Serviços Personalizados

Artigo

Inglês (pdf)

Inglês (pdf)

Artigo em XML

Artigo em XML Referências do artigo

Referências do artigo

Indicadores

Links relacionados

-

Citado por Google

Citado por Google -

Similares em Google

Similares em Google

Compartilhar

Permalink

PermalinkActa Commercii

versão On-line ISSN 1684-1999

versão impressa ISSN 2413-1903

Acta Commer. vol.23 no.1 Johannesburg 2023

http://dx.doi.org/10.4102/ac.v23i1.1049

ORIGINAL RESEARCH

Psychometric properties of an organisational effectiveness measure for state-owned enterprises

Petrus NelI; Martina KotzeII; Edson BadaraiIII

IDepartment of Industrial Psychology and People Management, School of Management, University of Johannesburg, Johannesburg, South Africa

IIDepartment of Industrial Psychology, Faculty of Economic and Management Sciences, University of the Free State, Bloemfontein, South Africa

IIIUFS Business School, Faculty of Economic and Management Sciences, University of the Free State, Bloemfontein, South Africa

ABSTRACT

ORIENTATION: Academics and practitioners raised concerns over appropriate public sector effectiveness measurement systems. In the case of state-owned enterprises (SOEs), selecting appropriate effectiveness measures is challenging. They are often set up for service provision and profitability while competing values, expectations and demands of various stakeholders are inherently part of their functioning

RESEARCH PURPOSE: To examine the psychometric properties of an adapted organisational effectiveness measure for SOEs, based on the competing values framework (CVF).

MOTIVATION FOR THE STUDY: Literature proposes the need for ongoing review of more appropriate and psychometrically sound effectiveness measures for SOEs.

RESEARCH DESIGN, APPROACH AND ME THOD: A quantitative, cross-sectional research design was employed to collect and analyse data from 302 managerial and non-managerial staff at 12 SOEs in Zimbabwe. Exploratory and confirmatory factor analysis, as well as bifactor analysis were employed to investigate the most appropriate solution.

MAIN FINDINGS: Various sub-dimensions of the CVF had acceptable reliabilities (≥ 0.8). Both the four-dimensional (rational goal, human relations, open systems and internal processes) and unidimensional (organisational effectiveness) factor structures had acceptable goodness-of-fit. In addition, omega hierarchical and explained common variance (associated with the bifactor model) supported the presence of a strong general factor (organisational effectiveness

PRACTICAL/MANAGERIAL IMPLICATIONS: Researchers may use this adapted measure of organisational effectiveness to understand the effectiveness of SOEs better. If managers require a fine-grained measure of the CVF dimensions, emphasis should be placed on the four-dimensional structure.

CONTRIBUTION/VALUE-ADD: The present study found that various statistical techniques are required to understand the most relevant conceptualisation and operationalisation of the CVF for use within semi-state organisations.

Keywords: organisational effectiveness; competing values framework (CVF); stakeholders; state owned enterprises (SOEs); exploratory factor analysis (EFA); confirmatory factor analysis; bifactor analysis.

Introduction

The economic and socio-political importance of state-owned enterprises (SOEs) has significantly increased in recent years. State-owned enterprises play a substantial role in many economies as they form part of fundamental industries, such as telecommunications, electricity and transportation, that are responsible for delivering key infrastructure services (Kikeri 2018; Klovienė & Gimžauskien 2014; Masekoameng & Mpehle 2018). They also contribute to the growth of both state and non-state economic sectors, while providing valuable fiscal resources (Mbo 2017; Tanlamai & Juta 2011). State-owned enterprises refer to enterprises where the state has either full, majority or significant minority ownership and significant control over the organisation (Organisation for Economic Co-operation and Development 2005) and usually has both public policy objectives and commercial objectives (Kikeri 2018). With a strong obligation to create public value (Cole & Parston 2006), these enterprises are expected to be managed in such a way as to ensure financial sustainability but also contribute to the public good (Masekoameng & Mpehle 2018). An SOE is usually not a single organisation, often consisting of a number of diverse entities with different mandates, requiring different scales of operation (Lindquist & Marcy 2014).

To ensure SOEs deliver on their public and financial mandates, emphasis should be placed on the effectiveness, efficiency and quality of their operations (Klovienė & Gimžauskien 2014). As these enterprises seek to please as many stakeholders as possible while achieving results (Bezuidenhout 2021), they are, like other profit-making public or non-profit organisations, under continuous scrutiny and pressure to develop strategies and adapt management practices to satisfy changing public needs and expectations (Eydi 2015). The effectiveness of SOEs should be measured regularly - not only to keep government informed of the effectiveness of these enterprises in terms of their contribution towards the well-being of society, but also to elicit the reasons for their effectiveness or ineffectiveness. This feedback is also key in assisting management in decision making, promoting transparency and stakeholder engagement and consolidating organisational processes (Burksiene & Dvorak 2020).

The failure of organisations, including the failure of SOEs, can be because of many factors (i.e. political, economic, social and technological changes). However, studies suggest that SOEs tend to be less effective than comparable private sector organisations (Pratuckchai & Patanapongse 2012), specifically in terms of financial sustainability (Masekoameng & Mpehle 2018) and service delivery (Kikeri 2018). According to Mbo (2017), several factors interact with each other to influence SOE performance, including governance, political and stakeholder interaction, as well as resource availability. Governance problems relate to issues such as a lack of disclosure practices to ensure accountability and transparency, as well as a lack of appropriate performance management systems (Kikeri 2018). In addition, Klovienė and Gimžauskien (2014) state that the accountability for the effectiveness of SOEs involves a complicated network of actors (management, ownership entities, ministries and government) - which gives rise to difficulties in corporate governance. Also, political pressures and activities often seem to affect the good governance of SOEs decisively in developing countries - not only leading to frequent leadership changes (Bezuidenhout 2021), but also sometimes exerting influence over the entire enterprise (Ikeanyibe et al. 2020; Mbo 2017). Studies (Luong, Jorissen & Paeleman 2019; Mbo 2017) showed that the higher the government's share in a SOEs capital, the significantly fewer economic and ethical indicators are included in the measurement of its effectiveness; and the higher the level of government involvement in SOEs operational affairs, the more detrimental it is to their performance.

