Serviços Personalizados

Artigo

Inglês (pdf)

Inglês (pdf)

Artigo em XML

Artigo em XML Referências do artigo

Referências do artigo

Indicadores

Links relacionados

-

Citado por Google

Citado por Google -

Similares em Google

Similares em Google

Compartilhar

Permalink

PermalinkJournal of Contemporary Management

versão On-line ISSN 1815-7440

JCMAN vol.2 no.1 Meyerton 2005

RESEARCH ARTICLES

The planning of key fundamentals used in the development of a beneficial project plan

GC Seager

University of Johannesburg

ABSTRACT

The project plan is an essential part of any project whether it is a micro or macro project. Therefore certain key fundamental issues need to be well planned in advance for the initial development of the project plan. This article will bring these key fundamentals to light and illustrate why each of them is important to the overall successful planning of the project plan and achievement of the end project deliverables and to illustrate the key fundamentals that affect all projects during their initial development of a valuable project plan These fundamentals will be related to a case study project on the Department of Justice and Constitutional Development (DoJ&CD), 'Management of Monies Held in Trust (MMT) project'.

Key phrases: project plan, initial development, achievement of project deliverables

INTRODUCTION

So what is a project? Young (2003:10) believes that a project is something special by its nature and by the fact that it is perceived as being an activity conducted outside of normal operations. Young then defines a project as "a collection of linked activities carried out in an organised manner with a clearly defined start point and finish point, to achieve some specific results (deliverables) that satisfy the needs of an organisation as derived from the organisation's plans".

Writing the project plan provides a structured framework for thinking about how the project will be conducted, and for considering the project risks. Usually, having a comprehensive plan requires the involvement of a range of functional experts, and it often requires the involvement of decision-makers. The significant value of writing a project plan is the process rather than the outcome. It forces stakeholders to think through their approach and make decisions about how to proceed. The project plan provides a vehicle to communicate to the various stakeholders, and describes the roles and responsibilities of those various stakeholders. The project plan should also specify what the project needs to accomplish (the deliverables), as well as how, when, by whom and for how much. Large complex projects may have many other separate plans that make up the project plan, i.e. risk planning, quality plan and stakeholders lists amongst others (Chapman 1997:Internet). The fundamentals are those aspects that need to be taken into consideration and planned for, before a beneficial project plan can be drawn up, and include:

· project scope

· stakeholders

· risk assessment

· resources planning

· budget/cost management

The planning of a project is essential for two reasons according to Dobson (2003:43). Firstly, the environment in which the project will take place is never completely predictable. The environment has many uncertainties in the situation, resources, other demands and emergencies. Secondly, the project itself carries inherent uncertainty with regard to the stakeholders. Does everyone see the project the same way? Do people seek the same outcome? "No matter how well or carefully you plan, you should never act on the assumption that you have thought of everything, and that nothing outside your carefully conceived universe will interfere".

DESCRIPTION OF PROJECT

The Management of monies held in trust (MMT) project was established with the objective of establishing financial management in compliance with the Public Finance Management Act (PFMA). The Department of Justice and Constitutional Development (DoJ&CD) receives approximately R2bn in trust monies (Bail, Child Maintenance, Fines, Estates and Guardians Fund transactions) per annum through its Lower Court Cash Halls countrywide. These funds are considered unauditable. Fraud and corruption is widespread because of a largely manual, paper-based transaction environment that is rife of human mistakes. Cash Halls lack the security required to protect the monies and staff, as well as the systems required to accurately account for these financial transactions. Service delivery remains unacceptable and is largely limited to the physical presence of beneficiaries at their Court/point jurisdiction (Mackenzie 2004:9).

The DoJ&CD is looking to outsource their financial and transaction sector to banks, retailers and the South African Post Office who currently offer account and nonaccount transactional payment facilities to manage transactions in a more efficient and convenient manner through a Public Private Partnership (PPP). The DoJ&CD will authorise certain banks, retailers ("receiving and payment agents") and the South African Post Bank so that the MMT Private Sector Service Provider can transact through these enabling service providers. As a result, all beneficiaries will in future be able to collect their maintenance from a DoJ&CD recognized agent - a convenient retail store, bank or post-office instead of being restricted to their court of jurisdiction.

