Serviços Personalizados

Artigo

Inglês (pdf)

Inglês (pdf)

Artigo em XML

Artigo em XML Referências do artigo

Referências do artigo

Indicadores

Links relacionados

-

Citado por Google

Citado por Google -

Similares em Google

Similares em Google

Compartilhar

Permalink

PermalinkJournal of Contemporary Management

versão On-line ISSN 1815-7440

JCMAN vol.19 no.1 Meyerton 2022

http://dx.doi.org/10.35683/jcm21071.149

Incubator management experiences engaging with public SMME financiers at national and provincial levels in South Africa

SJH Van Der SpuyI; AJ AntonitesII

IDepartment of Business Management, Sol Plaatje University, South Africa. Email: johann.vanderspuy@spu.ac.za; ORCID: https://orcid.org/0000-0001-6801-2612

IIDepartment of Business Management, University of Pretoria, South Africa Email: alex1@up.ac.za; ORCID: https://orcid.org/0000-0003-3579-6363

ABSTRACT

BACKGROUND: Public funding agencies are governmental funding organs tasked with supplying developmental finance to prospective and emerging entrepreneurs. These agencies focus on bridging the finance gap between investors and entrepreneurs, overcoming strict collateral and own contribution needs. Given South Africa's standing as a developing country, public funding agencies play a pivotal role in enfranchising and empowering emerging entrepreneurs from impoverished sectors of South African society

PURPOSE OF THE STUDY: The study's objective was to document the experiences that incubator managers have with public small, medium and micro-enterprise financiers at a national and provincial level.

DESIGN/METHODOLOGY/APPROACH: A qualitative research design was used in this study. Data were collected using semi-structured interviews that were recorded and transcribed. The sample consisted of 17 business incubator managers from separate business incubators all over South Africa. A combination of convenience, homogenous purposive and snowball sampling were employed.

RESULTS/FINDINGS: Findings revealed that negative experiences between public funding agencies and business incubators were poor lead times on applications, complicated application processes, strict funding requirements, ineffective financing and ineffective staff. Furthermore, findings revealed that positive experiences between public funding agencies and business incubators were improved credibility and higher chances of funding success when applicants are under the auspices of the business incubator.

MANAGERIAL RECOMMENDATIONS: Critical shortcomings in public funding agencies' funding processes were documented, and public funders have been advised to adopt a standardised list of funding requirements, improve communication with incubators and improve staff competencies

JEL CLASSIFICATION: L26

Keywords: Business incubator; entrepreneurial developmental finance; entrepreneurship; governmental finance; public funding agencies

1 INTRODUCTION

According to business incubator theory, incubators have a mandate to develop incubate-entrepreneurs that are 'weak but promising' (Hackett & Dilts, 2004a; Hackett & Dilts, 2004b; Bergek & Norrman, 2008; Calza et al., 2014; Meyer et al., 2016). A prominent weakness facing nascent entrepreneurs intending to start a business venture is the lack of external financial capital, also known as debt capital (Bruton et al., 2015; Sofer & Saada, 2017; Neville et al., 2018; Pham & Talavera, 2018). The struggle to access external finance is a global phenomenon that many nascent entrepreneurs experience worldwide (Block et al., 2018; Howell, 2018). Most nascent entrepreneurs finance their start-ups through debt capital (Baluku et al., 2016; Peel, 2016; Southern, 2016 Bellavitis et al., 2017; Kang, 2017; Cumming et al., 2019). Globally, governmental venture capital plays a pivotal role in funding entrepreneurs who would not succeed in accessing mainstream finances - most notably commercial banks (Ghouse et al,. 2017; Malmström et al., 2017).

The reason for this impasse with commercial banks stems from the entrepreneurs' inability to provide proof of cash-flow, sales traction and an absence of collateral to pledge as security on commercial loans (Fryges et al., 2015; Uddin et al., 2015; Ajagbe et al., 2016; Hulsink & Scholten, 2017; Atiase et al., 2018; Block et al., 2018; Kshetri & Voas, 2018; Mittal, Sengar et al., 2019). In an attempt to address this impasse, many governments have created access to public funds at reduced interest rates and lenient repayment terms - called soft loans - for entrepreneurs who do not qualify for loans elsewhere (Abdullahi et al., 2015; Kariv & Coleman, 2015; Adebayo, 2016; Mehtap et al., 2017; Lee, 2018; Peter, et al., 2018). In developing economies, such government public funding initiatives aim to enfranchise impoverished groups and reduce poverty (Eru et al., 2018; Chowdhury, et al., 2019; Miah & Chowdhury, 2019; Mittal et al., 2019).

South Africa is a developing country (Decoster et al., 2019; Dvoulety & Orel, 2019; Phiri, 2019). Small, medium and micro-enterprises (SMMEs) account for 91percent of all formal businesses in South Africa, contribute 52 percent to 57 percent of its gross domestic product, contribute to 40 percent of total economic activity and employ 61 percent of the employed persons in the country (Atiase et al., 2018; Cant & Rabie, 2018; Cant, Wiid et al., 2018; Kibuuka & Tustin, 2019). Many incubators within the developing environment depend on liaising with public funding agencies to fund new SMME start-ups (Liu et al., 2018; Breivik-Meyer et al., 2019; Shih & Aaboen, 2019).

Access to finance remains a hampering factor for South African entrepreneurs (Rankhumise & Rugimbana, 2010; Maziriri & Madinga, 2016; Hassan, 2018; Herrington & Coduras, 2019; Odeku & Rudolf, 2019). The South African government has attempted to enable South African entrepreneurs with funding through governmental funding agencies (Chinomona & Maziriri, 2015; Ngongoni et al., 2017; Igwe et al., 2018). However, in two separate studies conducted by Padiaychee (2016) and Pillay (2019), it was found that there is a disconnect, or chasm, that exists between entrepreneurs and public financiers. In a study conducted by Jones and Mhlambo (2013), it was found that 36.9 percent of South African entrepreneurs believe that there is far too much bureaucracy - 'red tape' - involved in applying for financial offerings from public funders in South Africa (Donaldson & Pauceanu, 2017; Owen & Mason, 2017).

Regardless of this, 46 percent of entrepreneurs in South Africa still apply for funding from governmental funding agencies (Mohalajeng & Kroon, 2016). In addition, many business incubators rely on a networked relationship with or are dependent on government funding agencies to fund incubate-entrepreneurs (Robinson, 2010; Xiao & North, 2017; Sanyal & Hisam, 2018; Njau et al., 2019). Business incubators often promote themselves to potential incubates by having enough management experience and network relationships with public financiers to facilitate funding between the two parties (Hjorts0 et al., 2017). Therefore, incubator management experiences can be defined as a recollection of past occurrences and interventions related to the development of SMMEs (Amankwah-Amoah et al, 2021). In a recent study by Milne (2020), it was reported that most incubator managers approach public financiers for finance. Furthermore, Milne (2020) touches on three aspects related to incubator management experiences with public financiers when seeking finance for incubate-entrepreneurs:

• A "wasteful use of time" that does not warrant the effort required to prepare an application;

• An archaic and manual application process that is outdated; and

• Funding that is not aligned with key performance indicators but as "strings attached to the money" or non-business-related issues.

Although this study points in the direction of incubator management experiences when interacting with public financiers for funding, it was not a deep investigation into the matter and only briefly mentions these experiences. With this information in mind, a research problem was formulated: the experiences that incubator management has with public funding agencies in South Africa remain unclear.

The purpose of this study is to explore the various experiences that incubator management has had when dealing with South African public funding agencies that fund incubate entrepreneurs - at both a national and provincial level. Municipal funding agencies were excluded from this study. Understanding the experiences that business incubators have when dealing with public financiers enabled this study to advise public financiers on shortcomings and recommend improvements.

Therefore, one research question guided this study:

What are incubator management's experiences with public funding agencies when attempting to secure financial products for incubate-entrepreneurs from them?

2 LITERATURE REVIEW

2.1 Dual-selection theory approach to incubation

The classic theory on business incubation identifies two critical aspects to the development of successful incubate-entrepreneurs. The two constructs identifiable in this theory is captured in the phrase "weak but promising" (Hackett & Dilts, 2004a). According to classic business incubation theory, entrepreneurial skills, business skills, a viable business opportunity and sufficient monetary capital must be present to create a strong business case (Gozali et al., 2015). Should all these factors be present, business incubation should not be needed as the entrepreneur possesses all the tangible and intangible ingredients needed to turn the opportunity into a successful business case (Bergek & Norrman, 2008). However, business incubation supports the entrepreneur that does not have all the required ingredients for a successful and sustainable start-up (Hackett & Dilts, 2004b). These may be referred to as resource gaps that identify the present resources as 'promise', whilst the absent resources are identified as 'weakness' (Hackett & Dilts, 2004b). Therefore, effective business incubators select incubate-entrepreneurs, sometimes called incubates, based on the availability of entrepreneurial skill, orientation, and experience, but who lack financial resources for a viable start-up or growth (Calza et al., 2014). Government-subsidised funding agencies for entrepreneurs link promising prospective entrepreneurs without capital with access to funds (Audretsch et al., 2016). This is done through governmental venture capital to alleviate the financial resources gap (Block et al., 2018).

