Serviços Personalizados

Artigo

Inglês (pdf)

Inglês (pdf)

Artigo em XML

Artigo em XML Referências do artigo

Referências do artigo

Indicadores

Links relacionados

-

Citado por Google

Citado por Google -

Similares em Google

Similares em Google

Compartilhar

Permalink

PermalinkJournal of Contemporary Management

versão On-line ISSN 1815-7440

JCMAN vol.8 no.1 Meyerton 2011

RESEARCH ARTICLES

South African automotive industry: trends and challenges in the supply chain

IM AmbeI; JA Badenhorst-WeissII

IDepartment of Business Management, UNISA

IIDepartment of Business Management, UNISA

ABSTRACT

The automotive industry is an important industry in the South African economy. The industry contributes extensively to the country's gross domestic product and employment. It has embraced technology and management practices that have transformed the manufacturing environment using cutting edge design and visualisation tools. However, all is not as rosy as painted: the industry has fragilities and faces new and emerging challenges.

The purpose of this article is to explore the South African automotive industry to determine the trends and challenges in the supply chain. The article, based on a theoretical analytical approach, reveals that the industry still has a long way to becoming a significant global player. The article concludes by mapping the challenges in the supply chain and suggests that the industry needs to fight to remain locally viable and internationally competitive, and should adopt a supply chain strategy that would be responsive to customer demands and expectations.

Key phrases: Automotive industry, Trends, Challenges, Supply chain management

1 INTRODUCTION

One of the important contributors to the South African economy is the automotive industry (Kaggwa 2008:3). The industry contributed 5.9% to the country's gross domestic product (GDP) and created 30 100 jobs in 2009 (Lamprecht 2010:130; NAAMSA 2011:2). The South African automotive industry was integrated into the global market in 1995, and has seen an increase in foreign ownership since then (Damoense & Simon 2004:252). The industry is stimulated by the Motor Industry Development Programme (MIDP). However, this policy will be replaced in 2013 by the Automotive Production and Development Programme (APDP) in order to negate the costs of importing components using long supply chains and weathering a fluctuating currency (Mphahlwa 2008:2).

The South African automotive industry adversely felt the effect of the global recession (Van der Merwe 2009:1). The industry experienced a reduction in operation, and many employees were retrenched across different original equipment manufacturer (OEMs) (Naude & Badenhorst-Weiss 2011:71). The industry faced shrinking demand and margins, while the resources available to address these developments also shrunk (Swiecki & Gert 2008:2). These situations led to a major decline in global unit production and new car registrations and a subsequent decline in GDP of 0.5% in 2009 and 2 571 job losses in 2009 (Deutsche Bank Research 2009 2). Naude and Badenhorst-Weiss (2011:96) assert that the South African automotive industry is not competitive due to its low percentage (an average of 35%) of local content in the final product (30% to 40% more expensive manufacturing than China and India).

Supply chain management (SCM) is one of the important functional areas in the automotive industry and its contribution has been particularly noteworthy (Pires & Neto 2008:328). In the automotive industry, most OEMs create 30% to 35% of value internally and delegate the rest to their suppliers (Afsharipour, Afshari & Sahaf 2006:5). As a result of intensified competition in the global market, the introduction of products with shorter lifecycles and growing customer service, automotive manufacturers have been forced to invest in and direct their attention to the supply chains (Naude & Badenhorst-Weiss 2011:70; Simchi-Levi, Kaminsky & Simchi-Levi 2009:1). However, SCM poses critical challenges for South African automotive manufacturers. Some of the challenges include the desire towards greater product differentiation, cost reduction and service improvement (Supplychainforesight 2007:9); global recession (KPMG 2009:24); structural changes in the automotive industry; low levels of collaboration (Mphahlwa 2008:2) and stiff competition among manufacturers (Lamprecht, 2010:159). The industry is challenged to maintain its place in the market (Tang & Qian 2008:288). Hence, understanding the trends and challenges of the supply chain is not only paramount for SCM practitioners but also for South Africa as a whole.

The purpose of the article therefore is to report on the trends and challenges of SCM in the South African automotive industry. The authors contend that the South African automotive industry has fragilities and faces significant challenges in the supply chain. Therefore, an appropriate supply chain strategy is required to take the industry to a new level. The article makes two possible important contributions to knowledge. Firstly, it explores the South African automotive industry, revealing the trends of automotive production and sales performance. Secondly, it reveals the challenges in the supply chain. These challenges need to be addressed for the industry to become a significant global player. The article concludes by mapping the challenges of the supply chain in the South African automotive industry.

The remaining section of the article present an overview of the global automotive industry, the South African automotive industry, SCM practices in the automotive industry and a related review of the challenges of the supply chain in the industry.

2 THE GLOBAL AUTOMOTIVE INDUSTRY

This section of the article presents an overview of the global automotive industry and its major components.

2.1 OVERVIEW OF THE GLOBAL AUTOMOTIVE INDUSTRY

The automotive industry is one of the most global of all industries, with its products spread around the world dominated by small companies enjoying worldwide recognition (Barnes & Morris 2008:32). The industry comprises the largest manufacturing sector in the world, with an output equivalent to that of the world's sixth largest economy (Organisation Internationale des Constructuers d'Automobiles (OICA) 2008:Internet). While the industry is a key activity in advanced industrial nations, the industry is also of increasing significance in the emerging economies of North and East Asia, South America and Eastern Europe (Nag, Benerejee & Chatterjee 2007:1).

The industry is also one of the largest investors in research and development (R&D), playing a key role in society-wide technological development (OICA 2009:Internet). The global automotive industry is currently led by the main manufacturers (OEMs), that is, Toyota, General Motors (GM), Volkswagen, Ford, Honda, PSA, Nissan, BMW and Chrysler, which function in an international competitive market (Naude 2009:33).

According to Ciferri and Revill (2008:1), the economic crisis in 2008 triggered a major decline in the number of OEMs, leading to consolidation in 2010.

