Serviços Personalizados

Artigo

Inglês (pdf)

Inglês (pdf)

Artigo em XML

Artigo em XML Referências do artigo

Referências do artigo

Indicadores

Links relacionados

-

Citado por Google

Citado por Google -

Similares em Google

Similares em Google

Compartilhar

Permalink

PermalinkJournal of Contemporary Management

versão On-line ISSN 1815-7440

JCMAN vol.20 no.1 Meyerton 2023

http://dx.doi.org/10.35683/jcman1023.206

RESEARCH ARTICLES

Corporate social responsibility applications in the retail sector: Lessons from the international experience

Niel RooiI; Doret BothaII, *; Gerrit Van Der WaldtIII

IDepartment of Public Safety, City of Johannesburg, South Africa. Email: nielrooi.phd@gmail.com; ORCID: http://orcid.org/0000-0001-7368-6785

IISociology, North-West University, South Africa Email: doret.botha@nwu.ac.za; ORCID: http://orcid.org/0000-0003-2787-8107

IIISocial Transformation, North-West University, South Africa. Email: gerrit.vanderwaldt@nwu.ac.za; ORCID: https://orcid.org/0000-0001-9458-1982

ABSTRACT

PURPOSE OF THE STUDY: The research aimed to uncover potential lessons from the international experience regarding corporate social responsibility (CSR) applications in the retail sector

DESIGN/METHODOLOGY/APPROACH: This study followed a qualitative document review approach, employing a literature review and content analysis. The document review focused on empirical work mainly done towards the latter part of the 20th century on the continents of Asia, the Americas, Europe and Africa. The document review approach allowed for a broad view of CSR applications in the retail sectors of multiple countries, with a specific focus on their maturity level and transformative CSR best practices

FINDINGS: The findings suggest that countries have different maturity levels with variant regulatory interventions. Countries such as India and the UK are trend leaders in their explicit CSR regulatory language. This is in stark contrast with the relatively vague CSR articulation in countries such as Poland and Egypt and limited to no regulatory intervention in countries such as the USA, Mozambique and Kenya

RECOMMENDATIONS/VALUE: If the reluctance to explicit regulatory intervention in the application of CSR in the international experience persists, the trend to primarily use CSR to advance businesses' public image may prevail. Therefore, the board of directors is recommended to oversee transformative CSR application by setting measurable CSR strategic priorities. Applying the DNA model and lessons learned, businesses should set key CSR indicators that conform to the socio-economic developmental agenda, and third-party oversight structures should enhance their vigilance in monitoring businesses' legislative compliance with socio-economic developmental aspects

MANAGERIAL IMPLICATIONS: The overall result of the study makes a significant contribution to the contemporary field of management in that the trend towards transformative CSR requires greater alignment to the socioeconomic developmental agenda of a country and CSR impact measurement requires additional oversight by authorities and relevant civil society organisations

JEL CLASSIFICATION: M14

Keywords: Corporate social responsibility; DNA model; International experience; Lessons learned; Retail sector; Transformative corporate social responsibility

1. INTRODUCTION

It is broadly accepted that countries and businesses (a reference to business throughout the paper implies the inclusion of the retail sector) operate in an ever-changing, interrelated world. In this context, as part of the government's responsibilities, it must ensure that civil rights are protected, that socially responsible behaviour is fostered, that virtuous social responsibility in their governance practices is demonstrated, that standardised business practices are complied with, and that policies are formulated in line with corporate social responsibility (CSR) (Kloppers, 2018). Governments must also consider the concerns of those citizens that are less influential in their social settings and economic position (Hoffman, 2013). In the South African context, despite all government legislative efforts and benevolent intentions from global and local CSR organisational bodies, there would appear to be a persistence of inert socio-economic development and inadequate progress pertaining to tangible socio-political transformation (Brown, 2018; The Presidency, 2020).

In this article, the authors analyse international and local transformative CSR trends and views with the premise that each nation is a sovereign state and has an independent perspective on legislatively implementing the concept. The exploratory analysis commenced with empirical work surrounding governmental legislative intercessions on four continents. By reviewing the available empirical data on transformational relevance, the authors sought to determine the notable mediating aspects through which CSR has been found through self-regulation to affect transformative socio-economic development.

2. LITERATURE REVIEW

This section provides a conceptualisation of transformative CSR, explains the transition from conventional CSR to transformative CSR, discusses the DNA model of transformative CSR, elaborates on exertions towards transformative CSR practices and outlines the peculiarities of CSR.

2.1 Conceptualising transformative CSR

The agenda to position CSR as a positive descriptive concept emerged since its articulation in 1953 (Bowen, 1953). The concept was initially developed in response to the normative question of whether organisations are responsible for promoting social wellbeing in addition to their economic and legal obligations (Carroll, 1999). However, the early international progression of the concept was mainly assigned an over-inclusive meaning, or it was conceptualised as a valuable publicity add-on for the business (Siegel & McWilliams, 2007) and assigned universal applicability (Carroll, 1991). Several thinkers disputed this blanket pertinency, and believe that the inherited Western nature of Carroll's CSR pyramid is problematic for the African context (Visser, 2006; Abdulai, 2015). Furthermore, the evolution of the concept was not always favourably accepted. Several descending voices described the concept as "elusive" (Clarkson, 1995:92), a "constable" (Windsor, 2006:93) and "epiphenomenal" (Van Oosterhout & Heugens, 2006:210). In contrast, others argued that CSR hampers a business's obligation to maximise profits (Friedman & Friedman, 2002).

Since the dawn of democracy in South Africa, the descriptive argument has been expanded, and CSR has been generally positioned as a socio-economic developmental tool. Many scholars agree that the uptake of the concept in South Africa is applaudable, but several criticise its lack of socio-economic transformation and impact (Brown, 2018; The Presidency, 2020). To further develop the explanatory concept of transformative CSR from the conceptual base donated by CSR, the authors followed the casual approach to concept formation as set out by Goertz (2012). Goertz believes that explanatory social science constructs must be expressed in terms of their most relevant general attributes discovered through empirical research.

The authors reviewed empirical research on the conventional CSR versus the developmental self-regulatory relationship to conceptualise the general attributes of transformative CSR. While early empirical research investigated the latter (Blowfield, 2004; Idemudia, 2014), other studies have documented that added transformational relevant variables mediate the general relationship of CSR versus development (Du Plessis & Grobler, 2014; Visser, 2014). The concept of transformative CSR in the South African context was glossed on by Wayne Visser (2012b) and subsequently developed further by him and others who explicitly linked it to the broad leadership dimensions of government, socio-economic development and business responsibility (Swanson, 2018; Edi, 2020).

2.2 The transition from conventional CSR to transformative CSR

The highly regarded South African Constitution forms the democratic foundation of government (ANC, 2017). However, considering the botch voluntary commitment to CSR, the government has since 1994 leniently and intermittently arbitrated legislatively to safeguard a mutual public policy that nurtures standardised socially responsible practices in the South African business sector (Kloppers, 2018). The government has also supported voluntary transnational and national CSR standards in amending legislation (Department of Trade Industry and Competition (DTIC), 2015; Institute of Directors South Africa (IoDSA), n.d.). To an extent, CSR standards, particularly the Global Reporting Initiative (GRI) Standards, conventionalised the monitoring of corporate social and ethical performance and social reporting to stakeholders (Rossouw, 2018).

According to the South African Institute of Charted Accountants, the Companies Act, 71 of 2008 were revised in 2018 to, among other things, reinforce the checks and balances in business governance (The South African Institute of Charted Accountants (SAICA), 2018). Subsequently, additional amendments were proposed in 2021 to strengthen the Companies Act further. The proposed Companies Amendment Bill 2021 seeks to cement the composition of the social and ethics committee and the presentation and approval of the social and ethics committee report (DTIC, 2021). However, if Bill's proposals are accepted entirely, the outcome of the modifications is still unknown.

Despite the amendments to the Broad-Based Black Economic Empowerment (B-BBEE) Codes of Good Practice, there are increasing pressures on the South African government to levy more guidelines and regulate businesses (Kloppers, 2018; RSA, 2017). Such demands could be reasonable as, despite the South African government's legislative interventions, evidence remains sketchy to cement the socio-economic development element of the B-BBEE Amended Codes of Good Practice as a co-driver of socio-economic transformation in the country (B-BBEE Commission, 2020).

Although businesses have been relatively active in the CSR realm, the impact of business activities might remain insignificant as long as legislation is silent on clear CSR requirements. This view is supported by Fredericksz (2015) and Johannes (2016) when they assert that it must be mandatory for CSR to form part of the governance structure and material CSR matters to influence business decision-making processes. If CSR is not part of governance settings some commercial entities might limit their CSR activities to the required minimum or wait for government intervention, the media or academia to expose any undesirable practices before behaving socially responsibly.

