Services on Demand

Article

English (pdf)

English (pdf)

Article in xml format

Article in xml format Article references

Article references

Indicators

Related links

-

Cited by Google

Cited by Google -

Similars in Google

Similars in Google

Share

Permalink

PermalinkWater SA

On-line version ISSN 1816-7950

Print version ISSN 0378-4738

Water SA vol.39 n.2 Pretoria Jan. 2013

Funding models for financing water infrastructure in South Africa: Framework and critical analysis of alternatives

Cornelius RuitersI, II, *

IGraduate School of Business Leadership (SBL), University of South Africa, PO Box 392, UNISA, 0003, South Africa

IIDepartment of Water Affairs, National Water Resources Infrastructure, Private Bag X3'3, Pretoria, 0001, South Africa

ABSTRACT

The Government of South Africa has been the main provider of public infrastructure, particularly in the water sector. Government administration and institutional structures continue to shape and influence infrastructure investment. The South African constitutional system imposes unique complexities and constraints on infrastructure investment. The country experiences a serious backlog in water infrastructure investment for the development and management of water resources and water services. In 2011, this under-investment was estimated at more than R600 billion (600 x 109 ZAR: South African Rand). The national Government traditionally had a pivotal role in shaping water infrastructure investment. Government needs to find a solution to this backlog by putting in place new institutional structures and funding models for effective strategies leading to prompt water infrastructure provision. The research identified several funding models for financing water infrastructure development projects. The existing public provision model continues to characterise much of the publicly-provided water infrastructure in South Africa. These models see Government planning, installing and financing infrastructure with pricing at marginal costs or on a loss-making basis, with returns recovered through the taxation system. Nowadays, water infrastructure provision is split between fully-public and mixed ownership by water entities. Public-private partnerships (PPPs) in the water sector are not yet a reality.

Keywords: Department of Water Affairs, funding models, water infrastructure, National Treasury, operations and maintenance

Introduction

Many developing countries need water infrastructure to improve the livelihoods of their citizens and their quality of life, and South Africa is no exception. While there are many constraints to the delivery of water infrastructure, one of the most obvious factors that hampers delivery is project costs. Access to finance is the lifeblood of water infrastructure delivery, as is the packaging of the funding model for each project or groups of projects. Unfortunately, the cost of water infrastructure delivery continues to escalate to the point where many developing countries simply cannot afford such infrastructure.

The World Bank (2010) indicates that infrastructure in Africa lags behind other developing countries. Not only are infrastructure networks in Africa deficient in coverage but the price for the services provided is exceptionally high by global standards. Conservatively, sub-Saharan Africa has a combined infrastructure deficit for water and sanitation of an estimated $93 billion (bn.) annually (World Bank, 2010). Thus, meeting Africa's infrastructure needs calls for a substantial programme of infrastructure investment and maintenance. Some two-thirds of this estimate relate to capital expenditure, with the remaining third linked to operation and maintenance requirements (Brineco-Garmendia et al., 2008; World Bank, 2010).

The backlog of water infrastructure provision and poor access to service delivery for poor communities have forced a new approach for governments, industries, financiers and other role players. Delays escalate the eventual cost of infrastructure even more. Countries like South Africa have no choice but to look at innovative approaches to ensure that they eliminate their water infrastructure backlogs. Efficient and productive infrastructure services are important inputs for all industries and hence vital for economic growth and efficiency, productivity and competitiveness. Continued growth in infrastructure productivity will play a crucial role in managing the emerging challenge of South Africa's growing population (DBSA, 2009; DWAF, 2004, 2008).

Problem analysis and rationale

A number of organisations have attempted to delineate the extent of the water infrastructure deficit and requirements in

South Africa, with limited success (DWAF, 2004, 2007; DBSA, 2009; CSIR and CIDB, 2007; CSIR, 2010; World Bank, 1994, 2010; DWA, 2011a, b; SAICE, 2011). Their efforts all underscore the pressing need to address the following:

• A detailed inventory of both the extent and condition of public infrastructure tracked on a yearly basis to measure progress towards reducing the infrastructure deficit

• New funding models are needed to supplement existing funding techniques that can no longer fully fund both the rehabilitation of public infrastructure and the expansion required to accommodate growth

• Infrastructure maintenance is often one of the first cuts made in spending when budgets are tight

• Capital investment in infrastructure continues to be viewed as a high priority

• Constrained budgets at all levels of government seem to render even modest programmes and projects unaffordable

The Department of Water Affairs (DWA) traditionally funded water infrastructure development projects in South Africa (DWAF, 2004, 2008; DBSA, 2009; Moseki et al., 2011; Ruiters, 2011). With the growing demands on water infrastructure, no appropriate and alternative analyses and models have since been proposed and finalised. There is therefore pressure to develop alternative funding models for improved national water infrastructure management, particularly by investigating relevant funding models implemented in similar emerging economies, e.g. Brazil, Mexico, and India (World Bank, 1994; Mayle et al., 2001; Matta and Ashkenas, 2003).

Research is needed on alternative funding (business) models that ensure the sustainable availability of finances that is essential for the development of water infrastructure. Key influential factors include:

• The impact of the financial crisis and slow economic growth on public sector budgets; changes in allocations by the National Treasury

• The impact of the economic environment on private (corporate or financial) sector funding by reducing investment levels

• The efficiency of different funding (business) models

• Funding models emerging in other developing countries

METHODS

Some basic quantitative and qualitative methods were used for the analyses and models involved in this research, namely, surveys (questionnaires), interviews, documentation review (reports), observations, focus group sessions and case studies (Cranston, 2004; Coldwell and Herbst, 2004). The research involved both primary and secondary data collection (Tustin et al. 2005).

Data collection

An increasingly useful method of quantitative data collection in management research is to carry out a survey of a sample of a population in order to observe the relationship between a given set of variables (Taylor, 2002; Coldwell and Herbst, 2004). Research questions were used to direct the project. Through the survey questionnaire (primary data collection) and the review reports and documents (secondary data collection), alternative funding models were formulated.

The representative sample size for the study population of the research project was finite. Based on the sampling framework, the sample included:

• Interviews with representatives of financial institutions (commercial and development banks): the World Bank (WB), the Development Bank of Southern Africa (DBSA) and the African Development Bank (AfDB)

• Interviews with representatives of an investment corporation: the Industrial Development Corporation (IDC)

• Interviews with representatives of selected Government departments (national and provincial): the Department of Water Affairs (DWA), National Treasury (NT), the Department of Cooperative Governance and Traditional Affairs (DCoG), the Department of Trade and Industry (the DTI), the Department of Public Works (DPW), the Department of Public Enterprises (DPE), and the Department of Energy (DoE)

• Water institutions (entities) and/or agencies: the Trans-Caledon Water Authority (TCTA), Komati Basin Water Authority (KOBWA), catchment management agencies (CMAs), water boards (Rand Water, Umgeni Water, Sedibeng Water)

• Surveys with a representative sample of municipalities

The primary and secondary data collection methods for the research involved the following:

• Primary data: interviews, surveys (questionnaires and checklists) and a series of workshops. The sample included the following:

- Twenty-five individual interviews in national departments, funding agencies, regulatory agencies and local government. To establish the new paradigm of funding models, the questionnaire was used as a guide to obtain the research data. Questions were used to explore new issues that had not previously been considered in existing funding models.

- Five workshops and focus group discussions; the national and provincial workshops were attended by 46 participants in total.

- Respondent groups and national organisations, e.g. DWA, NT, the DPE, the DTI, DCoG, the DoE.

- Funding agencies - the DBSA, the AfDB, the IDC, the European Investment Bank and the WB.

- Water institutions - TCTA, water boards, KOBWA, and CMAs.

- Local government - the South African Local Government Association (SALGA), and local, district and metropolitan municipalities.

- Technical assistance providers - the European Union (EU), the WB and United States Agency for International Development (USAID).

