Services on Demand

Article

English (pdf)

English (pdf)

Article in xml format

Article in xml format Article references

Article references

Indicators

Related links

-

Cited by Google

Cited by Google -

Similars in Google

Similars in Google

Share

Permalink

PermalinkSouthern African Journal of Entrepreneurship and Small Business Management

On-line version ISSN 2071-3185

Print version ISSN 2522-7343

SAJESBM vol.14 n.1 Cape Town 2022

http://dx.doi.org/10.4102/sajesbm.v14i1.590

ORIGINAL RESEARCH

Establishing turnaround potential before commencement of formal turnaround proceedings

Wesley J. Rosslyn-Smith; Marius Pretorius

Department of Business Management, Faculty of Economic and Management Sciences, University of Pretoria, Pretoria, South Africa

ABSTRACT

BACKGROUND: Determining the turnaround potential of a firm has plagued academia and practice. Existing failure prediction tools yield limited insight into turnaround potential and are heavily dependent on financial metrics. This framework made a valuable contribution to research in this field as it added a new perspective for decision-making purposes.

AIM: Practitioners, judges or directors require a quick, efficient framework to aid in developing a reliable opinion on the likelihood of liquidation of a firm intending to commence with reorganisation proceedings. The aim is to speed up the liquidation of economically inefficient firms that attempt to seek shelter in reorganisation.

SETTING: The study was conducted in South Africa and made use of experts in the field of turnaround management.

METHODS: The indicators were derived from a strong and widely used managerial tool known as the Delphi method. The relative importance of each element was allocated using a powerful mathematical model known as the analytic hierarchy process (AHP

RESULTS: This study identified key indicators for the nine liabilities with accompanied weights of relative importance for a likelihood of liquidation framework. Anchor scale values are proposed for each indicator to assist in its application. The framework is timely in its application, considers the availability of accurate data, inexpensive to implement and easy to interpret.

CONCLUSION: The likelihood of liquidation framework was developed to include a broader spectrum of liabilities to assist in deciding the viability of recovery of a firm in reorganisation.

Keywords: turnaround; reorganisation; insolvency; commencement standard; AHP; Delphi technique.

Introduction

In recent years there has been a significant contribution made by researchers and practitioners on the prediction of business failures (Wu, Gaunt & Gray 2010:36). Failure can be defined in various ways, taking into consideration the specific interest or condition of the firm under scrutiny. Reorganisation1 is often an important vehicle for failing firms and their creditors to pursue intensive turnaround strategies. However, one is often under the impression to conclude that reorganisation has failed if the firm is subsequently liquidated or sold, whereas this may be the desired outcome of an efficient process. Reorganisation is aimed at rescuing an economically viable firm that experiences temporary financial difficulty - financially distressed (Franks & Torous 1992). Critical to the decision to pursue turnaround efforts is the likelihood of the firm succumbing to liquidation. An economically distressed firm will not find any salvation within reorganisation and will simply erode the value of the firm away. Therefore, a commencement standard looks to screen out severely economically distressed firms that will not benefit from reorganisation proceedings. Such a standard may look to failure prediction models; however, traditional prediction models typically rely on financial metrics and have difficulty in considering other crucial elements of economic viability (Deakin 1977; Trahms, Ndofor & Sirmon 2013:1289). Furthermore, there is criticism over the lack of methodological rigour in identifying the turnaround potential of firms on which to conduct such analysis (Pandit 2000:32; Pearce & Robbins 1993:626). A valuable contribution to research in this field must therefore seek to redress this neglect, forming new ways of filtering these phenomena from proceedings. The likelihood of liquidation framework (LOL) was developed to include a broader spectrum of liabilities to assist in deciding the viability of recovery of a firm in reorganisation.

The LOL is a basic arrangement of liabilities used to determine the emergence of the firm from reorganisation in a solvent condition and with reasonable prospects of financial stability and success. The framework has been developed using the South African business rescue reorganisation process in a manner that allows adaptation to various other jurisdictions.

This article aims to continue the development of the LOL for its eventual use in practice. To do so, the study (1) identifies key indicators for the nine liabilities, then (2) investigates the relative importance of each liability/indicator, and finally (3) proposes anchor scale values for each indicator. The indicators were derived from a strong and widely used managerial tool known as the Delphi method. The relative importance of each element was allocated using a powerful mathematical model known as the analytic hierarchy process (AHP). The enhanced framework is expected to provide some indication of the reasonable prospect of a firm prior to the commencement of business rescue proceedings. If effective, this framework stands to reduce the number of economically distressed firms from abusing proceedings and ultimately preserve firm value.

The likelihood of liquidation framework

The LOL consists of nine liabilities that were derived from existing turnaround literature. For example, the liability of creditor composition is a construct drawn from Ayotte and Morrison (2009), Bergström, Eisenberg and Sundgren (2002) and Campbell (1996). Each liability represents an acute vulnerability of a firm during the formal turnaround process. The framework consolidates all these liabilities to assess the prospect of the firm succumbing to liquidation. Under the evidence of absence, LOL removes the intrinsic variables associated with failure to assume a reasonable prospect at the commencement of business rescue for the recovery of a firm. This however assumes the value maximisation principle remains valid. The framework allows decision-makers to consider the relevant factors before commencing reorganisation proceedings given the limited information and data accuracy associated at that point in time. The nine liabilities include functional business model, reorganisational slack, creditor composition, stakeholder influence, liability of smallness, liability of data, liability of leadership, liability of obsolescence and external legitimacy.

Each liability contributes to the overall likelihood of liquidation. In some circumstances, a liability may be unlikely, while in others it may serve as a 'fatal liability' thereby suggesting liquidation is almost certain. The intensity of each liability is determined by its indicators which were derived using the Delphi study.

