Services on Demand

Article

English (pdf)

English (pdf)

Article in xml format

Article in xml format Article references

Article references

Indicators

Related links

-

Cited by Google

Cited by Google -

Similars in Google

Similars in Google

Share

Permalink

PermalinkSouth African Journal of Information Management

On-line version ISSN 1560-683X

Print version ISSN 2078-1865

SAJIM (Online) vol.25 n.1 Cape Town 2023

http://dx.doi.org/10.4102/sajim.v25i1.1624

ORIGINAL RESEARCH

Adopting the technology acceptance model: A Namibian perspective

Mia Bothma; Leandrie Mostert

WorkWell Research Unit, Faculty of Economic and Management Sciences, North-West University, Potchefstroom, South Africa

ABSTRACT

BACKGROUND: The adoption of online banking is still a concern in developing countries, with limited research in investigating the factors that can lead to the intention to use and the actual usage of online banking.

OBJECTIVES: This research aims to broaden the knowledge about technology adoption by applying the technology acceptance model (TAM) to the online banking environment in Namibia.

METHODS: A descriptive, quantitative research design and structural equation modelling (SEM) were employed to analyse the data.

RESULTS: The adopted TAM had good model fit if applied to online banking in Namibia. Nine of the 12 hypotheses were accepted.

CONCLUSION: System quality and social influence act as external factors that influence the level of trust, perceived ease of use and perceived usefulness. High levels of ease of use and usefulness of the online banking system result in a positive attitude towards the online banking system that in turn leads to the intention to use the system and then actual usage.

CONTRIBUTION: This study adopted the TAM and included social influence, system quality and perceived trust as factors that can influence the usage of online banking. The study contributed towards the knowledge of technology acceptance from an online banking perspective and can aid the banking sector in increasing the adoption of online banking systems.

Keywords: online banking; technology acceptance model; the Namibian banking industry; perceived ease of use; perceived usefulness; attitude; behavioural intention; actual usage.

Introduction

Online banking services have been revolutionised because of the advancement in information and communication technologies within developing and developed countries (Patel & Patel 2018). Providing a more effective and simplistic way to conduct financial services, online banking overcomes the disadvantages of traditional banking and refers to the use of the Internet to perform banking tasks that increases access to financial systems and reduces poverty while providing opportunities to become part of the financial system (Fanta & Makina 2019; Safari, Bisimwa & Armel 2020). During the last 2-years, online banking users in the world have steadily risen from 1903 million users in 2020 to 2043 million users in 2021, and projections are that online banking users will reach 2551 million by 2024 (Norrestad 2022). Although various research within the online banking environment has been published, most research is conducted within developed countries or continents such as China, USA, Taiwan and Malaysia and limited studies that investigate developed countries/continents such as Africa and Namibia (Al-Emran & Granić 2020; Singh & Srivastava 2020). Namibia is viewed as a developing country and although all the major banks offer online banking, many Namibians are still hesitant to make use of online banking services and because of limited research conducted in developing countries, Namibian banks are in the dark in their quest to understand the drivers of online banking adoption of their client base (Amukeshe 2021).

When investigating the adoption and usage of information systems, intention-based models provide valuable information about an individual's behavioural intentions to predict their adoption rates and use of technology (Lee, Yiu & Cheung 2021). Various technology acceptance theories and models exist such as the theory of planned behaviour (Ajzen 1991), theory of reasoned action (Fishbein & Azjen 1975), technology acceptance model (TAM) (Davis, Bagozzi & Warshaw 1989), TAM2 (Venkatesh & Davis 2000), unified theory of acceptance and use of technology (UTAUT) (Venkatesh et al. 2003), TAM3 (Venkatesh & Bala 2008) and UTAUT2 (Venkatesh, Thong & Xu 2012). However, there are different schools of thought about which model is the best to use, specifically within the online banking environment. In a study to determine whether the TAM is still valid and current, Al-Emran and Granić (2020) established that the application and extensions of the TAM are still valid across various applications and disciplines and that the TAM has been mostly employed in the banking domain. In addition to the popularity of using the TAM, the TAM predicts user's technology adoption behaviours by investigating the beliefs and attitudes of the users towards the technology and can be used to evaluate the desire of a customer to use any technology systems (Singh & Srivastava 2020; Zhang, Lu & Kizildag 2018). The TAM is furthermore robust and parsimonious for predicting consumer behaviour across a wide range variety of information technology systems and has been numerously validated by 'psychometric measurement scales' such as a Likert scale that is used to measure consumer attitudes and intentions in accepting (or rejecting) information technology systems (Venkatesh & Davis 2000; Venkatesh et al. 2003). For these reasons, the TAM was used to investigate the technology acceptance of Namibian online banking customers.

