Services on Demand

Article

English (pdf)

English (pdf)

Article in xml format

Article in xml format Article references

Article references

Indicators

Related links

-

Cited by Google

Cited by Google -

Similars in Google

Similars in Google

Share

Permalink

PermalinkSouth African Journal of Higher Education

On-line version ISSN 1753-5913

S. Afr. J. High. Educ. vol.36 n.3 Stellenbosch Jul. 2022

http://dx.doi.org/10.20853/36-3-4647

GENERAL ARTICLES

Financial literacy in south african healthcare professionals: an unmet need in health professions education

A. MillenI; A. StaceyII

ISchool of Physiology, University of the Witwatersrand Johannesburg https://orcid.org/0000-0002-4831-7336

IIWits Business School, University of the Witwatersrand Johannesburg https://orcid.org/0000-0001-7580-911X

ABSTRACT

The holistic training of healthcare professionals as a strategy to build the healthcare system has received considerable attention. As part of training a holistic workforce, it is expected the healthcare professionals be component in management and governance. Financial literacy is low globally and impacts financial decision-making and business management. Despite high levels of education, medical professionals elsewhere in the world have low financial literacy. Financial literacy levels in South African healthcare professionals are unknown. This study investigated the degree of and contributors to financial literacy in South African healthcare professionals. A validated financial literacy questionnaire was completed by 473 healthcare professionals, of whom 130 owned private practices. Financial literacy scores were determined as a composite score based on financial knowledge, financial behaviour and financial attitudes. The independent contribution of demographic factors to financial literacy were determined in multivariate linear regression analysis. Financial literacy in healthcare professionals was relatively high (73%). Of the total cohort 24%, 27% and 63% did not reach acceptable scores for financial knowledge, behaviour, and attitudes, respectively. Sex, medical specialty and being in private healthcare predicted financial knowledge scores. Higher income and self-rated financial knowledge were associated with financial literacy. In business owners, business-specific financial literacy was low (51%), and not associated with general financial literacy (r=-0.11, p=0.40). Education in economics and finance predicted business-related financial literacy scores (p=0.02). Financial attitudes that favour the short term may impact financial decision-making in healthcare professionals in managing small businesses and state healthcare facilities. Current approaches in health professions education may impact the success of the healthcare system in South Africa.

Keywords: financial literacy, health professions education, health system, South Africa

INTRODUCTION

The World Health Organisation (WHO) has identified six core components that forms the framework for defining and monitoring health systems (WHO 2010). These core components include service delivery, the health workforce, information systems, access to essential medicine, finance and leadership and governance (WHO 2010). As the health workforce forms a key component that cuts across several components, it is not surprising that health professions education has received considerable attention over the past decade in an attempt to strengthen health systems globally (Frenk et al. 2010). In South Africa, a large focus of the transformation of health professions education has centred around an increase in student numbers and the demographics of student intake (Meela, Libhaber, and Kramer 2021). However, several other aspects in the transformation of health professions education require consideration. Furthermore, the quality of health professions education in South Africa has received considerable attention (Van Staden 2021). In this regard, the WHO's global strategy on human resources for the health workforce have highlighted the need for training programs that produce adequately skilled healthcare professionals who can build the health system (WHO 2016). Therefore, to strengthen health systems, it is suggested that health professions education should not only focus on training competent healthcare professionals, but also training well-rounded healthcare professionals that are competent in leadership, management and governance. Similarly, South Africa has also adopted a more holistic approach in its competency framework to health professions training (South African Qualifications Authority 2012). This framework suggests that the core competencies of health profession students include, amongst others, leadership, and management skills (South African Qualifications Authority 2012). Indeed, the inclusion of non-clinical competencies as part of the training of high-quality health profession graduates have been highlighted as a contributor to improved efficiency in the healthcare system and overall improved health service provision (Van Staden 2021).

Nevertheless, the implementation of these plans to strengthen health professions education in an attempt to improve health systems in South Africa has been fragmented (Van Staden 2021). Failure to address the needs of the transformed healthcare worker has implication for the quality of the health system in South Africa. The lack of sound financial management and leadership in the public healthcare system is well known (Maphumulo and Bhengu 2019) and have been highlighted as a contributing factor to the mismanagement of healthcare facilities in South Africa (Rispel, De Jager, and Fonn 2016). Globally, limited business, financial and leadership attributes have been cited as some of the shortcoming in the successful management of practices, clinics, departments and hospitals (Perry, Mobley, and Brubaker 2017). It has been proposed that medical professionals are expected to manage practices, departments and hospital and to make sound business decisions, yet they most likely do not have the necessary skills to do so (Perry et al. 2017). Furthermore, according to the Health Professions Council of South Africa (HPCSA), in 2018 approximately 14 000 medical professionals suspended their practitioner licences, of which only 55 were attributable to deaths (HPCSA 2018). This raises the question why these medical professionals are no longer registered to deliver health services? The empirical evidence to support the reasons for suspending medical practitioner licences are limited. Nevertheless, popular media suggests the top reasons for failure in medical practices globally are poor financial and strategic planning, poor financial and business decisions, and a lack of vision (Helbing 2016; Kalish 2016; PookieMD 2008; Walter 2015). Taken together, the need to train holistic healthcare workers are well established. Nevertheless, the quality of management of healthcare facilities and the significant number of the health workforce exiting the healthcare sector raises the question whether management and leadership skills are successfully included in the holistic training of the healthcare professionals. Whether the lack of financial literacy and business management skills impact the success of healthcare workers and the health system in South Africa warrant investigation.