South Africa has several national public funding agencies mandated by the government that enable entrepreneurs through funding support. These include the Small Enterprise Finance Agency (SEFA), the National Youth Development Agency (NYDA), the Industrial Development Corporation (IDC), the National Empowerment Fund (NEF) and the Technology Innovation Agency (TIA) (Jones & Mhlambo, 2013; Chinomona & Maziriri, 2015; Michelle & Tendai, 2016; Ayandibu & Houghton, 2017; Malebana, 2017; Dzomonda & Fatoki, 2018; Hassan, 2018). In addition to these national public funding agencies, there are three provincial public funding agencies: the Eastern Cape Development Corporation (ECDC), the Free State Development Corporation (FDC) and the Limpopo Economic Development Agency (LEDA) (Malebana, 2017).

2.2 South African public funding agencies

2.2.1 Small Enterprise Finance Agency

The SEFA is a merger of the South African Micro-Apex Fund, Khula Enterprise Finance and the SMME wing of the IDC formed in 2012 (Business Partners, 2017). It is mandated to provide direct financial-developmental products and services to SMMEs (Nkosi, 2017; Aluko, 2018; Mahambehlala, 2019). The purpose of this mandate is to alleviate poverty by stimulating entrepreneurship and economic growth in the South African SMME sector (Worku, 2016; Malebana, 2017; Adinolfi et al., 2018; Mahadea & Kaseeram, 2018). As a result, the SEFA is more prone to risk or possess a higher risk-appetite in order to provide funding to SMMEs that do not meet the normal funding eligibility of private debt investors and younger entrepreneurs with lower levels of entrepreneurial experience (Rector et al., 2016; Worku, 2016; Nkosi,

2017).

2.2.2 National Youth Development Agency

The NYDA is mandated to upskill and finance youth entrepreneurs in South Africa between 18 and 35 years old (Aziz, 2017). This public funding agency is mandated to be flexible to the challenges that youth entrepreneurs in South Africa face, such as lack of financial capital, collateral, and business skills (Ntoyanto, 2016; Zulu, 2016; Yusuf, 2017; Radebe, 2019). Financial support may be either a financial grant or loan (Dube & Nicholson, 2018). However, the NYDA has been plagued by financial mismanagement, lack of financial accountability, poor leadership, wasteful expenditure and non-compliance with the regulations of the National Treasury when procuring goods and services and affording contracts (Ntoyanto, 2016).

2.2.3 Industrial Development Corporation

The IDC, through its partnership with the SEFA, has been mandated with alleviating poverty as well as facilitating economic development in South Africa by occupying a leading developmental-funding role concerning SMMEs operating in the industrial and manufacturing sectors of the South African economy (Mqoqi, 2014; Kalumba et al., 2017; Sikwela & Fuyane, 2017; Khambule & Mtapuri, 2018; Goga et al., 2019). The IDC further explains its mandate as leveraging financial investment to develop innovative and high-growth SMMEs competing in the industrial manufacturing space (Khambule & Mtapuri, 2018; Langa et al., 2018).

2.2.4 Small Enterprise Development Agency

The Small Enterprise Development Agency (SEDA) was originally established to provide non-financial assistance to SMMEs in South Africa (Mahambehlala, 2019). Typical services offered by the SEDA include business-plan-writing workshops and business competency training, focusing on marketing and financial management training (Malebana, 2017; Mayombe, 2017; Motsepe & Fatoki, 2017). However, there is an exception. The SEDA Technology Transfer (TT) Fund has been established to provide SMMEs with technologically innovative production equipment and machinery (SEDA, 2019). SMMEs with an annual turnover of less than R5 million can apply for this funding as a grant under the auspices of the SEDA Technology Programme (Lose et al., 2016; SEDA, 2019).

2.2.5 Eastern Cape Development Corporation

The ECDC funds SMMEs based in the Eastern Cape Province of South Africa. It offers short and long-term loans to these SMMEs (Malebana, 2017; Rungani & Potgieter, 2018). This funding agency acknowledges that SMMEs have historically struggled to access loans based on a lack of collateral to present as security for such a loan. Therefore, the ECDC uses management capacity and viability of the business case to evaluate and award financial loans to SMMEs with insufficient collateral (ECDC, 2020). However, the ECDC requires entrepreneurs and SMMEs to contribute financially to the business proposal to indicate commitment. Where collateral is available, albeit less than 100 percent of the total loan value, the funding agency will attach such collateral as security for the loan (ECDC, 2020).

2.2.6 Limpopo Economic Development Agency

The LEDA boasts an enterprise development and finance function for SMMEs based in the Limpopo Province of South Africa (Masekoameng, 2016; LEDA, 2020). This agency resorts under the Limpopo Department of Economic Development (Masekoameng & Mpehle, 2018).

The LEDA has suffered from financial mismanagement and required a financial bailout from the South African government (Mahomole, 2017; Masekoameng & Mpehle, 2018).

2.2.7 The Free State Development Corporation

This public funding institution offers the following four services to SMMEs located within the Free State Province. Firstly, once-off bridging finance for SMMEs in the service, manufacturing and retail industries who have specific contracts or orders secured and simply need the bridging finance to deliver on the sale or contractual agreement. The SMME must, however, raise 20 percent of the required funds by itself, and the FDC will only provide 80 percent of the total bridging capital required. Therefore, an 80/20 principle applies to all bridging finances loaned. This is not a form of debt financing and will be recuperated in full by the corporation once the client receives payment. A cession is made against the legally binding sales contract, which allows for the corporation to recuperate its investment prior to the client (FDC, 2021).

Secondly, the FDC provides bridging finance for construction-related SMMEs on the same premise that a valid and signed tender of project contract can be presented. The FDC will fund a maximum of R5 000 000 for construction-industry SMMEs within the borders of the Free State Province. This offering may not exceed 50% of the contract value, and therefore, a 50/50 relationship may exist between bridging capital and equity provided by the SMME. Repayment of the borrowed funds may be structured according to the critical delivery and payment milestones specified within the project contract or tender. Therefore, it will not necessarily be recuperated once-off. Once again, cession will be secured over valid contracts and tenders prior to the disbursement of funds (FDC, 2021).

Thirdly, a general enterprise development fund not less than R50 000 and not exceeding R5 000 000 is available for general SMMEs in various industries, such as agro-processing, information and communications technology, tourism, general technology, various classes of transport vehicles, and industrial plant, equipment and machinery. The FDC requires no own contribution in terms of capital investment; however, at least 80% security on the loan is required as a bare minimum, whilst a 100 percent security on the loan is most desired. In terms of franchises, the risk is considered lower, and a 60 percent minimum security is required. The average loan repayment term is normally between 60 and 72 months, but in special cases may be prolonged without exceeding 120 months. A grace period of six months is offered to new start-ups, whereby existing SMMEs can expect no more than one month's grace on repaying the instalments as per the repayment schedule (FDC, 2021).

Lastly, an informal sector loan that ranges between a minimum of R5 000 and a maximum of R500 000 can be loaned to informal traders to purchase stock and equipment. The repayment period ranges between 60 and 72 months, and a 60 percent security minimum is required, although a 100 percent security is preferable. A grace period not exceeding three months may be granted (FDC, 2021).

2.3 The legislative framework for public SMME finance in South Africa

The White Paper on National Strategy for the Development and Promotion of Small Business in South Africa (Notice 213 of 1995) identified that South African SMMEs' lack of access to financial support is a major inhibitor of growth in this sector (Ladzani & Van Vuuren, 2002; Bryce, 2017). The White Paper suggested that a small business finance act be written and promulgated to reduce the failure rate of SMMEs in South Africa and which will provide specialised SMME financing and lending, recognise alternative forms of security for loans, and lastly, involve private commercial banks in SMME finance (Fatoki, 2015; Bryce, 2017). Although the White Paper recommended a small business finance act in South Africa, it never came into existence (Bryce, 2017).

2.4 The role of public funding agencies in South Africa

2.4.1 Bridge the finance gap

A problem many entrepreneurs face is access to financial resources to start or grow an entrepreneurial venture (Armanios et al., 2017; Rahman et al., 2019). This is also referred to as early-stage financing or seed-funding (Owen & Mason, 2017; Srhoj et al., 2019). This problem is exacerbated in the developing world, including South Africa, where most entrepreneurs do not have any security to obtain any form of credit (Padiaychee, 2016; Pillay, 2019). In this regard, public funding agencies are either the sole funder or guarantor enabling funding for such individuals (Abbasi et al., 2017; Lee, 2018; Fraser, 2019). In addition, capital may also be provided as subsidies or soft loans at lower interest rates or reduced instalments, compared to that offered by private financial institutions (Rojas & Huergo, 2016; Dvoulety, 2017; Huergo & Moreno, 2017; Peter et al., 2018).

