Services on Demand

Article

English (pdf)

English (pdf)

Article in xml format

Article in xml format Article references

Article references

Indicators

Related links

-

Cited by Google

Cited by Google -

Similars in Google

Similars in Google

Share

Permalink

PermalinkWater SA

On-line version ISSN 1816-7950

Print version ISSN 0378-4738

Water SA vol.46 n.1 Pretoria Jan. 2020

http://dx.doi.org/10.17159/wsa/2020.v46.i1.7880

RESEARCH PAPERS

Private sector impact investment in water purification infrastructure in South Africa: a qualitative analysis of opportunities and barriers

S McCallum; S Viviers

Department of Business Management, Stellenbosch University, Private Bag X1, Matieland, 7602, South Africa

ABSTRACT

Impact investing is gaining substantial traction globally and in sub-Saharan Africa. In contrast to conventional investors, impact investors not only seek financial returns, but also measurable, positive social and environmental impact. A growing number of impact investments have been observed in the region in recent years, particularly in water purification infrastructure. This study sought to identify the primary barriers and opportunities that impact investors face in this sector. Semi-structured personal interviews were conducted with 20 experts in the South African impact-investment value chain and water provision system. Participants identified more barriers than opportunities and were mainly concerned about the lack of lifecycle support, the possibility of political interference and low financial return expectations. Interviewees did, however, acknowledge the potential influence that these investments have on local communities and economies. Experts were of the opinion that the best opportunities are found in decentralised water purification infrastructure, especially where it involves innovation at a convergence of sectors. As the public funding gap in South Africa is likely to grow in future, innovative deal structures and government support will become even more important.

Keywords: impact investing, barriers, opportunities, water purification infrastructure, investment ready deals, political interference

INTRODUCTION

In the time it takes one to read the next 2 pages over 50 people globally would have died from diseases linked to unsafe drinking water (Gleick, 2002). The disease burden caused by inadequate water and sanitation infrastructure is estimated to result in approximately 5 million deaths per annum globally. Of this group, 2 million mortalities occur from water-related diarrhoea alone (Montgomery and Elimelech, 2007; Prüss et al., 2002).

The United Nations Human Rights Council Resolution 27/7 of September 2014 entitles every human, without discrimination, to have 'access to sufficient, safe, acceptable, physically accessible and affordable water for personal and domestic use and to have physical and affordable access to sanitation, in all spheres of life, that is safe, hygienic, secure, socially and culturally acceptable and that provides privacy and ensures dignity' (UNHRC, 2014).

Practically speaking, 'sufficient' access refers to a minimum of between 20 and 40 litres of water per person per day (Zolnikov and Salafia, 2016). Water is regarded 'safe' if it meets certain standards and does not pose a significant risk to the health of babies, the immune-compromised or the elderly over a lifetime of consumption. According to the World Health Organisation, a water source should be located within one kilometre of the user's place of residence for it to be considered 'physically accessible' (WHO, 2006). Although there is no consensus on what 'affordable' means, the United Nations suggests that the cost of water should not exceed 3% of an individual's personal income (Watkins, 2006).

Despite the fact that water is a basic human right, people the world over are facing a significant decline in the quantity and quality of available fresh water. The adverse effects of water crises on human health and economic activity are widespread and are likely to increase in future (The Global Risks Report 2017, 2017). Water scarcity and poor water quality not only pose health risks to individuals, but also limits productivity, results in lost education hours, creates concerns regarding food security and causes other adverse socio-economic implications (Adams et al., 2016; Bigas, 2012). Women and children are often disproportionally impacted as they are normally tasked with the responsibility of collecting water for the household (Connor, 2016). It is estimated that the water-related needs of approximately 15% of South African households could not be met by Government in 2016 (StatsSA, 2016; DWS, 2014). The status quo might be attributed, in part, to the insufficient planning, development and maintenance of water infrastructure (Van Vuuren, 2014).

Although the availability and quality of water also affect agricultural, commercial, mining and industrial users, the focus of this study was on domestic users. Many of these users reside in areas where no formal water infrastructure is provided. These areas, often referred to as peri-urban areas, exist on the fringes of city borders and typically consist of unplanned and informal settlements and are often excluded from national water-supply programmes (Peter-Varbanets et al., 2009).

The infrastructure necessary to provide potable water to domestic users, such as dams, filtration plants and pipelines, is costly to build and maintain. Although governments are primarily responsible for providing this public good, private sector investors are increasingly active in this sector (Rodriguez et al., 2012). Investment opportunities for private sector investors exist in both centralised and decentralised water provision systems.

In a centralised system, safe drinking water is continuously supplied to large areas such as cities. Fresh water is collected in a protected area (e.g. a dam), purified and delivered to domestic users through a system of pressurised pipes (Galada et al., 2014). Investment opportunities in centralised systems could take the form of investing in a desalination plant or water treatment plants connected to these systems. In contrast, a decentralised system provides water resources that are sourced close to households and communities who treat it themselves (e.g. rainwater tanks and groundwater extraction). Decentralised systems are typically observed in rural and peri-urban areas where it is not technically, economically or environmentally feasible to install centralised systems (Cook et al., 2009).

Several innovative water purification products have seen the light in recent years. Examples include faecal waste/sludge convertors and vapour compression distillers. These products could be used at household and/or community level. Decentralised systems have lower maintenance costs, require fewer upgrades, can be installed incrementally (based on demand) and work on a 'fit-to-purpose' concept (Galada et al., 2014). Other benefits include smaller investments, less bureaucracy and shorter delivery times (Ringwood, 2016).

An estimated R33 billion per annum is required to close the water infrastructure funding gap in South Africa over the next 10 years (DWS, 2018). This situation is not unique to South Africa (Rodriguez et al., 2012) and presents private sector investors with an opportunity to 'do good while doing well'. Investors who seek measurable, positive social and/or environmental impact alongside market-based, risk-adjusted returns are called impact investors (Harji and Jackson, 2012). Impact investing is one of several strategies available to responsible investors (Hebb, 2013).

Although there is no universally accepted definition of impact investing, a few key elements have emerged from the literature (Clarkin and Cangioni, 2016; Höchstädter and Scheck, 2015; Sales, 2015; Saltuk, 2015; Barby and Pedersen, 2014; Burand, 2014; Drexler et al., 2014; Jackson, 2013; Arosio, 2011; Freireich and Fulton, 2009). These elements include intentionality and measurability of impact attributable to the intervention. Furthermore, there should be a positive correlation between the intended social and/or environmental impact and the financial return of the investment. Lastly, an impact investment should lead to a net positive effect on society and/or the natural environment in addition to what would have occurred without the intervention.

Drawing on the aforementioned elements, impact investing was defined in this study as a responsible investment (RI) strategy where investors actively and intentionally seek to generate both measurable, positive social and/or environmental impact alongside financial return. Impact investors are typically institutional investors, such as pension funds and insurance companies, who pursue their dual goals by investing in for-profit entities that offer products and services ranging from microloans to affordable housing, renewable energy and sustainably grown crops. In the context of this study, impact investors could also invest in private equity funds and collective investment schemes that support the development of water and sanitation infrastructure. According to Jackson (2013), role players in the impact-investment market can be divided into categories. Examples of role players in each category are depicted in Table 1.

According to a study by the GIIN, the size of the global impact-investing market, based on assets under management, was approximately 502 billion USD at the end of 2018 (Mudaliar and Dithrich, 2019). This study shows that impact investing has gained significant momentum over the past decade as both an investment strategy and an approach to addressing pressing social and environmental challenges (ibid). A mere 4% of investments in this market was allocated to impact investments in water, sanitation and hygiene (Mudaliar et al., 2018).