Research methods and design

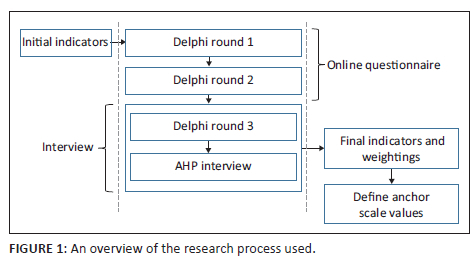

The study utilised a mixed method research design that assisted in completing the LOL framework. In line with Creswell (2012:543), an exploratory sequential mixed methods design, or two-phase model, is best suited for the task. This method involves the procedure of first gathering qualitative data to explore a phenomenon and then collecting quantitative data to explain relationships found in the qualitative data. Therefore, the researchers were able to identify measures actually grounded in the data obtained from study participants. The study consisted of two primary research techniques, Delphi and AHP, which fell into a sequence of steps as depicted in Figure 1. The use of these two methods in exploratory sequential mixed methods design was reinforced by Khorramshahgol and Moustakis (1988) when they termed the methodology the Delphic hierarchy process.

An initial set of between five and seven indicators were derived for each liability by the researchers from the literature. Each indicator was given a title and definition that were presented to the participants in the first round of the Delphi study. The participants consisted of 11 experts who were purposefully selected based on their knowledge and experience in the field of business turnaround. The sample size was also considered acceptable for both studies as it remains exploratory in nature (Cheng & Li 2002:197; Okoli & Pawlowski 2004:18; Wong & Li 2008:12). These experts were considered eligible to be invited to participate in the Delphi study as they shared related backgrounds and experiences concerning the target issue, were capable of contributing helpful inputs, and were willing to revise their initial or previous judgments for the purpose of attaining consensus. The researchers closely examined and seriously considered the qualifications of participants in addition to their acclaim and respect within the target groups of experts. The participants ranged from academics, business rescue practitioners to corporate recovery consultants. The methodology and findings from the two primary research techniques are described next.

The Delphi method

The Delphi method is a widely used and accepted method for attaining convergence of opinion regarding real-world knowledge solicited from experts in certain fields. The technique can be mostly attributed to Dalkey, Brown and Cochran (1969), who maintained that 'two heads are better than one, or…n heads are better than one' (Dalkey et al. 1969:6). According to Dalkey, there are three features of Delphi: (1) anonymity; (2) controlled feedback and (3) statistical group response. Anonymity is preserved by using a questionnaire and thereby lessening the impact of dominant individuals. Controlled feedback is ensured by conducting the study in a sequence of rounds where the results thereof are shared with the participants at the end of each round to promote objectivity. Finally, a broad definition of the response aims to decrease group pressure for conformity as towards the conclusion of the rounds there may still be a significant spread in individual opinions. Keeping this in mind, the inclusive group response is designed to assure that the opinion of every participant is incorporated in the final response.

Linstone and Turoff (2002) outline the process of a conventional Delphi study as firstly:

[D]esigning a questionnaire which is sent to a larger participant group. After the questionnaire is returned, the researcher summarises the feedback and, based upon the results, develops a new questionnaire for the participant group. The participant group were given at least an opportunity to re-evaluate its original answers based upon examination of the group response. To a degree, this form of Delphi is a combination of a polling procedure and a conference procedure which attempts to shift a significant portion of the effort needed for individuals to communicate from the larger participant group to the smaller monitor team. (p. 5)

This study made use of an online questionnaire for the first and second round that ran participants through a video tutorial explaining the LOL framework, objective of the study and what their role is in the Delphi process. The participants were asked to evaluate and add indicators in consideration of the SMART criteria (Specific, Measurable, Attainable, Realistic, Time-sensitive).

SMART

The SMART criteria assisted the participants in assessing and suggesting indicators that were relevant in relation to the study's objective. Each of the SMART elements is defined as follows:

-

Specific: Indicators should be detailed and as specific as possible. Loose, broad or vague indicators are not desirable.

-

Measurable: In order to clearly determine a value, indicators should not be ambiguous but rather as clear and concrete as possible. It is important that an indicator can be measurable. The measure may be quantitative or qualitative, but measurement should be against a standard of performance and a standard of expectation understood by an industry professional.

-

Attainable and aggressive: Success or failure is only fairly attributed against practical indicators. Indicators should not be out of reach. They should be reasonable and attainable within the typically hostile and chaotic environment experienced in business rescue. However, setting indicators is a balance between this degree of 'attainability' and challenge and aspiration.

-

Realistic and result-oriented: Extending the concept of attainability, a goal should be realistic. It is possible that a goal could be set that is attainable, but not realistic in the particular working conditions. Being realistic in the choice of indicators is helpful in examining the availability of resources and selecting indicators.

-

Time-sensitive: Indicators should be selected in view of the strict timelines afforded in business rescue. Success is dependant on finding information within a few days.

During the first-round, participants were obligated to suggest two of their own indicators before being presented with the initial set compiled by the researchers. Participants then had the opportunity to accept, reject or modify each indicator while providing their reasoning as well. Participants could add new indicators at any point during all three rounds.

To assist the participants the researchers compiled the first set of indicators that were derived from the literature and the researchers' knowledge and experience. These initial indicators ranged from standard to controversial in nature. They aimed to trigger innovative thinking and provide critical mass for the Delphi process to work from. During each round, the participants were asked to accept, modify or reject each indicator with reasoning and with a confidence level. New indicators could be suggested at any point during the study. After each round, the researchers reviewed all the indicators and incorporated all the participants' input based on the sound reasoning and level of confidence. A new set of indicators then emerged and were presented to the group with any modifications being clearly highlighted. Thereafter, each round offered individuals an opportunity to modify or refine their judgments based on their reaction to the collective views of the group.

