Servicios Personalizados

Articulo

Inglés (pdf)

Inglés (pdf)

Articulo en XML

Articulo en XML Referencias del artículo

Referencias del artículo

Indicadores

Links relacionados

-

Citado por Google

Citado por Google -

Similares en Google

Similares en Google

Compartir

Permalink

PermalinkJournal of Contemporary Management

versión On-line ISSN 1815-7440

JCMAN vol.8 no.1 Meyerton 2011

RESEARCH ARTICLES

Bank managers' views on relationship marketing

C RootmanI; M TaitII; G SharpIII

INelson Mandela Metropolitan University

IINelson Mandela Metropolitan University

IIINelson Mandela Metropolitan University

ABSTRACT

The purpose of this article is to investigate relationship marketing and customer retention in South African banks, based on the perceptions of bank managers. Banks can use relationship marketing and customer retention to attract and maintain profitable clients. However, often the views of managers and clients differ regarding the variables important for bank-client relationships. A self-developed, structured questionnaire was distributed via judgemental snowball sampling to bank managers in South Africa. Findings in the paper revealed that, according to bank managers, only two of the selected six variables influence relationship marketing. As this study forms part of a broader study, a difference in the viewpoints of bank managers and individual banking clients is evident.

This article focuses on how banks should change their bank managers' relationship marketing views to align these with the views of clients. Ultimately, strategies suggested by this article could improve bank-client relationships and banks' customer retention.

Key phrases: banks, relationship marketing, customer retention

1 INTRODUCTION

Marketing is one of the eight business functions performed in firms (Bosch, Tait & Venter 2011:14). Bosch et al. (2011:383) define marketing in a firm as the business function that is responsible for the satisfaction of consumer needs by adding value through appropriate products and/or services, reasonable prices and acceptable distribution channels using promotional strategies and marketing communication methods.

Two important concepts in the field of marketing are relationship marketing and customer retention. Grönroos (1994:4-20) initially defined relationship marketing as the strategy employed by firms to identify, establish, maintain, enhance, and, when necessary, terminate relationships with clients and other stakeholders at a profit so that the objectives of all parties involved are met. Kotler, Armstrong and Tait (2010:21,31) emphasise that marketing is increasingly shifting from trying to maximise the profit on each individual transaction to building mutually beneficial relationships with clients. Swartz and lacobucci (2000:96) also state that in recent years much focus in marketing was on the concept of developing relationships with clients. If "successful" marketing occurs, a firm will have high customer retention rates. According to Reichheld (1996:57), customer retention is a firm's "zero defections", or no switches, of profitable clients to competitors. Customer retention can also be defined as the longevity of a client's relationship with a firm (Menon & O'Connor 2007:157).

The main focus areas of prior research on relationship marketing were theoretical in nature; focused only on the relationship marketing of specific firms and focused extensively on the practical implementation of relationship marketing, namely the use of customer relationship management (CRM) processes and systems. In order to differentiate between relationship marketing and CRM for the purpose of this study, it is important to realise that most authors regard relationship marketing as the strategy used by firms to create and maintain client relationships. CRM is mainly regarded as the processes, systems and technology implemented in order to put relationship marketing into practice (Rootman 2011:70).

Through prior research, relationship marketing benefits for firms and their clients have been identified. Proper relationship marketing can lead to higher levels of service quality, client satisfaction, support and the retention of profitable clients (Bejou, Ennew & Palmer 1998:171; Eid 2007:1026; Karakostas, Kardaras & Papathanassiou 2005:857; Menon & O'Connor 2007:157; Rootman 2006). In addition, improved client-relationships can ensure firms of lower marketing costs and increased customer loyalty as well as special benefits, customised offerings and lower prices for clients (Ackermann & Van Ravesteyn 2005:149,152; Baron & Harris 2003:161; Bergeron, Roy & Fallu 2008:171; Customer relationship management benefits 2004:1; Eid 2007:1021; Mudie & Cottam 1999:257; Swartz & lacobucci 2000:96,328; Wilmshurst & Mackay 2002:346;). Especially in service industries, relationship marketing has become pertinent.

