Services on Demand

Article

English (pdf)

English (pdf)

Article in xml format

Article in xml format Article references

Article references

Indicators

Related links

-

Cited by Google

Cited by Google -

Similars in Google

Similars in Google

Share

Permalink

PermalinkSouthern African Journal of Entrepreneurship and Small Business Management

On-line version ISSN 2071-3185

Print version ISSN 2522-7343

SAJESBM vol.14 n.1 Cape Town 2022

http://dx.doi.org/10.4102/sajesbm.v14i1.563

ORIGINAL RESEARCH

The impact of the South African business environment on SMEs trade credit management effectiveness

Werner H. OttoI; Ilse BothaII; Gideon ElsII

IDepartment of Commercial Accounting, College of Business and Economics, University of Johannesburg, Johannesburg, South Africa

IIDepartment of Accounting, College of Business and Economics, University of Johannesburg, Johannesburg, South Africa

ABSTRACT

BACKGROUND: Given that the impact of the South African business environment on small and medium-sized enterprises' (SMEs) management of trade credit is largely unknown, this article argues that certain internal or external business environment variables could significantly impact SMEs' management of trade credit effectiveness, making it necessary to ask the impact of business environment in South Africa on SMEs' trade credit management effectiveness.

AIM: To determine the impact of internal (managerial competencies, collateral, financial and business information and networking) and external (legal system, ethics, macroeconomy and corruption) business environment variables on SMEs' management of trade credit effectiveness.

SETTING: This study was conducted by administering an online questionnaire..

METHOD: Quantitative research design with purposive sampling as the sampling method, administrated to 10 450 SMEs within South Africa

RESULTS: The results reveal several internal (5) and external (4) business environment factors significantly impacting SMEs' effectiveness in managing trade credit.

CONCLUSION: The article reveals how internal and external business environment factors contribute to increased SME effectiveness in managing trade credit and, in so doing, helps mitigate financial problems associated with SMEs' trade credit as a result of asymmetric information such as adverse selection, moral hazard and credit rationing, while also understanding the significance of corruption on SMEs' effectiveness in managing trade credit.

Keywords: trade credit; effectiveness; internal business environment; external business environment; management; small and medium-sized enterprises.

Introduction

South Africa suffers from high unemployment with an official unemployment rate of 35.3% (Statistics South Africa 2021). The sustainable development of small and medium-sized enterprises (SMEs) is widely regarded as a significant instrument to address the surging challenge of unemployment alongside other development challenges which are of pivotal importance to South Africa (Herrington & Kew 2018). The African Union Development Agency - New Partnership for Africa's Development (AUDA-NEPAD) supports this viewpoint (NEPAD 2008). Employment data for African countries provided in the 2017-2018 Global Entrepreneurship Monitor (GEM) Report alongside the 2017-2018 GEM South African Report reveal the critical importance of entrepreneurship in creating future employment, economic development and economic growth throughout Africa (Herrington & Kew 2018; Singer, Herrington & Menipaz 2018). These authors report that growing attention has focused on entrepreneurship as a solution in contributing towards Africa's economic growth and job creation, as the need for a sustainable SME sector is evident. On a global scale, SMEs are praised for contributing to approximately 80% of the global economic growth, while locally contributing close to 80% of gross domestic product in South Africa (Baker, Kumar & Singh 2019; Herrington & Kew 2018).

Despite the valuable contribution by SMEs in being instrumental in addressing key development challenges, the creation rate of new SMEs in South Africa is one of the lowest in the world, while the failure rate of SMEs is as concerning. The 2019-2020 GEM Report observed that South Africa had a fear of failure rate of 49.8%, ranking 9th out of 50 countries, positioning South Africa within the top 10 highest fear of failure rates for a participating country as part of the GEM survey (Bosma et al. 2020). In addition, the GEM Report, in which South Africa has participated since 2001, illustrates useful data in revealing the nature and extent of entrepreneurial activity in South Africa. South Africa's total early-stage entrepreneurial activity provided in the 2019-2020 GEM Report totalled 10.8%, a decrease from 11.0% as reported in the 2017-2018 GEM Report, positioning the county 25th out of 50 participating countries (Bosma et al. 2020; Herrington & Kew 2018). Therefore, from an entrepreneurial activity perspective, South Africa's performance is revealed to be mediocre yet alarming.

Furthermore, as far as can be established, limited research exists in relation to determining the impact of the South African business environment (internal and external variables) on SMEs' management of trade credit. Trade credit consists of both the time differential between the delivery of products and payment, including the cash discount allowed for earlier payment before due date (McGuinness, Hogan & Powell 2017). Trade credit is important to SMEs, as it regularly acts as the best and only available source of external funding for working capital needs, as SMEs' access to external debt from financial institutions is limited (Andrieu, Staglianò & Van Der Zwan 2018). This phenomenon is termed the 'finance gap' and is a major constraint to South African SMEs (Pretorius & Shaw 2004). Therefore, trade credit could be an important solution to SMEs becoming credit-rationed, emphasising the importance of applying effective trade credit management practices, particularly to those SMEs becoming credit-rationed (Stiglitz & Weiss 1981). The importance of managing trade creditors is essential in deciding upon a suitable credit provider, as SMEs should be responsible when deciding upon a suitable credit lender, because in the event of default, creditors can opt to siege the supply of products and inflate the trade credit contractual terms, disrupting operations until the default risk is mitigated (Cunat 2006). Because trade credit embodies a 'two-way transaction' in nature, apart from trade creditor financing, the importance of trade debtors should also be recognised (Martinez-Sola, Garcia-Teruel & Martinez-Solano 2013). Trade debtors, resulting an outstanding cash payment from credit sales, carry an element of default risk and should be carefully assessed when evaluating credit requests (Barad 2010). Therefore, the mismanagement of trade credit, creditor and debtor can lead to cash flow constraints impairing SMEs' ability to develop into sustainable enterprises, emphasising SMEs' responsibility to accomplish effective trade credit management because, if neglected, it could result in severe cash flow problems that contribute to SME failure rates (Padachi et al. 2008). According to the 2019-2020 GEM Report, unprofitability and financial problems are among the primary contributing reasons contributing to SME business failure (Bosma et al. 2020).

Furthermore, Bosma et al. (2020) reveal that entrepreneurs are subjected to several challenges while operating within the South African business environment. The volatility of the business environment raises SMEs' perceived risk according to the Organisation of Economic Cooperation and Development (OECD) (2020). Fluctuations within the business environment have a negative or positive effect on the growth or failure for majority-African SMEs (World Bank 2020), while the business environment places a direct influence on SMEs trade credit management implicating business sustainability. Small- and medium-sized enterprises do, however, operate within a business environment whereby trade credit management practices affect the availability of cash flow, as a positive cash flow cycle is instrumental to maintain survival and future enterprise growth (García-Teruel & Martinez-Solano 2007). Suggesting that effective trade credit management is paramount to SMEs, although the business environment in which these SMEs operate affects their sustainability, could also affect their working capital, specifically trade credit management. A need exists to determine the impact of the South African business environment on SMEs' management of trade credit.

The research aim and objective of this article is to determine the impact of selected factors of the South African business environment on SMEs' trade credit management.