2.2 IMPORTANCE OF THE GLOBAL AUTOMOTIVE INDUSTRY

According to the European Commission (2006:9), the automotive industry is a significant source of employment, a leading investor in innovative R&D, an investmentintensive industry, an important source of fiscal revenues and a momentous contributor to trade (Charles 2009:7). The automotive industry contributes from 4% to 8% of the GDP and accounts for 2% to 4% of the labour force in the Organisation for Economic Co-operation and Development (OECD) countries. Afsharipour et al. (2006:1) further noted that today more than 700 million motor vehicles are registered worldwide with over 550 million vehicles (75% passenger cars) registered in OECD countries.

In the world's largest automotive market, the USA, more than 850 000 people were employed in the manufacturing sector at the end of 2008. However, China overtook the USA to become the world's largest automotive market for the first time in 2009, with annual sales exceeding 13.64 million units. The Asian automotive giant Japan provided jobs to 725 000 people in the car manufacturing sector until 2008 (OICA 2009:Internet). The overview given above gave some idea of the importance of the industry to the world's economy.

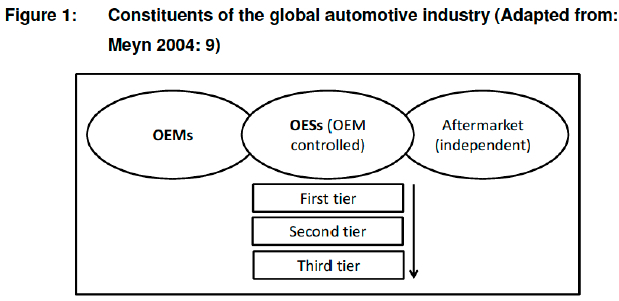

2.3 CONSTITUENT OF THE GLOBAL AUTOMOTIVE INDUSTRY

The global industry is constituted of the following major components, each with distinct requirements (Lamprecht 2006:16):

• OEMs. This segment comprises passenger car, commercial vehicle and bus manufacturing.

• OESs. This segment is made up of suppliers who manufacture and supply automotive parts and accessories directly to the OEMs for their service networks.

• The independent aftermarket. This segment is responsible for the manufacturing and sales of automotive replacement parts and accessories through independent retailers and repair shops directly to the consumer, rather than to the OEMs.

• First-, second- and third-tier component manufacturers. This segment is involved in the supply of manufactured parts and accessories to OEMs, OESs and the independent aftermarket. The distribution between the different tiers of component suppliers is indicative of the component manufacturer's role in the value chain.

Figure 1 presents the constituents of the global automotive industry

Having briefly looked at some of the components of the global automotive industry, the focus of the article now turns to the South African automotive industry.

3 THE SOUTH AFRICAN AUTOMOTIVE INDUSTRY

This section of the article reviews the South African automotive industry. It presents a background of the industry, the industry policy, major stakeholders in the industry, trends and development in the industry.

3.1 BACKGROUND TO THE SOUTH AFRICAN AUTOMOTIVE INDUSTRY

The South African automotive industry manufactures and exports motor vehicles and components. The industry has been the most protected industry prior to the trade liberalisation launch in the 1990s. The industry dates back to the 1920s, when Ford and GM established assembly plants in the country in 1924 and 1926 respectively.

This resulted in an acceleration in new car sales from approximately 13 500 units to 20 500 units between 1925 and 1929. The onset of the Great Depression in the 1930s halted the expansion of the industry until 1938/39, after which car sales improved. A third assembly company, the National Motor Assembly of Johannesburg, entered the market in 1939. In the aftermath of the Second World War, the South African automotive industry grew further and even faster. In 1945, the assembly plants Motor Assemblers and Car Distributors Assembly were established in Durban and East London respectively. The Chrysler Corporation established a plant in Cape Town, closely followed by South African Motor Assemblers and Distributors in Uitenhage in 1948 and later by the British Motor Corporation in Cape Town in 1955 (Flatters & Netshitomboni 2006:3).

All of the major vehicle manufacturers are represented in South Africa. Many of the major multinational companies use South Africa to source components and assemble vehicles for both the local and overseas markets. These manufacturers include Toyota, GM, Volkswagen, Ford (incorporating Mazda, Land Rover and Volvo), Nissan, BMW, DaimlerChrysler, and Fiat (Muller 2009:2).

3.2 SOUTH AFRICA'S AUTOMOTIVE INDUSTRY POLICY

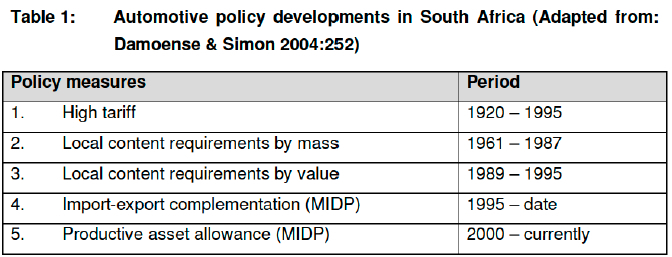

In South Africa, automotive production started in the 1920s. Government used tariff regulation and local content requirements to guide and protect industry growth (Kaggwa 2008:4). The initial phase that lasted until 1961 was a classical import substitution, favouring simple assembly in the domestic market. Very high protective tariff on imports created space for the development of an industry of small plants, producing many models in small volumes at a high cost (Department of Trade and Industry (DTI) 2004:8). By the early 1990s, it was evident that the hitherto inward looking policy stance was not sustainable in the long run. The industry had to comply with the General Agreement on Tariff and Trade (GATT) and World Trade Organization (WTO) trade regulations (Damoense & Simon 2004:252).

Domestic market constraints meant that exports had to play a big role in industry growth. The government realised that the industry needed encouragement with a number of 'sticks and carrots' to change and improve its competitiveness (Muller 2009:2). Of major importance to government was finding ways through which to maintain and grow the industry in a less protected trade environment (Myen 2004:8). Table 1 summarises the industry policy implemented from 1920 to date.