A satisfactory level of consensus was defined in this study when the participants no longer could add new indicators and accepted the remaining indicators. Minor modifications or rejections with low confidence levels and weak reasoning were regarded insufficient to warrant changes in the last round.

Ethical considerations

This article followed all ethical standards for research without direct contact with human or animal subjects.

Results

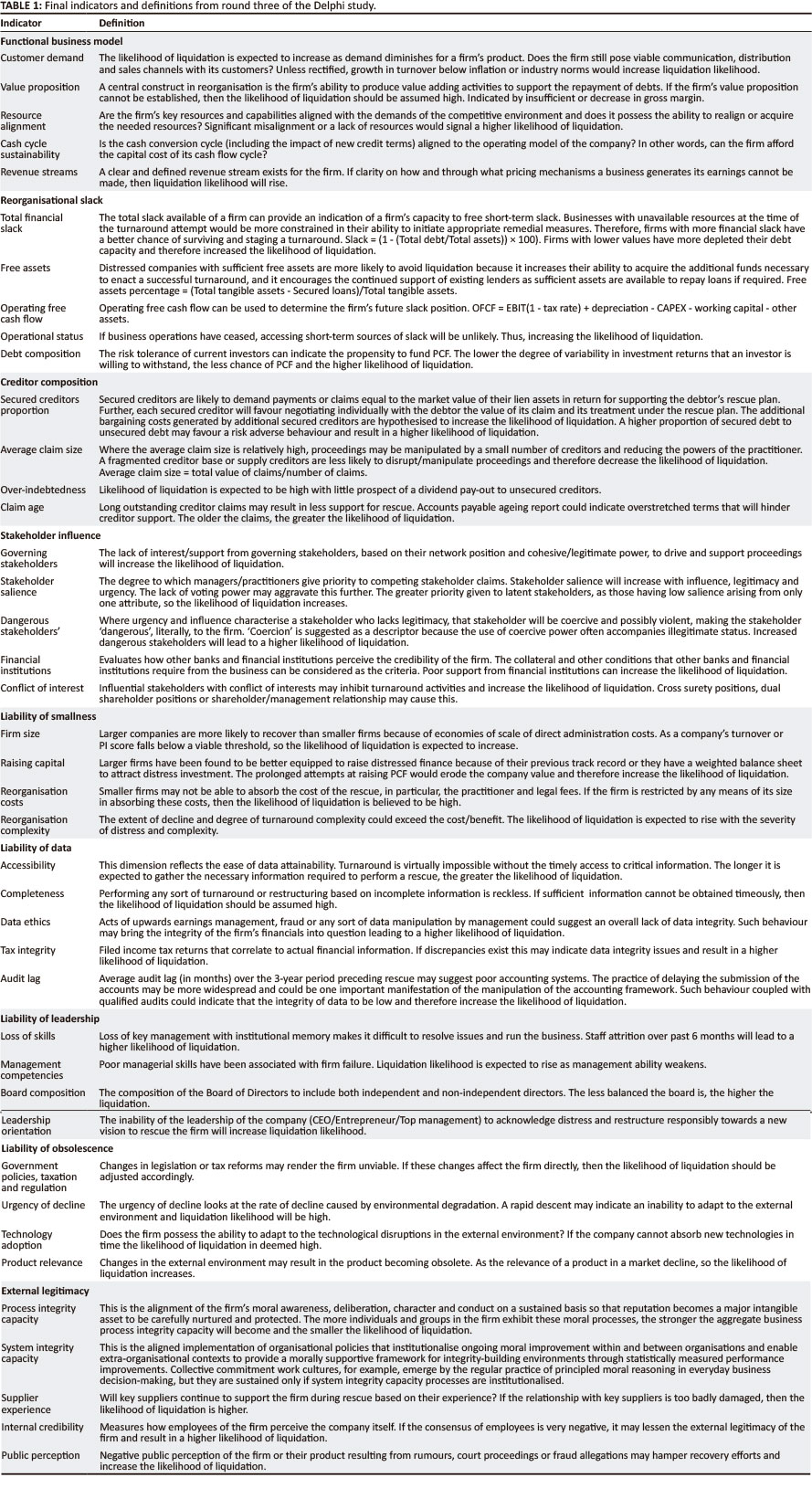

The first round of the Delphi study resulted in the most significant amount of changes and additions by the participants. Synthesising new indicators proved difficult because of the varying perspectives of the participants; however, this brought new and intriguing views to the fold. The number of indicators ranged from 56 in round one, 67 in round two and 41 in round three. The first round focused less on consensus and more on exposing all the differing positions advocated and the principal pro and con arguments for those positions. The average level of confidence increased progressively through the rounds as consensus emerged. A satisfactory consensus level was reached, by incorporating agreement and importance aspects, in round three with the final indicators emerging from the study listed in Table 1.

During the study, participants questioned indicators in their entirety as well as more detailed aspects of the definitions. The inclusion of the SMART criteria certainly helped the participants build consensus faster as it was often referenced during all three rounds. In an interesting turn of events, the participants took a preference to non-financial metrics in describing indicators. This may be the result of data integrity issues, time constraints and data lead times that are typically prone to information at commencement. The 41 indicators in Table 1 provided a non-exhaustive list obtained from numerous experts with domain knowledge that asses the likelihood of liquidation of a firm before commencing with reorganisation proceedings.