It is therefore suggested that the DoJ&CD closes all Cash Halls for the receipt and payment of monies held in trust. Therefore, all infrastructure required to implement the proposed solution is to be provided by the Private Sector. All MMT cash transactions and associated risks are therefore managed by the Private Sector within an existing infrastructure that is a far more secure payment system than the Public Sector can justify building. This suggested way forward should provide effective and timeously reporting as well as audit trail functionality that is required to overcome the financial control defects that currently exist in the management of monies in trust (Mackenzie 2004a:4-5).

Public Private Partnership (PPP)

A Public Private Partnership (PPP) is the joining forces and capabilities of a public organisation with a private entity. The PPP enables both parties to meet their respective obligations in order to deliver the objectives outlined in the agreement. The agreement involves building a good working relationship between the public and private parties, and requires continuous effort throughout the project term to make the project a success. The PPP must be managed proactively to anticipate future needs as well as reacting to unforeseen situations. The central aim of the PPP agreement is to ensure ongoing affordability, value for money and appropriate risk transfer (Mackenzie 2004c:4). The partnership between the DoJ&CD and the private party, should seek to optimise the effectiveness of the service deliverables and balancing of the associated costs and risks.

PROJECT SCOPE

The planning process starts with a clear understanding of what the particular need is, and must be reflected in the project scope. The better the definition and clarity of the project scope, the more complete the planning process will be (Steyn et al. 2003:170). When it comes to defining the project, all the relevant specifications must be collected and put together in the project scope of work statement (SOW) also known as the project chart (Young 2003:108). The scope of the project must include a narrative description of the project's detailed objectives, giving more information about each deliverable and benefit identified as well as a list of requirements that need to be met. If the scope is not properly defined and in detail, others might attempt to shift their scope onto the project, which is a fundamental condition for causing 'scope creep'. A well defined initial project scope is critical to managing scope creep later on in the project (Dobson 2003:134).

To uncover hidden scope issues, the project's assumptions and constraints should be listed. An assumption is something taken for granted as being true or certain without a factual basis. A constraint is a factor that limits or restricts the performance of the project (Dobson 2003:136). The scope must also identify the boundary limits of the project, clearly stating what is not going to be done as part of the project (Young 2003:108). It should also state the end-point of the project (Orwig & Brennan 2000:5). The scope statement should be considered to be a baseline and SMART: Specific; Measurable; Agreed; Realistic; Time-Bound (Steyn et al. 2003:66).

DELIVERABLES AND OBJECTIVES OF THE PROJECT

The key deliverable for the MMT project is to eliminate trust money cash handling at cash halls throughout South Africa. To accomplish this specific deliverable requires the project to meet the following objectives:

· enable focus on core functions within the courts and masters offices by outsourcing non-core functions;

· eliminate cash handling by departmental officials;

· ensure appropriate security and systems infrastructure for cash halls;

· develop and implement a general customer enquiry capability (call centre);

· attract appropriate private sector skills to assist the department in addressing challenges associated with MMT;

· automate, where possible to maximise efficiency, internal control, financial and management reporting within as short a timeframe as possible.

(Mackenzie 2004a:10)

As well as the objectives, the DoJ&CD needs that should be clarified in the project scope statement include the following (Mackenzie 2004b:9-11):

■ auditable records

■ integration with existing technical infrastructure

■ defined accountability

■ centralised, electronic MMT record keeping (data warehouse)

■ elimination of cash handling

■ reduction of foot traffic at court level

■ reduction and elimination of paper, cash management and manual processes;

■ ability of DoJ&CD staff to focus on core activities (legal process)

■ balanced approach to servicing rural and urban customers

■ reduction of fraudulent activities

■ improved security around cash hall processes

CONSTRAINTS AND ASSUMPTIONS OF THE PROJECT

The constraints of the project include the magnitude of the project, the geographic spread of the cash halls as well as the time and resource constraints. The funding plan and funding assumptions schedule identifying all sources, amounts and application of finance, conditions, terms, base costs, margins and fees (Mackenzie 2004b:45). The meeting of the MMT objectives and needs defined above are non-negotiable for those tendering for the project.