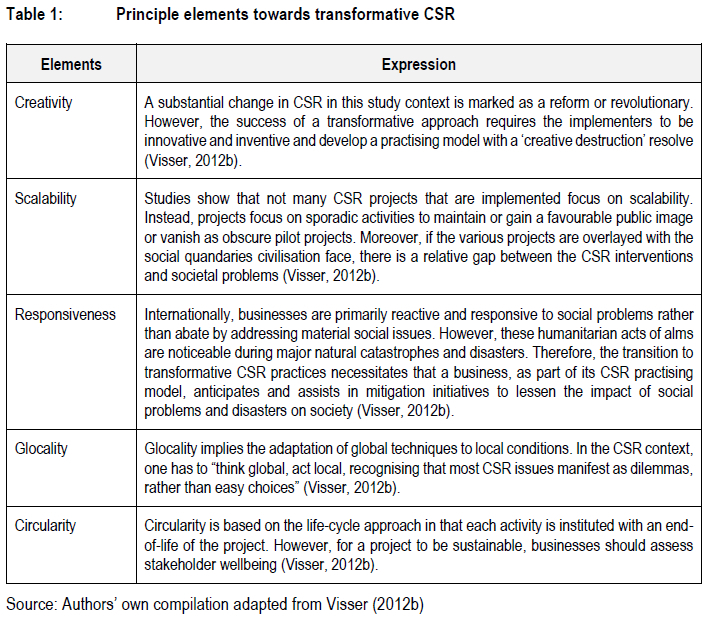

Considering the shortcomings of conventional CSR practice, the ascending voices argue that the current lack of tangible social interventions is not sustainable. Key to the arguments is that there is a need to move from conventional CSR practice toward transformative CSR practices. In a transformative CSR practice, the board of directors must have greater responsibility and accountability, whereas management's focus should be on stakeholder relations (management and engagement), strategy development, policy development and oversight (Visser, 2012b; Botha, 2016; B-BBEE Commission, 2020). For the South African civilisation to thrive in its pursuit of a transformative CSR reform, Visser (2012b) proposes five principle elements toward transformative CSR or CSR 2.0 depicted in Table 1.

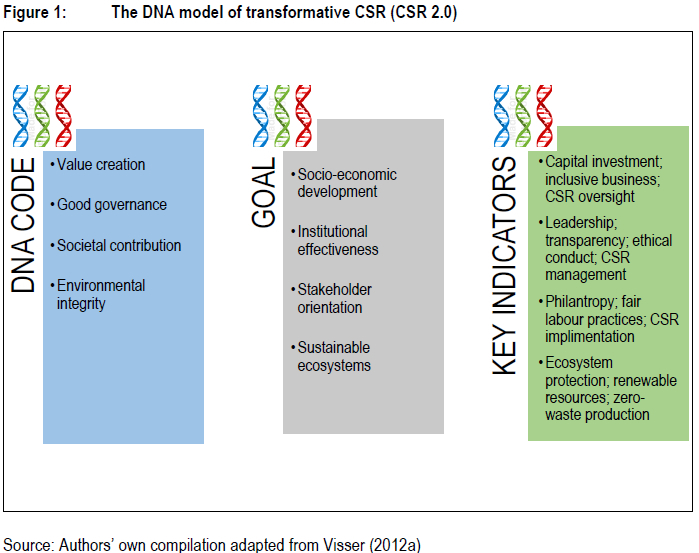

The advent of transformative CSR practices led to the emergence of the DNA model for the change pathway.

2.2.1 The DNA model of transformative CSR

The DNA model is primarily anchored in the notion that the ethical systems in the conventional CSR approach have failed ( Visser, 2012a; Henderson, 2018; Commission of Inquiry into State Capture, 2019). The model encourages practitioners to embrace and reform business practices through social value creation and environmental integrity (Visser, 2014). The DNA model comprises codes or key business domains that should be aligned with strategic business priorities and measured by utilising key performance indicators in Figure 1.

As depicted in Figure 1, a business requires more than just financial viability for shareholders to create value. Instead, businesses' societal contribution should be intensified by codes such as good governance, environmental integrity, skills development and job creation. Visser (2014:4) maintains that should businesses not utilise these codes, they will not add societal value and fail to improve "quality of life". In addition, Visser questions how the economic dividends emanating from business operations are apportioned. Visser (2014) argues that any deficiencies in CSR practices will cause "economic spoils" not to reach all stakeholders. The proper distribution of financial gain and eventual economic prosperity can only be achieved if boards of directors and executives follow a transformative CSR approach and practice "unswerving good corporate governance with veracity (Visser, 2014:4; Smit, 2019:4).

Widespread anecdotal international evidence suggests a general absence of the application of the DNA model codes. Poor corporate governance, inadequate leadership, lack of transparency, and misleading or unethical conduct especially in the retail business environment (Smit, 2019), seriously hamper societal value creation. Examples that encompass most of the recent lapses are the collapse of one of South Africa's most significant single retail holding companies, Steinhoff International (Naudé et al., 2018; Van der Linde, 2022) and African Bank Investment Limited (Giamporcaro & Marrian, 2018). The latter is compounded with several other retailers in distress, such as Edcon and Massmart (Teuteberg, 2020). As corporate citizens and contributors to the socio-economic development of communities, retail business crises have various degrees of deleterious impacts on the economic wellbeing of social stakeholders.

The DNA model has its footing in the principles in Table 1, which intends to bring about sustainable change in communities. The model's application would assist the retail sector in advancing corporate sustainability and its social responsibility beyond defensive, charitable, and self-promotional CSR. The model's inclusion is primarily to serve as a baseline to be expanded upon by the retail sector business domains and assist the CSR function in executing its transformative CSR interventions with strategic intent (goals) and measurable purposefulness (indicators) in creating value that meets the needs of society.

To expedite transformative goals and indicators, businesses in general and the retail sector, in particular, should re-evaluate their in-house CSR practices in order to be responsive to contemporary issues and realities and transform conventional CSR practices (Castillo et al., 2018; Vos, 2018). Visser (2014) proposes an environmental integrity code as an appraisal strategy to contribute to the transition to transformative CSR practices.

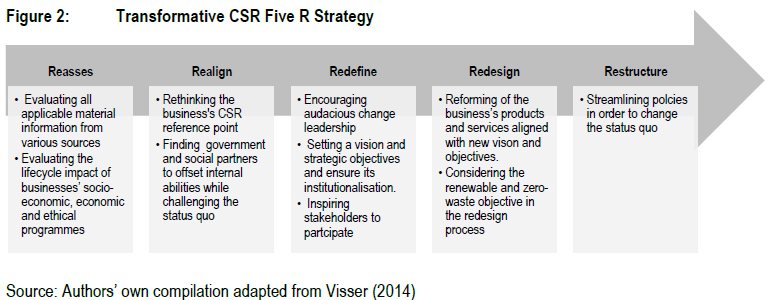

2.2.2 Exertions towards transformative CSR practices

Various assessments conducted in the South African retail environment reveal that transformation as a catalyst to redress the country's socio-economic challenges in its general sense has been dawdling (Sewell et al., 2014; Malgas, 2020). For businesses to transition from conventional CSR practices to practices that incorporate transformative principles, businesses need to reassess, realign, redefine, redesign and restructure how they institutionalise social value creation through the adoption of transformative CSR practices. In this regard, Visser (2014:85) proposes the application of the 'Five R' Strategy to facilitate this transition. This strategy, outlined in Figure 2, comprises five processes, namely reassess, realign, redefine, redesign and restructure.

The main aim of the Five R Strategy for transformative CSR is to refocus CSR interventions away from socially immaterial activities to a more socio-economic developmental model. This model should align contemporary developmental policies and strategies with tangible and beneficial business outcomes and positive socio-economic prospects. The Five R Strategy may also serve as an analytical tool to periodically attune CSR practices of businesses in the retail sector to international trends and best practices, national socio-economic developmental objectives, and address adverse business outcomes. The adoption of the transformative Five R strategy might not be without implications for the retail sector. Some of the potential business consequences may include:

• The need to remodel operational processes and procedures to align CSR outcomes with the respective operational business units;

• The adoption of change management programmes to adequately prepare affected business units and employees regarding the new operational direction and approach; and

• The potential need for additional human and other resources to successfully execute the transformative CSR approach and activities in operational business units.

2.3 CSR peculiarities

Among the myriad forces and trends that have shaped and periodically reshaped the international business landscape, CSR is undoubtedly the one with the most peculiarities (Yin & Jamali, 2016). Despite the diminutive research focus on the retail sector (Naidoo & Gasparatos, 2018), the general fundamentals of CSR are well documented and have grown exponentially. It seems that it is no longer considered good business practice if CSR does not have a strategic presence or if businesses do not regularly report on its socio-economic and ecological impact on society (Simöes & Sebastiani, 2017). It is evident that businesses should not yield profits without redistributing part of their revenue towards the socio-economic development of communities as well as for the protection of the natural environment (Fifka et al., 2018). This can only be facilitated through a transformative CSR model and on a business's willingness to contribute to value creation in society (Nasrullah & Rahim, 2014). Moreover, a transformative model should be supported by the government by proactively facilitating CSR's absorption into the business sector by endorsing, affiliating or incentivising tangible CSR initiatives.

