Serviços Personalizados

Artigo

Inglês (pdf)

Inglês (pdf)

Artigo em XML

Artigo em XML Referências do artigo

Referências do artigo

Indicadores

Links relacionados

-

Citado por Google

Citado por Google -

Similares em Google

Similares em Google

Compartilhar

Permalink

PermalinkJournal of Contemporary Management

versão On-line ISSN 1815-7440

JCMAN vol.8 no.1 Meyerton 2011

RESEARCH ARTICLES

Surviving the business life cycle: a theoretical framework for independent financial advisers

E Van TonderI; L Van ScheersII

IUniversity of Johannesburg

IIUniversity of South Africa

ABSTRACT

Independent financial advisers play a vital role in assisting clients to meet their financial goals. However, it appears that additional guidance is needed for these advisers to survive in their complex business environment, governed by strict legislation. To date, only a small amount of research has been conducted in this area and no formal research study in South Africa has provided a course of direction for these advisers. Consequently, this study aimed to expand the body of knowledge by investigating the potential problems posing a threat to the businesses of independent financial advisers in their business life cycle, as well as possible strategies that can be implemented to counter those obstacles. Based on the findings a theoretical framework was proposed, suggesting key areas independent financial advisers would need to focus on in their business life cycle to conquer the challenges they might encounter and survive. The study concluded with a number of hypotheses to set the direction for future empirical research regarding the survival and growth of independent financial advisers in South Africa.

Key phrases: Independent financial advisers, small businesses, strategies for survival

1 INTRODUCTION

There can be no doubt that the Financial Advisory and Intermediary Services Act is one of the most significant pieces of legislation ever instituted in the financial services industry (Swanepoel 2004:Preface). The main objective of the Act, which was promulgated in 2002, is to provide the core regulatory vehicle of market conduct, by regulating all the activities of financial advisers when giving financial advice to their clients (Botha, Geach, Goodall & Rossini 2003:127; INSETA 2011:10).

The introduction of the Financial Advisory and Intermediary Services Act brought about many changes to the life insurance industry. An operating licence will be granted only if a financial adviser is able to prove that he or she met all the fit and proper requirements (Anon 2004:5; INSETA 2011:11). These requirements include personal character qualities of honesty and integrity, operational ability and financial soundness (INSETA 2011:35; University of the Free State 2004:5-7). In addition to the fit and proper requirements, financial advisers also have to adhere to a code of conduct as stipulated by the Act (Anon 2004:5; INSETA 2011:148). The reason for the regulation is to assist financial advisers to be more advice-focused, rather than product-focused. Very strict requirements in terms of the processes to be followed are provided in the code of conduct to ensure that clients are given comprehensive, objective and suitable advice (Kruger 2004:43).

According to Kruger (2004:43), the Act has a great impact on independent financial advisers specifically, as they do not necessarily have the ability of a large company to take responsibility for all the compliance related issues. Independent financial are individuals or businesses that sell financial products, would normally operate small businesses and are expected to give "best advice" when recommending products to clients (UK Association of Independent Financial Advisers 2001:Internet; Wright 2008:Internet). To assist independent financial advisers in complying with the Act, numerous network organisations, such as Moonstone, Compliance Consulting and Oracle Compliance, have been established across the country (MoneyMarketing 2006:34).

These types of organisations offer valuable support and assistance, but independent financial advisers cannot only rely on their guidelines to survive and grow in the long term. Swanepoel (2004:25-26) cautions that although the Act's compliance requirements form a significant part of the business of a financial adviser and dictate their business's activities to a great extent, focusing too much on compliance related activities could destroy the business. As businesses progress through the various stages of growth, different problems also have to be solved (Hanks, Watson, Jansen & Chandler 1993:5; McKelvie & Wiklund 2010:Internet; Timmons & Spinelli 2007:261262). It further appears that small business owners do not have the necessary competencies and skills required to manage the business proficiently in the long term. According to Sha (2006:Internet) within the small business sector there is weak innovation as well as an absence of financial acumen, marketing (Van Scheers 2011:5048), entrepreneurial flair, practical knowledge and human resource management.

Because of these pitfalls, many small businesses do not reach their full potential and fail to grow. Statistics reveal that the failure rate for small businesses in South Africa specifically can be regarded as one of the highest in the world. Approximately 75% of new small businesses in South Africa do not survive. In fact, the probability of a new small business surviving more than 42 months is lower than in any other Global Entrepreneurship Monitored (GEM) sampled country (Olawale & Garwe 2010:730).

Consequently, given the background described above it appears that additional guidance is needed to assist independent financial advisers with the survival and growth of their small businesses. For them to prevail and grow in their competitive and complex business environment, they require more insight into the various problems threatening their survival and growth in their business life cycle, as well as the solutions that can be implemented to counter those obstacles.

To date, only a small amount of research has been conducted in this area and no formal research study in South Africa has provided a course of direction for these advisers, who perform a vital role in assisting clients to meet their financial goals. This article reports on the investigation into the matter and first attempts to identify the various problems that could threaten the survival of independent financial advisers in their business life cycle, followed by the potential solutions that can be implemented to counter those obstacles. Resulting from the investigation a theoretical framework was developed, suggesting key areas they would need to focus on in their business life cycle to conquer the challenges they might encounter and survive. Following the recommendations, a number of hypotheses are also formulated to set the direction for a follow-on empirical study that could provide further guidance to independent financial advisers regarding the survival and growth of their small businesses.