Literature review

Literature reveals certain theories of trade credit use among businesses, as these theories form the basis for any enterprise to partake in trade credit financing (Huyghebaert 2006). These are asymmetric information, price discrimination, transaction costs, financing advantage, liquidity and private benefits of control. Asymmetric information theory occurs when a situation of uncertainty arises concerning the financial health and creditworthiness of the buyer (Smith 1987). According to Smith (1987), the acceptance of high trade credit interest rates, defined by generally accepted trade credit terms, acts as a displaying mechanism portraying credit borrowers' default risk information asymmetrically. In case of trade credit, such information is highly valuable to creditors in protecting their investment in trade debtors or to forecast the possibility of default by debtors making the original investment nonsalvageable (Smith 1987). Trade credit regularly acts as an effective price cut mechanism (price discrimination theory), as a creditor, exploiting their market power, can manipulate product prices through credit terms variations offered to a debtor. In doing so, in an attempt to maximise sales when operating in a competitive environment, through effective price discrimination, trade credit is more likely to be offered the greater returns obtained from the offering through variation in the credit terms as a benefit to be exploited by creditors (Brennan, Maksimovic & Zechner 1988). Ferris (1981) indicated that trade credit can be effortlessly conceptualised as an instrument to facilitating the exchange of products given that trade credit can be used as a contractual alternative to immediate money utilisation. Therefore, trade credit becomes an alternative funding source to cash by alleviating transaction cost (transaction cost theory); however, trade credit does impose increased enforcement and information costs that must be reconciled against transactional cost savings achieved in the exchange of products and/or services (Ferris 1981). Due to the financing motive, SMEs are poised to extend credit to credit-restricted SME by providing a favourable environment to credit rationed or non-financially viable SMEs, enabling creditors to benefit from a cost advantage over standard financiers (Schwartz 1974). The liquidity theory suggests that credit-constrained SMEs are far more likely to utilise trade credit compared to larger businesses normally better positioned to acquire credit from financiers (Bhattacharya 2008). Small and medium-sized enterprises that are credit-rationed require even more trade credit from larger businesses and contribute increasingly more to the 'finance gap' that becomes a major obstacle to entrepreneurial development and growth (Herrington & Kew 2018). Private benefits of control advocate that creditors adopt a more lenient liquidation policy towards distressed SMEs by expanding the amount of credit offered to debtors during distress periods, thereby benefitting creditors by exploiting their private control benefits (Huyghebaert, Van De Gucht & Van Hulle 2001).

The business environment variables reviewed and examined in this article as identified by exploratory factor analysis (EFA) are managerial competencies (MC), collateral, financial and business information and networking (internal), including legal system, ethics, macroeconomy and corruption (external).

Internal business environment

A management team consisting of innovative capabilities is strongly associated with expanding organisational growth (Malinao & Ebi 2022). The study by Veliu and Manxhari (2017) supports this viewpoint, observing the lack of managerial capabilities as the main contributing reasons why businesses fail. The importance of education and training to new venture success is critical and especially relevant in the case of South Africa suffering from educational system inequalities (Bosma et al. 2020). Furthermore, the study by Malinao and Ebi (2022) observed a positive correlation between relative new venture profits and greater levels of education and experience possessed by the business. Therefore, it could become essential for credit managers to possess the needed managerial capabilities to manage trade credit effectively. In addition, should SMEs fail to meet stipulated lending criteria, it becomes mandatory to provide security as collateral during credit evaluation by trade creditors (Gassiah & Kikula 2022). Creditors portray a higher level of commitment and assurance with the extension of credit when collateral is available. Collateral solves problems derived from information asymmetric in valuation of projects, uncertainties pertaining to project sustainability and debtors' credit risk (Blumberg & Letterie 2008). Should debtors not commit to credit repayment, it is only when collateral requirements are enforced that such inducements are eliminated (Barbosa & Moraes 2004). Therefore, imposed collateral requirements, such as the frequency with which creditors guarantee collateral, including the stipulation of collateral requirements by creditors, could influence SMEs' trade credit management. In addition, inadequate financial and business information results in information asymmetry for SMEs, while on the contrary, availability of concrete financial and business information helps in reducing information asymmetry (Nguyen, Tran & Truong 2022). Vander Bauwhede, De Meyere and Van Cauwenberge (2015) found a direct link between the perceptions of the credit manager related to accounting information quality yielding an increase in lending volumes for audited firms. Therefore, the provision of concrete financial and business information leads to a reduction in asymmetric information problems as creditors feel more secure while simultaneously resulting in lessoning the effect of credit rationing mitigating the effects of a growing SME 'finance gap' (Vander Bauwhede et al. 2015). Small and medium-sized enterprises also need to account for networking while managing trade credit given that, due to the absence of efficient market institutions, networking plays an important role in transcending institutional knowledge detailing business practices (Ngoc, Le & Nguyen 2009). Networking can benefit SMEs in learning appropriate behaviour by acquiring needed support from specialised stakeholders towards effective trade credit management (Amoako & Matlay 2015). Networking brings about numerous entrepreneurial opportunities by allowing the creditor access to vital resources benefitting the credit lenders screening ability by sourcing valuable information pertaining to debtors' reputation disclosing their business legitimacy in alerting the creditor to possible default risks (El Ghoul & Zheng 2016).

External business environment

From a legal system perspective, the majority of business insolvencies results in liquidations amplifying the importance of creditor protection, especially given the relevance thereof to SMEs' trade credit management within the South African business environment (Atradius 2021). Trade creditors need to have their rights protected, as failure to do so would impair the creditors' operational capability, given that without properly enforced creditor rights, debtors would have little to no reason to commit to overdue payments. Therefore, the importance of an effective legal system in protecting creditor rights towards effective SMEs' trade credit management must be emphasised (Palacin-Sánchez, Canto-Cuevas & Di-Pietro 2019). The recovery of uncollected debt from insolvent business estates remains challenging for secured creditors due to procedural delays including relatively high enforcement process legal fees. The incapability of the South African legal system contributes to creditors being unprotected in resolving outstanding debt in the event of business insolvency, as the efficiency of contract enforcement in South Africa is utterly low (Fatoki 2010). Given the dependency of SMEs on trade credit while exposed to several internal and external variables in the South African business environment, as explained earlier, it is no surprise that SMEs fail on such a large scale, which requires investigation. The 2017-2018 GEM South African Report lists unprofitability and financial problems as major reasons for SME failure (Singer et al. 2018). In addition, from an ethical perspective, the viability of a credit agreement set out between creditor and debtor amplifies ethical business practices to mitigate possibilities of dishonesty among SMEs. Small and medium-sized enterprises' single most unethical practice is dishonesty in developing a credit agreement and not keeping to the policies stipulated in such credit agreement (Amoako, Akwei & Damoah 2020). Late payment results because of a lapse in business ethics, complemented by the actions of dishonesty, while the most effective procedure to mitigate late payments realities because of a lapse in business ethics is the reduction of financial advantages applicable to granting trade credit (Chittenden & Bragg 2012). However, given that SMEs' credit interdependency as trade credit embodies a 'two-way transaction', the implementation of such sanctions often impedes the sustainability of the credit lending SME. Therefore, SMEs' unethical behaviour influences the risk perception of the creditor in the extent to which the debtor can be trusted, thereby constraining the operational viability of SMEs. Because of this, SMEs' trade credit management should be directly affected because of the late payment risks associated with a lapse in ethics, implicating business sustainability. Furthermore, SMEs should also consider macroeconomic fluctuations such an economic downturns because of coronavirus disease 2019 (COVID-19), whereby business operations are severely impaired, leaving SMEs exposed to negative debt leverage (Lui 2020). According to Barbosa and Moraes (2004), a positive association exists between inflation and business financial leverage, as corporate debt positions of businesses were highest in high inflationary periods and lowest in low inflationary periods. Favourable macroeconomic conditions (MECs) or positive leverage is beneficial to SMEs' financial viability and may contribute to effective trade credit management. Conversely, negative leverage is a result from a depressed economy, exposing SMEs to difficult MECs, resulting in unfavourable business conditions such as sales and profit margin decreases. Adding to this, the effect of an economic downturn usually brings about an increase in SMEs' financial risk, as the enterprise becomes more vulnerable to severe cash flow constraints, thereby constraining the repayment ability from debtor to creditor (Coleman & Cohn 2000). Small and medium-sized enterprises are surrounded by numerous business environmental constraints, although because of corruption, SMEs are more exposed to economic policy adaptations (Rashid & Saeed 2017). Existing literature distinguishes between two stands regarding the presence of corruption in SMEs, namely 'grease in the wheels' and 'sand in the wheels' as a result of SME corruption, imposing several implications to SMEs' financial fragility (Le & Doan 2020; Ullah 2020). The latter strand mentioned resembles the devastation caused by corruption, as it affects the operational capacity of business because of a surge in financing constraints, undermining the practice of good corporate governance, and it hinders the possibility of securing investment for innovative business proposals (Le & Doan 2020; Ullah 2020). Therefore, the article is aligned to the 'sand-in-the-wheels' strand when considering the numerous negative implications of corruptions on SMEs' business operations that include trade credit management. Corruption creates uncertainty among credit lenders to enforce their claims against defaulting debtors, as it ultimately obstructs the preparedness of the creditor and will of creditor to grant loans or extend credit. However unfortunate, SMEs are subjected to corruption as the decision not to partake in corrupt activities could severely constrain SMEs' cash flow, affecting their management of trade credit. Therefore, it seems necessary to determine the impact of corruption and related variables on SMEs' management of trade credit.