Despite the endeavours to move the outcomes of CSR interventions towards greater socioeconomic developmental value, the general application thereof across industries and sectors remains to be subject to some challenges. For example, an investigation conducted by Welzel et al. (2007) identified a distorted CSR policy focus on the economy, society, governance and stakeholder collaboration in several countries. Nasrullah and Rahim (2014) confirm this finding by maintaining that countries such as Brazil, Argentina, Mexico, Poland, Slovenia, Hungary, South Africa, India, China and Malaysia developed functional frameworks, decrees, and public policies to support CSR absorption in business. A study conducted by Adams et al. (2019) on multinational companies in oil-rich developing countries found widescale non-compliance with CSR policies and practices. Adams et al. (2019) concluded that several multinational companies in the petroleum sector adopted some CSR strategies to gain legitimacy, with little or no meaningful contribution to the socio-economic development of the countries in which they operate.

It is thus evident that CSR is yet to be valued as more than simply charitable philanthropy. It should rather be regarded as a vehicle to add tangible socio-economic value through poverty alleviation endeavours and the enhancement of foreign direct investment (Wilson & Wilson, 2017; Agrawal & Chandrika, 2018). In order to fully comprehend the status of CSR adoption and application in business, it is necessary to analyse trends and perspectives from different countries. This will enable comparative analyses and the extraction of CSR best practices in business. Another concern is the weak alignment of business CSR objectives to the developmental objectives of the country as set out in its National Development Plan as a strategic agenda (World Bank Group, 2018).

It is thus evident that CSR is yet to be valued as more than simply charitable philanthropy. It should rather be regarded as a vehicle to add tangible socio-economic value through poverty alleviation endeavours and the enhancement of foreign direct investment (Wilson & Wilson, 2017; Agrawal & Chandrika, 2018). In order to fully comprehend the status of CSR adoption and application in business, it is necessary to analyse trends and perspectives from different countries. This will enable comparative analyses and the extraction of CSR best practices in business.

3. METHODOLOGY

This study followed a qualitative document review approach, employing a literature review and content analysis. According to Mouton (2015), a scientific literature review can establish the latest research in the field under investigation, support the research argument, and provide reliable scientific data, information and insight into how scholars investigated aspects of the problem(s) under investigation. Therefore, the researchers focused on the manifest (evidence) and latent (underlying meaning) content of the documents in a detailed and analytical way, as suggested by Sarantakos (2013).

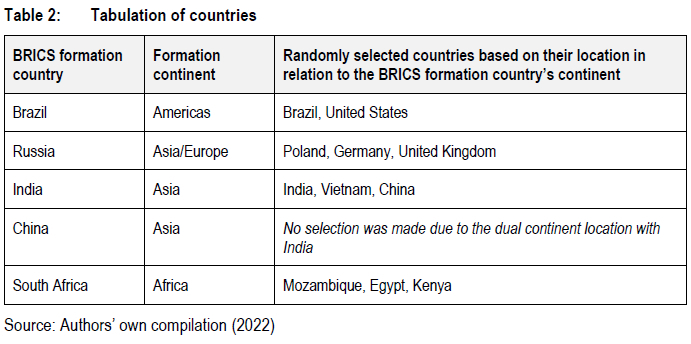

The document study focused on uncovering the trends and perspectives of CSR (transformative) practices, relating activities and policy progression on the purposively selected continents of Asia, the Americas, Europe and Africa. The continents were selected based on their locations relative to the BRICS (Brazil, Russia, India, China, and South Africa) member country formation, as indicated in Table 2. The BRIC formation was established in 2009 with the inclusion of South Africa in 2010 due to their similar emerging economies and stages of developmental maturity in relation to each other (Al-Mohamad, 2020).

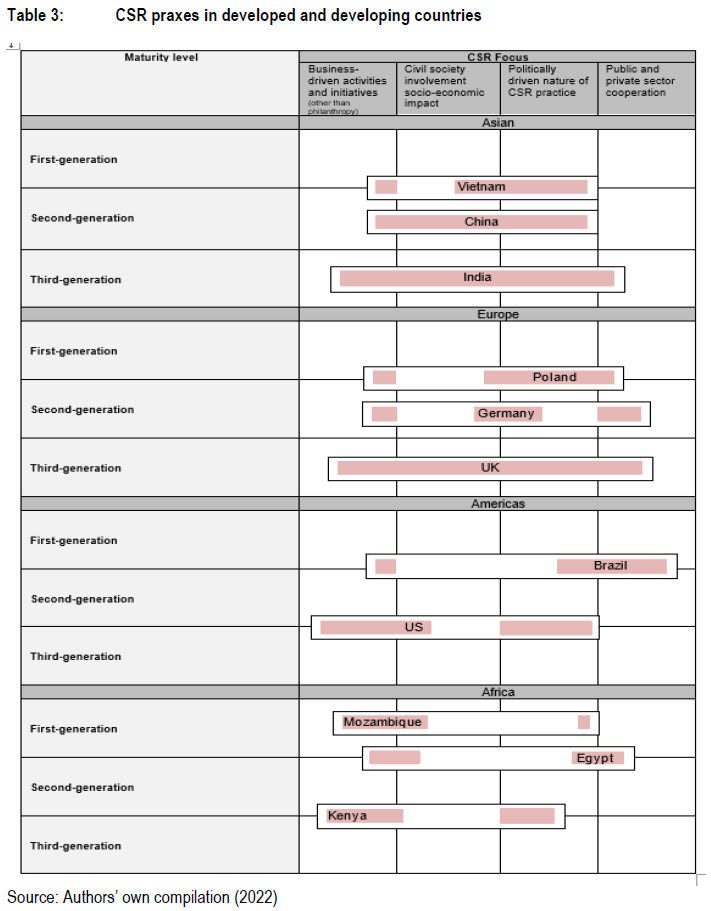

The document review approach allowed for a broad perspective of CSR applications in the retail sectors in these countries with a specific focus on their maturity level and transformative CSR best practices. The maturity levels were categorised into the following levels:

• First-generation level: No explicit CSR policies exist. A country lacks proficiency, measuring tools, and performing activities dissimilar to CSR.

• Second-generation level: A country has the essential CSR policies in place, has some proficiency, performs meaningful CSR activities, have basic CSR measuring tools and stakeholder involvement.

• Third-generation level: Exhibit elements of transformative CSR policies and practices, activities show considerable societal impact, and the country has public-private partnerships.

Transformative CSR best practices were those business-driven policy progressions with interventions that have a level of civil society impact or involvement, are politically driven and foster more significant public-private partnerships. To ensure access to the latest, applicable and reliable data, the following sources were utilised:

• Internet search engines, such as Google Scholar, EBSCOhost and SAePublications

• Scientific studies and research articles (conducted by governments, tertiary and other institutions)

• Statutory documents relevant to CSR in Asia, the Americas, Europe, and Africa

• Official organisational documents in the public domain

• Journal articles

• Papers presented at conferences and textbooks.

4. FINDINGS

With the increased presence of CSR in countries, governments in those countries implemented policies to regulate the entrée of the concept (Fifka et al., 2018). For purposes of analysis, the typology proposed by Hoffman (2013) regarding CSR trends and practices was applied. This typology makes provision for -

• Business-driven activities and initiatives (other than philanthropy)

• Civil society involvement and socio-economic impact

• Politically driven nature of CSR practices and compliance with national legislation and international protocols and conventions

• Public and private sector cooperation

Considering these themes, the findings of the selected cases are outlined next.

4.1 India

Business-driven activities and initiatives (other than philanthropy), recently, in the Indian retail sector have surpassed their charitable past and have grown to embrace the concept as a component of the overall business strategy enacted through dedicated CSR teams (Kohli & Bhagwati, 2011; Ministry of Law and Justice (MLJ), 2013; Pereira & Patel, 2014; Deepa & Chitramani, 2015). Retailers have teams that devise CSR-specific policy strategies and initiatives that are funded by the required 2 percent average of the businesses preceding three-year Net Profit After Tax allocation in each financial year (Agrawal & Chandrika, 2018).