This research, therefore, aims to broaden the knowledge about technology adoption in developing countries by applying an extended TAM to the online banking environment in Namibia. In addition, the study aims to provide Namibian banks and banks of emerging economies with a better understanding of the drivers that will lead to online banking adoption within a developing county.

Literature review and conceptual model

An overview of the technology acceptance model

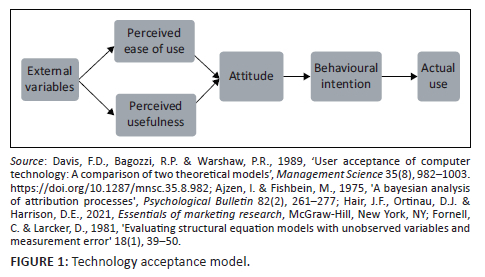

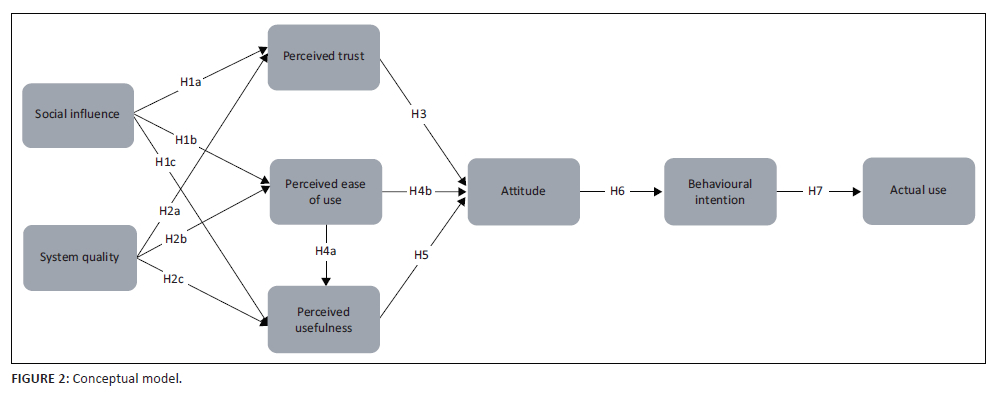

The TAM is based on the theory of reasoned action (Fishbein & Azjen 1975) and aims to better understand user acceptance or rejection of information technology systems by describing the motivational processes that mediate the system characteristics and user behaviour (Davis 1985). As presented in Figure 1, the TAM argues that a user's perception of the usefulness and ease of use of the system will influence their attitude towards the system, which will influence the user's behavioural intention to use the system and will result in the actual usage of the system (Davis et al. 1989). The external variables included refer to system characteristics, the nature of the implementation process, user participation design and user training (Venkatesh & Davis 1996). In addition to the variables included in the TAM of Davis et al. (1989), this research also investigated perceived trust as a higher level of trust increases a customer's certainty perceptions about a specific behaviour when using online services (Nguyen & Nguyen 2016). The online banking environment also includes sensitive information and trust might be a concern for consumers who might influence their behaviour towards online banking (Sharma & Sharma 2019). The TAM is presented in Figure 1.

Using the TAM to better understand technology acceptance within the online banking environment is contemporary with various research that has adapted and extended the TAM in different parts of the world. Hossain et al. (2020), for example, extended the TAM by including governmental support and risk among online banking customers in Bangladesh were as Albort-Morant, Pedregosa and Paredes (2022) compared the factors that influence the adoption of online banking among Spanish online banking customers in towns and cities. Also, among Indian online banking customers, the various constructs of the TAM and also factors such as perceived security, self-efficacy, social influence and customer support proved to have a significant impact on customers' behavioural intention to use mobile banking (Singh & Srivastava 2020).

External variables

External variables are important to consider while investigating the adaption of a technology system and are the set of variables that are used to address the characteristics of a system and influence the perceived usefulness and ease of use of the system (Davis et al. 1989; Wahab & Azzman 2019). This study included two external variables, namely social influence and system quality. Relevant to the online banking environment, social influence is the process where individuals affect others' behaviour, feelings and beliefs and is a key determinant in individual behaviour intentions (Wang, Molina & Sundar 2020). Social influence is based on the social influence theory (Kelman 1958) and refers to compliance, identification and internalisation that change attitudes. Compliance refers to individuals accepting influences from others to achieve a favourable reaction, identification occurs when individuals accept influence because they want to maintain a relationship with others that defines them, and internationalisation refers to individuals accepting influences because it is rewarding and integrated into their belief system (Kelman 1958; Xu et al. 2017). All three elements of social influence are relevant to the online banking environment because the social context of an individual can act as a catalyst to adopt new technology and was therefore included in the conceptual model (Mohammadi 2015).