Financial literacy is an umbrella terms that includes various concepts and perspectives of how equipped a person is to make financial decisions (Cude 2010; Huston 2010; Remund 2010; Zait and Bertea 2015). For a person to be considered financially literate, they require both an understanding and a practical application of financial principles (Zait and Bertea 2015). The degree of financial literacy globally is regarded as low (Lusardi and Mitchell 2011; Zait and Bertea 2015). In a large, international study, Atkinson and Messy (2012) reported that in 14 countries, financial knowledge of key financial concepts is low in more than 50 per cent of the population. In South Africa, financial literacy levels are concerning (Nanziri and Leibbrandt 2018). Financial literacy scores in South Africans were in the bottom global quartile (Atkinson and Messy 2012). These reports of low financial literacy in South Africa are supported by statistics on the high levels of indebtedness and poor savings culture (Zwane, Greyling, and Maleka 2016).

Financial literacy has been associated with various measures of economic success, financial health, and accumulation of wealth (Lusardi and Mitchell 2011; Lusardi and Mitchell 2007). People with lower financial literacy levels have a poor savings culture, they may experience more debt and may have difficulties with high-cost debt (Hilgert, Hogarth, and Beverly 2003; Lusardi and Tufano 2015). Besides financial outcomes, low financial literacy is also related to reduced productivity, higher divorce rates, emotional stress, depression, and mental illness (Bennett et al. 2012; Joo and Grable 2000; Kinnunen and Pulkkinen 1998). Several demographic characteristics including age, sex, ethnicity, geographic location, education level, work status and being self-employed impact financial literacy (Atkinson and Messy 2012; Lusardi and Mitchell 2011; Lusardi and Tufano 2015; Nanziri and Leibbrandt 2018). Although level of education influence financial literacy, a large portion of people with tertiary education display low financial literacy, especially students who pursue non-business-related careers (Chen and Volpe 1998; Van Rooij, Lusardi, and Alessie 2011).

Despite a high level of tertiary education, previous reports indicate low levels of financial literacy in medical professionals in the United States (US) (Ahmad et al. 2017; Jayakumar et al. 2017). In qualified healthcare professionals working at large medical institutions in the US, it was reported that levels of credit card debt were high, few had retirement savings and general knowledge on financial principles were low (Ahmad et al. 2017). Moreover, levels of student debt among medical professionals are high (Jayakumar et al. 2017). In South Africa, the level of financial literacy in healthcare professionals are unknown. Furthermore, a large portion of South African healthcare professionals require financial literacy for the management of small businesses in private practice and for management of hospital departments in public and private healthcare institutions. Indeed, it has been reported that low financial literacy and poor management practices are main contributors to small business failure in industrialised and developing nations, including South Africa (Kotzé and Smit 2008; Ye and Kulathunga 2019). Therefore, the aim of this study was to determine 1) the general level of financial literacy in healthcare professionals, 2) the business specific financial literacy in healthcare professionals managing private practices.

METHODS

Participants

Medical professionals between the ages of 18 and 65 years who were in their final year of medical training or have been practicing their specialty for less than 15 years were invited to participate in an anonymous and voluntary online survey. Research ethics was approved by the Human Research Ethics Committee (non-medical) at the University of the Witwatersrand (approval number: WBS/BA502906/669).

Procedures

An online survey was distributed via email or closed social media groups via the respective professional bodies for healthcare professionals in South Africa between November 2019 and February 2020. A validated questionnaire available from the Organisation for Economic Cooperation and Development (OECD) used to measure financial literacy (OECD 2018) were distributed to all participants. The questionnaire consists of basic demographic questions which included age, sex, marital status, household dependants, medical specialty, years since qualifying, and household income. Secondly the questionnaire consists of questions that measures financial knowledge, financial behaviour, and attitudes to finances, which together provide a composite score for financial literacy (OECD 2018). For participants that owned private practices or were directly responsible for making financial decisions in medical institutions, additional questions were provided that test the translation of financial literacy skills to business decisions in running small, medium and micro enterprises (OECD 2019).

Data analysis

Statistical analysis was performed using SAS software, version 9.4 (SAS Institute Inc., USA). Descriptive statistics are reported as mean (standard deviation), median (interquartile range) or proportions as appropriate. Multivariate regression analyses were performed to determine the relative contribution of demographic variables to financial literacy in healthcare professionals. To reduce the dimensionality of the dataset, cluster analysis was performed where groups were segmented based on demographic characteristics and/or sub-sector of healthcare professionals. Differences among the clusters were determined with unpaired t-tests, Chi-squared or one-way analysis of variance (ANOVA) where appropriate. Linear regression analysis was performed to determine the contribution of demographic variables to financial literacy scores.

Internal consistency of the questionnaire was determined by asking 10 participants in the study to repeat the questionnaire at least seven days after the initial response. There were no differences in selected demographic variable responses between the repeat questions as determined by paired t-tests (p=0.85, p=0.96, p=0.99, p=0.89, respectively). There were strong associations between financial knowledge (r=0.75, p<0.0001), financial behaviour (r=0.86, p<0.0001), financial attitude (r=0.90, p<0.0001) and financial literacy (r=0.81, p<0.0001) between the repeat responses. Internal consistence of the questionnaire for multi-item responses was determined by Cronbach alpha, and was considered acceptable (α=0.84).