2 PURPOSE

The purpose of this article is to provide a theoretical perspective on the various problems that could threaten the survival of independent financial advisers in their business life cycle as well as potential solutions that can be implemented to counter those obstacles. The theory presented in this paper serves as background to determine a framework of key areas independent financial advisers would need to focus on in their business life cycle to conquer the challenges they might encounter and survive. A follow-on empirical study could investigate the various hypotheses, formulated from the findings of this study, in more depth in order to provide further guidance to independent financial advisers regarding the survival and growth of their small businesses.

3 METHODOLOGY

Secondary sources, such as academic textbooks, research studies previously conducted on the subject matter, internet websites and scientific journals, were consulted to gain more insight into the research topic and to conduct the literature review of this study.

4 LITERATURE REVIEW

To achieve the objectives of this article, this section first deals with a general business life cycle model that could be representative of the businesses of independent financial advisers. The second part of the literature review is devoted to gain more insight into the various problems that independent financial advisers could possibly experience in their business life cycle, as well as potential solutions that can be implemented to counter those obstacles. The results from this investigation were then used as the foundation to develop the framework of key areas independent financial advisers would need to focus on in their business life cycle to conquer the challenges they might encounter and survive.

4.1 GENERAL BUSINESS LIFE CYCLE MODEL

Levie and Lichtenstein (2010:2) in their investigation of 104 organisational life cycle models came to the conclusion that the growth stages of a small business was actively researched from the period 1962 to 2006. The authors of this article were also not able to find any significant contributions made to the organisational life cycle theory after the year 2008.

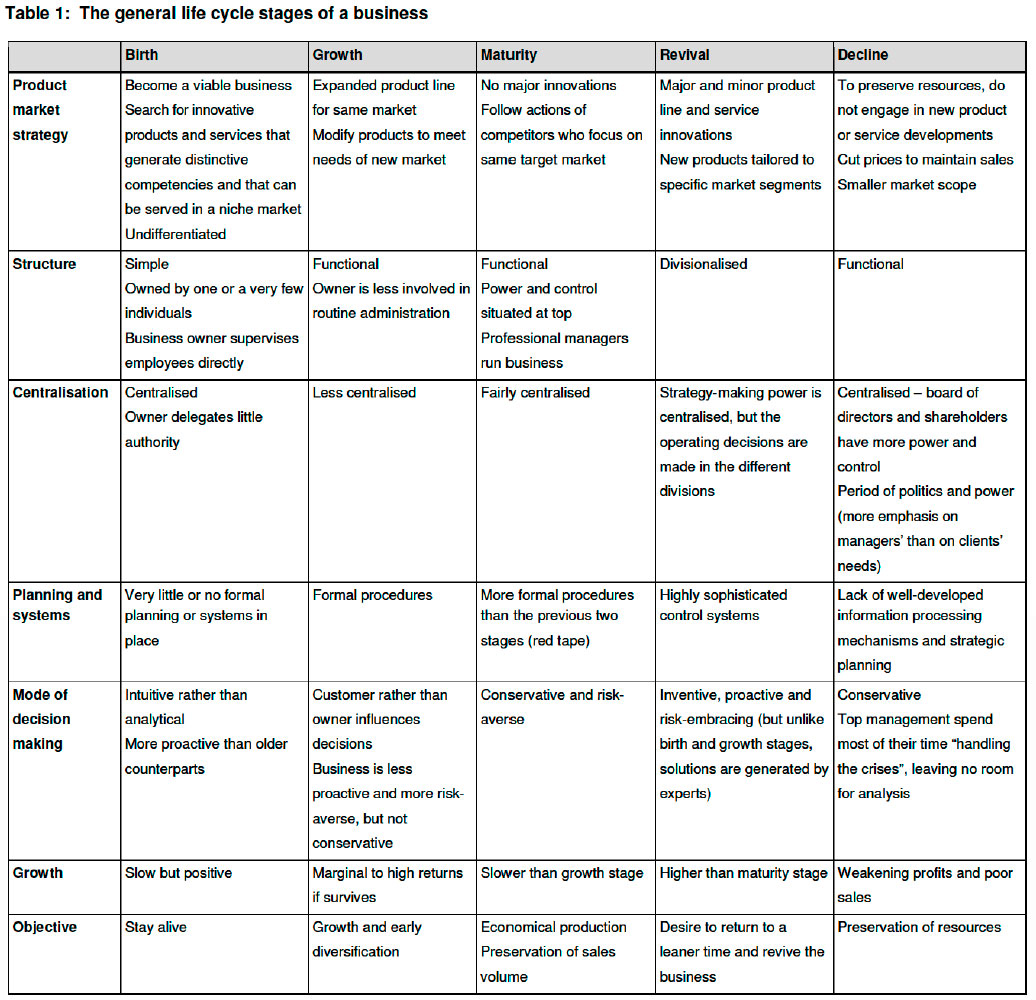

Subsequently, in the search for a justifiable general business life cycle model that could be representative of the businesses of independent financial advisers, it was decided to narrow the focus and only compare the life cycle models proposed by Churchill and Lewis (1983:Internet); Ferreira (2000:Internet); Lester and Parnell (2008:Internet); Miller and Friesen (1984:1161) and Smith, Mitchell and Summer (1985:Internet). Some of these models are dated, but were selected firstly because their contribution to the literature theory is still acknowledged today (Hill, Nancarrow & Wright 2002:362-363; Lester & Parnell 2008:540-553; Lester, Parnell & Carraher 2003:339-353) and secondly because the researcher wanted to ensure that there was a substantial review of all the major contributions to the business life cycle concept. The models proposed by Miller and Friesen (1984) and by Smith et al. (1985) are based on previous business life cycle models, while those proposed by Lester and Parnell (2008:Internet) and by Ferreira (2000:Internet) represent more recent research studies. Finally, in addition to representing small, large and general business life cycle models, all five models have been empirically tested. The results of the investigation are depicted in Table 1. Based on the comparison, it appears that businesses can progress through five general life cycle stages.