Customer retention has also been well researched. Many studies (Colgate, Stewart & Kinsella 1996:23; Jones, Mothersbaugh & Beatty 2000:259) have shown that a firm's most important asset is its existing client base - thus firms' ability to retain consumers is of the essence. Customer retention can lead to many advantages for firms, including higher sales and profits, lower costs to acquire new clients, positive word-of mouth recommendations, as well as aspects such as recognition, personalisation, power, risk reduction, status and affiliation for retained clients (Brink & Berndt 2008:43; Bruhn & Georgi 2006:18; Buttle 2004:17,26-27; Farquhar 2003:395; Karakostas et al. 2005:855). Aspects regarding customer retention have also been researched in United Kingdom banks (Clark 2002:93) and other financial services industries (Baker 2007/2008:35-38).

However, the influence of relationship marketing on the customer retention of banks, specifically from the viewpoints of bank managers, has not yet been researched in the South African banking industry. Being an industry where a service is offered, that is intangible, inseparable, perishable, variable and untransferable (Bosch et al. 2011:413; Boshoff & Du Plessis 2009:5-8; Bruhn & Georgi 2006:13-15; Kotler et al. 2010:234), the South African banking industry has many challenges. In addition, the South African banking industry is highly competitive and in order to compete, banks need to focus on their clients and their financial and banking needs. Therefore, a focus by banks on client relationships (relationship marketing) and customer retention can prove to deliver many advantages.

Previous research has shown that there often exist differences in viewpoints between the management of firms and their clients. A firm needs to be knowledgeable about how the clients perceive relationship marketing and which variables clients feel are influencing the firm's level of relationship marketing. Additionally, the firm needs to identify the viewpoint of the firm's management with regard to the firm's relationship marketing and how the two viewpoints differ. Any possible difference needs to be rectified. Chipunza (2008:148) confirms this by indicating that the service firm needs to monitor the relationship between what service employees think about the firm and its services, and what clients perceive.

In other words, the service firm needs to ensure that the relationship marketing issues experienced by the clients are understood by management and effectively attended to, revised and addressed by the firm to ensure sufficient levels of relationship marketing. Thus, it is also important in the South African banking industry to determine the views of managers regarding relationship marketing and customer retention and then to compare these with the views of banking clients. This may result in banks having clear knowledge about their clients' most important needs in terms of building and maintaining relationships with their banks and how banks' customer retention could be improved.

It is evident that strong client relationships (thus proper relationship marketing strategies) and higher customer retention rates can possibly increase the survival rate of banks around the world. However, are banks aware of the relationship marketing and customer retention aspects that are important to clients when building relationships with their banks?

A previous study in South Africa by Rootman (2011) has identified the relationship marketing and customer retention aspects important to clients. Now it is essential to identify bank managers' views on relationship marketing and customer retention in banks. Therefore, this research focuses on gathering insights into South African banks' relationship marketing and customer retention focus areas, as perceived by bank managers. This will shed light on managers' views compared to the views of clients (from the previous study) in order to identify differences to make relevant recommendations to banks.

2 LITERATURE OVERVIEW

The literature overview consists of a discussion on relationship marketing, customer retention and the current state of South African banks.

2.1 RELATIONSHIP MARKETING AND CUSTOMER RETENTION IN PERSPECTIVE

As mentioned above, relationship marketing is a core strategy used by firms to attract, interact with, and keep profitable clients, while ensuring mutual benefits for the firm and its clients (Walsh, Gilmore & Carson 2004:469). Also described above, is the concept customer retention. It has been established that customer retention can be described as the rate at which a firm keeps or retains its profitable clients, in other words, if firms retain their clients it means that their clients do not switch to competitors who provide similar products and services (Reichheld 1996:56-69).

Based on literature, the following variables linking to bank activities, actions and/or methods, have been identified for this study as variables possibly influencing relationship marketing and customer retention in banks: communication, empowerment, personalisation, fees, ethical behaviour and technology.

- Communication is the delivering of a message or information, through various methods, from one individual or group to another (Bosch et al. 2011:506; Lages, Lages & Lages, 2005:1041; Joiner, 1994:124). Included in the concept communication, to and from clients, are word-of-mouth (Chen & Xie 2008:477; Kotler et al. 2010:431) and marketing communication (Elliott, R. 2009 IN Boshoff & Du Plessis, 2009:274-277; Kotler et al. 2010:436-438).

- Empowerment is a firm strategy implemented to give employees more responsibility and authority to make decisions and control work processes (Longenecker, Moore, Petty & Palich 2006:362; Schreuder & Theron 2001:6).

- According to Brink and Berndt (2004:36) and Peppard (2000:322), personalisation occurs when a firm develops or tailors its offerings to satisfy unique client needs.