Research method

The article applied a quantitative research design. The researcher focused on SMEs (trade debtors and creditors) that operate within the following industries: distribution, engineering, financial services, government, information and communication technology (ICT), manufacturing, mining, professional services and retail. The population frame of SMEs was obtained from Interactive Direct through the services of iFeedback Consulting (Pty) Ltd. The population of SMEs operating within the aforementioned industries totalled 10 450. All SME names were crosschecked to eliminate double counting. Using the Zikmund sample size calculator at 5% margin of error and 95% confidence interval (Zikmund et al. 2010), the actual sample size for SMEs totalled 450 with 10 450 questionnaires (please refer to Online Appendix 1) distributed to SMEs and 434 completed questionnaires returned, making the response rate 4.15% of the total population. From the 434 questionnaires, 422 respondents completed between 70.41% and 100% of the questionnaire, and the remaining 12 respondents answered between 0% and 69.39%. The researcher decided to accept the 422 questionnaires presenting a completion rate between 70.41% and 100% and reject the remaining 12 questionnaires falling within the category of 0% - 69.39% rate of completion. In commencement with the research results, missing values presented a small challenge given that the low number of item nonresponse cases was evident. In total, the sample size for the purpose of statistical analysis equalled 422 responses; however, from the 422 responses, the number of item nonresponse cases might still vary because of missing data evident within the sample. The following steps were followed to reduce nonresponse cases - firstly, sensibly applying the needed care in designing and reworking the questionnaire from that used in a previous study; secondly, extensively checking the questionnaire, including the e-mail text and letter to respondents, for any sensitive text or questions and removing such items where applicable; and lastly, sending reminder e-mails to all respondents.

The survey research method was employed and data were collected through an online questionnaire (please refer to Online Appendix 1) via e-mail. Five- and six-point Likert scale questions were used across all questionnaire questions, excluding demographic questions. Given that no business is identical, for some question sets, the option of not applicable (N/A) was relevant and justified the use of six-point Likert-scale questions aimed to test SMEs' management of trade credit. The measuring instrument was designed to measure the internal and external business environment variables' impact on SMEs' management of trade credit effectiveness. For this purpose, a 49-item questionnaire (testing SMEs' business environment) and a 35-item questionnaire (testing SMEs' trade credit management) were designed, which constitute the two main questionnaire sections apart from the initial demographic section (please refer to Online Appendix 1). Between 4 and 8 items (statements) per variable were used to test SMEs' business environment, and between 4 and 20 items (statements) were used to test SMEs' trade credit management, with each variable not having an exact similar number of items. Items were obtained from a combination of studying the literature for theoretical constructs and empirical conclusions, reworking the questionnaire based on a questionnaire used in a previous study and help from experienced statisticians who set out to peer debrief the questionnaire statements. Exploratory factor analysis was applied for computing the underlying structure for large data sets. In case of EFA, the following steps were applied as supported by Pallant (2016). All variables were subjected to EFA. Eigenvalues greater than 1.00 were retained, and variables with factor loadings less than 0.300 were removed. In order to measure sampling adequacy, Bartlett's test of sphericity (BTS) and the Kaiser-Meyer-Olkin (KMO) are tests that can be applied to measure sampling adequacy (Pallant 2016). Section A of the questionnaire collected the demographical response data.

Summary statistics to justify factor analysis

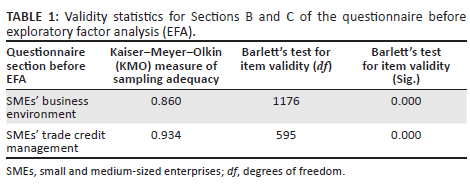

Table 1 indicates the relevant validity statistics for the two main sections of the questionnaire (please refer to Online Appendix 1, Section B and Section C) namely, SMEs' business environment variables and SMEs' trade credit management variables before EFA.

Reliability statistics for factors derived after exploratory factor analysis

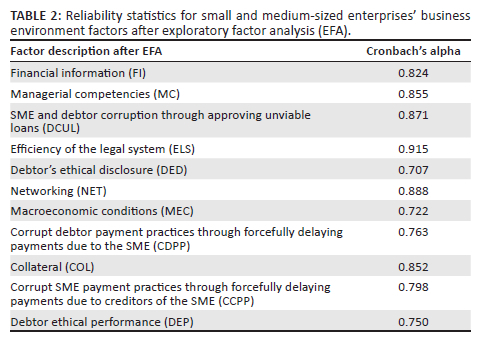

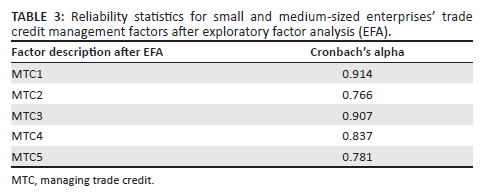

Table 2 provides the Cronbach's alpha for SMEs' internal and external business environmental factors after EFA. Table 3 does the same for SMEs' trade credit management factors after EFA.

Data were analysed using SPSS 26, employing statistical techniques such as descriptive statistics, frequency distribution, mean, standard deviation, internal consistency, factor analyses, correlations and comparisons and regression analyses. A p-value of 0.05 is considered significant for statistical tests unless otherwise stated.