The next question requiring further investigation is whether businesses relentlessly progress in a sequential manner through these five general life cycle stages.

4.2 THE SEQUENTIAL NATURE OF BUSINESS LIFE CYCLE STAGES

Over the past few decades a number of views have been voiced regarding the sequential nature of business life cycle stages. According to Quinn and Cameron (1983:33), business life cycle stages are "sequential in nature, occur as a hierarchical progression that is not easily reversed, and involve a broad range of organizational activities and structures". Other researchers argue that the progression of a business from one life cycle stage to another is a matter of strategic choice, expertise and resources. Not all small businesses want (Scott & Bruce 1987:45) or have the resources and expertise to grow their businesses (Bessant, Phelps & Adams 2005; McMahon 1998; Van Scheers 2011:5050).

It is, however, in the research study conducted by Miller and Friesen (1984:11751177) that clarity about this matter can be gained. Their findings reveal that some businesses do display a long-term evolutionary pattern that is roughly in line with the life cycle literature. These businesses progress from birth, to growth, to maturity and then to revival in a sequential manner. However, there are many exceptions. Some of the businesses in the revival stage revert to the maturity phase. (An unsuccessful attempt to diversify the business is given as a possible reason.) Furthermore, there are businesses in the decline stage that progress to the maturity and revival stages. Miller and Friesen (1984:1177) conclude that "while the stages of the life cycle are internally coherent and very different from one another they are by no means connected to each other in any deterministic sequence". The maturity stage could, for example, be followed by the decline, revival or even growth stage; the growth stage could be followed by the maturity or the decline stage; the revival stage may be before or after the decline stage, and so on. There is no common corporate life cycle, but there are indeed life cycle stages common to every business which are different from one another. It therefore appears that, while there are general life cycle stages common to businesses, businesses do not progress relentlessly through them in a sequential manner.

The development of the business can assume any form. According to the contributions by Bessant et al. (2005:lnternet); Churchill and Lewis (1983:lnternet); McMahon (1998:lnternet); Mount, Zingerand Forsyth (1993:111); Scott and Bruce (1987:45) and Siu and Kirby (1998:49-50), it seems that the business's resources, as well as its expertise and strategic choices play an important role in determining, at any point, whether it will progress to the next stage, remain at the current stage or deteriorate and perhaps die.

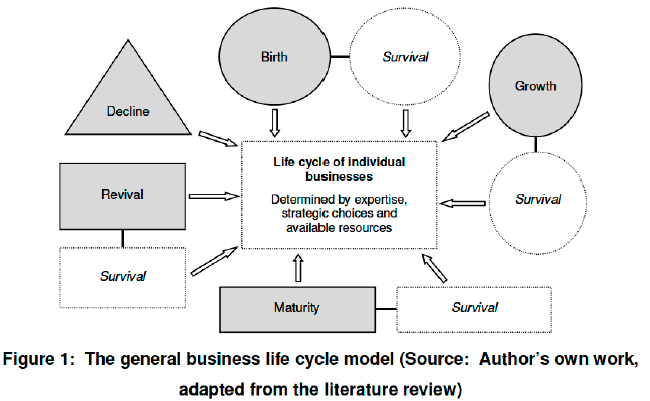

Finally, it appears that businesses that stop growing at a specific stage seem to keep the structure of that particular stage. According to Miller and Friesen (1984:1177), "the structures of no-growth firms may become arrested at the life-cycle stage in which strategy and size become fixed. Firms may then be similar to others within their stage but fail to progress to a different phase of the life cycle". Although one of the older research studies conducted, the findings of Miller and Friesen (1984:1177) can still be regarded as valuable today. They made use of a longitudinal research approach and were therefore able to conduct a very thorough and comprehensive investigation into the subject matter. Subsequently, based on the findings of the literature discussion, it is proposed in this article that the general life cycle model of a business could be graphically outlined as shown in Figure 1.

The five general life cycle stages identified in this section are depicted in grey. As each life cycle stage has its own unique characteristics, different shapes were used to illustrate them. Each shape has a duplicate form, representing the businesses which have the characteristics of that particular stage, but which stop developing, and simply remain in a state of survival. Since the decline stage represents businesses in demise, a duplicate survival form was not created for this stage.

Arrows point from each shape to the centre of the diagram, which represents the life cycle of the individual business. At birth, the business has a "clean slate". As the business develops, its "slate" is filled with a "chain" of general life cycle stages. This chain is unique to the business and is based on the business's expertise, available resources and the strategic choices it makes. The chain of general life cycle stages will eventually stop when the business dies.

4.3 POTENTIAL BUSINESS OBSTACLES AND COUNTERSTRATEGIES

Over the years a number of studies have been conducted to determine the obstacles businesses are confronted with. Arinaitwe (2006:Internet), for example, believes that the small business owners' technological capabilities or lack thereof is one of the main reasons why they still continue facing growth challenges - despite the support provided by the government and other organisations. Without technological capabilities, small business owners find it difficult to compete and grow their businesses. Hill et al. (2002:366), in another study conducted among small business owners in Britain and the USA, discovered that the typical problems that can be experienced by these owners include location, changing client needs, lack of finance, rapid early growth, poor general management skills, declining sales, competition, service, price and a changing market environment.

