by "special resolution of shareholders of the company".

The section does not mention approval by "shareholders of a class". The inference therefore is that all shareholders with voting rights are expected to cast a special resolution. The summary reflected in Figure 1 below is meant to illustrate repurchase of shares under section 48(8)(a) as already discussed above and were a determination has already been made by the board of directors under section 48(2)(a).

Figure 1 informs parties about two processes before a meeting is called by Company Z: (a) that shares are repurchased only from directors, prescribed officers or their related persons; and (b) that it is expected that all shareholders of that company with voting rights are present in a meeting to exercise those voting rights on the proposed transaction. Consequently, the section 48(8)(a) procedure does not lead to the activation of section 115(2)(a); the section provides for its own collective shareholder approval mechanism.58 Therefore, accepting that the above approach shall remain as the court determined in Capprec, and the latter case's decision is ultimately affirmed by higher courts to be correct; and assuming as well that the scheme to buy-back own shares is proposed only to shareholders who, within the meaning of section 48(8)(a) are not directors, prescribed officers or their related persons, it then appears safe to submit that the procedure under section 48(8)(a) cannot apply to approve a scheme. The above procedure makes it clear that when a company intends to create a scheme, and a transaction is proposed through section 114(1) of the 2008 Act, only the section 48(8)(b) procedure shall be activated.59

The challenge for the Act is that the proposition that only section 48(8)(b) shall be activated does not show clearly from the provisions. The conjunction "and" linking both the section 48(8)(a) and (b) paragraphs exacerbates the uncertainty. The word "and" appears to suggest that the Act contemplates that the two paragraphs under section 48(8) must always be read conjunctively, rather than be read disjunctively, at the relevant moment. At a glance, it appears that the drafters of section 48(8) should not have inserted "and" to link the two paragraphs; perhaps "or" would have been preferable. Disjunctively, the paragraphs would have read much more clearly, assuming that "and" was not inserted, that is, that either paragraph applies in a particular circumstance of a proposed buy-back application. One can but wonder whether there is a reason why "and" was used by the legislature. There seems to be a possible reason as explained later hereunder. Assuming that the possible reason to be explored below is not what could plausibly have been contemplated by the legislature. In that case, a solution to resolve a similar challenge between "and" and "or" was proposed in Panamo Properties (Pty) Ltd and Another v Nel N.O. and Others.60The contention in the case related to the drafting of the provisions of section 130(5)(a)(i) and (ii) of the 2008 Act. Sub-paragraphs (i) and (ii) are divided by the disjunctive "or". The aim of the court was to find common ground between the provisions so that there would be no inconsistency when shareholders held meetings. The court ruled that it was appropriate to read "or" conjunctively as if it were "and". The result would be a reconciliation between sections 130(1)(a) and 130(5)( a) so as to limit the grounds on which an application to set aside a resolution could be brought.61 Surely, in the context of section 48(8)(a) and (b), "and" could just as well be read as "or" where appropriate. What must be emphasised for now however, is that, from the aforesaid, it does not matter whether the proposed buy-back would simply be an arrangement under section 48(8)(a) or (b), or a scheme facilitated under section 114(1) - shareholders must nonetheless approve a proposed share buy-back.

3.2.2 Adoption of special resolution under s 115(2)(a)

Having disposed of the section 48(8)(a) route, what follows is an examination of the procedure a company must follow in order for shareholders of that company to have validly approved a proposed buy-back scheme under section 115(2)(a) of the 2008 Act. From the onset, what companies must note is that the adoption of a special resolution in a proposed buy-back scheme does not, after a proposal under section 114(1)(e), automatically proceed directly to approval under section 115(2)(a). First, the provisions of section 48 must be observed. To that extent, section 114(4) activates section 48 where the aim is to create a buy-back scheme under section 114(1)(e). Once section 48 is activated, first in line is that a board of a company has another hurdle or procedural step to navigate. Pursuant to the proposal agreed to by the board in terms of section 114(1), the board has to determine and adopt a resolution as section 48(2)(a) directs. Before this time, no board resolution need be adopted or is required. The wording under section 114(1) is that a board "proposes", whilst under section 48(2)(a) a board "determines". For example, under section 48(2)(a) the wording is "the board of a company may determine", whilst under section 114(1) the wording provides that "the board of a company may propose". In the author's view, it is clear that the Act aims to convey different legal meanings between "determine" and "propose", as the two words have a vast difference in legal meaning. In the context in which the two phrases are used, "determine" connotes "decide, find out, discover, estabIish, ascertain, or approve", while "propose" connotes "suggest, submit, recommend, or initiate". The difference in wording under both the latter sections seems to accord credence to the preceding thinking. Contextually compared together, the determination a board is empowered to make under section 48(2)(a) seems to carry more legal weight than the proposal envisaged under section 114(1).