Ethical considerations

All participating respondents gave their consent to complete the questionnaire. All respondents were properly informed as to the completion of the questionnaire being completely voluntary, while any and all information supplied by respondents alongside the identity of each respondent were treated as strictly confidential. The summary of all data collected will be reported on as a whole, as the researcher was restrained from reporting particulars for any individual respondent response. The researcher also encouraged sharing a summary of the research results with any respondent wishing to obtain such report. Required information relating to the study title and the purpose of the study was disclosed, along with the needed credentials for both the researcher and the supervisor that included the researcher's contact details. The researcher followed and completed the required ethical clearance process stipulated by the University of Johannesburg. Ethical clearance was obtained from the School of Accountancy Research Ethics Committee (reference number: SAREC20180502-02).

Results

The empirical results provided set out to determine the impact of the internal and external business environment on SMEs' effectiveness in managing trade credit.

Correlation and regression analysis

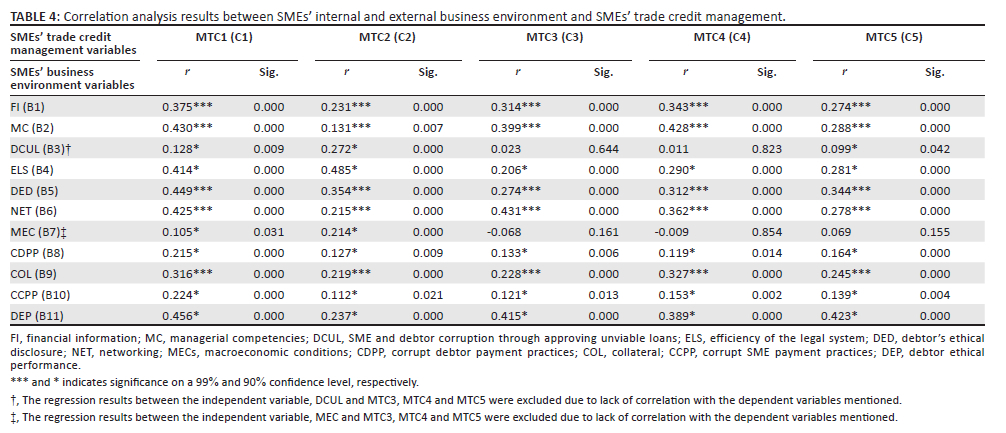

Table 4 tabulates the correlation analysis result between SMEs' internal and external business environment factors and SMEs' trade credit management factors, followed by the results of the five multiple regression models (Table 5).

Outline of results

The article sought to determine the impact of SMEs' internal and external business environment on SMEs' effectiveness in managing trade credit.

All necessary contact information was obtained from the representative sample (number of distributed questionnaires) (please refer to Online Appendix 1) via e-mail totalled 10 450, although the number of completed questionnaires (actual sample size) totalled n = 434 based on the database population received from iFeedback Consulting (Pty) Ltd. In continuing from the previous point, a letter was sent out to each SME detailing the title of the research project, a short introduction of the researcher, the time required to complete the questionnaire and the assurance that the completion of the questionnaire was voluntary, alongside the needed ethical practices disclosure. The electronic link to the completion of the online questionnaire was also available on the letter sent to respondents who opened the electronic link to the online questionnaire and completed the questionnaire. Repeated reminder e-mails, restricted to a maximum of three per respondent, were sent to respondents to attain questionnaire completion. Software used in administering the questionnaire were Typeform.com, as administered by the services of iFeedback Consulting (Pty) Ltd. After completion, the data for each questionnaire were saved for analysis. The researcher followed and completed the required ethical clearance process stipulated by a public university in the north-eastern region of South Africa.

Validity and reliability statistics for Sections B and C of the questionnaire

Table 1 depicts the results obtained after performing the KMO and BTS tests. For Section B, BTS was at 1176 (p = 0.000), and for Section C, BTS was at 595 (p = 0.000); therefore, the data were appropriate to perform a factor analysis. The result of the KMO measure of sampling adequacy was 0.860 (Section B) and 0.934 (Section C), indicating sufficient items for each factor. Although a pilot study was not conducted prior to main data collection, both tests support the appropriateness of the factor analysis technique given that the results from the KMO was very high and statistically significant indicating high validity for both questionnaire sections (please refer to Online Appendix 1, Section B and Section C). Table 2 indicates that Cronbach's alpha is very close to 1 for all 11 SMEs' business environmental factors after EFA, indicating that most of the factors are highly reliable, due to the very high internal consistency, ranging between 0.80 and 0.90 for six out of the 11 factors in total. Table 3 indicates that Cronbach's alpha is very close to 1 for all five SMEs' trade credit management factors after EFA, indicating that most of the factors are highly reliable, due to the very high internal consistency, ranging between 0.80 and 0.90 for three out of the five factors in total.

Factor analysis and total variance explained

Exploratory factor analysis was performed on the final 422 questionnaires (please refer to Online Appendix 1) returned by SMEs in the main survey to test the homogeneity of the underlying constructs. Exploratory factor analysis of the responses allowed for construct validity using Cronbach's alpha in order to analyse the 49 Section B and 35 Section C questionnaire components (please refer to Online Appendix 1, Section B and Section C). A principal component analysis extraction method was used with Oblimin rotation to reduce the data to a manageable number of factors for further analysis, amounting to 38 components (Section B: 11 items with loadings < 0.300 that were excluded) and 25 components (Section C: 10 items with loadings < 0.300 that were excluded). Section B's extracted components confirmed 11 SMEs' business environment factors, as labelled next: financial information (FI), MC, SME and debtor corruption through approving unviable loans (DCUL), efficiency of the legal system (ELS), debtor's ethical disclosure of accurate and transparent financial and business information (DED), networking (NET), MEC, corrupt debtor payment practices through forcefully delaying payments due to the SME (CDPP), collateral (COL), corrupt SME payment practices through forcefully delaying payments due to creditors of the SME (CCPP) and SME and debtor ethical performance (DEP). Section C's extracted components were labelled according to the following five factors: SMEs' effectiveness in providing trade credit management activities (MTC1), mechanism and insurance to assist with the collection of or protection against the risk of outstanding debt (MTC2), SMEs' effectiveness in managing trade credit management principles (MTC3), SMEs' effectiveness in managing trade credit management aspects (MTC4) and SMEs' effectiveness in applying credit policy components when granting credit (MTC5). For a detailed description of the EFA, refer to author.

According to the rules of factor analysis, only factors that have eigenvalues greater than one should be retained. The initial eigenvalues for questionnaire Sections B and C cumulative percentage were 70.374% and 65.824%, respectively.