Analytic hierarchy process

The AHP was developed by Thomas L. Saaty as a decision-making theory. It is a structural method that helps to elicit preference of expert opinion from decision makers using a multi-criteria decision-making method. Analytic hierarchy process allows decision makers to rank, select, evaluate and benchmark a wide variety of decision alternatives using the systematic procedure (Forman & Gass 2001; Golden, Wasil & Harker 1989; Saaty & Vargas 2012). The model utilises a hierarchical structure which consists of an objective, criteria, sub-criteria and alternatives. Based on pairwise comparison judgments, AHP integrates both criteria importance and alternative preference measures into a single overall score for ranking decision alternatives (Saaty 1990). The versatility of the AHP method can incorporate both qualitative and quantitative approaches to solve complex decision problems (Cheng & Li 2002). Analytic hierarchy process, therefore, offers a holistic analysis of complex relationships inherent in a problem and assists the decision maker in assessing whether the evaluation criteria are of the same order of importance so that the decision maker can compare such homogeneous alternatives accurately.

Analytic hierarchy process harnesses domain knowledge from experts and forms a systematic framework for conducting structured group decisions for a large number of both quantitative (financial ratios) and qualitative (non-financial) criteria (Park & Han 2002:3). This study applies the AHP methodology to exploit domain knowledge in acquiring weights from domain experts. The AHP approach has been applied to a variety of complex decisions in the business domain, including the problem of granting corporate credit, portfolio management and the assignment of sovereign debt ratings, among other business decision problems (Bolster, Janjigian & Trahan 1995; Clark et al. 1997; Lee, Kwak & Han 1995; Levary & Wan 1999).

This study used the AHP method to specify numerical weights representing the relative importance of each liability and indicator in the LOL framework. Participants were asked to consider the importance of one element over the other in consideration of the following objective: 'it's importance in increasing the likelihood of liquidation of a firm on commencement of business rescue'. The LOL framework was integrated within AHP by using the liabilities as criteria and the indicators identified by the Delphi process as sub-criteria. Pair-wise comparison judgments were made concerning the attributes of one level of hierarchy given the attribute of the next higher level of hierarchy - AHP consists of three principles namely, decomposition, comparative judgment and priority synthesis (Saaty 1990).

Using the AHP method for group decision making involves merging responses using geometric means (Lee et al. 1995:4; Saaty 2008:95). Dyer and Forman (1992) highlight three benefits for AHP in group decision making namely, (1) it accommodates both tangible and intangible characteristics, individual values and shared values in the group decision process, (2) assists in structuring a group decision so that the discussion centres on objectives rather than on alternatives and (3) enables the discussion to continue until all available and pertinent information have been considered.

Analytic hierarchy process is also able to solicit consistent subjective expert judgment using a consistency test. The consistency of the results is measured using a consistency ratio (actually 'inconsistency ratio'). The liabilities and indicators were regarded as highly interrelated and therefore a high consistency ratio was allowed. The consistency ratio of less than 10% is considered adequate to interpret the results (Carnero 2005:546). Saaty and Vargas (2012) recommend using a normalised eigenvector approach, which is best implemented by computer software such as AHP-OS.

The group consensus indicator quantifies the level of agreement on the outcoming priorities between participants. The consensus indicator is a derivative from the concept of diversity based on Shannon alpha and beta entropy (Jost 2006). The measure reflects the homogeneity of priorities between the participants and can also be interpreted as a measure of overlap between priorities of the group members. Note though that group decision-making aims to obtain consent, not necessarily the agreement of the participants by accommodating views of all parties involved to attain a decision that will yield what will be beneficial to the entire group (Herrera-Viedma et al. 2014:4). The consensus indicator, however, should be strictly distinguished from the consistency ratio.

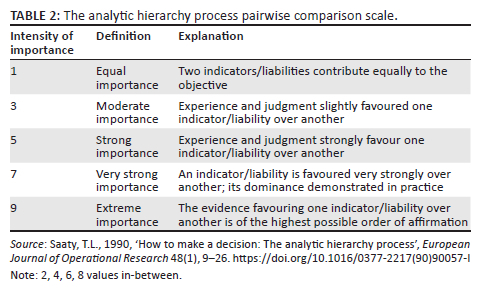

The relative importance of the criteria and sub-criteria were rated by the nine-point scale proposed by Saaty (1990:15), as listed in Table 2. The scale distinguishes the levels of relative importance from equal, moderate, strong, very strong, to an extreme level by 1, 3, 5, 7 and 9, respectively. The intermediate values between two adjacent arguments are represented by 2, 4, 6 and 8.

A comparison matrix is created by comparing pairs of criteria and sub-criteria (Saaty 1990:12). The pairwise comparison assists in judging independently the contribution of each criterion to the objective. The priority synthesis computes a composite weight for each alternative, based on preferences ascertained through the comparison matrix. Alternatives in this study took the form of various variables obtained from a distressed firm. Using the composite weight, the relative priority of each alternative can be obtained. A sensitivity analysis is applied to show how criteria weighting deviations can affect the changes of ranks of alternatives.

A questionnaire-based field survey was used to collect the participants' ratings. Through individual interviews with participants the data was concurrently transferred into an online application to test, in real time, the consistency of the data (Goepel 2017). This was done for several reasons, first, to reduce the time burden on participants as the number of pairwise comparisons were substantial. Secondly, the participant was alerted to when they exceeded the maximum consistency ratio and could make the necessary alterations without being influenced by the software's recommendations. During the interview, participants were allowed to re-examine their comparisons, calculated weights and the final results derived from their initial and subsequent responses. They were also allowed to assess the results and inspect the reasonableness of the rankings until they were completely satisfied with the outcomes. Finally, the interview also allowed the researchers to capture deeper insights into the participant's choices which lead to some fascinating findings.

Discussion

The output showcased in Table 3, Table 4 and Table 5 represent the final judgments of the group. Obviously, these tables were the results of many debates, persuasions and discussions. For example, there were occasions when some participants debated the meaning of their high inconsistency of choices which gave researchers deeper insight. It became obvious early on that AHP could contribute significantly more than just prioritising elements.