3.3 THE MOTOR INDUSTRY DEVELOPMENT PROGRAMME

The MIDP was initiated in 1995 to help the motor industry adjust to South Africa's reintegration into the global economy (Flatters & Netshitomboni 2006:3). The aim of the MIDP was to enhance component exports, improve international competitiveness, stabilise long-term employment and attract foreign investment (DTI 2004:8). The MIDP boosted exports by enabling local vehicle manufacturers to include total export values as part of their local content total, then allowing them to import the same value of goods duty-free (Muller 2009:2). In South Africa, the MIDP was not the first industrial policy for the sector. It was preceded by six different phases of official industrial policy, which started in 1961 and will be replaced in 2013 by a new policy, the APDP (Kok 2008:33).

The release of the detailed elements of the APDP that will run from 2013 through to 2020 will enable vehicle manufacturers and their suppliers to plan strategically for the future and to finalise investment decisions with confidence and certainty. Compliance with the World Trade Organisation (WTO) led to the South African government reviewing the MIDP and replacing it with the APDP. This involved a shift from export support to production support, while phased-down tariff reductions (albeit at a slower pace) are transitionally maintained as the MIDP gives way to the APDP (Mohubetswane 2010:53).

3.4 KEY ROLE PLAYERS IN THE SOUTH AFRICAN AUTOMOTIVE INDUSTRY

The key role players in the South African automotive industry are all part of the Motor Industry Development Council (MIDC). The MIDC was established in 1996 as a joint industry-government-labour body and is the major influence on strategies and policies for the automotive sector. The MIDC provides an effective platform for communication and cooperation and for all the relevant stakeholders to interact on automotive issues. The stakeholders in the automotive industry include government, labour and business (DTI 2004:99). Table 2 shows the key stakeholders and actors in the South African automotive industry.

3.5 PERFORMANCE INDICATORS OF THE SOUTH AFRICAN AUTOMOTIVE INDUSTRY

This sub-section of the article present the industry contribution to the country's GDP, aggregate employment levels and trends and the industry performance in a global context.

3.5.1 The automotive industry's contribution to the GDP in South Africa

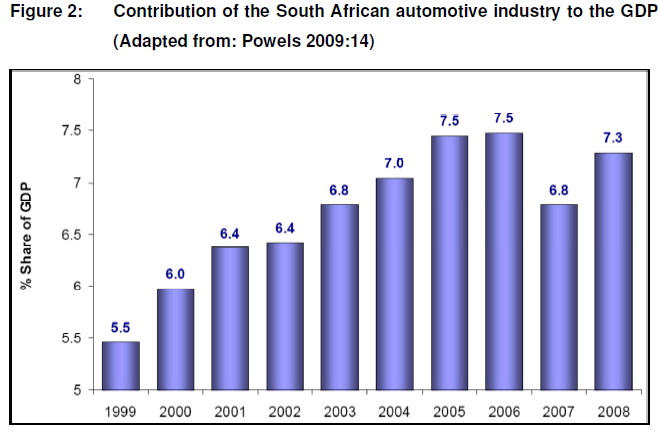

The industry's contribution to South Africa's GDP during 2008 increased to 7.29% from 6.79% in 2007. Despite negative growth in the industry due to the effect of the global recession, the industry's contribution to the GDP was close to the all-time high of 7.5% recorded in 2006 (NAAMSA 2009:Internet). Figure 2 shows the contribution of the automotive industry to the GDP from 1999 to 2008.

Based on research by Econometrix (Pty) Ltd, the automotive industry's contribution to South Africa's GDP during 2010 was calculated at 5.9% in 2009 and 6.2% in 2010 (NAAMSA 2011:4). This indicates that the industry is moving away from the recession.

3.5.2 Aggregate employment levels and trends

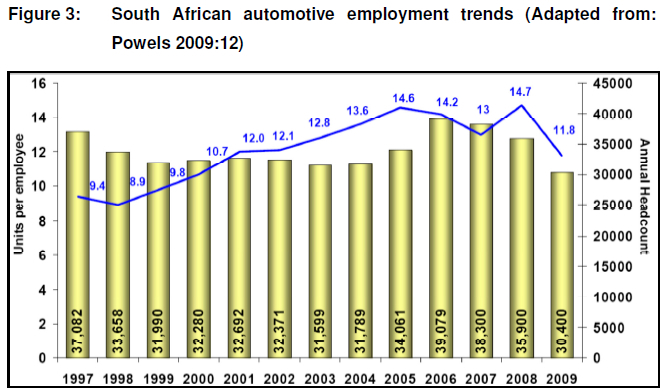

The number of people employed by the South African automotive industry (30 400 jobs) showed a decline in 2009 compared to 35 900 positions in 2008. The aggregate industry employment declined by 5 500 jobs. This could be attributed to the extremely difficult operating environment, where manufacturers were under pressure to reduce operational costs as a result of the effect of the global recession (NAAMSA 2009:Internet). Figure 3 shows the South African automotive employment for 13 years, from 1997 to 2009.

However, as indicated by NAAMSA (2010b:2), there was an encouraging increase in aggregate industry employment levels in 2010. The industry expanded by 1 217 jobs (4.3%) in 2010. Compared to 2010, the aggregate industry employment showed a marginal improvement of 0.2% in the first quarter of 2011 (NAAMSA 2011:2).

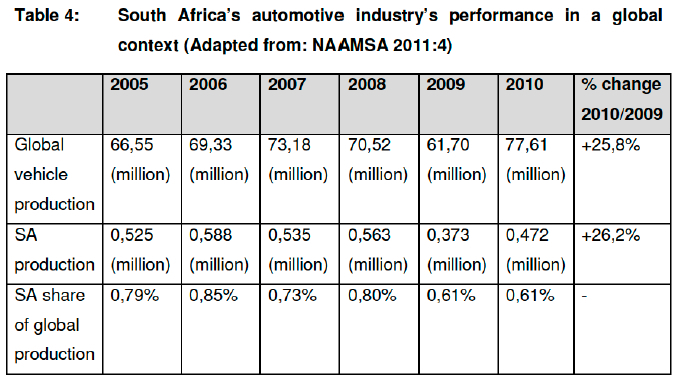

3.5.3 South Africa's automotive industry's performance in a global context

South Africa produced 78.7% of Africa's vehicle production in 2005 (NAAMSA 2009:Internet). This is relatively small in international terms, as it was less than 1% of the global market share and the country was ranked 19th by size globally in 2005.