- Ethics refer to the set of moral principles that determine human behaviour (Stevenson 2005:4) and therefore a firm's ethical behaviour refers to its degree of conforming to acceptable standards of behaviour (Joyner & Payne 2002:299; McDonald & Leppard, 1990:27) and its level of social responsibility (Longenecker et al. 2006:31). In the case of services rendered, such as banking services, the price charged to the client is often called the fee, rent, tariff, fare, premium or rate (Mostert, P. 2009 IN Boshoff & Du Plessis, 2009:143-144).

- Hoffman and Bateson (2006:269) define technology as the level of automation a firm utilises.

As this study focuses on how the above variables could influence the relationship marketing and customer retention of banks, it is important to discuss the South African banking industry.

2.2 THE SOUTH AFRICAN BANKING INDUSTRY

The South African banking industry is generally regarded as a strong, stable industry. The country's banking system has relatively well developed regulatory, legal and accounting infrastructures and is well regulated by the South African Reserve Bank (SARB) (Kemp 2002:1; Van den Berg 2009:12). The 2008 press release by FinScope revealed that the sophisticated South African banking industry is allowing the country to become a more financial inclusive society (Finscopeb 2008:1,4). The industry comprises of a few large, financially strong banks as well as a number of smaller banks. The four major banks control 84% of the total South African banking market and include Amalgamated Banks of South Africa Group Limited (ABSA), FirstRand Holdings Limited (FNB), Nedcor Limited (Nedbank) and Standard Bank Investment Corporation Limited (Standard Bank) (South African Reserve Bank 2008:55). In total 46 foreign banks have offices in the country. At the end of 2009, 150 619 people were employed in the South African banking industry (Banking Association of South Africa 2010:7).

However, because it is operating in a developing country, the South African banking industry faces many challenges: globalisation and the pressure to internationalise (Metcalfe 2009:24,26; Whitfield 2006:13); an increasingly competitive business environment (Ashton 2009) with new entrants, for example African Bank and Capitec, and foreign banks (Metcalfe 2009:6); devaluations of banks' shares (Duncan 2008:1; Harris 2008:13; Nedbank 2008:1; Whitfield 2008:20); government intervention resulting in increased obligations and regulations (Metcalfe 2009:21,24,26; Whitfield 2006:12) and technological advancements in the industry (Metcalfe 2009:16,24,26).

South African banks also face challenges such as competing for the more than 40% of the population that is un-banked (Finscopea 2009:4; Okeahalam 2008:1131), thus not currently making use of banking services; changing client behaviour (Fin24 2007:1); and the continuous enquiries about their banking fees (Mittner 2008:8; Nyamakanga 2007:1; Whitfield 2009:47). Following the above discussion, it is evident that a focus on relationship marketing and customer retention may be beneficial and contribute to the competitiveness and survival of South African banks.

3 OBJECTIVES AND HYPOTHESES

The primary objective of the research was to consider the current relationship marketing focus areas of banks, as viewed by bank managers. In addition, based on managers' viewpoints, the influence of relationship marketing on banks' customer retention was investigated. The aim was to gain insights from bank managers on the relationship marketing aspects important to banks when focusing on client relationships. In order to obtain the primary objective, firstly an extensive literature overview on relationship marketing and customer retention in South African banks was conducted. Secondly, an empirical investigation among bank managers was conducted to provide banks with relationship marketing and customer retention strategies as recommendations, based on the current perceptions of bank managers.

Therefore, a number of hypotheses were constructed based on the relationship marketing and customer retention knowledge obtained from the introduction and literature overview. In addition, a previous relationship marketing and customer retention study among banking clients by Rootman (2011:35,36) was consulted to construct the hypotheses for this bank manager study. Six hypotheses were constructed to determine whether relationships exist between each of the independent variables (communication, empowerment, personalisation, ethical behaviour, fees and technology) and the intervening variable (relationship marketing):

H1: A relationship exists between communication and relationship marketing, as perceived by bank managers.

H2: A relationship exists between empowerment and relationship marketing, as perceived by bank managers.

H3: A relationship exists between personalisation and relationship marketing, as perceived by bank managers.

H4: A relationship exists between ethical behaviour and relationship marketing, as perceived by bank managers.

H5: A relationship exists between fees and relationship marketing, as perceived by bank managers.

H6: A relationship exists between technology and relationship marketing, as perceived by bank managers.

One hypothesis was constructed to examine whether a relationship exists between the intervening (relationship marketing) and dependent (customer retention) variables:

H7: A relationship exists between relationship marketing and customer retention, as perceived by bank managers.