Stakeholders planning

The project stakeholders are those individuals and organizations that are actively involved in the project, or whose interests may be affected as a result of the project's execution or project completion.

Stakeholders may also apply influence over the project and its results. The project manager must identify the stakeholders, determine their requirements and manage their influence in relation to the requirements to ensure a successful project (PMBOK 2004:23). Stakeholders may have hidden agendas about what they expect from the project and these expectations need to be exposed before the project is defined (Young 2004:60).

Stakeholders can take on different names and categories, namely internal and external. Anyone inside the organisation who potentially has an interest in the project is an internal stakeholder. External stakeholders are outside of the organisation and generally expecting to gain work or benefits from the project.

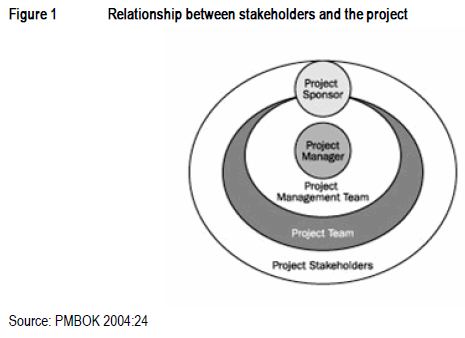

Examples of external stakeholders include suppliers, contractors, consultants and possibly government departments (Young 2004:59-60). Figure 1 illustrates the relationship between the stakeholders that have been identified within the project. It shows how the project manager is at the centre of the project and is surrounded by his project team.

The internal stakeholders surround the project manager and his team. The external stakeholders surround the entire project. The project sponsor also surrounds the project and has an overview the entire project.

Stakeholders will have varying levels of responsibility and authority when participating on a project. These can range from occasional contributions in surveys and focus groups to full project sponsorship by providing financial and political support. Stakeholders who ignore this responsibility can have a damaging impact on the project objectives. Sometimes, stakeholder identification can be difficult (PMBOK 2004:24). Therefore it is important to identify all stakeholders so that this problem can be controlled effectively and avoid problems later in the project. This planning stage should not be taken lightly.

Key stakeholders of the project

The following constitute the key stakeholders of the project:

■ project manager: the individual responsible for managing the project;

■ customer/end-user: the individual or organisation that will use the project's product;

■ performing organisations: the enterprises whose employees are most directly involved in doing the work of the project;

■ project team members: the group that is performing the work of the project;

■ sponsor: the individual or group that provides the financial resources, in cash or in kind, for the project (PMBOK 2004:24).

Therefore the stakeholders that have been identified for the MMT Project should be listed on a project stakeholder list as found in Young (2003:105). The executive sponsor for the project is the CFO (Chief Financial Officer) for the DoJ. He represents the needs of the clients and approves the project proposal, authorises expenditure and agrees to the success criteria. The end-customers are those people that will benefit from the output of the project. They are generally those people that travel extensively to the courts to receive their maintenance payments. The improved system should drastically cut down on time and money spent at the courts.

The Project Manager represents the sponsor and manages the project on his behalf. It is necessary to manage the project so that it achieves its objectives on time, within budget, and according to the requirements. It is also his duty to lead and motivate the team members. The team members are various. They contribute their specific skills and abilities to the project. The various team members represent their functional departments in the project and accept the leader of the project as manager within the scope of the project. The performing organisation is the DoJ&CD, whose employees are mostly involved in the project. Other stakeholders include the banks and other institutions that will be tendering as well as the post-office.

Identifying stakeholders is not only a start-up activity, because unidentified stakeholders may not appear until later in the project. Therefore it is important to regularly review the stakeholders list. Project managers must manage stakeholder expectations, which can be difficult, because stakeholders often have very different or conflicting objectives (Young 2004:61).