Malaquias and Hwang (2016) observe that if a consumer's social network perceives the risks of online banking to be low, their trust in these services will increase, which, in turn, will affect the consumer's likelihood of adopting the online banking services. In addition, Gong et al. (2019) established a positive correlation between the social influences and trust in the provider within an online health consultation services industry.

Consequently, it is plausible to argue that among Namibian online banking customers:

H1a: Social influence has a positive and significant effect on perceived trust

Perceived ease of use is the perceptions that an individual forms regarding the use of technology, how the use of the system could lead to a reduction in their mental stress levels as well as how efficiently their time will be spent in using the service (Raza, Umer & Shah 2017). Individuals will be more inclined to use online banking when they perceive the provided services are effortless, efficient and easy to use (Cho & Sagynov 2015; Davis et al. 1989). In addition, an individual's opinions formulated by important referents do impact their perceptions of the system or services at hand. Therefore, if family members, friends or important others perceive online banking to be easy to use, it is most likely that individuals will also adopt these services; therefore, social influences significantly affect perceived ease of use on internet of things and mobile commerce (Bashir & Madhavaiah 2015; Chaouali, Yahia & Souiden 2016; Tsourela & Nerantzaki 2020).

Consequently, it is plausible to argue that among Namibian online banking customers:

H1b: Social influence has a positive and significant effect on perceived ease of use

Perceived usefulness is an important concept in user acceptance or rejection of systems and relates to the degree that an individual feels his or her job performance is enhanced by engaging in the usage of the system at hand (Davis 1985). Perceived usefulness is an important contributing factor in Internet banking adoption because of the flexibility of internet banking services and that these services are becoming more superior to traditional banking services resulting in an increase in Internet banking adoption (Rawwash et al. 2020). If an individual believes that his or her social context (family, peers, colleagues) assumes that they should make use of a system, the beliefs of the social circle are incorporated into their own beliefs and as such they perceive the specific system to be useful (Abdullah, Ward & Ahmed 2016).

Consequently, it is plausible to argue that among Namibian online banking customers:

H1c: Social influence has a positive and significant effect on perceived usefulness

System quality

System quality relates to the system's overall performance following the needs and expectations of the consumer (Um 2021). Improving a retail bank's online system quality increases customers' trust perception (Namahoot & Laohavichien 2018). In addition, Ryu and Ko (2020) established that customers' trust levels increase if the system provides them with credible and reliable information, whereas customers start to doubt the competence of a bank when they receive poor system quality. Also, good system quality within an online shopping environment results in higher trust in the online store (Qalati et al. 2021).

Consequently, it is plausible to argue that among Namibian online banking customers:

H2a: System quality has a positive and significant effect on perceived trust

System quality has a positive and significant influence on perceived ease of use and perceived usefulness (Fearnley & Amora 2020; Koukopoulos et al. 2020). System quality characteristics such as reliability, availability, usability and adaptability influence the perceptions of customers relating to usefulness and the ease of use of a system as customers are more likely to find systems to be useful and easy to use when the system quality provided is acceptable (Mahande, Jasruddin & Nasir 2019). Therefore, if consumers receive the desired level of system quality, they are more likely to view the system as useful and easy to use (Fearnley & Amora 2020).

Consequently, it is plausible to argue that among Namibian online banking customers:

H2b: System quality has a positive and significant effect on perceived ease of use

H2c: System quality has a positive and significant effect on perceived usefulness

Perceived trust

Trust forms an integral part of developing and maintaining successful relationships in the online banking environment. It is based on customer expectations, refers to the degree to which the system performs as expected and reinforces the intention to use the system (Bashir & Madhavaiah 2015; Chatzoglou et al. 2020). Consumers who perceive the bank and the online services provided as trustworthy will be more likely to engage in transactions because of the positive attitude formed towards the service that contributes to the adoption of e-commerce (Indarsin & Ali 2017; Marakarkandy, Yajnik & Dasgupta 2017). More recently, within the social media environment, Naqvi et al. (2020) determined that when customers use social media and trust the platform, they also have a positive attitude towards adopting social media services.