New global motor vehicle production in 2006 reached 69 212 755 units. The South African vehicle manufacturing industry's share of global production rose steadily in recent years (from 0.7% in 2004 to 0.85% in 2006) (Naude 2009:32). According to NAAMSA (2009:lnternet), passenger car sales at 60 043 units recorded a decline of 25 726 units, or 30.0%, compared to the 85 769 new cars sold during the corresponding quarter of 2008.

Combined commercial vehicle sales during the first quarter of 2009 at 33 242 units reflected a fall of 22 173 units, or a decline of 40.0%, compared to 55 415 units sold during the corresponding quarter of 2008 (NAAMSA 2010a:lnternet). However, global new motor vehicle production reached a record of 77.6 million units in 2010 (2009: 61 703 997). This represents a massive increase of 15.9 million vehicles produced, or 25.8%, compared to the 61.7 million new vehicles produced during 2009 (NAAMSA 2011:4). Table 4 shows the South Africa's automotive industry's performance in a global context.

The performance indicators authenticate that the automotive industry is an important industry that contributes to the South African economy. The automotive sector, regarded as the leading manufacturing sector, has been identified by the South African government's 2007 and 2010 revised National Industrial Policy Framework and Industrial Policy Action Plan as one of the priority sectors to fast-track growth and development. The positive developments and achievements in the South African automotive industry since 1995 have been driven by a supportive automotive policy regime. The 2020 vision under the new APDP, shared by government and industry, is to double vehicle production from the 2006 levels of approximately 600 000 units to 1.2 million units by 2020, with a much stronger development of the automotive component sector. After the above overview of the global and national automotive industry, the focus of the article now shifts to SCM in the automotive industry.

4 SUPPLY CHAIN MANAGEMENT

This section of the article reviews the concept of SCM in the automotive industry. It presents the definition and background of SCM, the framework of the automotive supply chain as well as the changing structure of the automotive supply chain.

4.1 DEFINITION AND BACKGROUND OF SUPPLY CHAIN MANAGEMENT

The automotive industry is highly competitive, characterised by growing international competition and increasingly demanding customers (Christopher & Rutherford 2005:24). Increased competition and complexity has led to the supply chain becoming an important issue for companies (Hugo, Badenhorst-Weiss & Van Biljon 2004:5). According to Leenders and Fearon (2004:10), "SCM is the systems approach to managing the entire flow of information, materials and services from the raw materials suppliers through factories and warehouses to the end customer".

Christopher (2005:5) defines SCM as "the management of upstream and downstream relationships with suppliers and customers to deliver superior customer value at less cost to the supply chain as a whole". In general, SCM involves relationships and managing the inflow and outflow of goods, services and information (network) between and within producers, manufacturers and the consumers (Gripsrud, Jahre & Persson 2006:645). Although authors' definitions of SCM differ, it exists in all organisational types and can be classified into three categories: a management philosophy, implementation of a management philosophy and as a set of management processes (Klemencic 2006:13; Lambert 2006:13).

4.2 IMPORTANCE OF SUPPLY CHAIN MANAGEMENT TO THE AUTOMOTIVE INDUSTRY

Wisner, Tan and Leong (2008:17) observe that many businesses are only beginning to realise the benefits and problems that accompany an integrated supply chain. Businesses that practice SCM concepts continually improve their ability to reduce waste, decrease time, be flexible and cut costs, which ensure future profitability (Matsubara & Pourmohammadi 2009:91). With the implementation of a concept such as SCM, the automotive industry will become the largest growing and most lucrative industry (Zhu, Sarkis & Lai 2006:1041).

In the age of electronic business and global outsourcing, SCM plays a crucial role in many of these areas. These include best-in-class, high-performance solutions that can be utilised by the world's leading automobile manufacturing, logistics and distribution companies and retailers to blend the demand chain with the supply chain. SCM helps in demand forecasting; taking orders; giving accurate promise dates; sourcing and manufacturing the right goods; proper positioning of inventory; picking, packing and efficient transhipment; and, most importantly, SCM makes a world of difference to the manufacturers by maintaining a minimal finished goods inventory (goods in stock).

4.3 THE CHANGING STRUCTURE OF THE AUTOMOTIVE SUPPLY CHAIN

The automotive industry has undergone a transformational evolution over the last two decades (Zhu et al 2006:1042). Historically, the industry operated under a 'push' model. In this model, marketing and sales take a best guess at market demand and then supply these forecasts to the design, engineering, financial and manufacturing teams to determine make and/or model production volumes (Howard, Miemcyk & Graves 2006:91). With the boom of the internet, data have become much more accessible to both manufacturers and consumers of automobiles (Tang & Qian 2008:288).

The industry primarily used lean, just-in-time manufacturing processes and their supporting technologies. Because the price tag for reengineering and supporting technologies used to be prohibitively high, efforts were limited to OEMs and their firsttier suppliers. Important progress was made to 'commonise' process and technology.

However, these efforts were creating a widening process and technology gap between OEMs, first-tier suppliers and the rest of the automotive supply chain. As the internet became a common fixture in automotive business-to-business, competitive pressures grew exponentially (Tang & Qian 2008:288).

The automotive industry is known for adopting mass production as its standard production strategy. Mass production relies heavily on a company's ability to forecast demand accurately, which in turn guides the company's decisions regarding operations and production. Characterised as a push system, forecast-driven production is a highly efficient but rather rigid system that utilises historic data and projections to create a production plan and makes use of existing configurations to produce products for stock (Zhang & Chen 2006:668).