One wonders whether the difference in wording between sections 114(1) and 48(2)(a) is justified, considering that the sections are meant to kick-start different processes but have the same aim ultimately. The difference appears to be unnecessary and tedious. In the author's view, it would have been preferable if a similar wording to that in section 48(2)(a) had been inserted where a board intended to propose a buy-back in terms of section 114(1)(e). Had that been the approach, the Act would simply direct the board to observe sections 46, 48(3) and (8) in the same manner that section 48 mandates. As the sections currently stand, there is no justification that a share buy-back must first be "proposed", and later a "determination" be made, and a board resolution be adopted under section 48(2)(a), where a similar process could equally be initiated under section 114. It appears that had the sections been similarly worded, the determination which would have been made in terms of section 114(1) would have been equally adequate, and thus do away with the two-pronged "proposal" and "determination" processes. Alternatively, the "proposal" and "determination" could be added as a requirement under section 114(1).

In the author's view, the approval process would be less tedious than it is if the legislation incorporated similar wording under section 114(1), as it does in section 48(2)(a), given that both sections are in any case directed at the same aim, which is to ensure that shareholder rights or interests are adequately safeguarded. It is submitted that, as the sections currently stand, their approach to the approval of a proposed buy-back is cumbersome and unnecessary.

Once the above process has been observed, section 48(8)(b) is activated, which by its nature results in the requirement for approval by special resolution of the particular proposed arrangement under section 115(2)(a) of the 2008 Act. The section begins by providing that the decision of the board of a company contemplated in section 48(2)(a) be subject to the requirements of:

"sections 114 and 115 if, considered alone, or together with other transactions in an integrated series of transactions, it involves the acquisition by the company of more than 5% of the issued shares of any particular class of the company's shares."

It must be stated upfront that the Companies Amendment Bill, 2021 (Bill, 2021) proposes to completely repeal the latter section, with no alternative replacement provided.62 Currently, the section still applies. Accordingly, in order for a proposed share buy-back scheme to activate section 115(2)(a), the transaction must be at more than the 5% threshold, otherwise, if it is below, the latter section is not activated. In the context of this part, the aim must be to buy-back shares from shareholders with the intent to create a scheme, as the heading to section 114(1) specifies. Under the discussion on section 48(8)(a), it was highlighted that the 2008 Act contemplates approval from all shareholders only if the buy-back is made by the company from directors, prescribed officers or their related persons. Where a buy-back is to be approved by shareholders in terms of section 115(2)(a), the position is different. However, one must be mindful that it is likely that the latter persons may form part of the broad term "shareholders" and hold shares within the class or group of shareholders from whom a buy-back is proposed. The question is whether a share buy-back proposal that is not aimed at resulting in a scheme and is more than 5% can or must as well be approved through section 115(2)(a). The answer is not clear from the Act. The question arises because under section 48(8)(a) shareholder approval is contemplated only if a repurchase is from directors, prescribed officers or their related persons (for example, these persons may hold preference shares), and no approval is contemplated under this section if the repurchase is proposed to shareholders who are not directors, prescribed officers or their related persons.63 For the latter reason, the literal reading of the wording of the Act suggests in one's mind that the approval of a buy-back from persons listed under section 48(8)(a) should at all times be distinguished from approval contemplated under section 48(8)(b).

Only under section 114(1) does the Act expressly refer to the term "class" within the shareholder's voting process. Consistent with the observations made earlier, this obviously signals that the Act contemplates that voting by shareholders for proposed buy-back schemes orchestrated under sections 114 and 115(2)(a) shall be by class as opposed to being by all shareholders generally. Thus, the appearance is that the approval procedure under sections 48(8)(b) and 115(2)(a), unlike the approval process contemplated under section 48(8)(a), does not contemplate approval of a proposed share buy-back scheme by special resolution by all shareholders combined. It is the author's opinion that the wording of the sections does not suggest or support that approval be sought from all shareholders in order for a company to comply with the shareholder approval procedure envisioned under sections 48(8)(b) and 115(2)(a). Perhaps one may pause here to emphasise the point made above, that it is comforting that the section 48(8)(b) route is currently proposed to be repealed by the Bill, 2021. Clearly, the aim is to reduce uncertainties about how the shareholder approval procedure applies. However, under the proposed repeal, the sections 115(2)(a), 114(1) and (4) procedures as well as the section 48(8)(a) procedure remain intact.64 Thus, even after the repeal the procedures in the latter sections will remain the same.