2.4.2 Stimulate entrepreneurial start-ups and high-growth potential ventures

Historically, public finance agencies have been critiqued for funding marginal-funding proposals that present a high probability of failure, generate little economic development, and create few employment opportunities (Rojas & Huergo, 2016; Terjesen et al., 2016). For an improved return on investment, it is argued that public funding agencies should focus on funding high-growth driven and high-innovation and technology-driven entrepreneurial ventures rather than just the creation of multiple random SMMEs and self-employment (Rojas & Huergo, 2016; Terjesen et al., 2016; Noorali & Gilaninia, 2017; Akinyemi & Ojah, 2018). In addition, a high-potential entrepreneurial populace may be attracted by offering low-risk financial incentives to switch individuals from being employed to creating employment in high-potential ventures (Khare, 2017).

2.5 Challenges faced by South African entrepreneurs and business incubators in relation to public funding agencies

2.5.1 Extended lead times

Lead times can be defined as a sequential process through which credit application, credit appraisal and credit outcome are processed (Jagtiani & Lemieux, 2016; Padiaychee, 2016; Jilcha, Worku & Berhan, 2019; Serame, 2019). Time-intensive lead times often result in the diminishing exploitability and profitability of business opportunities, as they exist for a brief time window (Jagtiani & Lemieux, 2016; Mogashoa, 2017; Jilcha et al., 2019). From a South African perspective, public funding agencies are guilty of a lack of urgency or poor communication (or a complete absence thereof) and a constant request for more information and documentation (Padiaychee, 2016). Therefore, it is recommended that all necessary info is gathered and exchanged between the creditor and the applicant in the quickest possible way to avoid any delay in lead times (Lee & Black, 2017; Kikoni, 2018).

For the purpose of benchmarking, herewith is an indication of the lead times which are significantly shorter and more conducive to entrepreneurial expedience for SMME loans amongst private financiers:

• Amalgamated Banks of South Africa (ABSA) has a lead time (also referred to as turnaround time) of 14 working days (ABSA, 2022);

• Standard Bank of South Africa has reduced its former lead time of 30 working days to three minutes, employing an online application process (BUSINESSTECH, 2019);

• Vodacom Business Solutions has a lead time of 24 hours on SMME loan application evaluations and pay-outs (Vodacom Business, 2022);

• Business Partners does not commit to a specific timeframe but commits to be "as quick as possible" if the entrepreneur submits all the required documents in time (Business Partners, 2022); and

• Business Fuel has a 24-hour period within which an offer is made to the entrepreneur -if successful - and pays out the loan amount within 72 hours of the application (Business Fuel, 2022).

2.5.2 Challenging application process

A challenging application process can be described as time-consuming, bureaucratic, admin-intensive, difficult to understand and interpret, and inefficient, making it difficult and discouraging for applicants to apply for finance (Padiaychee, 2016; Schmidt et al., 2016; Serame, 2019). It is suggested that the amount of paperwork and restrictive actions be removed from the application process and communication during the application process be improved (Lee & Black, 2017).

2.5.3 Inefficient staff

Inefficient staff in the context of a public financier can be described as individuals who lack proficiency to assist with the application, may be corrupt, lack the necessary technical skill to assist and lack industry-related knowledge in the context of entrepreneurship enablement (Padiaychee, 2016; Rusanov et al., 2017; Rappleye & Un, 2018; Appiah, 2019). To counteract such incompetence, the authors recommended that staff are equipped with a professional conduct protocol, independent audits and training integrated with practice (Siwatibau, 1996; Rusanov et al., 2017; Yousefian et al., 2017).

2.5.4 Collateral

Collateral - most notably real-estate property - is the security that prospective entrepreneurs possess and against which business loans are secured from private and public financiers (Mello & Ruckes, 2017; Schmalz et al., 2017). Lack of collateral to secure these business loans is an obstacle globally and in South Africa (Padiaychee, 2016). It is suggested that the government provide credit guarantees for promising entrepreneurs without collateral to secure loans from financiers (Ben-Yashar et al., 2018; Cowling et al., 2018).

2.5.5 Awareness

From a South African perspective, it was found that many entrepreneurs remain uninformed or unaware of funding initiatives by public funding agencies within the country (Padiaychee, 2016). It is suggested that funding fairs be organised to link entrepreneurs with the available public financiers and their corresponding financial products (Padiaychee, 2016).

3 RESEARCH METHODOLOGY

3.1 Research design

An explorative-descriptive qualitative research design was followed. This type of research attempts to identify underlying themes by conducting in-depth discussions with participants and extensively studying the existing base of theory (Plano Clark et al., 2015; Hunter, et al., 2018; Umanailo et al., 2019). This research design allows researchers to better understand a research topic and the specific context from participant experiences and perceptions (Kim, Sefcik et al., 2017; Reidy et al., 2018). This context allowed the researchers to explore the lesser-researched topic of incubator management's experiences with South African governmental funding agencies.

A constructivist research paradigm or philosophy guided this study (Creswell, 2014). Constructivism attempts to understand the problem, appreciate the multiple meanings and complexities of many participants, understand the historical and social history preceding the research problem and generate theory from the above (Creswell, 2014). In this study, constructivism attempted to understand how incubator management perceived public financiers by collecting the knowledge and experiences these practitioners recalled (Adom et al., 2016). This study is empirical because it collected primary research first-hand.

3.2 Setting

Interviews were conducted in the conference suite of the Protea Hotel in Hatfield, Pretoria. This setting was ideal, as there was a nationwide business incubation conference held at this venue at the time. Therefore, it was convenient and effective to access business incubator managers from all provinces of South Africa without travelling excessively. In addition, interviews were conducted after the close of business so that individuals interviewed were relaxed, not pressed for time and did not have other commitments.

3.3 Study population and sampling strategy

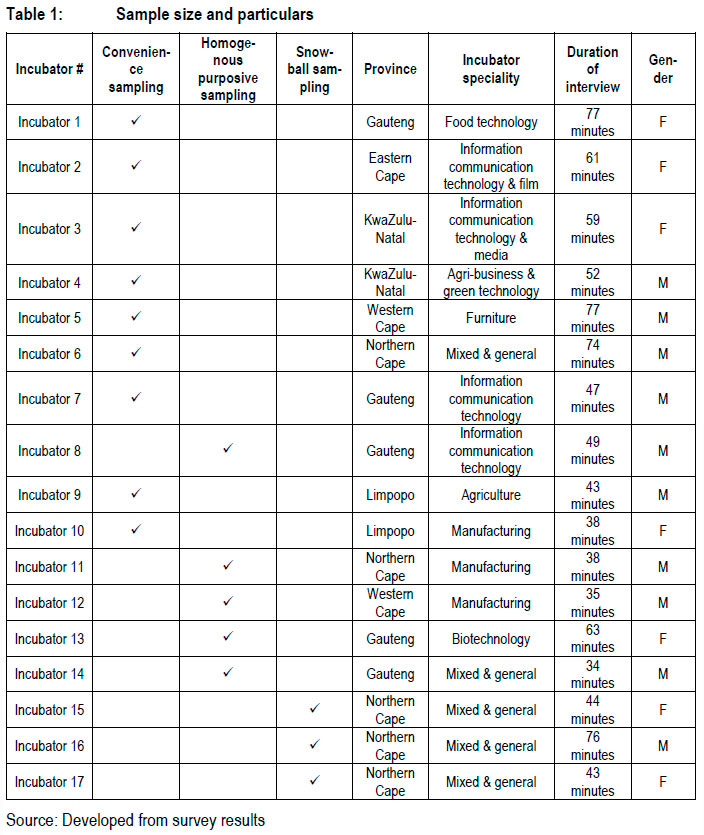

The unit of analysis for this study was business incubator managers within the Republic of South Africa's borders. The sample consisted of 17 business incubator managers. The study population consisted of five incubator managers from Gauteng, one from the Eastern Cape, two from KwaZulu-Natal, two from the Western Cape, five from the Northern Cape and two from Limpopo. A series of 17 once-off, semi-structured interviews were performed from August 2017 to January 2018. Non-probability sampling techniques were applied. The approach was deemed suitable due to limited time, resources, the workforce and a small sample size (Etikan et al., 2016; Taherdoost, 2016; Speak et al., 2018).

A combination of convenience sampling and homogenous purposive sampling was used to identify an initial sample to interview. Convenience sampling is a non-probability sampling technique whereby members of the target population in proximity at a specific time are selected (Etikan et al., 2016; Setia, 2016; Elfil & Negida, 2017). Convenience sampling was very effective in this study as a large portion of the participants were present during a business incubation conference that was held in Pretoria. Thus, incubator managers from all over the country were concentrated at one single location during the data collection. Homogenous purposive sampling requires the deliberate selection of potential participants based on specific characteristics that must be present to qualify for the research study (Plano Clark et al., 2015). This was the secondary manner of selecting participants by finding suitable candidates via incubation websites and then contacting them for potential participation.

In addition, snowball purposive sampling was employed to identify further additional participants for the sample. Snowballing purposive sampling requires referrals from the initial interview sample to gain access to further potential respondents and perform further interviews (Plano Clark et al., 2015; Etikan et al., 2016; Woodley & Lockard, 2016; Rao et al., 2017). Table 1 depicts the sample size, sampling strategy, geographical locations of participants, incubator industry and duration of the interview.