Civil society involvement and socio-economic impact. Historically, civil society's involvement in CSR during the early onset of the concept was modest to some degree as the retailing environment was primarily family-owned and run roadside shops (Sengupta, 2008). Shop owners executed the concept as part of their respective deep-rooted customs of community welfare and wellbeing (Balasubramanian et al., 2005). According to Deepa and Chitramani (2015) and Kumar (2019), civil society's involvement in CSR activities are largely through non-profit organisations due to a lack of interest by communities to participate and contribute to CSR activities. Therefore, the socio-economic impact of CSR was based on the business' benevolent traditions rather than a business CSR strategy (Kochhar, 2014). Calls are also made for retail segments, such as banking, to consider reporting their intervention initiatives individually to articulate the impact of the individual interventions (Maqbool & Zameer, 2018). Furthermore, to further focus on the socio-economic impact of setting baseline material interventions, the new Companies Act lucidly stipulates and delineates CSR disbursements (MLJ, 2019). However, Kumar (2019) argues that in order for these interventions to be impactful, there is a need for key challenges such as inter-alia significant capacity building in the NGO realm and greater transparency on the part of the local implementing agencies to be addressed.

Political-driven nature of CSR practices and compliance with national legislation and international protocols and conventions. India recently replaced its 56-year-old Companies Act, which makes CSR compulsory in that country and articulates exclusions of everyday business functions such as marketing and public relations activities or initiatives undertaken to benefit employees as CSR (MLJ, 2013; Thrasyvoulou, 2016). Key to the politically driven intervention through the new Companies Act is for businesses, including retailers, of a specific size to establish a CSR committee and spend 2 percent of their three-year average profit on CSR activities within the local community in which they operate (MLJ, 2013; Thrasyvoulou, 2016). The CSR committee must formulate, recommend to the board and monitor the business's CSR policy. The board of directors, in turn, must ensure that the CSR policy is ratified, that triennially the required 2 percent average turnover is ringfenced for CSR initiatives and that the business's CSR policy is readily available (MLJ, 2013).

Public and private sector cooperation. India has a broadly healthy collaboration between the public and private sectors. In a study conducted by Kumar (2019), he identified various cooperative CSR initiatives spanning from cooperative adoption/upliftment of villages (interventions to assist the elected village in becoming self-reliant and improving agricultural activities), health interventions (bringing back eyesight and medical check-ups) and disaster relief (benefaction and rehabilitation projects), among others.

4.2 Vietnam

Business-driven activities and initiatives (other than philanthropy). Despite the general sluggish uptake of CSR, evidence suggests that stakeholders are slowly demanding more business-driven activities and initiatives from the Vietnam retail sector (Ha, 2015; Le Doan Minh Duc et al., 2018). Generally, according to Le Doan Minh Duc et al. (2018) and Nguyen et al. (2019), to enhance business-driven activities and initiatives in Vietnam, there is a need for greater CSR commitment from boards and enhanced business awareness of the CSR concept.

Civil society involvement and socio-economic impact. Vietnam has been under Communist rule since 1975, making many societal members apprehensive about getting involved in social organisations (Human Rights Watch, 2015; Duiker, 2018). Despite the apprehension of local civil society, various international NGOs are raising awareness among businesses on sustainability and socio-environmental issues (Tran, 2017). It can be concluded that the general apprehension of the Vietnamese stakeholders to get involved deprives them of grasping the sincere intention of the CSR concept and the value and power it gives to society.

Political-driven nature of CSR practices and compliance with national legislation and international protocols and conventions. The Socialist Republic of Vietnam has heightened its attention to social issues by, one, introducing several policies and projects encompassed under the Vietnam Agenda 21, and, two, endorsing through the Vietnam Standard and Quality Institute, the ISO 26000:2010 standards as Tiêu chuán Viêt Nam or TCVN ISO 26000:2013 standards (Socialist Republic of Vietnam (SRV), 2012; Tran & Jeppesen, 2016; Anner, 2018). The ISO 26000:2010 standards intend to assist businesses in contributing to sustainable development through their CSR practices. However, despite the attempts to make CSR more socially inclusive in Vietnam, the concept has been emerging for decades and is generally treated by policymakers as an add-on subject that has weak compliance with international and domestic regulatory standards and is regarded mainly as philanthropic by its community (Tran & Jeppesen, 2016; Tran, 2017; Khanh 2018; Nguyen et al., 2018). Moreover, due to the country's large Confucianism following, policymakers believe that the Westernised CSR framework might not withstand the complexities in the Vietnamese context (Nguyen et al., 2018; Minh, 2021).

Public and private sector cooperation. Vietnam's one-party system control most of the public and private sectors. However, there is growing socio-economic advocacy for greater independent regulation of business practices in Vietnam, with greater regard to CSR (Khanh, 2018; Nguyen & Trinh, 2020). This push by businesses is to self-regulate their CSR interventions independently from the government's operational involvement but for government to provide legislative direction and act as enforcers.

4.3 China

Business-driven activities and initiatives. According to Ewing and Windisch (2007:3), historically embedded within the records of Chinese culture and philosophy (Confucianism), businesses "doing well by doing good" are considered by many as a social norm. Confucianism, in the main, promotes compassion towards others, righteousness in human relationships and a sincere desire to contribute towards societal wellbeing (Nguyeni et al., 2018).

Civil society involvement and socio-economic impact. Since introducing CSR reforms in the retail sector, it has become a crucial co-contributory driver of the country's socio-economic development. In a trend and development study conducted by Naseem et al. (2019) on CSR disclosure in Chinese listed companies, including retail companies, it was found, among other findings, that CSR initiatives across all sectors in China are primarily driven by social pain points underscored by mainstream civil society organisations (CSOs). However, the positive trajectory is not without its drawbacks. In an explorative study conducted among 15 companies in various sectors, it was found that their disclosed information primarily serves no value to stakeholders (Wu & Pupovac, 2019). Without reliable social sustainability information to stakeholders, measuring society's involvement and the various degrees of CSR's socioeconomic impact can be lacking.

Political-driven nature of CSR practices and compliance with national legislation and international protocols and conventions. The Chinese government reviewed its Companies Act in 2005 with the inclusion of some welcomed adjustments. The amendments, although described as vague by commentators, obligate businesses, including the retail sector in China, to be subject to scrutiny, comply with the country's statutes, submit to ethics and morality, act in good faith and embark on socially responsible activities (Lin, 2010; Jiang & Kim, 2015). According to Zhou et al. (2017:23), the amendments introduced a clear definition of CSR. In addition to the amendments, the Chinese government has published several other directives aimed at different areas of CSR. Among the fundamental directives are the introduction of CSR initiative disclosure and financial contributions for all businesses listed on the Shenzhen and Shanghai stock exchanges (Zhou et al., 2017). Furthermore, in December 2021, the Standing Committee of the 13th National People's Congress released additional draft amendments to the Company Act for comments (Ross et al., 2022). Critical to the proposed amendments are the strengthening of CSR practices, i.e. for businesses to have greater regard for the interest of stakeholders, to encourage businesses to participate in social welfare activities and for businesses to publish social responsibility reports.

Public and private sector cooperation. The Chinese government participate relatively in collaboration projects with the private sector. The country has ranked among the top public and private collaborators on the Asian belt (World Bank, 2016; Tan & Zhao, 2020). However, despite the public sector's high cooperation initiatives with the private sector, the collaborations are more vested in infrastructure development than social development (Osei-Kyei et al., 2019).

4.4 Poland

Business-driven activities and initiatives (other than philanthropy). After 2007, the rapid emergence of hypermarkets and retail chain stores led to a saturation of retail outlets in a country hampered by deprivation (Oczkowska & Smigielska, 2010; Dyczkowskaa et al., 2016). As a result, most of these retail outlets would regularly collect surplus food that is at times expired and offer it to the poor or reactively, in times of crises, offer material and financial assistance to the needy (Smigielska & Oczkowska, 2017). However, this trend is slowly waning as retailers in Poland work to shake this image and refocus their CSR interventions by (1) focusing on socio-economic development and ecological protection; (2) implementing voluntary international standards such as the ten principles of the United Nations Global Compact; and (3) complying with the country's statutory regulations in the wake of the economic downturn in Southern Europe (Simöes & Sebastiani, 2017; Habek et al., 2018. Although CSR reporting in Poland is on the upsurge, the drawback is that the general reporting practices on actual CSR initiatives and their impact have endured sporadic and fragmented reporting (Mazur, 2015; Habek et al., 2018).

Civil society involvement and socio-economic impact. Notwithstanding the intrinsic obstacles that emerged during the early stages of CSR realisation and implementation in Poland, the contemporary focus of deepening its understanding regarding the concept's relevance and beneficial effects for both individuals and society is on the uptake. A deliberate effort is made to demonstrate regard for social stakeholders and greater awareness and improves the effectiveness of CSR courses in Poland's tertiary institutions to encourage social involvement (Wolska & Kizielewicz, 2015; Grabara et al., 2016; Dancewicz, 2019; Kusio, 2021).