It is estimated that impact investments in sub-Saharan Africa constituted approximately 12% of the global market in 2018 (ibid). Within sub-Saharan Africa, South Africa represents the largest impact investment market (Giamporcaro et al., 2017; Mudaliar et al., 2016). No statistics could be found on the allocation of impact investments to water-related projects in sub-Saharan Africa in general or South Africa in particular. The authors are, however, of the opinion that it is likely to be higher than the global average (±4%).

As set out in South Africa's National Development Plan, Government has committed to invest 10% of gross domestic product (GDP) to three key areas, namely, transport, energy and water, over the next couple of years. Private sector investment is likely to follow suit. Water is one of the industries which President Ramaphosa singled out as presenting 'huge [investment] opportunities' for foreign investors (Johnson et al., 2018). The President even set up a national impact investing task force aimed at accelerating this investment strategy (Impact Investing South Africa, 2019). Water-related investments, including those intended at reducing water pollution, are also mentioned in the Government's Climate Change White Paper, New Growth Plan and National Industrial Action Plan.

Despite significant growth in impact investing in recent years, limited academic research has been conducted on the topic (Clarkin and Cangioni, 2016). As far as could be established no research has been conducted on impact investment in the water sector. Most studies on private sector involvement in the provision of a public good such as potable water centred on privatisation (Prasad, 2006; Hall, Lobina and De la Motte, 2005) and public-private partnerships (PPPs) (Ruiters and Matji, 2016; Ameyaw and Chan, 2015; Chitonge, 2013; Ruiters, 2013; Baruah, 2007; Grimsey and Lewis, 2002).

Access to finance is crucial for successful water service delivery. Ruiters and Matji (2016), Ruiters (2013) and Coppel and Schwartz (2011) provide insights into South Africa's existing and potential alternative water infrastructure funding models' opportunities and barriers.

Listed barriers include: prolonged projects; lack of technical, management and legal capacity in municipalities; heavy reliance on government grants, monitoring of private operator issues; and failure to deliver on tender which could lead to the collapse of the business operations. The current water pricing strategy does not generate enough revenue, therefore, the state consistently is in deficit. Barriers also mentioned were concerns over poor planning and adherence to municipal financial budgets, and not enough commitment, consistency or legislative protection for private sector to encourage long-term partnerships, as well as a politically volatile appropriation process. Customers are also weary of privatization and fear water charges would become another tax. Challenges in PPPs also involved risk sharing, cultural and language barriers and differing opinions about how things should be run.

Opportunities include multiple forms of project financing that involves government and private sector, and that certain PPP models allow for skills and knowledge transfer as well as creative solutions to maximise profit and achieve operational efficiency. Private sector involvement also allows government to harness capital markets. Other opportunities include specific pricing to achieve equitable and efficient allocation of water and to encourage efficient usage, and ability to manage demand side risk and to refinance the projects.

Given the aforementioned barriers, the South African Government has recognised that new delivery models are required to close the funding gap and alleviate the increasing demands on water infrastructure (Ruiters, 2013). According to this author, South Africa's limited financial resources, poor capital markets and inadequate governance structures require new long-term capital financing models that take account of environmental and social aspects as well as of economic imperatives. As such, impact investing could play a crucial role as an alternative financing model that could unlock capital and provide measurable social and environmental return.

In light of the research gap, the need for alternative funding models to improve national water infrastructure management, and the necessity for improved access to drinking water for better quality of life, this study set out to investigate barriers and opportunities associated with private sector impact investment in water purification infrastructure. Specific attention was given to the situation in South Africa for a number of reasons. The definite need for private sector involvement and investment is exemplified by the 55% South African Government budget shortfall to maintain and develop water infrastructure (Millson and Roux, 2015). Furthermore, South Africa is well positioned to accommodate impact investments as the country is the largest impact investment market in Sub-Saharan Africa (Sales, 2015). The amount of impact capital invested in South Africa is 15 times more than the country second to it in the Southern Africa region, namely, Zambia (Mudaliar et al., 2016). Impact investments, however, still only represent a small percentage of the total investment landscape in South Africa. Impact investing is considered so important in South Africa that a national task force for impact investment was launched in October 2018 to direct capital towards underfinanced impact projects.

Unless a better understanding of the hindrances and prospects of impact investments in water purification infrastructure is gained, the probability of the much-needed capital influx from the private sector is likely to remain small. In the following section a brief overview is provided of the barriers and opportunities that impact investors commonly face, as identified in the literature. Where possible, references were included on water purification infrastructure. The methods used to collect and analyse qualitative data are then described along with the main empirical findings. Next, conclusions and recommendations for impact investors and academicians are offered.

Barriers to impact investing in water purification infrastructure in South Africa

Many barriers to the general impact-investment market can by extension be applied to investments in water purification infrastructure. These barriers include the relatively small size and early stage of development of the impact-investing market (Choda and Teladia, 2018; Evans, 2013), which increases risk and could leave institutional investors circumspect about investment prospects due to their fiduciary duty to make prudent investment decisions in the best interest of their clients (Sales, 2015). One of the main hindrances to growing the impact-investment market is the limited number of investment-ready deals into which investors can place significant amounts of capital (Ormiston et al., 2015; Burand, 2014; Freireich and Fulton, 2009). As such, there is a shortage of high-quality investment opportunities with well-established track records (Clarkin and Cangioni, 2016; Brandstetter and Lehner, 2015; Saltuk, 2015; Burand, 2014). The lack of well-documented success stories has also resulted in a perception among investors that impact investing cannot provide market-related, risk-adjusted financial returns (Barby and Pederson, 2014; Saltuk, 2015). This perception might be the result of the belief that there must be a trade-off between financial return and social and/or environmental impact (Evans, 2013).

Another one of the most critical challenges to the growth of the impact-investing market is the limited number of intermediaries, which results in high transaction costs, more complex deal structures and more complicated due-diligence investigations (Saltuk et al., 2013; Bugg-Levine and Goldstein, 2009; Freireich and Fulton, 2009). A shared barrier for many impact investors, and investors in water purification infrastructure by extension, is the difficulty of exiting their investments due to their illiquidity (Burand, 2014; Harji and Jackson, 2012). Lastly, the impact-investing market does not have a universally agreed upon set of metrics to measure social and environmental impact, which complicates reporting (Choda and Teladia, 2018; Clarkin and Cangioni, 2016; Sales, 2015; Reeder, 2014; Rangan et al., 2011).

Barriers specific to impact investing in water purification infrastructure include political interference, financial risks inherent in water sector investments and the moral dilemma investors face of making a profit from a basic human right. These barriers will be discussed in more detail in the following sections.

Innovations in finance are available to improve acceptable access to water, but one of the main obstacles of making technological advancements available to the masses is what Osumanu (2008) calls the political factor. Water contracts and regulatory agreements are susceptible to political re-interpretation and interference (Winpenny, 2006), which increases the risk of investing and, therefore, is a barrier for impact investors. An increased risk factor generally results in investors demanding a higher return. High risk could discourage institutional investors, given their fiduciary duty to manage their clients' capital prudently.

Many South African municipalities responsible for water provision are ineffective due to in-fighting, corruption and inappropriate appointments (McGarry et al., 2010). Corruption in government is also a major issue when dealing with investments in water purification technology (Johnson et al., 2008). Likewise, bribery and 'under-the-table' deals increase initial costs of building water infrastructure.