RESULTS

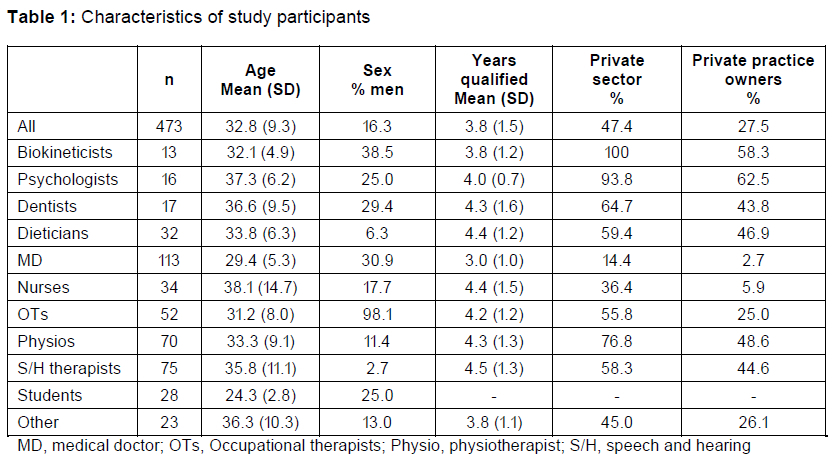

From the 570 healthcare professionals that responded to the online survey, 473 respondents completed at least 80 per cent of the financial literacy questionnaire and were included for data analysis. The demographic characteristics of the participants are summarised in Table 1. From the total sample, 130 participants indicated that they owned a private medical practise who completed the additional financial literacy questionnaire specific for small to medium sized business owners. The category of medical professionals labelled "other" included optometrists, forensic pathologists, genetics counsellors, pharmacists, nutritionists and medical researchers or medical scientists. In the student category, all students were in their final year of studies toward a medical degree.

The mean (SD) financial literacy score across all groups was 15.4 (2.5) out of a possible 21 points. The 21 points for financial literacy comprise of a maximum of seven points for financial knowledge, nine points for behaviour and five points for attitude (Figure 1). There was a significant difference in financial literacy scores across specialties (F=2.76, p=0.003). These differences were largely as a result of the differences across specialties in financial knowledge (F=5.15, p<0.0001). There were no differences in financial behaviour (F=1.7, p=0.08) or financial attitudes among the different specialties (F=1.02, p=0.42). In all participants, 24 per cent of respondents did not reach the threshold of scoring at least 5 out of 7 (70%) on financial knowledge. In medical doctors, 98 per cent of respondents scored above the threshold of what is expected for financial knowledge, while 42 per cent of nurses and 39 per cent of speech and hearing therapists did not achieve the threshold value. In all participants, 73 per cent of respondents reached the acceptable value of 67 per cent (6 out of 9) for financial behaviour. 92 per cent and 88 per cent of biokineticists and dentists, respectively, reached the threshold value for financial behaviour, while only 50 per cent of psychologists reached the acceptable score. With regards to financial behaviour, 67 per cent of respondents reported that their households have a budget and 73 per cent were actively saving in the preceding year. Furthermore, 51 per cent of respondents reported that they could not make ends meet, and 36 per cent of the total sample reported that they had to borrow money when this happened. Only 37 per cent of participants reached the threshold score (70%) for financial attitudes that favours the long-term. Only in the psychologists did at least 50 per cent of the participants reach acceptable financial attitude scores.

Table 2 shows the independent contributions of demographic variables to the calculated financial literacy scores. Male sex, being a medical doctor or a student, being in private healthcare or having a higher self-rating of financial knowledge were all independently related to a higher financial knowledge score. Being a nurse was associated with lower financial knowledge scores, while being an occupational therapist was associated with lower financial literacy scores. Higher income was independently associated with financial behaviour, and with financial literacy. Although the self-rate financial knowledge score (58%) was significantly lower than the financial knowledge score obtained in the questionnaire (77%, p=0.001), self-rated financial knowledge was significantly associated with all financial scores (all p <0.0001).

Table 3 shows the characteristics and financial literacy scores of private practice owners who completed the questions on financial literacy in small business owners. Financial knowledge specific to business was similar to general financial knowledge. Although financial behaviour was relatively high in personal finances, as indicated in the general score, business related financial behaviour score was low (49%). Forty-two per cent of respondents reported that they either used one bank account for personal and business finances, or that even though they have two accounts, they struggled to separate their business and personal finances. In the past 12 months, 34 per cent of private practice owners experienced financial difficulty. Majority of private practice owners reported that they outsource basic book-keeping (67%) and tax (62%) to third parties. Only 15 per cent of participants reported that they have received training in either business related finances or personal money management and less than 40 per cent of participants were exposed to accounting or economics related subjects during school or university education. Financial attitudes showed that a large portion of respondents (77%) tended to favour short term financial success, rather than positive attitudes toward long term financial planning. The financial literacy score determined specific for business owners was 23.8 per cent lower than the score obtained for general financial literacy (p<0.0001).

Medical specialty was not associated with financial knowledge or financial attitude scores (Table 4). Being a biokineticist, psychologist, dietician, physiotherapist, or speech and hearing therapist were all associated with low financial behaviour and financial literacy scores. Education in economics and finance related subjects in high school or university was the only other factor independently associated with business related financial knowledge and financial literacy scores (p=0.04 and p=0.02 respectively).