Earlier, a conjecture was made as to whether the inclusion by the legislature of the word "and" linking paragraphs (a) and (b) under section 48(8) was deliberate. The word causes confusion because when read in context it seems to direct courts to undertake a conjunctive interpretative posture when analysing the effect of the paragraphs, rather than a disjunctive one. The word suggests, contrary to the submission made earlier, that before any repurchase of shares by a company, shareholders with voting rights combined must first approve any type of a proposed share buy-back whether or not it will result in a scheme, and thereafter class members must also approve. Indeed, when one looks at the current proposed repeal of the 2008 Act, by the Bill, 2021, the Bill suggests this alternative observation. Earlier, it was submitted that section 48(8)(a) as it currently stands envisages that all shareholders of a company entitled to exercise voting rights shall vote. Therefore, it makes sense to conclude that the contemplated change by the Bill, 2021, to discard the section 48(8)(b) procedure, and remain only with the procedure under section 48(8)(a), suggests that a proposed share buy-back, determined by directors, must be approved by all shareholders combined. This change would then mean that for an approval of a proposed buy-back scheme, section 48(8)(a) will have to be complied with as well, in addition to sections 114(1)(e) and 115(2)(a) of the 2008 Act. After the repeal, section 48 will not have a provision cross-referring to sections 114 and 115.

Further, once the repeal is through, the class factor will still remain informed by section 36(2)(a) of the 2008 Act, which refers generally to approval by shareholders. But the latter section does not refer to approval by class of shareholders. It simply permits authorisation by a company of shares by class.65 The wording in section 114(1) buttresses the absence of voting by class, as it is to the effect that the board shall "propose and . implement any arrangement between the company and holders of any class of its securities .". Again, the wording does not suggest that shareholders must exercise their voting rights by class. It is not clear why the 2008 Act has not found it appropriate to expressly authorise that shareholder approval of a matter be by class, seeing that it does permit companies to cause their shares to be allocated according to class, and in addition be allocated preferences and rights, as the case may be.66

Under the 1973 Act, the position was much clearer than under the current one. Section 311 of the latter Act expressly provided for the court to order that there be summoned separate meetings of each of the distinct classes of creditors. It appears that the common law approach to formation of classes for purposes of voting shall apply to distribution of company money or property, as was determined in Verimark and LogikaI. In MarbIe, the company only had one class of shareholders who voted.67However, there were shareholders who were excluded from the offer to acquire shares from shareholders.

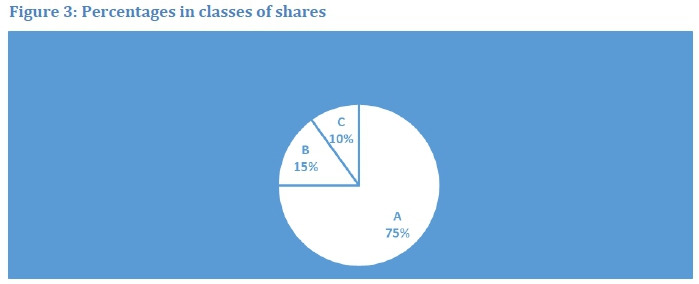

The case is a confirmation that at a particular time an offer to buy-back company shares may not be made to all shareholders of a company even if the company has one class of shares. It will depend in the circumstances of that offer or proposal.68 The summary provided in Figure 2 below exhibits the reacquisition option the 2008 Act provides for under section 115(2)(a). Company Z's shares are divided into three classes, namely A, B and C.

Figure 2 illustrates the classes of shareholders of Company Z who must adopt a special resolution contemplated under section 115(2)(a). Put briefly, the illustration clarifies, for the benefit of all parties forming part of a proposed scheme before a meeting is called, that it is only the shareholders constituting that particular class and whose rights shall be affected who must be present at the meeting and will be entitled to exercise voting rights.69 The position will remain the same until the changes proposed by the Bill, 2021 are in effect. One must not lose sight of other ancillary challenges which at times may arise as to who is entitled to vote and pose a conundrum for companies that contemplate engaging in a buy-back scheme.