However, with changing demands in the business environment and the focus shift to mass customisation, forecast-driven production could no longer cope with a rapidly changing market. Companies' operations are more initiated by the customer orders, not a forecast, hence the employment of a customer-order strategy (Holweg, Disney, Hines & Naim 2005:507). A customer-order-driven production approach is characterised as a pull system that produces the products for specific customer orders in a timely manner, thus avoiding stockpiles (Zhang & Chen 2006: 669).

4.4 TRENDS AND DEVELOPMENTS IN THE GLOBAL AUTOMOTIVE SUPPLY CHAIN

Some of the trends and developments that are transforming the automotive supply chain reviewed in this article include the following:

Globalisation: Globalisation is a key factor in the overall strategy of automotive suppliers. It has generated two kinds of suppliers in the automotive industry, namely global and local. Yesterday, giant companies either exported parts to offshore assembly plants or depended on local suppliers in each production location. Today, a new kind of supplier, the global supplier, has come on the scene. Suppliers with a global presence can concentrate volume production of specific components in one or a few locations. These materials are then shipped to plants close to the customer's final assembly plants where modules and sub-systems are built and sent to the final assembly line as needed. Apart from increasing competition in every market, globalisation provides organisations with the opportunity to find synergies and reduce costs (Mondragon, Lyons, Michaelides & Kehoe 2006:551).

Outsourcing: Outsourcing involves the use of specialists to provide competence, technologies and resources to parts of the whole. Differences in labour costs and disadvantages in scale and scope are influencing the outsourcing trend. Outsourcing has created opportunities for both automotive suppliers and SCM providers (such as logistics and IT companies) to expand their businesses into adjacent areas. The automotive industry has continued to source from low-cost countries as manufacturers and suppliers continue to complement their commodities with more complex products and services (Mondragon, Lyons, Michaelides & Kehoe 2006:552).

Modularisation: Modularity has become one of the most prevalent means to support product variety and achieve mass customisation. Carliss, Baldwin and Clark (1997:84), describe modularity as the process of "building a complex product or process from smaller subsystems that can be designed independently yet functions together as a whole". It is a dispersed assembly system where activities are pre-assembled and others are in a final assembled system (Fredriksson 2006:351). Modular architecture promised to make standardisation possible and offered a strategy for designing and mixing sets of standard components to provide maximum variety to the customer.

Supplier parks: A supplier park is the co-location of supplier facilities close to the plant and relates to the choice of individual suppliers to set up a dedicated facility close to a customer. A supplier park is defined as a concentration of dedicated production, assembly, sequencing or warehousing facilities run by suppliers or a third party in close proximity (i.e. within 3 km) to the OEM plant (Howard et al. 2006 92). The number of automotive supplier parks has grown over the past decade, especially in Europe. Most OEMs have implemented some kind of Supplier Park. Typical activities carried out in automotive supplier parks include warehouse and inventory management, sequencing, manual assembly and late configuration, and they range in size of having between seven and 24 suppliers (Chew 2003:21).

Built-to-order: Build-to-order (BTO) refers to a supply chain strategy in which products are not assembled until a customer order arrives (Zhao & Lv 2009:30). Intensified global competition has led automakers to attempt to institute a BTO approach in which consumers will define the desired features of their vehicles before they are produced. In the more traditional and still prevalent 'build-to-forecast' approach, production is based on forecast demand and information received from dealers regarding prior sales. Recent industry analyses show a rise in vehicle body styles, colours and options. Traditional car models such as sedans, vans, hatchbacks and pick-up trucks are increasingly fragmenting into niches. Derivative car models, on the other hand, such as coupes, roadsters, minivans and two-seaters, as well as crossover vehicles such as four-door coupes, SUV coupes and sport vans, are growing. Automotive experts suggest that BTO is taking hold gradually (Howard et al. 2006:94).

The next section of the article articulates the challenges of the global and South African automotive supply chain.

5 REVIEW OF SUPPLY CHAIN MANAGEMENT CHALLENGES IN THE AUTOMOTIVE INDUSTRY

In this section, a review of related literature on the global and South African supply chain challenges is presented.

5.1 GLOBAL AUTOMOTIVE SUPPLY CHAIN CHALLENGES

From a global perspective, fierce competition, fluctuating market demand and rising customer requirements have lead to customers becoming more demanding with increased preferences (Zhang & Chen 2006:668). Kotler Marketing Group (2009:3) noted that the automotive industry is faced with some of the most difficult and challenging circumstances and OEMs are scrambling to slash production and reduce manufacturing costs. OEMs are required to enhance quality, improve styling, increase organisational efficiencies and drive innovative features into their products in an effort to attract customers and expand into new markets. The industry is at the cutting edge, adopting new technologies. OEMs are continually pressurising their tiered suppliers to reduce costs and increase output and quality (Kotler Marketing Group 2009:3).

In recent years, the automotive industry has experienced strong competition on a global scale in highly competitive markets (Pires & Neto, 2008:328). From a worldwide standpoint, it has been challenged to face issues such as strong pressures to reduce price and delivery time; improve quality and overall customer service; deliver environmentally friendly products; substantially reduce product lifecycles; rapidly introduce new products; reduce the time-to-market and product development costs; supply new markets, both in geographical terms and in terms of new products; and strengthen relationships and intensify communication channels in supply chains in general (Pires & Cardoza 2007:72).

Furthermore, the effect of the economic meltdown has lead to many automotive companies restructuring their operations (Lamprecht 2010:159; Swiecki & Gerth 2008:2). In addition, the general macroeconomic and financial circumstances are not favourable. The cost of energy and raw materials continues to increase due to rising global demand. Strong fluctuations in exchange and interest rates pose another challenge. The government trade, safety and environmental regulations are also influential factors affecting the automotive industry (Veloso & Kumar 2003:26).