• Secondary data: a list of options for funding water infrastructure had been developed to facilitate discussion by the DWA and other policy makers during deliberations. Reviewed reports relating to infrastructure needs and funding, and researched infrastructure funding activities in other countries, were studied. Compiled data on current expenditures and revenue patterns of the DWA (NT, 2011a), DCoG (NT, 2011b) state agencies and utilities, metropolitan municipalities, district and local municipalities (NT, 2011c), and private sector expenditure for water infrastructure, were examined. Revenue streams, local debt, expenditure restrictions, and other information relative to funding water infrastructure were reviewed.

Statistical analysis

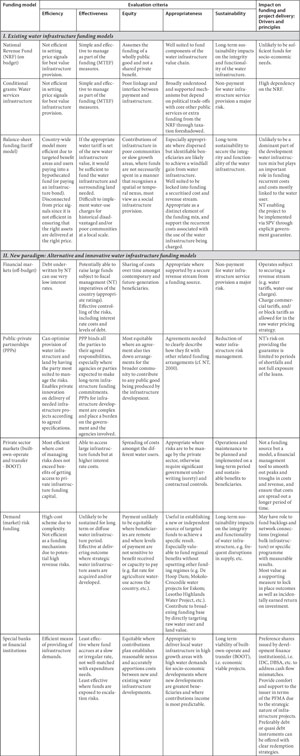

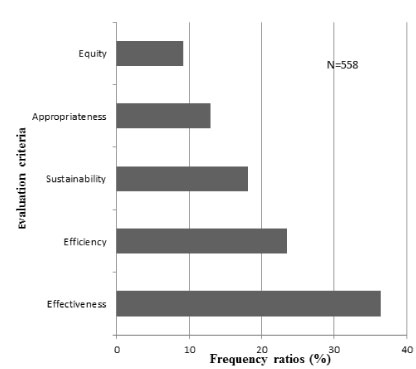

For the quantitative data analysis, i) nominal (categorical); and ii) ordinal (ranked) data (scales) types were considered and used, where appropriate (cf. Taylor, 2002; Coldwell and Herbst, 2004; Tustin et al., 2005). The statistical analysis for the research topic included the completeness of the survey data and helps to identify any information gaps or data inaccuracies (cf. Gilbert, 1987). However, since data were based on samples, they were subject to sampling error. Qualitative data were translated to quantitative data by ranking. Five qualitative evaluation criteria were identified from the primary data collection, i.e. equity, efficiency, appropriateness, effectiveness, and sustainability (cf. Appendix 1).

Descriptive statistics were used to summarise data sets into simpler and more understandable forms, such as the mean, median and standard deviations (SD). Inferential statistics were used to determine the level of uncertainty with which the findings should be treated. The non-parametric Spearman's rank correlation, rs, was used as a significance test statistic to test a hypothesis of no association between funding models and the evaluation criteria employed. Furthermore, from the sampled data the Chi-square test statistic (χ2) was used to test the Ho (null-hypothesis) to determine whether a dependency (or contingency) exists between the funding models and evaluation criteria through contingency tables.

RESULTS AND DISCUSSION

Water infrastructure funding models

The main purpose of current water infrastructure funding models is to provide guidance to managers on formalising and sourcing financing for the implementation and maintenance of such infrastructure. Funding models are not universal as the implementation environment of individual water infrastructure may differ, thus requiring adjustment to the models. However, conceptual funding models can be very important to water infrastructure development, since these can provide programme managers with answers to questions such as:

• Where and how does one seek funds?

• Over what period will the funds be disbursed?

• What are the effects of funding on pricing policies?

The answers to these questions are even more significant for South Africa and other developing countries. Such nations usually have very limited financial resources, poor capital markets and inadequate political governance structures (IIPF, 2001). Long-term capital financing models for water infrastructure implementation are therefore essential.

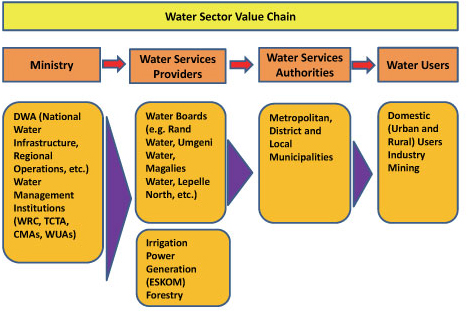

The water infrastructure value-chain is hierarchical (Fig. 1), based on administrative and/or political boundaries (cf. DWAF, 1997a, b, 1998). The hierarchy ranges from national to local levels with the responsibility for implementation varying from the government of the administrative boundaries to a combination of different aspects of the public sector. When designing funding models, there must thus be different implementation strategies for different levels of water infrastructure. The economic issues involved in the implementation of the water sector value-chain are guided by both strategic and operational management principles. Some challenging management issues that must be addressed include:

Figure 1

Hierarchical water sector value chain in South Africa

• The economic viability of water infrastructure (benefit-cost analysis)

• Strategic planning

• Financing and economic analysis

• Pricing policies

• The role of water infrastructure in the economy

• Economic issues associated with water infrastructure operations

Existing and alternative and innovative water infrastructure funding models

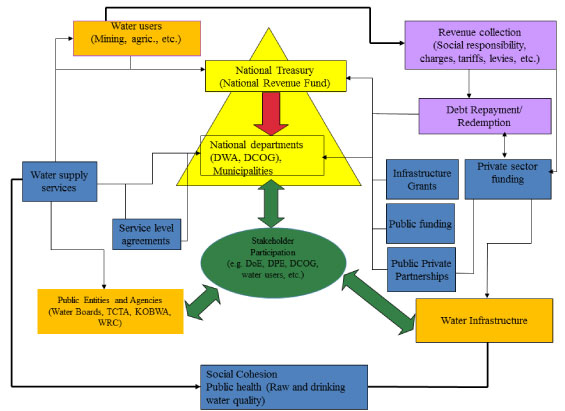

The framework for water infrastructure funding models was designed to meet the challenges presented by the current and growing imbalances that exist between the supply of and demand for water in South Africa (cf. Fig. 1). This requires a paradigm shift. Research identified existing funding models and others that would need a paradigm shift. Such models could constitute alternative and innovative water infrastructure funding models for the development of future water infrastructure projects in South Africa (Fig. 2). New or modified funding models could take the form of one or a combination of the following:

Figure 2

Main funding flows for water infrastructure in South Africa

• Existing water infrastructure funding models:

- Funding by the National Revenue Fund (on-budget)

- Funding through grants (Municipal Infrastructure Grant (MIG), Regional Bulk Infrastructure Grant (RBIG), Conditional Grants) from the National Revenue Fund (on-budget)

- Funding through the development of a tariff model (via balance sheet)

• New paradigm - Alternative and innovative water infrastructure models:

- Fundraising on financial markets (off-budget)

- Funding through public-private partnerships (PPPs) (hybrid of on- and off-budget)

- Funding from private sector markets (e.g. build-own-operate-transfer schemes)

- Demand risk funding model

- Financial institutions for funding water infrastructure.

Existing water infrastructure funding models

Funding by the National Revenue Fund (on-budget)

The DWA is primarily responsible for infrastructure development and has an allocated budget of R31.1 bn. from 2011/12 to 2013/14. (NT, 2011b). The DWA oversees and manages a total of 152 water and wastewater infrastructure projects at various levels of government throughout South Africa. The total estimated cost of these projects is R70.9 bn. (DWA, 2011a, b; NT, 2011b, c). The projects include new infrastructure and existing infrastructure being refurbished, rehabilitated, upgraded or maintained. Infrastructure spending includes direct expenditure on national water infrastructure projects and indirect expenditure on regional bulk water and wastewater infrastructure projects through transfers to water services authorities.

Currently, the DWA (through its supposedly 'ring-fenced' water trading entity) (NT, 1999) is not generating enough revenue due to price caps set by the water pricing strategy (DWAF, 2007), and has incurred consistent deficits annually. There is thus a cumulative backlog or deficit of R10.1 bn. for operations and maintenance of water resources infrastructure in the country (DWAF, 2008, 2011a).