Based on a research study of small business owners in Gauteng (South Africa), Brink, Cant and Lightelm (2003:Internet) claim that the success of the businesses is influenced by macro environmental variables, marketing related issues, management skills, management actions, social problems, human resource problems and financial problems. Timmons and Spinelli (2007:260-261, 536-538) have identified a further set of business obstacles and postulate that while there are a great variety of problems which a business might have to concentrate on, the problems they highlight are particularly critical for the business and, if not overcome, can seriously imperil the business. Accordingly, this article focuses mainly on the potential problems highlighted by Timmons and Spinelli (2007:260-261, 536-538). If independent financial advisers were found to experience these problems in their businesses, it would be vital to identify appropriate solutions to them.

However, since Timmons and Spinelli (2007:260-261, 536-538) were unable to plot the problems they identified against empirically tested business life cycle stages, this article can merely approach their problems as obstacles independent financial advisers could potentially experience during the course of their business life cycle. A further empirical research study would then need to be conducted in future to group the problems actually experienced by the advisers into the general business life cycle stages as identified in this study (which were derived from five life cycle models that had all previously been empirically tested).

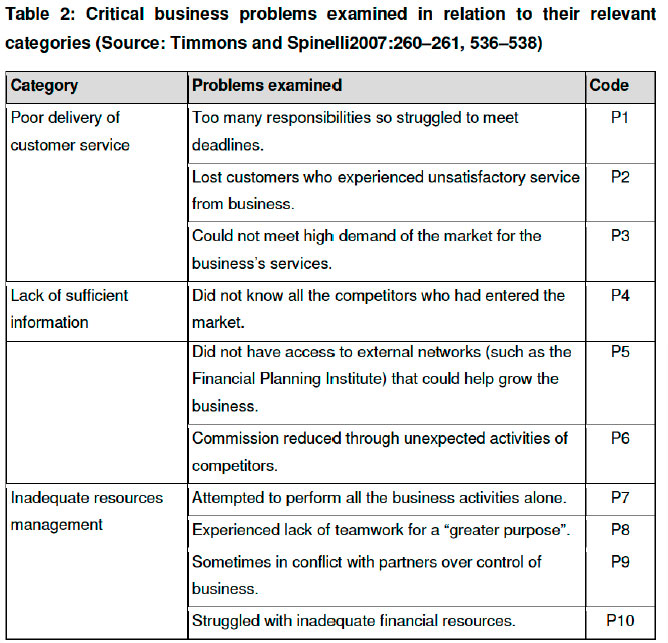

Finally, from a holistic perspective, it is possible to categorise the problems mentioned by Timmons and Spinelli (2007:260-261, 536-538) into three main categories, namely poor delivery of customer service, lack of sufficient information and inadequate resources management (refer to Table 2). The discussion of Timmons and Spinelli's problems and potential solutions in the remaining part of the literature investigation will subsequently be structured around these three areas.

4.3.1 Poor delivery of customer service

Business owners might struggle to meet deadlines due to the fact that they have too many responsibilities (P1). In the business context of an independent financial adviser, this statement could, for example, refer to a situation where they are unable to meet a client and discuss their financial strategy as arranged with them, due to the fact that they have too many errands they need to run. This problem could potentially be overcome by recruiting four types of employees as indicated by Jordaan and Prinsloo (2001:168), namely back office personnel, receptionist, sales personnel and personnel involved in the research and development of the marketing strategy that could assist the business owner to meet the deadlines required. Independent financial advisers would also need to ensure that these employees were remunerated sufficiently, as Jordaan and Prinsloo (2001:171) warn that employees who are not happy with their remuneration could cost the business more than the wages they are being paid through client loss.

Business owners could also experience a loss in customers who experienced unsatisfactory service from the business (P2). Motivating employees appropriately to deliver a positive service encounter might be a possible solution small business owners could implement to address this problem. An employee's level of motivation when interacting with clients will greatly influence the outcome of the service encounter. In a study conducted by Hennig-Thurau (2004:lnternet) among 989 students in Germany, it was discovered that the service employees' motivation to serve the clients in a customer-oriented manner as well as their social and technical skills impacted on the clients' satisfaction, emotional commitment and, as a result, the economic success of the business.

Various measures can be implemented to enhance the level of motivation of the employees. Baker (2003:369) as well as Nandanwar, Surnis and Nandanwar (2010:6), however, cautions that the employees' age should be taken into consideration when evaluating a motivational scheme, since different features will motivate the employees at a specific age. Older employees with larger families, for example, might prefer financial rewards, while younger, better educated employees with no families could prefer higher order rewards, such as recognition, respect and a sense of accomplishment.

Business owners may struggle to meet the high demand of the market for their business's services (P3). In the business context of an independent financial adviser, this problem could refer to a situation where the adviser is unable to meet all the clients who contacted the business and assist them with their financial planning. Jordaan and Prinsloo (2001:222-224) believe that a solution to the imbalances between supply and demand is presented through the distribution function of service businesses. Employees can be cross-trained to perform different job functions at peak periods. In the world of the financial adviser, this approach would, for example, mean that when the demand for the service is high, the secretary could assist in preparing quotations and completing application forms. This could then free the financial adviser's time to see more clients and sell policies to them.

4.3.2 Lack of sufficient information

The first problem listed under this category entails not knowing all the competitors who have entered the market (P4). Independent financial advisers might not, for example, be aware of all the other financial advisers that are also targeting their specific market segment. A potential solution to this problem could be to apply quality control in the service process to create a favourable impression among clients, thus convincing them to rather make use of the adviser's services. According to Zeithaml, Bitner and Gremler (2009:25), clients judge the service provided based on the business's service process. "[I]f an organization can deliver a high quality of service, its customers will receive better value and are more likely to be satisfied" (Ennew & Waite 2007:326). Research studies have proven this scenario to be true (Cronin & Taylor 1992:Internet; Zeithaml, Berry & Parasuraman 1996:Internet).