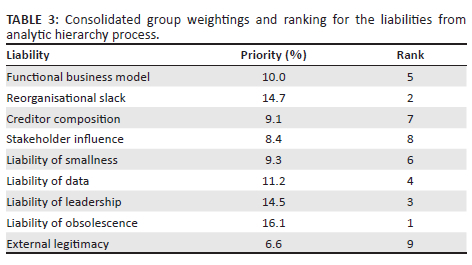

To analyse the survey findings, the judgment matrices were pair-wise compared and computed using the use of a software package (Goepel 2017). The AHP calculations therefore have been omitted in line with the recent articles (Chen et al. 2017; Herrera-Viedma et al. 2014; Okwir et al. 2017; Raviv, Shapira & Fishbain 2017). The local priority weights of all the liabilities and indicators were first calculated and then combined with all successive hierarchical levels in each matrix to obtain a global priority vector. A list of the global priorities for each indicator is presented in Table 3. The higher the mean weight of global priority vector, the greater the relative importance. Therefore, this serves to distinguish the more important indicators from the less important ones. Beyond the global priorities, the AHP survey revealed a number of interesting and unexpected results.

Surprisingly, participants considered external legitimacy (6.6%) to be the least important liability. The external legitimacy concerns the perceived integrity of the business by its external stakeholders. The low ranking of this liability may stem from the fact that the participants considered direct stakeholders of the firm to be more significant and influential in increasing the likelihood of liquidation. The AHP group consensus of 43.2% across the liabilities is regarded by Goepel (2013) as very low signifying a high diversity of judgments. Although participants were not able to add or remove any liability, the indicators selected in the Delphi process ultimately defined each liability. This probably explains the broad range of indicators that evolved from the Delphi process.

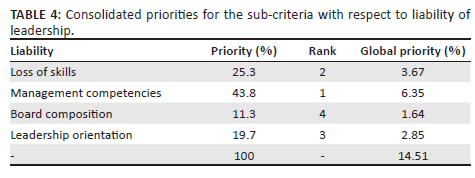

The consolidated group weightings for the liabilities (main criteria) are listed in Table 3. Participants reported that the liability of obsolescence (16.1%) is the most important liability in increasing the likelihood of liquidation of a firm on commencement of business rescue. The liability carried by reorganisational slack (14.7%) and liability of leadership (14.5%) weighed in slightly less respectively. The consolidated priorities for the indicators concerning liability of leadership are listed in Table 4. This liability seems to be mostly influenced by the management lower-case is perfect. (43.8% local priority) indicator which emerged with one of the highest global priorities as well. During the interviews, participants reiterated this by affirming that the competency of management plays a significant role in ensuring the firms' success. While the business rescue practitioner can substitute the leadership of a firm this indicator may suggest that in practice this is unlikely to happen fast enough. This supports the work of Lohrke, Bedeian and Palmer (2004:79) and Smith and Graves (2005:306) in that top management competency will directly affect the likelihood of reversing organisational decline.

The weightings for the liabilities ranged between 16.1% and 6.6%, which suggest a relatively even distribution. The strongest liability being liability of obsolescence (16.1%) is mostly made-up of urgency of decline and product relevance indicators.

Two indicators that emerged the most influential within the LOL framework were management competencies (6.3%) and product relevance (6.3%). The latter indicator shares a close resemblance to the customer demand (2.2%) indicator; however, it exhibits a key distinction that the researchers suspect accounts for its prevalent status. Customer demand focuses on diminishing demand for a firm's product resulting from internal factors such as a breakdown in communication, distribution and sales channels with its customers. While product relevance is orientated around changes in the external environment that may result in the product becoming obsolete. The distinction highlights an important feature of the LOL framework in that it is more concerned with factors that will have a certain impact on the outcome of liquidation rather than factors that could be rehabilitated in rescue.

Remaining within the liability of obsolescence, the third most influential indicator was the urgency of decline (5.1%). Francis and Desai (2005) echo this finding by explaining when the erosion of resources is severe (magnitude) and rapid (time), turnaround becomes exceedingly difficult. Interestingly participants with a predominately business background favoured this indicator. The urgency of decline at the commencement of proceedings can indicate the time and resources available to attempt any rehabilitation efforts.

This study reported a positive overall consistency ratio of 2.4%, which is far below the recommended 10% acceptable margin (Carnero 2005:546) and can be regarded as reasonably consistent. Although the participants individually pushed the limits of the ratio the consolidated matrix ratio was more than acceptable. Miller (1956) warns about the human limits on the capacity for processing information while dealing with several criteria and as the study involved numerous interrelated indicators this was a difficult task for participants.

A group consensus of 54.8% across all the indicators indicates a high diversity of judgments (100% refers to absolute consensus). This was a particularly interesting finding considering all the indicators emerged from Delphi study that involved the same group of participants. This finding may suggest that the perception of reasonable prospect of a firm varies between experts and could account for the conflict that arises around this term. The consensus indicator allows for deeper analysis of sub-groups (clusters) of participants with high consensus among themselves, but with a low consensus to other sub-groups. Bard and Sousk (1990:227) remind, however, that 'from the standpoint of consensus building, the AHP provides an accessible data format and a logical means of synthesising judgment. The consequences of individual responses are easily traced through the computations and can be quickly revised when the situation warrants'.