One such was addressed in Cilliers. In that case the court had to address the question of whether a shareholder in the holding company had a right to exercise his voting rights where it was the holding company's subsidiary which was the disposer of its own assets. The shareholder held no shares in the subsidiary company. From the case, a different picture appears if the decision is considered in the context of a buy-back of shares by a subsidiary company. The court held that the shareholders of the holding company will as well have to adopt a resolution approving the repurchase. It cannot exclusively be shareholders of the subsidiary disposing company who vote, otherwise section 115 would be rendered meaningless. However, only shareholders who have a right to vote on the matter shall vote.70 That will be so even if a shareholder does not hold securities in the subsidiary company, but only in the holding company; nevertheless, section 115 will have to be complied with. A shareholder would not need to specifically hold shares in the subsidiary company in order to exercise voting rights, where the argument is that the disposal or matter only relates to the subsidiary's shares.71

4 EXAMINATION OF THE ADOPTION OF SPECIAL RESOLUTION OF BUY-BACK SCHEMES IN AUSTRALIA

4.1 Adoption of resolution under section 411 and 257D of the Corporations Act of 2001

The roadmap to adopt proposed buy-back schemes differs between the 2008 Act and the Australia Corporations Act of 2001. Although, under both statutes, separate provisions regulate schemes and buybacks, under the 2008 Act companies are required to adopt a streamlined procedure. Under the Corporations Act, companies have to follow two parallel procedures. As the discussion under this part shows, the two contrasting procedures suggest dissimilarities with respect to what the statutes expect with regard to shareholder approval of proposed buy-back schemes. In Australia, arrangements are regulated under Part 5.1 of the Corporations Act 2001 alongside Regulation 5.1 and Schedule 8, and Part 3 of the Corporations Regulations which prescribe the procedural rules for schemes.72 The procedure followed in Australia to vary class rights is similar to the UK Companies Act.73Village Roadshow shows that how shareholder rights must be construed shall be determined based on what a company has scribed in its constitution.74 The Corporations Act 2001 defines an arrangement under section 9 to include a reorganisation of the share capital of a body corporate by the consolidation of shares of different classes.75 These shares are divided into different classes or by both methods.76 The challenge for companies and shareholders alike tends to be the translation of what is in a company's constitution into the document proposing the share buy-back scheme, and whether the meaning of what is scribed conforms to what the provision of the Act contemplates when the matter a statute regulates is interpreted or construed. Obviously, this would arise because in the main such proposed arrangements are normally concerned with the affecting of the rights and interests of members and obligations of companies.

Approval of proposed schemes of arrangement is regulated by section 411 of the Corporations Act 2001. For companies to comply with the Corporations Act where class rights are varied, they must not only comply with the solvency and liquidity test - for example where buy-backs must not materially prejudice the company's ability to pay its creditors77 - but must also comply with the procedure by which that buy-back must be conducted.78 From Village Roadshow, the latter means that whether or not a company proposes a scheme, companies must in addition comply with the procedure provided under one of the five share buy-back methods permitted by the Corporations Act. Accordingly, when a company proposes a scheme, section 411(4)(a)(ii)(A) and (B) of the Corporations Act specifically sets out the member's voting procedure a company is expected to satisfy to obtain shareholder or member approval.79 Compared to section 115(2)(a) of the 2008 Act, the approval contemplated is similar for companies with share capital, and is by a special resolution passed at a meeting of the class of members holding shares in the class, or of the class of members whose rights shall be varied. Before voting, shareholders must be apprised of their rights through the explanatory statement companies are obliged to prepare (scheme booklet).80 Similar to section 114(2) and (3) of the 2008 Act, the scheme booklet must set out all the material information regarding the proposed scheme and its effect on shareholder's rights. It must also reflect on the independent expert's report stating whether or not the proposed scheme shall be in the best interests of shareholders.81 The latter requirement, similarly to the 2008 Act, does not refer to the interests of the company but to those of shareholders. A further similarity is that, under the 2008 Act, the Panel must issue a certificate before a proposed share buy-back scheme is approved.82

The same is contemplated under the Corporations Act, where a proposed scheme must have been assessed by ASIC before being approved by a court.83 The scheme booklet must be assessed by ASIC to ascertain whether or not its terms reflect fairness and comply with the Corporations Act before the scheme is referred to court for the first time, so that the court can grant the company an order to convene the first meeting with shareholders for a vote on the proposed scheme. Consequently, ASIC is empowered by the Corporations Act to raise any terms in the proposed scheme that it might consider to be unreasonable or unfair to shareholders or the company before the issue of a certificate. Where all the substantive steps are adhered to, the court shall consider, and where according to its discretion it sees fit, grant the order.84 It is at this stage that a company sends out the booklet to shareholders for purposes of consultation, based on the test that each have sufficient similar interests. Separate meetings are required to be held for different classes of shareholders (for example, ordinary, preference or option shareholders).85 Contrary to the silent position adopted by the 2008 Act when arranging meetings for shareholders to approve a proposed scheme by special resolution, the Corporations Act specifically and expressly directs companies that such meetings should be held by different classes of holders.86 As was argued earlier, there is no such provision under the 2008 Act. However, the route to section 115(2)(a) begins in section 114(1), which contemplates a scheme to be proposed to a class of shareholders. By implication therefore, only this class shall vote to approve that proposed scheme.