Funding through grants for water services infrastructure

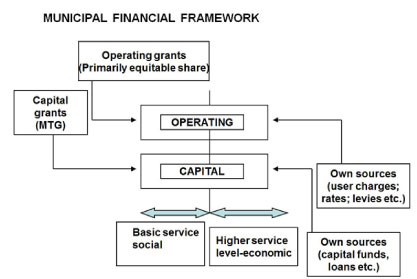

The results from the primary data collected indicate a concern over poor planning and adherence to a municipal financial framework model as required (Fig. 3). Ideally, the financial planning should include high-level planning for all infrastructure, drawing from the detailed sector infrastructure plans and providing a sense of what is possible within financial and institutional constraints.

Figure 3

Municipal financial framework for water infrastructure at local government level (municipalities) in South Africa

All sources show the broad extent to which many households lack basic services (Table 1). Water services and sanitation (wastewater) are the biggest concern in terms of backlogs in 3 provinces, i.e. Eastern Cape, KwaZulu-Natal and Limpopo. For these backlogs to be addressed or eradicated, an alternative or a combination of funding models is needed. The total capital required (for new as well as maintaining and upgrading of existing infrastructure) to meet current backlogs and projected future demand is estimated at R970 bn. over 10 years, with approximately R265 bn. required for water services infrastructure backlogs alone (including provision for escalation) (DCoG, 2010).

Using the municipal infrastructure investment framework (MIIF) models it was possible to quantify funding requirements for the different services for municipalities (high, medium and low-capacity categories) (Table 1). The MIIF aimed to assess the required levels of capital and operating expenditure to meet 2014 service targets against the available finance. The estimated capital requirement for 2010/2011 (Year 1) alone was some R83.424 bn. compared to the current budget of R44.6 bn. and an allocated Municipal Infrastructure Grant (MIG) of R12.529 bn. (cf. Table 1) (DCoG, 2010; NT, 2011a). These figures include the capital investment required for water services infrastructure, estimated in Year 1 to be R22.815 bn., to meet this 10-year target (DCoG, 2010). Operating expenditure was calculated in the MIIF as the amount required to adequately manage water services infrastructure. The total required operating expenditure for all services infrastructure in all municipalities was calculated to be R2 726 bn. over 10 years (DCoG, 2010). These figures include the operating capital investment required for water services infrastructure, estimated in Year 1 to meet this 10-year target to be R31.168 bn., compared to the current budget of R176.534 bn. and an estimated operating revenue of R183.301 bn. (Table 1) (DCoG, 2010).

The data, using Year 1, showed that low-capacity municipalities require more substantial capital for water infrastructure rehabilitation than for new infrastructure. At the other end of the spectrum, high-capacity municipalities require a focus on new infrastructure (mainly economic infrastructure, e.g. water services, urban transport systems) as well as rehabilitation (mainly water supply systems and roads) (DCoG, 2010). Municipal budgets target a total income of more than R24 bn., of which R19.5 bn. is collected from water supply and R4.6 bn. from sanitation services (DCoG, 2010). Water services generated a net surplus of about R4.1 bn., which is used to cross-subsidise other services; in a few municipalities this is used for the recapitalisation of water services assets (DCoG, 2010). About 55% of the operating expenditure (R12 bn.) is used in the 6 metropolitan municipalities; of the remainder, R7 bn. is used by local municipalities and about R2 bn. by district municipalities (DCoG, 2010).

The municipal infrastructure grant (MIG) transfer to municipalities is R40.04 bn. over the MTEF period, with a significant increase from R11.44 bn. (adjusted appropriation) in the financial year 2011/12 to R14.7 bn. in 2012/13 (NT, 2011b; NT, 2011c). This represents a mean annual allocation of R13.4 bn., with a mean annual increase rate of 15.7% (SD ±7.7%) (NT, 2011b, c). In addition, there is the water services regional bulk infrastructure grant which required that 'enabling infrastructure' connect water resources over vast distances with bulk and reticulation systems, for which R9.002 bn. has been allocated over the MTEF period (DWA, 2012). However, it is estimated that total funding of R171 bn. is needed for all regional bulk infrastructure (including provision for escalation) in the country (DWA, 2012).

Balance-sheet funding (tariff model)

The economic value of water refers to the assessment of the economic benefits typically achieved through the use of water in different sectors of the economy. From an economic perspective, however, it is important that the value of water derived from its application for economic production should be more than the cost of water supply for that particular use. This does not, however, apply to the primary uses of water such as basic human needs.

Charges for achieving an equitable and efficient allocation of water (economic charge) must be implemented. An administratively-determined charge can be used in water-stressed catchments to provide an incentive for existing users to increase economic efficiency. Such a charge will be based on the opportunity cost of water as determined by prevailing trading transactions, but will be capped to the level of the return-on-assets-charge for the relevant scheme or system (DWAF, 2007).

In the development of any tariff model, the marginal cost of water must be understood. Thus, the following detail for each water infrastructure scheme is important (DWAF, 2007):

• Total fixed costs per scheme (return-on-investment + depreciation charges) or finance charges

• Total variable costs per scheme (operations and maintenance charges)

• Volumes sold from each scheme

• Projected future demand

• Cost of infrastructure development and expansion

The economic use of water is charged at the full cost of supplying water to the users over a 20-year term (DWAF, 2007). It requires the payment of a capital unit charge (CUC) to repay the off-budget loan funding. This CUC is normally payable on a take-or-pay basis from the water infrastructure development projects when commissioned on the full licensed volume of each off-taker. Users agree upfront to pay on their license volume and not on actual demand for water, to increase the bankability of the revenue stream. A systems tariff will apply where all commercial users will pay the same tariff. If the project's full funding is provided by National Treasury, the economic cost of water for the scheme to be paid back to government could be interest-free and will then be reduced substantially.

New paradigm: Alternative and innovative water infrastructure funding models

The research results indicate a few alternatives to consider to make the water infrastructure development projects bankable and to ensure implementation (cf. Appendix 1). These options seek to provide clarity on the form of credit enhancement with the related impact on government (cf. Lang and Merion, 1993; AASHTO, 1995; World Bank, 2010).

The funding models in respect of the government guarantee suggest a paradigm shift in the structure of a traditional guarantee model, in that the financial exposure will be limited to the shortfall in the income stream from the users as a result of timing mismatches (cf. AASHTO, 1995; Goodman and Hastak, 2006; World Bank, 2010). The research results showed that the characteristics of a good business model, which can determine whether it will be effective, depend on the following criteria (Casadesus-Masanell and Ricart, 2011; cf. Figs. 6-8; Appendix 1):

Figure 4

Frequency ratios (%) for the evaluation criteria for alternative and innovative funding models for water infrastructure in South Africa

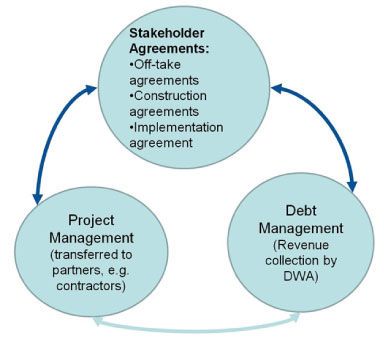

Figure 5

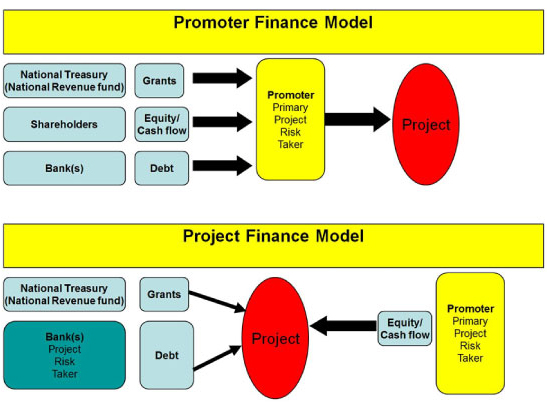

Promoter finance and finance models for PPPs for water infrastructure development in South Africa

