Services on Demand

Article

English (pdf)

English (pdf)

Article in xml format

Article in xml format Article references

Article references

Indicators

Related links

-

Cited by Google

Cited by Google -

Similars in Google

Similars in Google

Share

Permalink

PermalinkJournal of Contemporary Management

On-line version ISSN 1815-7440

JCMAN vol.19 n.1 Meyerton 2022

http://dx.doi.org/10.35683/jcm21081.144

ARTICLES

Direct and indirect influence of attachment in retaining wealth management customers

Hester SpiesI, ; Falkor Frank Norman EckardtII; Leon T De BeerIII

IWorkWell Research Unit, North-West University, South Africa. Email: hester.spies@nwu.ac.za; ORCID: https://orcid.org/0000-0003-0710-2256

IIWorkWell Research Unit, North-West University, South Africa. Email: falkoreckardt@gmail.com; ORCID: https://orcid.org/0000-0003-4391-7460

IIIWorkWell Research Unit, North-West University, South Africa. Email: DeBeer.Leon@nwu.ac.za; ORCID: https://orcid.org/0000-0001-6900-2192

ABSTRACT

ORIENTATION: The financial gain of retaining wealth management customers cannot be contested. In order to enhance customer retention rates, various researchers are of the opinion that organisations should focus their relationship marketing strategies on attached customers

PURPOSE OF THE STUDY: The purpose of this study was to determine whether customer attachment can be valuable to wealth managers in enhancing customer retention

MOTIVATION FOR THE STUDY: The relationship building construct attachment which might influence retention has received no scholarly attention. Attachment has also never been modelled together with key retention constructs (satisfaction and trust

DESIGN/METHODOLOGY/APPROACH: A quantitative descriptive research design was used to collect data through online computer administered questionnaires from a sample of 1230 wealth management customers in South Africa. A structural equation modelling approach was used to the test the hypotheses

FINDINGS: The results established that respondents' attachment directly influenced retention and indirectly influenced the relationships between satisfaction and retention as well as trust and retention. The results also indicated that satisfaction and trust was significantly related to both attachment and retention

CONTRIBUTION/VALUE-ADD: This study not only empirically confirms the direct effect of customer attachment on retention but also its indirect effect on satisfaction and retention as well as trust and retention. This is the first time that this combination of factors are modelled together, to assess the extent to which they are interrelated and collectively contribute to retention

MANAGERIAL IMPLICATIONS: The findings could assist wealth managers in their efforts to retain customers, by establishing customer attachment, satisfaction and trust

JEL CLASSIFICATION: M31

Keywords: Attachment, retention, satisfaction, trust, wealth management.

1. INTRODUCTION

Customer retention has consistently proven to serve as a key concept for any organisation's long-term success as it ensures various beneficial outcomes (profitability, reduced costs, premium pricing and positive word-of-mouth endorsement) (Lovelock & Wirtz, 2018; Zeithaml et al., 2018; Almohaimmeed, 2019). The importance of retaining customers is even more prevalent in today's competitive marketplace, as customers are increasingly exposed to diverse attractive alternatives (Chen & Liu, 2019). This is particularly the case for the wealth managers in South Africa who are confronted with the growth of unexpected players that provide in-house advisory and digital solutions, low-cost operating models and enhanced supply-chain integration (PwC (Price Waterhouse Coopers), 2018). Therefore, it not surprising that various financial institutions make every endeavour to better understand how to increase repeat business (Darzi & Bhat, 2018). The popularity of customer retention has not only attracted practitioners, but also researchers who have over the years confirmed and understood customer retention as an outcome of key factors, namely, trust, satisfaction and switching costs (Simarmata et al., 2017; Amanah et al., 2021).

One variable that could impact customer retention and which has not been fully explored is that of customer attachment. Customer attachment centres around the bond formed between the customer and the organisation or employee (Moussa & Touzani, 2017; Verbeke et al., 2017). Various researchers regard the bond in customer-organisational relationships as the quintessence of strong relationships as it motivates customers to return and continue the relationship (Moussa & Touzani, 2013; Awwad & AL-Qralleh, 2014). Consequently, the impact of customer attachment on retention should not be undervalued and requires further investigation. A review of the related literature reveals that although customer attachment and retention has been intensively investigated as individual constructs, no study has empirically tested how these two specific constructs relate to each other. Consequently, little is known about the empirical understanding of the impact of customer attachment on retention. Relying on the relationship marketing view - which is often implemented by financial institutions to obtain a competitive advantage (Darzi & Bhat, 2018), this paper sets out to not only determine the direct effect of customer attachment on retention, but also its indirect effect through mediation. Examining the relationship between customer attachment and retention will not only empirically clarify and explicate the role of customer attachment in retention strategies, but also contribute to the attachment and retention research stream, which may encourage future research on the topic.

Furthermore, to assist with indirect effect of customer attachment, this study identified satisfaction and trust as independent variables that could influence both customer attachment (Ercis, 2011; Yang et al., 2019) and retention (Simarmata et al., 2017). Although satisfaction and trust in relation to customer attachment and retention has been measured before, these factors have never been modelled together, to assess the extent to which they are interrelated and collectively contribute to retention. Hence, it seems a model is required that makes provision for the interrelationships between satisfaction, trust and attachment and the contribution they make in facilitating retention. Investigating the above mentioned relationships may add to the developing body of research on satisfaction, trust and attachment and these concepts' importance to the stream of research on retention. From a practical perspective, the findings may be of value for wealth managers in South Africa who aim to differentiate themselves from their competitors through implementing effective retention strategies.

Consequently, to contribute to both theory and practice, it was the aim of this to determine whether customer attachment can be valuable to wealth managers in enhancing customer retention. In the subsequent section, the theoretical framework and hypotheses development are presented. This is followed by the research methodology, results and discussion of results. The paper concludes by discussing the limitations and providing directions for future research.

2. LITERATURE REVIEW AND RESEARCH HYPOTHESES

2.1 The wealth management industry in South Africa

The South African wealth management industry is regarded as the hub of wealth management on the African continent as it holds over twice as many High Net-Worth Individuals (HNWIs) as any other African country and is home to five US-dollar billionaires, each with net assets of $1 billion or more (AfrAsia, 2018; NWWealth (New World Wealth), 2020). Despite holding the status as the largest wealth market in Africa, there can be little doubt that many challenges remain, of which inequality and unemployment are among the most pressing as it contributes towards stagnating economic growth, corruption and "state capture" (Rudin, 2018). The recent global Covid-19 pandemic has also contributed to the number of new and unique challenges faced by wealth managers. This includes having to maintain customer confidence amidst changing and volatile market conditions, implementing new digital communication and security measures, and retaining existing customer relationships through remote working conditions (Alexander, 2020; BlackRock, 2020). These challenges have led to the rise in a number of unexpected players that provide in-house advisory solutions that adhere to current digital solution trends, low-cost operating models and supply-chain integration (KPMG, 2018; Ciriani, 2021).