The literature has shown that there is a difference in how organisational effectiveness is measured in the public sector in comparison to the private sector (Olivier 2014), as these two sectors differ in relation to interested stakeholders, purpose, objectives, motivations, flexibility, culture and impact of decisions (Bezuidenhout 2021; Cristina & Ticlau 2012). In contrast to private sector corporations, SOEs are often protected from major threats affecting private companies, such as bankruptcy and takeovers (Organisation for Economic Co-operation and Development 2005). Some authors argue that it is easier to assess private sector organisations' effectiveness because profit as an effectiveness criterion is mostly used in the private sector (Aubert & Bourdean 2012; Olivier 2014). Although financial measures also apply to the public sector (Masekoameng & Mpehle 2018), profit maximisation is not the major purpose of public sector organisations (Aubert & Bourdean 2012). Public organisations usually pursue multiple goals simultaneously, of which most outcomes are non-economical. The use of financial indicators only therefore could mask the real effectiveness of public organisations, thereby misinforming stakeholders and compromising the quality of service delivery (Mihaiu 2014). Furthermore, SOEs have various internal and external stakeholders with diverse value perspectives that influence their views and interpretation of the entity's activities and results (Martz 2008). These competing values culminate in competing demands and expectations (Lindquist & Marcy 2014) that necessitate the recognition of the existence of several competing logics (Aubry & Hobbs 2011). In other words, the pursuit of certain important values in governance inevitably limits pursuing other values; for instance, efficiency and equality necessarily conflict with each other in public policies (Lindquist & Marcy 2014; Van der Wal, De Graaf & Lawton 2011).

Concerns have been raised by academics and practitioners who expressed that effectiveness measurement systems are elusive and problematic to implement in the public sector (Kloot & Martin 2000; Muterera et al. 2012). More specifically, Moynihan and Pandey (2004) and Muterera et al. (2012) highlight the difficulties in finding objective measures of effectiveness in the case of public sector organisations. This is because of multiple programmes embarked on by the public sector, which make it difficult to compute organisational effectiveness on a unitary objective measure. Some researchers (Škerlavaj et al. 2007) emphasise that organisational effectiveness cannot be measured without taking organisational goals into account. However, in the case of the public services sector, a multi-goal orientation is required, as the consequences of the various needs, expectations and perceptions of the multiplicity of stakeholders (e.g. society, employees, shareholders, lenders, customers, suppliers and government) for the organisation's effectiveness should be considered (Cuganesan, Guthrie & Vranic 2014; Hillman & Keim, 2001; Martínez-González & Martí 2006). It can be argued that the value-based nature of organisational effectiveness is often ignored in the measurement of organisational effectiveness (Martz 2008).

This calls into question the issue of the appropriateness of effectiveness measures in SOEs. As the measurement of SOE effectiveness is a necessity for policymakers, academia and civil society, effectiveness criteria that are holistic and all-encompassing in nature need to be applied - especially where SOEs are set up for both service provision as well as profitability. The lack of agreement on a single organisational effectiveness measure that is appropriate for all scenarios of organisational setups (Mafini & Pooe 2013) accentuates the need for the constant review of more appropriate measures for SOEs (Gao 2015; Heath & Radcliffe 2007).

Aim of the study

In the light of the need for the continuous review of appropriate effectiveness measures for SOEs, the aim of this study was to examine the psychometric properties of an adapted measure of organisational effectiveness for SOEs based on the competing values framework (CVF).

Literature review

Organisational effectiveness: The construct

Although organisational effectiveness serves as the theoretical focal point for all organisational models and represents the ultimate outcome variable for organisational studies (Eydi 2015), its conceptualisation, explanation and measurement still pose substantial challenges (Eydi 2015; Martz 2008; Oghojafor, Muo & Aduloju 2012; Olivier 2014). Several authors agree that there is no universal definition of organisational effectiveness: it means different things to different people (Eydi 2015; Martz 2008) with definitions being influenced by the conceptual worldview of the researchers studying it (Oghojafor et al. 2012). However, the majority of authors agree that the organisational effectiveness construct is multidimensional and complex and that it requires the evaluation of different functions and the measuring of multiple criteria, while both processes (means) and outcomes (ends) should be considered in assessing the construct (Eydi 2013; Martz 2008; Oghojafor et al. 2012).

For the purpose of this study, organisational effectiveness is defined as a 'socially constructed, abstract notion' (Quinn & Rohrbaugh 1983:374) that is broader than the concepts of organisational performance (e.g. shareholder return and financial, operational and product market performance) (Olivier 2014) and organisational efficiency (e.g. the amount of resources involved) (Martz 2008). Where the evolution of organisational effectiveness models reflects a construct perspective, the evolution of organisational performance and efficiency measures reflects a process perspective (Martz 2008). Therefore, organisational effectiveness encapsulates both organisational performance and efficiency (Martz 2008; Venkatraman & Ramanujam 1986), as well as additional external indicators or measures that pertain to factors beyond economic assessment that are important to customers, managers and shareholders (e.g. social responsibility) (Richard et al. 2009).

Models of organisational effectiveness: The competing values framework

There are several models or frameworks used to measure organisational effectiveness. These models reflect different values and preferences of schools of thought regarding effectiveness. According to Eydi (2013) the best-known models are the goal model, the system resource model, the internal process approach, the multiple constituency models and the competing values approach. The goal attainment approach is characterised by an identification of goals to measure organisational effectiveness. However, in the case of the public services sector, a multi-goal orientation is required, as the effects of the various needs, expectations and perceptions of the multiplicity of stakeholders (e.g. society, employees, shareholders, lenders, customers, suppliers and government) on the organisation's effectiveness should be considered (Hillman & Keim 2001). The system resource approach focuses on an organisation's ability to attract resources to ensure viability and highlights the ability to measure some inputs and outputs, but this is not necessarily a measure of effectiveness (Eydi 2013). The internal process approach emphasises the importance of the dynamics among employees as an important effectiveness criterion and regards factors such as trust, integrated systems and smooth functioning as more accurate measures of organisational effectiveness compared to, for example, the goal attainment approach. The strategic-constituencies approach focuses on the identification of key stakeholders' views of effectiveness and how each constituent group has a different interest in the way the organisation performs (Eydi 2013).