Notwithstanding that companies make offers to shareholders to buy-back their own shares, McConvill submits that in Australia companies are required to enter into an agreement with their shareholders in order to buy-back shares.87 As a result, it is essential that "any shareholder to whom the company makes an offer to buy-back may decide whether or not to sell".88 This suggests that even where companies propose a buy-back through a scheme, all shareholders to be affected have a right to approve. On the day of voting, it is only the relevant shareholders with the right to vote who must be present and vote. Share buy-backs are currently regulated under sections 257A-257J of the Corporations Act of 2001.89 On considering approving a proposed buy-back scheme under section 411 of the Corporations Act 2001, the relevant procedures under section 257J (providing for signposts of other applicable/related sections to buy-backs) or sections 256 and 257D, are not cross-referred similarly to the 2008 Act under section 114(4). When a scheme is contemplated, section 411 of the Corporations Act does not, for example, cross-refer to the section 257D procedure. Notwithstanding the omission, Village Roadshow shows that, where companies in Australia have proposed a scheme of arrangement where a share buy-back will be the subject of the transaction, then one of the five buy-back modes has to be utilised or activated and the relevant requirements for that buy-back must be met.90 Thus, in proposed share buy-back schemes, section 257D, which regulates selective buy-backs,91 should be satisfied alongside section 411, which scribes its own procedure as demonstrated above and which companies are expected to satisfy when proposed schemes are to be approved. Under the 2008 Act, the obligation to utilise the section 48 procedure to adopt a proposed share buy-back scheme is made pertinently clear through section 114(4) of same Act. Disappointingly, under the Corporations Act this is not as clear-cut. The approval route under both sections 257D and 48(8)(a) contemplates that the first resolution be passed by "all shareholders of that company" in a general meeting of the company.92 The position under section 411(4)(a)(ii) of the Corporations Act and section 115(2)(a) of the 2008 Act is different.

Ultimately, in Australia courts play a pivotal role,93 as is the case in Canada94 and the United Kingdom (UK), in approving the setting up of the first meeting by a company, and in eventually approving a proposed scheme.95 Under the 2008 Act, the latter procedure has since been discarded; instead, a court's role comes subsequent to application by a party.96 The test used is multi-fold: (i) the common law test established in cases similar to Verimark; and (ii) voting based on a two-fold test approach: a majority in number (numerosity test); and that 75% or more votes in value be cast by shareholders to support a resolution.97 Notably, approval by shareholders under section 411 is similar in contemplation to section 115(2)(a) of the 2008 Act only so far as the 75% threshold requirement.98 Otherwise, it is different with respect to the lower threshold (head-count of majority in number), since the 2008 Act does not require a head-count in number, but requires shareholders to be "sufficiently present to exercise 25 percent of voting rights". The rationale behind the numerosity test is that it provides for checks and balances and protects those in the minority, especially where a small group of large shareholders could pass a resolution that is against the interests of a large number of small opposing shareholders. A court is therefore unable to approve a scheme at the sanctioning stage if the numerosity test is not met even if the 75% majority in value is achieved.99 Once a scheme is approved by the requisite percentages of shareholders it is referred back to court for final approval.100 At this last approval stage, the court assesses whether the scheme is fair and reasonable, using the honest and intelligent business person test.101 Where the 50/75 test has clearly been achieved, it is rear that Australian courts do not approve a proposed scheme.102 However, they normally make it essential that it be shown that there is a commercial reason for a scheme.103

4.2 Village Roadshow Limited v Boswell Film GmbH104

In the Australian Supreme Court of Appeal in ViIIage Roadshow Limited, Callaway JA of Victoria's Supreme Court of Appeal had to rule on an appeal on the operation of section 257D of the Corporations Act.105 Callaway JA narrowed the issues the court had to decide to two questions. The first was whether section 257D prevented a person whose shares were proposed to be bought back pursuant to a selective buy-back from voting against a special resolution of the kind referred to in section 257D(1)(a). The second was, if section 257D had the effect of preventing a person to vote, the court had to establish whether preference shareholders were entitled to vote against the special resolution that was proposed pursuant to section 257D at the general meeting held on November 2003.106

4.2.1 Appellants and respondent's contentions

In the appeal, the appellants contended for an affirmative answer to the first issue, and a negative to the second. Their contention revolved around the argument that provisions regulating reduction of share capital, and those regulating buybacks, should be read as requiring separate treatment, and as such, the two provisions gave the impression that such provisions may be interpreted as requiring separate action. Hence, the company drafted article 2.4(a)(i) of the company's constitution in the manner it did. On the other hand, the respondents, who were holders of both ordinary and preference shares and successfully opposed the scheme in the court a quo, contended for a negative answer to the first question and an affirmative to the second because their view was that they were not prevented from "voting against" the proposed scheme.107