In order to face these challenges and remain competitive, Graseck et al. (2020) posit that wealth managers should focus on developing deeper relationships with their customers, as it will allow them to gain a better understanding of the concerns, motivations and preferences that customers may have during these turbulent times. This view is supported by Deloitte (2020) who maintain that the future success of wealth management will rely on recognising and understanding customer goals and needs while also distinguishing themselves from competitors by improving customer relationships. To build and maintain successful long-term customer relationships, various researchers are of the opinion that financial institutions should focus their relationship marketing strategies on those customers who demonstrates high levels of satisfaction, trust (Damberg et al., 2021) and attachment (Blasius & Hady, 2018) which, in turn motivates them to return and continue the relationship.

2.2 Satisfaction

The positive outcomes of customer satisfaction in terms of loyalty, repurchasing, recommendation, cross-buying and lower price elasticity cannot be underestimated or contested. For this reason, customer satisfaction lies at the core of profitable long-term customer-organisational relationships (Pleshko & Heiens, 2015; Ozkan et al., 2019; Herjanto & Amin, 2020). Oliver (2010) defines customer satisfaction as the formation of customers' attitudes or assessments, by comparing their pre-purchase expectations (what they would receive from a product) with their subjective perceptions of the performance (what they actually did receive). Customers will, therefore, be satisfied if the performance of a product or service meets or exceeds their expectations. However, if customers' expectations are not met, they will be dissatisfied. It therefore becomes vital for organisations not only to meet customers' expectations, but also to exceed them to ensure satisfaction (Rust & Huang, 2012).

When evaluating customer satisfaction, marketing researchers usually consider one of two components, which are transaction-specific satisfaction (post-choice evaluation of a specific purchase occasion) and overall or cumulative satisfaction (customers' evaluation of the overall consumption experience with a product or service over time). While transaction-specific satisfaction provides insight into a specific service encounter, overall satisfaction serves as a better predictor of customers' future behavioural intentions (Oliver, 2010). This research consequently applies the overall satisfaction component. According to Oliver (2010), overall satisfaction can also be viewed as a function of the expectancy-disconfirmation paradigm, which is a utility of both expectations and performance. When actual performance exceeds expectations, positive disconfirmation occurs and leads to satisfaction, while actual performance below expectations results in negative disconfirmation and dissatisfaction. Organisations aiming to generate high levels of customer satisfaction should therefore ensure that their overall performance corresponds with their customers' expectations (Ozkan et al., 2019). Establishing high levels of customer satisfaction will lead not only to the abovementioned positive outcomes, but also ultimately, towards the development of successful long-term customer-organisational relationships (Herjanto & Amin, 2020).

2.3 Attachment

Bowlby, along with his student, Ainsworth formulated the fundamental principles of attachment theory, describing it as an innate, evolutionary based motivational system that protects infants from predation and environmental dangers through the maintenance of proximity to a consistent caregiver (Bowlby, 1958; Ainsworth et al., 1978). Infants communicate physiological and emotional needs in a variety of ways, including crying, reaching and eye contact, and it is the caregiver's task to comprehend these signals and to sensitively respond to them. The infant's experiences of the caregiver's availability and need gratification moulds their attachment relationship with that caregiver in the long run. Children in their infant and preschool years form multiple attachment relationships with caregivers, and all of these relationships build a repertoire of attachment related memories which they internalise as an internal working model. Internal working models shape interactions with fellow human beings and become especially relevant in times of distress throughout the person's life. Internal working models accumulate and regulate expectations of relationships, needs and emotions to develop into attachment styles at adulthood (Shaver & Mikulincer, 2005; Main et al., 2011). Infants in secure attachment relationships experience their caregivers as responsive and protecting, thus forming positive internal working models that they use to guide their perceptions and expectations in future relationships (Bowlby, 1977).

Research reveal that the majority of attachment studies focus on parent-child and adult relationships (Shaver & Mikulincer, 2005; Sutton, 2019), yet research has shown that internal working models additionally regulate individuals' perceptions and behaviours when engaging with brands and organisations (Beldona & Kher, 2015; Spies & Mackay, 2020). Attachment theory is consequently relevant to marketing research and this research investigates customer's attachment to their wealth manager. Understanding customers' internal working models may enhance the customer-organisational relationship by providing relationship marketing managers with a deeper understanding of customers' behaviours relative to the organisation (Spies & Mackay, 2020). Previous research in psychology reveals that attachment styles are best conceptualised and measured alongside two dimensions, namely attachment anxiety and attachment avoidance. Attachment anxiety stems from an individual's uncertainty about the organisation's availability in times of need and is observed in his/her heightened dependence on confirmation by the organisation. In contrast, attachment avoidance is seen as an emphasis on independence to the extent that there is an emotional and cognitive distancing from the organisation's attempts to engage (Yip et al., 2018; Sutton, 2019). Customers with low scores on these dimensions have secure customer attachment styles, while those with high scores have insecure attachment styles (Mende & Van Doorn, 2015). Customers with secure attachments form longer-lasting relationships with organisations, as they display higher levels of trust and are more satisfied with their relationship experience (Paulssen, 2009; Mende & Bolton, 2011). It would thus be advisable for organisations to focus their relationship marketing strategies on this segment of customers, as such an investment would develop into enduring customer-organisation relationships with better relationship outcomes (Aldlaigan & Buttle, 2005).

2.3.1 The link between satisfaction and attachment

Danjuma and Rasli (2012) and Xiaofei et al. (2021) regard satisfaction as an important driver of attachment. These authors argue that customers who are satisfied with the brand or organisation's service experience, are more willing to improve and sustain a bond with the brand or organisation. A stronger bond between the customer and brand or organisation eventually results in attachment. Research by Ercis (2011) and Bahri-Ammari et al. (2016) has further empirically supported and confirmed the positive relationship between satisfaction and attachment. It is therefore hypothesised that:

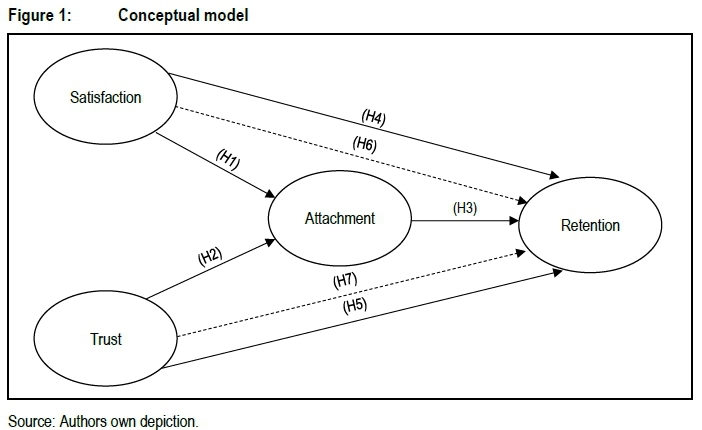

H1: Customers' satisfaction significantly impacts their attachment towards their wealth manager.

