Servicios Personalizados

Articulo

Inglés (pdf)

Inglés (pdf)

Articulo en XML

Articulo en XML Referencias del artículo

Referencias del artículo

Indicadores

Links relacionados

-

Citado por Google

Citado por Google -

Similares en Google

Similares en Google

Compartir

Permalink

PermalinkSouth African Journal of Higher Education

versión On-line ISSN 1753-5913

S. Afr. J. High. Educ. vol.38 no.1 Stellenbosch mar. 2024

http://dx.doi.org/10.20853/38-1-6271

SPECIAL SECTION

Barriers towards research activities among academics in the chartered accountancy stream at the Northwest University, South Africa

S. Sekgota

School of Accounting, North-West University, Mafikeng, South Africa. https://orcid.org/0000-0002-6971-4787

ABSTRACT

Generally, departments of accounting at universities in South Africa that are accredited by the South African Institute of Chartered Accountants (SAICA) mainly focus on teaching the syllabus as prescribed by the Institute. There is no research methodology module in this syllabus neither at undergraduate nor honours level. To qualify as a chartered accountant, one needs to pass an honours degree in accounting and write and pass two board exams. A qualified chartered accountant (CA/SA) will most likely encounter a research methodology module for the first time at master's-degree level. Since 2008, in addition to teaching and learning and community engagement, the departments of accounting have embraced their scholarly activities, which include supervision and/or publishing. As a result, there is an increased effort by the departments of accounting to have its staff members with a chartered accountancy qualification to enrol for master's and doctoral degrees (De Jager, Lubbe, Papageorgiou 2018). It is commonly believed that it seems easier to supervise students or write articles after attaining these qualifications. The purpose of this study was to investigate the barriers that are encountered by academics from a chartered accountancy background to engage in scholarly activities willingly. A qualitative research approach was followed in this study and data was collected by means of interviews. The population was accounting academics at the North-West University. The analysis of data was done qualitatively by means of thematic analysis. The findings revealed barriers such as not knowing where to start due to lack of background or knowledge in conducting research, time, workload, lack of management and lack of access to experienced mentors.

Keywords: chartered accountancy, research, barriers, academics, South Africa

INTRODUCTION

For accounting departments at South African universities accredited by the South African Institute of Chartered Accountants (SAICA), the focus is generally on teaching the Institute's prescribed syllabus (Van der Schyf 2008). This syllabus is based on a prescriptive competency framework issued by SAICA to all universities that are accredited by SAICA to provide undergraduate and postgraduate programmes (Venter and De Villiers 2013; Verhoef and Samkin 2017; Terblanche and Waghid 2021). This syllabus does not include a research methodology module at the undergraduate or postgraduate level (Steenkamp 2014). The current SAICA syllabus does not require any research skills to be learnt. Accredited universities in South Africa therefore do not include research in the postgraduate diploma in accounting or honours commonly known as the Certificate Theory of Accounting (CTA) curriculum (Nieuwoudt and Wilcocks 2005). Students enrolling for these accredited undergraduate or postgraduate programmes aim to become chartered accountants of South Africa, commonly referred to as CA(SA)s (Terblanche and Waghid 2020).

In order to qualify as a CA(SA) in South Africa, a student has to overcome many hurdles, with passing a CTA degree being one of the hurdles (Steenkamp 2014). In addition, the student has to write two challenging qualifying exams, namely the Initial Test of Competence (ITC) and Assessment of Professional Competence (APC) that are administered through SAICA. This means that accounting academics with a professional background will only come into contact with research methodology when they start to work towards a master's or doctoral degree (PhD) (Nieuwoudt and Wilcocks 2005).

The standard prerequisite for a senior lecturer position in accounting at universities in most developed countries is a PhD. An associate professor or full professor in accounting is often required to have, at the very least, a PhD and a specified number of publications in high-impact academic journals (De Jager et al. 2018). Until 2015/2016, at many universities and universities of technology in South Africa, a qualified CA(SA) without a master's or PhD was considered for a senior lecturer's position at the entry level (West 2006; Niewoudt and Wilcocks 2005). The reason for this was, firstly, mainly because of the shortage of CA(SA)s in the country, and secondly, for salary purposes to attract and retain CA(SA)s at universities because few were willing to come into academia (Venter and De Villiers 2013). In addition, at some universities, most academics with CA(SA) qualifications plus coursework master's and no published articles were offered associate professor positions (De Jager et al. 2018).