Correlation analysis results

The main study objective was to analyse the impact of SMEs' internal and external business environment factors on SMEs' trade credit management factors. Therefore, correlation analysis and multiple regression analysis were applied. The Pearson correlation (Table 4) was used to test for the direction and strength of the relationship between SMEs' internal and external business environmental variables and SMEs' trade credit management variables. The p-values for each variable were compared against a significance level of 0.05. If the p-value is < 0.05, a significant relationship exists between the particular variable and SMEs' management of trade credit. In Table 4, internal variables discussed first, FI displays a weak to moderate significant positive correlation with all SMEs' trade credit management factors, followed by MC displaying a weak to moderate significant positive correlation with all SMEs' trade credit management factors. Similarly, results from Table 4 show that DED shows a significant positive correlation, ranging between weak and moderate, with all SMEs' trade credit management factors. In addition, results from Table 4 show that NET obtained a weak to moderate significant positive correlation with all SMEs' trade credit management factors. Similarly, COL shows a weak to moderate significant positive correlation with all SMEs' trade credit management factors. Related to the external variables (Table 4), DCUL displays a weak significant positive correlation with three computed SMEs' trade credit management factors. In addition, ELS display a significant positive correlation, ranging between weak and moderate, with all SMEs' trade credit management factors. Also provided in Table 4, MEC obtained a weak significant positive correlation with two computed SMEs' trade credit management factors; for the remaining two corruption factors (CDPP and CCPP), both factors display significant weak positive correlations with all SMEs' trade credit management factors. Lastly, a weak to moderate significant positive correlation was found between DEP and all SMEs' trade credit management factors.

Multiple regression analysis results

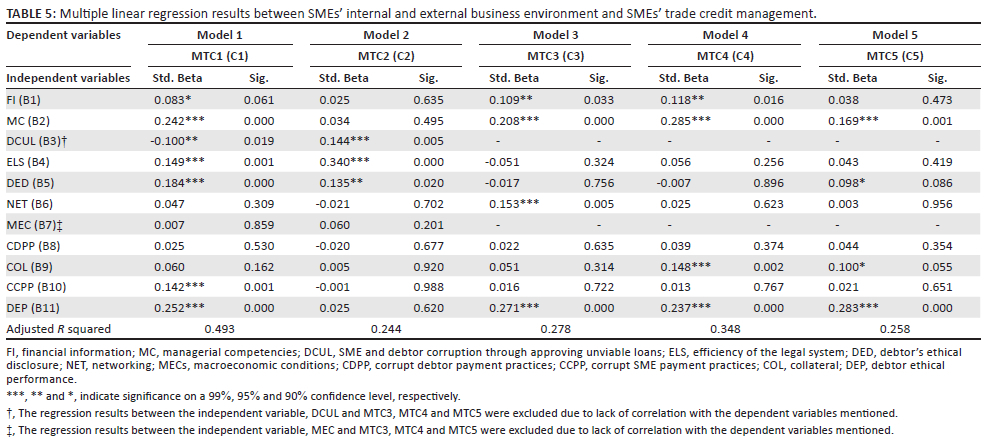

Regression analysis (Table 5) is used to test the significant effect of one variable on another variable (Scott 1997). The linear regression equation denotes that one variable(s) is a dependent variable (Y), with the other variable(s) being an independent (X) variable. Linear regression analyses were used to determine the significant impact between SMEs' internal and external business environment factors with corresponding SMEs' trade credit management factors. Table 5 results indicate that the following internal variables significantly impact on MTC1, MC (β = 0.242, sig. 0.000) followed by DED (β = 0.184, sig. 0.000) and FI (β = 0.083, sig. 0.061). The following external variables significantly impact on MTC1, DEP (β = 0.252, sig. 0.000), ELS (β = 0.149, sig. 0.001), CCPP (β = 0.142, sig. 0.001) and DCUL (β = −0.100, sig. 0.019). The results indicate that one internal and two external variables significantly impact on MTC2, provided from highest to the lowest significant impact, ELS (β = 0.340, sig. 0.000), DCUL (β = 0.144, sig. 0.005) and DED (β = 0.135, sig. 0.020). In addition, Table 5 results show that MC (β = 0.208, sig. 0.000), NET (β = 0.153, sig. 0.005) and FI (β = 0.109, sig. 0.033), all internal variables and DEP (β = 0.271, sig. 0.000), external variable, significantly impact on MTC3. Furthermore, three internal variables and one external variable significantly impact on MTC4, namely MC (β = 0.285, sig. 0.000), COL (β = 0.148, sig. 0.002), FI (β = 0.118, sig. 0.016) and DEP (β = 0.237, sig. 0.000), respectively. Lastly, three internal variables and one external variable significantly impact on MTC5, namely MC (β = 0.169, sig. 0.001), COL (β = 0.100, sig. 0.055), DED (β = 0.098, sig. 0.086) and DEP (β = 0.283, sig. 0.000), respectively (Table 5).

Discussion of results

Internal business environment factors significantly impacting small and medium-sized enterprises' effectiveness in managing trade credit

The results reveal the importance of FI to SMEs' management of trade credit effectiveness, which helps to mitigate SMEs' FI supply gap (Palazuelos, Crespo & Del Corte 2018; Vander Bauwhede et al. 2015). Information asymmetry is the cause of financial problems for SMEs, while the availability of concrete FI reduces information asymmetry (Nguyen et al. 2022). Therefore, the article results reveal that for creditors, a decrease in asymmetric information received from debtors is of pivotal importance towards increasing SMEs' effectiveness in managing trade credit, as FI provision would equip creditors to make informed trade credit supply decisions, positively impacting SMEs' management of trade credit. In addition, this mitigation of information asymmetry can positively affect trade credit availability, alleviating SME constraints related to credit rationing (Padachi et al. 2008). Moreover, because of this decrease in asymmetric information received from SME debtors, SMEs should benefit from the formation of a credit agreement by which the creditor can exploit the undeserved cash discount related to the market power theory of trade credit (Frank & Maksimovic 2003). In relation to MC significantly impacting SMEs' management of trade credit effectiveness, the results illustrate the importance of having managerial competent trade credit managers improving education and experience improving problem solving, communication and business skills in order to improve SMEs' effectiveness in managing trade credit. The results are in line with literature observing the importance of MC for business performance in order to mitigate business failure (Malinao & Ebi 2022; Veliu & Manxhari 2017). In support of this, the 2017-2018 GEM South Africa Report observes that the increase in entrepreneurial activity is stifled due to the country's poor school educational system (Herrington & Kew 2018). Furthermore, the results reveal the significance of DED on SMEs' effectiveness in managing trade credit, which are in line with the findings by Vander Bauwhede et al. (2015) and Palazuelos et al. (2018), observing the importance of providing accurate and transparent financial and business information in mitigating information asymmetries and increasing lending volumes (credit rationing theory). In relation to NET significantly impacting SMEs' management of trade credit, several authors point out that it is because of the formation of networks that resources become more accessible between credit lender and borrower. In view hereof, the results are consistent with the findings by Song, Yang and Yu (2020), given that networking contributes to a more secure climate for trade credit supply, as because of increased information, through reduced information asymmetries, accessibility is improved. To this end, SMEs' access to trade credit should become less restricted, improving the redistribution of trade credit as a result of networking between credit lender and borrower. Also, Petersen and Rajan (1997) indicated the importance of networking in diminishing creditor-debtor costs as a mutual benefit comes into existence should SMEs do business in closely linked networks to lower combined trade credit transaction costs (transaction cost theory), thereby in line with the study results as lowered transaction costs contribute to SMEs' effectiveness in managing trade credit. In case of COL, the results are in line with the findings by Gassiah and Kikula (2022) related to the asymmetric information theory, including the findings by Voordeckers and Steijvers (2006) and Cole, Cowling and Liu (2022) related to the redistribution theory of trade credit. This holds true as an increase in COL could lower the debtors' default risk (asymmetric information theory), as SMEs would be more effective in managing trade credit management aspects and applying credit policy components, which, once attained, could reduce the likelihood of having to provide additional security as collateral. Those SMEs once labelled as probable to default risk can now utilise COL as a signalling mechanism to minimise information asymmetries, including mitigating adverse selection risks. This in turn would improve SME management of trade credit while expanding SMEs' potential for trade credit redistribution as a spinoff benefit from supplying adequate COL.