The affordability of water is a key element to ascertain as there is much debate surrounding the level at which potable water becomes 'too expensive' for the poor (Fankhauser and Tepic, 2007). High rates of poverty in South Africa manifest in the inability to pay for water services and other basic needs (Turton et al., 2016). The repercussion for institutional investors when individuals are unable to pay is directly related to financial returns. As a result, investors might not receive the expected returns.

The profitability of water in developing countries is at the centre of the financing problem (Winpenny, 2006). According to this author, financing water is considered risky in emerging markets. There have been several high-profile cases in developing countries illustrating losses which have increased the high-risk perception among institutional investors (Tecco, 2008). The higher risk factor in developing countries is a barrier to investment due to the uncertainty of returns associated with the higher risk.

An additional contributing factor to higher financial risk is the high initial costs of water infrastructure (Rodriguez et al., 2012). Water sector infrastructure often only serves a single function so investors depend solely on future revenue to create the desired returns (Tecco, 2008). The high initial investment and the uni-functional characteristic of the water infrastructure create the risk of serious financial loss should the system fail.

Investors could also face a moral dilemma when investing to address a problem involving a basic human right. A moral dilemma involves a tension between individual rights and the greater good. The dilemma in this case is the tension of generating financial returns when those returns originate from providing acceptable access to a basic human right such as drinking water. One of the key points in the Human Rights Council Resolution 27/7 of September 2014 is that water for domestic use should be affordable. The fact that governments and companies providing purified water should charge consumers an 'affordable' price thus raises questions of what an acceptable price is. The price should be affordable, but should also be economically viable for private sector investors. There is, however, concern that the private sector's short-term profit focus might override the long-term sustainability considerations of water purification infrastructure.

Barriers that correspond with existing models include negative perceptions of private sector involvement, financial risks inherent to water sector investments and the lack of skilled government officials. New or differing barriers comprise of the possibility of political interference, moral dilemma associated with profiting from a basic human right and specific barriers associated with community-level water purification systems.

Opportunities in impact investing in water purification infrastructure in South Africa

Despite the many barriers, there are great opportunities found in impact investments in water purification infrastructure. Most opportunities in the impact-investment asset class are found in private markets which include real assets, private debt, private equity and venture capital (Barby and Pedersen, 2014). Many of the opportunities in the broader impact-investment market can be applied by extension to impact investments in water purification infrastructure. These opportunities include the growing interest and acceptance of impact investing as an RI strategy (Höchstädter and Scheck, 2015; Sales, 2015; Saltuk, 2015), increasing amount of capital flowing into South Africa (Mudaliar et al., 2016; Sales, 2015) and positive changes in the regulatory environment that could unlock additional opportunities in impact (Mudaliar et al., 2016; Drexler et al., 2014). Opportunities more specific to impact investing in water purification infrastructure include: financial returns from investing in water, increased interest from institutional investment in water purification infrastructure and the opportunity to create social and/or environmental impact.

The water sector is poised for significant growth in the near future. As the world's population increases so will the demand for potable water. Financial analysts have predicted high growth potential in the water market globally (Bigas, 2012). The current global water market size is estimated to be 591 billion USD and forecasts show that it could reach a market size of 1 trillion USD between 2020 and 2025 (Robecosam, 2015).

Investments in safe drinking water and sanitation have the potential to generate returns of between 3 and 34 USD/USD invested, depending on the region and technology (Connor, 2016). Recent WHO estimates forecast a 4.3 USD return on every US dollar invested and a predicted gain of 1.5% of global gross domestic product (WHO, 2014). In Africa alone, investment in small-scale projects that provide access to water and sanitation infrastructure could return an estimated 28.4 billion USD per annum (Connor, 2016). Furthermore, there is an economic gain estimate of 5% of the country's gross domestic product for small-scale projects that provide drinking water in Africa. Similarly, certain segments of the water sector can be expected to generate annualised returns of between 5 and 10% until 2030 (Roca et al., 2015).

According to South Africa's National Water Resource Strategy 2 (DWS, 2013), the financing gap left by the DWS and related water provision institutions is estimated at R700 billion. It is this funding gap that has caught the interest of the institutional investors. In the areas where Governments is struggling to improve water provision, an opportunity exists for impact funding to support financially viable and market-based solutions to address social and/or environmental problems. The private sector has increasingly been recognised as crucial to filling the financing gap (Bayliss, 2013; Briscoe, 1999). The South African National Water Resource Strategy 2 indicates that the private sector will be encouraged contribute to the social component of infrastructure investment (DWS, 2013). Correspondingly, the investments could be part of their corporate social investment strategies and should benefit the communities from which they draw their labour force.

In addition to the growing interest from the private sector, water-treatment technologies are also becoming more affordable (DWS, 2013). Part of the reason is a result of improved technologies and the intensifying scarcity of water in many parts of Sub-Saharan Africa. These reasons encourage innovation and create significant investment opportunities to fund research and development of water-efficient technologies to provide for those who do not have acceptable access to potable water (Slaughter, 2010).

Institutional investors who devote capital towards water purification infrastructure have the opportunity to create significant social and/or environmental impact in these areas. Alongside the financial returns, the social and environmental advantages of water infrastructure investments include health benefits, education gains, increased productivity, reduced water and soil pollution and a better quality of life (WHO, 2014; OECD, 2011). Better access to water infrastructure will also create more dignified and hygienic sanitary environments and increase quality of life (OECD, 2011).

Similarly, investments in water purification infrastructure can create environmental impact. By purifying water, major sources of pollution are combatted (WHO, 2014; Turner, 2013; OECD, 2011). Improvements in the levels of water pollution through water purification are quantifiable and therefore impact investors will be able to demonstrate measurable environmental impact.

Opportunities that correspond with existing models include new infrastructure, with models to fund the infrastructure needed, and a large public financing gap that necessitates private sector involvement by harnessing capital markets. New or differing opportunities comprise of increased interest among institutional investors in water purification infrastructure, certain models that allow for skills and knowledge transfer and the opportunity to create social and environmental impact.

METHODS

Although impact investing has become more recognised and researched globally, limited academic research has been undertaken in emerging markets where over two-thirds of impact investment transactions occur (Burand, 2014). Given the exploratory nature of the study, a qualitative research paradigm was deemed appropriate. Secondary data were collected through an extensive review of academic journal articles, industry reports and books. Primary qualitative data were sourced from experts in the local impact-investment market and the water provision process.

At the time of conducting the primary research, no usable population or sample frame existed outlining the role players in the local impact-investment market. A sample frame thus had to be compiled from sources such as Mudaliar et al. (2016), Rockey (2016) and Sales (2015). A second sample frame was assembled from individuals and entities that were identified as experts in the research and development of water purification infrastructure and that were listed in the South African Water Directory (WRC, 2017).