The core responsibilities of academics around the world and in South Africa are teaching and learning, research, and community engagement (West 2006; Nzuza and Lekhanya 2019). In order to enjoy international recognition, universities have to be classified as research-led. Therefore, most South African universities aspire to pursue a research mission (Nzuza and Lekhanya 2019). In research-intensive universities, the argument is strong that departments of accounting should be equally committed to this aspiration and to professional education (given that all these departments are an integral part of their universities and their missions). Most academics consider research to be an essential function of their roles, notwithstanding that its main purpose may be to inform their teaching (Lubbe 2015). However, there has been a positive shift in the accounting departments from a teaching-only culture to include research activities in order to address the existing supervision capacity in these departments (Van der Schyf 2008).

PROBLEM STATEMENT

According to Mbambo, Olarewaju and Msomi (2022), accounting academics in South African universities view their primary responsibility to be teaching the prospective Chartered Accountants (CA(SA)s rather than advancing knowledge through research. Therefore, it is no surprise that few South African accounting academics participate actively in research given the background above (Mbambo et al. 2022). Previous studies have shown that, until recently, few accounting academics have engaged actively in research (Nzuza and Lekhanya 2019). There are only a few scholars in the field of accounting, and recent studies have clearly shown that there is a substantial shortage and a strong demand for scholars in accounting (Mbambo et al. 2022). As a result, the research outputs of accounting academics in South Africa seem to fall behind those of their counterparts overseas (West 2006). Therefore, chartered accountants in academia are perceived to lack a research culture (Lubbe 2015).

PURPOSE OF THE STUDY AND RESEARCH QUESTION

The purpose of this study was to investigate the barriers that are encountered by academics from a chartered accountancy background to engage in scholarly activities willingly. Therefore, the research question is: What are the barriers to research among accounting academics who have obtained an accredited SAICA postgraduate degree at a South African university?

LITERATURE REVIEW

The culture of accounting departments in South Africa is beginning to shift from being teaching-oriented to a more balanced approach towards teaching and research (De Jager et al. 2018). Various studies on barriers towards research by academics in different fields, including accounting in the world and in South Africa, will be summarised and discussed below. The barriers will inform the theoretical framework that will underpin this study.

Mbambo et al. (2022) studied factors influencing accounting research output in South Africa's universities of technology. Their sample was 100 accounting academics across the six universities of technology. Data was collected by means of a questionnaire. The purpose of their study was to investigate why academics are not performing in the way they intend; that is, in terms of producing more research output. Their findings included the following factors: lack of ambition, less autonomy, job insecurity, non-competitiveness, time constraints, financial burden, slow career development and lack of decision-making as barriers towards producing research output.

Similarly, Nieuwoudt and Wilcocks' (2005) study was on the attitudes and perceptions of South African accounting academics about research. This study used a questionnaire to gauge the personal opinions, perceptions, and attitudes towards research held by South African accounting academics. The results indicate that the main limitations to research output are inadequate qualifications and a lack of skills with regard to conducting research (only 10% of the respondents possessed a doctoral degree), insufficient time for conducting research, financial factors, and a lack of mentorship and departmental support.

Other findings include a lack of practical contribution, quality of teaching was not enhanced by research and difficulty finding research topics.

The barriers/factors between the two above-mentioned studies differed mainly because of the sample/population. In Mbambo et al.'s (2022) study, the population was academics at universities of technology (formerly known as Technikons). In Nieuwoudt and Wilcocks' (2005) study, the population was academics at a traditional university and possibly a former historically white institution. At most traditional universities, the accounting undergraduate and postgraduate degree programmes are accredited by SAICA. Therefore, the majority of the academics would have a CA(SA) qualification. Whereas, at universities of technology, where accounting diplomas are offered, which are not SAICA accredited, a few lecturers would have CA(SA) qualifications. Most lecturers would have different professional qualifications, for example, SAIPA, CIMA and ACCA in addition to postgraduate degrees (Mbambo et al. 2022). Previously, universities of technology and historically disadvantaged institutions did not receive much funding from the government for research purposes, and therefore it is expected that the research culture will be different to that of historically white institutions (McKenna et al. 2017)

However, both studies mentioned time and financial constraints as barriers towards conducting research. In terms of time, the SAICA syllabus is vast and demanding (Terblanche and Waghid 2021). Most lecturers, in most universities, teach a minimum of two modules. It is common knowledge that most universities offer staff discounts to study at the same university, and rarely at other universities. Supervision capacity in accounting is a challenge (Mbambo et al. 2022. Therefore, it could mean that if a staff member can only find a supervisor at another university, they have to pay for their studies themselves. In addition, difficulties in finding grants to fund research activities could also be an explanation of financial barriers (CHE 2022 report).