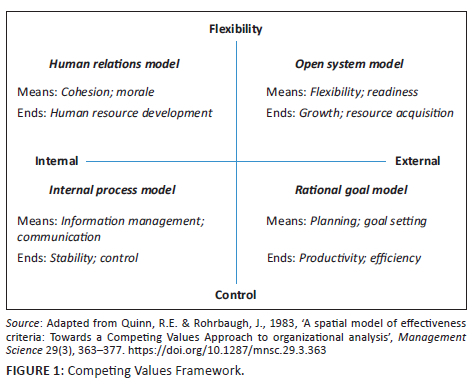

The CVF regards effectiveness as being based 'on the recognition that organizations goals are simultaneously pulled in opposite directions by the expectations of multiple constituencies' (Lee 2004:22) and that 'organisations do many things and have many outcomes', while having 'disagreements and competing viewpoints about what constitutes effectiveness: which goals to pursue and measure, and how to measure them' (Oghojafor et al. 2012:98). The CVF is the result of extensive theoretical and empirical organisational effectiveness research completed by expert scholars (Quinn 1981; Quinn & Rohrbaugh 1981) during the 1980s (Lee 2004; Lindquist & Marcy 2014; Ncume 2018) and is proposed as an organisational effectiveness approach applicable to the measurement of organisational effectiveness of SOEs (Muterera et al. 2012). The framework is anchored on mainly three axes or value dimensions (see Figure 1) and incorporates the organisational focus, organisational structure and the means and ends (Quinn & Rohrbaugh 1983). The organisational focus axis includes an internal and external thrust - where the internal thrust is the micro emphasis related to the well-being and development of employees, and the external thrust is the macro emphasis related to the well-being and development of the organisation. The organisational structure axis emphasises stability (control) and flexibility, while the value dimension relates to means and ends. Means focus on vital processes (such as planning and setting organisational goals), while ends emphasise the outcomes (such as productivity and efficiency) (Quinn & Rohrbaugh 1983).

In developing the CVF, Quinn and Rohrbaugh (1983) identified 17 effectiveness criteria. These criteria are sub-divided into the four models for effectiveness, namely the human relations model (HRM), rational goal model (RGM), internal process model (IPM) and open systems model (OSM). These criteria cater for various stakeholders.

The RGM holds that organisational effectiveness is related to goal achievement and emphasises control and an external focus (Gimžauskienė & Klovienė 2007; Quinn & Rohrbaugh 1983). This model assumes that organisations are there to pursue a purpose and to achieve a clear set of measurable goals as determined by the stakeholders (Muterera et al. 2012). Therefore, the organisation is regarded as effective if it achieves its specific objectives (Ncume 2018), which include productivity and profit (Morais & Graça 2013). Organisational effectiveness criteria in this model include planning and goal setting (as means) and productivity and efficiency (as ends) (Quinn & Rohrbaugh 1983).

The HRM emphasises staff cohesion and morale (means), as well as flexibility and an internal focus (Quinn & Rohrbaugh 1983). Other components of this model include human resource development (ends) and human commitment and training (Gimžauskienė & Klovienė 2007). The focus is on the fulfilment of employees' potential and their commitment to the organisation's operations. Organisations perform well in this area if participation, team cohesion and openness result in the overall development of employees (Muterera et al. 2012). Besides the participation of staff members, conflict resolution and consensus building are critical in the HRM (Morais & Graça 2013).

The OSM assumes that the organisation must have resources in the form of goods and services from the environment, which are then used productively in pursuit of organisational goals (Muterera et al. 2012). This model emphasises 'flexibility and readiness (as means) and growth, resource acquisition and external support (as ends)' (Quinn & Rohrbaugh 1983:371), and it is anchored in adaptation and innovation (Morais & Graça 2013). Furthermore, the OSM has some thrust towards the organisation's adaptation to the external environment (economic, social and political environment) (Gimžauskienė & Klovienė 2007), which is key to organisational effectiveness (Tregunno et al. 2004). An organisation that is flexible and adaptable, with the ability to utilise the environment to obtain scarce and valuable resources, will therefore be effective (Muterera et al. 2012).

The IPM is focused on the internal (micro) environment and is based on stability and control (Tregunno et al. 2004). It has its focus on communication processes and how information is managed (as means), resulting in stability and control (as ends) (Muterera et al. 2012). Effectiveness is therefore based on the processes involved in the production and provision of goods and services. Besides showing how various processes are to be measured, the IPM also involves documentation, defining responsibility and measurement. These are important to ensure that there is clarity on roles and responsibilities, besides showing how various processes are to be measured (Morais & Graça 2013).

The CVF integrates the competing values in an organisation (i.e. all four models) into a single framework to assist organisations to deal with the dilemma of competing models. Even though these models compete, they can be combined in the CVF, depicting an organisation as a political arena with the different competing models interacting with each other (Minvielle et al. 2008). The dimensions represented by the four models of the CVF (Quinn & Rohrbaugh 1983) show what people value about an organisation's effectiveness. As an effectiveness measurement system, the CVF is effective in helping meet the various stakeholders' requirements (Atkinson, Waterhouse & Well 1997). Whetten and Cameron (1994:141) argue that this framework allows for the inherently paradoxical nature of organisational life where managers 'must not only make trade offs between day-to-day competing demands on the organization's resources', but they also must 'balance competing expectations regarding the identity of the organization as an institution'. The CVF further emphasises that the pursuit of a single criterion of organisational effectiveness is less likely to become effective than is a broader and a more balanced approach (Gulosino, Franceschini & Hardman 2016). Therefore, it provides an integrated and systematic approach to investigate organisational effectiveness, allowing for flexibility when dealing with diverse organisational settings and contexts (Lee 2004).

Van der Wal et al. (2011) regard the CVF as the most widely recognised model for competing values in management and organisation and state that the main tension described in this framework relates to present debates on reconciling opposing or clashing values. State-owned enterprises attempt to balance two conflicting values: traditional governmental or bureaucratic values (e.g. legality and neutrality) on the one hand and so-called business-like values (e.g. effectiveness, responsiveness, innovation and efficiency) on the other hand. The CVF is widely accepted and has also been used in a wide array of academic disciplines for organising and understanding many individual and organisational issues, such as organisational culture (Morais & Graça 2013), leadership (Komarek, Knight & Bielefeldt 2017), organisational decision making, organisational communication and organisational transition (Zlatković 2018).

Given the above discussion, it seems as if there are several benefits of applying the CVF to SOEs. Firstly, it can assist these entities to balance public interest and commercial goals (public good vs. financial sustainability). Secondly, SOEs will be in a better position to manage the expectations from multiple stakeholders (government, policy makers, employees and the public). Lastly, it is highly likely that when SOEs apply the CVF, they would be able to better manage the risks associated with competing values and interests of different stakeholders in terms of financial sustainability and reputation.