3.4 Data collection

Data were collected by using a semi-structured interview protocol during the participant interviews. A total of 17 semi-structured interviews were conducted. The interviews between participants and the researcher were conducted on an individual basis. Interviews were captured on a mobile sound recorder and then transcribed into a Microsoft Word document in verbatim format. The semi-structured interview protocol (also called the discussion guide) was constructed by reviewing the available literature on national and provincial public funding agencies in South Africa. Municipal funding agencies were excluded from the study.

3.5 Data analysis

Thematic analysis was performed, and deductive and inductive analyses were used. Deductive analysis was performed by conducting a rigorous and comprehensive literature review on the existing body of knowledge surrounding the role and functions of state funding agencies (Plano Clark et al., 2015; Maine et al., 2017; Hunter et al., 2018; Moser & Korstjens, 2018; Cramer-Petersen et al., 2019). Patterns and themes in the data were then identified and connected to existing themes in the literature through a process of inductive analysis (Braun & Clarke, 2012; Nowell et al., 2017; Ashmore, et al., 2018; Pearse, 2019). New themes that were not present in the existing body of theory were also reported. A systematic, dualistic deductive-to-inductive qualitative data-analysis process was thus used (Roberts et al., 2019). All transcripts were loaded onto Atlas, a qualitative software analysis tool, to identify themes and patterns that emerge from the data. Therefore, Atlas software allowed the researchers to code similar responses into themes, which were then organised categorically by the software. The software provided exact reports on the themes identified and reported the number of times they were mentioned. If the same theme was reported repeatedly and consistently, it was considered a pattern of importance.

3.6 Trustworthiness

Qualitative research must be credible, transferable, confirmable, and dependable (Moon et al., 2016; Le Roux, 2017; Gill et al., 2018; Korstjens & Moser, 2018; Le Roux, 2017). Credibility is achieved when the researcher establishes truth-value in the data and how the data were interpreted (Mclnnes et al., 2017). In this regard, site triangulation was employed to include participants from various geographical origins and independent business incubators to ensure that findings were not from a single geographical area that could not be applied to other geographical areas and incubators (Johnson et al., 2017; Fold et al., 2018; Harper, 2019). In addition, member checking was employed through prolonged discussion with participants to clarify certain information provided to further enhance credibility. This was done so that misinterpretation could be avoided, and the plausible and correct interpretation of data was achieved (Anney, 2014; Ramsook, 2018; Sivagurunathan et al., 2019).

In order to comply with the requirement of transferability, the research must be relevant or transferable to the context of other settings (Korstjens & Moser, 2018; Smith, 2018). This was achieved by providing a detailed description of the participants, the data-analysis technique and a thorough literature review of the topic (Creswell, 2007; Polit & Beck, 2012; Mostert et al., 2017). Furthermore, this was achieved by reflectively and descriptively transferring the participants' lived experiences (Alase, 2017; Smith, 2018).

A further requirement of qualitative research is to ensure confirmability (Watkins, 2012). Confirmability entails that the research findings are based solely on the experiences and opinions of participants and not that of the researcher (Moon et al., 2016). In order to enhance confirmability, the study relied on dual sources of data: data collection and information gathered via the literature review conducted before data collection, thus pursuing internal and external validity (Watkins, 2012; Treharne & Riggs, 2014; Vermeulen et al., 2016; Mostert et al., 2017).

Lastly, qualitative research requires dependability, which entails the stability and transparency of findings over time (Moon et al., 2016; Tong et al., 2016; Kalu & Bwalya, 2017; Korstjens & Moser, 2018). This is achieved by following a strict data collection and analysis process protocol (Wu et al., 2016; Walther et al., 2017; Johnson et al., 2020). This was achieved by transcribing the voice recording verbatim to a Microsoft Word document and using a computerised coding system (Tong et al., 2016:901). The prior literature review and novel codes derived from secondary data were partly derived from secondary data. In order to further enhance the dependability of the research, a systematic peer debriefing was used: four international reviewers specialising in business incubation scrutinised and audited the study transcripts, coding and findings to judge their accuracy, applicability and correctness.

4 FINDINGS

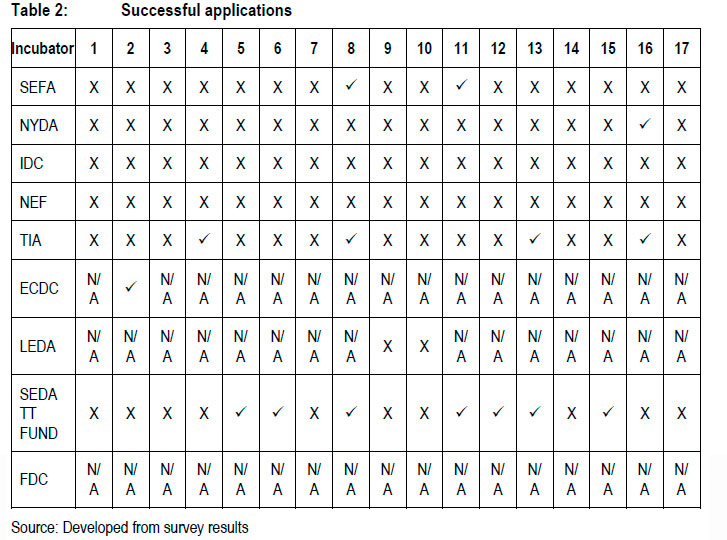

4.1 Application successes

The application success rate is the number of times the incubate, with the assistance of the incubator, has had to apply for funding with various public funders until successful - if successful at all (Teixeira & Sharifu, 2017). Incubators 8 and 11 reported successful funding applications for incubates from the SEDA. Incubators 8 and 11 motivated that the SEFA to fund the incubates if a final purchase order was presented. Therefore, the financier can be assured that an income-generating transaction will service the loan.

In addition, Incubators 4, 8, 13 and 16 reported successful funding for incubates from the TIA. Incubator 4 had a ring-fenced seed fund with the TIA, according to which the incubator, at their discretion, may invest funds on behalf of the TIA. Incubator 8 reported that the TIA had funded incubates based on the presence of a business plan, business registration documents, own contribution and a credit record that would pass a credit check by the financier. Incubator 13 achieved funding success from the TIA by advising incubates to partake in innovation competitions and secure finance via that platform. Incubator 16 reported that they recommend high-potential incubates for finance, successfully linking financiers to their incubates.

Incubator 2 reported successful finance applications for incubates via the ECDC. The motivation provided for successful applications with the ECDC was the maintenance of a close relationship between the financier and incubator. As a result, the financier trusts the recommendations of the incubator and views applicants from the incubator with greater credibility. The most prevalent funder of incubates was the SEDA through its TT Fund. Incubators 5, 6, 8, 11, 12, 13 and 15 reported success in funding applications for incubates via the SEDA TT Fund. Incubators 5, 6 and 8 have successfully sourced funding for incubates when a signed tender, business contract or letter of intent is presented to the SEDA TT Fund, assuring the financier that income will be generated to service the loan. Incubator 11 reported that a ring-fenced amount of funds is allocated to the incubator, which in turn can allocate funds to incubates using their discretion, on behalf of the SEDA. Incubators 12, 13 and 15 reported that they could source funds from the SEDA TT Fund based on a strong relationship built over time. Incubator 12 reported that the presence of collateral to put down as security for the loan is essential for finance to be awarded.

Incubator 16 reported successful applications from the NYDA because of a successful grant application made to the NYDA, which does not require repayment. However, no incubator in the sample reported any success in sourcing funding from the IDC, the NEF or the LEDA for incubates. As there were no participants in the study who originated from the Free State Province of South Africa, the FDC could not be measured and reported and has thus been indicated as not applicable. Furthermore, incubators not originating from the Free State, Eastern Cape or Limpopo provinces were supplied with not applicable (N/A) code, as incubators cannot obtain funding from these financiers if they are not based within these provinces. Table 2 summarises the sample incubators' successful and unsuccessful applications to public finance agencies.

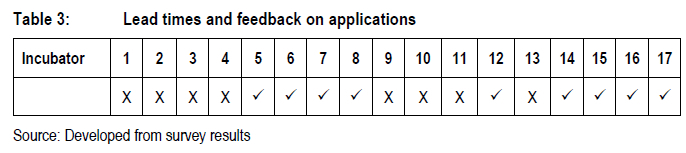

4.2 Poor lead times

Incubators 5, 6, 7, 8, 12, 14, 15, 16 and 17 reported frustratingly slow lead times on finance applications from public financiers. Incubator 13 reported waiting six months before sums of money were paid out to the entrepreneurs. Incubator 5 reported a two-year waiting period for pay-out, and Incubator 7 spent a year waiting for pay-out. Incubator 6 reported waiting two years (with no feedback) for the outcome of a finance application, as public financiers often do not provide any form of feedback on an application. Incubator 15 had not received a response from the financiers two years after having applied. This finding corresponds with prior research by Padiaychee (2016) that identified poor lead times as an obstacle to entrepreneurs. In the context of this study, it remains a problem inside the confines of the business incubator.

