Serviços Personalizados

Artigo

Inglês (pdf)

Inglês (pdf)

Artigo em XML

Artigo em XML Referências do artigo

Referências do artigo

Indicadores

Links relacionados

-

Citado por Google

Citado por Google -

Similares em Google

Similares em Google

Compartilhar

Permalink

PermalinkJournal of Contemporary Management

versão On-line ISSN 1815-7440

JCMAN vol.1 no.1 Meyerton 2004

RESEARCH ARTICLES

An ongoing project audit using control systems

R Macdonald

Siemens Ltd

ABSTRACT

While automatic control systems for projects have been considered over the years, most authors finally realised that "systems do not manage projects, people do." Project auditing requires data; the data needs to be accurate and consistent. This article proposes a method, although rudimentary, for controlling projects by use of cybernetic controls. The feedback loop, while mostly always requiring the intervention of the project manager, facilitates a control mechanism consistent by design. The consistency and ongoing frequent requirement for updates generates the accuracy, consistency and reliability of the data. All too often by the time a post mortem study is done on a project, data has been adjusted to either make the project appear successful or the project manager appear dependable.

The forms developed are proposed in a spreadsheet format allowing for the control and flagging of costs, budgets, orders and resource usage overruns. The process of flagging prompts project manager intervention, and forces timely interaction with the project.

This article adds to recent research done in the development of control boards or dashboards for project monitoring, and adds the possibility for further study in the development of project simulation systems.

Key phrases: automatic control, cybernetic control system, integrated project control, post project control, project auditing

INTRODUCTION

Recent articles on project auditing allude to the fact that projects can be reviewed and or audited in an effort to correct inappropriate practices. It is however felt that corrective action taken on one project may well be the same action that needs correction on another.

It is also appreciated that within the same industry common practices associated with costs controls, scheduling control, change controls (to name a few control systems), should be managed in the same manner across similar projects. If automated control systems were in place, these mechanisms could be managed, repeatedly, in the same way. It should also then be appreciated that a control system could be put in place that monitors the project on an ongoing basis and flags project and program managers for deviations in output, which exceed programmed norms.

Ranchod (2001) resolved that a project cockpit could be used by management to monitor projects, it would also provide early warning signals to which management could respond.

It is the intention of this article to extend the concepts proposed by Ranchod (2001) towards the development of a cybernetic control system that would present the application pages necessary for a project manager to have hands on control with the benefit of automatic response and prompting. This automated and prompted response sets up the data history required for auditing a project.

CONTROL SYSTEMS DEFINED

Subhash (1998:380) reviews control processes as being fundamental to all living systems. In the context of organisation, it is crucial to the achievement of goals and objectives. The control process essentially involves measurement of the actual state and comparison with the desired state. The control systems aid the manager in providing the data needed for the measurement of the actual state, therefore, managers and administrators require a broad understanding of the control system as well as the control process related to formal and insidious controls.

Though the subject of management control systems had its roots in management accounting, the thinking in this field has been considerably influenced by other disciplines such as economics, control system engineering, cybernetics, management science, general systems theory, behavioural science and computer science.