External business environment factors significantly impacting small and medium-sized enterprises' effectiveness in managing trade credit

The results reveal that DEP significantly positively impacts SME management of trade credit effectiveness, thereby revealing the importance of implementing an ethical business practice of nondefault to payments payable in respect to SME to creditor and debtor to SME. Therefore, it can be observed that the relationship between creditor and debtor is delicate and largely dependent on ethics, given that ethical performance, supported by an ethical code of conduct which includes honesty and trust, is instrumental to SMEs' management of trade credit effectiveness. The findings of Ibeh, Wilson and Chizema (2012) and Amoako et al. (2020) support this result. The result is of further value for SMEs to attain effective trade credit management, as ethics play a pivotal role in any business environment in order to reduce agency problems such as asymmetric information, as supported by Stiglitz and Weiss (1981) and Howorth and Moro (2006). In addition, these authors observed that asymmetric information, adverse selection and moral hazard problems can affect the availability of credit (credit rationing theory), while ethics is important to reduce monitoring and screening costs (transaction cost theory), making DEP, as observed from the results, profoundly important towards SMEs' effectiveness in managing trade credit. The results show that corruption (see DCUL and CCPP in Table 5) significantly positively impacts SMEs' management of trade credit effectiveness, which is consistent with the findings by Wellalage and Thrikawala (2021), resembling that businesses do in fact benefit from corrupt practices in developing countries weakened by a defective government, such as South Africa. Although the article result is of great value in revealing the act of corruption on both SMEs and SME debtor's trade credit management, it is unfortunate that the article results align with the 'grease-in-the-wheels' perspective, as supported by Wellalage, Locke and Samujh (2019a) and Wellalage, Locke and Samujh (2019b). In rationalising this finding, SMEs and SME debtors are therefore willing to partake in corruption as they benefit from a form of joint alliance resulting in mutual benefit, which therefore becomes acts of corruption whereby SME and SME debtors' trade credit management improves because of their willingness to partake in corruption. However, results from Model 1 reveal that DCUL significantly negatively impacts SMEs' effectiveness in managing trade credit specific to MTC1. Compared to the previous finding, this result is more expected and aligns with the 'sand-in-the-wheels' perspective by Gbetnkom (2012) and Le and Doan (2020), who proclaim that corrupt practices such as bribery are detrimental to all businesses, especially to SMEs, as they hamper SME development, resulting in corporate financial fragility. Furthermore, the results reveal that a more efficient legal system (see ELS in Table 5) will enable SMEs to be better protected against cash flow shortages associated with the risks of outstanding debt while becoming more effective in providing trade credit management activities, improving SMEs' trade credit management effectiveness and financial viability. The findings of Palacin-Sánchez et al. (2019) support the results. This study finding is of further value to SMEs' effectiveness in managing trade credit, as, firstly, information asymmetric costs incurred in relation to product quality will increase for those SMEs operating in countries categorised by less efficient legal systems and vice versa (quality guarantee theory). Secondly, debtors are prone to exercise market power to mitigate asymmetric information problems, especially in countries categorised by less efficient legal systems and vice versa (Van Horen 2007), which holds a credit risk for SMEs, as a surge debtor surplus (as a result of exploiting market power) expands the degree of asymmetric information between credit and debtor (market power theory).

Results from the multiple regression analysis indicated that several SME business environment factors have a direct, positive, statistically significant relationship with SMEs' effectiveness in managing trade credit, while one external (DEP) and one internal (MC) factor repeatedly ranked either as having the biggest or second-biggest significant impact on SMEs' effectiveness in managing trade credit. However, DCUL obtained a direct negative statistically significant relationship with SMEs' management of trade credit.

Recommendation

Given that several internal and external business environment factors significantly impact on SMEs' effectiveness in managing trade credit, it is recommended that the South African government approve legislation detailing the provision of standardised financial information for SMEs that enforce all SME debtors to provide transparent, accurate and truthful financial information. In view of this, the South African Institute of Charted Accountants (SAICA) should work closely with government in providing knowledge to develop the required FI standard. In addition, public and private sector institutions should contribute to upskill SMEs' managerial capabilities by funding regular training sessions. To attain this, local government should institute policy for government-funded tertiary level educational institutions to redevelop curricula to teach managerial competency disciplines. It is also recommended that local government should change SMEs' tax legislation, thereby providing a tax rebate to all SMEs involved in building networking relations. Furthermore, local government must construct and implement a legal framework policy, creating courts specialising in SME insolvencies that would decrease the time to obtain judgement against defaulting SMEs, including the employment of more judges. It is also recommended that the nonprofit and public sector organisations create awareness around the devastation caused by acts of SME corruption, including the seriousness of corruption from a prosecution perspective. Channels to report corruption must be accessible for SMEs, and nonprofit organisations must take charge by directing awareness to this end to SMEs on a national level. All anticorruption organisations must uphold their mandate to eradicate public and private sector corruption by broadening existing policies to include the investigation of SMEs and SME debtor corruption relating to improving effectiveness in managing trade credit. Lastly, local government should sanction a policy necessitating all SME funding applications to include proof of documentation pertaining to SMEs' ethical business practices.

Conclusion

For the purpose of this article, the impact of the South African business environment on SMEs' management of trade credit was attained.

The results indicate that all five internal business environment factors significantly impact SMEs' trade credit management. The results indicate significant positive beta coefficients between MC and MTC1, MTC3, MTC4 and MTC5. In addition, the results indicate significant positive beta coefficients between FI and MTC1, MTC3 and MTC4. Debtor's ethical disclosure significantly impacts MTC1, MTC2 and MTC5. Networking significantly impacts MTC3. Lastly, COL significantly impacts MTC4 and MTC5. Furthermore, the results indicate that four external business environment factors significantly impact SMEs' trade credit management. The results indicate significant positive beta coefficients between DEP and MTC1, MTC3, MTC4 and MTC5. Therefore, ELS significantly impacts MTC1 and MTC2. For corruption, firstly, DCUL significantly impacts MTC1 and MTC2. Secondly, CCPP significantly impacts MTC1.

The practical value of the article is in the understanding that specific internal and external business environment factors contribute to increased SME effectiveness in managing trade credit. By determining the impact between the relevant independent and dependent variables, the article broadens the understanding of the association between internal and external business environment factors and SMEs' management of trade credit. In doing so, the research can contribute to the mitigation of financial problems associated with SMEs' trade credit as a result of asymmetric information such as adverse selection, moral hazard and credit rationing while also understanding the significance of corruption on SMEs' management of trade credit.

Limitations

The article focuses only on trade credit management as a funding source. A dynamic survey to examine the impact of the business environment on the management of debt and equity (total capital) as perceived by SMEs could help to further confirm the findings of this article.

Acknowledgements

The authors acknowledge all anonymous reviewers for comments that greatly improved the manuscript.

Competing interests

The authors declare that they have no financial or personal relationships that may have inappropriately influenced them in writing this article.