"And unfortunately, this client, we actually had to keep them almost a year longer in the system because they were waiting for the answer from TT Fund, because the TT Fund was, at that stage, two years behind in terms of its applications."

Transcript 5. Incubator 5. Incubator manager. Male.

"You see, [with] NYDA, the problem is you have applicants waiting for up to two years, you know? And sometimes, they just go silent on you, you know? I've got an applicant that wasn't successful at SEFA and NEF."

Transcript 6. Incubator 6. Incubator manager. Male.

Table 3 below indicates which incubators experienced long waiting periods for feedback on finance applications. Incubators who reported a long lead time are indicated with a correct mark ( ), and incubators who did not report a long lead time are indicated with a cross (X).

), and incubators who did not report a long lead time are indicated with a cross (X).

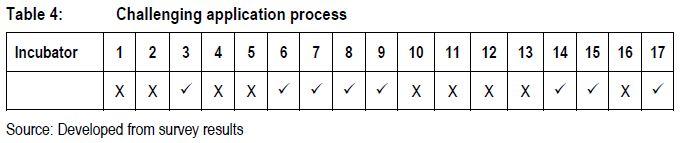

Incubators 3, 6, 7, 8, 9, 14, 15 and 17 experienced a challenging application process when applying for finance from public funding agencies. Incubators 3, 6 and 15 reported an unstructured application process that goes "back and forth" without progress. This was reported to be extremely frustrating and irritating to incubator management and the incubates. Incubator 9 reported that public financiers impose too much red tape on incubates by requesting a large volume of documents that many SMMEs do not have immediate access to. Therefore, incubators find it difficult to prepare all the documentation for incubates to be application ready. Incubators 3, 12 and 15 further lamented the application process that public funding agencies follow because applications get lost during the application process. In those cases, one is expected to repeatedly resubmit the same documentation without any progress - or response in many cases. This finding is supported by several authors who have also identified a challenging application process as an impediment to entrepreneurial development (Padiaychee, 2016; Schmidt et al., 2016; Serame, 2019).

"I mean, I understand that there must be rules and processes and that everyone must be treated fairly, but I feel that they don't inspect properly before giving funding. Also, when people apply for funding...they've not been taught how to apply for funding, and I feel they do it irresponsibly. When someone applies for funding, shouldn't they rather arrange for a workshop so that they can come in, and they can make them understand why they can't fund you? You can't get funding because. I've never had one of my entrepreneurs succeed in obtaining funding from any of these government funds, and we have applied in the past. We waited two years for a verdict on an application, but eventually, it got lost."

Transcript 15. Incubator 15. Incubator manager. Female.

"They'll go; they'll be patient, and they'll go to SEDA, and they'll go here. Do you know, they'll go to the development agency; they'll go here. They'll go to everybody, and they'll still come back with a big zero. I think it just disappears because, remember, you're sending the person from point A to point B. SEDA will say that now go to SEFA. Then SEFA will say, 'Okay, fill in all of these things'. And then maybe when they go back to SEFA, this is not right, or but you know, oh I can't help you because you don't have this, or we won't fund you because, you know, and it's just like ... It's chasing your tail."

Transcript 3. Incubator 3. Incubator manager. Female.

Table 4 below provides a summary of the incubators who reported a complicated application process as an experience when dealing with public finance agencies.

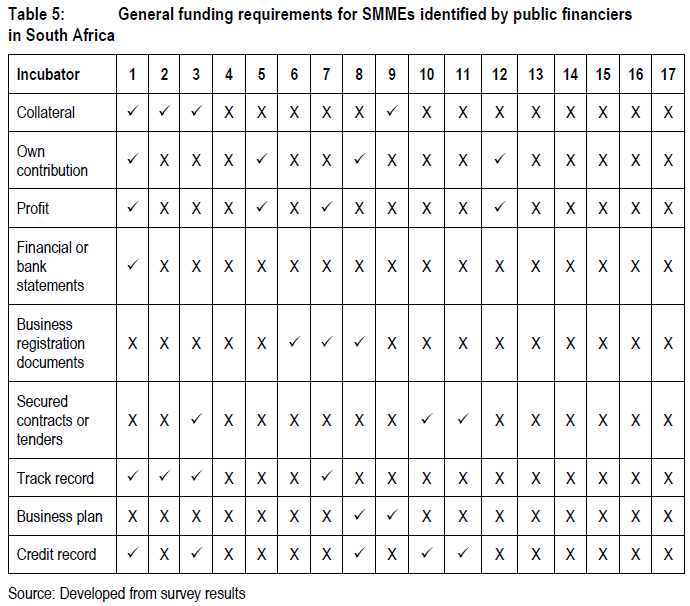

4.4 General funding requirements for SMMEs identified by public financiers in South Africa

It was reported by Incubator 1 that funding, in general, is very strict. Incubator 6 reported that their experience with the NEF proved that non-compliance with any of the requirements would result in an unsuccessful application. This is in contrast to the existing body of knowledge, which is in consensus that public funding agencies should provide soft loans for entrepreneurship development at reduced interest rates and more lenient allocation criteria (Abdullahi et al., 2015; Kariv & Coleman, 2015; Adebayo, 2016; Mehtap et al., 2017; Lee, 2018; Peter et al., 2018).

"The most ... these funding agencies of government are getting stricter. And this is not just in our industry; it's in any industry. So, if they feel in any way that there is an element of risk, they want collateral. Sometimes their interest rates are worse than that of commercial banks."

Transcript 1. Incubator 1. Incubator manager. Female.

"I think NEF is extremely strict. But he was strict with that and said, 'Listen here, this is one of the [criteria], and I cannot take shortcuts when it comes to that.' You know? I mean, from one application that I took there, that was one of, I think, three or four things that he emphasised to say, 'Your application will not be approved due to that.' I have made, you know, interventions in terms of going to SEFA and going to the NEF, but you find that they... I think SEFA, in fact, I thought SEFA was bad, but the NEF is on another level ... I think NEF is extremely strict."

Transcript 6. Incubator 6. Incubator manager. Male.

Incubators 1, 2, 3 and 9 reported that public funding agencies require collateral as a condition to acquire a loan. Collateral entails pledging assets with sufficient value as security on which the loan can be secured.

"The most... these funding agencies of government are getting stricter. And this is not just in our industry; it's in any industry. So, if they feel in any way that there is an element of risk, they want collateral. Sometimes their interest rates are worse than that of commercial banks."

Transcript 1. Incubator 1. Incubator manager. Female.

"There's another company called SEFA...Those guys are actually issuing out loans. So, they look into issues of security."

Transcript 9. Incubator 9. Incubator manager. Male.

Incubators 1, 5, 8 and 12 reported that public funding agencies require an "own contribution" before awarding a financial loan. Own contribution entails personal funds that the incubate-entrepreneur has saved in their personal capacity and pledges as a part of the initial capital investment of the proposed venture. Incubators 1, 5 and 8 indicated that the own contribution is usually 10 percent to 20 percent of the total loan required. This is significantly less than the 50 percent own contribution required by private financiers in South Africa and acts as a gesture of commitment from the incubate-entrepreneur to the proposed business venture (Venter, 2019).

"You know, but, like, those [types] of funds, they would require a 10 percent, a 20 percent, upfront contribution by the client."

Transcript 5. Incubator 5. Incubator manager. Male.

"For example, at [the Department of Trade, Industry and Competition] again... now to the small business development, there's a programme called the [Black Business SEDA Technology Programme] programme, whereby, you know, 80% can be funded through their fund, but 20 percent would be. You know, the entrepreneur has to contribute towards that."

Transcript 8. Incubator 8. Incubator manager. Male.

Incubators 1, 5, 7 and 13 reported that public financiers require a profitable flow of revenue when considering funding an incubate-entrepreneur. However, only Incubator 1 reported that public financiers require actual financial or bank statements.

"If they have a registered company, I want the company registration documents and copies of the [Companies and Intellectual Property Commission] documents. I want copies of all of the members and directors' ID documents. I want your tax clearance certificate if you are already in business. If you're already in business, I want to see your financial statements or your bank statements."

Transcript 1. Incubator 1. Incubator manager. Female.

"Like, for instance, the fund requires you to have...I can't remember now...but it's an X amount of revenue that you already generated."

Transcript 7. Incubator 7. Incubator manager. Male.

Incubators 6, 7 and 8 reported that financiers require business registration documents prior to considering financing an incubate-entrepreneur. From a South African perspective, business registration documents include a tax registration certificate, company registration documentation and a broad-based black economic empowerment (BBBEE) compliance certificate (Akinyemi & Adejumo, 2018).

"It's tough, so the normal requirement is that you must have X revenue. Most young entrepreneurs don't meet that. You must have employed X number of people. Most young entrepreneurs don't meet that. The ones they can meet is a registered company. They would need the [black economic empowerment] certificate. Another criterion these guys normally have is saying that your business must be running for two to three years. Our incubates don't meet that. Ja, from the top of my head, I think there are probably more, but at this very point in time, these are the main reasons.why don't we go to these guys."

Transcript 7. Incubator 7. Incubator manager. Male.