4 RESEARCH METHODOLOGY

In order to gather the viewpoints of South African bank managers, the quantitative or positivistic research methodology was followed to satisfy the problem statement and research objectives of this study. A "positivistic paradigm" is a research philosophy that is associated with deductive reasoning, which has been adopted from the natural sciences (Collis & Hussey 2009:85; Saunders, Lewis & Thornhill 2009:146). The quantitative research method was used, as the study's focus was on testing the hypotheses, as well as on analysing and interpreting the gathered data quantitatively (Burns & Burns 2008:14-19; Neill 2007:1).

Both primary and secondary sources were used to collect information on banks and relationship marketing as well as customer retention aspects and strategies. For the empirical investigation, a self-developed measuring instrument in the form of a structured questionnaire was distributed to branch managers of banks throughout South Africa. The purposive or judgemental non-probability sampling technique (Zikmund 2003:382) was used, as the major banking groups agreed to distribute the questionnaire to their manager databases. In addition, snowball sampling was used as managers were encouraged to forward the questionnaire to other managers in the industry. Sections 1 - 9 were in the format of a seven-point Likert-type scale ranging from 'strongly disagree' (1) to 'strongly agree' (7) and gathered information on bank managers' viewpoints regarding relationship marketing and customer retention. Section 10 gathered biographical data of the respondents and their employer banks.

The Microsoft Excel, Statistica (Version 9) and AMOS (Version 18) computer programs were used to statistically analyse the gathered data in three phases:

- Firstly, the data analysis consisted of performing various descriptive statistics to summarise the sample data;

- Secondly, structural equation modelling (SEM) was conducted in order to measure the goodness-of-fit of the data to the model. This was done by imposing the banking client model of a preceding study (Rootman 2011:300) on the bank manager data set of this study. Five goodness-of-fit indices were used, namely the normed chi-square (x2/df), Root mean squared error of approximation (RMSEA), Comparative fit index (CFI), Tucker-Lewis index (TLI) and Parsimony goodness-of-fit index (PGFI); and

- During the third and final data analysis step, the existence of the hypothesised relationships was tested by evaluating the point and interval estimates of the parameters from the SEM procedure. In addition, the variable mean scores of the bank manager respondents were interpreted.

It should be noted that the validity and reliability of the measuring instrument used in this study were confirmed by the preceding study by Rootman (2011:309-312). Cronbach Alpha correlation coefficients of higher than the recommended 0.7 cut-off (Nunnally & Bernstein 1994:264-265) were obtained for each of the variables. Due to this preceding study, the validity and reliability results are not reported in this study.

5 EMPIRICAL RESULTS

In the section that follows, the empirical results will be discussed in the same order as the data analysis steps provided above. Table 1 illustrates the descriptive statistics (both frequencies and percentages) of the biographical data of the bank manager respondents.

The majority of the 67 bank manager respondents were male (56.72%; η = 38) and from the European ancestry population group (62.69%; η = 42). Most bank manager respondents belonged to the middle age groups of between 35 and 44 years (43.28%; η = 29) and between 45 and 55 years (34.33%; η = 23). The majority of the respondents were educated with a tertiary qualification (86.57%; η = 58). A small 8.96% (n = 6) of the bank manager respondents only had secondary school education. For confidentiality reasons the question relating to the employer bank of the managers was not compulsory to answer. Therefore, 13 managers (19.40%) did not answer this question. Most of the remaining managers were employed by ABSA (26.87%; η = 18) and FNB (40.30%; η = 27). On average, bank managers have been employed in the banking industry for approximately 18 years.

During the SEM analysis phase the researcher imposed the same structure or model from this study's preceding study, on the relationship marketing perceptions of banking clients (Rootman 2011:300), on this study's bank manager dataset to determine whether or not the data fits the model adequately. This Imposed Bank Managers' Model is presented in Figure 1.

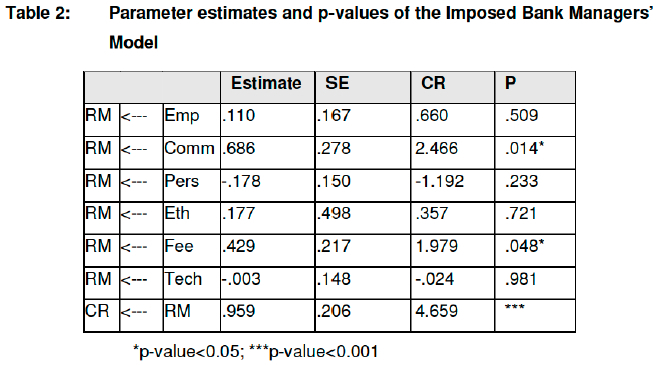

Table 2 provides the parameter estimates, standard errors and p-values of the Imposed Bank Managers1 Model.