The measuring instrument

To operationalise the CVF, various measuring scales were developed to validate the framework. However, despite the fact that the CVF was developed to 'integrate the main dimensions of organizational effectiveness' (Morais & Graça 2013:129), many researchers used alternative conceptualisations of the CVF - focusing mostly on leadership behaviour or organisational culture, instead of organisational effectiveness (e.g. Helfrich et al. 2007; Vilkinas & Cartan 2006). Those studies that did use the framework to focus on the measuring of organisational effectiveness were mainly conducted towards the end of the previous century (Kalliath, Bluedorn & Gillespie 1999; Pounder 2000; Quinn & Spreitzer 1991), leaving a gap in more recent research to validate the basic assumptions of the CVF in measuring and describing organisational effectiveness (Zlatković 2018).

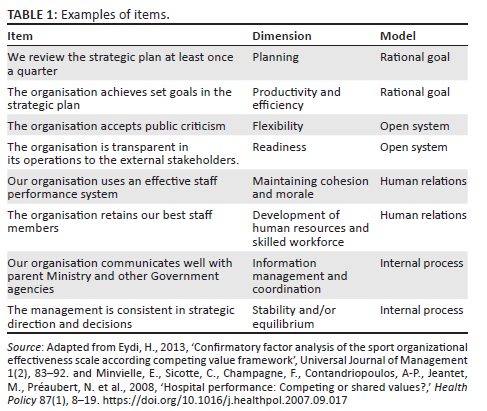

Quinn and Spreitzer (1991) developed a scale consisting of 16 items to measure organisational effectiveness based on the CVF. Using multidimensional scaling and multitrait-multimethod techniques, they found support for the four dimensions (i.e. models) associated with the CVF, as well as acceptable reliabilities for each of the four dimensions. Several other researchers investigated the usefulness of Quinn and Spreitzer's measuring scale using alternative statistical techniques. After conducting structural equation modelling and more specifically CFA, Kalliath et al. (1999) revised the 16-item scale developed by Quinn and Spreitzer and found acceptable goodness of fit for the four dimensions associated with the CVF. Subsequently, in order to measure the effectiveness of a hospital in Paris, Minvielle et al. (2008) developed a 66-item measure representing the four dimensions associated with the CVF and the results of the exploratory factor analysis (EFA) supported the four models associated with the CVF. Eydi (2013) developed a measure for organisational effectiveness representing the four dimensions associated with the CVF for use within a sporting federation. The 65-item measure focused on eight effectiveness dimensions, reflecting the means and ends associated with each of the four models.

After studying these various measuring scales, the present study opted to adapt the questions developed by Eydi (2013) and Minvielle et al. (2008) to be more relevant in the context of SOEs. For example, when considering the variable 'productivity' (which is part of the RGM), the original item focused on financial stability. However, the present study adapted this item to reflect the complexity of the SOE context, with one item focusing on the profitability of the SOE, while a second item focused on a weak cashflow position. The adapted measure consisted of 85 questions across all four of the models associated with the CVF: rational goal model (Planning = 11 items; Productivity and Efficiency = 11 items), OSM (Flexibility and Readiness = 12 items; Growth and Resource Acquisition = 10 items), HRM (Maintaining Cohesion and Morale = 11 items; Development of Human Resources and Skilled Workforce = 12 items), IPM (Information Management and Coordination = 11 items; Stability and/or Equilibrium = 7 items). A seven-point Likert scale was used to indicate how often the SOE successfully engaged in each activity (1 = Never; 7 = Almost always). Examples of items associated with the eight dimensions are shared in Table 1.

To determine the psychometric properties (i.e. reliability and validity) of an adapted organisational effectiveness measure within the context of SOEs, a quantitative, cross-sectional research design was employed.

Research methods and design

The study included SOEs operating in Zimbabwe. Twelve SOEs representing seven sectors (financial, transport, health, energy, power, telecommunications and petroleum) were included in the study. Using convenience sampling, managerial and non-managerial staff employed at these SOEs were approached to participate in the survey. A total of 302 participants completed the adapted organisational effectiveness measure.

To determine the psychometric properties of the adapted measure of organisational effectiveness (based on the CVF), several statistical techniques were used. A two-step process using factor analysis was employed. Firstly, EFA, including parallel analysis (Timmerman & Lorenzo-Seva 2011), was used to determine whether the items loaded on a single factor (i.e. model). FACTOR software was used to conduct the EFA (Lorenzo-Seva & Ferrando 2006). Secondly, CFA using Mplus (Muthén & Muthén 2017) was applied to evaluate the goodness of fit of the four-dimensional structure (rational goal, human relations, open systems and internal processes) of the CVF. This was compared with a competing conceptualisation of the four models measuring a single construct (i.e. organisational effectiveness) employing various goodness-of-fit statistics to evaluate the models (e.g. Comparative Fit Index [CFI], Root Mean Square Error of Approximation [RMSEA], Standardised Root Mean Square Residual [SRMR] and Akaike's Information Criterion [AIC]) (Hu & Bentler 1998, 1999). In addition to the CFA, the present study employed two bifactor statistical indices (omega hierarchical and explained common variance) to determine the presence of a general factor (i.e. organisational effectiveness). When both these indices are high (≥ 0.80 and ≥ 0.70, respectively) it is highly likely that the measure in question could be treated as unidimensional in nature (Rodriguez, Reise & Haviland 2015). The omega routine in the psych library (Revelle 2021) available in the R 4.05.00 statistical package (R Core Team 2021) was used to obtain estimates for both omega hierarchical and explained common variance.

Ethical considerations

Ethical clearance to conduct the study was obtained from the University of the Free State Faculty of Economic and Management Sciences Ethics Committee (No. UFS-HSD2017/1150). The ethics committee recommended that in order to safeguard the participants, no biographical data (e.g. gender, age, SOE employed at) be collected. Hence, the committee only granted ethical clearance for participants to complete the questions in the survey. As part of the informed consent process, participants were informed that their participation was voluntary and that their responses would be anonymous.

Results

The results associated with both exploratory and confirmatory factor analysis as well as the outcome of the bifactor analysis, follow.