Discussion

The main findings of the current study were that healthcare professionals had relatively high financial literacy scores, which varied across medical specialties. Although the overall general financial literacy was relatively high, a large proportion of participants did not reach an acceptable minimum score in financial behaviour or financial knowledge. Especially in financial attitudes, majority of participants did not reach an acceptable long-term view of financial planning. Among medical professionals a large portion were unable to make ends meet and more than one third of medical professionals borrowed money to make ends meet. In sub-group analysis in medical professionals that own private practices or make business decisions, business related financial literacy was substantially lower than general financial literacy. Demographic factors were not associated with business related financial literacy, however, education in economics and finance predicted business related financial literacy. There was a discrepancy in business related financial literacy among different medical specialties.

The current study aids our understanding of financial literacy in healthcare professionals in a South African setting. Financial literacy was relatively high in healthcare professionals (79%), compared to the average of 65 per cent (Atkinson and Messy 2012) and 48 per cent (Nanziri and Leibbrandt 2018), previously reported in the general South African population. Both financial knowledge and financial behaviour scores were high and contributed to the high financial literacy scores. Using the same measurement instrument, previously it has been reported that only 33 per cent and 43 per cent of South Africans scored above the acceptable threshold values for financial knowledge and behaviour respectively (Atkinson and Messy 2012). In contrast, in the current study 76 per cent and 73 per cent of healthcare professionals met the acceptable financial knowledge and behaviour scores, respectively. However, the number of respondents reaching the acceptable scores varied widely across the medical specialties. Medical doctors displayed high financial knowledge and behaviour scores, while nurses, speech and hearing therapists, and psychologists were amongst the specialties that scored low in these areas. Interestingly, current medical students scored no different in financial knowledge and behaviour from that of the qualified medical professionals. The discrepancy between financial knowledge scores in the current study and previous studies in the general South African population may be, at least in part, explained by tertiary education. Indeed, previous studies showed that financial knowledge is impacted by level of education (Atkinson and Messy 2012; Nanziri and Leibbrandt 2018; Lusardi and Mitchell 2011; Van Rooij et al. 2011). Nanziri and Leibbrandt (2018) reported that South Africans with a University education had financial literacy scores approximately 15 per cent higher than that of the general population. All participants in the present study have a tertiary education or were in the final year of their degree programmes. Considering that less than 30 per cent of young South Africans are engaged in training or education, it may explain at least in part, the differences between the financial knowledge scores between medical professionals and the general South African population.

Although financial behaviour was acceptable in majority of participants, half of healthcare professionals in this study were unable to make ends meet and more than one third had to borrow money when this happened. Using the same measuring tool, borrowing behaviour was higher in medical professionals compared to the general South African population, where only 26 per cent of people displayed this behaviour as previously reported (Atkinson and Messy 2012). Although financial behaviour scores were high, several healthcare professionals engaged in less than desirable financial behaviour. This is supported by evidence that 36 per cent of participants do not budget, and 27 per cent do not actively save. These values are comparable to previously published values in the general South African population where 24 per cent and 26 per cent do not actively save or budget, respectively (Atkinson and Messy 2012). Indeed, others have also reported a poor savings culture and high levels of debt in South Africans (Zwane et al. 2016). Our results on financial behaviour are in keeping with findings from healthcare professionals globally. Indeed, previous reports showed that medical students and early career medical doctors in the US had high levels of credit card debt and few had retirement savings (Ahmad et al. 2017; Jayakumar et al. 2017).

Scores in financial attitudes towards long-term financial planning was low among medical professionals. In contrast, in the general South African population using the same measurement tool, 54 per cent reached the acceptable financial attitude score (Atkinson and Messy 2012), while only 37 per cent of healthcare professionals reached this score. This is far below the world average of between 60 and 70 per cent of people having attitudes that favour long term behaviour (Atkinson and Messy 2012). This suggest that even though medical professionals may have high financial knowledge and acceptable financial behaviour, they tend to favour a short-term financial outlook.

Several demographic variables were associated with financial literacy in the current study. We showed that men had higher financial knowledge scores, but that financial behaviour and attitude scores were not different between men and women. Similar to previous reports, but in contrast to others, we showed the composite financial literacy score were similar between men and women (Atkinson and Messy 2012; Lusardi and Mitchell 2011; Lusardi and Mitchell 2007; Lusardi and Tufano, 2015; Nanziri and Leibbrandt 2018). In medical professionals, Jayakumar et al. (2017) reported that men had higher financial literacy compared to women. In contrast to previous studies, we showed no association between age groups and financial literacy. These contrasting finding may be as a result of the relatively homogenous age range and the large proportion of women in the current study. Nevertheless, the number of years since qualifying were not associated with financial literacy. The lack of association between financial literacy and age and years since qualifying, suggests that the training of medical professionals in skills other than healthcare have not changed over the past decade. Although the health sector (public versus private sector) was not associated with financial literacy, medical specialty contributed to financial knowledge, but not to financial behaviour and attitudes. Similar to previous reports, we showed that higher income levels were associated with higher financial literacy scores in the general population (Nanziri and Leibbrandt 2018) and in medical professionals (Jayakumar et al. 2017). Self-rated financial knowledge was strongly associated with the financial scores obtained in the questionnaire in the present study. Similar to our findings, others have shown that self-rated financial knowledge is strongly linked to calculated financial knowledge scores in the general population (Atkinson and Messy 2012) and in medical professionals (Jayakumar et al. 2017).