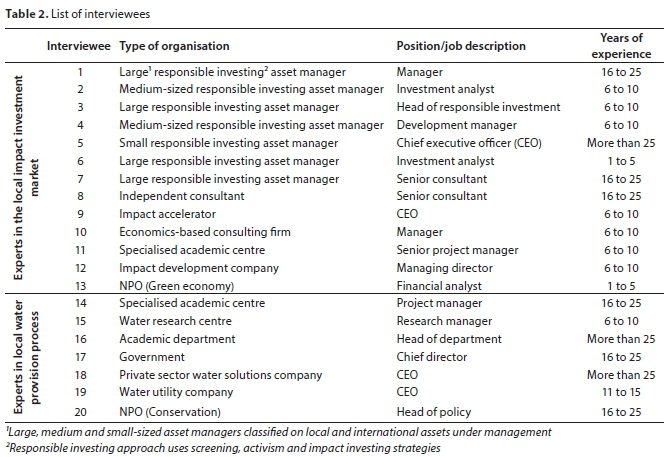

Judgemental and snowball sampling techniques were used to identify eligible participants. The sample consisted of 8 impact investors, some of whom were employed at large asset managers and others at small boutique investment houses. In addition, 5 role players in the impact-investment market were included as well as 7 experts in the water provision process. The latter group consisted of academics, researchers and consultants. Thus, the range of eligible participants that were considered is consistent with what constitutes a representative sample in existing studies on both impact investing (Ngoasong et al., 2015) and water partnerships (Ganoulis et al., 2011). A more detailed description of the participants is provided in Table 2.

To qualify for inclusion, a participant had to be an executive decision maker or person in a managerial role who has made or has helped facilitate one or more impact investments over the period 2011 to 2016. Similarly, role players in the water provision process were identified based on their expertise in different water purification processes and their involvement with the research and development of water purification infrastructure. These individuals were either an executive decision maker or a person in a managerial role who has had experience in the water provision process over the past 5 years.

The sample consisted of an equal number of men and women. The average age (30 to 39) shows that a mature group of individuals participated in this study. They were also experienced, as demonstrated by the average number of years work experience (11 to 15 years). The senior positions that were held by the participants at the time of the study provide further evidence that authoritative opinions were gathered. Of the 20 participants, 4 were CEOs, 5 were heads of departments, 6 were managers and the remaining 5 were consultants and analysts. In addition, 13 of the participants had masters' or doctoral degrees.

An interview guide was developed to facilitate semi-structured personal interviews. In addition to requesting biographical details, open-ended questions were posed to determine the participants' views on the barriers and opportunities in impact investing and those specific to investing in water purification infrastructure. All interviews were audio-recorded and professionally transcribed. Data collection continued until data saturation was achieved.

The first step of the data analysis involved the conversion of the raw data into a more user-friendly format. The 20 Word documents provided by the professional transcriber were used to undertake the directed content analysis. This method was selected as it provides a systematic and objective way for researchers to describe and understand a particular phenomenon such as impact investing in water purification infrastructure (Elo and Kyngäs, 2007). This data analysis method furthermore validates insights gained from the literature review (Hsieh and Shannon, 2005).

Firstly, key words drawn from answers in the interview guide were used to manually code the textual data into categories of the barriers and opportunities. Thereafter, all textual data were imported into the qualitative data analysis software ATLAS.ti. The software was used to make data coding more organised, simple and reliable. The textual data were coded into explicit themes representing similar meanings so that patterns that were found could be easily described. Thereafter, the authors conducted further directed content analysis and inductive reasoning to code and synthesise common and contrasting themes.

Credibility was ensured by gauging the views of experts in the local impact-investment market, audio-recording the interviews, taking meticulous notes and triangulating thoughts and ideas. To achieve dependability, a reflective appraisal was conducted to confirm that the findings reflected the essence of the raw data gathered. Steps were also taken to ensure that the focus remained on the opinions of the participants and not on those of the authors. Ethics clearance was obtained given the nature of the study.

FINDINGS AND DISCUSSION

Although participants confirmed the existence of several barriers and opportunities highlighted in the literature, a few new ones were also uncovered.

Barriers to impact investing in water purification infrastructure in South Africa

The majority of interviewees agreed that the relatively small impact-investment market in South Africa could limit opportunities in this market. However, they qualified this opinion by saying that it was a question of what type of transaction was available. The participants emphasised that the lack of investment-ready deals represented a much greater barrier. The shortage of investment-ready deals in the impact-investment market in South Africa was considered to be the largest barrier to impact investing in general in South Africa and to water purification infrastructure by extension.

Most of the barriers related to the nascent impact-investment market are influenced by the shortage of investment-ready deals. Considering that most impact investors in South Africa only invest in more mature entities, the authors believe that these barriers are actually related to a more critical barrier. This barrier is the lack of lifecycle support. For example, small and medium-sized social enterprises in South Africa are often adversely affected by the lack of lifecycle support to assist in their development. Therefore, these enterprises are often too early in their development for impact investors to consider investing in them. The investment mandates of some impact investors may restrict their involvement in early-stage entities.

Therefore, the authors are of the opinion that private sector impact investors claim that there are not enough investment-ready deals, but that they are taking too narrow a view of the water provision process. This process includes the protection of rivers and catchment areas, the construction, refurbishment and advancement of infrastructure (dams, pipelines, water treatment works) and the distribution of water to a range of users (DWS, 2015). At present most impact investors focus on the latter part of the process (distribution) by investing in businesses that sell bottled water or water purification equipment. Consequently, the impact-investment market is likely to remain stunted until there is more support across the business lifecycle for small and medium-sized social enterprises or until impact investors become less risk-averse.

The general outlook was that there is also a lack of impact investments in general and in water purification infrastructure with established track records across the risk/return spectrum in South Africa. The shortage of investment-ready deals was again perceived as the main contributor to this.

Most participants regarded the perception that impact investments in South Africa are unable to yield market-related, risk-adjusted returns to be a major barrier to further investment. However, the interviewees emphasised that this perception is not true.

The majority of participants agreed that there is a limited number of specialised intermediaries in the local impact-investment market which causes a dearth of awareness of impact investing. Furthermore, the lack of a coordinated impact investment 'ecosystem' was highlighted by a few participants as a major barrier as it creates hesitation among role players to share information. This barrier results in incoherent actions amongst the role players.

In the extant literature claims are made that the due-diligence process is more complex to execute given the limited number of specialised intermediaries (Bugg-Levine and Goldstein, 2009; Freireich and Fulton, 2009). The participants had varying opinions on this barrier. The investors indicated that they do not perceive this to be a barrier because the majority of asset managers have their own well-trained due-diligence teams. However, the other role players in the impact investment market sample disagreed, given that there are large inefficiencies in this area of the market which makes due-diligence more complex. They argued that there is 'a hesitation to share information and use shared knowledge for the greater good' which results in inefficiencies. Therefore, due-diligence investigations take longer and are more complex than they should be. The authors are of the opinion that the real barrier is not the lack of specialised intermediaries. Instead, the complexity of due-diligence investigations is attributed to the lack of shared knowledge.

The largest contingent of interviewees was of the opinion that the lack of bespoke metrics was not a barrier to impact investing in South Africa. Many of the participants agreed that there are enough metrics available. They commented that most investors use their own metrics that are tailored for their specific projects as the available standardised metrics are regarded as 'restrictive and limiting'. Participants, however, highlighted the dearth of knowledge of how to report social and/or environmental impact as there is no standardised format for doing this. Therefore, the reporting of social and/or environmental impact is inconsistent and not comparable across investment time horizons. As such, the authors found that the real barrier to measurement is related to an absence of a standardised format to impact reporting.

Barriers specific to water purification infrastructure investments in South Africa

PPPs were mentioned as a suitable way to address grand challenges in impact investments in general and in water purification infrastructure in South Africa. The large public financing gap and relatively positive perceptions of PPPs in South Africa were regarded as motivating factors for private sector involvement in the financing of water purification infrastructure. Participants, however, mentioned the possibility of political interference and distrust between government and private sector preventing the establishment of PPPs as a major barrier to private sector investment. Therefore, the lack of trust and coordination between government and the private sector might hamper the growth of the impact-investment market in South Africa. Political interference was regarded as one of the most pertinent obstacles to investments in water purification infrastructure in South Africa. However, the participants did not consider corruption and bribery as particularly important barriers. Although most of the interviewees agreed that political interference could leave investors hesitant, they did not think the risk is higher than it is with investments in other economic sectors.