Figure 6

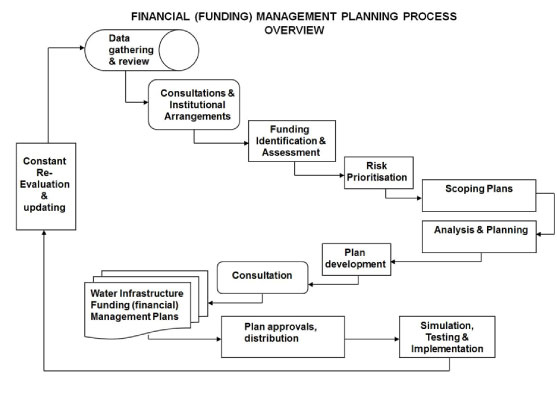

Proposed water infrastructure funding flow process in South Africa

Figure 7

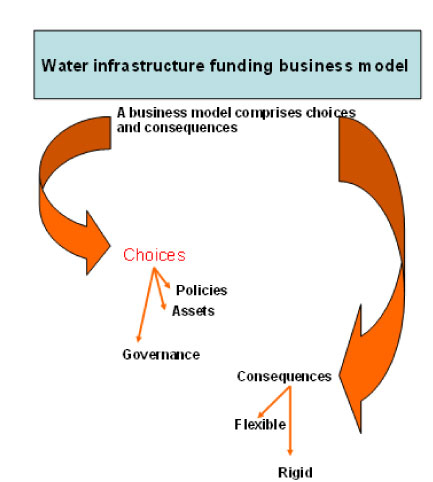

Possible funding business model for water infrastructure (after Casadesus-Masanell and Ricart, 2011)

Figure 8

Risk model for water infrastructure development projects in South Africa

• It must be aligned with organisational, company or institutional goals. The funding model chosen should enable an organisation to achieve its goals.

• It should be self-reinforcing. The choices made while creating a funding model should complement one another.

• It should be robust. A good model should be able to sustain its effectiveness over time.

The data obtained confirmed that Government (private sector may have vested interests) must embrace and lead innovative financing as the preferred alternative to delivering certain large public water infrastructure projects (Figs. 2, 4-7). The Spearman rank correlation r , indicates that there is no association between the ranking of the financial models and the ranking of the data (ratios) (rs = 0.2; p<0.05; n = 5), thus the H0 is accepted for α = 0.05 of no association between the two populations (evaluation criteria and the frequency ratios) (Fig. 4). In addition, the H0 that the funding models and the evaluation criteria are dependent is rejected with χ2 > 41.3372, with α=0.05 and d.f. = 8. Because the value of the χ2 test statistic (χ2 = 141.96) exceeds the critical value of χ2, the H0 (null hypothesis) is rejected at α=0.05 level of significance (Fig. 4).

Three innovative financing alternatives allow the public and private sectors to forge efficient partnerships and enable a robust pipeline of economic water infrastructure to be built around the country without delay (Figs. 6 and 7). Importantly, these alternatives allow the public sector to provide capital that can also earn a potential return and is recycled (cf. Lang and Merion, 1993; AASHTO, 1995; Goodman and Hastak, 2006; Figs. 2, 5-8):

• Alternative 1: Public sector subordinated treasury notes or bonds

Aside from mitigation of demand risk, one of the key considerations in financing economic infrastructure projects is how public funding can best be structured alongside private sector capital (Figs. 2, 6, 8). Innovative funding solutions will ensure a true public/private sector partnership with consideration of how public sector capital is secured and ranked alongside private sector debt and equity (Figs. 2, 6, 8). More complex funding instruments should be used rather than simple upside sharing of revenue (Figs. 6, 7). One way to achieve this is through government-issued subordinated notes or bonds.

• Alternative 2: Public sector development entities (state-owned enterprises)

An alternative option would be for government to take responsibility for the project during the development stage (Figs. 2, 6-8). The intention is to refinance the project with private sector capital after it is built and revenue streams have been proven. Projects could be structured along commercial lines aiming to replicate the private sector (Figs. 2, 6-8). Water-use charges would be set to provide a viable finance plan (cf. Figs. 2, 6-8).

• Alternative 3: Public sector-supported super fund vehicles

The third alternative aims to tap into superannuation funds. Due to their long-term investment horizon and conservative risk profile, superannuation funds are the logical long-term investments for 'economic' water infrastructure assets. The public sector might co-invest equity alongside superannuation funds and provide revenue guarantees over the asset for a specific period of time (Figs. 6-8). The guarantee would fall away once certain revenue thresholds have been met, which could be 3 to 4 years after the new infrastructure has been opened. Here, the public sector is simply providing a bridge for private sector finance (Fig. 2).

Raising funds on the financial markets (off-budget)

Local capital markets are a major source of water infrastructure finance in South Africa. Local water infrastructure finance consists primarily of commercial bank lending, some corporate bonds, stock exchange issues (commercial paper), and a nascent entry of institutional investors (e.g. Public Investment Corporation (PIC), Government Employees Pension Fund (GEF), private pension funds, etc.). Currently, special purpose vehicles (SPVs) are raising funds from the financial markets for financing of bankable mega-water resource infrastructure projects, i.e. the TCTA, and the Komati Basin Water Authority (KOBWA). In total, R32.2 bn. has been raised from the capital and financial markets for the implementation of water infrastructure projects (TCTA, 2012; NT, 2012). The money (capital) is raised in the financial markets by issuing interest-bearing South African Government bonds via the National Treasury and by providing explicit guarantees. Furthermore, local government, i.e. mostly metropolitan municipalities or cities do issue municipal bonds to generate money for day-to-day operations and specific municipal projects such as infrastructure development.

The SPVs derive their revenue from the sale of raw water and the provision of advisory services to the water sector to redeem the capital investment costs. Revenue collection, by the 'ring-fenced water trading entity' of the DWA for the SPVs, currently stands at R3.6 bn. (for raw water sales only) and will marginally increase to R3.7 bn. in the 2013/14 financial year. The marginal increase masks some important developments in the work of the SPV. Revenue collected by water boards comes mainly from the sales of bulk potable water (water services) to water services authorities in their areas (DWAF, 2007).

Funding through public-private partnerships (PPPs)

Very limited public-private partnership initiatives have been used for the implementation of water infrastructure development projects. While municipalities are responsible for the provision of these services, there are important delivery partners which have been allocated responsibility for the actual delivery of these services. There are a few contracts with private operators for service provision, for example, concessions in Mbombela (Nelspruit) Municipality; a lease-type contract in Lukanji (Queenstown) Municipality; and an operating contract in uThungulu District Municipality for its area (DCoG, 2010). Recently, an institutional framework was developed to guide this type of development (NT, 2000). The use of this framework is essential in including the private sector in the implementation of water infrastructure development projects (NT, 2000). More importantly, this would also help to convince the public that private involvement or other forms of non-traditional funding or delivery are appropriate. There have been attempts to involve the private sector in the creation of public infrastructure but not with the commitment, consistency, or legislative protection that would encourage and protect private sector investment and encourage long-term partnerships (DCoG, 2010).

Other governments (Australia, Brazil, Canada, Mexico, Finland, UK, Malaysia, Indonesia, Thailand, Philippine, etc.) have managed to establish mechanisms and controls that allow the involvement of the private sector in the provision of some public infrastructure (RCCAO, 2006; Sihombing, 2008; Rowey, 2009; Laitinen et al., 2010; Leach, 2010). Control and public benefit are secured through legislation and a strict method of measuring the benefits of the non-traditional approach. Meaningful involvement by the private sector is, however, not automatic. Experience in other countries has shown that important prerequisites for such financing are political commitment; enabling legislation that can be readily applied; an evaluation framework; expertise; project prioritisation; risk management; and standardisation (RCCAO, 2006; Sihombing, 2008; Rowey, 2009; Laitinen et al., 2010; Leach, 2010).