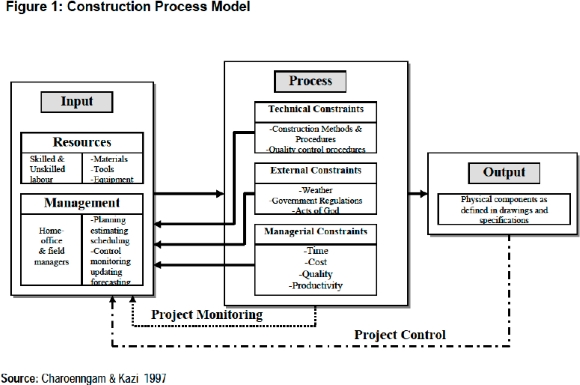

According to Charoenngam & Kazi (1997:29), project cost and schedule planning and /control information systems have been focal considerations of the construction industry since the early 1970s, after the development of the critical path method (CPM) and cost and schedule control system criteria (C/SCSC). Studies have identified the project cost and schedule planning and control information system as one of the major determinants of a project's success. Significant resources have been invested by the construction industry to try to improve the technical aspects of the system, including theoretical frameworks and advanced computer technology (hardware and software). Advancements in computer technology have enabled information systems to integrate cost, schedule, and resource performance data. Computer technology is used extensively in construction organisations and has drastically changed the norms of project cost and schedule planning and control. Computerised information systems possess the potential to improve work at both the office and field levels. This improvement may help to reduce project costs, either by improving the labour productivity or by improving the use of other resources through improved management decision-making.

An information system is expected to provide accurate, timely, and meaningful information, such as proactive identification of problem areas or cost and schedule deviations from the project execution plan.

The construction process model in Figure 1 identifies a closed-loop control system where the adjustment of management planning affects control, influences constraints and ultimately varies the output. Optimisation of project control elements for maximisation of project performance through management directives is the primary focus of the model.

PROJECT MANAGEMENT CONTROL SYSTEMS

Blok & Schuil (1988:D.6.1) identified project control systems as a beneficial tool to be integrated into organisations. Integrated project control (IPC) involves many elements (e.g. planning and scheduling, budgeting, cost control) and is a subject that attracts a lot of attention. Many organisations claim to have it successfully operational for many years, with some exceptions perhaps.

The older systems are generally file oriented, resulting in duplication of data and inconsistencies, or are based on a hierarchical database management system, which tends to be inflexible. Relational Database Management Systems (RDBMS), fourth generation language (4GL) programs and object oriented programming available today offer much more flexibility required for IPC. These tools make it possible to develop an IPC system, which meets not only the requirements of the project team, but also the requirements of clients and company management.

A flexible IPC system which not only allows for the production of standard reports, but which also allows for ad hoc reporting and dealing with "what if type of questions, is of great value to any organisation. Ultimately IPC will improve the control of projects, both in time and money. Earlier indication of potential problems combined with the ability to simulate various options will increase the control of the project, ¡n particular of the project management team (Blok & Schuil 1988:D.6.1).

Ranchod (2001) defines the essence of control as the act of reducing the difference between plan and reality. Because control of projects is such a mixture of feeling and fact, of humans and mechanisms, of causation and random chance it is felt that control theory should be described in the form of cybernetic control loops. This system provides a comprehensive but reasonable illustration of all the elements necessary to control any system. From this model the types of control that are most often applied to projects are considered.

The process of controlling a project (or any system) is far more complex than simply waiting for something to go wrong and then, if possible, fixing it. We must decide at what points in the project we will try to exert control, what is to be controlled, how it will be measured, how much deviation from plan will be tolerated before we act, what kind of interventions should be used, and how to spot and correct deviations before they occur, among a great many other things. In order to keep these and other such issues sorted out, it is helpful to begin a consideration of control with a brief exposition on the theory of control.

No matter what our purpose in controlling a project, there are three basic types of control mechanisms that can be used:

• Cybernetic control

• Go/no-go control

• Post control.

Each one of these will be introduced briefly.

Cybernetic Control

Raven (1987:442) states that cybernetic control systems are described in order to clarify the elements that are present in any control system and define the background of control theory in engineering disciplines.

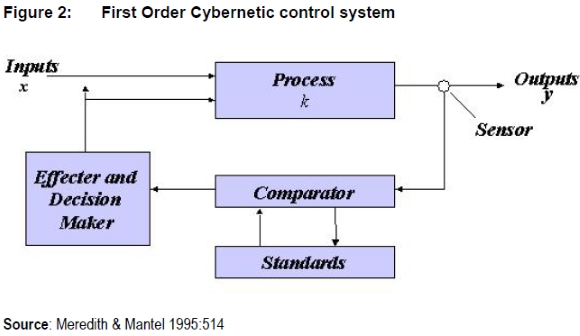

Cybernetic control, or steering, is by far the most common type of control system. (Cyber is the Greek word for helmsman). The key feature of cybernetic control is its automatic operation. Consider figure 2 below.