De Jager et al. (2018) pursued a study titled The South African chartered accountant academic: Motivations and challenges when pursuing a doctoral degree. This study's aim was to determine what factors motivate accounting academics who are chartered accountants to obtain a PhD in an environment where promotion is possible without a PhD. A total of 22 academic CA(SA)s with doctorates and 18 academic CA(SA)s studying towards doctorates were surveyed.

The study found that career progression and intrinsic personal reasons were the reasons CA(SA)s were pursuing doctorates. Their main challenges were finding time for family and social life as well as lack a of support from colleagues and their institution. Time and lack of support are similar to the other two studies, as discussed above. Financial support was not a barrier. Perhaps because it seems current practice at most universities in South Africa is that prospective PhD students usually source for a PhD supervisor themselves. At the master's level, a supervisor is usually provided by the university. Therefore, staff are more likely to study at the same institution they are employed at (CHE 2022).

Other studies worldwide that are not in accounting academia were, however, selected on the basis that they add to the literature that informed the underlying theoretical framework for this study include the following:

Dadipoor et al. (2019) conducted a cross-sectional study on the barriers to research activities as perceived by medical university students at Hormozgan Medical University in Iran. A total of 400 students participated in this cross-sectional study. The sampling method was proportional stratification, and the data collection instrument was a questionnaire that comprised demographic information, personal barriers, and organisational barriers. The findings were that the most prevalent personal barriers were inadequate knowledge of research methodology and inadequate skill in research conduction. In the realm of organisational barriers, limited access to information sources was the most prevalent barrier.

Hagan, Armbruster, and Ballard's (2019) study was on barriers to research among faculty at a Health Sciences University. The purpose of this study was to examine barriers to research among academic faculty at a public university health sciences centre in the United States of America (USA) and to investigate how these barriers are related to faculty member characteristics. A survey was distributed to investigate barriers to research among dentistry, nursing and allied health professionals in the faculty.

Lack of time to do research was found to be the single largest barrier to their own research activity and this item had a higher mean score than all other barriers to research examined. The other barriers included a lack of financial or other resource to facilitate research, lack of institutional research infrastructure, lack of availability of experienced research mentors, and a lack of incentives or rewards to do research. More barriers were lack of research knowledge or skills, feeling intimidated by research since research is not part of one's job, having no ideas for research projects or topics, and a lack of leadership support. In addition, a lack of research training opportunities, and a lack of administrative/clerical support for research grant submission were also found as barriers. Findings also included lack of accessibility to a research committee, lack of training and educational background, lack of interest in research, research not valuable, and relevance of research to clinical practice as barriers (Hagan et al. 2019).

Okoduwa et al. (2018) carried out a study that explored the attitudes, perceptions, and barriers to research and publishing among academic staff in the Nigerian Institute of Leather and Science Technology, (NILEST) Zaria, Nigeria. A structured self-administered questionnaire was distributed among 130 research and teaching staff at the various directorates in NILEST. Some of the obstacles reported to have prevented research activities included a lack of funding, lack of professional mentorship, lack of training, benefits of research, writing experience, high publishing fees, long waiting period for peer review and inadequate research facilities.

Most of the barriers or factors are similar to studies done in South Africa, i.e. notably time, lack of support and lack of mentorship, though some were done in a developed country such as the USA. Nigeria and Iran are considered developing countries like South Africa (Eja and Ramegowda 2020). Another similarity was the lack of knowledge or research skills that was identified by the health professionals in the USA and accounting academics in South Africa. Therefore, it seems the barriers towards research at universities in other countries regardless of the field of study are similar.

METHODOLOGY

Population and sampling

This study followed a qualitative research approach. Data was collected by means of interviews and was analysed using thematic analysis (Saunders, Lewis, and Thornhill 2015). Participants were interviewed over Zoom using the same questionnaire. The questionnaire was structured, and the interviewer derived the questions from the literature review. The target population was accounting academics at the North-West University. The North-West University is a merger between a previously historically advantaged (white) institution and historically (disadvantaged) black institutions. It has three campuses, namely Potchefstroom, Mafikeng and Vanderbijlpark. Each has its own School of Accounting Sciences, but are headed by one director.