Consequently, it is plausible to argue that among Namibian online banking customers:

H3: Perceived trust has a positive and significant effect on customer attitude

Perceived ease of use and perceived usefulness

Perceived ease of use relates to the assessments made by individuals on the difficulty or ease of using a system with the focus on the process that leads to the outcome of using the specific system (Cho & Sagynov 2015; Lazard & King 2020). At the beginning of the century, Venkatesh and Davis (2000) established that perceived ease of use directly affects the perceived usefulness of technology because individuals who perceive the system to be effortless will most likely use the system more often. Subsequent to this research, various researchers such as Cho and Sagynov (2015) and more recently, Jatimoyo, Rohman and Djazuli (2021), established that the easier it is to use the system, the more useful users perceive the system to be.

Consequently, it is plausible to argue that among Namibian online banking customers:

H4a: Perceived ease of use has a positive effect on perceived usefulness

Consumer attitude refers to the negative or positive feelings towards performing a specific behaviour (Elkheshin & Saleeb 2020). Consumer attitude towards online banking services depends on the perceptions formed while using the services; however, consumer perceptions are subject to change (Verma & Kumar 2020). If individuals believe that online banking services have attributes that could improve their job performance and increase their productivity, they will develop favourable attitudes towards using such services (Matikiti, Mpinganjira & Roberts-Lombard 2018). In addition to the usefulness of the system, when online banking customers perceive the system to be easy to use, they will also form positive attitudes towards the system (Normalini 2019; Rasull et al. 2020).

Consequently, it is plausible to argue that among Namibian online banking customers:

H4b: Perceived ease of use has a positive effect on customer attitude

H5: Perceived usefulness has a positive effect on customer attitude

Attitude

The TAM consists of a core relationship that determines the acceptance of a technology, and that core relationship is between an individual's attitude and intention towards using a technology (Davis et al. 1989). Specifically, within an online banking environment, the key predictors that influence an individual's acceptance or rejection of online banking services are the attitudes and intentions towards such services and are important to consider when evaluating the adoption of an online system (Ahmad, Bhatti & Hwang 2020; Mohammadi 2015; Rahi, Ghani & Alnaser 2017).

Consequently, it is plausible to argue that among Namibian online banking customers:

H6: Customer attitude has a positive and significant effect on behavioural intention

Behavioural intention

Actual use is defined as the degree or way that individuals capitalise on the capabilities of an information system or the time spent using and interacting with the system (Amin et al. 2019) compared with behavioural intention that is the subjective probability that an individual will engage in a specific behaviour (Ajzen & Fishbein 1975).

In an online environment, behavioural intention directly influences the use of technology and information systems (Mashroofa, Jusoh & Chinna 2019). Therefore, when an online banking customer intends to use the online banking system, they will use it (Ahmad et al. 2020; Marakarkandy et al. 2017).

Consequently, it is plausible to argue that among Namibian online banking customers:

H7: Behavioural intention has a positive and significant effect on actual usage

Based on the hypotheses formulated, the conceptual model of this study is presented in Figure 2.