The bank managers' model shows three significant relationships between the factors. The significant relationships are between two of the independent variables, namely communication and fees, and the intervening variable, relationship marketing. In

addition, a significant relationship exists between relationship marketing (the intervening variable) and customer retention (the dependent variable). Based on these results, the following hypotheses are accepted: H1, H5 and H7. As a result the researchers fail to accept the hypotheses H2, H3, H4 and Η6. The results of the goodness-of-fit indices for the Imposed Bank Managers' Model, as shown in Table 3, indicate that the model fit could improve.

As shown above, the SEM indices indicate a poor fit for the Imposed Bank Managers' Model. Therefore, a second model was derived for the managers' dataset by removing all the insignificant factors from the Imposed Bank Managers' Model. This Adapted Bank Managers' Model is presented in Figure 2.

Table 4 provides the parameter estimates, standard errors and p-values of the Adapted Bank Managers' Model.

The Adapted Bank Managers' Model shows no insignificant relationships between factors. Table 5 presents the results of the goodness-of-fit indices for the Adapted Bank Managers' Model. It is evident that the Adapted Bank Managers' Model is a noticeable improvement on the Imposed Bank Managers' Model. All parameters are significant, all indices are improved and the PGFI for the Adapted Bank Managers' Model is larger than that of the Imposed Bank Managers' Model. However, most of the SEM indices do not meet the minimum acceptance criteria. Therefore, it has to be said that the final model for the bank managers (Adapted Bank Managers' Model), although showing significant relationships between factors, is not a reasonably good fit.

This, however, was anticipated by the researchers as it was expected that bank managers would be a biased sample. Bank managers might feel obligated to their employer banks to project positive views on all matters pertaining to their employer banks' client relationships and customer retention strategies. The results are potentially skewed to give favourable responses, as bank managers possibly provided positive results for their employer banks, even if they personally might not agree. Table 6 lends support to this by providing the bank managers' mean scores for each factor relating to relationship marketing and customer retention.

The mean scores in Table 6 indicate overwhelmingly positive responses from the respondents. All the means are above the value of 5, and thus showing bank managers tend to agree and lean towards strongly agreeing that their employer banks focus on communication, empowerment, personalisation, ethical behaviour, justifiable fees and the use of technology. In addition, bank managers are agreeing that their employer banks have good bank-client relationships (mean = 5.522) and sufficient customer retention rates (mean = 5.134).

The question is: Do banking clients have the same views regarding their banks' focus on relationship marketing and customer retention aspects? According to the study by Rootman (2011), this is not the case: banking clients and bank managers have different views regarding banks' relationship marketing and customer retention aspects. This study shows that bank managers are much more positive regarding their banks' application of the relationship marketing and customer retention aspects. Banking clients from the Rootman (2011:327,344) study have more negative responses on their banks' relationship marketing and customer retention performances.

There is also a difference in the factors regarded as important by banking clients and bank managers. According to Rootman (2011:317), banking clients rank fees, ethical behaviour and personalisation as important aspects influencing relationship marketing. This study shows that bank managers only view communication and fees as factors significantly influencing relationship marketing. Based on these findings, another question arises: How can bank managers understand the views of banking clients as well as align their banks' strategies with banking clients' relationship marketing and customer retention needs?

6 CONCLUSION AND RECOMMENDATIONS

The literature overview presented in this article and the empirical investigation of this study have led to the formulation of relationship marketing and customer retention recommendations for banks, based on the perceptions of their managers. The empirical findings showed that bank managers regard communication and fees as the most important variables influencing client relationships, however the previous study (Rootman 2011:317) has shown that many other variables are also applicable, based on banking clients' perceptions. This emphasises the need for banks to align their managers' viewpoints and focus areas with those of clients to ensure the satisfaction of clients' needs and expectations. In other words, together with the preceding study, the answer was negative to the following question: Do banking clients have the same views regarding their banks' focus on relationship marketing and customer retention aspects?

In addition, this study's findings provided another relationship marketing question that should be answered in future related studies, namely: How can bank managers understand the views of banking clients as well as adapt their banks' strategies to adhere to banking clients' relationship marketing and customer retention needs?