4.2.2 Court's analysis of the company's constitution, the notice and the booklet

The court, as it had to, began its interpretation by reference to section 257D(1) of the Corporations Act as well as article 2.4(a)(i) of the company's constitution (which specified what rights preference shareholders held with respect to voting).108 The judge set out what the constitution's articles provided for on capital reduction, what article 2.4 provided for on the entitlement of shareholders to adopt special resolutions, as well as the booklet and the notice of the general and scheme meetings.109 Callaway JA's deduction was that the company drafted the scheme booklet and the notice of general meeting based on the belief that none of the exceptions in article 2.4(a)(i) applied.110Both the booklet and the notice were drafted on the belief that, by reason of section 257D, members of the company who held ordinary and preference shares (combined shareholders) were not entitled to vote on the resolution required by the section, even on the bases of their ordinary shares. The booklet and the notice expressly stated this fact.111 Accordingly, the manner in which the articles and the booklet were drafted gave the impression that preference shareholders were not entitled to vote at all at the general meeting. The notice was also silent on whether or not the said holders were entitled to attend.112 ASIC's view on the interpretation of section 257D was that the combined shareholders were not prevented from "voting against the scheme", but agreed that they could not "vote in favour".113 After engaging with ASIC on the wording of the notice and booklet, and before voting took place, the company issued another notice to the effect that the combined shareholders could not vote for, but could "vote against".114 However, not all members were aware of this notice, and as such, on the day of voting some did not exercise their right to vote on the basis of the initial notice.

Callaway JA answered the first question in the negative.115 The judge put the wording of s 257D into perspective. Contrary to the view of the appellants, he interpreted the phrase "no votes in favour of" scribed in section 257D as not suggesting "no votes in favour of or against".116Further, the judge reasoned that the drafting of the words by the Australian legislature was aimed at ensuring that persons seeking to comply with the law, or to enforce it such as ASIC, could rely on the words.117 Therefore, the court held that the combined shareholders were "entitled to vote against" the buy-back resolution in respect of their ordinary shares, and that section 257D did not prohibit preference shareholders, or the combined shareholders in respect of their preference shares, from "voting against" the resolution if they were otherwise entitled to do so pursuant to article 2.4(a)(i) of the company's constitution.118 The latter suggests that if, according to the company's constitution, the excluded shareholders had voting rights in terms of the constitution, but in the instant case they however were excluded only on the basis of a deliberate exercise or mistake of interpretation of the law, then the excluded were entitled to vote against the resolution as the law did not prohibit them from "voting against". From the notice and the scheme booklet, the excluded shareholders were not excluded from voting if a matter pertained to their rights or interests, such as voting for reduction of a company's share capital. If they were excluded by the notice or booklet, then their exclusion was legally untenable.

4.2.3 Was the company justified not to have regarded the buy-back as distribution ?

The appellant's arguments were predicated on the preference shareholders being excluded from exercising their voting rights on a proposed reduction of a company's share capital. Thus, the question here is whether the company was justified in not having regarded the buy-back as a reduction of share capital so that shareholders could vote? In response, the court confirmed that a share buy-back was a reduction of the share capital of the company. Consequently, a reduction has an effect on shareholder rights.119 For the court, the determinative words were "a proposal to reduce the share capital of the Company" scribed in the notice. As a result, Callaway JA reasoned that preference (combined) shareholders had an interest in a proposal of such a nature, as much as they would do in any proposal to wind up a company or for the sale of its undertaking.120 The judge of appeal emphasised that when a vote is passed pursuant to section 257D, the shares would have to be cancelled by a company; thus, any argument which suggests that to merely vote does not reduce share capital is misplaced. Critically for shareholders, no other opportunity would arise so that they protect their rights or interests by voting on the proposal, except in the general meeting. Thus, the position would be the same in a proposed vote to approve a scheme which includes a proposed share buy-back.121So, where a holder of preference shares is as a matter of ordinary language (that is, language in section 257D of the Corporations Act) permitted to vote in terms of article 2.4(a)(i)(C) of the company's constitution to adopt a buy-back, then the position should be no different in a case of voting in a proposed scheme.122

The above manner of reasoning led the court to hold affirmatively on the second question.123 The court saw no reason justifying differentiation in the voting of preference shareholders; that is, if such shareholders are allowed to vote to reduce a company's ordinary or preference share capital, why could they not be allowed to vote in a proposed share buy-back? Ultimately, Callaway JA reasoned that a proposed reading of a provision - article 2.4(a)(i)(C) of the company's constitution - should not cause anomalies as the appellants had suggested.124