The Mafikeng campus has the highest number of accounting academics without master's degrees compared to the other two campuses. One of the reasons could be that Mafikeng Campus previously offered undergraduate degrees in accounting only until 2017 when the honours in Financial Accountancy was introduced. Most of the academics at Mafikeng have a CA(SA) qualification or have gone through the CA(SA) route by completing a SAICA-accredited undergraduate and postgraduate honours degree plus other professional qualifications. The sampling methodology was purposive. Therefore, this campus provided a sufficient target sample. The total number of staff members at Mafikeng was 19. The number of academics who met this criterion was 11. Nine of them agreed to be interviewed. The point of saturation was reached by the interview with participant 7.

Data collection and analysis

Thematic analysis was used to analyse the data obtained through the interviews in which coding of the data was used to allow the identification of themes. Coding is defined as a process of arranging raw data into a standardised form (Saldana 2009, 8). In this study, data from the interviews was listened to and transcribed. The responses from the participants were then grouped together under each question. Thereafter, themes were identified. The results were interpreted using the research objectives, research questions and literature review.

Validity

Rose (2014) states that validity, at its most basic, is about whether the research findings are really about what they claim to be. In this study, the questions for the interview were derived from the literature review to ensure that questions that are relevant to the research topic are used. In addition, interviews were recorded to ensure that correct responses were captured during data analysis and were interpreted appropriately.

Reliability

Maree (2016) states that reliability has to do with the consistency or repeatability of an instrument. High reliability is obtained when the instrument gives the same results if the research is repeated on the same sample. For the purpose of this research, an interview guide was prepared for use during the interviews to ensure participants were asked similar questions. This interview guide was piloted with two participants before it was submitted for ethics clearance and data collection.

Ethical clearance

Human participants were interviewed in this study. Ethical clearance was obtained through the North-West University's ethics committee. The ethical clearance number is NWU-00650-23-A4. Before the interviews, the researcher read out the consent letters to the participants, who then agreed to Zoom recordings. This agreement to recording then served as a guarantee that their participation was voluntary and that the participants understood all the rights they had during the conduct of the study.

Limitations of the research

The study consists of participants from one university. Therefore, this population size is a limitation, and the findings are not meant to be generalised to other universities in South Africa as a whole. This study is exploratory in nature and only investigated a small population within one university.

RESULTS

The section that follows reflects on the results from the interviews conducted with interviewees, i.e., the analysis of their verbal responses during the interviews. The data from the questionnaire used in the interviews will be structured according to the some of the barriers as discussed in the literature review.