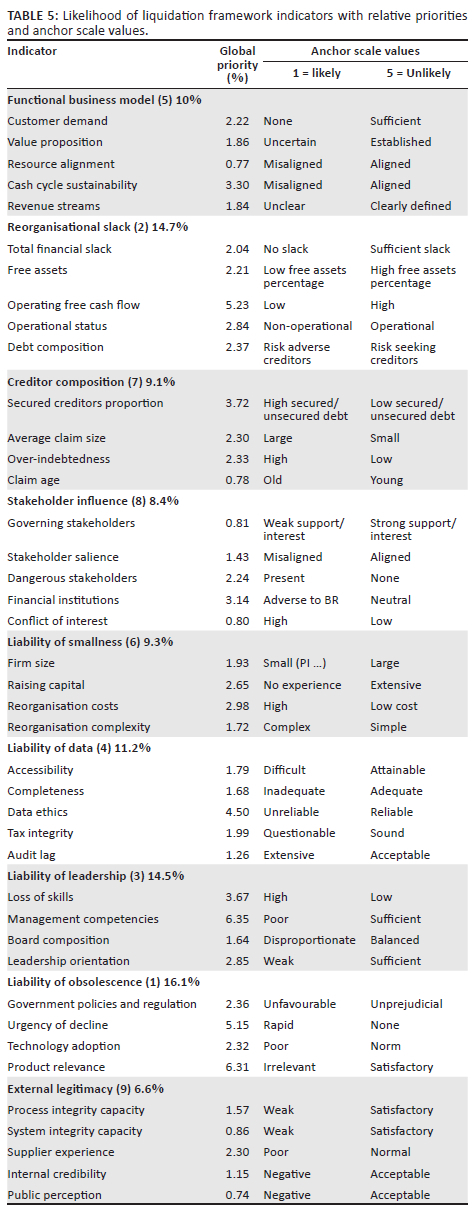

Group consensus was highest in the liability of leadership (74.6%), stakeholder influence (74.1%) and creditor composition (71.1%). Curiously, participants from financial backgrounds weighted Operational Status of the firm far higher than the other participants. Conversely, the chosen business rescue practitioners signalled indicators such as secured creditors proportion and dangerous stakeholders proportionally more. Analytic hierarchy process accommodated each participant's views in order to attain a decision that yielded what will be beneficial to the entire group and not necessarily to the particular individuals involved. The global priorities listed in Table 5 reflect the views of a balanced group of experts on the importance of each indicator in increasing the likelihood of liquidation of a firm on commencement of business rescue.

Proposed framework

To recap, the objective of this study is to continue the development of the LOL framework for its eventual use in practice. The results from the Delphi process identified 41 key indicators for the nine liabilities. Analytic hierarchy process investigated the relative importance of each liability/indicator from which weights were derived. Finally, to complete the LOL framework, the study proposes anchor scale values for each indicator.

Assigning values to the likelihood of liquidation framework indicators

To transform the qualitative indicators into a form more suited to computing the likelihood of liquidation the study adopted a five-point scale to assess the magnitude of an indicator. For each indicator, the researchers have recommended anchor values listed in Table 5. The anchor values aim to provide a standardised approach to assessing the magnitude of an indicator in a firm. The popular Likert scale (1-5) was applied between the two values in equal intervals to measure the proportionality of severity of the indicator. The scale values are anchored with one contributing significantly to the outcome of liquidation and five indicating an unlikely impact on the eventuality of liquidation. The unlikely anchor value (5) reflects the position where the indicator has no contributing effect to the LOL score. Therefore, the indicator is measured on a monotone increasing semantic differential scale consisting of five negative adjectival statements (see Table 5). The anchor scale value chosen to best describe an indicator's manifestation in a firm is referred to as an indicator's value (a).

Likelihood of liquidation framework score

The LOL score is a closed unit interval [0, 1] that signals the firms' likelihood of liquidation at the commencement of reorganisation proceedings. A value of 0 will indicate a high likelihood of liquidation while a value of 1 will indicate that liquidation is unlikely. It is important to note that the LOL score is not a prediction of failure but an indication at a particular point in time of the likelihood of liquidation and should be used to determine if reorganisation is suitable for the value maximisation of the firm. The LOL score can be calculated using the following formula:

where N is the number of indicators (41), ai is the value for each indicator with i and ai (1, 2, 3, 4, 5) and wi is the weight for each indicator i. The LOL score is calculated from the sum of the weighted values of all the indicators. As the LOL score diminishes in value from 1 to 0, so the higher the likelihood of the firm conceding to liquidation there is during reorganisation.

The LOL framework, in addition, considers the notion of a 'fatal liability' which refers to resources (or the absence thereof) that pose an imminent threat to a firm's survival. Should any indicator be deemed significant enough in its totality to induce liquidation then it may be deemed a fatal liability. The identification of a fatal liability therefore results in an LOL score of 0.

Conclusion

It has been a stated desire for academics and practitioners to assess the turnaround potential of a firm prior to any sort of formal restructuring procedure is initiated. The task, however, remains highly complex, and although turnaround research has made significant strides over the past years, there is still little consensus on the matter. As reorganisation grows in popularity within an environment prone to rapid and radical discontinuous change, so the need to screen out severely economically distressed firms becomes more urgent. This article has presented a value weighted assessment framework that estimates the likelihood of the firm entering liquidation. The important features of the framework are that it is timely in its application, considers the availability of accurate data, inexpensive to implement and easy to interpret. Practitioners, judges or directors can use the framework as a decision aid when developing an expert opinion regarding the likelihood of liquidation of a firm intending to commence with reorganisation proceedings. The aim is to speed up the liquidation of economically inefficient firms that attempt to seek shelter in reorganisation.

Prior studies have concentrated on predicting the insolvency filing event or discriminating between healthy and financially distressed firms. This study utilises a robust new liquidation identification methodology that links collective expert decision-making with both financial and non-financial metrics. The LOL framework does not limit the firm's turnaround potential but rather works on the reverse assumption that removes the likelihood of liquidation. Therefore, a commencement decision can be determined without knowledge of the possible turnaround strategies that may be deployed. There is no guarantee in any reorganisation attempt that when a reasonable prospect exists at commencement it will necessarily translate into successful turnaround of the firm.