The empirical results suggest that the South African Government should be primarily responsible to finance water infrastructure in the country. However, given the shortage of capacity and financial resources, private sector involvement was considered a necessity. Participants cited the lack of financial capacity, the country's small tax base and the limited municipal capability as reasons for the government's inability to accept full responsibility of the financing of such infrastructure.

Participants considered the shortage of skilled government officials and engineers in the appropriate positions a barrier to impact investments in water purification infrastructure in South Africa. According to the authors of the study, there seems to be a shortage of government officials who are strategically focused on repairing and maintaining water infrastructure in South Africa. Having said this, the deficiency of skills to repair and maintain water infrastructure does not appear to be the main barrier to impact investments. Instead, the barrier to impact investments in the local water infrastructure is the lack of skilled government officials and engineers in the appropriate and needed positions.

The general opinion was that substantial financial returns could not be earned from investments in water purification infrastructure. The majority of participants considered poor profitability predictions of investments in water purification infrastructure to be a critical barrier to impact investments. One of the challenges that was highlighted is the unclear commercial opportunity. There is an apparent mismatch between the impact an investor could make and the return requirements. As the current water tariff structure in South Africa is low, the revenue-raising ability of water is constrained.

Many authors regard illiquidity and the difficulty to exit impact investments as major barriers that hinder the growth of the impact-investment market (Sales, 2015; Burand, 2014; Harji and Jackson, 2012). However, the general opinion of participants was that impact investors in South Africa have a good understanding of the nature of the assets that they are investing in and often structure exits before committing capital. However, the overall view among participants was that the perceived high initial costs of water infrastructure are a fundamental barrier to impact investments in water purification infrastructure. The main concern was that the water tariff structure is not aligned with the initial capital investment. Therefore, the deals should be structured over long periods with doubts about financial returns.

Most of the interviewees were of the opinion that impact investors do not face a moral dilemma when making a return from providing a basic human right. However, they did caveat their statements by indicating that the price of the goods or services provided should be affordable. The authors of the study share the view that impact investors do not face a moral dilemma as long as they do not exploit the end-users' needs by charging unaffordable prices. Establishing a reasonable price that does not compromise financial return, but provides acceptable access was, however, emphasised as a major challenge for impact investors. As a result, this challenge was regarded as a barrier to impact investments in water purification infrastructure.

Two of the impact investors indicated that the complexities involved in multiple stakeholder engagement are a barrier to impact investments. They noted that there are too many interest groups that must be engaged before an investment in water purification infrastructure can be made and that some investors are consequently hesitant to get involved in such investments.

Opportunities for impact investing in water purification infrastructure in South Africa

The majority of the sampled experts agreed that there was a growing interest among institutional investors in water purification infrastructure investments in South Africa. However, they did not perceive that the interest has resulted in more investment opportunities yet. Many mentioned that they expected it to be a growing area of investment in the future. These participants furthermore commented that there are still too many barriers to overcome and that the water market in general is still very isolated and fragmented.

Similarly, the majority of the participants also perceived that the amendments to Regulation 28 of the Pension Fund Act (No. 24 of 1956) and Section 12J of the Income Tax Act (No. 58 of 1962), as well as the implementation of the B-BBEE Act (No. 53 of 2003), have prompted interest in and thinking about impact investments. Nonetheless, there has not been an increase in demand and capital deployment due to these changes in the South African regulatory environment. Therefore, these amendments should rather be considered as enablers and motivators.

Although there are many challenges, interviewees believed that investments in decentralised systems of water supply provide the best opportunities when investing in water purification infrastructure. According to these participants, bulk infrastructure is well funded in the local water provision system through grants. Therefore, the best investment opportunity would be where the centralised water systems end. Furthermore, other participants regarded the best focus for impact investments would be on the research and development of technology and innovation at a convergence of sectors. Most of these participants indicated that there should be a focus on decentralised water purification infrastructure as they felt it would provide the largest impact.

Most of the participants acknowledged that major social and/or environmental impact can be generated from impact investments in water purification infrastructure. Participants highlighted opportunities to achieve impact in peri-urban areas, regions of rapid population growth and by supplementing the large public financing gap in water purification infrastructure. Furthermore, investments in alternative infrastructure and in new innovation in a convergence of sectors were considered opportunities in investments in water purification infrastructure.

The high level of poverty in South Africa was not considered a barrier to impact investments in water purification infrastructure. Instead, participants saw opportunities to provide products and services to an untapped market at the bottom of the pyramid. The complexity of deal structuring in water purification infrastructure was perceived as an additional barrier which did not feature in the original conceptual framework.

The majority of participants believed that there are investment opportunities in different forms of innovation in water purification infrastructure. The examples highlighted by the interviewees revealed that the best investment prospects are found in a convergence of sectors. The authors agree that an investment in innovative technologies that combines the water, agricultural, mining and energy sectors could generate the best financial returns.

SUMMARY, CONCLUSIONS AND RECOMMENDATIONS

The lack of a standardised format to social and/or environmental impact reporting was discussed as a barrier to impact investing in general and in water purification infrastructure by extension. It is difficult to envision standardised reporting without universally accepted metrics. Therefore, industry experts should focus on developing a standardised format to report impact that could be applied across different categories/dimensions over multiple years instead of a set of universally accepted metrics. It is recommended that the GIIN provide more workshops on consistent impact reporting. These workshops could start with how to clearly articulate impact objectives that match financial objectives.

The South African impact-investment market needs more investors across the risk/return spectrum, especially angel investor and venture capitalists, to ensure more lifecycle support for small and medium-sized social enterprises. Without an increase in angel investors and venture capitalists, the impact-investment market will remain small and the competition to invest in the same later-stage entities will continue. Furthermore, more engagement is required from financial institutions, research and service providers, educators and policy makers to increase the lifecycle support of social enterprises and impact businesses in South Africa, particularly in the water sector.

It was evident that at the time this study was conducted many participants did not see viable opportunities in investing directly in water purification infrastructure. In similar vein, participants in the present study favoured decentralised systems in these areas as they believed it would offer better investment opportunities. However, many interviewees indicated that direct investments in decentralised water purification infrastructure might not be a plausible investment yet. Instead, impact investments in innovative water technologies that could address challenges beyond the need for potable water should also be considered. These investments could be made in a grouping of sectors, such as water-energy-food nexus, where some of the greatest threats to the South African economy are found.

The large public financing gap and the lack of capacity are evidence that government needs assistance to address the difficulties related to the provision, development and maintenance of water infrastructure in South Africa. The authors of the study recommend that PPPs should be used in developing countries more often to, amongst others, combat inefficient and expensive infrastructure development and maintenance.

The authors express the hope that more municipalities and private sector companies will issue water-based green bonds in future. In the United States of America, the San Francisco Public Utilities Commission recently issued such bonds (Whiley, 2019). The funds raised through this bond issue will be used to improve the region's sewerage and flood response infrastructure. Similar bonds have also been issued by DC Water (2019) to improve water quality, flood resistance and the promotion of biodiversity. A recent GIIN report highlighted opportunities for impact investors to get involved in the Lesotho Highlands Water Project (Mudaliar et al., 2016). This multi-billion USD, multi-phase project, which will divert water from Lesotho to Johannesburg, spans different stages of the water provision process, including bulk infrastructure.