"In relation to government development agencies, obviously all the companies must be compliant in terms of your business registration documents,.BBBEE certificate or affidavit,.. .[South African Revenue Service] tax clearance certificate [and] business plan."

Transcript 8. Incubator 8. Incubator manager. Male.

Incubators 3, 10 and 11 reported that public financiers require proof of secured future business by proving that future business contracts or tenders have been secured.

"They've got a programme in place where if you have.an approved tender, it's given to you. So, assume you wanted to supply a 1 000 of these glasses to the Tshwane Municipality, and they've given you the tender, and.you're going to supply this, but you know you don't have money to go and buy this and supply the municipality, where are you going to get the R60 000.00 for this? So, you go to the funder with that approved tender. They will fund you then. They will fund the tender."

Transcript 3. Incubator 3. Incubator manager. Female.

"[They] would like to see letters of intent. So, if you don't have those letters of intent to prove that there is a market for your product or your service, then you won't be approved."

Transcript 11. Incubator 11. Incubator manager. Male.

Incubators 1, 2, 3 and 7 reported that public financiers require proof of the business track record prior to considering the application.

"The failure rate of these types of businesses are not unique to our incubator. It is so in general. So, in other words, what happens is that the guys [who] do the financing, whether it be SEFA, IDC or commercial banks, in 99 percent of the cases, they don't want to fund these food businesses due to the high failure rate. So, these guys first need to get the business on its legs and...build a track record before someone will look at them to consider financing them."

Transcript 1. Incubator 1. Incubator manager. Female.

"The fund requires you to have...I can't remember now...but it's an X amount of revenue that you already generated. They want you to have employed X number of people, and in the future, they want you.and specify two or three years. Like, you must have over 100 employees and all these difficult things."

Transcript 7. Incubator 7. Incubator manager. Female.

Only Incubators 8, 9 and 11 reported that incubate-entrepreneurs must present a business plan to public financiers to be considered for finance.

"Well, we put them in the pre-incubation phase. So, we assist them with [their] application for funding. [We] assist them with drawing up of proposals [and] business plans to make sure that they comply with all the things that the funders want."

Transcript 8. Incubator 8. Incubator manager. Male.

"Normally, we would.use outside providers. Let's say SEDA. SEDA will be conducting.due diligence to see whether this business plan is feasible or not."

Transcript 11. Incubator 11. Incubator manager. Male.

Incubators 1, 3, 8, 10 and 11 reported that a healthy credit score is essential to have an incubate-entrepreneur's application considered for finance.

"I think it...would really depend on if it's the bank or financiers...it will probably be issues related to their credit records. To the credit record or...a client may not necessarily meet the requirements.or they may not necessarily have the co-funding capability in terms of the fund."

Transcript 8. Incubator 8. Incubator manager. Male.

"[They're] normally looking at the risk profile. The credit-the credit risk profile of an incubate. And they're not looking just from the business aspect of it."

Transcript 11. Incubator 11. Incubator manager. Male.

Table 5 provides a summary of the various funding requirements required by public funding agencies in South Africa.

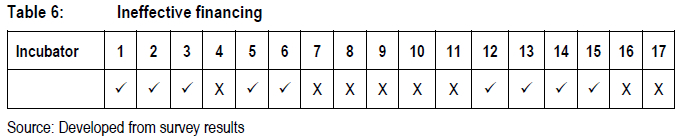

4.5 Ineffective financing

Incubators 2, 3, 5, 12, 13, 14 and 15 reported that public financiers are ineffective when funding incubate-entrepreneurs. Incubator 14 reported that they observed a substantial impairment rate at the SEFA. This entails that entrepreneurs funded by the SEFA are often unable to pay the instalments on loans issued by the SEFA. Incubator 15 made the following remark concerning the lending behaviour of the majority of public SMME financiers:

"These guys are funding the poorest of the poor; the dirt poor. And they have no prospect of receiving any sort of repayment from 80% of the people they give loans to. That's why I believe that in many cases, it is irresponsible lending, because they are setting them up to default."

Transcript 15. Incubator 15. Incubator manager. Female.

Herein lies a problem that presents itself to public SMME financiers with a mandate to fund disadvantaged entrepreneurs, as discussed in the literature review of this paper. During a 2011 presentation of SEFA at an entrepreneurship networking event held at the University of Pretoria, a representative of SEFA presented the mandate that "we are here for those who do not have collateral or sufficient own contribution, but if you have it, we'll take it" (Molefe, 2011). The topic of this paper is not specifically focused on irresponsible or reckless lending, but this impasse poses a challenging research problem for future research. There seems to be a chasm between lenient soft loans and the enforcement of loan repayment.

Incubator 15 reported ineffective financing because the release of approved funding takes exceptionally long to be transferred to approved incubate-entrepreneurs. Lastly, Incubator 15 reported that funding should be considered irresponsible in certain situations, as individuals who are not funding-ready are funded. Incubators 2, 5, 12 and 13 reported ineffective financing because all the submitted applications were ignored, unsuccessful or received no feedback. Therefore, they perceive it as impossible to secure any funding from public funding agencies in South Africa. Lastly, Incubator 13 reported additional ineffective financing based on corrupt funding practices at certain public funding agencies.

"Go look at their impairment rate, and then you tell me. Go look at SEFA's impairment rate, and you tell me if they miss the mark. In fact, I think their grant funding does more harm than good in the long run because it creates a false economy, and it creates a false reality that, effectively, there's no muscle tone required. It's just a good business plan and fancy talking and some relationships.

I'm very cynical when it comes to them. Impairment rate is the failure rate of the entrepreneur to pay back the loan."

Transcript 14. Incubator 14. Incubator manager. Male.

"I very seldom work with government functions because they are very frustrating to me. I don't think they see the bigger picture, and they don't know how to spend their money. They are not quite there where they understand what to do with their money, and they frustrate the people. I mean, why must it take six months to pay out someone? Or all these red-tape processes? I heard of a guy that got a contract to wash hospital linen. Now, to do that tender, you got to know what you are doing because you are working with human contamination. When we went to visit him, he had two ladies washing linen with their hands. They didn't even have a washing machine. I feel that they don't check properly before they do funding, and when people do apply for funding, they weren't taught how to apply for funding. And I think they fund irresponsibly. When someone comes to apply for funding, why don't you hold a workshop to tell them why you can't fund them? You can't get funding because..."

Transcript 15. Incubator 15. Incubator manager. Female.

Table 6 below provides a visual representation of the incubators within the sample that reported ineffective financing as an experience when dealing with public funding agencies.

4.6 Ineffective staff

Incubators 1, 2, 3, 12, 14 and 15 reported inefficient staff at public funding agencies. Incubator 14 reported specific inefficiencies amongst staff as lacking financial and accountancy skills, such as reading financial statements and determining profit. In addition, Incubators 14 and 15 criticised the staff at government funding agencies for being non-entrepreneurial, and therefore, largely unable to advise and support the entrepreneurs they exist to support. Furthermore, Incubator 15 reported that enthusiastic and capable staff at government agencies quickly become disillusioned with the bureaucratic system, and as a result, become demotivated and lose their effectiveness. These reports are supported by prior studies finding that ineffectual staff at public finance agencies are a stumbling block to entrepreneurial finance (Padiaychee, 2016; Rusanov et al., 2017; Rappleye & Un, 2018; Appiah, 2019).

"Whether they are failing or succeeding, it depends whether you ask them or other people. If you ask them, they are going to tell you that they are succeeding. Let me give you my liquid test. There are three government managers I would employ in my incubator. I've told all three [that] when they're ready to come, I'm ready. There are so many flaws but let me start with the headline. The headline is a philosophical one. For me, the philosophical issue is when you have a not-for-profit teaching people how to make [a] profit. That is Number 1. And Number 2, the types of people who are running it are not entrepreneurs. Number 3, the people who are supposed to be mentors are not mentors at all. Just to give you some data on that: in 2015, there was a case study among 31 quasi-government and government mentors. Effectively, it was an income statement in written form, and they had to work out what the net profit is. Out of 31, only two could work out the net profit margin - only 6.5 percent. These are the people [who] are training other people how to do business. Now, in order to get the skill issue out of the way, they've brought in a piece of software from overseas. Those, I think, are the big issues. And I have to say: with exceptions. There are exceptions out there, and it's not fair to crush everyone. There are government agencies that are doing well, and that is due to the people [who] are leading it, [who] are brilliant. I am generalising, and it is easy to bash [the] government, but those are the big issues for me."

Transcript 14. Incubator 14. Incubator manager. Male.

"It's about more than simply giving people money. You need them to think like businesspeople; otherwise, we're not going to go forward in this country. We are going to stagnate, and people are just going to continue sitting in the [South African Social Security Agency] queue. It makes me crazy. They are just places that got government funding and believe themselves that they are doing good things. Every now and then, you get a gem, a person [who's] very excited to work for these public agencies, but after six months, you can see they've worn him down - the system. Because it's a very large bureaucratic system. You can't now ask a civil servant to develop an entrepreneur; he's never owned a business in his life. He doesn't have the desire to do that because it's difficult to run a business. And to run a business incubator and mentorship programme in the rural context is much more than just giving them money."