Mazzarol (2004:Internet) conducted a study of small businesses in the UK and Australia to investigate the connection between their operational practices and the high sales growth they achieved. The results revealed that the relationships these small businesses had built with their clients, employees, suppliers and support networks were a critical factor in their success. Consequently, a lack of external networks (where information could be shared) to continue business growth has been listed in Table 2 as another potential problem that independent financial advisers could experience in their businesses (P5). Following the network activities and resulting benefits discussed above, however, it appears that independent financial advisers would have to focus on building good relationships with their employees, suppliers (such as insurance companies) and support networks (i.e. the Financial Planning Institute) to address the problem and to grow their businesses.

Small business owners could also experience the problem of a reduction in commission (sales) through the unexpected activities of their competitors (i.e. other financial advisers) (P6). To address this problem, independent financial advisers could potentially make use of the strategies recommended by Lovelock (1996:472) and Timmons and Spinelli (2007:139-141) to improve their competitive intelligence. These strategies include investigating published resources such as formal business information guides, the Internet, journal articles, market studies and client expenditures; other resources including trade associations, employees and consulting firms; networking and conducting competitive market surveys to compare the business relative to its competitors.

4.3.3 Inadequate resources management

Business owners could attempt to perform all their business activities alone and not rely on their employees for assistance (P7). This approach, however, would not be feasible for advisers wishing to grow their businesses. Timmons and Spinelli (2007:261-262) recommend that these type of small business owners refrain from following an autocratic management style to manage employees who strive for achievement, responsibility and results. A more correct approach would be to focus on close collaboration with employees and entrusting power and control to them.

Independent financial advisers, however, might in their attempts to work closely with their employees experience a lack of teamwork for a "greater purpose" (P8). According to Zeithaml et al. (2009:369), a potential solution to this problem would be to ensure that every employee is aware of the essential role they play in the final delivery of quality service. This will promote teamwork and enable the employees to deliver excellent service.

Another potential problem that might occur involves being in conflict with partners over control of the business (P9). Timmons and Spinelli (2007:267) suggest that proficient business managers follow a distinct conflict management approach. Characteristics of creativity are normally displayed, consensus is generated and information is shared. In addition, they also facilitate discussion regarding problems, do not become defensive when others disagree with their views and rather blend ideas. Timmons and Spinelli (2007:267) conclude that the benefits proficient business owners gain from following this approach include motivation, commitment and teamwork. In addition, new disagreements do not restrain business growth, since there is both high clarity and broad acceptance of the overall goals and underlying priorities.

The conflict management description illustrated by Timmons and Spinelli (2007:267), which can assist businesses in benefiting from unrestricted business growth, therefore presents a possible solution that independent financial advisers could implement to address the problem of conflict between partners over business control. The final potential problem listed in Table 2 which businesses could encounter entails experiencing difficulties with inadequate financial resources (P10). Cunningham and Hornby (1993:Internet) present a potential solution to this problem. In a survey which investigated 12 small business case studies in the UK, it was found that these small business owners attempted, by operating from a low-cost venue such as their houses, to keep their overhead expenses as low as possible. The rationale was that if the business overheads were kept low, the business would be able to establish competitive pricing strategies independently of business overheads. Other businesses have also implemented this strategy successfully in more recent years (Read 2004:227). In the business context of an independent financial adviser, reduced overhead expenses would enable them to charge lower commission and consequently make their services more attractive to clients.

5. FINDINGS

Following the literature discussion, it is possible to make the following observations:

5.1 OBSERVATIONS

Firstly, Table 2 highlighted a total of ten problems that could potentially occur during the course of the independent financial adviser's business life cycle. Of the ten potential solutions proposed in section 4.3 (one strategy for each problem), five of the solutions are based primarily on employee-driven factors. It therefore appears that independent financial advisers would need to pay special attention to their employment practices in order to overcome the challenges they are confronted with and survive. They would need to appoint more employees in the capacity of back office personnel, personnel involved in the research and development of the marketing strategy, receptionists and sales personnel that can efficiently assist them with the execution of all the business's responsibilities.

They would also need to ensure that the employees are aware of the role they would need to perform in the business and cross-train them to assist with other functions in the business during periods of high demand and to prevent customers from turning to competitors because of poor customer service. To truly benefit from these training initiatives, however, independent financial advisers would need to be prepared to entrust power and control to their employees and ensure that they are remunerated appropriately.

Independent financial advisers, however, should not invest all their time and resources only in their employment practices. Based on the remaining five potential solutions proposed in section 4.3, it is suggested that independent financial advisers would also need to pay attention to ensuring the quality of the services provided, focusing on building good networking relationships, sourcing competitor information, managing conflict with partners and operating a home-based office to save on overhead expenses and survive. Consequently, given the observations made in this section it is now possible to propose the theoretical framework of this study and to suggest key areas independent financial advisers would need to focus on in their business life cycle to conquer the challenges they might encounter and survive.