Political-driven nature of CSR practices and compliance with national legislation and international protocols and conventions. The polish government developed a national policy for CSR with a series of onset steps (Simeonov, 2013). However, since the policy development, the government and businesses at large have been preoccupied with capacity building and managing sustainability issues, neglecting to strengthen foundational CSR issues (Dyduch & Krasodomska, 2017). However, the general pace of this trend is determined by the aptitudes of the various stakeholders involved in it to persevere with the momentum (Potocki, 2015; Dyczkowskaa et al., 2016). According to Potocki (2015), the government of Poland "ought to become a model of ethical conduct and therefore transform into a trustworthy institution because otherwise its decisions and activities will never win social recognition". The lack or no effectiveness of a robust government drive to CSR contrasts with the deliberate efforts made by the business for a more significant socio-economic impact of its actions.

Public and private sector cooperation. Generally, collaborations between the public and private sectors are regarded as mutual supplementary support to achieve a common objective. Similarly, according to Wolska and Kizielewicz (2015), businesses that are socially responsible and operate in Poland will significantly support the public sector in addressing the array of social problems in the county. But unfortunately, cooperation between the sectors is relatively minimal and underdeveloped (Simeonov, 2013; Kusio, 2021).

4.5 Germany

Business-driven activities and initiatives (other than philanthropy). According to Bleher et al. (2013), German retail businesses are starting to communicate their interventions broadly and cover various issues in different publication mediums. However, only a few business groups published progressive CSR reports that comply with the GRI Standards' requirements, indicating that although it's only a few businesses, steps are taken in line with international best practices (Global Reporting Initiative (GRI), 2018; Safari & Areeb, 2020).

Civil society involvement and socio-economic impact. CSR in Germany is rooted in its socio-economic system with a non-sector-specific approach (Simeonov, 2013). This approach sees the government pushing for an overall CSR strategy through the multi-stakeholder National CSR Forum rather than sector-specific initiatives. The National CSR Forum, an advocate for socio-economic development, was applauded in 2015 by Andrea Nahles, the then Federal Labour Minister, for its dedication and commitment to the socio-economic system (Federal Ministry of Labour and Social Affairs (FMLSA), n.d).

Political-driven nature of CSR practices and compliance with national legislation and international protocols and conventions. According to Bauer (2018), the German government has adopted a multi-stakeholder approach to leading by example. As a result, it has developed several tools, ranging from interactive government websites to providing CSR information for businesses and sectors to use as a blueprint when developing CSR guidelines.

Germany has a vibrant public and private sector cooperation regime enacted through a forum. Although fragmented, the forum focuses mainly on coalitions and partnerships and is driven by the Ministry of Economics and Labour (Sun, 2018). The forum comprises inter-agency bodies and different federal government ministries that work closely with the private sector and civil society (Nasrullah & Rahim, 2014; The Federal Government, 2017).

4.6 The United Kingdom

Business-driven activities and initiatives (other than philanthropy). A trend observed during the last few years with the advent of Covid 19 is the relative generosity of businesses across sectors. Despite the increased business-driven initiatives, it isn't easy to classify them as business value-driven, benevolent, responsive or publicity-driven activities. In a study conducted by Ahmed et al. (2021), they found that several businesses, including retailers, have provided a great deal of humanitarian assistance to communities and their employees in general as a response to the Covid-19 disaster. The researchers further state it was difficult to ascertain if the disaster-related initiatives were part of the business CSR activities since many, other than summarised highlights, make public complete CSR strategies. However, in another case study conducted at a major retailer by Dal Mas et al. (2022), it was found that it had a CSR strategy. Still, the activities it reported on were spread over several business units with no dedicated oversight department. Uncoordinated CSR activities could potentially dilute the initiative's envisioned outcome and socio-economic impact.

Civil society involvement and socio-economic impact. The British civil society is very much involved in CSR to the degree that there is a debate that business behaviour might be, to a degree, powerfully predisposed to society involvement ( Voegtlin et al., 2012; Vertigans, 2015). Due to the close involvement of civil society, in the study conducted by Dal Mas et al. (2022), it was found that social stakeholders have raised concerns over the lack of credible CSR information in the retail sector and doubts about the fundamental socio-economic impact and environmental changes along the retail value chain.

Political-driven nature of CSR practices and compliance with national legislation and international protocols and conventions. The UK saw the appointment of a Minister of CSR in early 2000 to oversee the development of CSR policies and guidelines (Mullerat, 2013; Simeonov, 2013). Introduced in 2006, the UK's pioneering Companies Act has been deemed a comprehensive guideline with impending repercussions for several CSR actors (Keay & Iqbal, 2018). According to Horrigan (2007), the Act explicitly obligates directors to manage the business' risk exposure, do corporate reporting and compels businesses to have a greater stakeholder sensitivity in their structure content and implementation. The Act also obligates directors to act in good faith while considering the impact of their operations on the broader community and the natural environment (Keay & Iqbal, 2018). In the UK, sector-specific policies are primarily enacted by regulatory agencies and not necessarily by government departments - exhibiting a relatively flexible approach (Simeonov, 2013).

Public and private sector cooperation. UK allows CSR collaborations to operate more under a liberal partnership-based paradigm between businesses and NGOs with little government involvement (Nasrullah & Rahim, 2014). These partnerships are seen as mutually beneficial for both businesses and NGOs. NGOs use partnerships primarily as a funding source and or partner to address the course(s) or material concern(s) it advocates (Rohwer & Topic, 2019).

4.7 Brazil

Business-driven activities and initiatives (other than philanthropy). Brazilian businesses considerably improved their understanding of the CSR concept. These are significant signals that Brazilian businesses are incorporating CSR into their business strategies and that CSR may advance beyond the discourse field. In an analytical study conducted by Do Prado et al. (2012), in which they studied the internet sites and other secondary sources of 10 prominent retailers in Brazil, it was found that the sampled retailers do publish annual responsible practice reports (Do Prado et al., 2012). On the other hand, a trend has emerged in some Brazilian retail segments, such as the banking sector, in which a large portion of the sector elects to hire CSR communications to institute a set of publicity initiatives that are specifically developed to enhance the interest, image and offerings of the business but reported as CSR interventions (Scharf & Fernandes, 2013). This reporting practice potentially contributed to some extent to the reason why a significant portion of the Brazilian population views its banking sector with scepticism.

Civil society involvement and socio-economic impact. The private sector has primarily driven CSR in Brazil without much stakeholder involvement. According to Sinay et al. (2019), several businesses, including retail sectors, lack transparency, issue, and stakeholder management. The researchers also found that the broader business sector needs to find ways to involve civil society in its activities to increase the impact of its interventions.

Political-driven nature of CSR practices and compliance with national legislation and international protocols and conventions. CSR and its aspects in Brazil are steadily growing, and there were advances to make reporting compulsory by introducing various standards (Lima Crisostomo et al., 2014). Prevalent standards used either as a standalone or in combination by Brazilian businesses are those introduced by the Brazilian Institute of Social and Economic Analysis or IBASE, GRI standards and the International <IR> Framework. IBASE seeks to reinforce the associative fabric of civil society, build an autonomous culture of rights, extend the inclusion of citizen participation in policymaking and advance the social balance sheet model to track social activities in Brazil (Institute of Social and Economic Analysis (IBASE), n.d; Sinay et al., 2019). Whereas GRI standards focus on systematically and transparently reporting the impacts of a business's activities to stakeholders, the <IR> aims to enhance the quality of information about how the businesses resources "the capitals" was used and going to be used into the future to create or preserve value (GRI, n.d; International Integrated Reporting Council (IIRC), 2013).

Public and private sector cooperation. Although some policies are in place, the government generally keeps a modest distance from CSR interventions. There is a sporadic collaboration with non-state actors implementing civil society CSR promotional activities (Lima Crisostomo et al., 2014; Bremermann et al., 2019).

4.8 The United States of America

Business-driven activities and initiatives (other than philanthropy): Businesses in the USA moved away from seeing CSR mainly as a public relations and compliance function to incorporating it into the organisational strategy. There is also a shift from CSR being largely publicity-focused to any philanthropy or acts of alm being more impact-based (DeCourcey, 2020). The issued CSR reports discuss topics ranging from well-spread background information on the retailer to its ecological and community involvement, with very little CSR financial disclosure and information on CSR social impact (Patten & Zhao, 2014). This type of disclosure trend has been a long-standing concern in that retailers' standalone reports appear to be more about discussing strategies and the image of the business rather than providing meaningful implementation, action, performance and impact data (Cho et al., 2014; Patten & Zhao, 2014). However, Patten and Zhao (2014) believe this trend might change for the better as retailers become knowledgeable in meeting the requirements of standalone reporting. Internationally, other observers argue that taking into consideration the infrequent deceptive financial reporting practices, issuing third-party assurance certificates on CSR reports can add to the trustworthiness of these reports ( Casey & Grenier, 2015; Birkey et al., 2016). However, CSR reporting has gained momentum in the USA (Birkey et al. (2016), and most of the published CSR reports lack external assurance (Peter, 2021).