Funding through private sector markets

Customers are wary of full-scale water privatisation; thus, a well-structured privatisation model could be part of the water infrastructure development, operations and maintenance solutions (Figs. 2, 6). Often customers fear that water charges would become 'another tax' with no improvement in the quantity and quality of the water infrastructure. Customers would want to see clear incentives and commitments for extra capacity.

While major investment of over R600 bn. is necessary to close the infrastructure deficit gap, significant institutional funds appear to be available for the right type of projects. A more proactive approach to funding would be to table all future financing requirements in advance, i.e. 1-3 years, with funds raised to match those maturities. Furthermore, in order to promote interest in the commercial paper programme, funds could be raised ahead of any financing requirement and invested until the specific need for funding arises. Consequently, SPVs (e.g. TCTA) can maintain a strong presence in the commercial paper market and be able to secure funding at competitive prices. However, global limits are already being set by National Treasury and govern the total limit of gross liabilities of water infrastructure projects. The individual limit is set internally from time to time when markets are suited to move from one instrument to the other. The borrowing limits for bonds are offset from the available utilisation on the bond as approved. The current CPI-adjusted issued maturities for TCTA are R6.3 bn. (variable interest rate instrument), with a nominal maturity of R3.525 bn., and the figure is R16.146 bn. (fixed interest rate instruments) for the commercial paper (TCTA, 2012). The limits for commercial paper and the individual bonds are the authorised limits for utilisation of the individual bonds and commercial paper, R30.5 bn. with a total borrowing authority global limit of R20.55 bn. Utilisation of the commercial paper and bonds is capped by the total borrowing authority limit. South Africa's largest public sector pension fund, e.g. Government Employees Pension Fund (GEPF) managed by the Public Investment Corporation (PIC), could announce a major shift in its investment policy away from equities towards infrastructure as an asset class. However, the scale of water sector related bonds and commercial paper is small in relation to the scale of pension funds, which is perhaps most contentious and opportunistic.

Harnessing the significant potential for capital markets to finance water infrastructure, particularly local bond markets, is contingent on their strengthening and further development. It is, thus, also contingent on further reforms, especially those that would deepen the local institutional investor base. Well-functioning and appropriately institutional investors (pension funds, insurance companies, etc.) would be natural sources of long financing for water infrastructure because liabilities would better match the longer terms of water infrastructure projects (cf. Inderst, 2009; World Bank, 2010; TCTA, 2012). Private pension providers must begin to emerge with a shift from defined-benefit to defined-contribution schemes, viewed as less costly, more transparent, and easier to manage. Moreover, South African local institutional investors (i.e. pension funds) must take a more diversified portfolio approach to asset allocation.

Demand (market) risk funding model

If finance were not forthcoming for national water infrastructure, there would be a number of associated risks and actions. The finance available should be used to first augment, in the most economic manner, rehabilitation and refurbishment that have the highest economic benefit, and then be used for future investment.

If tariffs were not tapered rapidly to a reasonable economic level with explicit subsidies and social pricing as inherent ingredients, operations and maintenance will continue to decline and stagnate. This will have serious consequences for the population's health and livelihoods, whether they be agricultural, industrial or other.

The first challenge is to explore the availability of finance from traditional sources, i.e. NT, and through off-balance sheet funding via SPVs. The second challenge is to see whether a further line of finance to be run directly by the DWA can be provided by the NT. The third challenge is to explore other off-balance sheet sources of finance, both from development and/ or investments agencies and the private sector. The fourth challenge is to obtain political support for tariff change improvements to the regulatory framework, and the recognition that enhanced tariffs applied equitably are essential.

These types of water infrastructure projects are where the private sector bears market (demand) risk and revenues are typically derived directly from the users of the infrastructure rather than government (cf. Fig. 8). Market risk, the fair value or cash flows of a financial instrument, will fluctuate due to change in market prices and reflects currency risk, interest rate risk, and other price risks. Financial activities for the implementation of water infrastructure projects are exposed primarily to the financial risks of changes in foreign currency exchange rates and interest rates which can be managed through redemption strategies. Therefore, a variety of derivative financial instruments must be entered into to manage its exposure to foreign currency risk (exchange rate fluctuations) and interest rate risk. Interest rate fluctuations can negatively impact debt exposures, including the re-pricing of floating rate debt obligations and the short-term rollover of maturing debt. But, since managing interest rate risk is more complex than increasing or decreasing the duration of liabilities mismatch, duration matching is used as a guiding principle and can be used in conjunction with other interest rate risk mitigation measures such as the sensitivity of the debt curve to changes in the capital structure, water demand, inflation and interest rates. Hence, interest rate risk is managed by establishing risk-sensitive funding strategies which apply concepts such as duration and capital structure in the long-term, and redemption, derivative and other hedging instruments in the short-term. Furthermore, any exposure associated to both refinancing and re-pricing risk associated with large maturities (bonds and commercial paper) can be minimised by matching its assets and liabilities. Whereas minimising credit risk, the risk that counterparty will default on its contractual obligations resulting in financial loss is critical, by only dealing with creditworthy counterparties and obtaining sufficient collateral where appropriate. This information is supplied by independent rating agencies where available or, if not available, uses other publicly available financial information and trading records to rate its major customers.

This approach to sourcing (capital) revenue differs markedly from so-called social infrastructure projects (water services supplied to communities) where the government retains demand risk and provides revenue directly. The SPVs as multi-disciplinary organisations specialising in project financing and implementation are specialised liability management entities. Their mandate is to raise off-budget finance for the development of bulk raw water infrastructure which delivers water for industries and consumers in a cost-effective manner (Fig. 8). The impact of a more risk-averse approach will undoubtedly constrain the amount of private sector capital for funding water infrastructure. This is essentially so if the funding model were to be undertaken with the projected water revenue stream providing the source of repayment. The inevitable end result would be that government would need to supplement private sector capital. This has already been implemented on completed water infrastructure deals, where the Government contributed funding for part of the capital works. This potentially transforms the risk profile for government and additional safeguards are required to avoid the public sector co-investing in poorly-structured private projects or taking on unreasonable termination liabilities.

Financial institutions for financing of water infrastructure

There is an urgent need to at least redefine the mandate of the Development Bank of Southern Africa (DBSA) as the financial institution to finance critical national infrastructure, such as water infrastructure projects. Such a national infrastructure institution should help finance transformative infrastructure projects of national strategic importance (Rowey, 2009; Tyson, 2011). Properly designed and governed, the DBSA would assist in overcoming weaknesses in the current selection of infrastructure projects by removing funding decisions from politically-volatile appropriation processes (Rowey, 2009; Tyson, 2011). Investments could be selected after independent and transparent cost-benefit analysis has been done by objective experts.

Relevant financial institutions could provide the most appropriate form of financing for each project, drawing on a flexible set of tools, such as direct loans, loan guarantees, and grants, and issuing medium and long-term tax-free bonds for specific or dedicated water infrastructure funding. However, this is very dependent on market conditions; research should be conducted on present and future market conditions before pursuing this option as well as interest subsidies for possible 'Build South African Bonds' (Lamb, 1984; Rowey, 2009; Tyson, 2011). Such a bank could be given the authority to form partnerships with private investors, which could increase funding for infrastructure investments and foster efficiency in project selection, operation and maintenance. That would enable the bank to tap into the significant pools of long-term private capital in pension funds and dedicated infrastructure equity funds. The concept of the DBSA fulfilling the role of an infrastructure bank with a pool of funds for low-interest loans has been endorsed already, e.g. in the form of infrastructure loans from the DBSA to municipalities in South Africa (cf. Lamb, 1984; Urban Logic, 2000; DBSA, 2012). Other measures considered by Lamb (1984) involve privatisation, and would include sale-leasebacks and service contracts. Yet other approaches could be liquidation or recapitalisation of non-public-purpose or marginally-public-purpose facilities to private ownership (cf. Fraser et al., 2000). Lastly, the creation of water infrastructure as a service entity, could lead to issuing of 'Build South African Bonds' in this new organisation on the stock exchange or through private subscriptions, accessing of capital markets for specific and dedicated financial assistance such as revolving loans and other similar debt structures, and possible application of incentives such as matching ratios to stimulate investment (cf. Urban Logic, 2000; Nebert, 2001). The central government would match (according to the specified ratio) the amount of funds invested in the water infrastructure by other groups. This type of venture would encourage governments to seek out investment for their water infrastructure so that they can access funds (cf. Urban Logic, 2000; Nebert, 2001; Rowey, 2009).