5.2 THEORETICAL FRAMEWORK

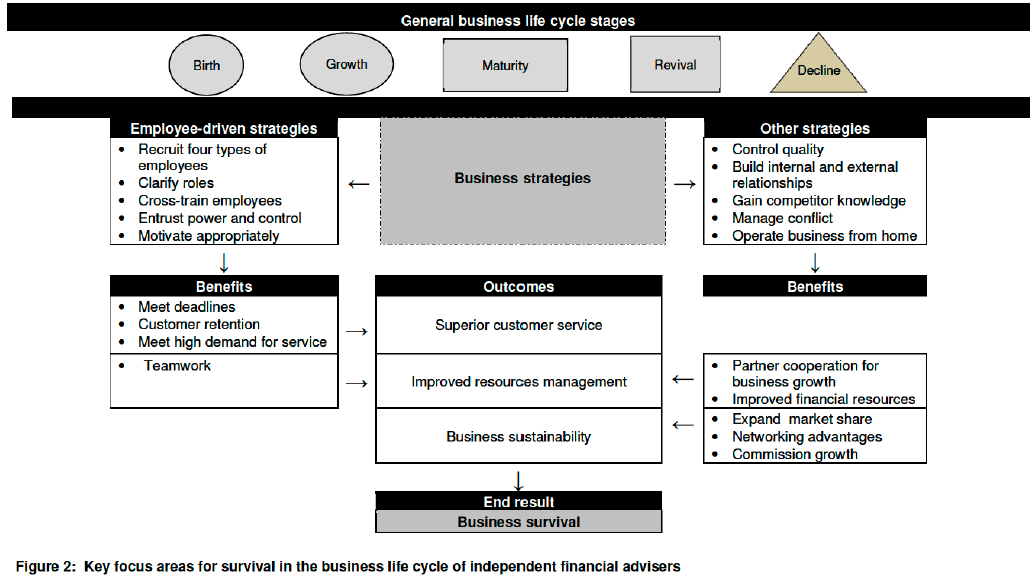

The theoretical framework proposed in this study is outlined in Figure 2.

5.2.1 General business life cycle stages

In section 4.1 it was pointed out that a business can progress through five general life cycle stages, namely birth, growth, maturity, revival and decline. It was also highlighted that not all businesses progress in a sequential manner through these stages. In fact, at birth, the business has a "clean slate". As the business develops, its "slate" is filled with a "chain" of general life cycle stages. This chain is unique to the business and is based on the business's expertise, available resources and the strategic choices it makes. The chain of general life cycle stages will eventually stop when the business dies.

Consequently, the five figures at the top of the diagram represent the five general life cycle stages through which the business of an independent financial adviser may progress. Within these stages, independent financial advisers should then make a number of strategic choices to survive and grow; hence the arrow pointing at the bottom of the figures towards the business strategies.

5.2.2 Business strategies, benefits and outcomes

The business strategies depicted in Figure 2 represent the potential solutions as identified in the literature section. There are two focus areas:

• Employee-driven strategies

Independent financial advisers would need to focus on appointing the right types of employees, providing sufficient training, motivating them appropriately and entrusting power and control to them. These employment practices would then assist the financial adviser in obtaining the benefits of meeting deadlines, meeting the high demand for the business's service through effective teamwork and retaining more customers. Ultimately, the outcome of these benefits would lead to the business having the reputation as being able to manage resources effectively and providing superior customer service, which would then attract more clients to the business and assist the adviser in generating more commission.

• Other strategies

Independent financial advisers would also need to pay attention to the other strategies listed on the right of the diagram. These strategies can further assist in generating favourable benefits for them. Partners who are able to cooperate and manage conflict would be able to manage the business for growth more effectively. Operating from a home-based office would further assist the financial adviser in managing the resources more effectively, by saving on overhead expenses and managing for business growth.

Market share can be expanded by controlling the quality of the service provided, as clients might prefer an adviser who provides quality service. Effective networking strategies would help the financial adviser to benefit from the knowledge and resources of other strategic partners. Independent financial advisers would also be able to generate more commission growth should they become more aware of the activities of their competitors and defeat them. Ultimately, the outcome of these benefits could be business sustainability. A more efficient business operation, together with a growing market share and commission base, would assist the financial adviser in continuing business operations.

• End result

In the end, the effective implementation of the various potential strategies recommended in this article could assist financial advisers to address the various challenges they are confronted with, become more successful and survive in the long term.

6 TOWARDS A RESEARCH AGENDA

This study identified potential problems posing a threat to the businesses of independent financial advisers in their business life cycle as well as possible strategies that can be implemented to counter those obstacles.

However, these problems and solutions have not been tested empirically among the businesses of independent financial advisers and still require further investigation. Consequently, the first two hypotheses that can be formulated and investigated further in a future empirical study are as follows:

Hypothesis 1: Independent financial advisers experience the ten potential critical problems in their businesses listed in Table 2.

Hypothesis 2: Independent financial advisers make use of the potential solutions to address the various problems discussed in section 4.3.

There is a further possibility that the problems outlined in Table 2 are not really critical to the survival of independent financial advisers and that there might be other problems that are more important and that should rather receive the attention of the financial adviser. Consequently, the third hypothesis that can be formulated and investigated further in a future empirical study is:

Hypothesis 3: There is still a range of unknown critical problems that could specifically threaten the business survival of independent financial advisers.

From the conceptual framework proposed in this study it became clear that independent financial advisers would need to pay more attention to their employment practices if they were to overcome the problems most experienced in their businesses and survive. This approach would initially be very expensive to execute and it is suggested that independent financial advisers currently operating on a small scale consider appointing only one or two additional employees as a start to help them perform the various functions of the business and meet the deadlines.

The question that still remains then is whether this strategy would be sustainable and assist the financial adviser's business to survive in the longer term. Consequently, the fourth hypothesis that can be formulated from the results and that should be investigated further in a future research study is:

Hypothesis 4: Independent financial advisers will fail in the long term if they do not pay sufficient attention to their employment practices.