2.4 Trust

Trust refers to the customer's belief that the organisation is honest, benevolent and predictable in its behaviour. These qualities serve to break down psychological barriers and reduce the customer's level of perceived risk and uncertainty when engaging with the organisation (Viviers & Theron, 2019; Kidron, 2021). The concept of customer trust generally comprises of two aspects. The first aspect is the customer's willingness to accept a position of vulnerability based on their pre-determined expectations of the product or service that they plan to purchase from the organisation (Bugandwa et al., 2021). The second aspect refers to the faith that both the customer and organisation place in the other's undertakings (Kidron, 2021; Roberts-Lombard & Petzer, 2021). With both these aspects in mind, trust can be seen as the belief or expectation that any action the organisation takes will be in the customer's best interest (Bugandwa et al., 2021; Roberts-Lombard & Petzer, 2021). Zeka et al. (2016) and Eriksson et al. (2020) state that trust plays especially an important role in customer's relationships with their financial advisor who have an implicit responsibility to manage their customers' funds and provide reliable and sufficient financial advice. By establishing trust among their customers, financial advisors will not only be able to reap the benefits of committed customers, but also a loyal customer base.

2.4.1 The link between trust and attachment

Chinomona (2013) are of the opinion that customers with higher levels of trust are prepared to go to greater lengths to improve and sustain a bond they have with an organisation as it provides feelings of warmth and enjoyment. It is through the bond with the organisation that the customer becomes more attached towards the organisation, increasing the likelihood of developing a successful, long-term relationship. Previous studies conducted by Moussa and Touzani (2013) and Yang et al. (2019) confirm the positive relationship between trust and attachment. Therefore, it can be hypothesised that:

H2: Customers' trust significantly impacts their attachment towards their wealth manager.

2.5 Retention

Grounded in the relationship marketing theory, retention is considered to be a key factor in managing customer-bank relationships (Darzi & Bhat, 2018). The importance of retention within the relationship marketing context lies in the knowledge that existing customers are significantly less expensive to retain and more profitable to serve in the long run than acquiring new customers, which necessitates the investment of valuable resources and time (Zeithaml et al., 2018). Hanaysha (2018) define retention as the continuation of a business relationship between a customer and an organisation. The continuity of these relationships will generally provide organisations with a variety of benefits which comprises of economic benefits (greater profit margins, improved return on investment, repeat purchases, reduced costs and premium pricing), customer behaviour benefits (free advertising, customer voluntary performance and social benefits) and human resource benefits (customer involvement in the service delivery process, developing bonds between customers and employees and relational competitive advantages) (Lovelock & Wirtz, 2018; Zeithaml et al., 2018; Almohaimmeed, 2019).

Organisations, however, are not the sole recipients of the benefits relating to customer retention; customers also stand to benefit in the form of confidence benefits (higher trust levels, reduced anxiety and a sense of comfort), social benefits (sense of familiarity with the organisation or its employees) and special treatment benefits (reduced prices and faster or individualised services) (Zeithaml et al., 2018). Khan (2012) and Darzi and Bhat (2018) advise that if organisations wish to retain their customers, they must first endeavour to understand and address their ever-changing needs. According to these authors, should organisations sufficiently understand and address the needs of their customers, they might be able to reap the benefits of higher profit margins and a competitive advantage.

2.5.1 The link between attachment and retention

A customer's intention to return and maintain a business relationship is grounded on forming emotional bonds with the organisation and the belief that remaining in a relationship with that organisation will yield greater benefits (Awwad & AL-Qralleh, 2014). Moussa and Touzani (2013) and Awwad and AL-Qralleh (2014) explain that customers who have developed a bond with an organisation have a stronger emotional attachment to the organisation. Customers who are attached to the organisation may fear the consequences of losing the relationship (such as their relationship bond and benefits) which, in turn motivates them to return and continue the relationship. Although the relationship between attachment and retention has not been empirically tested before, it is supported by theory. As such, the following hypothesis is presented for this research:

H3: Customers' attachment significantly impacts their retention towards their wealth manager.

2.5.2 Link between satisfaction and retention

According to Ibojo (2015), the process of ensuring that customers are satisfied is an integral part of any organisation's objectives. This is because when an organisation strives to satisfy the needs of its customers, they lay the foundation for building and maintaining long-lasting relationships. Zeithaml et al. (2018) add that if the organisation can continuously satisfy the needs of its customers, they will be more likely to remain in a relationship with the organisation. These authors explain that as the customers' levels of satisfaction increase, so will their loyalty to the organisation, which in turn results in higher customer retention. This positive relationship between satisfaction and retention is supported and confirmed through research studies done by Simarmata et al. (2017) and Shrestha (2020) who established that satisfaction is a significant driver of retention. Therefore, it can be hypothesised that:

H4: Customers' satisfaction significantly impacts their retention towards their wealth manager.

2.5.3 Link between trust and retention

Once a customer trusts an organisation, they will hold firm in their belief that the organisation will refrain from any opportunistic behaviour. Therefore, enhancing the customer's belief in an organisation's trustworthiness will significantly reduce their sense of uncertainty and vulnerability when dealing with the organisation (Bugandwa et al., 2021). Diminishing these uncertainties will enable customers to make confident predictions about the organisation's future dealings, which in turn will increase their desire to return and maintain their relationship with the organisation (Eriksson et al., 2020; Bugandwa et al., 2021). The relationship between trust and retention is supported and confirmed through research studies done by Simarmata et al. (2017) and Islam et al. (2020), who established that trust serves as a significant driver of retention. Therefore, it can be hypothesised that:

H5: Customers' trust significantly impacts their retention towards their wealth manager.

2.6 The mediating effect of attachment

The proposed relationships discussed in the previous sections shed further light on the possibility of attachment to serve as a potential mediating variable between satisfaction and retention as well as between trust and retention. Hence, it is proposed that:

H6: Customers' level of satisfaction has a significant and indirect effect on their retention, as mediated by their attachment to their wealth manager.

H7: Customers' level of trust has a significant and indirect effect on their retention, as mediated by their attachment to their wealth manager.

Figure 1 demonstrates the hypothesised relationships between the relevant constructs under investigation, as proposed from the above literature discussion.

3. METHODOLOGY

3.1 Population, research design, data collection and sampling approach

This study followed a positivism, deduction research philosophy paradigm as existing theory was used to develop hypotheses. Various statistical tests were utilised to test the theory by collecting new data from respondents and observe the findings (Rahi, 2017; Saunders et al., 2019). The participants in this study were residents of South Africa who made use of wealth management services. Before observing and investigating the behaviour of these participants, ethical clearance was obtained from the necessary governing body to ensure that ethical standards were followed. Following the ethical clearance, a quantitative descriptive (cross-sectional) research design was carried out. Data were collected using computer administered questionnaires that were posted on different residential Facebook groups. Online questionnaires were selected as this type of data collection method is inexpensive and allowed for easy access to the sample of the study (Malhotra et al., 2017). The largest residential online Facebook groups in all nine provinces were surveyed, with smaller online Facebook groups in each province. Although the members of each Facebook group were known to the researcher, their contact details were not available, making them inaccessible. Consequently, multiple non-probability sampling methods (convenience and snowball sampling) were used. Based on convenience, members were invited to participate in the study by posting a hyperlink of the online questionnaire in the newsfeed of each Facebook group. Upon completion of the survey, each respondent was presented with the option to recommend the survey to other eligible respondents within their respective networks. Snowball sampling was deemed necessary as the High Net-Worth Individual (HNWI) population in South African consist of approximately 38 400 individuals (NWWealth, 2020), making it is difficult to identify wealth management customers in South Africa.