Transcript 15. Incubator 15. Incubator manager. Female.

Table 7 below provides a visual representation of incubators who encountered ineffective staff when dealing with staff employed at public funding agencies. Incubators who reported ineffective staff are indicated with a correct mark ( ), and incubators who did not report ineffective staff are indicated with a cross (X).

), and incubators who did not report ineffective staff are indicated with a cross (X).

4.7 Increased credibility associated with the incubator

Incubators 1, 2, 4, 5, 8, 11, 12 and 13 reported that public finance agencies are more likely to fund an incubate-entrepreneur if the incubator provides support. Therefore, incubate-entrepreneurs with incubator support have a greater chance of funding success than incubate-entrepreneurs who apply for funding on their own and without incubator support and credibility.

"We've had instances where we've had to go with the incubate to actually try and.set up a meeting with ECDC just to try and get some form of - I don't want to say leeway - but to make ECDC understand the reason behind the request for these funds. So, it almost boosts.the chances of the actual entity acquiring that finance. Because we are a somewhat known brand. So, we already have a brand. So.we say to ECDC, 'We are willing to stand with this person; assist, please'. ECDC then decides, 'Okay, maybe let me give them a chance in a way'. So, we've had those kinds of meetings where [the] situation has been difficult, and we've had to go with the actual client and be part and parcel of that.pitch or.application."

Transcript 2. Incubator 2. Incubator manager. Female.

"We facilitate financing through various agencies. Like, for example, there [are] about nine of our clients [who were] successful with the TT Fund, which we assisted them with their applications...We submitted the applications on their behalf to SEDA - it's... TT Fund."

Transcript 5. Incubator 5. Incubator manager. Male.

Table 8 below provides a visual representation of the incubators who reported experiencing increased credibility when dealing with public funding agencies.

5 CONCLUSION

5.1 Summary of findings and theoretical implications

The purpose of this study was to explore the various experiences that incubator management has with public funding agencies in South Africa. The most prominent public financier in the sample was the SEDA TT Fund. Seven incubators within the sample reported successful applications with this public financier. The second most prominent public financier was the TIA, who funded four incubators within the sample. The SEFA was reported to have provided financial products to incubate-entrepreneurs from only two incubators in the sample. The NYDA and the ECDC provided financial products to incubate-entrepreneurs from only one incubator each within the sample. The LEDA, the IDC and the NEF were absent from the sample in terms of funding incubate-entrepreneurs from respective incubators within the sample.

The first research question guiding this study attempted to identify negative experiences incubator managers had when dealing with South African public funding agencies. The most prevalent experience reported by nine incubators was public financiers' extremely slow turnaround times on incubator managers' financial product applications. Some incubators reported waiting for up to two years, whilst others reported applications that were never acknowledged as received, successful or declined. In short, no communication was received from the relevant public financiers in such cases. Another prevalent theme identified was frustration with the application processes for financial products offered by public funding agencies. Eight incubators reported that the process was unstructured, unclear, extremely bureaucratic and complicated, with a significant requirement for various documentation. In addition, applications often got lost in the process and required repeated resubmissions.

Only Incubator 4 could identify a comprehensive spectrum of requirements needed by public financiers to submit a legitimate application. The requirements identified were sufficient collateral, own contribution, proven profitability, a proven track record, financial statements and an acceptable credit record. The most prevalent requirements for a successful application were reported as an acceptable credit record, own contribution, track record, collateral and business registration documentation.

Nine incubators reported ineffective financing. For example, Incubator 14 identified a high impairment rate as evidence of ineffective financing. This respondent cited a high impairment rate - defaulting on loan instalments due to an inability to repay - by, specifically, the SEFA. Other indicators of ineffective financing were the funding of applicants with poor business propositions and the flow of funds via corrupt activities. Lastly, the inability to secure any form of finance from public financiers, even with strong funding propositions, was also cited as ineffective financing.

Six incubators reported ineffective staff as a negative experience with public funding agencies. Firstly, it was reported that the staff component within public funding agencies responsible for evaluating and judging the feasibility of applicant funding proposals was unable to do so. Secondly, it was reported that a lack of accounting knowledge and skills kept the staff from making scientifically based decisions. Lastly, extreme bureaucracy and an ineffective administrative system discouraged staff and reduced their enthusiasm for performing their functions effectively.

The second research question guiding this study attempted to identify the positive experiences incubator managers had with public funding agencies. Nine incubators reported that public funding agencies were more likely to fund incubate-entrepreneurs who had the support of and an association with an incubator when applying for funding than entrepreneurs who did not. The study context was located within seven of the nine South African provinces. It contributed to identifying the various challenges and efficiencies incubator managers experience when dealing with public financiers. Because of the inclusion of participants from various provinces, thus wide geographical distances, this paper could be generalised to the general incubator population of South Africa.

5.2 Practical implications

The study recommends that the public finance sector creates a more accessible and desired range of financial services. It is suggested that a standardised list of requirements be created for prospective applicants and then clearly communicated to incubator managers and staff.

The purpose of such action would be to ensure that all stakeholders and role players have a clear and concise understanding of what is needed to apply for public finance products. It is also recommended that public funding agencies establish a clear, precise and transparent internal process for handling finance applications. In addition, it is once again recommended that this process be well communicated to stakeholders, especially incubator staff, for the process to be considered ethical and fair. An auditable trail of paperwork and receipts is suggested to avoid the lamented complaints of no response or responses going dormant after some point in the process. The public finance sector must first understand that they have a unique role in the entrepreneurial finance landscape. It is essential that they empower entrepreneurs who would be unable to pursue private sector finance. To do that, the public finance sector needs employees who are in tune with the realities of developmental finance for entrepreneurs and have decisive skills to eliminate weak prospects.

5.3 Limitations of the study and future research

As the study employed non-random sampling techniques, combined with the smallish sample size of 17 participants, bias in responses may have occurred. To reduce the probability of bias, the researcher drew participants from multiple provinces around South Africa and a diverse range of incubators specialising in various business industries. In addition, because snowball sampling was used to gain access to participants, this may have resulted in similar views and responses, as participants may have recommended other participants with views similar to their own. To combat the likelihood of this, the researcher emphasised anonymity in participation and reporting to enhance the likelihood of unbiased responses from participants.

As this study did not investigate recommendations for improving the public SMME finance sphere, it is a possible future research avenue. Therefore, the research question for such a study may be phrased as follows: What recommendations would business incubator managers provide to improve access to finance by public SMME financiers in South Africa?

REFERENCES

- Abbasi, W.A., Wang, Z. & Abbasi, D.A. 2017. Potential sources of financing for small and medium enterprises (SMEs) and role of government in supporting SMEs. Journal of Small Business and Entrepreneurship Development, 5(2):39-47. [ Links ]

- Abdullahi, M.S., Abubakar, A., Aliyu, R.L., Umar, K., Umar, M.B., Sabiu, I.T., Naisa, F.U.K., Khalid, S.S. & Abubakar, L.S. 2015. The nature of small and medium scale enterprises (SMEs): government and financial institutions support in Nigeria. International Journal of Academic Research in Business and Social Sciences, 5(3):525-537. [ Links ]

- ABSA see Amalgamated Banks of South Africa. [ Links ]

- Adebayo, P.O. 2016. Impact of government entrepreneurial programmes on youth SMEs participation in Nigeria. Journal of Business and African Economy, 2(2):32-45. [ Links ]

- Adinolfi, M.C., Jacobs, M. & Tichaawa, T.M. 2018. Unpacking factors limiting and promoting black-owned SMMEs to participate actively within the tourism value chain in South Africa. Africa Insight, 48(3):88-104. [ Links ]

- Adom, D., Yeboah, A. & Ankrah, A.K. 2016. Constructivism philosophical paradigm: implication for research, teaching and learning. Global Journal of Arts, Humanities and Social Sciences, 4(10):1-9. [ Links ]

- Ajagbe, A.M., Olujobi, J.O., Uduimoh, A.A., Okoye, L.U. & Oke, A.O. 2016. Technology-based entrepreneurship financing: lessons for Nigeria. International Journal of Academic Research in Accounting, Finance and Management Sciences, 6(1):150-163 [https://doi.org/10.6007/IJARAFMS/v6-i1/2009]. [ Links ]

- Akinyemi, F.O. & Adejumo, O.O. 2018. Government policies and entrepreneurship phases in emerging economies: Nigeria and South Africa. Journal of Global Entrepreneurship Research, 8(1):1-18. [ Links ]

- Akinyemi, F. & Ojah, K. 2018. Transition probabilities between entrepreneurship phases in Africa's emerging economies: the case of Nigeria and South Africa. Journal of Developmental Entrepreneurship, 23(3):1-20 [https://doi.org/10.1142/S1084946718500164]. [ Links ]

- Alase, A. 2017. The interpretative phenomenological analysis (IPA): a guide to a good qualitative research approach. International Journal of Education and Literacy Studies, 5(2):9-19 [https://doi.org/10.7575/aiac.ijels.v.5n.2p.9]. [ Links ]