A system is operated with inputs being subjected to a process that transforms them into outputs. It is this system that we wish to control and for that reason need to monitor the output. Measurements taken by the sensor are transmitted to the comparator, which compares them with a set of predetermined standards. The difference between actual and standard is sent to the decision-maker/(PM), which determines whether or not the difference is of sufficient size to deserve correction. If the difference is large enough to warrant action, a signal is sent to the effecter, which acts on the process or on the inputs to produce outputs that conform more closely to the standard. It is also possible to automatically correct for deviations from known standards and only notify the project manager of deviations that are out of set boundaries or limits.

A cybernetic control system that acts to reduce deviations from standard is called a negative feedback loop; i.e. if the system output moves away from the standard in one direction, the control mechanism acts to move it in the opposite direction.

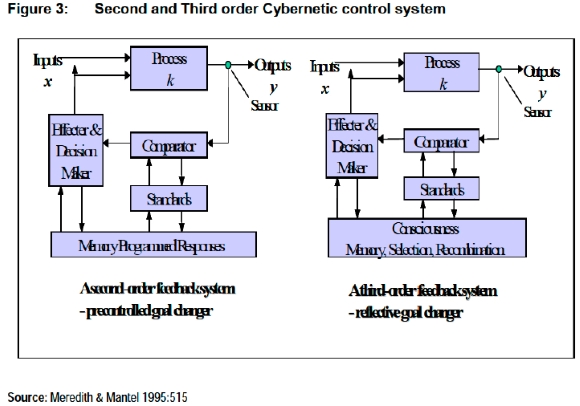

Cybernetic control systems come in three varieties, or orders, differing in the sophistication with which standards are set. Figure 2 showed a simple first order control system, a goal-seeking device. In a second order control system, as in Figure 3, the devise can alter the system standards according to some predetermined set of rules or program. A third order control system can change its goal without specific pre-programming. It can reflect on systems performance and decide to act in ways that are not contained in its instructions. These have reflective consciousness and thus must contain humans.

Go/no-go Controls

Go/no-go controls simply check whether or not a specific condition has been met. This type of control can be used on almost every aspect of a project. For most aspects of performance, cost and time, it is sufficient to know that the predetermined specifications for the project output have been met. The project plan, budget and schedule are all control documents, so the project manager has a pre-designed control system complete with specified milestones as control checkpoints. While cybernetic controls are automatic and will check the operating system continuously or as often as designed to do so, go-no-go controls operate only when and if the controller/project manager uses them. Control is best exerted while there is still time for corrective action.

Post Control

This is directed towards improving the chances for future projects to meet their goals whereas cybernetic and go/no-go controls are directed towards accomplishing the goals of an ongoing project. It tries to capture the essence of project success and failures so that future projects can benefit from past experience; i.e. the generation of a Learning Organisation and Knowledge Based Systems.

No matter how designed, all control systems described have used feedback as a control process. The control of performance, cost, and time usually requires different input data. To control performance the PM may need such specific documentation as engineering change notices, test results, quality checks, rework notices, scrap rates and maintenance activities. For cost control, the PM compares budgets to actual cash flows, purchase orders, labour hour charges, amount of overtime worked, absenteeism, financial variance reports, financial projections, income reports, cost exception reports, and the like.

With a few exceptions, control of projects is always exercised through people. The purpose is always the same, to bring the actual schedule, budget and deliverables of the project into reasonably close congruence with the planned schedule, budget and deliverables.