Comparative analysis: Solving the water infrastructure funding problem

A solution to the funding of water infrastructure could be a combination of the models discussed. Some of these models exist, but are fragmented and need serious review and reconfiguration. If water infrastructure is said to be an essential part of the nation's basis for economic, social and environmental development, funding models should be in place, similar to existing funding models for other capital infrastructure development, e.g. electricity, energy, transportation and telecommunications. Combining the models would depend on the government structure, financial markets and the political climate, to name but a few (cf. Appendix 1). If water infrastructure is classified as an essential part of a nation's capital infrastructure producing goods for public benefits, models should provide favourable alternatives for obtaining capital financing (cf. Appendix 1). These models can be consolidated to create a water infrastructure funding model pool (Fig. 2, 6-8; cf. Appendix 1). From this pool, suitable model(s) can be selected for water infrastructure financing based on the implementation environment (Figs. 2, 6-8; cf. Appendix 1).

The following financing and funding imperatives have been identified (cf. Fig. 2, 6-8; Appendix 1):

• Funding through reserves or equity

• Debt finance

• Co-funding

• Grant funding (MIG; RBIG; conditional grants; equitable share; maintenance grant)

• Water-user funding

While the required investment appears daunting, it could be achieved through an approach consideration of the following considered possibilities:

• Infrastructure 1 - Change existing fiscal plans that ring-fence government departments such as the DWA so that the only area of public spending to be ring-fenced is infrastructure investment, because of its positive impact on the supply-side of the economy and long-term GDP growth.

• Infrastructure 2 - Commit to a new strategic investment fund (set at 1.5% of GDP per annum) earmarked for the most strategic water infrastructure projects, and funded from savings on non-capital expenditure elsewhere in the public sector. The fund could be used to pursue many small infrastructure investments, as they would add up and have an impact of strategic significance.

• Infrastructure 3 - Critical to success will be the ability to leverage private investment on the back of the public sector and accelerated planning approval through the National

Planning Commission. The key to maximising investment will be the policy environment.

• Infrastructure 4 - Ring-fence the future proceeds from privatised revenue collection and earmark these for infrastructure investment. Potential revenue could be more than R6 bn.. Other potential funding sources could include privatisation of the water infrastructure network.

• Infrastructure 5 - Do not be compelled to identify every possible funding source at the outset.

These mechanisms could be introduced since the return-on-asset (ROA) investment route is not sufficient and the DWA has not been able to create enough reserves for capital expenditure on new water infrastructure and for operations and maintenance of existing water infrastructure (cf. Appendix 1). The first task would be to overcome the highly-visible and well-documented backlog in existing water infrastructure. The second task is to establish new, forward-looking and resilient institutional frameworks to facilitate timely infrastructure investment by integrating the full range of strategic planning, management and technical expertise in South Africa's public and private sectors.

After considering various financing and procurement options, the government determined that alternative financing and procurement (AFP) will allow South Africa to finance and implement many large infrastructure projects better and sooner, without tying up public funds that can be used for other purposes. Construction work could thus be financed and undertaken by the private sector, which will assume the financial risks of ensuring that the project is finished on time and on budget. The completed facility would be publicly-owned, publicly-controlled and publicly accountable. AFP models can be selected for given projects, based on the principles articulated in the national water resource strategy (NWRS; DWAF, 2004) framework for planning, financing and procuring public infrastructure. The government has also made it clear that it is committed to keeping core public services such as water and sewage treatment facilities under public ownership and control.

In terms of general infrastructure provision, significant changes started in the 1990s with corporatisation and agentisation of water infrastructure (Eberhard, 1999; Hazelton, 1998; Palmer Development Group, 1998, 2000, 2002; Hollingworth et al., 1994). Nowadays, infrastructure is split between fully public (mostly water, ports, airports, electricity), fully private (some energy, gas pipelines, telecommunications) and mixed ownership (e.g. telecommunications). The trend towards private provision of infrastructure has been reinforced by the emergence of significant capital availability in South Africa for infrastructure investment resulting from financial deregulation and South Africa's superannuation policies in the post-1994 era. Private direct investment in new infrastructure has significant potential, while governments continue to avoid or delay investment in new capacity. Water infrastructure offers the potential for private sector investment, especially if network access and pricing outcomes are resolved. The supply of significant new infrastructure via PPP frameworks seems most likely. Further innovation in infrastructure investment, including reducing the gap between public- and private-sector capital, is required. Complex issues of pricing, access, public policy and regulation, risk-sharing, tendering processes, taxation and governance have arisen as key challenges that will influence whether private provision of infrastructure can grow as a viable new model in South Africa (cf. Appendix 1). Sustainability has introduced a further dimension into the calculus of infrastructure provision (cf. Appendix 1). A framework that takes account of environmental and social aspects, as well as of economics, is now widely accepted as necessary. Long and costly bureaucratic processes are a frequent complaint of private-sector participants involved with infrastructure provision and financing. South Africa has an impressive and world-class range of managerial, financial and engineering skills in the private sector. These should be deployed together with public-sector expertise, into the national task of infrastructure provision.

South Africa has to benchmark and align the funding models for the financing of water infrastructure development projects with international best practices and guidelines (i.e. the WB, the AfDB, the Asian Development Bank (ADB), the European Investment Bank (EIB), etc.). It is recommended that South Africa should increase the assistance available through existing or new infrastructure grant and loan programmes, and provide greater fiscal flexibility with existing resources. South Africa has well-established policies and procedures, not only to select projects where innovative financing procedures could apply, but also to ensure that the 'deal' meets established project guidelines (Hollingworth et al., 1994; Hazelton, 1998; Palmer Development Group, 1998, 2000, 2002; Eberhard, 1999; Conningarth Economists, 2002; DWAF, 2003, 2004, 2007, 2008; Matthews, 2009). Thus, annual investment in public infrastructure must be funded in a non-traditional manner involving private sector financing.

Other emerging, developing and developed countries face similar, significant infrastructure funding deficits (Mayle et al., 2001; Matta and Ashkenas, 2003; RCCAO, 2006; Sagar, 2006; Sihombing, 2008; Rowey, 2009; Laitinen et al., 2010; Leach, 2010; World Bank, 2010; Tyson, 2011). Some have found acceptable methods or models of integrating private funds and initiatives to help pay for some of their public infrastructure requirements. South Africa can learn from the experiences of these countries.

Innovative approaches to financing can be considered only where definite value-for-money can be demonstrated, but not at the expense of existing public sector funding. Innovative financing models can be considered only under the following conditions:

• The private sector has to be experienced and there has to be formal, demonstrated value-for-money.

• Expected service outputs must be clearly defined and measured by third-party performance audits.

• It must be demonstrated that involving the private sector as part of an innovative financing scheme is the best procurement model, given other possible options.

• It must be possible to life-cycle cost the service over on extended period of time.

• Projects must be of a sufficient size and the scale of transaction costs must not be disproportionately large.

Conclusions

The South African Government has recognised that new delivery models are required to close the infrastructure funding gap to extend access to water and sanitation to communities who have long been neglected and are often far from existing infrastructure. Over the past few years, South Africa has made impressive strides in the right direction with its New Growth Path (NGP), new investment strategies and initiatives to encourage investment in public infrastructure, e.g. National Water Resource Strategy (NWRS), Water for Growth and Development (WfGD; DWAF, 2008), and the Strategic

Framework for Water Services (SFWS) for planning, financing and procuring public infrastructure. The objectives are:

• long-term growth and infrastructure renewal planning across the provinces;

• determining project priorities;

• utilising the expertise in the DWA to manage the implementation of AFP projects; and

• committing to infrastructure expenditures in the MTEF budget.