- Aluko, T.O. 2018. The effectiveness of small enterprise cost-sharing and cooperative grant incentive schemes in South Africa. Stellenbosch: Stellenbosch University. (Doctoral dissertation). [ Links ]

- Amalgamated Banks of South Africa. 2022. Get the funding to grow your small business. [Internet: https://www.absa.co.za/business/funding-my-business/kzn-small-business-funding/; downloaded on 15 January 2022]. [ Links ]

- Amankwah-Amoah, J., Khan, Z. & Wood, G. 2021. COVID-19 and business failures: the paradoxes of experience, scale, and scope for theory and practice. European Management Journal, 39(2):179-184 [https://doi.org/10.1016/j.emj.2020.09.002]. [ Links ]

- Anney, V.N. 2014. Ensuring the quality of the findings of qualitative research: looking at trustworthiness criteria. Journal of Emerging Trends in Educational Research and Policy Studies, 5(2):272-281. [ Links ]

- Appiah, I. 2019. The determinants of non-performing loans amongst tier 4 banks in Ghana: a case study of FNB bank Ghana Limited. Accra: University of Ghana. (Doctoral dissertation). [ Links ]

- Armanios, D.E., Eesley, C.E., Li, J. & Eisenhardt, K.M. 2017. How entrepreneurs leverage institutional intermediaries in emerging economies to acquire public resources. Strategic Management Journal, 38(7):1373-1390 [https://doi.org/10.1002/smj.2575]. [ Links ]

- Ashmore, D.P., Thoreau, R., Kwami, C., Christie, N. & Tyler, N.A. 2018. Using thematic analysis to explore symbolism in transport choice across national cultures. Transportation, 47(2):1-34 [https://doi.org/10.1007/s11116-018-9902-7]. [ Links ]

- Atiase, V.Y., Mahmood, S., Wang, Y. & Botchie, D. 2018. Developing entrepreneurship in Africa: investigating critical resource challenges. Journal of Small Business and Enterprise Development, 25(4):644-666 [https://doi.org/10.1108/JSBED-03-2017-0084]. [ Links ]

- Audretsch, D.B., Lehmann, E.E., Paleari, S. & Vismara, S. 2016. Entrepreneurial finance and technology transfer. The Journal of Technology Transfer, 41(1):1-9 [https://doi.org/10.1007/s10961-014-9381-8]. [ Links ]

- Ayandibu, A.O. & Houghton, J. 2017. External forces affecting small businesses in South Africa: a case study. Journal of Business and Retail Management Research, 11(2):49-64. [ Links ]

- Aziz, G. 2017. Youth ministry as an agency of youth development for the vulnerable youth of the Cape Flats. Verbum et Ecclesia, 38(1):1-6 [https://doi.org/10.4102/ve.v38i1.1745]. [ Links ]

- Baluku, M.M., Kikooma, J.F. & Kibanja, G.M. 2016. Does personality of owners of enterprises matter for the relationship between start-up capital and entrepreneurial success? African Journal of Business Management, 10(1):13-23. [ Links ]

- Bellavitis, C., Filatotchev, I., Kamuriwo, D.S. & Vanacker, T. 2017. Entrepreneurial finance: new frontiers of research and practice. Venture Capital, 19(1):1-17 [https://doi.org/10.1080/13691066.2016.1259733]. [ Links ]

- Ben-Yashar, R., Krausz, M. & Nitzan, S. 2018. Government loan guarantees and the credit decision-making structure. Canadian Journal of Economics/Revue canadienne d'économique, 51(2):607-625 [https://doi.org/10.1111/caje.12332]. [ Links ]

- Bergek, A. & Norrman, C. 2008. Incubator best practice: a framework. Technovation, 28(1-2):20-28 [https://doi.org/10.1016/j.technovation.2007.07.008]. [ Links ]

- Block, J.H., Colombo, M.G., Cumming, D.J. & Vismara, S. 2018. New players in entrepreneurial finance and why they are there. Small Business Economics, 50(2):239-250 [https://doi.org/10.1007/s11187-016-9826-6]. [ Links ]

- Braun, V. & Clarke, V. 2012. Thematic analysis. In Cooper, H. (ed). APA handbook of research methods in psychology. Vol. 2. Washington, DC: American Psychological Association. pp. 57-71. [ Links ]

- Breivik-Meyer, M., Arntzen-Nordqvist, M. & Alsos, G.A. 2019. The role of incubator support in new firms' accumulation of resources and capabilities. Innovation, 3(20):1-22 [https://doi.org/10.1080/14479338.2019.1684204]. [ Links ]

- Bruton, G., Khavul, S., Siegel, D. & Wright, M. 2015. New financial alternatives in seeding entrepreneurship: microfinance, crowdfunding, and peer-to-peer innovations. Entrepreneurship Theory and Practice, 39(1):9-26 [https://doi.org/10.1111/etap.12143]. [ Links ]

- Bryce, R.J. 2017. The flourishing entrepreneur: a case for legislative intervention to support healthy SMME financial access in South Africa. Cape Town: University of Cape Town. (Master's thesis). [ Links ]

- Business Fuel. 2022. Business loans up to R3 million. [Internet: https://www.businessfuel.co.za/?utmsource=google&utmmedium=cpc&utmcampaign=brand&gclid=CjwKCAiAomPBhBBEiwAcg7smV3rn8LUIy373kFjKLdN8soHE47BaHqUMfw86dhO9uIGRb3dY7WE6hoCAe4QAvDBwE#; downloaded on 15 January 2022]. [ Links ]

- Business Partners. 2017. SME toolkit, small enterprise finance agency. [Internet: https://smetoolkit.businesspartners.co.za/en/content/small-enterprise-finance-agency-sefa; downloaded on 12 May 2020]. [ Links ]

- Business Partners. 2022. Our application process. [Internet: https://www.businesspartners.co.za/business-funding/?gclid=CjwKCAiAomPBhBBEiwAcg7smfAC5uvFtSQxuLLLsEs8p31n-g-sMtG3oBurvxF5KqS6MFKUpaMEhoC3rcQAvDBwE; downloaded on 15 January 2022]. [ Links ]

- BUSINESSTECH. 2019. Standard Bank reduces business loan application times: from a month to 3 minutes. [Internet: https://businesstech.co.za/news/banking/348270/standard-bank-reduces-business-loan-application-times-from-a-month-to-3-minutes/; downloaded on 15 January 2022]. [ Links ]

- Calza, F., Dezi, L., Schiavone, F. & Simoni, M. 2014. The intellectual capital of business incubators. Journal of Intellectual Capital, 15(4):597-610 [https://doi.org/10.1108/JIC-07-2014-0086]. [ Links ]

- Cant, M.C. & Rabie, C. 2018. Township SMME sustainability: a South African perspective. Acta Universitatis Danubius. Cconomica, 14(7):227-247. [ Links ]

- Cant, M.C., Wiid, J.A. & Hung, Y.T. 2018. Internet-based ICT usage by South African SMEs: are the benefits within their reach? Problems and Perspectives in Management, 13(2-si):444-451. [ Links ]

- Chinomona, E. & Maziriri, E.T. 2015. Women in action: challenges facing women entrepreneurs in the Gauteng province of South Africa. International Business & Economics Research Journal, 14(6):835-850 [https://doi.org/10.19030/iber.v14i6.9487]. [ Links ]

- Chowdhury, M.S., Ahmmed, F. & Hossain, M.I. 2019. Neoliberal governmentality, public microfinance and poverty in Bangladesh: who are the actual beneficiaries? International Journal of Rural Management, 15(1):23-48 [https://doi.org/10.1177/0973005218817657]. [ Links ]

- Cowling, M., Ughetto, E. & Lee, N. 2018. The innovation debt penalty: cost of debt, loan default, and the effects of a public loan guarantee on high-tech firms. Technological Forecasting and Social Change, 127:166-176 [https://doi.org/10.1016/j.techfore.2017.06.016]. [ Links ]

- Cramer-Petersen, C.L., Christensen, B.T. & Ahmed-Kristensen, S. 2019. Empirically analysing design reasoning patterns: abductive-deductive reasoning patterns dominate design idea generation. Design Studies, 60:3970 [https://doi.org/10.1016yj.destud.2018.10.001]. [ Links ]

- Creswell, J.W. 2007. Qualitative inquiry and research design: choosing among five approaches. 2nd ed. Thousand Oaks, CA: SAGE. [ Links ]

- Creswell, J.W. 2014. A concise introduction to mixed methods research. Thousand Oaks, CA: SAGE. [ Links ]

- Cumming, D., Deloof, M., Manigart, S. & Wright, M. 2019. New directions in entrepreneurial finance. Journal of Banking & Finance, 100:252-260 [https://doi.org/10.1016/j.jbankfin.2019.02.008]. [ Links ]

- Decoster, A., Pirttilà, J., Sutherland, H. & Wright, G. 2019. SOUTHMOD: modelling tax-benefit systems in developing countries. International Journal of Microsimulation, 12(1):1-12 [https://doi.org/10.34196/iim.00192]. [ Links ]