A total of 1591 respondents responded to the online questionnaire, with 1230 respondents completing the questionnaire, resulting in a 77.31 percent response rate. The realised sample size of 1230 respondents exceeded the sample size of 500 as suggested by Hair et al. (2019) for model development. In the realised sample, the majority of the respondents who participated in this study were female (60.3%), married (59.2%) and white (88.6%), and belonged to the age group of 48 to 66 years old (34.4%). A total of 86 percent of the respondents indicated they were self-employed or employed full-time by an organisation. The respondents were further invited to indicate the duration for which they had been making use of their wealth manager's services. The results revealed that the majority indicated a period of 1 to 5 years (41%).

3.2 Questionnaire development

The questionnaire utilised for this study was in the form of an online survey developed using Google forms, comprising three sections. The first section commenced with a preamble that explained the instructions for completing the questionnaire, the purpose of the research, and respondents' rights and obligations. A screening question was also included in the preamble to ensure that only eligible respondents completed the questionnaire (i.e. residents of South Africa who made use of wealth management services). The second section of the questionnaire aimed to obtain some socio-demographic information of respondents, and the third section measured the related constructs (i.e. satisfaction, trust, attachment and retention). The constructs used in this research were measured using labelled five-point Likert-type scales (with 1 representing "strongly disagree" and 5 representing "strongly agree") adapted from existing, valid and reliable scales. Satisfaction and trust were measured using a scale adapted from the works of Brady and Robertson (2001) as well as Dagger and O'Brien (2010). To measure attachment, a scale was adapted from Mende et al. (2013), and to measure retention, a scale was adapted from the works of Nguyen and Leblanc (2001) as well as Hennig-Thurau (2004). The questionnaire was pilot tested on a convenience sample of 30 respondents from the target population, resulting in some technical adjustments.

3.3 Data analysis

The data was analysed utilising both the IBM SPSS (version 27) and Mplus 8.3 programmes. The descriptive statistics and Cronbach's alpha coefficients were assessed by means of IBM SPSS, and Mplus was used to apply latent variable modelling via structural equation modelling (SEM) to compare the relationships between respondents' satisfaction, trust, attachment and retention (Muthen & Muthen, 2017). SEM was deemed an appropriate statistical technique to apply for this research, as it allows the researcher to test how well the theory fits the reality by stipulating all the applicable research variables into one model. In the SEM, the Maximum Likelihood was used for parameter estimation, as this has been considered most suitable for multivariate normal data. Mplus also generated a zero-order correlation matrix, which allowed the researcher to investigate the correlations between the latent variables. Effect sizes for the correlation values were considered to have a large practical effect with r > 0.50 (Hair et al., 2019).

With regard to the fit indices of the measurement model (confirmatory factor analysis [CFA]), the comparative fit index (CFI), the Tucker-Lewis index (TLI) and the root mean square error of approximation (RMSEA) were considered as indices to assess the fit of the measurement model to the data (Van de Schoot et al., 2012). Van de Schoot et al. (2012) and Hair et al. (2019) suggest that the cut-off values for both the CFI and TLI should be above 0.90 and the RMSEA requires a value of up to 0.10 to be considered acceptable. Finally, through Mplus, the model's indirect function was specified in accordance with the hypotheses to investigate the potential mediating variables in the research model. The mediation was tested through bootstrapping resampling with requests for 5000 draws and bias-corrected 95 percent confidence intervals in the output, focusing on the size of the indirect effects. An investigation was therefore made to assess whether the indirect effects would not cross zero at that level.

4. RESULTS

4.1 Measurement model

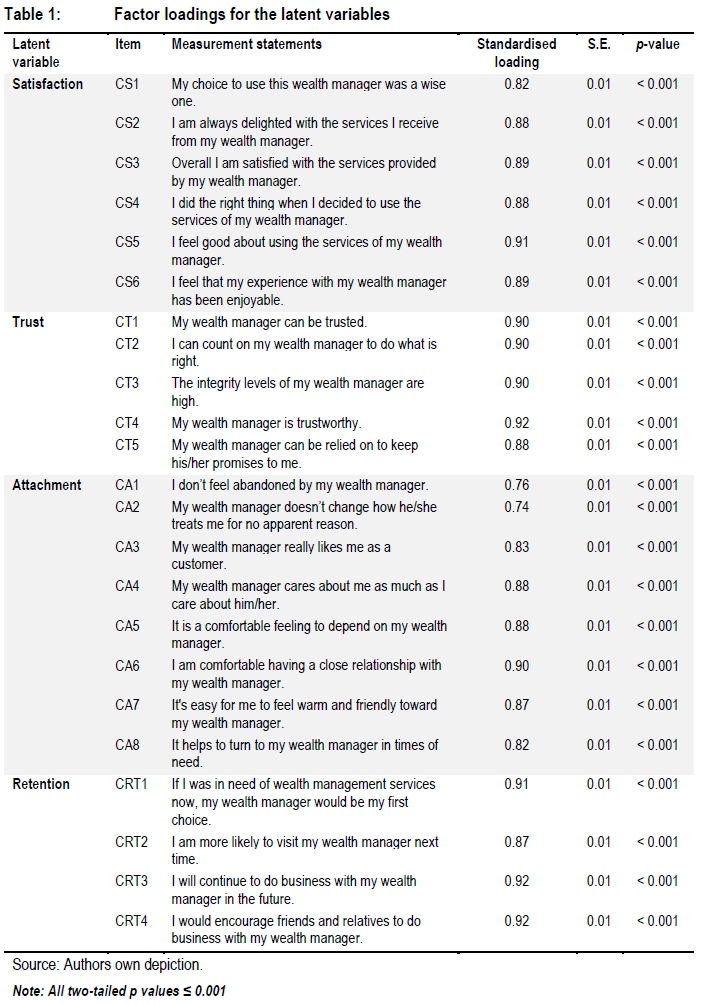

The results of the confirmatory factor analysis revealed that the specified model was an acceptable fit to the data: the CFI (0.97) and TLI (0.97) were both above the lower bound cutoff point of 0.90 and the RMSEA (0.06) was below the value of 0.08. The factor loadings for the latent variables were also calculated and are presented in Table 1.