In any Public Private Partnerships, all stakeholders have a vital interest in the quality of the service to be provided. Specifically, the DoJ&CD retains overall responsibility for the service delivered through the PPP. The private party relies on the quality of the products and services provided by consortium members, personnel, subcontractors and suppliers to meet the specifications. Lenders need to be assured that the service will be sufficient to continuously earn the unitary payment (and by so doing service debt). Users of the service must be provided with a quality that meets their requirements (Mackenzie 2004b:31).

RISK ASSESSMENTS

"Everything that can go wrong, will!" - Murphy's Law

What is risk in terms of project planning? Risk is defined as any uncertain event that, if it occurs, could prevent the project realising the expectations of the stakeholders as stated. A risk only becomes a reality if it is not assessed properly and then managed. Success is dependent on maintaining a high commitment to risk management procedure throughout the project. At the planning stages of the project a valid initial risk assessment should be conducted.

Two fundamental types of risks (Young 2004:110) are always present;

■ project risk: associated with the technical aspect of the work to achieve the required outcomes.

■ process risk: associated with the project process, procedure, tools and techniques used, controls, communication, stakeholders and team performance.

Risks can have specific types of impacts on the project, namely to delay the project (time risk), threaten to increase incorrect use of funds and other resources (cost risk), or to degrade the quality or functionality of the deliverables as well as the scope of the project (performance risk). The project manager therefore needs to plan for the overall project risks. Firstly, all the potential risks of the project need to be identified. Secondly, assess the probability and impact to determine which risks require acting on. Thirdly, a potential response, either preventive or corrective actions, needs to be developed for those risks. Lastly, implement the plans that have been developed (Dobson 2003:226-230).

Project teams therefore need to hold planning meetings to develop the Risk Management Plan. Attendees at these meetings should include the project manager, the project team leaders, as well as anyone in the organization with responsibility to manage the risk planning. Basic plans for conducting the risk management activities are defined in this meeting. Risk responsibilities will be assigned. Risks should be categorised and defined by the levels of risk probability (likelihood that a risk will occur) by type of risk and impact by type of objectives. The outputs of these activities will be summarized in the Risk Management Plan (PMBOK 2004:187).

Main project risks

Relating the risk element to the MMT project, outsourcing to the public sector, essentially passes on a significant element of the risk. However, the department still retains certain risks. This is due to the cash halls' responsibilities and the risk relating to the operating systems within the courts. Three main risks have been identified.

■ Service Level Agreement Management: The services provided by the private sector will be managed in terms of the Service Level Agreement. The monitoring and management of this agreement will be expected to take up significant amounts of departmental and private sectors' management time and resources. This is an example of a process risk.

■ Losses due to fraud: The improved controls from outsourcing to the public sector should reduce the risk of fraud. However, fraudulent activities may still be possible in the sectors that are not managed by the public sector. Two examples of fraudulent transactions are; department employees creating false beneficiaries and identification materials i.e. cards and pins could be obtained illegally to gain access to beneficiary's accounts. This is also an example of process risk.

■ Inefficiency due to incorrect or corrupt data: The cash halls will remain the source of data related to new cases. In instances where incomplete or inaccurate data is received, the department will incur additional costs on order to resolve these queries. This will result in the requirement for additional staff to resolve disputed data queries, checking of suspect data and proactive data sampling at the Data Management Agency (Mackenzie 2004b:25)

Other risks are also present, and include inflation assumptions and risk allocation. These risks are reduced and dealt with in certain manners. Inflation risk is shared by setting a common inflation rate to all bidders so to make comparison easier. The risk profile proposed by each bidder in their proposal is tested according to:

■ nature and extent of the risk

■ likelihood of the risk

■ passing down of the risk and obligations assumed by the private party in the PPP agreement to the other key contractors (Mackenzie 2004b:45-48)

MMT risks

During the risk analysis, certain MMT risks were identified, and therefore can be mitigated. The risks identified in the MMT Discussion Document (Mackenzie 2004a:17-19) include:

■ high levels of fraudulent activities

■ cash handling by departmental employees

■ improve audit trails and accountability

■ problem of poor timeously reconciliations

■ risk associated by poor service delivery

■ continual loss of data, back-up and business shortcomings

The PPP introduced additional risk matters that would need to be properly managed:

■ interface risk between the department and private sector service provider;

■ reliant on existing staff to provide information on previous fraudulent activities;

■ reliant on existing staff who may have skills limitations;

■ requirement for detailed contingency planning around system failure/downtime;

■ implementation risk;

Implementation and conversion remains the single largest risk area to the MMT PPP project. If the entire conversion/implementation process is not suitably planned and executed, it will cause a vast and significant interruption and possible failure of the MMT project (Mackenzie 2004a:34).