With regards to the business specific questions, business owners scored 71 per cent, 49 per cent and 23 per cent for financial knowledge, behaviour and attitudes, respectively. The business-specific composite financial literacy score (51%) was substantially lower than the score (73%) obtained in the general financial literacy section. This suggests that general personal financial knowledge do not necessarily predict the financial knowledge and skill to ensure business success. Several studies in small business owners have reported low levels of business-related financial literacy and undesirable management practices (Dahmen and Rodríguez 2014; Fatoki 2014; Kotzé and Smit 2008; Oseifuah 2010). Moreover, the current study results are in accordance with previous studies that showed despite having tertiary education, financial literacy was low in medical students (47%) and medical doctors (51%) (Ahmad et al. 2017; Jayakumar et al. 2017). In these aforementioned studies, financial literacy was measured using similar questions as in the business specific questionnaire employed in the current study. These findings support the suggestion that education per se cannot be used as a proxy for financial literacy (Lusardi and Mitchell 2011). Indeed, previous reports showed that even people with tertiary education may display low financial literacy (Van Rooij et al. 2011), especially in those who do not pursue business-related careers (Chen and Volpe 1998).

Although business specific financial knowledge was relatively high in the current study, financial behaviour was concerning. We showed that almost half of healthcare professionals who own private practices do not separate their personal and business finances. Our results are similar to previous reports where majority of small business owners in South Africa do not separate business and personal accounts (Fatoki 2014). Moreover, more than one third of private practice owners could not cover business expenses at some time during the preceding 12 months. Majority of business owners in the current study do not take responsibility for their own financial management, but rather outsource these functions. Although outsourcing financial functions of businesses, per se, is not unexpected, the concern lies with the lack of understanding of financial concepts, which may lead to poor financial behaviour (Atkinson and Messy 2012; Hilgert et al. 2003). Previously it has been reported that in medical students, those with lower financial knowledge displayed undesirable financial behaviour (Jayakumar et al. 2017). Hence, the lack of engagement in financial practices in medical professionals may predispose them to poor financial behaviour. Furthermore, when these medical professionals are in management positions, they may lack the skills to make sound financial decisions and practice good financial behaviour. Therefore, the low scores in financial behaviour and ultimately financial literacy in healthcare professionals are concerning as they may impact business success. Indeed, financial behaviour (Kotzé and Smit 2008; Ye and Kulathunga 2019), low financial literacy and poor management practices play a major role in small business failure (Kotzé and Smit 2008; Ye and Kulathunga 2019), business sustainability and growth (Adomako, Danso, and Ofori Damoah 2016; Ye and Kulathunga 2019).

The lack of engagement in the financial management of the business in healthcare professionals is not surprising as majority of business owners (83%) reported that they have never received training in business management and that they have not encountered any financial or economic training during their medical education. Other studies have also reported a lack of training in financial concepts during the medical curriculum (Ahmad et al. 2017; Jayakumar et al. 2017). Importantly, training in business finance and economics was the only variable that predicted business-related financial literacy in the current study. These findings are similar to previous results that showed training in business and finance-related subjects independently predicted financial literacy in healthcare professionals (Jayakumar et al. 2017). Considering the low proportion of participants who have received business management training and it being the only variable that predicted business related financial literacy, our results suggest that generally healthcare professionals may be ill-equipped at successfully managing private practices or making sound financial business decisions. This finding has consequences for the socio-economic development and growth of the healthcare system in South Africa.

Besides the socio-economic consequences, the strong association between education in economics related subjects and financial literacy in healthcare professionals also has important implications for health sciences education. In this regard, the theoretical framework that underpins financial literacy can be drawn from several psychological theories. Several different psychological theories propose that financial literacy is the result of an interaction between personal attributes, knowledge, skills and engagements with the environment (King and Levine 1993; Nanziri and Leibbrandt 2018). Moreover, the conceptual definition of financial literacy requires both the acquisition of financial knowledge and skills and the ability to apply this knowledge (Zait and Bertea 2015). Therefore, if financial literacy is a product of knowledge, skills acquired and interaction with the environment, then it is important to consider whether the current approach to health sciences education adequately prepares students for competency in financial literacy.

Health sciences education is informed by several theories, each with its own merits (Kauffman 2019, 37-69). Although a comprehensive discussion of each learning theory is beyond the scope of this work, it is important to consider some of these theories used in health science education, to better understand the current results. Behavioural, cognitive learning and experiential learning theories often form the basis of health professions education, as the curricula of health sciences programmes are largely competency or outcomes based (Taylor and Hamdy 2013; Killen and Hattingh 2004). However, behaviourist learning approaches are limited in that they are teacher-centred rather than learner centred. Learners are instructed what to learn and know and are assessed based on these outcomes, rather than allowing them to take ownership of their learning (Killen and Hattingh 2004). These passive learning approaches fail to provide students with the necessary tools to be able to find the knowledge and skills they need. Indeed, evidence has shown that current health professions education produces a mismatch in the competencies of health professionals compared to the demands of the health system (Frenk et al. 2010). As a result, more constructivist learning approaches, which are characterised by active learning strategies, have received considerable attention in health professions education (Sandars and Cleary 2011). There are several theories in this category, the first of which is based on humanistic theories that promote self-directed learning (Taylor and Hamdy 2013). Self-directed learning theories suggest that learners are able to plan, conduct and assess their own learning (Sandars and Cleary 2011). However, the major shortcoming of a pure self-directed learning approach is that it ignores the social context of learning, and it has been questioned whether it is truly achievable (Taylor and Hamdy 2013). Indeed, the social context is critical in learning. In this regard, the importance of communities of practice is highlighted as a major influence in social learning theories. This suggest that both the context and the community influence learning (Taylor and Hamdy 2013). Other theories included in the constructivist category include self-determination theory and reflective learning, where both the motivation and self-reflective practice of the student are considered central aspects to learning (Sandars and Cleary 2011).