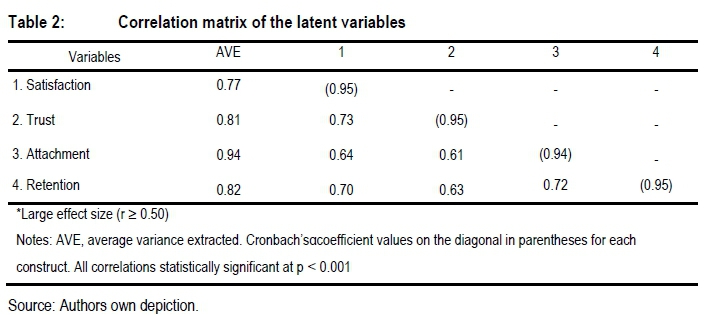

From Table 1 it can be observed that the factor loadings of all the items loaded significantly on the corresponding latent factor, ranging from 0.74 to 0.92 (above the suggested threshold of 0.5) (Hair et al., 2019). The standard errors for each of the standardised estimates were small, demonstrating accuracy in estimation of these values. Table 2 reflects the statistics for the correlation matrix for the latent variables, as well as the AVE and the Cronbach's reliability estimates on the diagonal.

The results of Table 2 demonstrate that all correlations between the latent constructs were significant (p < 0.001), and the AVE for any two individual constructs was greater than the squared correlation estimate between them, providing supportive evidence for separate constructs. The model therefore demonstrates discriminant validity among the constructs assessed. The results of the model also confirm convergent validity as the AVE and composite reliability as presented on the diagonal in parentheses were above the cut-off value of 0.50 and 0.70 respectively. The composite reliability scores also indicate high reliability and internal consistency of the research constructs as the overall Cronbach's alpha value for each construct is greater than 0.7 (Hair et al., 2019).

4.2 Structural Model

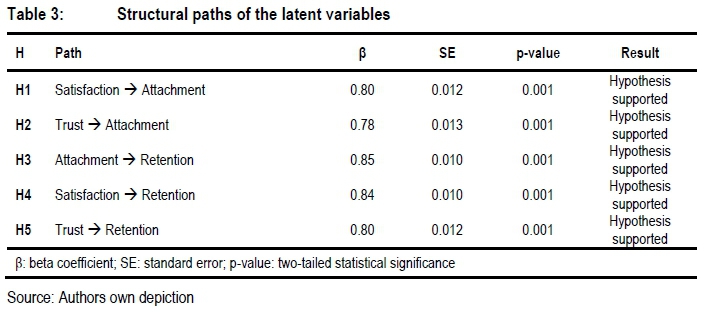

The acceptable model fit of the measurement model (CFA), factor loadings, reliability, correlational relationships as well as discriminant and convergent validity allowed for the continued analysis by specifying a structural model and adding regressions to the measurement model, as hypothesised from the literature. Table 3 presents the results of the structural model estimated.

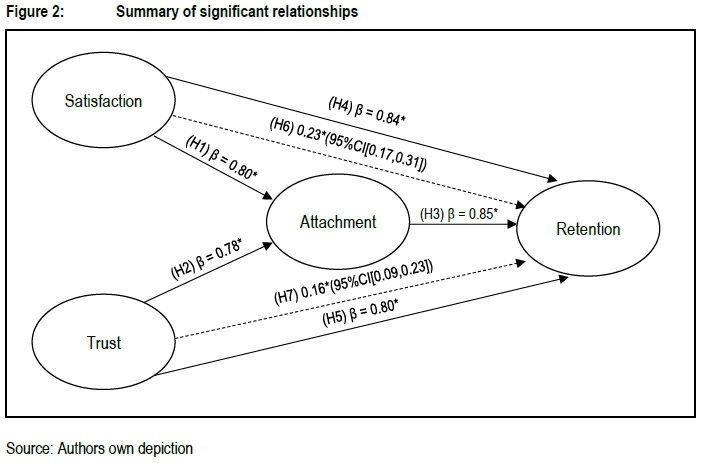

The regression results revealed that satisfaction had a significant impact on attachment (P = 0.80; SE = 0.012; p < 0.001; supporting H1) and retention (P = 0.84; SE = 0.010; p < 0.001; supporting H4). Attachment, in turn, had a significant impact on retention (P = 0.85; SE = 0.010; p < 0.001; supporting H3). Lastly, in terms of regression, trust had a significant impact on attachment (P = 0.78; SE = 0.013; p < 0.001; supporting H2) and retention (P = 0.80; SE = 0.012; p < 0.001; supporting H5).

4.3 Structural model: Indirect effects

Due to the significant relationship from satisfaction to attachment as well as trust to attachment, and their subsequent relationships to retention, both indirect effects were investigated, as indicated in Table 4.

Results from the bootstrapping resampling implementation revealed that both indirect effects were significant: the relationship from satisfaction to retention through attachment (0.23; 95% CI [0.17, 0.31]; p< 0.001) and from trust to retention through attachment (0.16; 95% CI [0.09, 0.23]; p< 0.001). A summary of the significant relationships identified in the SEM is presented in Figure 2.

5. DISCUSSION, CONCLUSIONS, LIMITATIONS AND RECOMMENDATIONS FOR FUTURE RESEARCH

5.1 Theoretical discussion

Attaining customer retention is of value for any organisation aiming to increase sales and profit margins as it renders various benefits in the form of reduced costs, premium pricing and positive word-of-mouth. It is this cost-saving, profit enhancing property that encourages relationship marketing managers and researchers to continuously explore the customer retention topic to gain further insight and enable organisations to take full advantage of its benefits. The current study contributes to the conversation on customer retention in several ways. First, the study confirms the work of earlier scholars who have confirmed the effects of customer satisfaction and trust on both attachment (Ercis, 2011; Yang et al., 2019) and retention (Simarmata et al., 2017). When customers are satisfied with an organisation, and when a relationship of trust has been established, they may become more attached with and return to the organisation. Second, the research findings also confirmed that customer attachment statistically significantly influences retention. This result is consistent with arguments of Moussa and Touzani (2013) as well as Awwad and AL-Qralleh (2014), who argue that attached customers develop a bond with an organisation which motivates them to return and continue the relationship. Regardless of the well-reasoned arguments supporting the relationship between attachment and retention, the relationship between these two constructs have not been empirically tested previously. Therefore, this paper empirically contributes to the theory by confirming the relationship between attachment and retention.

Third, support for H1-H5 further leads to the discovery that attachment also serves a mediating role in strengthening the connection between satisfaction and retention as well as between trust and retention. This result is unique in that previous studies have not examined these indirect relationships which could better explain the relationships between the above-mentioned constructs. It appears that while it is important for organisations to establish satisfaction and trust among their customers when developing retention strategies, they should consider that customer attachment plays a central role in retaining their customers. Therefore, wealth managers cannot rely on customer satisfaction and trust alone to generate retention. These results are noteworthy, as extant research has not provided a comprehensive explanation of the role and relevance of satisfaction, trust and attachment, while simultaneously being measured for their contribution to customer retention. Therefore, the results of this study provide new insight into the interrelationships between satisfaction, trust and attachment in contributing to customer retention, which makes an original contribution to the body of knowledge in understanding customer retention.