RESOURCES PLANNING

The process of estimating or planning of resources is a difficult tack because errors are easily made. The organisation and the customer require quality information to determine how long the project will take, what human and other resources the project will consume and how much the project will cost (Dobson 2003:180). Projects are generally constrained by the lack of resources. Therefore there is an important need to manage these limited resources. Human Resource (HR) Management describes the process needed to make the most effective use of the people involved with the project. It consists of human resource planning, acquiring and developing the project team as well as managing the project team processes (PMBOK 2004:11). HR is considered to be the most expensive resource, and the different skills that are required at the different stages of a project need to be planned and coordinated (Steyn et al. 2003:171).

Therefore the project manager should control the assigned project resources to best meet the projects objectives. Activity resource planning is estimating resource requirements for each activity. Planning activity resources involves determining what physical resources (people, equipment, and materials), what quantities of each resource should be used, and when the resource would be available to perform project activities. It must be closely coordinated with cost estimating and availability of those resources (PMBOK 2004:106).

However, the resources that will be needed to successfully implement the project are held by the winning tender for the project. Therefore, before the project can begin, a winning tender must be announced. Once the winning organisation is known, sufficient resources can be planned for.

BUDGET AND COST MANAGEMENT

It is not unusual to spend more time justifying the budget than presenting almost any other aspect of the project. The cost estimate of a project represents the perceived idea of what it will cost to complete the project. The budget, on the other hand, is a request for actual funds or the statement of actual funds available. Cost baseline is a comparison of actual costs to planned costs for the purpose of monitoring. There are a number of different types of project costs, namely direct costs (actual cost of labour, materials etc.) fixed costs (cost not varying with quantity), variable costs and indirect/overhead costs (water and lights) (Dobson 2003: 262-5).

There are certain factors which may influence costs during a project. The project contract can have a huge influence on the cost of a project such as the MMT Project. The nature of the contract can play a role in influencing how costs are calculated and planned for. A cost engineer is a person who has both financial and technical skills. Their responsibility is to monitor both the costs and technical aspects of the project. Projects are time-based activities and therefore the estimate of costs can prove to be very difficult. Projects of long duration are especially susceptible to escalations. Escalation can occur for various reasons i.e. increase pricing of materials, currency fluctuations and labour strikes (Steyn et al. 2003:167-70).

The two best-known approaches to estimating the cost of a project are the 'top-down' and the 'bottom-up' methods.

The top-down method is also known as the analogous estimating method and uses the actual cost of previous similar projects as a basis. The costs derived from this method are carefully escalated in order to arrive at an achievable figure.

The bottom up method estimates the cost of each activity or work pack as determined by the work breakdown structure. Each cost package is added together to arrive at a total figure. However, a disadvantage of this method is that contingencies (unforeseen events) are often included into each activity, leading to excess contingency allowance and increased costs (Steyn et a2003:174).

When planning the budget, care must be taken because once the budget has been finalised, it is difficult to change, even though it is largely based on estimates. It is the responsibility of the financial group to bind the various parts of the budget into an integrated unit. However, it is not the sole responsibility of the financial unit, but also the teams who will carry out the work.

The budgeting process should begin with the establishment of a cost code structure. The process subdivides the activities of the project where costs will be incurred into a meaningful structure for ease of identifying and managing the costs of the project. The budget can only be established when the estimates of the various project costs have been allocated to the various cost codes. The budget should also include at what stage and rate the funds to purchase the resources should be made available. The budget forms the cost baseline of the project and is the tool used to manage the finance of any project (Steyn et al. 2003:176-7).