Limitations and future research

This study does have limitations that should be revisited in future studies. Firstly, the sample size of the study was limited because of the intensive contribution required by experts in the field. Future research may wish to isolate various liabilities and gather data from more experts. Secondly, during AHP analysis there seems to be the notion that experts may exhibit unique perspectives on reasonable prospects that are stereotypical of their organisation. Future research may want to explore this phenomenon further. Non-financial indicators seem to be more useful for practitioners, creditors and judges in assessing reasonable prospect. This relates to another important public policy issue of the relevance of accounting disclosure. It is recommended that the indicators identified be allowed to inspire new perspectives on the going concern qualification. Lastly, the LOL framework lacks statistical evidence of its effectiveness in assessing the likelihood of liquidation. The researchers strongly suggest that the framework is expanded on in future studies. The LOL score has the potential to assist in estimating the recovery rate in reorganisation. It is therefore hoped that this research will provide a stimulus for further work that will help increase the understanding of this highly complex yet intriguing aspect of insolvency.

Acknowledgements

Competing interests

The authors declare that they have no financial or personal relationships that may have inappropriately influenced them in writing this article.

Authors' contributions

W.R.S. wrote and conceptualised the article, and M.P. acted as the supervisor.

Funding information

This research received no specific grant from any funding agency in the public, commercial or not-for-profit sectors.

Data availability

Data sharing is not applicable to this article as no new data were created or analysed in this study.

Disclaimer

The views and opinions expressed in this article are those of the authors and do not necessarily reflect the official policy or position of any affiliated agency of the authors.

References

Ayotte, K.M. & Morrison, E.R., 2009, 'Creditor control and conflict in chapter 11', Journal of Legal Analysis 1(2), 511-551. https://doi.org/10.1093/jla/1.2.511 [ Links ]

Bard, J.F. & Sousk, S.F., 1990, 'A tradeoff analysis for rough terrain cargo handlers using the AHP: An example of group decision making', IEEE Transactions on Engineering Management 37(3), 222-228. https://doi.org/10.1109/17.104292 [ Links ]

Bergström, C., Eisenberg, T. & Sundgren, S., 2002, 'Secured debt and the likelihood of reorganization', International Review of Law and Economics 21(4), 359-372. https://doi.org/10.1016/S0144-8188(01)00075-8 [ Links ]

Bolster, P.J., Janjigian, V. & Trahan, E.A., 1995, 'Determining investor suitability using the analytic hierarchy process', Financial Analysts Journal 51(4), 63-75. https://doi.org/10.2469/faj.v51.n4.1922 [ Links ]

Campbell, S.V., 1996, 'Predicting bankruptcy reorganization for closely held firms', Accounting Horizons 10(3), 12. [ Links ]

Carnero, M.C., 2005, 'Selection of diagnostic techniques and instrumentation in a predictive maintenance program. A case study', Decision Support Systems 38(4), 539-555. https://doi.org/10.1016/j.dss.2003.09.003 [ Links ]

Chen, L., Ng, E., Huang, S.-C. & Fang, W.-T., 2017, 'A self-evaluation system of quality planning for tourist attractions in Taiwan: An integrated AHP-Delphi approach from career professionals', Sustainability 9(10), 1751. https://doi.org/10.3390/su9101751 [ Links ]

Cheng, E.W. & Li, H., 2002, 'Construction partnering process and associated critical success factors: Quantitative investigation', Journal of Management in Engineering 18(4), 194-202. https://doi.org/10.1061/(ASCE)0742-597X(2002)18:4(194) [ Links ]

Clark, C.E., Foster, P.L., Hogan, K.M. & Webster, G.H., 1997, 'Judgmental approach to forecasting bankruptcy', The Journal of Business Forecasting 16(2), 14-18. [ Links ]

Creswell, J.W., 2012, Educational research: Planning, conducting, and evaluating quantitative and qualitative research, Pearson, Boston, MA. [ Links ]

Dalkey, N.C., Brown, B.B. & Cochran, S., 1969, The Delphi method: An experimental study of group opinion, Rand Corporation, Santa Monica, CA. [ Links ]

Deakin, E.B., 1977, 'Business failure prediction - An empirical analysis', in E. Altman & A. Sametz (eds.), Financial crises: Institutions and markets in a fragile environment, pp. 117-138, John Wiley & Sons, New York, NY. [ Links ]

Dyer, R.F. & Forman, E.H., 1992, 'Group decision support with the analytic hierarchy process', Decision Support Systems 8(2), 99-124. https://doi.org/10.1016/0167-9236(92)90003-8 [ Links ]

Forman, E.H. & Gass, S.I., 2001, 'The analytic hierarchy process - An exposition', Operations Research 49(4), 469-486. https://doi.org/10.1016/0167-9236(92)90003-8 [ Links ]

Francis, J.D. & Desai, A.B., 2005, 'Situational and organizational determinants of turnaround', Management Decision 43(9), 1203-1224. https://doi.org/10.1108/00251740510626272 [ Links ]

Franks, J.R. & Torous, W.N., 1992, 'Lessons from a comparison of US and UK insolvency codes', Oxford Review of Economic Policy 8(3), 70-82. https://doi.org/10.1093/oxrep/8.3.70 [ Links ]

Goepel, K.D., 2013, 'Implementing the analytic hierarchy process as a standard method for multi-criteria decision making in corporate enterprises - A new AHP excel template with multiple inputs', in Proceedings of the International Symposium on the Analytic Hierarchy Process, Creative Decisions Foundation Kuala Lumpur, Kuala Lumpur, Malaysia, vol. 2, No. 10, pp. 1-10. [ Links ]

Goepel, K.D., 2017, AHP online system - BPMSG, viewed 06 September 2017, from https://bpmsg.com/academic/ahp.php. [ Links ]