The knowledge domain is critical for the health care professionals and hence behaviourism has it merits in health professions education. However, several other outcomes in health professionals are related to attitude, such as professionalism, communication, empathy and professional development (Taylor and Hamdy 2013). Moreover, several skills from the affective learning domains such as leadership, management and governance have been incorporated in the core competencies of health professions (South African Qualifications Authority 2012). When active learning approaches are taken from constructivism and contextualized through communities of practice, there is potential for the development of additional skills that are not situated in the cognitive learning domain (Taylor and Hamdy 2013). Indeed, the redesign of health professions education to better address the needs of the health system has received considerable attention (Frenk et al. 2010). It has been suggested that there is a need to move from informative learning (acquiring knowledge and skills) to transformative learning, that impacts on attitudes and beliefs, and leads to the development of transformational leaders and societal reform (Frenk et al. 2010; Freire 1970). However, the implementation has been slow (Frenk et al. 2010). Interestingly, in the current study, self-rated financial knowledge was significantly lower than the actual financial knowledge score obtained in the questionnaire. Previously Zait and Bertea (2015) suggested that people are unaware of their deficiency of financial knowledge, yet our results have shown medical professionals seem to underestimate their financial knowledge. This may be, in part, as a result of the behaviourist and the passive learning approaches in health professions education. Because financial, management and leadership skills are not part of the outcomes in the current medical curricula, students perceive their knowledge in this regard as poor. Hence, there is a need to equip students with the tools to become self-regulated learners that possesses the metacognition to take responsibility to learn the skills they need, rather than waiting for someone else to structure their learning path.

LIMITATIONS AND FUTURE RESEARCH

The method of distribution of questionnaires may have result in a non-representative sample. Questionnaire data are cross sectional and hence inferences about cause and effect may not be drawn. The comparability of financial literacy between healthcare professionals in the current study (2020) and a prior study in the general South African population (Atkinson and Messy 2012) may be limited as financial literacy in the general population may have changed over the past decade. Nevertheless, this the aforementioned study is the only available study that used a similar measurement tool to assess financial literacy in the general population (Atkinson and Messy 2012). Moreover, more recent data on financial literacy (Nanziri and Leibbrandt 2018) and financial behaviour (Zwane et al. 2016) in South Africans using different measuring tools are comparable to the findings from earlier reports (Atkinson and Messy 2012) as well as the current results. Although our findings were similar to previous reports in healthcare professionals in the USA, using different instruments to measure financial literacy may limit the comparability of the results. Therefore, the research may not be generalizable to healthcare professionals outside South Africa. Nevertheless, future studies should determine whether medical professionals may benefit for exposure to financial literacy training during their clinical training or as part of continued professional development, to ensure sustainable business management practices for small enterprises and state healthcare facilities.

CONCLUSION

Our results suggest that general financial knowledge, is relatively high in healthcare professionals compared to the general South African population, which may be ascribed to the level of education in this cohort. Despite high financial knowledge scores, many healthcare professionals did not display good financial behaviour. Healthcare professionals struggled to meet their household and/or business financial needs and borrowing behaviour was higher in healthcare professionals than in the general South African population. Majority of healthcare professionals favoured a short-term outlook to finances and may be a cause for concern in this group. Although general financial literacy may be relatively high in healthcare professionals, this was not predictive of business-related financial behaviour or financial literacy. Our results of low scores in business related financial literacy are similar to previous reports in healthcare professionals globally. Attitudes towards finances in healthcare professionals are particularly concerning, which may impact financial decision making and sustainability and growth of medical practices and medical departments in state healthcare. Our results further strengthen the need for health professions education and training programs that ensure the development of a holistic health workforce. Health professionals who will not only be able to deliver quality health services, but who are also skilled in management and governance to strengthen the health system in South Africa.

ACKNOWLEDGEMENTS

The authors would like to thank the participants in the study and the relevant professional societies for distributing the questionnaires.

COMPETING INTERESTS

The authors declare no competing interest exists.

FUNDING SOURCES

The authors received no financial support for the research, authorship, and/or publication of this article

DATA AVAILABILITY

Derived data supporting the findings of this study are available from the corresponding author upon reasonable request.

DISCLAIMER

The views and opinions expressed in this article are those of the authors and do not necessarily reflect the official policy or position of any affiliated agency of the authors.

REFERENCES

Adomako, Samuel, Albert Danso, and John Ofori Damoah. 2016. "The moderating influence of financial literacy on the relationship between access to finance and firm growth in Ghana." Venture Capital 18(1): 43-61. https://doi.org/10.1080/13691066.2015.1079952. [ Links ]

Ahmad, Fahd A., Andrew J. White, Katherine M. Hiller, Richard Amini, and Donna B. Jeffe. 2017. "An assessment of residents' and fellows' personal finance literacy: an unmet medical education need." International Journal of Medical Education 8: 192. https://doi.org/10.5116/ijme.5918.ad11. [ Links ]

Atkinson, Adele and Flore-Anne Messy. 2012. "Measuring Financial Literacy: Results of the OECD / International Network on Financial Education (INFE) Pilot Study" https://doi.org/10.1787/5k9csfs90fr4-en. (Accessed 12 December 2019). [ Links ]