5.2 Managerial implications

The purpose of this study was to determine whether customer attachment can be valuable to wealth managers in generating customer retention. The results confirm that attachment does play a central role in generating customer retention in this industry. Therefore, from a managerial perspective it is evident that wealth managers should facilitate customer retention strategies by focusing on customer attachment. Specifically, wealth managers are advised to identify securely attached customers and then attempt to build relational bonds with them. This can be achieved by being receptive and attentive to customers' signals of distress and taking action to resolve the source of the distress. As wealth managers provide their services, customers will experience various doubts or concerns about the way their money is being managed as well as various trends that may arise in the market. By being perceptive in these situations and addressing customers' concerns, the wealth manager will position themselves in their customers' minds as a secure base from which they can safely explore various wealth management avenues. This, in turn, will allow wealth managers to develop relational bonds with their customers which over time, will lead to the formation of secure attachments.

Seeing as the results also revealed that satisfaction and trust significantly influenced both attachment and retention, it is suggested that wealth managers establish satisfaction among their customers by exceeding their expectations. They should, however, carefully manage customer expectations and guard against over-promising. Customer satisfaction can also be achieved by consistently acquiring feedback from customers to address their ever-changing problems and needs. Customers will be more willing to provide valuable feedback to management if they are provided with proper communication channels like phone numbers and e-mail addresses. Wealth mangers should always strive to provide prompt service and encourage their customers to become more involved. Customer involvement assist wealth managers in tailoring their customers' financial products and services to their specific needs. Customer's overall level of satisfaction with their wealth manager may increase should these strategies be implemented consistently. Lastly, with regard to establishing customer trust it is advised that wealth managers take steps to be as transparent and forthright as possible about the services they provide as it could potentially decrease the extent to which customers feel either uncertain or vulnerable about entrusting their money to the wealth manager. Wealth managers should also aim to be available for customer queries or concerns. The increased availability may serve to enforce the customer's belief that the organisation holds their best interests at heart and will be available to them in times of need regardless of the hour. The implementation of this strategy can reduce the customer's feelings of doubt and vulnerability that they may associate with their wealth manager and thereby allow for the formation of trust between them.

5.3 Limitations and recommendations for future research

First, owing to the absence of a sample frame, non-probability sampling was implemented to select respondents, which imposes limitations on the generalisation of the results to the entire South African population. The generalisability of the results is also limited to one service setting, namely wealth management. Future research should therefore not only attempt to obtain a sample frame (such as from available customer databases), but should also consider replicating this research in other service industries, which would contribute to greater confidence in generalising the current results.

Second, although the interrelationships between satisfaction, trust, attachment and retention were adequately motivated by the literature, the research did not examine other prevalent relationship marketing elements that could provide additional insight into the relationship between a customer and a wealth manager. Consequently, future research could consider including other relationship marketing elements (such as commitment, loyalty, shared values and detachment), which are also believed to influence the formation of customer-organisational relationships.

6. CONCLUSION

The aim of this article was to determine whether customer attachment can be valuable to wealth managers in generating customer retention. The results reveal that customer attachment does contribute towards retaining customers as it directly influences retention and indirectly influence the relationships between satisfaction and retention as well as trust and retention. This research is the first to link customer attachment to retention in customer-organisational relationships. It is also the first study to model attachment together with key retention constructs (satisfaction and trust). This research study, therefore, does not only contribute towards the attachment and retention theories but also empirically clarifies the influence of attachment on retention that contributes towards retaining wealth management customers. The importance of attachment in retaining and building customer-wealth management relationships should therefore not be ignored, and wealth managers are encouraged to build bonds with their customers, with the aim of retaining these customers. This aim can also be achieved by ensuring customers are satisfied and by instilling a sense of trust among them.

REFERENCES

AfrAsia. 2018. The AfrAsia bank South Africa wealth report. [Internet: https://www.afrasiabank.com/media/2770/south-africa-2018.pdf: download on 18 March 2021]. [ Links ]

Ainsworth, M.D.S., Blehar, M.C., Waters, E. & Wall, S. 1978. Patterns of attachment: a psychological study of the strange situation. Erlbaum: Oxford. [https://doi.org/10.1037/t28248-000]. [ Links ]

Aldlaigan, A. & Buttle, F. 2005. Beyond satisfaction: customer attachment to retail banks. International Journal of Bank Marketing, 23(4):349-359. [https://doi.org/10.1108/02652320510603960]. [ Links ]

Alexander, O. 2020. Asset & wealth management and COVID-19: emerging stronger from uncertain times. [Internet: https://www.pwc.com.au/asset-management/asset-wealth-management-and-covid-19.html: downloaded on 22 February 2021]. [ Links ]

Almohaimmeed, B. 2019. Pillars of customer retention: an empirical study on the influence of customer satisfaction, customer loyalty, customer profitability on customer retention. Serbian Journal of Management, 14(2):421-435. [http://dx.doi.org/10.5937/sjm14-15517]. [ Links ]

Amanah, D., Handoko, B. & Hafas, H.R. 2021. Customer retention: switching cost and brand trust perspectives. PalArch's Journal of Archaeology of Egypt/Egyptology, 18(4):3552-3561. [ Links ]

Awwad, M.S. & AL-Qralleh, A.A. 2014. Relationship marketing and customer retention: the case of Jordanian mobile telecommunications companies. Administrative Sciences, 41(2):435-450. [https://doi.org/10.12816/0007481]. [ Links ]

Bahri-Ammari, N., Van Niekerk, M., Khelis, H.B. & Chtioui, J. 2016. The effects of brand attachment on behavioral loyalty in the luxury restaurant sector. International Journal of Contemporary Hospitality Management, 28(3):559-585. [https://doi.org/10.1108/IJCHM-10-2014-0508]. [ Links ]

Beldona, S. & Kher, H.V. 2015. The impact of customer sacrifice and attachment styles on perceived hospitality. Cornell Hospitality Quarterly, 56(4):355-368. December issue. [https://doi.org/10.1177%2F1938965514559048]. [ Links ]

BlackRock. 2020. Adapting to uncertainty: the impact of Covid-19 on wealth managers in Europe. [Internet: https://www.blackrock.com/ch/individual/en/literature/brochure/adapting-to-uncertainty-en-emea-pc-brochure.pdf; downloaded on 25 February 2021]. [ Links ]

Blasius, F.J. & Hady, H. 2018. Emotional attachment investigation, customer relationship management, creating customer loyalty in priority banks in Indonesia. American Research Journal of Business and Management, 4(1):1-21. [ Links ]

Bowlby, J. 1958. The nature of a child's tie to his mother. International Journal of Psychoanalysis, 99(1):265-272. [ Links ]

Bowlby, J. 1977. The making and breaking of affectional bonds. The British Journal of Psychiatry, 130(3):201-210. [https://doi.org/10.1192/bjp.130.3.201]. [ Links ]

Brady, M.K. & Robertson, C.J. 2001. Searching for a consensus on the antecedent role of service quality and satisfaction: an exploratory cross-national study. Journal of Business Research, 51(1):53-60. [https://doi.org/10.1016/S0148-2963(99)00041-7]. [ Links ]