Results of the exploratory factor analysis

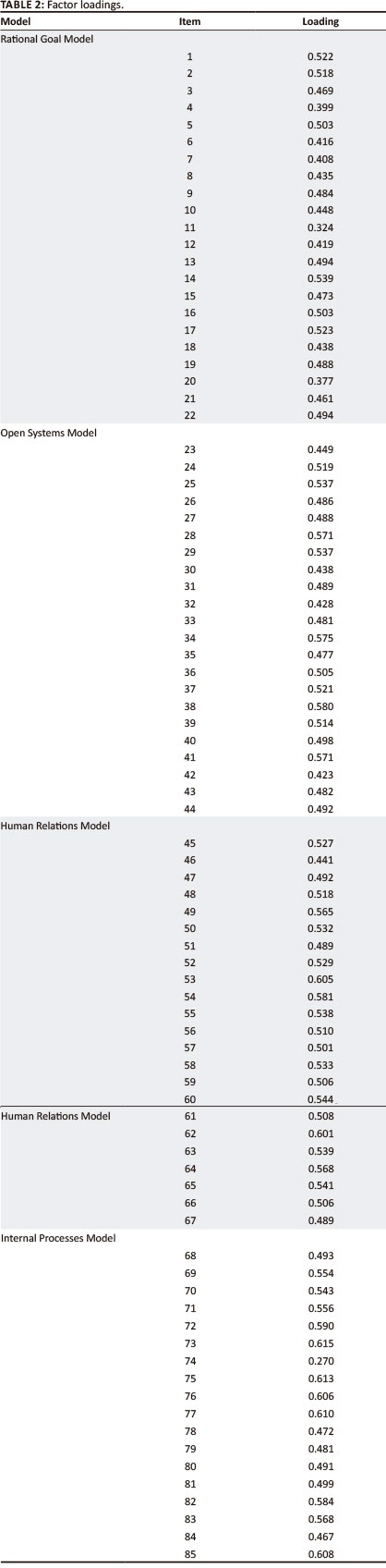

Parallel analysis suggested that the 22 items associated with the RGM are best viewed as a unidimensional construct. Regarding the factor structure of the OSM, parallel analysis suggested that the 22 items measure a unidimensional construct. A similar conclusion was reached for the 23 items associated with the HRM. Finally, the 18 items associated with the IPM also are best conceptualised as measuring a single construct. All the items had factor loadings of more than 0.3, except for item 74. However, the loading of this item was not substantially lower (0.270) and was therefore retained. According to Hair et al. (2006), factor loadings of 0.3 and higher are deemed statistically significant (see Table 2).

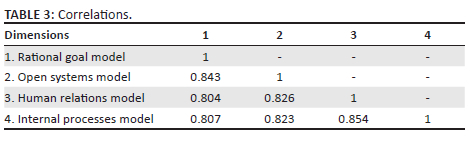

The reliability estimates for the four dimensions were: (1) RGM: α = 0.854; (2) OSM: α = 0.881; (3) HRM: α = 0.899; and (4) IPM: α = 0.873. The correlations among the four dimensions are reported in Table 3. It is evident that the four dimensions are highly correlated (≥ 0.8), suggesting that organisational effectiveness (as assessed by the present measure) might be unidimensional.

Results of the confirmatory factor analysis

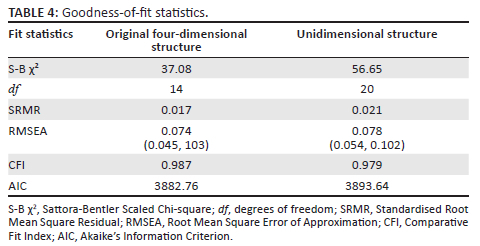

The present study continued to determine the goodness of fit associated with two different conceptualisations of the CVF: the original four-factor solution and a unidimensional factor solution. To minimise model complexity, item parcels were used to create indicators associated with each of the four models (Hair et al. 2006; Little et al. 2013). More specifically, the parcels reflected the various means and ends associated with each of the four models (as originally conceptualised by the CVF). In addition to this four-dimensional model, the present study also evaluated the goodness of fit associated with a unidimensional model (measuring organisational effectiveness) with the different means and ends associated with each of the four models of the CVF.

From Table 4, it is evident that both the correlated factor model (i.e. original four-dimensional structure associated with the CVF) and the unidimensional model have acceptable levels of fit, with the values associated with the RMSEA slightly above the recommended value (≤ 0.06) and the values associated with the SRMR below the recommended value (≤ 0.08) (Hu & Bentler 1988, 1999). In addition, the CFI was higher and better than the recommended value (≥ 0.95) (Hu & Bentler 1998, 1999). However, the original four-dimensional conceptualisation seems to be the better model when looking at AIC (which is lower than the AIC value of the unidimensional model).

Results of the bifactor analysis

The present study continued fitting a bifactor model (using all 85 items) to the data and conducted a Schmid-Leiman transformation to investigate the presence of a general factor. Omega hierarchical (0.83) and explained common variance (0.75) were obtained from the bifactor model. Both these values point to the presence of a general factor (i.e. organisational effectiveness).

Discussion

According to Moulin (2017), public sector organisations experience challenges related to: (1) the improvement of outcomes for various stakeholders (e.g. service users) and (2) developing measures of performance and effectiveness. The aim of this study was to examine the psychometric properties of an adapted measure of organisational effectiveness based on the CVF within the SOE context. The results were indeed promising.

The various items reflecting the four models associated with the CVF were found to be highly reliable. With all the reliability estimates exceeding 0.8, these results were slightly higher than those reported by Quinn and Spreitzer (1991), Kalliath et al. (1999) and Eydi (2013). Quinn and Spreitzer (1991) found acceptable reliabilities for each of the four dimensions: (1) human relations = 0.84; (2) internal processes = 0.77; (3) open systems = 0.81; and (4) rational goal = 0.78. Kalliath et al. (1999) also investigated the usefulness of Quin and Spreitzer's measuring scale and found all four dimensions had acceptable reliabilities (human relations = 0.90; internal process = 0.80; open systems = 0.83; and rational goal = 0.83) - which are fairly similar to those estimates reported in the present study. Although Minvielle et al. (2008), who conducted their research in a hospital setting, did not report the reliability estimates associated with each of the four models, they did state that 11 of the 13 sub-dimensions associated with the four models exceeded 0.7, while the sub-dimensions of effectiveness and productivity were 0.54 and 0.59, respectively.

In terms of model fit, the present study found acceptable goodness of fit associated with both the four-dimensional and unidimensional conceptualisations of organisational effectiveness (using the CVF). Although the four-factor model provided a slightly better fit with the data, the unidimensional factor model is preferable for the following reason: the four dimensions are highly correlated with one another, pointing to the possibility of a unidimensional structure. In addition, the results of the bifactor analysis point to a unidimensional structure when looking at the values associated with omega hierarchical and explained common variance. The results of the present study are mostly in line with those reported by Quinn and Spreitzer (1991), Kalliath et al. (1999) and Eydi (2013).