Civil society involvement and socio-economic impact. Communities have a relatively large involvement in CSR in the USA. The concept is mainly driven by business and civil society (Singh & Misra, 2021). On the business end, CSR has historically primarily been used as a public relations and compliance function. However, it is slowly re-establishing itself as a strategic function with measurable outcomes-based activities with more significant socioeconomic impact (DeCourcey, 2020).

Political-driven nature of CSR practices and compliance with national legislation and international protocols and conventions. Although several states generally support CSR, the activities between states vary considerably due to the federal constitutional republic political system and the separation of powers between the federal and state governments (Welzel et al., 2007). Policymakers in the USA scarcely intervene in the social responsibility interventions enacted by businesses or in issues about ecological change. Discretion is left to the businesses to be the leaders and drivers of CSR interventions chosen and decide on the best probable sustainable ecological behaviours (Camilleri, 2017).

Public and private sector cooperation. Public and private sector collaboration varies from state to state, mainly due to the separation of powers between the federal and state governments. However, as a general federal restraint as government, they refrain from getting involved in CSR activities of the business (Tang et al., 2015; Camilleri, 2017).

4.9 Africa

Unlike first-world countries, CSR in Africa goes beyond conceptualising the concept as inferred and applied by the developed countries. Instead, the concept is applied in Africa to incorporate the role of businesses in poverty alleviation. The following three subsections give an all-embracing CSR trend and analysis of Mozambique, Egypt and Kenya as part of the African continent contingent.

4.9.1 Mozambique

Business-driven activities and initiatives (other than philanthropy). Global retail entries into Mozambique face certain constrictions, ranging from language barriers and restrictive laws to stringent regulations for the largely informal retail sector (Aga et al., 2019; Louw et al., 2019). Nevertheless, despite the lack of coordination and a systematic approach to CSR activities from the business sector, CSR-related activities are slowly increasing (Ferri et al., 2021).

Civil society involvement and socio-economic impact. Generally, civil society other than foreign aid organisations has little involvement in CSR activities in Mozambique. According to Madime and Goncalves (2022), the government and society, in general, seem to have still not realised the potential socio-economic value and impact that can be harnessed from CSR initiatives if applied correctly.

Political-driven nature of CSR practices and compliance with national legislation and international protocols and conventions. Despite the economic upturn, the government has been inefficient and ineffective in significantly reducing deprivation levels and providing a broader basis for socio-economic development or CSR guidance (Castel-Branco, 2014; Kaufmann & Simons-Kaufmann, 2016). The Global Compact Network established by the United Nations in Mozambique's uptake failed and was abandoned in 2010 (Thomsen, 2010). According to Kaufmann and Simons-Kaufmann (2016), the country is not following an explicit political-economic vision or strategy but instead applies a mix of various political concepts with different elements. These range from neo-liberal principles to strong socialist ideologies. However, given the weak state capacity and compliance enforcement, CSR in that country is more driven towards minimum compliance to the few legislative guidelines than an attempt to go beyond compliance.

Public and private sector cooperation. Mozambique's retail economy has been driven mainly by small to medium family-owned or multi-national enterprises. However, ongoing public sector corruption has hampered corporations between the government and the private sector (Thomsen, 2010; Nuvunga & Orre, 2019). Where there are collaborations, according to Nuvunga and Orre (2019), the partnerships are tainted. Nuvunga and Orre (2019) found that the common practice is for public officials to participate in public-private cooperative negotiations and acquire a shareholding in a private company that collaborates with the public sector.

4.9.2 Egypt

Business-driven activities and initiatives (other than philanthropy). Several Egyptian businesses, including some retailers, report annually on their CSR activities (Soliman et al., 2013). However, according to Elsayed (2018), under military rule, the economic condition in Egypt weakened and was aggravated by constraints on foreign donations, funding and humanitarian work. The Egyptian retail sector was initially overshadowed by small-scale, primarily family-owned shops that largely disregarded mainstream distribution channels and showed little to no interest in the CSR concept as it was applied in the rest of the world (El-Amir & Burt, 2008; Zidan, 2015). Although there was some minimal entrée of international businesses into the retailing environment over the years, they had a marginal effect on the general CSR practices in the Egyptian retail sector (Ziyadat, 2019). Most Egyptians do not place much weight on the likely impact of CSR, considering the constraints placed on CSOs and the socio-economic conditions ( Eshra & Beshir, 2017; Elsayed, 2018).

Civil society involvement and socio-economic impact. In post-revolutionary Eqypt, citizens are getting increasingly involved in CSR and participating in activism for the concept; however, there has been limited change in the CSR practice (Alshorbagy, 2016). Egypt lacks a formal institutional framework for organising sustainable development goals or similar strategies to its CSR activities to make the socio-economic impact of the concept more measurable in that country. Civil society has limited CSR involvement and has a hostile and constrained relationship with government and business (Osman, 2021).

Political-driven nature of CSR practices and compliance with national legislation and international protocols and conventions. The government's role in advancing CSR in Egypt is largely ineffective (Alshorbagy, 2016). Alshorbagy also states that the concept in Egypt is generally underdeveloped, and it seems that there is no political will to drive the CSR practice. The lack of a formal government framework to guide CSR in Egypt leads to a missing opportunity by the government to link the onset of CSR to sustainable development strategies or goals (Abdelhalim & Eldin, 2019).

Public and private sector cooperation. Historical political instability in Egypt has generally slowed or halted public-private partnerships to a large extent. However, in recent times public partnerships in Egypt have been mainly used to revitalise the country's education system and infrastructure development (Helmy et al., 2020). The collaborations are driven by strong government support to see the successful implementation of partnership projects.

4.9.3 Kenya

Business-driven activities and initiatives (other than philanthropy). Kenya is one of several countries on the African continent plaque with socio-economic developmental challenges. A study conducted in the banking sector found that the problems affecting the implementation of CSR strategies by banks in Kenya were mainly due to the extent of deprivation in the country and the country's elevated tax rates (Mbogoh & Ogutu, 2017). According to Cheruiyot and Tarus (2016), business-driven CSR in Kenya is, to a large extent, still in its infancy and underdeveloped.

Civil society involvement and socio-economic impact. CSR in Kenya is driven mainly by international and civil society organisations. The work of the United Nations generally influences the concept's practices in Kenya, NEPAD (New Partnership for Africa's Development) and international civil society organisations focusing on overarching human rights issues rather than issues related explicitly to CSR (Cheruiyot & Tarus, 2016).

Political-driven nature of CSR practices and compliance with national legislation and international protocols and conventions. The Kenyan government has initially been averse to imposing guidelines and standards and/or facilitating regulations on businesses that encourage CSR interventions that address the country's socio-economic challenges (Gachanja et al., 2013; Nyaga, 2016). However, with the succour of the Dutch Ministry of Foreign Affairs, it would appear that the Kenyan government has shifted its stance against CSR interventions in the country. The Dutch government funded the Kenyan Knowledge Management Centre to modernise the understanding of the CSR concept in the country and stimulate a multi-stakeholder cooperative approach to CSR (Moratis & Slaa, 2016). Mbogoh and Ogutu (2017) believe that the Kenyan government should tackle the poverty levels and the excessive taxes head-on. They also posit that the banking sector should understand and consult the communities in which it operates and on matters that affect them. Despite the above, CSR in Kenya is gaining traction (Kariuki, 2021).

Public and private sector cooperation. Kenya has a vibrant cooperation between the public and private sectors. Collaboration projects span from education and green energy to food security (Achiba, 2019; Robinson, 2022). Considering the government's broader role in providing basic services, collaborations between the public and private sectors have contributed greatly towards that country's developmental maturity.

5. SYNOPSIS OF BEST PRACTICES AND LESSONS LEARNED

During the analysis, what became evident is that different countries on different continents are at different maturity levels and focus on various aspects of CSR. Table 3 sets out a tabulated synopsis of CSR praxes in developed and developing countries per the analysed continents.

Internationally, the CSR focus in countries such as Vietnam, Poland, Brazil and Egypt are progressively shifting to an early onset of transformative CSR. Countries such as China, the USA and Kenya show promise in their advancement towards becoming mature in transformative CSR practices. India and the UK have shown the most transformative CSR progression in their practices. In Africa, Kenya is gradually moving towards a transformative CSR nation, with Egypt as a clear contender among the countries selected on the continent. This suggests that in addition to Africa's changing economic climate, there are observable changes to the political will of the continent's legislators. It can be inferred that businesses operating on the African continent's CSR initiative are essentially charitable or philanthropic actions. Therefore, they need to transform these practices, enhance their stakeholder relations and participate in more meaningful and sustainable CSR interventions.