Bugandwa, T.C., Kanyurhi, E.B., Akonkwa, D.B.M. & Mushigo, B.H. 2021. Linking corporate social responsibility to trust in the banking sector: exploring disaggregated relations. International Journal of Bank Marketing, 39(4):592-617. [https://doi.org/10.1108/IJBM-04-2020-0209]. [ Links ]

Chen, C.M. & Liu, H.M. 2019. The moderating effect of competitive status on the relationship between customer satisfaction and retention. Total Quality Management & Business Excellence, 30(7-8):721-744. [https://doi.org/10.1080/14783363.2017.1333413]. [ Links ]

Chinomona, R. 2013. The influence of brand experience on brand satisfaction, trust and attachment in South Africa. International Business & Economics Research Journal, 12(10):1303-1316. [https://doi.org/10.19030/iber.v12i10.8138]. [ Links ]

Ciriani, C.M. 2021. Overcoming the three biggest threats facing wealth management. [Internet: https://internationalbanker.com/brokerage/overcoming-the-three-biggest-threats-facing-wealth-management/; downloaded 14 January 2022]. [ Links ]

Dagger, T.S. & O'Brien, T.K. 2010. Does experience matter? differences in relationship benefits, satisfaction, trust, commitment and loyalty for novice and experienced service users. European Journal of Marketing, 44(9/10):1528-1552. [https://doi.org/10.1108/03090561011062952]. [ Links ]

Damberg, S., Schwaiger, M. & Ringle, C.M. 2021. What's important for relationship management? the mediating roles of relational trust and satisfaction for loyalty of cooperative banks' customers. Journal of Marketing Analytics, 1-16. [https://doi.org/10.1057/s41270-021-00147-2] [ Links ]

Danjuma, I. & Rasli, A. 2012. Service quality, satisfaction and attachment in higher education institutions: a theory of planned behaviour perspective. International Journal of Academic Research, 4(2):96-103. [ Links ]

Darzi, M.A. & Bhat, S.A. 2018. Personnel capability and customer satisfaction as predictors of customer retention in the banking sector: a mediated-moderation study. International Journal of Bank Marketing, 36(4):663-679. [https://doi.org/10.1108/IJBM-04-2017-0074]. [ Links ]

Deloitte. 2020. Wealth management and advice in the time of coronavirus: a Deloitte perspective on the industry impact of COVID-19. [Internet: https://www2.deloitte.com/content/dam/Deloitte/ca/Documents/financial-services/ca-en-fsi-wealth-management-advice-aoda.pdf; downloaded 24 February 2021]. [ Links ]

Ercis, M.S. 2011. Factors affecting customer attachment in the marketing communication and its implementation on tourism sector. Online Journal of Communication and Media Technologies, 1(3):83-95. [https://doi.org/10.30935/ojcmt/2340]. [ Links ]

Eriksson, K., Hermansson, C. & Jonsson, S. 2020. The performance generating limitations of the relationship-banking model in the digital era-effects of customers' trust, satisfaction, and loyalty on client-level performance. International Journal of Bank Marketing, 38(4):889-916. [https://doi.org/10.1108/IJBM-08-2019-0282]. [ Links ]

Graseck, B.L., Stoklosa, M.L., Lord, N., Cyprys, M.J., Gosalia, M., Kenny, R., ... Schroeder, P. 2020. Global wealth management report: after the storm. [Internet: https://www.oliverwyman.com/content/dam/oliver-wyman/v2/publications/2020/jun/Global-Wealth-Management-Report-2020.pdf; downloaded on 16 March 2021]. [ Links ]

Hair, J.F., Black, W.C., Babin, B.J. & Anderson, R.E. 2019. Multivariate data analysis. 8th ed. Cengage: Hampshire. [ Links ]

Hanaysha, J.R. 2018. Customer retention and the mediating role of perceived value in retail industry. World Journal of Entrepreneurship, Management and Sustainable Development, 14(1):2-24. [https://doi.org/10.1108/WJEMSD-06-2017-0035]. [ Links ]

Hennig-Thurau, T. 2004. Customer orientation of service employees: its impact on customer satisfaction, commitment, and retention. International Journal of Service Industry Management, 15(5):460-478. [https://doi.org/10.1108/09564230410564939]. [ Links ]

Herjanto, H. & Amin, M. 2020. Repurchase intention: the effect of similarity and client knowledge. International Journal of Bank Marketing, 38(6):1351-1371. [https://doi.org/10.1108/IJBM-03-2020-0108]. [ Links ]

Ibojo, B.O. 2015. Impact of customer satisfaction on customer retention: a case study of a reputable bank in Oyo, Oyo state Nigeria. International Journal of Managerial Studies and Research, 3(2):42-53. [ Links ]

Islam, J.U., Shahid, S., Rasool, A., Rahman, Z., Khan, I. & Rather, R.A. 2020. Impact of website attributes on customer engagement in banking: a solicitation of stimulus-organism-response theory. International Journal of Bank Marketing, 38(6):1279-1303. [https://doi.org/10.1108/IJBM-12-2019-0460]. [ Links ]

Khan, I. 2012. Impact of customers' satisfaction and customers' retention on customer loyalty. International Journal of Scientific & Technology Research, 1(2):106-110. [ Links ]

Kidron, A. 2021. Investigating trust in the Israeli banking system from the reciprocating perspectives of customers and bankers: a mixed methods study. International Journal of Bank Marketing, 39(1):167-188. [https://doi.org/10.1108/IJBM-07-2020-0360]. [ Links ]

KPMG (Klynveld, Peat, Marwick, Goerdeler). 2018. Refocus on the customer: how customer experience is shaping the future of wealth management. [Internet: https://assets.kpmg/content/dam/kpmg/it/pdf/2018/06/Refocus-on-customer.pdf; downloaded on 16 March 2021]. [ Links ]

Lovelock, C. & Wirtz, J. 2018. Essentials of services marketing. 3rd ed. Pearson: Harlow. [ Links ]

Main, M., Hesse, E. & Hesse, S. 2011. Attachment theory and research: overview with suggested applications to child custody. Family Court Review, 49(3):426-463. [https://doi.org/10.1111/j.1744-1617.2011.01383.x]. [ Links ]

Malhotra, N.K., Nunan, D. & Birks, D.F. 2017. Marketing research: an applied approach. 5th ed. Pearson: Harlow. [ Links ]

Mende, M. & Bolton, R.N. 2011. Why attachment security matters: how customers' attachment styles influence their relationships with service firms and service employees. Journal of Service Research, 14(3):285-301. [https://doi.org/10.1177%2F1094670511411173]. [ Links ]

Mende, M., Bolton, R.N. & Bitner, M.J. 2013. Decoding customer-firm relationships: how attachment styles help explain customers' preferences for closeness, repurchase intentions, and changes in relationship breadth. Journal of Marketing Research, 50(1):125-142. [https://doi.org/10.1509%2Fjmr.10.0072]. [ Links ]