5.2 SUPPLY CHAIN CHALLENGES IN THE SOUTH AFRICAN AUTOMOTIVE INDUSTRY

The South African automotive industry faces several challenges supplemented by fierce competition (Muller 2009:2; Supplychainforesight 2010:Internet). As stated by the Supplychainforesight report of 2007, although the automobile industry in South Africa is in an advanced stage compared to other industries with regard to the management of the supply chain activities, the industry faces challenges of cost reduction and service improvement. The Supply Chain Intelligence Report (CSIR) (2009:Internet) indicated that the majority of companies in the automotive industry in South Africa not only operate with low levels of collaboration, but are also not market-sensitive or reactive to the changing market. The Supplychainforesight report (2010:Internet) further highlights that the industry supply chain is more vulnerable than ever as a result of huge swings in demand and volumes experienced because of the global recession.

In the study conducted by Naude (2009:99), important challenges for the South African automotive industry indicated are to produce at a competitive cost and to have the ability to respond quickly and reliably to first-world market demands. Naude (2009:265) further noted that the main supply chain problems in the South African automotive industry include pressure by OEMs to reduce prices, the price of materials, cancellation of orders, excessive inventory, the unreliability of rail transport and rail capacity problems, the high cost of South African ports, the cost of replacing outdated technology and broad-based black economic empowerment - achieving and verifying black economic empowerment scorecards. Further problems include a lack of skills and labour problems, both of which are time consuming to resolve.

Furthermore, logistics issues are affirmed by Van der Merwe (2009:1), who states that on the World Bank's Logistics Performance Index, in terms of logistics expenditure, South Africa ranked 124th out of 150 countries reviewed. This was blamed on various logistics problems such as inadequate infrastructure, rising fuel costs and increased road freight volumes. Muller (2009:2) highlighted a number of issues that currently have an influence on the competitiveness of the South African automotive industry.

These include globalisation and market convergence (owing to the effects of liberalisation, national markets are increasingly globalised), individualisation (products need to be tailored and tailorable to satisfy individual requirements), required accelerated modification and diversification of the product portfolio (manufacturers therefore have to shorten product lifecycles in order to react with innovative products to the expectations of changing consumer demands), increasing safety requirements and a regulatory necessity and increased pressure for innovation and flexibility in development and manufacturing.

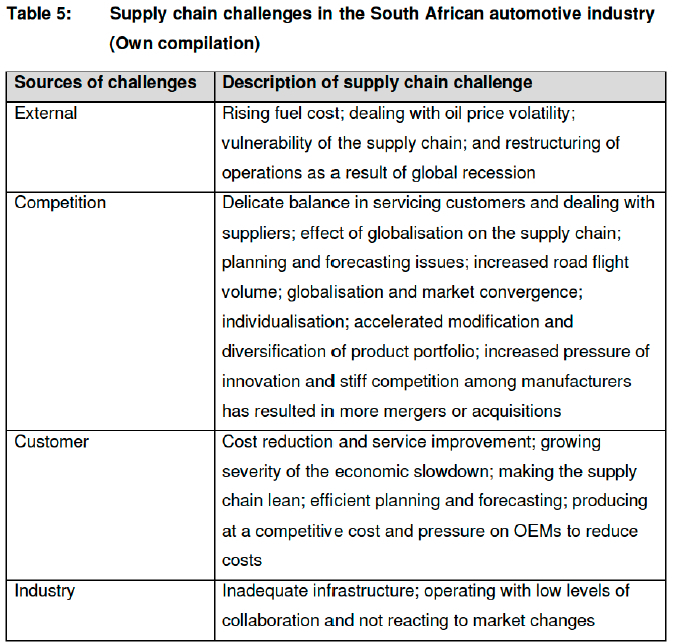

Based on the review discussed above, the article articulates that supply chain challenges in the global and South African automotive industry stem from the external environment, the customers, competition and the automotive industry. Table 5 illustrates the supply chain challenges in the South African automotive industry and their main sources.

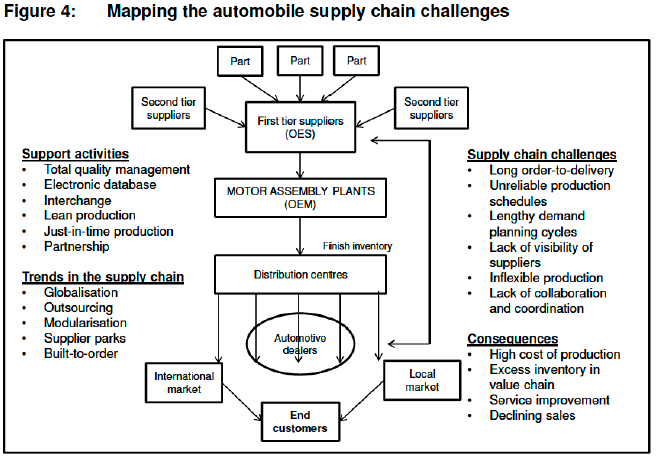

From the review above, the article maps the supply chain challenges, the support activities in the supply chain, trends in the supply chain and the consequences of the challenges to the automotive industry. Figure 4 maps the South African automotive supply chain challenges.

6 CONCLUSION

This article is a report on the trends and challenges of the supply chain in the South African automotive industry. In the course of the article, the global and South African automotive industry was reviewed. SCM in the automotive industry was discussed and the challenges in the South African automotive industry were analysed. The article concludes by mapping the challenges of the supply chain in the South African automotive industry.

The South African automotive industry operates in a highly competitive environment characterised by growing international competition and increasingly demanding customers. SCM is paramount for the success of the industry due to increased competition and complexities that constitute critical issues for automotive companies. Some of the SCM challenges affecting the industry include long order-to-delivery lead times, unreliable production schedules that lead to excess inventory throughout the value chain, lengthy demand planning cycles and lack of visibility to suppliers, material and production constraints causing scheduling delays and short-term production changes.