Golden, B.L., Wasil, E.A. & Harker, P.T., 1989, 'The analytic hierarchy process', in B.L. Golden, E.A. Wasil, P.T. Harker (eds.), Applications and studies, p. 265, Springer Science & Business Media, Berlin. [ Links ]

Herrera-Viedma, E., Cabrerizo, F.J., Kacprzyk, J. & Pedrycz, W., 2014, 'A review of soft consensus models in a fuzzy environment', Information Fusion 17(1), 4-13. https://doi.org/10.1016/j.inffus.2013.04.002 [ Links ]

Jost, L., 2006, 'Entropy and diversity', Oikos 113(2), 363-375. https://doi.org/10.1111/j.2006.0030-1299.14714.x [ Links ]

Khorramshahgol, R. & Moustakis, V.S., 1988, 'Delphic hierarchy process (DHP): A methodology for priority setting derived from the Delphi method and analytical hierarchy process', European Journal of Operational Research 37(3), 347-354. https://doi.org/10.1016/0377-2217(88)90197-X [ Links ]

Lee, H., Kwak, W. & Han, I., 1995, 'Developing a business performance evaluation system: An analytical hierarchical model', Engineering Economist 40(4), 343-358. https://doi.org/10.1080/00137919508903159 [ Links ]

Levary, R.R. & Wan, K., 1999, 'An analytic hierarchy process based simulation model for entry mode decision regarding foreign direct investment', Omega 27(6), 661-677. https://doi.org/10.1016/S0305-0483(99)00032-8 [ Links ]

Linstone, H.A. & Turoff, M., 2002, The Delphi method: Techniques and applications, Addison-Wesley, Boston, MA. [ Links ]

Lohrke, F.T., Bedeian, A.G. & Palmer, T.B., 2004, 'The role of top management teams in formulating and implementing turnaround strategies: A review and research agenda', International Journal of Management Reviews 5(2), 63-90. https://doi.org/10.1111/j.1460-8545.2004.00097.x [ Links ]

Miller, G.A., 1956, 'The magical number seven, plus or minus two: Some limits on our capacity for processing information', Psychological Review 63(2), 81-97. https://doi.org/10.1037/h0043158 [ Links ]

Okoli, C. & Pawlowski, S.D., 2004, 'The Delphi method as a research tool: An example, design considerations and applications', Information & Management 42(1), 15-29. https://doi.org/10.1016/j.im.2003.11.002 [ Links ]

Okwir, S., Ulfvengren, P., Angelis, J., Ruiz, F. & Guerrero, Y.M.N., 2017, 'Managing turnaround performance through collaborative decision making', Journal of Air Transport Management 58(C), 183-196. https://doi.org/10.1016/j.jairtraman.2016.10.008 [ Links ]

Pandit, N.R., 2000, 'Some recommendations for improved research on corporate turnaround', M@n@gement 3(2), 31-56. [ Links ]

Park, C.-S. & Han, I., 2002, 'A case-based reasoning with the feature weights derived by analytic hierarchy process for bankruptcy prediction', Expert Systems with Applications 23(3), 255-264. https://doi.org/10.1016/S0957-4174(02)00045-3 [ Links ]

Pearce, J.A. & Robbins, K., 1993, 'Toward improved theory and research on business turnaround', Journal of Management 19(3), 613-636. https://doi.org/10.1177/014920639301900306 [ Links ]

Raviv, G., Shapira, A. & Fishbain, B., 2017, 'AHP-based analysis of the risk potential of safety incidents: Case study of cranes in the construction industry', Safety Science 91(C), 298-309. https://doi.org/10.1016/j.ssci.2016.08.027 [ Links ]

Saaty, T.L., 1990, 'How to make a decision: The analytic hierarchy process', European Journal of Operational Research 48(1), 9-26. https://doi.org/10.1016/0377-2217(90)90057-I [ Links ]

Saaty, T.L., 2008, 'Decision making with the analytic hierarchy process', International Journal of Services Sciences 1(1), 83-98. https://doi.org/10.1504/IJSSCI.2008.017590 [ Links ]

Saaty, T.L. & Vargas, L.G., 2012, Models, methods, concepts & applications of the analytic hierarchy process, Springer, Norwell, Massachusetts. [ Links ]

Smith, M. & Graves, C., 2005, 'Corporate turnaround and financial distress', Managerial Auditing Journal 20(3), 304-320. https://doi.org/10.1108/02686900510585627 [ Links ]

Trahms, C.A., Ndofor, H.A. & Sirmon, D.G., 2013, 'Organizational decline and turnaround a review and agenda for future research', Journal of Management 39(5), 1277-1307. https://doi.org/10.1177/0149206312471390 [ Links ]

Wong, J.K. & Li, H., 2008, 'Application of the analytic hierarchy process (AHP) in multi-criteria analysis of the selection of intelligent building systems', Building and Environment 43(1), 108-125. https://doi.org/10.1016/j.buildenv.2006.11.019 [ Links ]

Wu, Y., Gaunt, C. & Gray, S., 2010, 'A comparison of alternative bankruptcy prediction models', Journal of Contemporary Accounting & Economics 6(1), 34-45. https://doi.org/10.1016/j.jcae.2010.04.002 [ Links ]

Correspondence:

Correspondence:

Wesley Rosslyn-Smith

wesley.rosslyn-smith@up.ac.za

Received: 29 June 2022

Accepted: 19 Aug. 2022

Published: 27 Oct. 2022

1 . The word 'reorganisation' is occasionally used in a general sense to denote the rehabilitation of a distressed business, but it may also be used more narrowly to refer only to the process of rehabilitation under a formally recognised legal insolvency procedure, whose statutory titles may vary from administration, business rescue or reorganisation.

{kind=link}