The two questions above lead to a number of recommendations. Firstly, banks should regularly conduct surveys, such as customer satisfaction surveys, to determine the most important banking aspects for clients' and their level of satisfaction with the bank's client relationships. This does not only refer to short surveys requesting clients to briefly rate their banks' service. More in-depth or detailed questions concerning banks' relationship marketing efforts should be posed to clients. Informal focus group sessions should be held between bank managers and valued clients to stay abreast of client concerns and needs. Bank websites should have facilities where clients can pose questions, raise concerns and provide suggestions concerning bank-client relationships. These website comments from clients should be responded to in a limited time to provide immediate feedback and relevant action by banks. Another strategy for bank managers to employ, to identify the most important client relationship aspects, is to benchmark their banks against other leading banks.

Based on the results of this study and the preceding study by Rootman (2011:315), fees are the only variable according to both managers and clients that influences banks' relationship marketing. Thus, for bank management it is important to investigate bank fees and changes in fee structures more regularly. For example, clients should be well informed about increases in fees in advance, and if necessary, the increases in fees should be explained or justified to clients. Differences in fee structures for different client groups should be well communicated and reasons for these differences should be understood by clients to ensure that they feel fairly treated. In addition, instead of all major banks charging similar fees for the same banking products and/or services, fees could be used as a variable by banks to sustain a competitive advantage. Thus, banks can charge fees significantly different to those of their competitors.

In future studies the geographical reach could expand by including bank managers in other countries, for example the bank managers employed in Canada, the country often regarded as the one with the most successful banks worldwide in terms of relationship marketing (Cole 2009:1, Ptak 2001:38, Skousen 2009:1). It is evident that this article provides evidence that bank managers and clients often have different relationship marketing views and banks should adjust their institutions' focus areas according to those of clients to better satisfy clients' banking needs. Instead of only focusing on their bank's communication and fees, managers should identify and focus on relationship marketing variables important to clients. This article's recommendations will lead to improved bank management, increased banking client satisfaction and overall more successful banks.

REFERENCES

ACKERMANN P.L.S. & VAN RAVESTEYN. L.J. 2005. Relationship marketing: The effect of relationship banking on customer loyalty in the retail business banking industry in South Africa. Southern African Business Review, 10(3):149-167. [ Links ]

ASHTON M. 2009. Footprint frustrates Nedbank. [Internet: http://www.fin24.com; downloaded 2009-09-03. [ Links ]]

BAKER P.S. 2007/2008. Customer retention and the value of mortgage-servicing rights. Bank Accounting and Finance, December 2007-January 2008:35-38. [ Links ]

BANKING ASSOCIATION OF SOUTH AFRICA. 2010. South African banking sector overview. [Internet: http://www.banking.org.za/getdoc/getdoc.aspx?docid=1130; downloaded 2011 -06-21. [ Links ]]

BARON S. & HARRIS K. 2003. Services marketing: Texts and cases. New York: Palgrave. [ Links ]

BEJOU D., ENNEW C. T. & PALMER A. 1998. Trust, ethics and relationship satisfaction. International Journal of Bank Marketing, 16(4):170-175. [ Links ]

BERGERON J., ROY J. & FALLU J. 2008. Pleasantly surprising clients: A tactic in relationship marketing for building competitive advantage in the financial services sector. Canadian Journal of Administrative Sciences, 25:171-184. [ Links ]

BOSCH J., TAIT M. & VENTER E. 2011. Business management: An entrepreneurial perspective. Port Elizabeth: Lectern Publishing. [ Links ]

BOSHOFF C. & DU PLESSIS F. Services marketing: A contemporary approach. Lansdowne, Cape Town: Juta & Company. [ Links ]

BRINK A. & BERNDT A. 2008. Relationship marketing and customer relationship management. Lansdowne, Cape Town: Juta & Company. [ Links ]

BRUHN M. & GEORGI D. 2006. Services marketing: Managing the service value chain. England: Pearson Education. [ Links ]

BURNS R.B. & BURNS R.A. 2008. Business research methods and statistics using SPSS. London: Sage Publications. [ Links ]

BUTTLE F. 2004. Customer relationship management: Concepts and tools. Oxford: Butterworth-Heinemann. [ Links ]

CHEN Y. & XIE J. 2008. Online consumer review: Word-of-mouth as a new element of marketing communication mix. Management Science, 54(3):477-491. [ Links ]

CHIPUNZA C. 2008. A comparison of perceptions of loyalty between bank tellers and internal customer groups in a retail bank in South Africa. The Service Industries Journal, 28(2):139-149. [ Links ]