Quinn and Spreitzer (1991) also found support for two competing conceptualisations: a unidimensional model (representing a measure of organisational effectiveness) and a four-factor model with the sub-dimensions associated with the four models of the CVF. In terms of the four-factor model, the results of the present study are also fairly similar to those reported by Quinn and Spreitzer (1991).

Kalliath et al. (1999), who investigated the usefulness of Quin and Spreitzer's measuring scale by using structural equation modelling and confirmatory factor analysis, found acceptable goodness of fit for the four dimensions associated with the CVF based on a revised version of the 16-item measuring scale developed by Quinn and Spreitzer (1991) (χ2 = 111.14; df = 999; RMSEA = 0.02; Goodness of Fit Index = 0.98). Kalliath and his colleagues (1999) hypothesised that there would be positive and significant correlations among the four dimensions. However, this was not confirmed for the relationship between open systems and internal process dimensions. In contrast, the present study found significant positive correlations among the four dimensions associated with the CVF.

Eydi (2013) evaluated two competing conceptualisations by using confirmatory factor analysis: (1) a model consisting of the eight sub-dimensions associated with the four dimensions of the CVF and (2) a unidimensional model (with all eight sub-dimensions as indicators of organisational effectiveness). Although the four-factor model fitted the data well (CFI = 0.93; Non-normed Fit Index = 0.92), the unidimensional model fitted the data much better (CFI = 0.99, RMSEA = 0.039). The reliability estimates associated with the eight sub-dimensions all exceeded 0.7. The present study found the original four-dimensional model to be a slightly better conceptualisation than the unidimensional conceptualisation of organisational effectiveness (based on the goodness-of-fit statistics). However, based on the bifactor model, the results of the present study are similar to those of Eydi (2013) who found the unidimensional measure of organisational effectiveness to be a better conceptualisation than the four-factor model.

Although the present study found support for the reliability and validity of the adapted measure of organisational effectiveness for SOEs, it is not without limitations. Firstly, the study was conducted using a sample of 302 individuals employed in SOEs in Zimbabwe. Although the results are trustworthy, care should be taken when generalising the findings. It is suggested that future studies use the adapted measure in SOEs in other countries. Secondly, the adapted measure of organisational effectiveness is fairly lengthy. Although this did not deter the respondents from completing the survey, a shorter measure might need to be explored without negatively influencing the measurement properties of the scale. It is thus suggested that future studies investigate the possibility of a shorter measure for use in SOEs.

Conclusion

The results of the present study suggest that it would be more appropriate to use the adapted measure of organisational effectiveness based on the CVF as an indicator of overall organisational effectiveness. Although a four-dimensional structure was obtained, it appears that they are highly correlated. Future researchers are therefore encouraged to investigate the factor structure of this measure in various SOEs in different countries. It might also be useful to investigate the relative importance of each of the four models in a given SOE. Irrespective of the above, it can be concluded that if SOEs would like to obtain a measure of their overall effectiveness, the unidimensional structure should be used. However, when evidence about the four models of the CVF is required, the four-factor model conceptualisation could be considered.

Acknowledgements

Competing interests

The authors declare that they have no financial or personal relationships that may have inappropriately influenced them in writing this article.

Authors' contributions

P.N. was responsible for the visualisation and conceptualisation of the research, methodology; data analysis; and writing of the results, discussion and conclusion. M.K. was involved in the conceptualisation of the research; the writing of the introduction and literature review; the review and editing of the article. E.B. was responsible for the data-gathering, project administration and obtaining the necessary resources.

Funding information

This research received no specific grant from any funding agency in the public, commercial or not-for-profit sectors.

Data availability

The data that support the findings of this study are available upon reasonable request from the corresponding author, P.N.

Disclaimer

The views and opinions expressed in this article are those of the authors and do not necessarily reflect the official policy or position of any affiliated agency of the authors.

References

Atkinson, A.A., Waterhouse, J.H. & Well, R.B., 1997, 'A stakeholder approach to strategic performance measurement', Sloan Management Review Spring 38(3), 25-37. [ Links ]

Aubry, M. & Hobbs, B., 2011, 'A fresh look at the contribution of project management to organizational performance', Project Management Journal 42(1), 3-16. https://doi.org/10.1002/pmj.20213 [ Links ]

Aubert, B.A. & Bourdeau, S., 2012, 'Public sector performance and decentralization of decision rights', Canadian Public Administration 55(4), 575-598. https://doi.org/10.1111/j.1754-7121.2012.00238.x [ Links ]

Bezuidenhout, M., 2021, 'The effect of the economic crisis on pay-performance link in South African state-owned enterprises', South African Journal of Business Management 52(1), a1747. https://doi.org/10.4102/sajbm.v52i1.1747 [ Links ]

Burksiene, V. & Dvorak, J., 2020, 'Performance management in protected areas: Localizing governance of the Curonian Spit National Park, Lithuania', Public Administration Issues 5(SI), 105-124. https://doi.org/10.17323/1999-5431-2020-0-5-105-124 [ Links ]

Cristina, M. & Ticlau, T., 2012, 'Transformational leadership in the public sector: A pilot study using MLQ to evaluate leadership style in Cluj county local authorities', Revista de cercetare si interventie sociala 36, 74-98. [ Links ]

Cole, M. & Parston, G., 2006, Unlocking public value - A new model for achieving high performance in public service organizations, Wiley, Hoboken, NJ. [ Links ]

Cuganesan, S., Guthrie, J. & Vranic, V., 2014, 'The riskiness of public sector performance measurement: A review and research agenda,' Financial Accountability & Management 30(3), 279-302. https://doi.org/10.1111/faam.12037 [ Links ]

Eydi, H., 2013, 'Confirmatory factor analysis of the sport organizational effectiveness scale according competing value framework', Universal Journal of Management 1(2), 83-92. [ Links ]

Eydi, H., 2015, 'Organizational effectiveness models: Review and apply in non-profit sporting organizations', American Journal of Economics, Finance, and Management 1(5), 460-467. [ Links ]

Gao, J., 2015, 'Performance measurement and management in the public sector: Some lessons from research evidence', Public Administration and Development 35(2), 86-96. https://doi.org/10.1002/pad.1704 [ Links ]

Gimžauskienė, E. & Klovienė, L., 2007, 'Changes of performance measurement system: The role of organizational values', Economics and Management 12, 30-37. [ Links ]