With overwhelming demand for the provision of regional bulk infrastructure assets to be accelerated around the country, implementation of any of these models will go a long way toward leveraging private sector investment in economic infrastructure assets and allowing the government to recycle its capital and share in the future recovery of financial markets, while at the same time addressing demand risk.

South Africa needs to retain the 'user pays' principle by charging water users for the use of infrastructure. This provides the benefit of enabling non-government funding to be raised, but it also leads to proper market-based pricing signals being employed, which drives more efficient utilisation of infrastructure. Moreover, there is more rigorous due diligence on projects, as well as a more detailed, shared understanding between the public and private sectors of the key drivers of demand. This will help to encourage the development of infrastructure assets on a true PPP basis. Although water-user fees of various types partially fund some of South Africa's public infrastructure, the link between costs and use is not well established in the public's mind. Reinforcing awareness of this relationship could lead to conservation measures and would also make it much easier to create stable funding vehicles that do not depend solely on general tax revenues. To encourage funding vehicles that use private funds to invest in South Africa, recent initiatives (e.g. Berg River Dam, Spring Grove Dam, Mokolo-Crocodile Water Augmentation Project, etc.) should be continued. The government should also create a stable investment environment through political commitment (but not interference), consistency, a regular and predictable flow of deals, and suitable framing legislation. This will ensure life-cycle costing and the establishment of true user costs. A reasonable transfer of risk to the public sector should be a minimum government requirement of any partnership with the private sector. Third-party performance audits are also required for successful partnering. User fees should be considered and a strong public communication programme developed to support the process. The standardisation of risk-allocation models, tendering processes, bidding processes, contracts, and evaluation would significantly reduce bidding costs. The well-established link between investment in public infrastructure and economic competitiveness means that South Africa must act now if it is to avoid a widening infrastructure gap.

In future we will see more conservative financing plans and we must expect that project agreements will be negotiated to mitigate demand risk and incorporate mechanisms to expressly protect private sector investment. Moreover, if specific possible events that affect demand are identified that can be influenced by the public sector; provisions to expressly protect private sector investment against such events will need to be explored. In addition, the commercial framework should incentivise the private sector to partner with the public sector in mitigating the impact of those risks. Long-term financial planning should be conducted to provide for the large capital investments for water resources development, together with the relevant operating and maintenance costs, that will be needed during the coming decades.

However, as the models discussed show, there are ways to incentivise the private sector to partner with the public sector and at the same time mitigate the impact of demand risks and allow both parties to share in the upside. Such new thinking is needed to get the next wave of infrastructure assets off the ground. If the public sector is unable to fund the required infrastructure spending and the private sector is unwilling to take on the entire burden itself, new and imaginative means of generating private investment will need to be developed. Certain projects are likely to be easier to fund privately than others. The infrastructure funding gap was compounded by the impact of the financial crisis, but this should not be seen as an insurmountable barrier. While the government will need to act very carefully in order not to distort savings and investment markets, the scale of the infrastructure challenge in South Africa demands innovative solutions and new forms of funding models to maximise private sector investment. Even in the absence of the financial and fiscal crisis, a game-changing upward shift in infrastructure investment is urgently needed in South Africa.

Acknowledgements

Financial assistance from the DWA is appreciated. Staff members of organisations who have made this research project possible are appreciated. The comments from the anonymous reviewers enhanced and improved the manuscript.

References

AASHTO (AMERICAN ASSOCIATION OF STATE HIGHWAY AND TRANSPORTATION OFFICIALS) (1995) Innovative Transport Financing. AASHTO, Washington, DC. [ Links ]

BRINECO-GARMENDIA C, SMITS K and FOSTER V (2008) Financing infrastructure in Sub-Sahara Africa: Patterns, issues, and options. In: AICD Background Paper 15, Africa Infrastructure Sector Diagnostic. World Bank, Washington DC. [ Links ]

CASADESUS-MASANELL R and RICART JE (2011) How to design a winning business model. Harv. Bus. Rev. 89 (1/2) 100-107. [ Links ]

CONNINGARTH ECONOMISTS (2002) Cost-Benefit Analysis in SA for Water Resource Development. WRC Report No. TT 177/02. Water Research Commission, Pretoria. [ Links ]

COLDWELL D and HERBST F (2004) Business Research. Juta, Cape Town. [ Links ]

CRANSTON S (2005) Old Mutual: Closing the gap. Financial Mail, 28 January 2005. URL: http://www.businessday.co.za_(Accessed 30 April 2011). [ Links ]

CSIR (2010) The State of Water and Sanitation in South Africa. Report No. 100403. CSIR, Pretoria. [ Links ]

CSIR and CIDB (2007) The State of Municipal Infrastructure in South Africa and its Operation and Maintenance: An Overview. CIDB, Pretoria. [ Links ]

DCoG (DEPARTMENT OF COOPERATIVE GOVERNANCE AND TRADITIONAL AFFAIRS, SOUTH AFRICA) (2010) Strategy for Accelerating and Improving Municipal Infrastructure Provision. Department of Cooperative Governance and Traditional Affairs, Pretoria. [ Links ]

DWA (DEPARTMENT OF WATER AFFAIRS, SOUTH AFRICA) (2011a) Strategic Plan 2010/11-2012/13. URL: http://www.dwaf.gov.za/documents (Accessed 01 October 2012). [ Links ]

DWA (DEPARTMENT OF WATER AFFAIRS, SOUTH AFRICA) (2011b) Annual Report 2010-2011. URL: http://www.dwaf.gov.za/documents (Accessed 1 October 2012). [ Links ]

DWA (DEPARTMENT OF WATER AFFAIRS, SOUTH AFRICA) (2012) Annual Performance Plan 2012/13-2014/2015. URL: http://www.dwaf.gov.za/documents (Accessed 1 October 2012). [ Links ]

DWAF (DEPARTMENT OF WATER AFFAIRS AND FORESTRY, SOUTH AFRICA) (1997a) White Paper on a National Water Policy for South Africa. URL: http://www.dwaf.gov.za/Documents/Policies/nwpwp.pdf (Accessed 01 February 2011). [ Links ]

DWAF (DEPARTMENT OF WATER AFFAIRS AND FORESTRY, SOUTH AFRICA) (1997b) Water Services Act. Act No. 108 of 1997. Government Printer, Pretoria. [ Links ]

DWAF (DEPARTMENT OF WATER AFFAIRS AND FORESTRY, SOUTH AFRICA) (1998) National Water Act. Act No. 36 of 1998. Government Printer, Pretoria. [ Links ]

DWAF (DEPARTMENT OF WATER AFFAIRS AND FORESTRY, SOUTH AFRICA) (2003) Water Services Strategic Framework. Government Printer, Pretoria. [ Links ]

DWAF (DEPARTMENT OF WATER AFFAIRS AND FORESTRY, SOUTH AFRICA) (2004) National Water Resource Strategy of South Africa. Government Printer, Pretoria. [ Links ]

DWAF (DEPARTMENT OF WATER AFFAIRS AND FORESTRY, SOUTH AFRICA) (2007) Raw Water Pricing Strategy of South Africa. Government Printer, Pretoria. [ Links ]

DWAF (DEPARTMENT OF WATER AFFAIRS AND FORESTRY, SOUTH AFRICA) (2008) Water for Growth and Development, Version 8. URL: http://www.dwaf.gov.za/Documents/Notices/WFGD Framework v8.pdf (Accessed 31 January 2011). [ Links ]

DBSA (DEVELOPMENT BANK OF SOUTHERN AFRICA) (2009) Water Security in South Africa. Development Planning Division Working Paper Series No.12. DBSA, Midrand, South Africa. [ Links ]