Bennett, Jarred S., Patricia A. Boyle, Bryan D. James, and David A. Bennett. 2012. "Correlates of health and financial literacy in older adults without dementia." BMC Geriatrics 12(1): 30. https://doi.org/10.1186/1471-2318-12-30. [ Links ]

Chen, Haiyang and Ronald P. Volpe. 1998. "An analysis of personal financial literacy among college students." Financial Services Review 7(2): 107-128. https://doi.org/10.1016/S1057-0810(99)80006-7. [ Links ]

Cude, Brenda J. 2010. "Financial Literacy 501." Journal of Consumer Affairs 44(2): 271-275. https://doi.org/10.1111/j.1745-6606.2010.01168.x. [ Links ]

Dahmen, Pearl and Eileen Rodriguez. 2014. "Financial literacy and the success of small businesses: An observation from a small business development center." Numeracy 7(1): 3. http://dx.doi.org/10.5038/1936-4660.7.1.3. [ Links ]

Fatoki, Olawale. 2014. "The financial literacy of micro entrepreneurs in South Africa." Journal of Social Sciences 40(2): 151-158. https://doi.org/10.1080/09718923.2014.11893311. [ Links ]

Freire, Paulo. 1970. Pedagogy of the oppressed. New York: Seabury Press. [ Links ]

Frenk, Julio, Lincoln Chen, Zulfiqar A. Bhutta, Jordan Cohen, Nigel Crisp, Timothy Evans, Harvey Fineberg, et al. 2010. "Health professionals for a new century: Transforming education to strengthen health systems in an interdependent world." The Lancet 376(9756): 1923-1958. https://doi.org/10.1016/S0140-6736(10)61854-5. [ Links ]

Health Professions Council of South Africa. 2018. "Annual Report 2017/18." https://www.hpcsa.co.za/Uploads/editor/UserFiles/downloads/publications/annual _reports/hpcsa_annual_report_2017_2018.pdf. (Accessed 12 September 2019). [ Links ]

Helbing, R. 2016. "Top ten reasons why medical practices fail to maximize revenue." https://suncoastadvisorygroup.com/top-ten-reasons-medical-practices-fail-to-maximize-revenue/. (Accessed 14 September 2019). [ Links ]

Hilgert, Marianne A., Jeanne M. Hogarth, and Sondra G. Beverly. 2003. "Household financial management: The connection between knowledge and behavior." Federal Reserve Bulletin 89: 309-322. [ Links ]

HPCSA see Health Professions Council of South Africa.

Huston, Sandra J. 2010. "Measuring financial literacy." Journal of Consumer Affairs 44(2): 296-316. https://doi.org/10.1111/j.1745-6606.2010.01170.x. [ Links ]

Jayakumar, Kishore L., D. Justin Larkin, Sara Ginzberg, and Mitesh Patel. 2017. "Personal Financial Literacy Among U.S. Medical Students." MedEdPublish 6(1): 35. https://doi.org/10.15694/mep.2017.000035. [ Links ]

Joo, So-Hyun and John E. Grable. 2000. "Improving employee productivity: The role of financial counseling and education." Journal of Employment Counseling 37(1): 2-15. https://doi.org/10.1002/j.2161-1920.2000.tb01022.x. [ Links ]

Kalish, D. 2016. "Top 10 Reasons Functional Medicine Practices Fail". The Element Online. https://edu.emersonecologics.com/2016/06/23/top-10-reasons-functional-medicine-practices-fail/. (Accessed 16 September 2019). [ Links ]

Kauffman, David M. 2019. "Teaching and learning in medical education: How theory can inform practice." In Understanding medical education: Evidence, theory, and practice, ed. Tim Swanwick, Kirsty Frost and Bridget C. O'Brien, 37-69. Oxford: Wiley. [ Links ]

Killen, Roy and S. A. Hattingh. 2004. "A theoretical framework for measuring the quality of student learning in outcomes-based education: Perspectives on higher education." South African Journal of Higher Education 18(1): 72-86. https://hdl.handle.net/10520/EJC37053. [ Links ]

King, Robert. G. and Ross Levine. 1993. "Finance and growth: Schumpeter might be right." The Quarterly Journal of Economics 108(3): 717-737. https://doi.org/10.2307/2118406. [ Links ]

Kinnunen, Ulla and Lea Pulkkinen. 1998. "Linking economic stress to marital quality among Finnish marital couples: Mediator effects." Journal of Family Issues 19(6): 705-724. https://doi.org/10.1177/019251398019006003. [ Links ]

Kotzé, Liezel and Alphonso v. A. Smit. 2008. "Personal financial literacy and personal debt management: The potential relationship with new venture creation." The Southern African Journal of Entrepreneurship and Small Business Management 1(1): 35-50. https://doi.org/10.4102/sajesbm.v1i1.11. [ Links ]

Lusardi, Annamaria and Olivia S. Mitchell. 2007. "Baby boomer retirement security: The roles of planning, financial literacy, and housing wealth." Journal of Monetary Economics 54(1): 205224. https://doi.org/10.1016/j.jmoneco.2006.12.001. [ Links ]

Lusardi, Annamaria and Olivia S. Mitchell. 2011. "Financial literacy around the world: An overview." Journal of Pension Economics and Finance 10(4): 497-508. https://doi.org/10.1017/S1474747211000448. [ Links ]

Lusardi, Annamaria and Peter Tufano. 2015. "Debt literacy, financial experiences, and overindebtedness." Journal of Pension Economics & Finance 14(4): 332-368. https://doi.org/10.3386/w14808. [ Links ]