Question 1

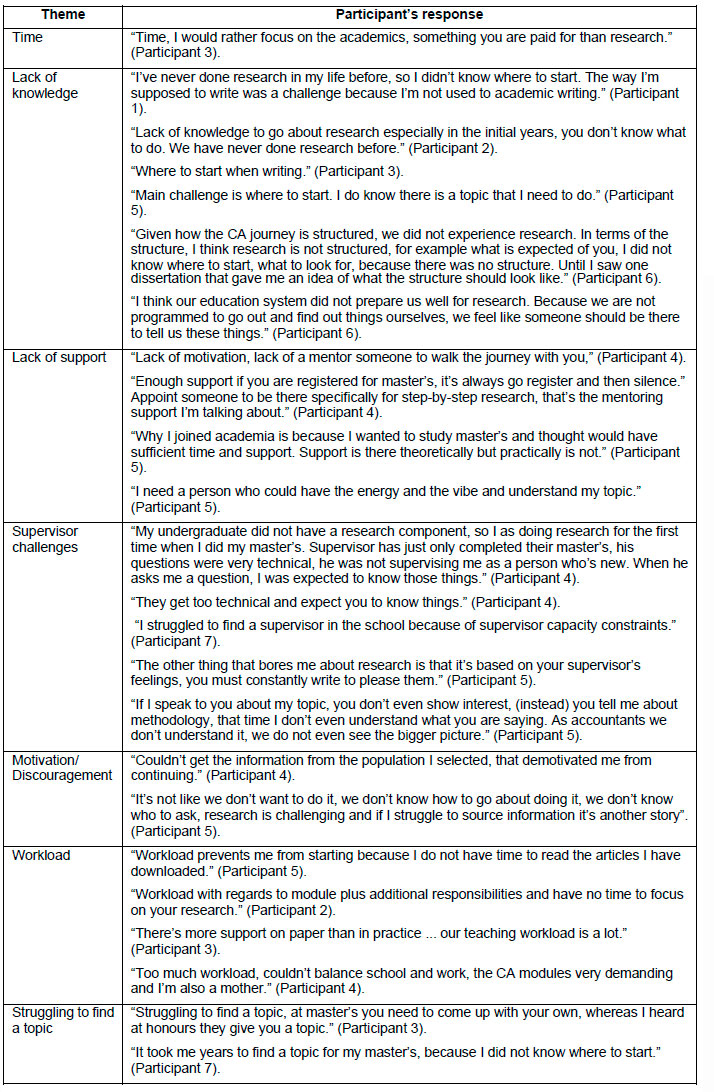

Did you or do you have any challenges/barriers that you face/d in starting with your research journey? This includes studying for a master's or PhD, writing and publishing articles. If Yes, what are/were those barriers/challenges? If No, why? This question was asked to set rapport and set the course for the direction of the study. The themes identified were time, lack of knowledge in conducting research, lack of support, supervisor challenges, motivation/discouragement, and workload. The responses to support these themes are as follows.

Question 2

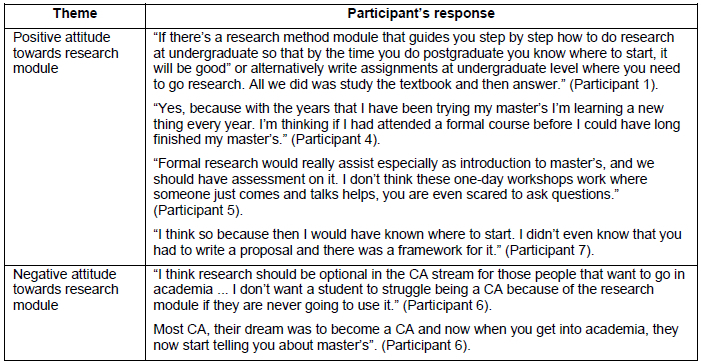

Do you think attending a formal research module (either undergraduate or postgraduate level) would have helped with some of the challenges you faced when you started with your research journey? If Yes, why? If No, why? The purpose of this question was to detect the attitude towards the introduction of research module in the SAICA syllabus. The responses to support this theme are as follows:

Question 3

Are you aware of any research training programmes/workshops/webinars offered at the university? If Yes, why? If No why? The theme was awareness of the research training opportunities within the university and the responses were as follows:

Question 4

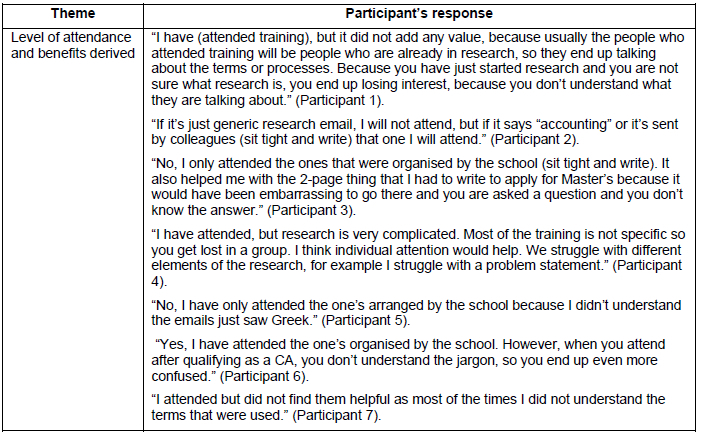

Have you taken any initiative to attend research training programmes/workshops/webinars offered at the university or elsewhere? If Yes, how did they address the challenges that you had? If No, why and what would encourage you to attend? This question was asked to gauge the level of attendance and benefits derived from the research workshops or webinars. The responses to these themes are as follows:

Question 5

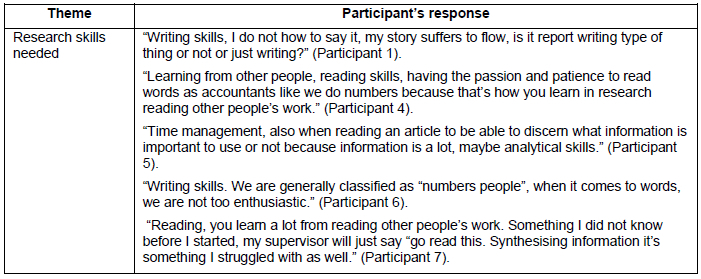

What skills do you think will help with your research journey? The question was asked to identify the skills that the participants thought they needed to engage in research. The theme was research skills needed such as academic writing skills, reading and time management. The responses to the theme are as follows:

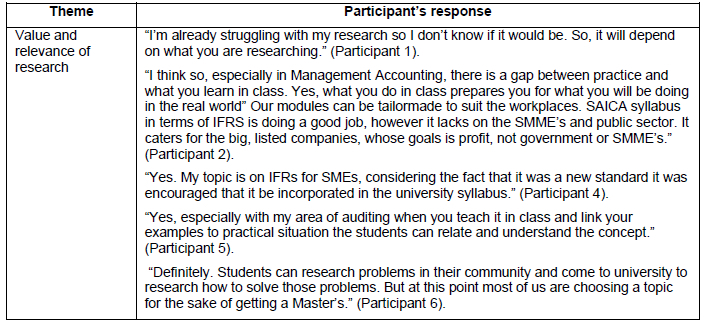

Question 6

Do you think research in your field (accounting, taxation, management accounting, auditing) will make a practical/academic contribution? If Yes, why? If No, why? The theme for this question was whether the research was relevant and valuable in these four fields mentioned above. The responses were as follows:

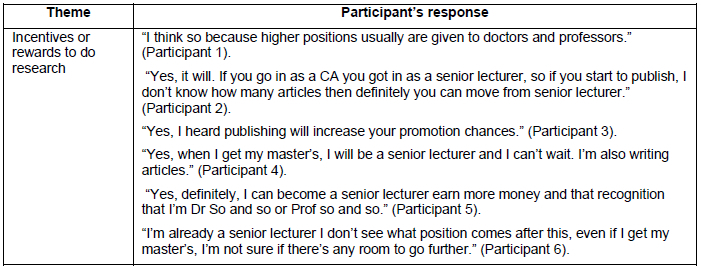

Question 7

Will research enhance the opportunity for you to be promoted within the university? If Yes, why? If No, why? The theme was awareness of incentives to do research and the responses were as follows:

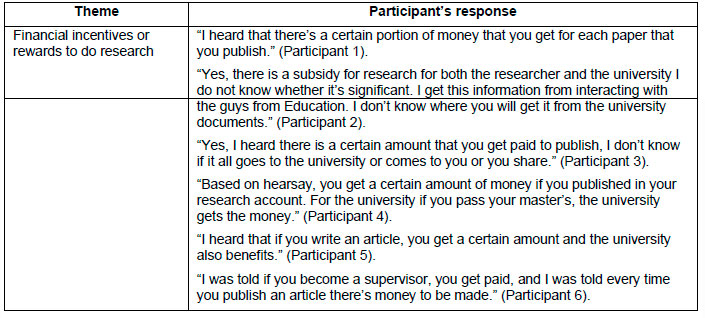

Question 8

Do you know the financial benefits (whether personal or for the university) linked to research? If Yes, why? If No, why? The theme was awareness of the financial incentives to do research and the responses were as follows:

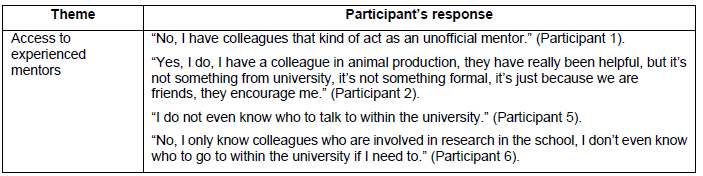

Question 9

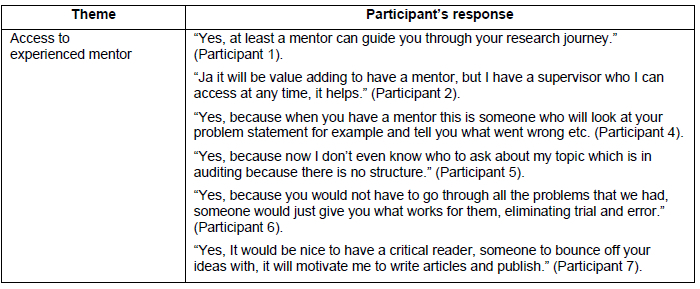

Do you have access to an experienced research mentor within the University to assist/help you with your research journey? If Yes, why? If No, why? The theme was addressed at experienced mentors and the responses were as follows:

Question 10

Would you like to have access to an experienced research mentor within the university willing to help you with your research journey? If Yes, why? If No, why? The theme was addressed at experienced mentors and the responses were as follows:

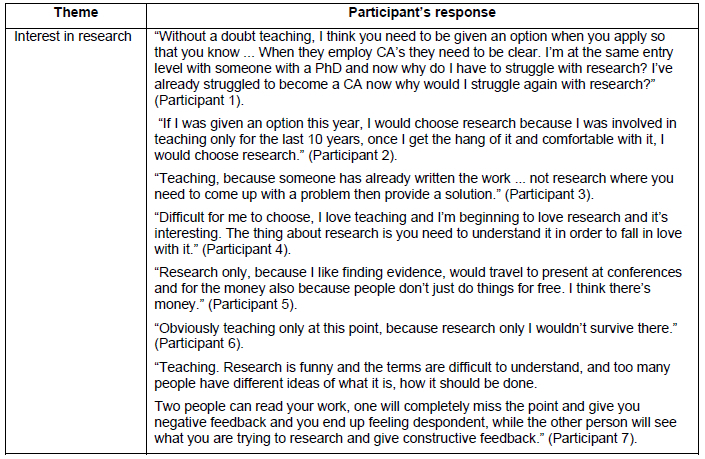

Question 11

If you were given the option to choose between research only and teaching only, which one would you choose and why? The question was to gauge the level of interest in research and the responses were as follows:

INTERPRETATION OF THE RESULTS

The results show that the participants' main barrier was not knowing where to start due to a lack of background or knowledge in conducting research (Okoduwa et al. 2018). This was because they had never studied any research methodology module in undergraduate or postgraduate studies. Participants who enrolled for a full dissertation master's degree mentioned that it seemed it was expected of them by their supervisors to "teach themselves" research methodology. They were just told "go read about this" and to figure out things for themselves. Participants who did the coursework master's found the "mini-dissertation part" of their studies difficult. They felt that the guidance given by supervisors when it came to research methodology was not enough.

Time, workload, lack of support from management in the school and lack of experienced mentors in the school and university also came up as main barriers in line with the literature (Mbambo et al. 2022; Terblanche and Waghid 2021). The participants felt that there was too much workload in terms of the SAICA syllabus, number of modules taught and administration workload such as setting tests, attending management meetings, preparing audit files for the university as well as SAICA accreditation review after every three years. Therefore, they do not have time for research. Because of all these reasons, participants felt they do not have management support.

It seems most participants had a positive attitude towards research because comments included, "once participants understand what needs to be done, they begin to love it". The participants saw research as valuable and will contribute towards teaching and learning. As stated before, the Mafikeng campus had the highest number of staff without master's degrees. At the time of writing this article, one staff member had just completed PhD and had only supervised two master's students to completion. Another was studying for a PhD. Two staff members had only just completed their master's in 2021 and 2022 and have never supervised. Four staff members with or without master's degrees had published articles. Of the remaining five staff members who had obtained their master's on or before 2016, only one was involved as a co-supervisor and co-author. Three participants are currently enrolled for master's degrees.

Participants also knew about promotion aspects and heard about the financial incentives of writing and publishing articles. However, this seems not to be enough to entice them to do research willingly.

CONCLUSION

One participant summed it up well by saying: "We need to push through because this thing (research) is the future. Our hearts want it, but our brains cannot comprehend it." (Participant 5). There is a call to SAICA from other academics to include the research module in the syllabus (Terblanche and Waghid 2021). Perhaps this may help future CA(SA)'s in academia in knowing where to start when doing research. However, the academics that completed master's recently in the school at Mafikeng have started a community practice, which is referred to as "sit tight and write" in the comments. This initiative has seen an increased interest in research among the participants.

RECOMMENDATIONS

Participants felt they needed tangible support from management in the school. Perhaps one way to show this tangible support by management would be if less teaching workload is given to staff who show interest in research activities or are studying towards master's or PhD degrees. The School of Accounting Sciences in the three campuses should consider collaboration with other schools/departments in the university. For example, co-supervision, where one supervisor concentrates on the accounting or tax or auditing or management accounting technical aspects of the thesis while the second supervisor helps with research methodology. In this way, supervision capacity and sharing of expertise might increase. As a result of this collaboration, mentors within the school and university can be found, and a research mentorship programme that is more structured can be introduced or enhance already-in-place research mentorships within the university.