5 COMMENTS, OBSERVATIONS AND CONCLUSION

What the preceding discourse avers is that, essentially, section 115(2)(a), like similar provisions from Australia, are proactively aimed at guarding against adverse decisions which might have ex post facto effects detrimental to shareholder rights or interests. From that context, section 115(2)(a) and similarly intended provisions are essential as tools to safeguard shareholder rights or interests. When directors determine the disposal of assets of their companies, or decide to amalgamate or merge or to enter into schemes of arrangement which include re-acquisition of own shares without shareholder contribution in the decision-making process, the rights or interests of shareholders are at the mercy of the choices which directors make on their behalf. The scale of balance between the rights of these parties would therefore cause disconcertment in favour of company directors to the disadvantage of shareholders. Judgments in cases such as Juspoint, Village Roadshow, and Cilliers patently show the predicament to which shareholder rights or interests might be subjected or exposed where the interests of shareholders are entirely placed in the hands of company directors as the ultimate decision-makers. They show that the end product would be legally untenable, to say the least.

5.1 Practical illustration of the operation of s 115(2)(a)

Figure 3 below illustrates the intended operation of section 115(2)(a) of the 2008 Act, assuming, as was referred to earlier, that Company Z classified its shares into three classes, namely: A, B and C, in the percentages shown.

The understanding that the graph seeks to reveal is the different categories into which companies may divide their shares. For a company to be able to buy-back own-issued shares from its directors and prescribed officers or persons related to them, under section 48(8)(a) of the 2008 Act two pertinent questions will have to be addressed:

(i) whether that person has locus standi as a shareholder of that company to vote on the proposed special resolution;125 and

(ii) whether the securities' holding of that person is endowed with voting rights.

The preceding questions appear more or less similar to the issues determined in Village Roadshow seeking to interpret section 257D of the Corporations Act 2001. However, the difference is that, under section 48(8)(a), a repurchase is made to directors, presiding officers and their related persons, whilst section 257D of the Corporations Act does not specify persons in the same way as section 48(8)(a), but simply refers to members of the body. That notwithstanding, the character of persons to whom the buy-back may be made appears to be the same, since section 257D regulates selective buy-backs. To answer the latter questions, the court in Village Roadshow referred to the wording of section 257D, article 2.4(a)(i) of the company's constitution, the notice sent to shareholders as well as the scheme booklet. The court did not refer to the particular section in the Corporations Act which regulates how class rights may be varied by companies.

Under the 2008 Act, to answer the questions one might start by referring to section 37(2). The latter section is instructive because it accords a general voting right to each issued company share regardless of its class, not unless excepted by the Act or that company's MOI.126 The latter was the argument made in Juspoint. Unlike the position under section 257D of the Corporations Act, which required the second question posed in Village Roadshow to be answered in the negative, under the 2008 Act both questions must be answered in the affirmative. Where that occurs, a shareholder shall be entitled to vote under section 115(2)(a) of the 2008 Act in the adoption of a resolution approving a proposed share buy-back scheme. However, if either of the questions is answered in the negative, the person shall not vote even if the person holds securities in the company. That shall be so even if the securities are held through a nominee. In the latter instance, Juspoint and Marble inform us that the nominee shall assume the right to vote in the stead of the beneficial owner.127 So, it is possible that some shareholders may not vote on certain company matters because their shares might be held by a nominee, or because they might not have been endowed with voting rights. If all shareholders are entitled to vote under section 48(8)(a) as owners of and/or investors in the company, then all of them shall cast a vote to approve or disapprove, as the case may be, the determination made by directors to buy-back own issued shares.

Secondly, under section 115(2)(a) of the 2008 Act, and assuming that the board of directors would also have recommended a buy-back from shareholders belonging to a particular class, that is, either class A, B or C, as one anticipates they would have, then, where the proposed buy-back is offered only to class C, both the section and Verimark direct that only shareholders holding shares in class C shall be entitled to pass a special resolution, as does section 257D and section 411(4)(a)(i) of the Corporations Act. Furthermore, fundamentally, it shall be the "presence of a sufficient number of persons to constitute 25 percent of voting rights of the class of shareholders" who are entitled to vote that the 2008 Act contemplates at the meeting, as opposed to the majority expected under the Corporations Act.

Assuming therefore that, in the context of the 2008 Act, each of the three classes consist of five members, then if, for example, out of the five members in Class C the voting rights of three of the shareholders constituted 75% and these shareholders are present on the day the particular buy-back is to be voted on, then the threshold minimum sufficient number of persons to vote 25% of their shares required by the 2008 Act, as well as the provisions of section 64(3) of same Act, shall be satisfied.128Figure 4 below illustrates the point.