The theoretical framework proposed also suggests that independent financial advisers not only pay attention to employee-driven strategies, but also focus on other important aspects of the business. However, given the fact that five potential problems could be solved by only focusing on employee-driven strategies, it might be necessary for a future research study to perhaps also investigate whether it is more important for the financial adviser to manage the employees of the business than focus on any other aspect of the business. Consequently, the fifth hypothesis can be formulated as follows:

Hypothesis 5: It is more important for the financial adviser to manage the employees of the business than focus on any other aspect of the business.

Finally, the general life cycle stages proposed in this article require further investigation to determine whether they are in fact applicable specifically to the businesses of independent financial advisers. Consequently, the last hypothesis can be formulated as follows:

Hypothesis 6: Independent financial advisers do progress through the five general life cycle stages as identified in this study.

7 CONCLUSIONS

For independent financial advisers to survive and grow in their competitive and complex business environment, they require more insight into the problems posing a threat to their businesses in their business life cycle as well as the strategies that can be implemented to counter those obstacles. This study expanded the body of knowledge and, based on a comprehensive literature investigation, a theoretical framework was developed, suggesting key areas independent financial advisers would need to focus on in their business life cycle to conquer the challenges they might encounter and survive.

Resulting from the recommendations, a number of hypotheses were also formulated to set the direction for future research regarding the survival and growth of independent financial advisers in South Africa. It is hoped that these hypotheses will stimulate further research on this very important topic and would lead to the provision of additional guidance to independent financial advisers to survive and grow their businesses in the long term.

REFERENCES

ANON. 2004. Bill to regulate financial salesmen. Star, 25 March:5. [ Links ]

ARINAITWE SK. 2006. Factors constraining the growth and survival of small scale businesses. A developing country analysis. Journal of American Academy of Business, Cambridge, 8(2):167-179. [Internet: http://proquest.umi.com/login; downloaded on 2006-12-23. [ Links ]]

BAKER MJ. 2003. The marketing book. Oxford: Butterworth-Heinemann. [ Links ]

BESSANT J, PHELPS B & ADAMS R. 2005. A review of the literature addressing the role of external knowledge and expertise at key stages of business growth and development. [Internet: https://aerade.cranfield.ac.uk/bitstream/1826/1036/1/Bessant-Phelps-Adams-Rev+of+Lit+Business+Growth+and+Development-Final+Report; downloaded on 2008-01-27. [ Links ]]

BOTHA M, GEACH B, GOODALL B & ROSSINI L. 2003. The South African financial planning handbook. Pietermaritzburg: LexisNexis. [ Links ]

BRINK A, CANT M & LIGHTELM A. 2003. Problems experienced by small businesses in South Africa. [Internet: http://74.125.77.132/search?q=cache:4_MBIr8j9UEJ:www.cric.com.au/seaanz/resources/NewdocCant.pdf+Problems+experienced+by+small+businesses+in+South+Africa&hl=af&ct=clnk&cd=1&gl=za&lr=lang_en; downloaded on 2008-11-15. [ Links ]]

CHURCHILL N & LEWIS V. 1983. The five stages of small business growth. Harvard Business Review, 61(3):30-50. [Internet: http://search.global.epnet.com; downloaded on 200809-01. [ Links ]]

CRONIN JJ & TAYLOR SA. 1992. Measuring service quality: a reexamination and extension. Journal of Marketing, 56:55-69. [Internet: http://www.emeraldinsight.com; downloaded on 2008-12-31. [ Links ]]

CUNNINGHAM D & HORNBY W. 1993. Pricing decision in small firms: theory and practice. Management Decision, 31(7):46-56. [Internet: http://proquest.umi.com/login; downloaded on 2006-05-13. [ Links ]]

ENNEW CT & WAITE N. 2007. Financial services marketing. London: Elsevier. [ Links ]

FERREIRA JJ. 2000. Development and study of a taxonomy of stage configurations of the life cycle, applied to the SME of the Beira interior region. [Internet: http://74.125.77.132/search?q=cache:A_u0_MUsNGYJ:sbaer.uca.edu/research/icsb/2000/pdf/081.PDF+Development+and+study+of+a+taxonomy+of+stage+configurations+of+the+life+cycle,+applied+to+the+SME+of+the+Beira+interior+region&hl=af&ct=clnk&cd=1&gl=za&lr=lang_en; downloaded on 2008-08-26. [ Links ]]

HANKS SH, WATSON CJ, JANSEN E & CHANDLER GN. 1993. Tightening the life-cycle construct: a taxonomic study of growth stage configurations in high-technology organisations. Entrepreneurship: Theory & Practice, 18(2):5-9. [Internet: http://search.global.epnet.com; downloaded on 2007-04-28. [ Links ]]

HENNIG-THURAU T. 2004. Customer orientation of service employees. International Journal of Service Industry Management, 15(5):460-479. [Internet: http://www.ingentaconnect.com; downloaded on 2006-05-01. [ Links ]]

HILL J, NANCARROW C & WRIGHT LT. 2002. Lifecycles and crisis points in SMEs: a case approach. Marketing Intelligence & Planning, 20(6):361-369. [Internet: http://www.emeraldinsight.com; downloaded on 2006-06-01. [ Links ]]

INSETA. 2011. FSB regulatory examination preparation. [Internet: http://www.brcs.co.za/wp-content/uploads/2011/04/Section-1-1 st-level-Reg-Exam-FSPs-Sole-Proprietors-Key-Individuals-Cat-I-II-III-IV; downloaded on 2011 -11-04. [ Links ]]