CLARK M. 2002. The relationship between employees' perceptions of organizational climate and customer retention rates in a major UK retail bank. Journal of Strategic Marketing, 10:93-113. [ Links ]

COLE R. 2009. Canadian banking: Sober, boring, and successful. [Internet: http://www.investmentu.com/2009/June/canadian-banking.html; downloaded 2010-06-18. [ Links ]]

COLGATE M., STEWART, K. & KINSELLA R. 1996. Customer defection: A study of the student market in Ireland. International Journal of Bank Marketing, 14(3):23-29. [ Links ]

COLLIS J. & HUSSEY R. 2009. Business research: A practical guide for undergraduate and postgraduate students. 3rd edition. New York: Palgrave Macmillan. [ Links ]

DUNCAN F. 2008. Whither the banking industry? [Internet: www.moneyweb.co.za/mw/view/mw/en/page38?oid=235622&sn=Detail; downloaded on 2009-02-10. [ Links ]]

EID R. 2007. Towards a successful CRM implementation in banks: An integrated model. The Services Industries Journal, 27(8):1031-1039. [ Links ]

ELLIOTT T. 2009. Integrated service marketing communications. In BOSHOFF C. & DU PLESSIS F. (eds). Services marketing: A Contemporary approach. Lansdowne, Cape Town: Juta & Company. [ Links ]

FARQUHAR J.D. 2003. Retaining customers in traditional retail financial services: Interviewing "les responsables". International Review of Retail, Distribution and Consumer Research, 13(4), October, p. 393-404. [ Links ]

FIN24. Crime tops banks' fear list. [Internet: http://www.fin24.com/Business/Crime-tops-banks-fear-list-20070619; downloaded 2009-09-02. [ Links ]]

FINSCOPEa. Finscope South Africa. [Internet: http://www.finscope.co.za/documents/2009/Brochure_SA09.pdf; downloaded 2010-06-11. [ Links ]]

FINSCOPEb. Banking comes to more people. [Internet: http://www.finscope.co.za/documents/2009/PRFS08_banking.pdf; downloaded 2010-06-11. [ Links ]]

GRÖNROOS C. 1994. From marketing mix to relationship marketing: Towards a paradigm shift in marketing. Management Decisions, 32(2):4-20. [ Links ]

HARRIS S. 2008. Small beer, big on potential: Except for a few oddities. Finweek, 22 May, p. 13. [ Links ]

HOFFMAN K.D. & BATESON J.E.G. 2006. Services marketing: Concepts, strategies and cases. 3rd edition. USA: Thomson South-Western. [ Links ]

JOINER B.L. 1994. Fourth generation management: The new business consciousness. New York: McGraw-Hill. [ Links ]

JONES M.A., MOTHERSBAUGH D.L. & BEATTY S.E. 2000. Switching barriers and repurchase intentions in services. Journal of Retailing, 76(2):259-297. [ Links ]

JOYNER B.F. & PAYNE D. 2002. Evolution and implementation: A study of values, business ethics and corporate social responsibility. Journal of Business Ethics, 41 (4):297-311. [ Links ]

KARAKOSTAS B., KARDARAS D. & PAPATHANASSIOU E. 2005. The state of CRM adoption by the financial services in the UK: An empirical investigation. Information & Management, 42:853-863. [ Links ]

KEMP S. 2002. Banks still facing new challenges. [Internet: http://m1.mny.co.za/twshr.nsf/0/C2256ADB0022EC2F42256C22002FCA28?OpenDocument; downloaded 2004-02-24. [ Links ]]

KOTLER P., ARMSTRONG G. & TAIT M. 2010. Principles of marketing: Global and Southern African perspectives. Cape Town: Pearson Education. [ Links ]

LAGES C., LAGES, C.R. & LAGES L.F. 2005. The RELQUAL scale: A measure of relationship quality in export market ventures. Journal of Business Research, 58:1040-1048. [ Links ]

LONGENECKER J.G., MOORE, C.W., PETTY, J.W. & PALICH L.E. 2006. Small business management: An entrepreneurial emphasis. China: Thomson South-Western. [ Links ]

MCDONALD M.H.B. & LEPPARD L.W. 1990. To sell a service: Guidelines for effective selling in a service business. Oxford: Heinemann Professional Publishing. [ Links ]

MENON K. & O'CONNOR A. 2007. Building customers' affective commitment towards retail banks: The role of CRM in each 'moment of truth'. Journal of Financial Services Marketing, 12(2):157-168. [ Links ]