Authors' contributions

W.H.O. is the main author of this study. I.B. is the main supervisor, providing supervising guidance to the study. G.E. is the co-supervisor, providing additional supervising guidance to the study.

Funding information

This research received no specific grant from any funding agency in the public, commercial or not-for-profit sectors.

Data availability

The authors confirm that the data supporting the findings of this research project are available within the article.

Disclaimer

The views and opinions expressed in this article are those of the authors and do not necessarily reflect the official policy or position of any affiliated agency of the authors.

References

Amoako, I.O., Akwei, C. & Damoah, I., 2020, 'We know their house, family and workplace: Trust in entrepreneurs' trade credit relationships in weak institutions', Journal of Small Business Management 59(6), 1-30. https://doi.org/10.1111/jsbm.12488 [ Links ]

Amoako, I.O. & Matlay, H., 2015, 'Norms and trust-shaping relationships among food-exporting SMEs in Ghana', International Journal of Entrepreneurship & Innovation 16(2), 123-124. https://doi.org/10.5367/ijei.2015.0182 [ Links ]

Andrieu, G., Staglianò, R. & Van Der Zwan, P., 2018, 'Bank debt and trade credit for SMEs in Europe: Firm-, industry-, and country-level determinates', Small Business Economics 51, 245-264. https://doi.org/10.1007/s11187-017-9926-y [ Links ]

Atradius, 2021, International debt collections handbook: Atradius Debt Collection Report, October 2021, viewed 23 November 2021, from https://group.atradius.com/publications/global-international-debt-collections-handbook.html [ Links ]

Baker, H.K., Kumar, S. & Singh, H.P., 2019, 'Working capital management: Evidence from Indian SMEs', Small Enterprise Research 26(2), 143-163. https://doi.org/10.1080/13215906.2019.1624386 [ Links ]

Barad, M.M., 2010, 'A study on liquidity management of Indian steel industry', PhD thesis, Saurashtra University, Rajkot, viewed 27 September 2016, from http://etheses.saurashtrauniversity.edu/id/eprint/77. [ Links ]

Barbosa, E.G. & Moraes, C.C., 2004, Determinants of the firm's capital structure: The case of the very small enterprises, viewed 08 April 2015, from http://econpa.wustl.edu.8089/eps/fin/papers0302/0302001.pdf. [ Links ]

Bhattacharya, H., 2008, Theories of trade credit: Limitations and applications, viewed 11 June 2018, from https://papers.ssrn.com/sol3/papers.cfm?abstract_id=1286443. [ Links ]

Blumberg, B.F. & Letterie, W.A., 2008, 'Business starters and credit rationing in small business', Small Business Economics 3(1), 187-200. https://doi.org/10.1007/s11187-006-9030-1 [ Links ]

Bosma, N., Hill, S., Ionescu-Somers, A., Kelley, D., Levie, J. & Tarnawa, A., 2020, Global entrepreneurship monitor report, viewed 28 March 2020, from https://www.gemconsortium.org/file/open?fileId=50443. [ Links ]

Brennan, M., Maksimovic, V. & Zechner, J., 1988, 'Vendor financing', Journal of Finance 43(5), 1127-1141. https://doi.org/10.1111/j.1540-6261.1988.tb03960.x [ Links ]

Chittenden, F. & Bragg, R., 2012, 'Trade credit, cash flow and SMEs in the UK, Germany and France', International Small Business Journal 16(1), 22-35. https://doi.org/10.1177/0266242697161002 [ Links ]

Cole, R., Cowling, M. & Liu, W., 2022, The effect of collateral on small business rationing of term loans and lines of credit, EFMA, Norfolk, Virginia. [ Links ]

Coleman, S. & Cohn, R., 2000, 'Small firm use of financial leverage: Evidence from 1993 national survey of small business finance', Journal of Business Entrepreneurship 12(3), 81-98. [ Links ]

Cunat, V., 2006, 'Trade credit: Suppliers as debt collectors and insurance providers', The Review of Financial Studies 20(2), 491-527. https://doi.org/10.1093/rfs/hhl015 [ Links ]

El Ghoul, S. & Zheng, X., 2016, 'Trade credit provision and national culture', Journal of Corporate Finance 4(1), 475-501. https://doi.org/10.1016/j.jcorpfin.2016.07.002 [ Links ]

Fatoki, O., 2010, 'The impact of the South African business environment on the availability of debt finance to new small and medium enterprises in South Africa', PhD thesis, Business Management, University of the Free State. [ Links ]

Ferris, J.S., 1981, 'A transactions theory of trade credit use', Quarterly Journal of Economics 96(2), 243-270. https://doi.org/10.2307/1882390 [ Links ]

Frank, M.Z. & Maksimovic, V., 2003, Trade credit, collateral and adverse selection, University of Maryland working paper, SSRN, Rochester, New York. [ Links ]

Garcia-Teruel, P.J. & Martinez-Solano, P., 2007, 'Effects of working capital management on SME profitability', International Journal of Managerial Finance 3(2), 164-177. https://doi.org/10.1108/17439130710738718 [ Links ]

Gassiah, N. & Kikula, J., 2022, 'Challenges small and medium enterprises (SMEs) face in acquiring loans from commercial banks in Tanzania', African Journal of Business Management 16(4), 74-81. https://doi.org/10.5897/AJBM2021.9295 [ Links ]

Gbetnkom, D., 2012, 'Corruption and small and medium-sized enterprise growth in Cameroon', in S. Kayizzi-Mugerwa, A. Shimiles, A. Lusigi & A. Moummi (eds.), Inclusive growth in Africa: Policies, practice and lessons learnt, pp. 37-58, Routledge, New York, NY. [ Links ]

Herrington, M. & Kew, P., 2018, Global entrepreneurship monitor South African report, viewed 10 July 2020, from https://www.gemconsortium.org/economy-profiles/south-africa. [ Links ]

Howorth, C. & Moro, A., 2006, 'Trust within entrepreneur bank relationship: Insight from Italy', Entrepreneurship Theory and Practice 5(2), 26-40. [ Links ]

Huyghebaert, N., 2006, 'On the determinant and dynamics of trade credit use: Empirical evidence from business start-ups', Journal of Business Finance and Accounting 33(1-2), 305-328. https://doi.org/10.1111/j.1468-5957.2006.001364.x [ Links ]

Huyghebaert, N., Van De Gucht, L. & Van Hulle, C., 2001, The demand for debt finance by entrepreneurial firms, EFA 2001 Barcelona Meetings, Katholieke Universiteit, Belgium, Department of Applied Economics Working Paper no. 0110, SSRN, Rochester, New York. [ Links ]

Ibeh, K., Wilson, J. & Chizema, A., 2012, 'The internationalization of African firms 1995-2011: Review and implications', Thunderbird International Business Review 54(4), 411-427. https://doi.org/10.1002/tie.21473 [ Links ]

Le, A. & Doan, A., 2020, 'Corruption and financial fragility of small and medium enterprises: International evidence', Journal of Multinational Financial Management 57-58, 1-22. https://doi.org/10.1016/j.mulfin.2020.100660 [ Links ]

Lui, A., 2020, 'Understanding the shift in trade credit in the COVID-19 pandemic', S & P Global: Market intelligence, viewed 06 May 2020, from https://www.spglobal.com/marketintelligence/en/news-insights/blog/understanding-the-shift-in-trade-credit-in-the-covid-19-pandemic. [ Links ]