Gulosino, C., Franceschini III, L. & Hardman, P., 2016, 'The influence of balance within the competing values framework and school academic success on teacher retention', Journal of Organizational & Educational Leadership 2(1), 3. [ Links ]

Hair, J.F., Black, B., Babin, B., Anderson, R.E. & Tatham, R.L., 2006, Multivariate data analysis, 6th edn., Prentice-Hall, Upper Saddle River, NJ. [ Links ]

Heath, G. & Radcliffe, J., 2007, 'Performance measurement and the English ambulance service', Public Money and Management 27(3), 223-228. https://doi.org/10.1111/j.1467-9302.2007.00583.x [ Links ]

Helfrich, C.D., Li, Y.F., Mohr, D.C., Meterko, M. & Sales, A.E., 2007, 'Assessing an organizational culture instrument based on the competing values framework: Exploratory and confirmatory factor analyses', Implementation Science 25(2), 13. https://doi.org/10.1186/1748-5908-2-13 [ Links ]

Hillman, A.J. & Keim, G.D., 2001, 'Shareholder value, stakeholder management, and social issues: What's the bottom line?,' Strategic Management Journal 22(2), 125-139. https://doi.org/10.1002/1097-0266(200101)22:2%3C125::AID-SMJ150%3E3.0.CO;2-H [ Links ]

Hu, L. & Bentler, P.M., 1998, 'Fit indices in covariance structure modeling: Sensitivity to underparameterized model misspecification', Psychological Methods 3(4), 424-453. https://doi.org/10.1037/1082-989X.3.4.424 [ Links ]

Hu, L. & Bentler, P.M., 1999, 'Cutoff criteria for fit indexes in covariance structure analysis: Conventional criteria versus new alternatives', Structural Equation Modeling 6(1), 1-55. https://doi.org/10.1080/10705519909540118 [ Links ]

Ikeanyibe, O.M., Obiorji, J., Osadebe, N.O. & Ugwu, C., 2020, 'Politics, peer review and performance management in Africa: A path to credible commitment for Nigerian politicians?,' Public Administration Issues 5, (SI), 35-58. https://doi.org/10.17323/1999-5431-2020-0-5-35-58 [ Links ]

Kalliath, T.J., Bluedorn, A.C. & Gillespie, D.F., 1999, 'A confirmatory factor analysis of the competing values instrument', Educational and Psychological Measurement 59(1), 143-158. https://doi.org/10.1177/0013164499591010 [ Links ]

Kloot, L. & Martin, J., 2000, 'Strategic performance management: A balanced approach to performance management issues in local government', Management Accounting Research 11, 231-251. https://doi.org/10.1006/mare.2000.0130 [ Links ]

Kikeri, S., 2018, Corporate governance in South African state-owned enterprises, World Bank, Washington, DC, viewed 12 July 2021, from https://openknowledge.worldbank.org/handle/10986/30029. [ Links ]

Klovienė, R. & Gimžauskien, E., 2014, 'Performance measurement model formation in state-owned enterprises', Procedia - Social and Behavioral Sciences 156, 594-598. https://doi.org/10.1016/j.sbspro.2014.11.247 [ Links ]

Komarek, R., Knight, D. & Bielefeldt, A.R., 2017, 'Exploring the use of the competing values framework in engineering education', paper presented at 2017 ASEE Annual Conference & Exposition, ASEE, Columbus, Ohio, June 2017. [ Links ]

Lee, D., 2004, 'Competing models of effectiveness in research centers and institutes in the Florida State university system: A data envelopment analysis', PhD dissertation, Askew School of Public Administration and Policy, College of Social Sciences, Florida State University. [ Links ]

Lindquist, E.A. & Marcy, R.T., 2014, 'The competing values framework: Strategic implications for leadership, conflict and change in public organizations', in 3rd Research Conference of the Canadian Association of Programs in Public Administration, Queen's University, Kingston, Ontario, 19 May 2014, 17 pages. [ Links ]

Little, T.D., Rhemtulla, M., Gibson, K. & Schoemann, A.M., 2013, 'Why the item versus parcels controversy needn't be one', Psychological Methods 18(3), 285-300. https://doi.org/10.1016/j.sbspro.2014.11.247 [ Links ]

Lorenzo-Seva, U. & Ferrando, P.J., 2006, 'FACTOR: A computer program to fit exploratory factor analysis models', Behavior Research Methods 38, 88-91. https://doi.org/10.3758/BF03192753 [ Links ]

Luong, T.H.T, Jorissen, A. & Paeleman, I., 2019, 'Performance measurement for sustainability: Does firm ownership matter', Sustainability 11, 4436. https://doi.org/10.3390/su11164436 [ Links ]

Masekoameng, R. & Mpehle, Z., 2018, 'Financial sustainability of South African state-owned enterprises: A case of Limpopo Economic Development Agency', London Journal of Research in Humanities and Social Sciences 18(3), 21-32. [ Links ]

Mafini, C. & Pooe, D.R., 2013, 'The relationship between employee satisfaction and organisational performance: Evidence from a South African government department', SA Journal of Industrial Psychology 39(1), a1090. https://doi.org/10.4102/sajip.v39i1.1090 [ Links ]

Martínez-González, A. & Martí, J., 2006, 'Accountability and rendering of accounts: New approaches for the public sector', International Advances in Economic Research 12(1), 67-80. https://doi.org/10.1007/s11294-006-6135-x [ Links ]

Martz, W.A., 2008, 'Evaluating organizational effectiveness', PhD dissertation, Depart. of Interdisciplinary PhDs in Evaluation, Western Michigan University, viewed 20 July 2021, from https://scholarworks.wmich.edu/dissertations/793. [ Links ]

Mbo, M., 2017, Drivers of organisational performance: A state-owned enterprise perspective, Stellenbosch University, Stellenbosch. [ Links ]

Mihaiu, D., 2014, 'Measuring performance in the public sector: Between necessity and difficulty', Studies in Business and Economics 9(2), 40-50. [ Links ]

Minvielle, E., Sicotte, C., Champagne, F., Contandriopoulos, A-P., Jeantet, M., Préaubert, N. et al., 2008, 'Hospital performance: Competing or shared values?,' Health Policy 87(1), 8-19. https://doi.org/10.1016/j.healthpol.2007.09.017 [ Links ]