DBSA (DEVELOPMENT BANK OF SOUTHERN AFRICA) (2012) Annual Report 2011/12. DBSA, Midrand, South Africa. [ Links ]

EBERHARD R (1999) Supply Pricing of Urban Water in South Africa. WRC Report No. 678/1/99. Water Research Commission, Pretoria. [ Links ]

FRASER N, BERNHARDT I, JEWKES E and TAJIMA M (2000) Engineering Economics in Canada. Prentice Hall, Scarborough, Ontario. [ Links ]

GILBERT RO (1987) Statistical Methods for Environmental Pollution Monitoring. Van Nostrand Reinhold, New York. [ Links ]

GOODMAN AS and HASTAK M (2006) Infrastructure Planning Handbook: Planning, Engineering, and Economics. McGraw-Hill, New York. [ Links ]

HAZELTON D (1998) Cost recovery for water schemes to developing urban communities. WRC Report No. 521/1/98. Water Research Commission, Pretoria. [ Links ]

HOLLINGWORTH B, KOCH P, CHIMUTI S and MALZBENDER D (1994) An investigation into the water infrastructure development financial allocation pathways in municipalities. WRC Report No. TT 476-10. Water Research Commission, Pretoria. [ Links ]

INDERST G (2009) Pension Fund Investment in Infrastructure. OECD Working Papers on Insurance and Private Pensions. Report No. 32. OECD Publishing, Paris. DOI:10.1787/227416754242. [ Links ]

IIPF (INSTITUTE OF INTERNATIONAL PROJECT FINANCE) (2001) Project financing in developing countries. URL: http://members.aol.com/projectfin/emerging.html (Accessed 5 February 2011). [ Links ]

LAITINEN I, LEINONEN J and VIRTANEN K (2010) New and Innovative Infrastructure Procurement Models - The Need for New Financing Models in Finland for Social and Economic Infrastructure. ERES, Milan, Italy. [ Links ]

LAMB RA (1984) Creative financing of the infrastructure. Ann. NY Acad. Sci. 431 54-58. DOI: 10.1111/j.1749-6632.1984.tb27028.x. [ Links ]

LANG HJ and MERINO DN (1993) The Selection Process for Capital Projects. John Wiley and Sons, New York. [ Links ] LEACH G (2010) Infrastructure - mind the gap! Institute of Directors, UK. [ Links ]

MATTA NF and ASHKENAS RN (2003) Why good projects fail anyway. Harv. Bus. Rev. 81 (9) 109-114. [ Links ]

MATTHEWS W (2009) The Development of an Activity-Based Costing Model to Quantify the Real Costs of Delivering Water Services in Rural Areas. WRC Report No. 1614/1/09. Water Research Commission, Pretoria. [ Links ]

MAYLE DT, HANDS CN and HINTON A (2001) What really goes on in the name of benchmarking. Open Univ. Bus. School 17 (1) 33-41. [ Links ]

MOSEKI C, TLOU T and RUITERS C (2011) National water security: Planning and implementation. In: Schreiner B and Rashid H (eds.) Transforming Water Management in South Africa: Designing and Implementing a New Policy Framework. Springer, Dordrecht. [ Links ]

NT (NATIONAL TREASURY OF SOUTH AFRICA) (1999) Public Finance Management Act. Government Printer, Pretoria. [ Links ]

NT (NATIONAL TREASURY OF SOUTH AFRICA) (2000) South African National Treasury PPP unit. URL: http://www.treasury.gov.za/organisation/ppp/default.htm (Accessed 20 January 2011). [ Links ]

NT (NATIONAL TREASURY OF SOUTH AFRICA) (2011a) The Estimates of National Expenditure 2011: Vote 3 Cooperative Governance and Traditional Affairs. FormeSet Printers Cape (Pty) Ltd, Pretoria. [ Links ]

NT (NATIONAL TREASURY OF SOUTH AFRICA) (2011b) The Estimates of National Expenditure 2011: Vote 38 Water Affairs. FormeSet Printers Cape (Pty) Ltd, Pretoria. [ Links ]

NT (NATIONAL TREASURY OF SOUTH AFRICA) (2011c) The Division of Revenue Bill. Government Printer, Pretoria, South Africa. [ Links ]

NT (NATIONAL TREASURY OF SOUTH AFRICA) (2012) What are RSA bonds? National Treasury of South Africa, Pretoria. [ Links ] NEBERT D (2001) Developing spatial data infrastructures: The SDI Cookbook. URL: http://www.gsdi.org/pubs/cookbook/cook-book0515.pdf (Accessed 20 February 2011). [ Links ]

PALMER DEVELOPMENT GROUP (1998) Water Supply Services Model Manual. WRC Report No. KV109/98. Water Research Commission, Pretoria. [ Links ]

PALMER DEVELOPMENT GROUP (2000) Guidelines for Setting Water Tariffs with a Focus on Industrial, Commercial and other Non-Residential Consumers. WRC Report No. 992/1/00. Water Research Commission, Pretoria. [ Links ]

PALMER DEVELOPMENT GROUP (2002) Corporatisation of Municipal Services Providers. WRC Report No. TT 199/02. Water Research Commission, Pretoria. [ Links ]

RCCAO (RESIDENTIAL AND CIVIL CONSTRUCTION ALLIANCE OF ONTARIO) (2006) The Infrastructure Funding Deficit: Time to Act. RCCAO, Ontario, Canada. [ Links ]

ROWEY K (2009) U.S. Infrastructure Investment in a Time of Uncertainty and Global Recession. Freshfields Bruckhaus Deringer LLP, Washington DC. [ Links ]

RUITERS C (2011) Funding models for the financing of water infrastructure in South Africa: A framework and comparative analysis of alternatives. MBA thesis, University of South Africa, Pretoria. [ Links ]

SAGAR A (2006) Infrastructure and project financing Asia-Pacific scenario. In: Global Infrastructure Report of Project Finance International Magazine. Asian Development Bank, Manila. [ Links ]

SIHOMBING LB (2008) Financial Innovation for Infrastructure Financing. Citra, Indonesia. [ Links ] SAICE (SOUTH AFRICA INSTITUTION OF CIVIL ENGINEERING) (2011) SAICE infrastructure report card for South Africa 2011. URL: http://www.saice.org.za/html (Accessed 26 March 2011). [ Links ]

TAYLOR P (2002) Analysing quantitative data. In: Charlesworth J, Lewis J, Martin V and Taylor P (eds.) Toolkit 2: Investigating Performance and Change. The Open University Press, Hampshire, UK. [ Links ]

TCTA (TRANS-CALEDON TUNNEL AUTHORITY) (2012) Annual Report 2011/12. Trans-Caledon Tunnel Authority, Pretoria, South Africa. [ Links ]

TUSTIN DR, LIGTHELM AA, MARTINS, JH and VAN WYK H DE J (2005) Marketing Research in Practice. University of South Africa Press, Pretoria. [ Links ]

TYSON LD (2011) A better stimulus plan for the U.S. economy. Harv. Bus. Rev. 89 (1/2) 53. [ Links ]

URBAN LOGIC (2000) Financing the NSDI: National Spatial Data infrastructure. URL: http://www.fgdc.gov/whatsnew/whatsnew.html#financing (Accessed 10 March 2011). [ Links ]

WORLD BANK (1994) World Bank Development Report: Infrastructure for development. Oxford University Press, New York. [ Links ]

WORLD BANK (2010) Africa's infrastructure: A time for Transformation. World Bank, Washington DC. [ Links ]

Received 29 March 2012

Accepted in revised form 8 March 2013.

* To whom all correspondence should be addressed.

Current affiliation: Council for Scientific and Industrial Research (CSIR), Built Environment, PO Box 395, Pretoria, 0001, South Africa +27 12 841 3051; fax: +27 12 841 4446; e-mail: cruiters@csir.co.za

Appendix 1

Evaluation criteria for alternative and innovative funding models for water infrastructure in South Africa (See text for abbreviations)