It was emphasised that the South African Government is primarily responsible for the development and maintenance of water infrastructure. They could, however, outsource more stages of the water provision process to the private sector than they currently do. The possibility of government subsidisation in rural areas should be considered to decrease the complexity of deal structuring in impact investing in water purification infrastructure and the low financial return expectations. Such subsidisation could counter the low water tariff recovery rates, paving the way for more investment opportunities. Government could also ensure agreements with the underlying small and medium-sized social enterprises for the future selling or purchasing of resources which could mitigate some of the financial risks that the private sector investors face.

Given the large number of stakeholders in the water provision process and a deliberate focus on private sector investments, not many public sector role players were interviewed. Therefore, future researchers could conduct interviews with more government officials. These interviews can be supplemented with the opinions of individuals who do not have acceptable access to potable water.

At present there are more barriers than opportunities in impact investments in water purification infrastructure in South Africa. However, the authors remain optimistic about the future prospects in this area. Water, often named 'the blue gold', is a resource related to many sectors. The authors of the study believe that an effective and innovative deal structure offers endless possibilities to create impact. Increased government focus on this responsible investment strategy (through the national task force) is also a positive development.

ACKNOWLEDGMENTS

The Harry Crossley Foundation is thanked for providing financial support. A word of gratitude is also extended to the interviewees for sharing their insights with the authors.

REFERENCES

ADAMS EA, BOATENG GO and AMOYAW JA (2016) Socioeconomic and demographic predictors of potable water and sanitation access in Ghana. J. Soc. Indic. Res. 126 (2) 673-687. https://doi.org/10.1007/s11205-015-0912-y [ Links ]

AMEYAW EE and CHAN APC (2015) Risk ranking and analysis in PPP water supply infrastructure projects: An international survey of industry experts. J. Facil. 8 (7) 428-453. https://doi.org/10.1108/F-12-2013-0091 [ Links ]

AROSIO M (2011) Impact investing in emerging markets. Global Impact Investment Network. URL: https://thegiin.org/assets/binary-data/RESOURCE/download_file/000/000/252-1.pdf (Accessed 1 April 2017). [ Links ]

BARBY C and PEDERSEN M (2014) Allocating for impact. Social Investment Taskforce. URL: http://www.socialimpactinvestment.org/reports/AssetAllocationWGpaperFINAL.pdf (Accessed 4 April 2017). [ Links ]

BARUAH B (2007) Assessment of public-private-NGO partnerships: Water and sanitation services in slums. Nat. Resour. For. 31 (3) 226-237. https://doi.org/10.1111/j.1477-8947.2007.00153.x [ Links ]

BAYLISS K (2013) The financialization of water. Rev. Radical Polit. Econ. 46 (3) 292-307. https://doi.org/10.1177/0486613413506076 [ Links ]

BIGAS H (2012) The global water crisis: Addressing an urgent security issue. United Nations. URL: http://inweh.unu.edu/wp-content/uploads/2013/05/WaterSecurity_The-Global-Water-Crisis.pdf (Accessed 3 February 2017). [ Links ]

BRANDSTETTER L and LEHNER OM (2015) Opening the market for impact investments: The need for adapted portfolio tools. Entrepreneurship Res. J. 5 (2) 87-107. https://doi.org/10.1515/erj-2015-0003 [ Links ]

BRISCOE J (1999) The changing face of water infrastructure financing in developing countries. Int. J. Water Resour. Dev. 15 (3) 301-308. https://doi.org/10.1080/07900629948826 [ Links ]

BUGG-LEVINE A and GOLDSTEIN J (2009) Impact investing: Harnessing capital markets to solve problems at scale. Community Dev. Invest. Rev. 5 (2) 30-41. [ Links ]

BURAND D (2014) Resolving impact investment disputes: When doing good goes bad. J. Law Polic. 48 (1) 55-88. https://openscholarship.wustl.edu/law_journal_law_policy/vol48/iss1/9 [ Links ]

CHITONGE H (2013) Who will foot the bill? Water services infrastructure backlog in sub-Saharan Africa. J. Afr. Stud. Dev. 5 (7) 41-56. https://doi.org/10.5897/JASD13.001 [ Links ]

CLARKIN JE and CANGIONI CL (2016) Impact investing: A primer and review of the literature. J. Entrepreneurship Res. 6(2) 135-173. https://doi.org/10.1515/erj-2014-0011 [ Links ]

CHODA A and TELADIA M (2018) Conversations about measurement and evaluation in impact investing. Afr. Eval. J. 6 (2) 1-11. https://doi.org/10.4102/aej.v6i2.332 [ Links ]

CONNOR R (2016) Water and jobs. United Nations Educational, Scientific and Cultural Organization. URL: http://www.unesco.org/new/en/natural-sciences/environment/water/wwap/wwdr/2016-water-and-jobs/ (Accessed 5 June 2018). [ Links ]

COPPEL GP and SCHWARTZ K (2011) Water operator partnerships as a model to achieve the Millenium Development Goals for water supply? Lessons from four cities in Mozambique. Water SA 37 (4) 575-584. [ Links ]

COOK S, TJANDRAATMADJA G, HO A and SHARMA A (2009) Definition of decentralised systems in the South East Queensland context. Queensland: Urban Water Security Research Alliance. URL: http://www.urbanwateralliance.org.au/publications/uwsra-tr12.pdf (Accessed 8 June 2018). [ Links ]

DC WATER (2019) Green bonds. URL: https://www.dcwater.com/green-bonds (Accessed 9 October 2019). [ Links ]

DREXLER M, NOBLE A, CLASSON E and MERCEP E (2014) Charting the course: how mainstream investors can design visionary and pragmatic impact investing strategies. World Economic Forum. URL: http://www3.weforum.org/docs/WEF_ImpactInvesting_Report_ChartingTheCourse.pdf (Accessed 7 October 2017). [ Links ]

DWS (Department of Water and Sanitation, South Africa) (2018) National water and sanitation master plan. URL: http://www.dwa.gov.za/National%20Water%20and%20Sanitation%20Master%20Plan/Documents/20180329%20NWSMP%20Volume%202%20Final%20Draft%20(3.3).pdf (Accessed 5 December 2018). [ Links ]

DWS (Department of Water and Sanitation, South Africa) (2015) Strategic overview of the water sector in South Africa. [Pretoria]: The Department of Water and Sanitation. URL: http://nepadwatercoe.org/wp-content/uploads/Strategic-Overview-of-the-Water-Sector-in-South-Africa-2013.pdf (Accessed 12 July 2016). [ Links ]

DWS (Department of Water and Sanitation, South Africa) (2014) Blue Drop Report. URL: https://www.green-cape.co.za/assets/Water-Sector-Desk-Content/DWS-2014-Blue-Drop-report-national-overview-part-1-of-2-2016.pdf (Accessed 6 June 2017). [ Links ]

DWA (Department of Water Affairs, South Africa) (2013) National Water Resource Strategy. June 2013 Second Edition. Department of Water Affairs, Pretoria. URL: http://www.dwa.gov.za/documents/Other/Strategic%20Plan/NWRS2-Final-email-version.pdf (Accessed 6 June 2017). [ Links ]

ELO S and KYNGÄS H (2007) The qualitative content analysis process. J. Adv. Nurs. 62 (1) 107-115. doi:10.1111/j.1365-2648.2007.04569.x [ Links ]

EVANS M (2013) Meeting the challenge of impact investing: how can contracting practices secure social impact without sacrificing performance? J. Sustainable Fin. Invest. 3 (2) 138-154. https://doi.org/10.1080/20430795.2013.776260 [ Links ]