VISUALISING THE CONTROL BOARD

The control board needs to be managed on a regular ongoing basis. Cowan (1992:70) explores the efficiencies of operation of control boards, these systems must be properly managed to provide the efficiency for which they were established. Most systems are consulted daily and even hourly, while others may be checked on a weekly, monthly or quarterly basis.

Control boards for projects and specifically scheduling systems have benefited organisations for many years. Barsody & Nochaharli (1988:D.3.5) discovered the benefits of a computer based control system for scheduling nearly twenty years ago.

They found the benefits to include

• increased communication among project functional areas

• faster schedule analysis and identification of problems

• better visibility of problems and accountabilities, allowing project managers to address problems across multiple interfaces

• increased senior management awareness of the status of all active projects.

Today computers are networked throughout organisations, making it possible to run control boards on spreadsheet applications. These control boards can integrate the use of control systems for pre warning and flagging of out of bounds responses. Consolidated views can be prepared for senior management who could have access by networked shared files. This would still leave full control and updating responsibilities with the project manager.

PROPOSALS FOR CONTROL BOARD MEASURES AND VIEWS

The first requirement of variable identification needs to be observed. Take for example the following variables that are to be managed:

• project incoming costs

• costs to completion

• tracking project order values with variations

• resource information and loading

• profitability

• known risks.

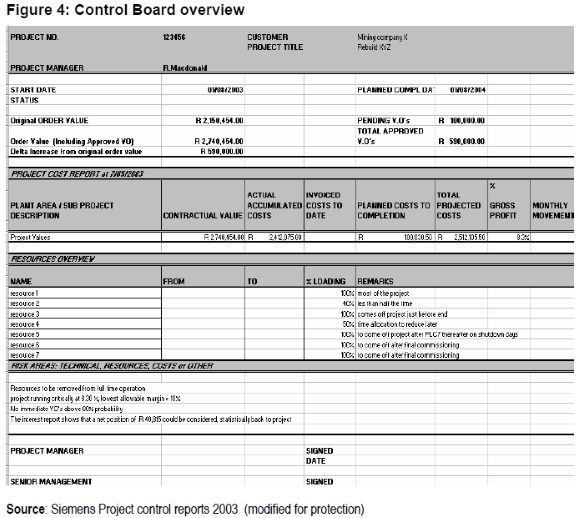

Key to all the data acquisition is that the source of the original data be interrogated for the control board from its original capture source (single source entry). This allows for more accuracy and efficiency of data by not allowing second entries of data. All sources are linked via inSQL computer links or other computer aided data imbedding systems.

Figure 4 describes a possible overview screen displaying variables in static form as well as automatically adjusted variables from the balance of the spreadsheet. Here key data can be observed on a single screen. The companies ERP system is accessed via an inSQL link and the data in this spreadsheet is updated automatically with live project data.

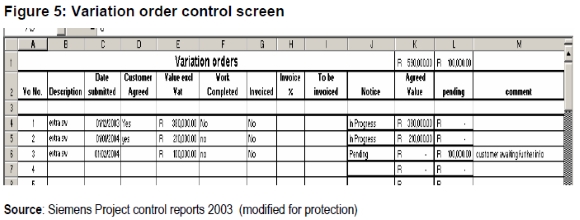

Figure 5 shows an entry form for the management of variation orders. Large projects require more elaborate systems to track changes and variations; key data like acquisition dates and remarks are often a convenient form of reference.