Based on the review in this article, it can be claimed that the South African automobile industry is an important contributing industry to the South African economy as well as the economy of the African continent. However, the industry still has a long way to becoming a significant player in the global automotive industry. In order to address the challenges in the supply chain and obtain a competitive advantage, the industry should adopt a supply chain strategy that would be responsive to meet customer demand and expectations.

In addition, the South African automotive sector has to fight to remain locally viable and internationally competitive. On the local side, demand will have to be increased through vehicle financiers developing innovative ways to encourage new buyers. The industry will also have to make the best of the maintenance sub-sector, which will receive more attention as consumers hold on to their old cars. From a competitiveness perspective, the local component manufacturers will have to increase their capacity through focused government policy and financial assistance. The development of skills will also be crucial in helping not only component manufacturers but also vehicle manufacturers.

The most important factor in reducing costs and improving competitiveness is increasing local content of locally produced vehicles. This will mitigate the high costs of component imports as well as the logistical issues of having to import them. The transport and infrastructure issues will also have to be ironed out, with efficient and cost-effective port services being a cornerstone of a globally competitive automotive industry.

REFERENCES

AFSHARIPOUR A., AFSHARI A. & SAHAF L. 2006. E-procurement in the Automobile Supply Chain of Iran, Master's thesis, Lulea University of Technology. [ Links ]

BARNES J. & MORRIS M. 2008. Staying alive in the global automotive industry: what can developing economies learn from South Africa about linking into global automotive value chains? The European journal of development research, 20(1), 31-55. [ Links ]

CARLISS Y., BALDWIN B. & CLARK C. 1997. Managing the age of modularity. Harvard Business Review, 57(5), 84-93. [ Links ]

CHARLES D. 2009. The importance of the Australian automotive industry to Australia. Deloitte Touche Tohmatsu. [Internet: http://www.autocrc.com/files/File/pres/Charles-pres.pdf; downloaded on 2010-08-24]. [ Links ]

CHEW E. 2003. Carmakers reap benefits of supplier park concept. Automotive News Europe, 8: 2. [ Links ]

CIFERRI L. & REVILL J. 2008. Who will survive the auto crisis? Automotive news Europe, 13 (25/26), 8: 1-2. [ Links ]

DEUTSCHE BANK RESEARCH. 2009. The News Era Unfolding for the Automobile Industry, Report on European Integration. EU Monitor 62. [ Links ]

DEPARTMENT OF TRADE AND INDUSTRY (DTI). 2004. Current developments in the automotive industry. September, 2004. [ Links ]

CHRISTOPHER M. & RUTHERFORD C. 2004. Creating supply chain resilience through agile six sigma. Critical Eye, 24-28. [ Links ]

CHRISTOPHER M. 2005. Logistics and supply chain management: Creating value-added networks. Harlow, England: Prentice Hall. [ Links ]

DAMOENSE M.Y. & SIMON A. 2004. An analysis of the impact of the first phase of South Africa's Motor Industry Development programme (MIDP), 1995-2000. Development Southern Africa, 21(2), 251-269. [ Links ]

EUROPEAN COMMISSION. 2006. A competitive automotive regulatory system for the 21st century, Belgium, 2006. [ Links ]

FLATTERS F. & NETSHITOMBONI N. 2006. Trade and poverty in South Africa: Motor industry case study. University of Cape Town's Southern Africa Labour and development Research Unit Trade and Poverty Project. [ Links ]

FREDRIKSSON P. 2006. Mechanisms and rationales for the coordination of a modular assembly system: The case of Volvo cars. International journal of operations and production management, 26(4), 350-370. [ Links ]

GRIPSRUD G., JAHRE M. & PERSSON G. 2006. Supply chain management - back to the future. International Journal of physical distribution and logistics management, 36(8): 643-659. [ Links ]

HOLWEG M., DISNEY S.M., HINES P. & NAIM M.M. 2005. Towards responsive vehicle supply: a simulation-based investigation into automotive scheduling systems. Journal of Operations Management, 32(5): 507-30. [ Links ]

HOWARD M., MIEMCYK J. & GRAVES A. 2006. Automotive supplier parks: An imperative for build-to-order? Journal of purchasing and supply management, 12: 91-104. [ Links ]

HUGO W.M.J., BADENHORST-WEISS J.A. & VAN BILJON E.H.B. 2004. Supply chain management: logistics in perspective. 3rd Edition. Pretoria: Van Schaik. [ Links ]

KAGGWA M. 2008. Modelling South Africa's incentives under the motor industry development programme. PhD thesis, University of Pretoria. [Internet: http://upetd.up.ac.za/thesis/available/etd-04072009-203959: downloaded on 2010-07-16]. [ Links ]

KLEMENCIC E. 2006. Management of Supply Chain-Case of Danfoss District Heating Business Area, Faculty of Economics. Ljubljana University, February 2006. [ Links ]

KOK L. 2008. The impact of the Motor Industry Development Programme on the competitiveness of the automotive component manufacturers. Master's thesis, University of Pretoria. [ Links ]

KOTLER MARKETING GROUP. 2009. Sales best practices in the global automotive supplier industry. [ Links ]

KPMG. 2009. Momentum: KPMG's Global Auto Executive Survey 2009, Industry concerns and expectations 2009-2013. [Internet: http://www.kpmg.com/Global/en/IssuesAndInsights/ArticlesPublications/Momentum/Documents/Momentum-AutoExec-2009.pdf; downloaded on 2010-08-30]. [ Links ]

LAMPRECHT N. 2006. Analysis of the Motor industry development programme (MIDP) as a promotional tool for the South African automotive industry in the global automotive environment. Master's Thesis, University of South Africa. [ Links ]

LAMPRECHT N. 2010. The impact of the Motor Industry Development Programme (MIDP) on the export strategies of the South African light motor vehicle manufacturers. Doctoral Thesis, University of South Africa, Pretoria. [ Links ]

LEENDERS M.R & FEARON H.E. 2004. Purchasing and supply chain management.. Chicago: Irwin, (11th ed). [ Links ]