FANKHAUSER S and TEPIC S (2007) Can poor consumers pay for energy and water? An affordability analysis for transition countries. J. Energ. Polic. 35 (2) 1038-1049. https://doi.org/10.1016/j.enpol.2006.02.003 [ Links ]

FREIREICH J and FULTON K (2009) Investing for social and environmental impact: A design for catalyzing an emerging industry. Monitor Institute. URL: http://monitorinstitute.com/downloads/what-we-think/impact-investing/Impact_Investing.pdf (Accessed 11 November 2018). [ Links ]

GALADA HC, MONTALTO FA, GURIAN PL, SHELLER M, AYALEW TB and CONNOR SO (2014) Assessing preferences regarding centralized and decentralized water infrastructure in post-earthquake Leogane, Haiti. J. Earth Perspect. 1 (5) 1-13. https://doi.org/10.1186/2194-6434-1-5 [ Links ]

GANOULIS J, SKOULIKARIS H, and MONGET JM (2011) Water operator partnerships as a model to achieve the Millenium Development Goals for water supply? Lessons from four cities in Mozambique. Water SA37 (4) 575-584. http://dx.doi.org/10.4314/wsa.v37i4.17 [ Links ]

GIAMPORCARO S, DHLAMINI X and MAKHABANE T (2017) The African investing for impact barometer. 5th Edition. Bertha Centre, URL: http://www.gsb.uct.ac.za/files/ImpactBarometer5.pdf (Accessed 2 October 2019). [ Links ]

GLEICK PH (2002). Dirty water: Estimated deaths from water-related diseases 2000-2020. Pacific Institute. URL: http://www.pacinst.org/wp-content/uploads/sites/21/2013/02/water_related_deaths_report3.pdf (Accessed 3 June 2016). [ Links ]

GRIMSEY D and LEWIS MK (2002) Evaluating the risks of public private partnerships for infrastructure projects. Int. J. Project Manage. 20 (2) 107-118. https://doi.org/10.1016/S0263-7863(00)00040-5 [ Links ]

HALL D, LOBINA E and DE LA MOTTE R (2005) Public resistance to privatisation in water and energy. J. Dev. Pract. 15 (3-4) 286-301. https://doi.org/10.1080/09614520500076126 [ Links ]

HARJI K and JACKSON ET (2012) Accelerating impact: Achievements, challenges and what's next in building the impact investing industry. The Rockefeller Foundation. URL: https://www.rockefellerfoundation.org/app/uploads/Accelerating-Impact-Full-Summary.pdf (Accessed 23 June 2016). [ Links ]

HEBB T (2013) Impact investing and responsible investing: What does it mean? J. Sustainable Fin. Invest. 3 (2) 71-74. https://doi.org/10.1080/20430795.2013.776255 [ Links ]

HÖCHSTÄDTER AK and SCHECK B (2015) What's in a name: An analysis of impact investing understandings by academics and practitioners. J. Bus. Ethics 132 (2) 449-475. https://link.springer.com/article/10.1007/s10551-014-2327-0 [ Links ]

HSIEH H and SHANNON SE (2005) Three approaches to qualitative content analysis. J. Qual. Health Res. 15 (9) 1277-1288. doi:10.1177/1049732305276687 [ Links ]

IMPACT INVESTING SOUTH AFRICA (2019) URL: http://impactinvestingsouthafrica.co.za/ (Accessed 9 October 2019). [ Links ]

JACKSON ET (2013) Interrogating the theory of change: evaluating impact investing where it matters most. J. Sustainable Fin. Invest. 3 (2) 95-110. https://doi.org/10.1080/20430795.2013.776257 [ Links ]

JOHNSON DM, HOKANSON DR, ZHANG Q, CZUPINSKI KD and TANG J (2008) Feasibility of water purification technology in rural areas of developing countries. J. Environ. Manage. 88 (3) 416-427. https://doi.org/10.1016/j.jenvman.2007.03.002 [ Links ]

JOHNSON G, QUINN V and HENDERSON R (2018) Energy, water are 'huge' opportunities, says Ramaphosa investment envoy. Bloomberg, 19 October. URL: https://www.fin24.com/Economy/South-Africa/energy-water-are-huge-opportunities-says-ramaphosa-investment-envoy-20181019 (Accessed 2 October 2019). [ Links ]

MCGARRY M, MUGISHA S, HOANG-GIA L, UNHEIM P and MYLES M (2010) Water sector governance in Africa. African Development Bank. URL: https://www.afdb.org/fileadmin/uploads/afdb/Documents/Project-and-Operations/Vol_1_WATER_SECTOR_GOVERNANCE.pdf (Accessed 23 June 2016). [ Links ]

MILLSON C and ROUX A (2015) Water market intelligence report. Green Cape. URL: http://greencape.co.za/assets/Uploads/GreenCape-Market-Intelligence-Reports-Water.pdf (Accessed 1 February 2017). [ Links ]

MONTGOMERY MA and ELIMELECH M (2007) Water and sanitation in developing countries: Including health in the equation. J. Environ. Sci. Technol. 41 (1) 17-24. https://doi.org/10.1021/es072435t [ Links ]

MUDALIAR A and DITHRICH H (2019) Sizing the impact investing market. Global Impact Investment Network, April. URL: https://thegiin.org/assets/Sizing%20the%20Impact%20Investing%20Market_webfile.pdf (Accessed 2 October 2019). [ Links ]

MUDALIAR A, BASS R and DITHRICH H (2018) 2018 Annual Impact Investor Survey. 8th Edition. Global Impact Investment Network, June. URL: https://thegiin.org/assets/2018_GIIN_Annual_Impact_Investor_Survey_webfile.pdf (Accessed 2 October 2019). [ Links ]

MUDALIAR A, MOYNIHANS K, BASS R, ROBERTS A and DEMARSH N (2016) The landscape for impact investing in Southern Africa. Global Impact Investing Network. URL: https://thegiin.org/knowledge/publication/southern-africa-report (Accessed 5 March 2017). [ Links ]

NGOASONG M, PATON R and KORDA A (2015) Impact Investing and Inclusive Business Development in Africa: A research agenda. IKD Working Paper No. 76, The Open University, Milton Keynes. URL: https://oro.open.ac.uk/42157/1/ikd-working-paper-76.pdf (Accessed 18 November 2019). [ Links ]

OECD (Organization for Economic Cooperation and Development) (2011) Benefits of investing in water and sanitation: An OECD perspective. URL: http://www.oecd.org/berlin/47630231.pdf (Accessed 5 March 2017). [ Links ]

ORMISTON J, CHARLTON K, DONALD MS and SEYMOUR RG (2015) Overcoming the challenges of impact investing: Insights from leading investors. J. Soc. Entrepreneurship 6 (3) 1-27. https://doi.org/10.1080/19420676.2015.1049285 [ Links ]

OSUMANU IK (2008) Private sector participation in urban water and sanitation provision in Ghana: Experiences from the Tamale Metropolitan Area. J. Environ. Manage. 42 (1) 102-110. https://doi.org/10.1007/s00267-008-9107-5 [ Links ]

PETER-VARBANETS M, ZURBRUGG C, SWARTZ C and PRONK W (2009) Decentralized systems for potable water and the potential of membrane technology. J. Water Res. 43 (2) 245-265. https://doi.org/10.1016/j.watres.2008.10.030 [ Links ]