Morais, L.F. & Graça, L.M., 2013, 'A glance at the competing values framework of Quinn and the Miles & Snow strategic models: Case studies in health organizations', Revista Portuguesa de Saúde Pública 31(2), 129-144. https://doi.org/10.1016/j.rpsp.2012.12.006 [ Links ]

Moulin, M., 2017, 'Improving and evaluating performance with the public sector scorecard', International Journal of Productivity and Performance Management 66(4), 442-458. https://doi.org/10.1108/IJPPM-06-2015-0092 [ Links ]

Moynihan, D.P. & Pandey, S.K., 2004, 'Testing how management matters in an era of government by performance management', Journal of Public Administration Research and Theory 15(3), 421-439. https://doi.org/10.1093/jopart/mui016 [ Links ]

Muterera, J., Hemsworth, D., Baregheh, A. & Garcia-Rivera, B.R., 2012, 'The leader-follower dyad: Exploring the link between public sector leadership, employee satisfaction and performance', Journal of Knowledge & Human Resource Management 4(9), 53-70. [ Links ]

Muthén, L.K. & Muthén, B.O., 2017, Mplus user's guide, 6th edn, Muthén & Muthén, Los Angeles, CA. [ Links ]

Ncume, L.S., 2018, 'Organizational culture and effectiveness in Parliaments: A case study in the Gauteng Provincial Legislature', MPhil thesis, Faculty of Arts and Social Sciences, Stellenbosch University. [ Links ]

Organisation for Economic Co-operation and Development, 2005, Guidelines on Corporate Governance of State-owned enterprises, viewed 02 August 2021, from https://www.oecd.org/daf/ca/oecd-guidelines-corporate-governance-soes-2005.htm. [ Links ]

Oghojafor, B.E.A., Muo, F.I. & Aduloju, S.A., 2012, 'Organisational effectiveness: Whom and what do we believe?,' Advances in Management & Applied Economics 2(4), 81-108. [ Links ]

Olivier, B.H., 2014, 'The development and validation of an assessment framework for measuring the organisational effectiveness of a metropolitan municipality in South Africa', DAdmin, Depart. of Industrial and Organisational Psychology, University of South Africa. [ Links ]

Pounder, J.S., 2000, 'A behaviourally anchored rating scales approach to institutional self-assessment in higher education', Assessment & Evaluation in Higher Education 25(2), 171-182. https://doi.org/10.1080/713611422 [ Links ]

Pratuckchai, W. & Patanapongse, W., 2012, 'The study of management control systems in state owned enterprises: A proposed conceptual framework', International Journal of Organizational Innovation 5(2), 83-115. [ Links ]

Quinn, R.E., 1981, 'A Competing Values Approach to organizational effectiveness', Public Productivity Review 5(2), 122. https://doi.org/10.2307/3380029 [ Links ]

Quinn, R.E. & Rohrbaugh, J., 1983, 'A spatial model of effectiveness criteria: Towards a Competing Values Approach to organizational analysis', Management Science 29(3), 363-377. https://doi.org/10.1287/mnsc.29.3.363 [ Links ]

Quinn, R. & Spreitzer, G., 1991, 'The psychometric of the Competing Values culture instrument and an analysis of the impact of organizational culture on quality of life', in R.W. Woodman & W.A. Pasmore (eds.), Research in organizational change and development, JAI Press, Greenwich, pp. 115-142. [ Links ]

R Core Team, 2021, 'R: A language and environment for statistical computing', R Project, R Foundation for Statistical Computing, viewed 12 December 2021, from https://www.R-project.org. [ Links ]

Revelle, W., 2021, 'Procedures for psychological, psychometric, and personality research', Personality Project, viewed 14 December 2021, from https://personality-project.org/r/psych. [ Links ]

Richard, P.J., Devinney, T.M., Yip, G.S. & Johnston, G., 2009, 'Measuring organizational performance as a dependent variable: Towards methodological best practice', Journal of Management 35(3), 718-804. https://doi.org/10.1177/0149206308330560 [ Links ]

Rodriguez, A., Reise, S.P. & Haviland, M.G., 2016, 'Applying bifactor statistical indices in the evaluation of psychological measures', Journal of Personality Assessment 98(3), 223-237. https://doi.org/10.1080/00223891.2015.1089249 [ Links ]

Škerlavaj, M., Štemberger, M.I., Škrinjar, R. & Dimovski, V., 2007, 'Organizational learning culture: The missing link between business process change and organizational performance', International Journal of Production Economics 106(2), 346-367. https://doi.org/10.1016/j.ijpe.2006.07.009 [ Links ]

Tanlamai, U. & Juta, P., 2011, 'Performance assessment in Thai state-owned enterprises', Journal of American Academy of Business 17, 223-231. [ Links ]

Timmerman, M.E. & Lorenzo-Seva, U. 2011, 'Dimensionality assessment of ordered polytomous items with parallel analysis', Psychological Methods 16(2), 209-220. https://doi.org/10.1037/a0023353 [ Links ]

Tregunno, D., Ross Baker, G., Barnsley, J. & Murray, M., 2004, 'Competing values of emergency department performance: Balancing multiple stakeholder perspectives', Health Services Research 39(4pt1), 771-792. https://doi.org/10.1111/j.1475-6773.2004.00257.x [ Links ]

Van der Wal, Z., De Graaf, G. & Lawton, A., 2011, 'Competing values in public management: Introduction to the symposium issue', Public Management Review 13(3), 331-341. https://doi.org/10.1080/14719037.2011.554098 [ Links ]

Venkatraman, N. & Ramanujam, V., 1986, 'Measurement of business performance in strategy research: A comparison of approaches', Academy of Management Review 11(4), 801-814. https://doi.org/10.2307/258398 [ Links ]

Vilkinas, T. & Cartan, G., 2006, 'The integrated competing values framework: Its spatial configuration', Journal of Management Development 25(6), 505-521. https://doi.org/10.1108/02621710610670092 [ Links ]

Whetten, D.A. & Cameron, K.S., 1994, 'Organizational effectiveness: Old models and new constructs', in J. Greenberg (ed.), Organizational behavior: The state of the science, Routledge, New York, NY, pp. 135-154. [ Links ]

Zlatković, M., 2018, 'Organizational effectiveness in Bosnia and Herzegovina: A competing values approach', Strategic Management 23(4), 15-25. https://doi.org/10.5937/StraMan1804015Z [ Links ]

Correspondence:

Correspondence:

Petrus Nel

petrusn@uj.ac.za

Received: 19 Apr. 2022

Accepted: 13 Mar. 2023

Published: 03 Aug. 2023