MONDRAGON A.E.C., LYONS A.C., MICHAELIDES Z.. & KEHOE D.F. 2006. Automotive supply chain models and technologies: a review of some latest developments. Journal of enterprise information management, 19(5): 551-562. [ Links ]

MOHUBETSWANE M.A. 2010. Changes in Work and Production Organisation in the Automotive Industry Value Chain: An evaluation of the responses by labour in South Africa. Master's thesis, University of the Witwatersrand, Johannesburg. [ Links ]

MPHAHLWA M.P. 2008. Automotive development programme announcement.. [Internet:: www.dti.gov/za/articleview.asp; downloaded on 2009-07-02]. [ Links ]

MULLER M.L. 2009. Current automotive industry: how leaders practice CI. Competitive intelligence, 11(3):1-6. [ Links ]

MYEN M. 2004. An export performance of the South African automotive industry. New stimuli by the EU-South Africa Free Trade Agreement. Tralac, Working paper, No.8 (2004). [ Links ]

NAG B., BENERJEE S. & CHATTERJEE R. 2007. Changing features of the automobile industry in Asia: Comparison of production, Trade and market structure in selected countries, Asia-Pacific Research and training network on Trade, Working paper series, No.37, July 2007. [ Links ]

NAAMSA (NATIONAL ASSOCIATION OF AUTOMOBILE MANUFACTURERS). 2009. Quarterly review of business conditions: Motor vehicle manufacturing industry, 1st quarter (2009). [ Links ]

NAAMSA (NATIONAL ASSOCIATION OF AUTOMOBILE MANUFACTURERS). 2010a. Quarterly review of business conditions: Motor vehicle manufacturing industry. 1st quarter 2010. [ Links ]

NAAMSA (NATIONAL ASSOCIATION OF AUTOMOBILE MANUFACTURERS). 2010b. Quarterly review of business conditions Motor vehicle manufacturing industry: 4th quarter 2010. [ Links ]

NAAMSA (NATIONAL ASSOCIATION OF AUTOMOBILE MANUFACTURERS). 2011. Quarterly review of business conditions: Motor vehicle manufacturing industry. 1nd quarter 2011. [ Links ]

NAUDE M.J.A. 2009. Supply chain management problems experienced by South African automotive manufacturers. Doctoral dissertation, University of South Africa, Pretoria. [ Links ]

NAUDE M.J. & BADENHORST-WEISS J.A. 2011. Supply chain management problems at South African automotive component manufacturers. Southern African Business Review, (15):1. [ Links ]

OICA, VIDE ORGANISATION INTERNATIONALE DES CONSTRUCTUERS D'AUTOMOBILES. 2008. [Internet: www.oica.net; downloaded on 2010-01-01]. [ Links ]

OICA, VIDE ORGANISATION INTERNATIONALE DES CONSTRUCTUERS D'AUTOMOBILES. 2009. [Internet: www.oica.net; downloaded on 2010-01-025]. [ Links ]

POWELS, D.C. 2009. The South African automotive industry: a reflection on the first year of economic crisis. NAAMSA 2009. [ Links ]

PIRES R.I.S. & NETO M.S. 2008. New configurations in supply chains: the case of a condominium in Brazil's automotive industry. Supply Chain Management: An International Journal, 13 (4): 328-334. [ Links ]

PIRES S. & CARDOZA G. 2007, "A study of new supply chain management practices in the Brazilian and Spanish auto industries", International Journal of Automotive Technology and Management, 7 (1): 72-87. [ Links ]

SIMCHI-LEVI D., KAMINSKY P. & SIMCHI-LEVI E. 2009. Designing and Managing the Supply Chain: Concepts, Strategies and Case Studies. New York: McGraw-Hill, 3rd edition. [ Links ]

SUPPLYCHAINFORESIGHT. 2007. Survey conceptualised and initiated by Barloworld Logistics, South Africa. [Internet: www.supplychainforesight.co.za; downloaded on 2008-06-06]. [ Links ]

SUPPLYCHAINFORESIGHT 2010. Survey conceptualised and initiated by Barloworld Logistics, South Africa. [Internet: www.supplychainforesight.co.za; downloaded on 2010-05-01]. [ Links ]

SUPPLY CHAIN INTELLIGENCE REPORT (CSIR). (2009). Auto industry crisis-part own making. [Internet: www.bizcommunity.com/Article/196/168/38180.html; downloaded on 201009-20]. [ Links ]

SWIECKI B. & GERTH R.J. 2008. Collaboration in the Automotive Supply Chain - Realising the Full Potential of a Powerful Tool. Centre for Automotive Research, October 2008. [ Links ]

TANG D. & QIAN X. 2008. Product lifecycle management for automotive development focusing on supplier integration. Computers in industry, 59: 288-295. [ Links ]

VAN DER MERWE J.P. 2009. The state of the automotive sector in South Africa. TradeInvest. [Internet: www.tradeinvestsa.co.za/feature_articles/344969.htm; downloaded on 2010-02-02]. [ Links ]

VELOSO F. & KUMAR R. 2003. The Automotive supply chain: Global Trends on Asian perspectives. ERD Working paper series No 3. [ Links ]

WISNER J.D., TAN K.C. & LEONG G.K. 2008. Principles of supply chain management: A balanced Approach. Mason, Ohio: South-Western Cengage learning. [ Links ]

ZHANG X. & CHEN R. 2006. Forecast-driven or customer-order-driven? An empirical analysis of the Chinese automotive industry. International Journal of Operations & Production Management, 26(6): 668-688. [ Links ]

ZHAO Z. & LV Z. 2009. Global Supply Chain and the Chinese Auto Industry. Chinese Economy, 42(6): 27-44. [ Links ]

ZHU Q., SARKIS J. & LAI K.H. 2006. Green supply chain management: pressures, practices and performance within the Chinese automobile industry. Journal of Cleaner Production, 15: 1014 - 1052. [ Links ]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}