Assuming that shareholders 1, 2 and 3 of the five shareholders in the graph have a combined shareholding constituting voting power of 75%, and are present and have voted in terms of s 115(2)(a), then according to the 2008 Act as well as Juspoint, the proposed buy-back shall be adopted irrespective of whether shareholders 4 and 5 were present but did not vote or were present but voted opposing the proposed scheme of arrangement. In the context of the Corporations Act, the 75% will also pass muster, but if the majority had voted against the resolution, the proposal would not pass even if the 75% was attained.

Under the 2008 Act, if shareholders 4 and 5 intend to challenge the adoption of the special resolutions, then to be entitled to do so in terms of section 115(3), (6) and (7) of the 2008 Act or make a demand in terms of section 164 of same Act, their "presence and voting" shall automatically qualify them to embark on either course.129 However, depending on which course they opt for, that is, section 115(3), (6) and (7) or a section 164 challenge, the shareholders will have to satisfy the requirements provided for by the sections. Of importance for companies to note is that shareholders - those contemplated to vote in terms of sections 48(8)(a) and 115(2)(a) - would be entitled to be informed, through a notice, of the meeting and their rights, and be provided with sufficient, clear and unambiguous information to be in a position to make informed decisions whether or not to vote in favour or to oppose a proposed scheme.130 In Juspoint, Capprec and Village Roadshow, the correct procedure to inform shareholders about the proposed changes was followed. However, what was in contention was the unfairness by which the arrangements were structured so as to prejudice shareholders. For example, in Village Roadshow, the court found that the notice and the booklet were deliberately crafted to mislead the preference and combined shareholders.

5.2 Conclusion

In sum, there are slight variances in the wording of provisions intended to protect shareholders between the statutes consulted. This notwithstanding, it is commendable that under all the statutes the passing of special resolutions to approve a buy-back is the norm. This norm is adhered to in Canada as well, even though the CBCA does not expressly provide for shareholder approval within its provisions on fundamental changes but only where a company's capital is to be reduced.131 The exception is with respect to the UK Companies Act 2006, the CBCA, and the Corporations Act 2001 jurisdictions, where a court-approval process is mandatory as well.

Until recently, the challenge to shareholder protection regulated under section 115(2)(a) of the 2008 Act as well as its veracity have been slow to be determined before South African courts. It is encouraging that, currently, the paucity of case law interpreting the provision is beginning to be supplemented. Indeed, in time more case law will unravel and provide proper clarity and context to the application of the section. Such clarity will especially be welcome when coming from the Superior Courts so that section 115(2)(a) can firmly find its footing. The judgments consulted, such as Juspoint, Moraitis, Marble, Village Roadshow and Cilliers, exhibit how important shareholder participation is to approve, but in the same breathe, for shareholders to participate in company affairs where their rights/interests are at stake. The 2008 Act has made it the responsibility of shareholders to protect themselves against contemplated changes in the capital structure of their companies and guard themselves against adverse effects.

BIBLIOGRAPHY

Books

Blackman MS, Jooste JD & Everinghan K Commentary on the Companies Act 2008 Claremont: Juta (2018) [ Links ]

Bottomley S et al Contemporary Australian corporate law 2ed United Kingdom: Cambridge University Press (2020) [ Links ]

Cassim FHI et al Contemporary company law 2ed Claremont: Juta (2012) [ Links ]

Cilliers HS & Benade ML Corporate law 3ed Durban: Butterworths (2000) [ Links ]

Delport PA, Vorster Q & Henochsberg ES Henochsberg on the Companies Act 71 of2008 Durban: LexisNexis (2011) [ Links ]

Paine J Schemes of arrangement: Theory, structure and operation United Kingdom: Cambridge University Press (2014) [ Links ]

Journal articles

Bidie SS "Dismantling obstacles impeding better governance in companies: Affirming the expansion of the interpretation of 'shareholder and director' in section 163 of the 2008 Act" 2021 (25) Law, Democracy & Development 377-410 [ Links ]

Cassim FHI "The reform of company law and the capital maintenance concept" 2005 South African Law Journal 287-293 [ Links ]

Chakraborty T "Share repurchases in India, U.S.A. and U.K.: A comparative study" 2002-2004 Caluniv BS Journal 159-171 [ Links ]

Chan K et al "Share repurchases as a potential tool to mislead investors" (2010) Journal of Corporate Finance 16 (2) 137-158 [ Links ]

Dharmawan GV & Mitchell JD "The legislative framework of share buy-backs: A comparison of the 'old' and 'existing' requirements" 1999 (18) University of Tasmania Review 283-308 [ Links ]