JORDAAN Y & PRINSLOO M. 2001. Grasping service marketing. Pretoria: Grapevine News. [ Links ]

KRUGER P. 2004. The effect of regulation. Richer Life, August:43. [ Links ]

LESTER DL & PARNELL JA. 2008. Firm size and environmental scanning pursuits across organizational life cycle stages. Journal of Small Business and Enterprise Development, 15(3):540-554. [Internet: http://emeraldinsight.com; downloaded on 2008-09-15. [ Links ]]

LESTER DL, PARNELL JA & CARRAHER S. 2003. Organizational life cycle: a five-stage empirical scale. International Journal of Organizational Analysis, 11 (4):339-354. [ Links ]

LEVIE JD & LICHTENSTEIN BB. 2010. A terminal assessment of stages theory: introducing a dynamic states approach to entrepreneurship. Entrepreneurship theory and practice, 34(2): 317-350. [ Links ]

LOVELOCK CH. 1996. Services marketing. Upper Saddle River, NJ: Prentice Hall. [ Links ]

MAZZAROL T. 2004. Partnerships: a key to growth in small business. [Internet: http://www.sbaer.uca.edu/research/icsb/1998/pdf/136.pdf; downloaded on 2006-04-30. [ Links ]]

MCKELVIE A & WIKLUND J. 2010. Advancing firm growth research: A focus on growth mode instead of growth rate. [Internet: http://onlinelibrary.wiley.com/doi/10.1111/j.15406520.2010.00375.x/full; downloaded on 2011-11 -05. [ Links ]]

MCMAHON RGP. 1998. Stage models of SME growth reconsidered. [Internet: http://commerce.flinders.edu.au/researchpapers/98-5.htm; downloaded on 2005-10-22. [ Links ]]

MILLER D & FRIESEN PH. 1984. A longitudinal study of the corporate life cycle. Management Science, 30(10):1161-1183. [ Links ]

MONEYMARKETING. 2006. Financial adviser directory. Randburg: Primedia. [ Links ]

MOUNT J, ZINGER JT & FORSYTH GR. 1993. Organizing for development in the small business. Long Range Planning, 26(5):111-120. [ Links ]

NANDANWAR MV, SURNIS SV & NANDANWAR LM. 2010. Intervening factors affecting the relationship between incentives and employee motivation: a case study of pharmaceutical manufacturing organisation in Navi Mumbai. Journal of Business Excellence, 1 (2):6-11. [ Links ]

OLAWALE F & GARWE D. 2010. Obstacles to the growth of new SMEs in South Africa: a principal component analysis approach. African Journal of Business Management, 4(5):729-738. [ Links ]

QUINN R & CAMERON K. 1983. Organisational life cycles and shifting criteria of effectiveness: some preliminary evidence. Management Science, 29:33-41. [ Links ]

READ BB. 2004. Home workplace: a handbook for employees and managers. Okanogan: CMP Books. [ Links ]

SCOTT M & BRUCE R. 1987. Five stages of growth in small business. Long Range Planning, 20(3):45-52. [ Links ]

SHA S. 2006. An investigation into problems facing small-to-medium sized enterprises in achieving growth in the Eastern Cape: enhancing the strategy for developing small 'growth potential' firms in the Eastern Cape. [Internet: http://eprints.ru.ac.za/archive/00000288; downloaded on 2008-07-09. [ Links ]]

SIU W & KIRBY DA. 1998. Approaches to small firm marketing. A critique. European Journal of Marketing, 32(1/2):40-60. [ Links ]

SMITH KG, MITCHELL TR & SUMMER CE. 1985. Top level management priorities in different stages of the organizational life cycle. Academy of Management Journal, 28(4): 799-819. [Internet: http://proquest.umi.com/login; downloaded on 2008-09-15. [ Links ]]

SWANEPOEL A. 2004. Comply like a pro! Johannesburg: Creda Communications. [ Links ]

TIMMONS JA & SPINELLI S. 2007. New venture creation. Entrepreneurship for the 21st century. Singapore: Irwin/McGraw-Hill. [ Links ]

UK ASSOCIATION OF INDEPENDENT FINANCIAL ADVISERS. 2001. Response by the UK Association of Independent Financial Advisers to the commission document on European governance. [Internet: http://ec.europa.eu/governance/contrib_ukifa_en; downloaded on 2006-10-04. [ Links ]]

UNIVERSITY OF THE FREE STATE. 2004. Study guide for post graduate diploma in financial planning 711: the financial planning environment. Bloemfontein: Faculty of Law. [ Links ]

VAN SCHEERS L. 2011. SMEs' marketing skills challenges in South Africa. African Journal of Business Management, 5(13):5048-5056. [Internet: http://www.academicjournals.org/AJBM; downloaded on 2011-11-04. [ Links ]]

WRIGHT SA. 2008. What is an independent financial adviser? [Internet: http://www.discoveryarticles.com/articles/127563/1/What-is-an-Independent-Financial-Adviser/Page1.html; downloaded on 2008-09-14. [ Links ]]

ZEITHAML VA, BERRY LL & PARASURAMAN A. 1996. The behavioural consequences of service quality. Journal of Marketing, 60:31-47. [Internet: http://search.global.epnet.com; downloaded on 2009-01-14. [ Links ]]

ZEITHAML VA, BITNER MJ & GREMLER DD. 2009. Services marketing. Integrating customer focus across the firm. Singapore: McGraw-Hill. [ Links ]

{kind=link}

{kind=link}

{kind=link}

{kind=link}