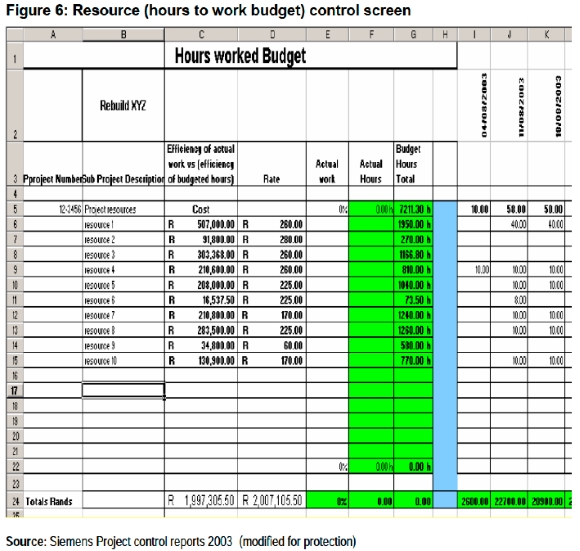

In Figure 6 the data set-up up in Gantt chart programs like MS-Project, is linked with the spreadsheet so that data controlled in the scheduling of resources and costs are automatically updated in the control board view. This would represent the first of the budgeting screens associated with resources.

Ultimately the control board software must generate reports and indications to the project manager for cost usage against budget, revenue inflows versus cost outflows and possible auto prompting via e-mail or cell phone SMS. Cash flow calculations in the background will indicate the efficiency with which the capital resources are used and timed against incoming revenues.

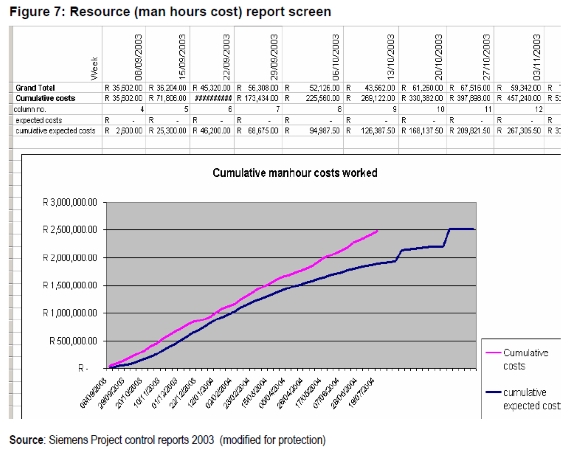

Figure 7 shows the graphing of man hour cost build up versus the budget, indications here show the advantage of continuous updates, as it can be seen early on in the project that cost overruns seem to be occurring against a planned S-curve of cost budget. Again automatic updating of these hours and costs are retrieved from the live ERP system via inSQL link.

CLOSURE

Auditing a project requires an intervention that will scrutinise records, analyse systems & procedures and recommend corrective action where necessary. A control board approach to the management of projects using a system of cybernetic controls by implementing negative feedback control loops via a project manager, offers most of the data necessary for a project audit. Automated audit report screens could be implemented into the control board views and is a possible developmental area for this type of control system. Further research and modification could explore the development of a training simulation system using data retrieved from actual projects.

BIBLIOGRAPHY

BARSODY A & NOCHAHARLI P. 1988. Transmission and distribution: Projects control system. American association of costs engineers: D.3.5. [ Links ]

BLOK F & SCHUIL J. 1988. Getting "Integrated project control" to work. American Association of Cost Engineers: D.6.1. [ Links ]

CHAROENNGAM H & KAZI A. 1997. Cost /Schedule information system: A human-centred approach. Cost Engineering. 39(9): pp. 29. [ Links ]

COWAN W. 1992. Visual control boards are a key management tool. Office Systems. 9(10): 70-. [ Links ]

MEREDITH J & MANTEL S. 1995. Project Management: A Managerial Approach. 3rd ed. New York: Wiley. [ Links ]

RANCHOD J. 2001. Potential Benefits of an Executive Control Cockpit for Project Management in a Diversified Electrical Engineering Organisation. Oxfordshire: Henley Management College (MBA-Dissertation). [ Links ]

RAVEN F. 1987. Automatic Control Engineering. 4th ed. (Chapter: The background of control theory in engineering disciplines. [ Links ])

SIEMENS. 2003. Project control reports [ Links ]

SUBHASH S. 1998. Management control systems: text & cases. Tata:McGraw Hill. [ Links ]