Malinao, C.W.M. & Ebi, R.G., 2022, 'Business management competencies as the driver of small-medium enterprises' survival during COVID-19 pandemic', Puissant 3, 296-315. [ Links ]

Martinez-Sola, C., Garcia-Teruel, P.J. & Martinez-Solano, P., 2013, 'Trade credit and SME profitability', Small Business Economics 42(3), 561-577. https://doi.org/10.1007/s11187-013-9491-y [ Links ]

McGuinness, G., Hogan, T. & Powell, R., 2017, 'European trade credit use and SME survival', Journal of Corporate Finance 49, 81-103. https://doi.org/10.1016/j.jcorpfin.2017.12.005 [ Links ]

New Partnership for Africa's Development (NEPA), 2008, Market access initiative, viewed 10 February 2016, from http://www.unido.org.hleadmin/import/11340. [ Links ]

Ngoc, T.B., Le, T. & Nguyen, T.B., 2009, 'The impact of networking on bank financing: The case of small and medium enterprises in Vietnam', Entrepreneurship Theory and Practise 33(4), 867-887. https://doi.org/10.1111/j.1540-6520.2009.00330.x [ Links ]

Nguyen, D.N., Tran, Q.N. & Truong, Q.T., 2022, 'The ownership concentration - Innovation nexus: Evidence from SMEs around the world', Emerging Markets Finance and Trade 58(5), 1288-1307. [ Links ]

Organisation of Economic Cooperation and Development (OECD), 2020, Economic surveys: South Africa, viewed 06 August 2020, from http://www.treasury.gov.za/comm_media/press/2020/20200731%20OECD% 20Economic%20Survey%20SA%202020.pdf. [ Links ]

Padachi, K., Narasimhan, M.S., Durbarry, R. & Howorth, C., 2008, 'An analysis of working capital structure and financing pattern of Mauritian small manufacturing firms', Journal of Applied Finance 14(7), 41-62. [ Links ]

Palacin-Sánchez, M.J., Canto-Cuevas, F.J. & Di-Pietro, F., 2019, 'Trade credit versus bank credit: A simultaneous analysis in European SMEs', Small Business Economic 58, 1079-1096. https://doi.org/10.1007/s11187-018-0101-x [ Links ]

Palazuelos, E., Crespo, A.H. & Del Corte, J.M., 2018, 'Accounting information quality and trust as determinants of credit granting to SMEs: The role of external audit', Small Business Economics 51, 861-877. https://doi.org/10.1007/s11187-017-9966-3 [ Links ]

Pallant, J., 2016, SPSS survival manual: A step-by-step guide to data analysis using IBM SPSS, Allen & Unwin, Sydney. [ Links ]

Petersen, M.A. & Rajan, R.G., 1997, 'Trade credit: Theories and evidence', Review of Financial Studies 10(4), 661-691. https://doi.org/10.1093/rfs/10.3.661 [ Links ]

Pretorius, M. & Shaw, G., 2004, 'Business plan in bank-decision making when financing new ventures in South Africa', South African Journal of Economics and Management Science 7(2), 221-242. https://doi.org/10.4102/sajems.v7i2.1377 [ Links ]

Rashid, A. & Saeed, M., 2017, 'Firms' investment decisions - Explaining the role of uncertainty', Journal of Economic Studies 44(5), 833-860. https://doi.org/10.1108/JES-02-2016-0041 [ Links ]

Schwartz, R.A., 1974, 'An economic model of trade credit', Journal of Financial and Quantitative Analysis 9(4), 643-657. https://doi.org/10.2307/2329765 [ Links ]

Scott, L.J., 1997, Regression models for categorical and limited dependent variables: Advanced quantitative techniques in the social sciences, Sage, Newbury Park, California. [ Links ]

Singer, S., Herrington, M. & Menipaz, E., 2018, Global entrepreneurship monitor report, viewed 02 September 2019, from http://www.gemconsortium.org/report. [ Links ]

Smith, J.K., 1987, 'Trade credit and informational asymmetry', Journal of Finance 42(4), 863-872. https://doi.org/10.1111/j.1540-6261.1987.tb03916.x [ Links ]

Song, H., Yang, X. & Yu, K., 2020, 'How do supply chain networks and SMEs' operational capabilities enhance working capital financing? An integrative signalling view', International Journal of Production Economics 220, 107447. https://doi.org/10.1016/j.ijpe.2019.07.020 [ Links ]

Statistics South Africa, 2021, Quarterly Labour Force Survey (QLFS), 4th quarter 2021, viewed 30 May 2022, from https://www.statssa.gov.za/?page_id=1854&PPN=P0211&SCH=73254. [ Links ]

Stiglitz, J. & Weiss, A., 1981, 'Credit rationing in markets with imperfect information', American Economic Review 71(3), 393-410. [ Links ]

Ullah, B., 2020, 'Financial constraints, corruption, and SME growth in transition economies', The Quarterly Review of Economics and Finance 75, 120-132. https://doi.org/10.1016/j.qref.2019.05.009 [ Links ]

Vander Bauwhede, H., De Meyere, M. & Van Cauwenberge, P., 2015, 'Financial reporting quality and the cost of debt of SMEs', Small Business Economics 45, 149-164. https://doi.org/10.1007/s11187-015-9645-1 [ Links ]

Van Horen, N., 2007, Customer market power and the provision of trade credit: Evidence from Eastern Europe and Central Asia, vol. 4284, World Bank Publications, Washington, DC. [ Links ]

Veliu, L. & Manxhari, M., 2017, 'The impact of managerial competencies on business performances: SME's in Kosovo', Vadyba Journal of Management 30(1), 59-65. [ Links ]

Voordeckers, W. & Steijvers, T., 2006, 'Business collateral and personal commitments in SMEs lending', Journal of Banking and Finance 30(11), 3067-3086. https://doi.org/10.1016/j.jbankfin.2006.05.003 [ Links ]

Wellalage, N. & Thrikawala, S., 2021, 'Does bribery sand or grease the wheels of firm level innovation: Evidence from Latin American countries', Journal of Evolutionary Economics 31(3), 891-929. https://doi.org/10.1007/s00191-020-00717-0 [ Links ]

Wellalage, N.H., Locke, S. & Samujh, H., 2019a, 'Corruption, gender and credit constraints: Evidence from South Asian SMEs', Journal of Business Ethics 159(1), 267-280. https://doi.org/10.1007/s10551-018-3793-6 [ Links ]

Wellalage, N.H., Locke, S. & Samujh, H., 2019b, 'Firm bribery and credit access: Evidence from Indian SMEs', Small Business Economics: An Entrepreneurial Journal 55(1), 1-22. https://doi.org/10.1007/s11187-019-00161-w [ Links ]

World Bank, 2020, Overview, viewed 13 July 2020, from https://www.worldbank.org/en/country/southafrica/overview. [ Links ]

Zikmund, W.G., Babin, B.J., Carr, J.C. & Griffin, M., 2010, Business research methods, 8th edn., Cengage Learning South-Western Cengage, Mason, Ohio. [ Links ]

Correspondence:

Correspondence:

Werner Otto

wernero@uj.ac.za

Received: 04 Apr. 2022

Accepted: 29 June 2022

Published: 20 Oct. 2022

Note: Additional supporting information may be found in the online version of this article as Online Appendix 1.

{kind=link}

{kind=link}