Maphumulo, Winnie T. and Busisiwe R. Bhengu. 2019. "Challenges of quality improvement in the healthcare of South Africa post-apartheid: A critical review." Curationis 42(1): 1-9. https://doi.org/10.4102/curationis.v42i1.1901. [ Links ]

Meela, M., E. Libhaber, and B. Kramer. 2021. "Tranformation of a health sciences postgraduate population (2008-2017) at a higher education institution in South Africa: Has this occurred?" South African Journal of Higher Education 35(1): 209-230. [ Links ]

Nanziri, Elizabeth L. and Murray Leibbrandt. 2018. "Measuring and profiling financial literacy in South Africa." South African Journal of Economic and Management Sciences 21(1): 1-17. http://dx.doi.org/10.4102/sajems.v21i1.1645. [ Links ]

Organisation for Economic Cooperation and Development. 2018. "OECD/INFE Toolkit for Measuring Financial Literacy and Financial Inclusion" http://www.oecd.org/financial/education/2018-INFE-FinLit-Measurement-Toolkit.pdf. (Accessed 9 September 2019. [ Links ])

Organisation for Economic Cooperation and Development. 2019. "OECD/INFE survey instrument to measure the financial literacy of MSMEs." http://www.oecd.org/financial/education/2019-survey-to-measure-msme-financial-literacy.pdf. (Accessed 9 September 2019. [ Links ])

OECD see Organisation for Economic Cooperation and Development.

Oseifuah, Emmanuel Kojo. 2010. "Financial literacy and youth entrepreneurship in South Africa." African Journal of Economic and Management Studies 1(2): 164-182. http://dx.doi.org/10.1108/20400701011073473. [ Links ]

Perry, Jennifer, Foster Mobley, and Matt Brubaker. 2017. "Most doctors have little or no management training, and that's a problem." Harvard Business Review 2 no 8. [ Links ]

PookieMD. 2008. "10 Reasons your medical practice is failing, and how to fix it." https://pookiemd.wordpress.com/2008/11/21/10-reasons-your-medical-practice-is-failing-and-how-to-fix-it/. (Accessed 16 September 2019). [ Links ]

Remund, David L. 2010. "Financial literacy explicated: The case for a clearer definition in an increasingly complex economy." Journal of Consumer Affairs 44(2): 276-295. https://doi.org/10.1111/j.1745-6606.2010.01169.x. [ Links ]

Rispel, Laetitia C., Pieter De Jager, and Sharon Fonn. 2016. "Exploring corruption in the South African health sector." Health Policy and Planning 31(2): 239-249. https://doi.org/10.1093/heapol/czv047. [ Links ]

Sandars, John and Timothy J. Cleary. 2011 "Self-regulation theory: Applications to medical education: AMEE Guide No. 58." Medical Teacher 33:11: 875-886. https://doi.org/10.3109/0142159X.2011.595434. [ Links ]

South African Qualifications Authority. 2012. Core Competencies for Undergraduate Students in the Clinical Associate, Dentistry and Medical Teaching and Learning programmes in South Africa. Pretoria: South African Qualifications Authority. [ Links ]

Taylor, David C. M. and Hossam Hamdy. 2013. "Adult learning theories: Implications for learning and teaching in medical education: AMEE Guide No. 83." Medical Teacher 35(11): e1561-e1572. https://doi.org/10.3109/0142159X.2013.828153. [ Links ]

Van Rooij, Maarten, Annamaria Lusardi, and Rob Alessie. 2011. "Financial literacy and stock market participation." Journal of Financial Economics 101(2): 449-472. https://doi.org/10.1016/j.jfineco.2011.03.006. [ Links ]

Van Staden, D. 2021. "Investing in health professions education: A national development imperative for South Africa." South African Journal of Higher Education 35(1): 231-245. [ Links ]

Walter, A. 2015. "Top 4 reasons why medical practices fail ... and how you can mitigate your risk." https://blog.gppcpa.com/blog/2015/07/30/top-4-reasons-why-medical-practices-fail-and-how-you-can-mitigate-your-risk. (Accessed 14 September 2019. [ Links ])

WHO see World Health Organisation.

World Health Organisation. 2016. "Global strategy on human resources for health: Workforce 2030. " Geneva: World Health Organization. https://www.who.int/hrh/resources/global_strategy_workforce2030_14_print.pdf. (Accessed 20 April 2021. [ Links ])

World Health Organisation. 2010. "Monitoring the building blocks of health systems: A handbook of indicators and their measurement strategies." Geneva: World Health Organization. https://www.who.int/healthinfo/systems/WHO_MBHSS_2010_full_web.pdf. (Accessed 20 April 2021. [ Links ])

Ye, Jianmu and K. M. M. C. B. Kulathunga. 2019. "How does financial literacy promote sustainability in SMEs? A developing country perspective." Sustainability 11(10): 2990. https://doi.org/10.3390/su11102990. [ Links ]

Zait, Adriana and Patricea Elena Bertea. 2015. "Financial literacy - Conceptual definition and proposed approach for a measurement instrument." The Journal of Accounting and Management 4(3): 37-42. [ Links ]

Zwane, Talent, Lorraine Greyling, and Mokadi Maleka. 2016. "The determinants of household savings in South Africa: A panel data approach." International Business & Economics Research Journal 15(4): 209-218. https://doi.org/10.19030/iber.v15i4.9758. [ Links ]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}