6. DISCUSSION

This article explored the global and domestic transformative CSR trends and perspectives on four continents, Asia, the Americas, Europe and Africa, with the aim to determine the notable mediating aspects through which CSR has been found to affect transformative socioeconomic development.

Regarding the business-driven activities and initiatives (other than philanthropy), the study found that all sample countries' businesses drive CSR to some extent, although in different variations. Some of the significant praxes, for example, are in India, where retailers are obligated to have dedicated teams managing the development, implementation and funding model of the business' CSR activities and initiatives. Other than enhancing compliance with national and international CSR standards and legislature, Poland's refocused activities and initiatives axle the contribution CSR can make to the country's socio-economic development agenda. Brazil developed standards to refine concerns such as material issues and stakeholder management and transparency within its local context. The US retail sector shifted its CSR activities from primarily a compliance requirement and public relations function to one of the business's strategic objectives. US businesses are also taking the initiative to comply with the reporting guidelines set by international organisations to provide meaningful CSR performance and impact data. Considering the principle elements of the DNA model of transformative CSR, businesses and, more specifically, the retail sector should creatively reassess the materiality of their socio-economic value creation (Visser, 2014). Furthermore, the reassessment outcomes must be aligned with the transformative socio-economic agenda of a country (World Bank Group, 2018). To transition from the conventional CSR to a transformative CSR practice, the board of directors must redefine their transformative goals through redesigned key indicators, allowing for the scalability of transformative CSR interventions that are responsive to societal material needs through a measurable strategy (B-BBEE Commission, 2020; MLJ, 2013; 2019).

Concerning civil society involvement and socio-economic impact, the study found that although CSR in its construction advocate for greater civil society involvement in social interventions and promotes interventions with sustainable socio-economic impact, most of the continents assessed to have no to little regard for stakeholder engagement. However, in countries such as India, China and the UK, there is some civil society involvement through NGOs and Civil Society Organisations. To effect transformative CSR, capacity needs to be built amongst the implementation or representative agencies (NGOs), and businesses need to put in place intervention measuring tools and methodically report on their intervention impact to stakeholders (Hoffman, 2013; GRI, n.d.; Kumar, 2019).

With reference to the political-driven nature of CSR practices and compliance with national legislation and international protocols and conventions, the study shows that most of the sample countries, to some extent, make some legislative contribution towards CSR. For example, the study found that India reviewed its Companies Act to set distinguishable criteria that exclude marketing, public relations, or employee-related activities from CSR activities. In addition, retailers that exceed a specific size must establish a CSR committee that is directly accountable to the board. Finally, the board must ensure that the CSR policy is approved and that the required funding is available for CSR activities and initiatives. Unlike the explicit articulation in the Indian case, both 21st-century amendments in the South African context fell short of such clear expression (DTIC, 2018; 2021). Similarly, the UK board of directors is obligated to do corporate reporting, have greater stakeholder sensitivity, and consider the impact of their operations on civil society and the environment. In the South African context, the board of directors is accountable in terms of regulations 26 and 43 of the Companies Act 71 of 2008. The Companies Act 71 of 2008 also stipulates that specific social and ethical activities, principles and constitutional rights must form an essential part of the governance structure of the business (Kirby, 2014; Visser, 2012b). The assessment further revealed that the Vietnam policymakers assumed that the Western CSR frameworks might not endure the country's cultural complexities. Similar views have been articulated in South Africa in that socio-economic development and transformation in the country are unique (The Presidency, 2020; Visser, 2012b), particularly when considering the South African cultural complexities and its historical past (Reeve & Pincin, 2018; Visser, 2006). Therefore, it is articulated that for transformative CSR to succeed, the Western CSR frameworks might not be fully applicable, more so where the political-drive is to effect compliance to the concept and to an extent, advancing poverty alleviation and socio-economic transformation through statute and international protocols (Abdulai; 2015; Nguyen et al. 2018; World Bank Group, 2018).

With regard to public and private sector cooperation, the study identified no significant scientifically analysed CSR-focused collaborations between government and business. However, to some extent, India and Brazil have some interventions executed mainly by NGOs rather than the private sector directly. Transformative CSR fundamentally builds on the prerequisite that government and businesses accept its obligatory socio-economic responsibility to participate and collaborate on CSR activities to advance the common good (Carroll, 1999; Edi, 2020; The Presidency, 2020).

7. RECOMMENDATIONS

Based on the literature review and the lessons learned from the international experience, the following practical recommendations and areas for further research are suggested:

• The lessons learned from the international experience underscore the centricity of government as a transformation driver. Considering the sluggish impact of the concept in countries where its articulation is vague against the reasonable success where its articulation is explicit and conspicuous, governments ought to reassess their stance. Governments, as change drivers, have a crucial role in their responsiveness by setting the governance agenda through explicit legislative interventions.

• The experiences in various countries underscore fundamentally the importance of directors redefining their CSR strategic intend with the inclusion of stakeholders in order for the transformative CSR interventions to have a greater socio-economic impact. Governments ought to be more explicit and unapologetic in their drive to transform the CSR practice in the country in order for the broader business sector, including the retail sector, to comply with statutes and standards in order to drive the broader socio-economic transformative agenda.

• CSR has developed from being a main goodwill concept into a management function that needs to be driven by business. Therefore, a business should be elevated and incorporate the function as a business unit with strategic management considerations.

• Collaborations between the government and the private sector are increasingly becoming more relevant in the CSR context. This is because the sectors share a common objective: both are concerned with sustainable socio-economic development.

• The literature and document reviews underscore the importance of public and private sector collaboration to enhance the socio-economic impact of CSR. Further research is recommended with a specific focus on the respective CSR-specific cooperation between sectors toward the implementation of common material CSR issues and the consequent impact.

• The retail sector is a vast layered industry consisting of various segments. The sector and its segments still appear to be understudied, despite its significance in the socioeconomic developmental value chain and the sector's proximity to communities. It is recommended that greater attention be given to the research area. Different theoretical investigations into the retail sector's CSR applications would not only expand the scientific knowledge base, but they would also encourage the sectors' various segments to improve their reporting and, therefore, better communicate the impact of their interventions and enhance compliance with statutes and standards.

8. CONCLUSION

This paper analysed CSR business praxes in various countries regarding the status of a transformative agenda in business. It was established that the application of the DNA model could serve as a valuable instrument to guide businesses towards broader socio-economic development. It is evident that businesses should set key CSR indicators that conform to this transformative agenda and that third-party oversight structures should enhance their vigilance in monitoring businesses' legislative compliance with socio-economic developmental policies and strategies. Governments can draw from the lesson and experiences of these countries to design more suitable and domain-specific interventions.

It is further apparent that several lessons can be learned from South Africa's pursuit to enhance the impact of conventional CSR practices in retail and in the broader business sector. The outcomes of the study offer insight and several implications not only for further exploration but also for CSR applications. It provides insight into the general direction CSR is taking internationally and informs government institutions that despite the variations in CSR applications in the international experience, the developmental role of CSR in socio-economic transformation is undisputed. The study furthermore directs scholarly inquiry by accentuating transformative socio-economic aspects of CSR as the study domain.

The availability of scientific studies conducted in English in certain countries limited a more extensive case study analysis. However, the authors solaced that transformative CSR is still emerging as a scholarly field of investigation and that this study is a vital prelim for further exploration.

REFERENCES

Abdulai, D. 2015. From charity to mutual benefit: a new and sustainable look at CSR in Africa. In O'Riordan, L., Zmuda, P. & Heinemann, S. (eds). New perspectives on corporate social responsibility: locating the missing link. Esson: Springer. pp. 422-442. [ Links ]

Abdelhalim, K. & Eldin, A.G. 2019. Can CSR help achieve sustainable development? Applying a new assessment model to CSR cases from Egypt. International Journal of Sociology and Social Policy, 39(9/10):773-795. [https://doi.org/10.1108/IJSSP-06-2019-0120]. [ Links ]

Achiba, G.A. 2019. Navigating contested winds: development visions and anti-politics of wind energy in northern Kenya. Land, 8(1):1-29. [ Links ]

Adams, D., Adams, K., Ullah, S. & Ullah, F. 2019. Globalisation, governance, accountability and the natural resource 'curse': implications for socio-economic growth of oil-rich developing countries. Resources Policy, 61:128-140. [ Links ]

Aga, G., Campos, F., Conconi, A., Davies, E. & Geginat, C. 2021. Informal firms in Mozambique: status and potential. [Internet: https://openknowledge.worldbank.org/bitstream/handle/10986/35883/Informal-Firms-in-Mozambique-Status-and-Potential.pdf?sequence=1; downloaded on 15 July 2021]. [ Links ]

Agrawal, S. & Chandrika, K. 2018. Corporate social responsibility: an enabler to inclusive growth. International Journal of Management and Information Technology, 3(2):37-41. [ Links ]