MMT Budget

The allocated budget for the MMT project is as follows:

2003/04 R10 million

2004/05 R70 million

2005/06 R70 million

2006/07 R70 million plus 6% = R74.2 million

The allocation for MMT is part of the baseline allocation of the department and will remain so until removed. Additional funding is available from sources including interest earnings, bank charge savings, and switch fees on transactions (Mackenzie 2004a:10).

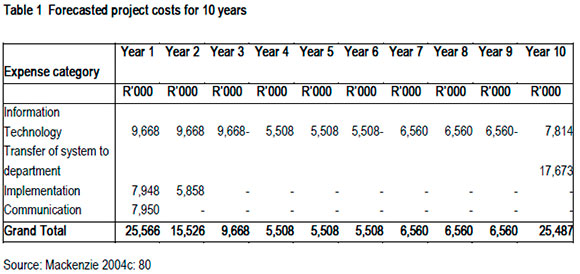

MMT costs

The costs of the project are set out below in table 1. The costs have been divided into four major categories. The costs for the project have been forecasted for the next 10 years.

The IT cost indicates the cost if the equipment were bought once off. The IT equipment cost also includes the cost of the servers and infrastructure. It is assumed that all other IT equipment costs will be paid for by the department. The cost implementation includes all users that will undergo a 5 day system procedural training course and 15 day computer training. A national advertising campaign will communicate the changes as well the benefits of the proposed new system to the users of the MMT system (Mackenzie, Feasibility Study Document 2004: 80-82).

CLOSURE

The article started with an explanatory description of the MMT project undertaken by the DoJ&CD, as well as the meaning of a PPP. The article has introduced a set of fundamental items that need to be well planned for, so that a successful project can be undertaken.

Starting with the project scope, it was shown that a deep understanding of the project is necessary before planning or any other activities have begun. The project scope must also be 'SMART'. It is vital to identify all stakeholders to the project, and make sure all their opinions and requirements have been documented so to avoid complications at the end. Different kinds of risks were identified, with three main risks pertaining to the MMT project.

Resource planning is also necessary, for all involved to know what resources they have at hand and if any additional resources need to be brought in. Lastly, budget and cost planning is vital because the stakeholders will want to know what the project is costing.

The MMT project seems to be well planned out, because they have taken the fundamental aspects of project management and have planned each of those aspects well.

BIBLIOGRAPHY

PMBOK 2004. A Guide to the Project Management Body of Knowledge. Official document of the PMI. 3rd ed. [Internet: http://edulink.rau.ac.za/SCRIPT/05STB08X7/scripts/serve_home; accessed: 28/02/2005]. [ Links ]

CHAPMAN JR. 1997. The project plan. [Internet: http://www.hyperthot.com/pm_plan.htm; accessed: 10/04/2005] [ Links ]

DOBSON MS. 2003 Project management: how to manage people, processes, and time to achieve the results you need. New York: Adams Media. [ Links ]

MACKENZIE A. 2004a. Office of the CFO Management of Monies in Trust (MMT): Discussion Document. August [ Links ]

MACKENZIE A. 2004b. Request for Proposal (RFP) for the Provision of Information Technology infrastructure, systems and services to manage the financial trust money transactions that result from legal process at the Department of Justice and Constitutional Development of the Republic of South Africa. October . [ Links ]

MACKENZIE A. November 2004c. Performance Enhancement Programme (PEP) Progress Report. Pretoria: Department of Justice and Constitutional Development [ Links ]

ORWIG RA & BRENNAN J. 2000. An integrated view of project and quality management for project-based organizations. International Journal of Quality& ReliabilityManagement, 17(4):351-363. [Internet: www.emeraldinsight.com.raulib.rau.ac.za; accessed: 10/03/2005]. [ Links ]

STEYN H, BASSON G, CARRUTHERS M, DU PLESSIS Y, KRUGER D, PROZESKY-KUSCHKE B, VAN ECK S & VISSER K. 2003. Project management: a multi-disciplinary approach. Pretoria : FPM. [ Links ]

YOUNG TL. 2003. The handbook of project management: a practical guide to effective policies and procedures. 2nd ed. London: Kogan Page. [ Links ]