Mende, M. & Van Doorn, J. 2015. Coproduction of transformative services as a pathway to improved consumer well-being: findings from a longitudinal study on financial counselling. Journal of Service Research, 18(3):351-368. [https://doi.org/10.1177%2F1094670514559001]. [ Links ]

Moussa, S. & Touzani, M. 2013. Customer-service firm attachment: what it is and what causes it? International Journal of Quality and Service Sciences, 5(3):337-359. [https://doi.org/10.1108/IJQSS-01-2013-0002]. [ Links ]

Moussa, S. & Touzani, M. 2017. The moderating role of attachment styles in emotional bonding with service providers. Journal of Consumer Behaviour, 16(2):145-160. [https://doi.org/10.1002/cb.1605]. [ Links ]

Muthén, L.K. & Muthén, B.O. 2017. Mplus user's guide. 8th ed. Author: Los Angeles. [ Links ]

Nguyen, N. & Leblanc, G. 2001. Corporate image and corporate reputation in customers' retention decisions in services. Journal of Retailing and Consumer Services, 8(4):227-236. [https://doi.org/10.1016/S0969-6989(00)00029-1]. [ Links ]

NWWealth (New World Wealth). 2020. SA wealth report 2020: the wealthiest cities and town in South Africa. [Internet: https://cms.cnbcafrica.com/wp-content/uploads/2020/04/South-Africa-2020-1.pdf; downloaded on 24 February 2021]. [ Links ]

Oliver, R.L. 2010. Satisfaction: a behavioral perspective on the consumer. 2nd ed. M.E. Sharpe: Armonk. [ Links ]

Ózkan, P., Süer, S., Keser, i.K. & Kocakog, i.D. 2019. The effect of service quality and customer satisfaction on customer loyalty: the mediation of perceived value of services, corporate image, and corporate reputation. International Journal of Bank Marketing, 38(2):384-405. [https://doi.org/10.1108/IJBM-03-2019-0096]. [ Links ]

Paulssen, M. 2009. Attachment orientations in business-to-business relationships. Psychology & Marketing, 26(6):507-533. [https://doi.org/10.1002/mar.20285]. [ Links ]

Pleshko, L.P. & Heiens, R.A. 2015. Customer satisfaction and loyalty in the Kuwaiti retail services market: why are satisfied buyers not always loyal buyers? The International Review of Retail, Distribution and Consumer Research, 25(1):55-71. [https://doi.org/10.1080/09593969.2014.880936]. [ Links ]

PwC (Price Waterhouse Coopers). 2018. The future of banking: a South African perspective. [Internet: https://www.pwc.co.za/en/publications/the-future-of-banking.html; downloaded on 30 October 2018]. [ Links ]

Rahi, S. 2017. Research design and methods: a systematic review of research paradigms, sampling issues and instruments development. International Journal of Economics & Management Sciences, 6(2):1-5. [https://doi.org/10.4172/2162-6359.1000403]. [ Links ]

Roberts-Lombard, M. & Petzer, D.J. 2021. Relationship marketing: an S-O-R perspective emphasising the importance of trust in retail banking. International Journal of Bank Marketing, 39(5):725-750. [https://doi.org/10.1108/IJBM-08-2020-0417]. [ Links ]

Rudin, A.J. 2018. Don't underestimate South Africa's wealth market. [Internet: https://blogs.cfainstitute.org/investor/2018/06/29/dont-underestimate-south-africas-wealth-market/; download on 15 March 2021]. [ Links ]

Rust, R.T. & Huang, M. 2012. Optimizing service productivity. Journal of Marketing, 76(2):47-66. [https://doi.org/10.1509%2Fjm.10.0441]. [ Links ]

Saunders, M.N.K., Lewis, P. & Thornhill, A. 2019. Research methods for business students, 8th ed. Pearson: England. [ Links ]

Shaver, P.R. & Mikulincer, M. 2005. Attachment theory and research: resurrection of the psychodynamic approach to personality. Journal of Research in Personality, 39(1):22-45. [https://doi.org/10.1016/j.jrp.2004.09.002]. [ Links ]

Shrestha, S.K. 2020. Impact of relationship marketing on customer retention in higher education. Management Dynamics, 23(2):33-44. [https://doi.org/10.3126/md.v23i2.35804]. [ Links ]

Simarmata, J., Keke, Y., Silalahi, S.A. & Benkova, E. 2017. How to establish customer trust and retention in a highly competitive airline business. Polish Journal of Management Studies, 16(1):202-214. [http://dx.doi.org/10.17512/pjms.2017.16.1.17]. [ Links ]

Spies, H. & Mackay, N. 2020. An empirical investigation of the mediating role of customer attachment in South African private hospitals. Organizacija, 53(4):332-345. [http://doi.org/10.2478/orga-2020-0022]. [ Links ]

Sutton, T.A. 2019. Review of attachment theory: familial predictors, continuity and change, and intrapersonal and relational outcomes. Marriage & Family Review, 55(1):1-22. [https://doi.org/10.1080/01494929.2018.1458001]. [ Links ]

Van de Schoot, R., Lugtig, P. & Hox, J. 2012. A checklist for testing measurement invariance. European Journal of Developmental Psychology, 9(4):486-492. [https://doi.org/10.1080/17405629.2012.686740]. [ Links ]

Verbeke, W., Belschack, F., Bagozzi, R.P., Pozharliev, R. & Ein-Dor, T. 2017. Why some people just "can't get no satisfaction": secure versus insecure attachment styles affect one's "style of being in the social world. International Journal of Marketing Studies, 9(2):36-55. [https://doi.org/10.5539/ijms.v9n2p36]. [ Links ]

Viviers, S. & Theron, E. 2019. The effect of public investor activism on trust: a case study in the asset management sector. Journal of Economic and Financial Sciences, 12(1): 1 -14. [https://doi.org/10.4102/jef.v12i1.199]. [ Links ]

Xiaofei, Z., Guo, X., Ho, S.Y., Lai, K.H. & Vogel, D. 2021. Effects of emotional attachment on mobile health-monitoring service usage: an affect transfer perspective. Information & Management, 58(2):1-13. [https://doi.org/10.1016/j.im.2020.103312]. [ Links ]

Yang, S.B., Lee, K., Lee, H. & Koo, C. 2019. In Airbnb we trust: understanding consumers' trust-attachment building mechanisms in the sharing economy. International Journal of Hospitality Management, 83:198-209. [https://doi.org/10.1016/j.ijhm.2018.10.016]. [ Links ]

Yip, J., Ehrhardt, K., Black, H. & Walker, D.O. 2018. Attachment theory at work: a review and directions for future research. Journal of Organizational Behavior, 39(2):185-198. [https://doi.org/10.1002/job.2204]. [ Links ]

Zeithaml, V.A., Bitner, M.J. & Gremler, D.D. 2018. Services marketing: integrating customer focus across the firm. 7th ed. McGraw-Hill: New York. [ Links ]

Zeka, B., Antoni, X., Goliath, J. & Lillah, R. 2016. The factors influencing the use of financial planners. Journal of Economic and Financial Sciences, 9(1):76-92. [ Links ]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}