Ahmed, J.U., Islam, Q.T., Ahmed, A., Faroque, A.R. & Uddin, M.J. 2021. Corporate social responsibility in the wake of COVID-19: multiple cases of social responsibility as an organizational value. Society and Business Review, 16(4):496-516. [https://doi.org/10.1108/SBR-09-2020-0113]. [ Links ]

Al-Mohamad, S., Rashid, A., Bakry, W., Jreisat, A. & Vo, X.V. 2020. The impact of BRICS formation on portfolio diversification: Empirical evidence from pre-and post-formation eras. Cogent Economics & Finance, 8(1):1-19. [https://doi.org/10.1080/23322039.2020.1747890]. [ Links ]

Alshorbagy, A.A. 2016. CSR and the Arab spring revolutions: how is CSR not applied in Egypt. Wisconsin International Law Journal, 34(1):1-30. [ Links ]

ANC (African National Congress). 2017. Social transformation discussion document. Johannesburg: African National Congress. (5th National Policy Conference 30 June to 5 Jul.). [Internet: https://anc1912.org.za/wp-content/uploads/2022/08/National-Policy-Conference-2017-Social-Transformation.pdf; downloaded on 15 November 2021]. [ Links ]

Anner, M. 2018. CSR participation committees, wildcat strikes and the sourcing squeeze in global supply chains. British Journal of Industrial Relations, 56(1):75-98. [ Links ]

Bauer, T. 2018. CSR in Germany: the role of public policy. The critical state of corporate social responsibility in Europe. Critical Studies on Corporate Responsibility, Governance and Sustainability, 12:101-120. [https://doi.org/10.1108/S2043-905920180000012005]. [ Links ]

Balasubramanian, N., Kimber, D. & Siemensma, F. 2005. Emerging opportunities or traditions reinforced? An analysis of the attitudes towards CSR, and trends of thinking about CSR, in India. Journal of Corporate Citizenship, 17:79-92. [ Links ]

B-BBEE Commission. 2020. National status and trends on broad-based black economic empowerment. Pretoria. [Internet: https://bbbeecommission.co.za/wp-content/uploads/2020/07/National-Status-and-Trends-on-Broad-Based-Black-Economic-Empowerment.pdf; downloaded on 18 January 2022]. [ Links ]

Birkey, R.N., Michelon, G., Patten, D.M. & Sankara, J. 2016. Does assurance on CSR reporting enhance environmental reputation? An examination in the US context. Accounting Forum, 40(3):143-152. [ Links ]

Bleher, D., Brunn, C., Moon, J. & Chapple, W. 2013. Impact measurement and performance analysis of CSR (IMPACT): the future impact of CSR in the food retail sector on climate change. CSR Impact, November:1-67: 1-67. [Internet: https://www.oeko.de/oekodoc/2247/2015-028-en.pdf; downloaded on 9 March 2022]. [ Links ]

Blowfield, M. 2004. CSR and development: is business appropriating global justice? Development, 47(3):61-68. [ Links ]

Botha, T. 2016. Responsible leadership. In Lamb, A. (eds). Corporate citizenship. Cape Town: Oxford University Press. pp. 115-132. [ Links ]

Bowen, H.R. 1953. Social responsibility of the businessman. New York, NY: Harper. [ Links ]

Brown, G. 2018. Leading change: change we initiate vs imposed change. Leadership Excellence, 35(7):34-36. [ Links ]

Bremermann, L.E., Teplov, R., Mortazavi, S., Väätänen, J. & Gupta, S. 2019. Public-private partnership as a mechanism to encourage MNEs' contributions to sustainable development goals: Insights from Brazilian experience. [Internet: https://www.researchgate.net/publication/337204022_Public-private_partnership_as_a_mechanism_to_encourage_MNEs%27_contributions_to_sustainable_development_goals; downloaded on 14 December 2022]. [ Links ]

Camilleri, M.A. 2017. Corporate social responsibility policy in the United States of America. In Idowu, S.O., Vertigans, S. & Burlea, S.A. (eds). Corporate social responsibility in times of crisis: practices and cases from Europe, Africa and the world. New York, NY: Springer. pp. 129-143. [ Links ]

Carroll, A.B. 1991. The pyramid of corporate social responsibility: toward the moral management of organisational stakeholders. Business Horizons, 34(4):39-51. [ Links ]

Carroll, A.B. 1999. Corporate social responsibility: evolution of a definitional construct. Business and Society, 38(3):268-295. [ Links ]

Casey, R.J. & Grenier, J.H. 2015. Understanding and contributing to the enigma of corporate social responsibility (CSR) assurance in the United States. Auditing: A Journal of Practice and Theory, 34(1):97-130. [ Links ]

Castel-Branco, C.N. 2014. Growth, capital accumulation and economic porosity in Mozambique: social losses, private gains. Review of African Political Economy, 41(1):26-48. [ Links ]

Castillo, V.E., Mollenkopf, D.A., Bell, J.E. & Bozdogan, H. 2018. Supply chain integrity: a key to sustainable supply chain management. Journal of Business Logistics, 39(1):38-56. [ Links ]

Cheruiyot, T.K. & Tarus, D.K. 2016. Corporate social responsibility in Kenya: Reflections and implications. [Internet: https://www.researchgate.net/publication/292286410_Corporate_Social_Responsibility_in_Kenya_Reflections_and_Implications; downloaded on 14 December 2022]. [ Links ]

Cho, C.H., Michelon, G., Patten, D.M. & Roberts, R.W. 2014. CSR report assurance in the USA: an empirical investigation of determinants and effects. Sustainability Accounting, Management and Policy Journal, 5(2):130-148. [ Links ]

Clarkson, M.B.E. 1995. A stakeholder framework for analyzing and evaluating corporate social performance. Academy of Management Review, 20(1):92-117. [ Links ]

Commission of Inquiry into State Capture. 2019. The judicial commission of inquiry into allegations of state capture. [Internet: https://www.sastatecapture.org.za/; downloaded on 31 March 2019]. [ Links ]

Dal Mas, F., Tucker, W., Massaro, M. & Bagnoli, C. 2022. Corporate social responsibility in the retail business: a case study. Corporate Social Responsibility and Environmental Management, 29(1):223-232 [ Links ]

Dancewicz, B. & Struve, F. 2019. The Influence of MNEs on CSR in Poland. In Dtugopolska-Mikonowicz, A. & Przytuta, S. & Stehr, C. (eds). Corporate Social Responsibility in Poland. New York, NY: Springer. pp. 149-165. [ Links ]

Deepa, S. & Chitramani, P. 2015. CSR in the retailing industry: a case of three retail stores. International Journal of Business and Administration Research Review, 3(9):128-135. [ Links ]

DeCourcey, M. 2020. Looking ahead: top CSR trends for 2020. US Chamber of Commerce Foundation. [Internet: https://www.uschamberfoundation.org/blog/post/looking-ahead-top-csr-trends-2020; downloaded on 20 February 2020]. [ Links ]

Do Prado, L.S., Mafud, M.D., Merlo, E.M. & Neves, M.F. 2012. Corporate social responsibility: retail actions in Brazilian market. São Paulo: University of São Paulo Press. [ Links ]

DTIC (Department of Trade, Industry and Competition). 2015. Department of Trade and Industry: the amended codes of good practice for the broad-based black economic empowerment amendment act. (Notice 408). Government Gazette, 38766, 6 May. Pretoria: Government Printer. [ Links ]

DTIC (Department of Trade, Industry and Competition). 2018. Companies Amendment Bill. Pretoria: Government Printer. [ Links ]

DTIC (Department of Trade, Industry and Competition). 2021. Companies Amendment Bill. Pretoria: Government Printer. [ Links ]

Duiker, W.J. 2018. The communist road to power in Vietnam. 2nd ed. New York, NY: Routledge. [ Links ]

Du Plessis, N. & Grobler, A.F. 2014. Achieving sustainability through strategically driven CSR in the South African retail sector. Public Relations Review, 40(2):267-277. [ Links ]

Dyczkowskaa, J., Krasodomskab, J. & Michalakc, J. 2016. CSR in Poland: institutional context, legal framework and voluntary initiatives. Accounting and Management Information Systems, 15(2):206-254. [ Links ]

Dyduch, J. & Krasodomska, J. 2017. Determinants of corporate social responsibility disclosure: an empirical study of Polish listed companies. Sustainability, 9(11):1934. [ Links ]

Edi, A.C. 2020. Can CSR be politically transformative? discussing its prospects and challenges. Politika: Jurnal Ilmu Politik, 11(1):76-95. [ Links ]

El-Amir, A. & Burt, S. 2008. Sainsbury's in Egypt: the strange case of Dr Jekyll and Mr Hyde? International Journal of Retail and Distribution Management, 36(4):1-40. [ Links ]