METCALFE B. 2009. Strategic and emerging issues in South African banking. Johannesburg: PricewaterhouseCoopers. [ Links ]

MITTNER M. 2009. Kenners maan oor gerugte dat Barclays Absa wil smous. Die Burger, 26 January, pp. 26. [ Links ]

MOSTERT P. 2009. The pricing of services. In BOSHOFF C. & DU PLESSIS F. (eds). Services marketing: A Contemporary approach. Lansdowne, Cape Town: Juta & Company. [ Links ]

MUDIE P. & COTTAM A. 1999. The management and marketing of services. 2nd edition, Oxford: Butterworth-Heinemann. [ Links ]

NEDBANK. Nedbank Group Annual Report. 2008. [Internet: http://www.nedbankgroup.co.za/financials/Nedbank_ar08/o/focus-areas-for-2009.asp; downloaded 2010-02-17. [ Links ]]

NEILL J. 2007. Qualitative versus quantitative research: Key points in a classic debate. [Internet: http://wilderdom.com/research/QualitativeVersusQuantitativeResearch.html; downloaded 200903-29. [ Links ]]

NO AUTHOR. Customer relationship management benefits. [Internet: http://www.info-electronics.com/en-crm-home.htm; downloaded 2004-11-02. [ Links ]]

NUNNALLY J.C. & BERNSTEIN I.H. 1994. Psychometric theory. 3rd edition. New York: McGraw-Hill. [ Links ]

NYAMAKANGA R. 2007. "Big four" banks join battle over fee cuts. Business Day, 24 May, p. 1. [ Links ]

OKEAHALAM C. 2008. Client profiles and access to retail bank services in South Africa. Applied Financial Economics, 18:1131-1146. [ Links ]

PEPPARD J. 2000. Customer relationship management in financial services. European Management Journal, 18(3):312-327. [ Links ]

PTAK L. 2001. Measuring client value. CMA Management, June:38-40. [ Links ]

REICHHELD F.F. 1996. Learning from customer defections. Harvard Business Review, March/April:56-69. [ Links ]

ROOTMAN C. 2011. An international comparative study on the relationship marketing and customer retention of retail banks: lessons for South Africa. Unpublished Doctoral Thesis, Nelson Mandela Metropolitan University, Port Elizabeth. [ Links ]

ROOTMAN C. 2006. The influence of customer relationship management on the service quality of banks, Unpublished Masters Dissertation, Nelson Mandela Metropolitan University, Port Elizabeth. [ Links ]

SAUNDERS M., LEWIS P. & THORNHILL A. 2009. Research methods for business students. 5th edition, England: Pearson Education. [ Links ]

SCHREUDER M.G. & THERON A.L. 2001. Careers: An organizational perspective. Lansdowne, Cape Town: Juta & Company. [ Links ]

SKOUSEN M. 2009. Canadian banks: An oasis of financial calm. [Internet: http://www.investmentu.com/2009/February/canadian-banks.html; downloaded 2010-06-18. [ Links ]]

SOUTH AFRICAN RESERVE BANK. 2008. Annual economic report. Government Communications (GCIS), Pretoria. [ Links ]

STEVENSON J. 2005. The complete idiot's guide to philosophy. 3rd edition. London: Alpha. [ Links ]

SWARTZ T.A. & IACOBUCCI D. 2000. Handbook of services marketing and management. Thousand Oaks: Sage Publications. [ Links ]

VAN DEN BERG S. 2009. SA banke vaar goed. Die Burger, 23 February, p. 12. [ Links ]

WALSH S., GILMORE A. & CARSON D. 2004. Managing and implementing simultaneous transaction and relationship marketing. International Journal of Bank Marketing, 22(7):468-483. [ Links ]

WHITFIELD B. 2009. Differentiating its offerings: Nedbank gambles the wealthy will pay more. Finweek, 23 April 2009, p. 47. [ Links ]

WHITFIELD B. 2008. ABSA cuts management jobs. Finweek, 10 July 2008, p. 20. [ Links ]

WHITFIELD B. 2006. Local stays lekker: But some banks reaching outside the lucrative home market. Finweek, 30 March 2006, p. 12-14. [ Links ]

WILMSHURST J. & MACKAY A. 2002. The fundamentals and practice of marketing. 4th edition. Oxford: Butterworth-Heinemann. [ Links ]

ZIKMUND W.G. 2003. Business research methods. 7th edition. USA: Thomson SouthWestern. [ Links ]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}