PRASAD N (2006) Privatisation results: Private sector participation in water services after 15 years. Dev. Polic. Rev. 24 (6) 669-692. https://doi.org/10.1111/j.1467-7679.2006.00353.x [ Links ]

PRÜSS A, KAY D, FEWTRELL L and BARTRAM J (2002) Estimating the burden of disease from water, sanitation, and hygiene at a global level. J. Environ. Health Perspect. 110 (5) 537-542. https://doi.org/10.1289/ehp.110-1240845 [ Links ]

RANGAN KV, APPLEBY S and MOON L (2011) The promise of impact investing. Harvard Business School, Background Note, (512-045). URL: http://psm.org.mx/wp-content/uploads/downloads/ThePromiseofImpactInvesting.pdf (Accessed 1 April 2017). [ Links ]

REEDER N (2014) The effect of social value measurement on impact investment decisions. J. Fin. Risk Perspect. 3 (3) 81-91. https://doi.org/10.1080/20430795.2015.1063977 [ Links ]

RINGWOOD F (2016) Getting water and wastewater back on track. Water Sanit. Afr. 11 (1) 4-5. URL: https://issuu.com/glen.t/docs/wasa_may_june_2016 (Accessed 3 June 2016). [ Links ]

ROBECOSAM (2015) Water: The market of the future. URL: http://www.robeco.com/images/RobecoSAM_Water_Study.pdf (Accessed 4 February 2017). [ Links ]

ROCA E, TULARAM GA and REZA R (2015) Fundamental signals of investment profitability in the global water industry. Int. J. Water 9 (4) 395-424. https://doi.org/10.1504/IJW.2015.072155 [ Links ]

ROCKEY N (2016) Impact investing in South Africa: What the future holds. Cape Town: Trialogue, 29 July, URL: http://trialogue.co.za/impact-investing-south-africa-future-holds/ (Accessed 31 March 2017). [ Links ]

RODRIGUEZ DJ, VAN DEN BERG C and MCMAHON A (2012) Investing in water infrastructure: Capital, operations and maintenance. The World Bank. URL: http://water.worldbank.org/sites/water.worldbank.org/files/publication/water-investing-water-infrastructure-capital-operations-maintenance.pdf (Accessed 11 August 2017). [ Links ]

RUITERS C (2013) Funding models for financing water infrastructure in South Africa: Framework and critical analysis of alternatives. Water SA 39 (2) 313-326. [ Links ]

RUITERS C and MATJI MP (2016) Public-private partnership conceptual framework and models for the funding and financing of water services infrastructure in municipalities from selected provinces in South Africa. Water SA 42 (2) 291-305. http://dx.doi.org/10.4314/wsa.v42i2.13 [ Links ]

SALES T (2015) Impact investment in Africa: Trends, constraints and opportunities. United Nations Development Programme. URL: http://www.undp.org/africa/privatesector (Accessed 28 September 2017). [ Links ]

SALTUK Y (2015) Eyes on the horizon: The impact investor survey. Global Impact Investment Network. URL: https://thegiin.org/knowledge/publication/eyes-on-the-horizon (Accessed 28 September 2017). [ Links ]

SALTUK Y, BOURI A, MUDALIAR A and PEASE M (2013) Perspectives on progress: The impact investor survey. Global Impact Investment Network. URL: https://thegiin.org/knowledge/publication/perspectives-on-progress (Accessed 28 September 2017). [ Links ]

SLAUGHTER S (2010) Improving the sustainability of water treatment systems: Opportunities for innovation. The Solutions J. 1 (3) 42-49. [ Links ]

STATSSA (2016) Community Survey. URL: http://cs2016.statssa.gov.za/wp-content/uploads/2016/07/NT-30-06-2016-RELEASE-for-CS-2016-_Statistical-releas_1-July-2016.pdf (Acccessed 4 November 2018). [ Links ]

SOUTH AFRICAN RESERVE BANK (2016) Guidelines: South African institutional investors. URL: https://www.resbank.co.za/RegulationAndSupervision/FinancialSurveillanceAndExchangeControl/Guidelines/Guidelines%20and%20public%20awareness/Guidelines%20South%20African%20Institutional%20Investors.pdf (Accessed 24 January 2017). [ Links ]

TECCO N (2008) Financially sustainable investments in developing countries water sectors: What conditions could promote private sector involvement? Int. Environ. Agreements: Polit. Law Econ. 8 (2) 129-142. https://link.springer.com/article/10.1007/s10784-008-9066-6 [ Links ]

THE GLOBAL RISKS REPORT 2017 (2017) World Economic Forum, 12th Edition. URL: http://www3.weforum.org/docs/GRR17_Report_web.pdf (Accessed 5 December 2018). [ Links ]

TURNER G (2013) Money down the drain: Getting a better deal for consumers of the water industry. Centre Forum. URL: http://bluegreenuk.com/references/government_institutional/Money%20Down%20the%20Drain.pdf (Accessed 17 June 2018). [ Links ]

TURTON A, DU PLESSIS A, WALKER J and SWANEPOEL S (2016) Running on empty: What business, government and citizens must do to confront South Africa's water crisis. ActionAid. URL: http://www.actionaid.org/sites/files/actionaid/running_on_empty_-_water_efficiency_report.pdf (Accessed 2 December 2018). [ Links ]

UNHRC (United Nations Human Rights Council) (2014) The human right to safe drinking water and sanitation. URL: http://ap.ohchr.org/documents/dpage_e.aspx?si=A/HRC/27/L.11/Rev.1 (Accessed 11 November 2016). [ Links ]

VAN VUUREN L (2014) Water loss: Are we wasting our way into a potential water crisis? The Water Wheel 13 (6) 34-37. https://journals.co.za/content/waterb/13/6/EJC162536 [ Links ]

WATKINS K (2006) Human development report 2006. United Nations Development Programme. URL: http://hdr.undp.org/sites/default/files/reports/267/hdr06-complete.pdf (Accessed 20 August 2018). [ Links ]

WHILEY A (2019) SFPUC seeks to widen investor base with latest wastewater infrastructure green bonds. Climate Bonds, 19 July. URL: https://www.climatebonds.net/2018/07/sfpuc-seeks-widen-investor-base-latest-wastewater-infrastructure-green-bonds (Accessed 9 October 2019). [ Links ]

WHO (World Health Organization) (2014) Investing in water and sanitation: Increasing access, reducing inequalities. URL: http://apps.who.int/iris/bitstream/10665/143953/2/WHO_FWC_WSH_14.01_eng.pdf (Accessed 4 April 2017). [ Links ]

WHO (World Health Organisation) (2006) Guidelines for drinking-water quality. URL: http://www.who.int/water_sanitation_health/dwq/gdwq0506.pdf (Accessed 4 April 2017). [ Links ]

WINPENNY J (2006) Financing water: Risks and opportunities. United Nations Environmental Programme Finance Initiative. URL: http://www.unepfi.org/fileadmin/documents/WRR_Issues_Paper.pdf (Accessed 3 March 2018). [ Links ]

WRC (Water Research Commission, South Africa) (2017) Water Directory. URL: http://www.wrc.org.za/Pages/Resources_waterdirectory.aspx (Accessed 16 June 2017). [ Links ]

ZOLNIKOV TR and SALAFIA EB (2016) Improved relationships in Eastern Kenya from water interventions and access to water. J. Health Psychol. 35 (3) 273-280. https://doi.org/10.1037/hea0000301 [ Links ]

Correspondence:

Correspondence:

S McCallum

steve@phanos.co.za

Received: 09 October 2018

Accepted: 10 December 2019

{kind=link}

{kind=link}