REFERENCES

CHE see Council on Higher Education.

Council on Higher Education. 2022. Doctoral Degrees National report. Pretoria. [ Links ]

Dadipoor, S., A. Ramezankhani, T. Aghamolaei, and A. Safari-Moradabadi. 2019. "Barriers to research activities as perceived by medical university students: A cross-sectional study." Avicenna Journal of Medicine 9(01): 8-14. [ Links ]

De Jager, P., I. Lubbe, and E. Papageorgiou. 2018. "The South African chartered accountant academic: Motivations and challenges when pursuing a doctoral degree." Meditari Accountancy Research 26(2): 263-283. [ Links ]

Eja, K. M. and M. Ramegowda. 2020. "Government project failure in developing countries: A review with reference to Nigeria." Global Journal of Social Sciences 19: 35-47. [ Links ]

Hagan, J. L., P. Armbruster, and R. Ballard. 2019. Barriers to research among faculty at a health sciences university. American Journal of Educational Research 7(1): 44-48. [ Links ]

Lubbe, I. 2015. "Educating professionals - perceptions of the research-teaching nexus in accounting (a case study)." Studies in Higher Education 40(6): 1085-1106. [ Links ]

Mbambo, M., O. Olarewaju, and T. S. Msomi. 2022. "Factors influencing accounting research output in South Africa's universities of technology." Cogent Business & Management 9(1): 2099607. [ Links ]

Maree, K. 2016. 1st steps in research. 2nd Edition. Pretoria: Van Schaik. [ Links ]

McKenna, S., J. Clarence-Fincham, C. Boughey, H. Wels, and H. van den Heuvel. 2017. Strengthening Postgraduate Supervision. Stellenbosch: African Sun Media. [ Links ]

Nieuwoudt, M. J. and J. S. Wilcocks. 2005. "The attitudes and perceptions of South African accounting academics about research."Meditari Accountancy Research 13(2): 46-66. [ Links ]

Nzuza, Z. Z. and M. Lekhanya. 2019. "Effectiveness of University Research Policy in Promoting Research Engagement among Accounting Academics in Public Universities in KwaZulu-Natal." International Journal of African Higher Education 6(1): 27-49. [ Links ]

Okoduwa, S. I., J. O. Abe, B. I. Samuel, A. O. Chris, R. A. Oladimeji, O. O. Idowu, and U. J. Okoduwa. 2018. "Attitudes, perceptions, and barriers to research and publishing among research and teaching staff in a Nigerian Research Institute." Frontiers in Research Metrics and Analytics 3: 26. [ Links ]

Rose, S. 2014. Management Research: Applying the principles. 1st Edition. New York: Routledge. [ Links ]

Saldana, J. 2009. The coding manual for qualitative researchers. London: Sage. [ Links ]

Saunders, M., P. Lewis, and A. Thornhill. 2015. Research methods for business students. 7th Edition. England: Pearson education. [ Links ]

Steenkamp, G. 2014. "How pre-admission characteristics affect the performance of CTA students at a South African university." Journal of Economic and Financial Sciences 7(2): 283-298. [ Links ]

Terblanche, J. and Y. Waghid. 2020. "The chartered accountant profession in South Africa: In dire need of decoloniality and ubuntu principles." Citizenship Teaching & Learning 15(2): 221-238. [ Links ]

Terblanche, J. and Y. Waghid. 2021. "Chartered accountancy and resistance in South Africa." South African Journal of Higher Education 35(3): 239-253. [ Links ]

Van der Schyf, D. B. 2008. "The essence of a university and scholarly activity in Accounting, with reference to a department of Accounting at a South African university." Meditari Accounting Research 16(1): 1-26. [ Links ]

Verhoef, G. and G. Samkin. 2017. "The accounting profession and education: The development of disengaged scholarly activity in accounting in South Africa." Accounting, Auditing & Accountability Journal 30(6): 1370-11398. [ Links ]

Venter, E. R. and C. de Villiers. 2013. "The accounting profession's influence on academe: South African evidence." Accounting, Auditing & Accountability Journal 26(8): 1246-1278. [ Links ]

West, A. 2006. "A commentary on the global position of South African accounting research." Meditari: Research Journal of the School of Accounting Sciences 14(1): 121 -137. [ Links ]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}