Methodology

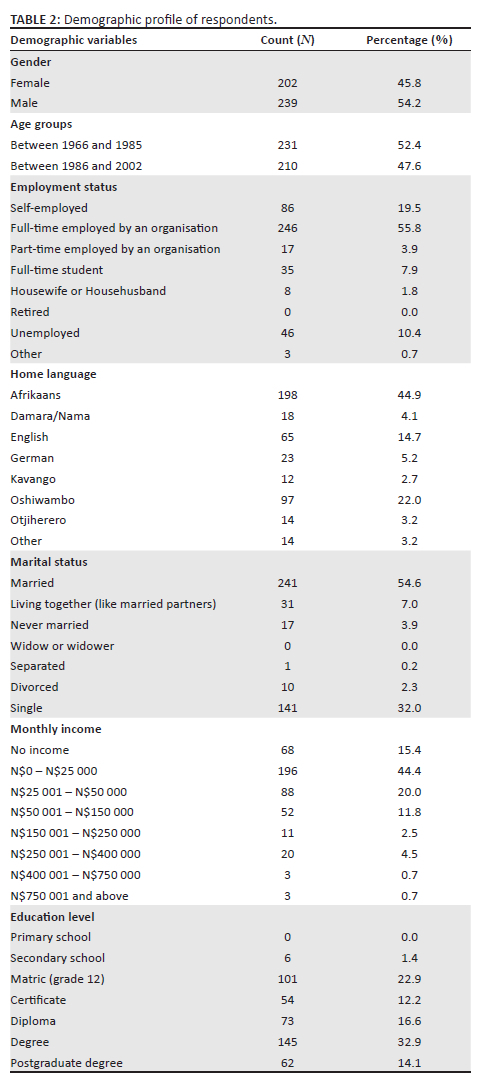

A descriptive research design was followed that included quantitative, primary data collection. Self-administrated questionnaires were used to collect data through a link to the questionnaire posted on Facebook, which individuals could follow to complete the questionnaire. The population of this study included males and females born between 1966 and 2002 who reside in Namibia and are making use of online banking. A sample frame could not be obtained because of the confidentiality agreements between banks and their clients, and therefore non-probability sampling, which included quota and convenience sampling, was used. The demographic profile of the respondents included in this study were well represented amongst different demographic variables, as indicated in Table 2. The realised sample size of this study was 441, which is based on the recommendations of Hair et al. (2019) and followed the observations per variable ratio of at least 20:1. The study had a total of eight constructs. No respondents' personal information was collected, thus ensuring their anonymity and confidentiality. Structural equation modelling (SEM) was used to test the study's hypothesis using MPlus (Version 8.7).

Measurement instrument

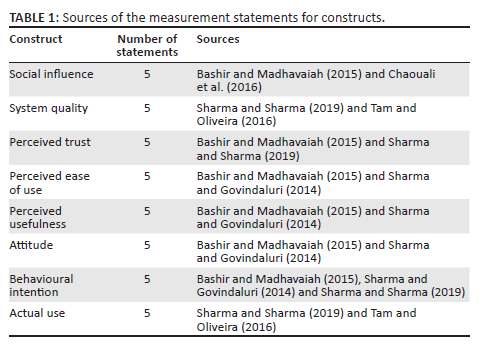

The questionnaire included five sections: the preface, screening questions, construct measurement, demographic information and postscript. The preface explained the aim of the study and indicated how the data would be used. The screening questions were used to confirm that the respondents were older than 18 years, used online banking and resided in Namibia. The constructs were measured using existing and reliable measurement statements. Respondents had to indicate their level of agreement with each of the statements using a six-point labelled Likert scale, where '1' indicated strongly disagree and '6' indicated strongly agree. Table 1 indicates the measurement statements' sources for each of the constructs.

Ethical considerations

This study was approved as a minimal risk study by the Economic and Management Sciences Research Ethics Committee (EMS-REC) of the North-West University on 15 February 2022 (No. NWU-00888-20-A4).

Results

Demographic profile

A total of 441 usable questionnaires were obtained. The demographic profile of the Namibian banking customers who participated in this study is presented in Table 2.

It is evident from Table 2 that a good spread among the different demographic variables participated in this research.

Reliability and validity of the measurement instrument

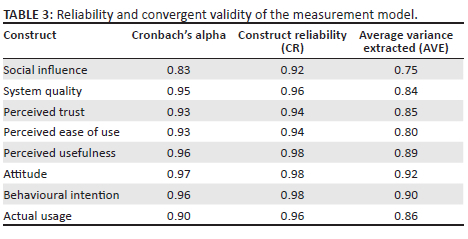

The reliability and validity of the measurement instrument were determined by calculating the Cronbach's alpha values and performing a confirmatory factor analysis (CFA). The Cronbach's alpha values of all the measurement constructs were greater than 0.70, indicating satisfactory internal consistency (Hair et al. 2021:178). As indicated in Table 3, the Cronbach's alpha values ranged between 0.83 and 0.97.

Convergent and discriminant validity were tested through a CFA. Convergent validity was tested by calculating the standard factor loadings, average variance extracted (AVE) and the construct reliability (CR) values of the measurement model (Hair et al. 2019:676). The factor loadings of Social influence 3 (SOCIF 3), Perceived ease of use 3 (PEOU 3) and Actual usage 2 (USAGE 2) were lower than 0.50; therefore, these items were omitted from the data analysis. As indicated in Table 3, the AVE values of the measurement model's constructs were above the recommended cut-off value of 0.50, thus indicating acceptable convergence of the measured statements. It is furthermore evident from Table 3 that internal consistency is present for all the measured constructs, and the CR values of the measurement model's constructs were above the recommended cut-off value of 0.70. Based on the examination of the standardised factor loadings, the calculation of the AVE and CR values of the measurement model, it can be concluded that all eight constructs of the measurement model have convergent validity.

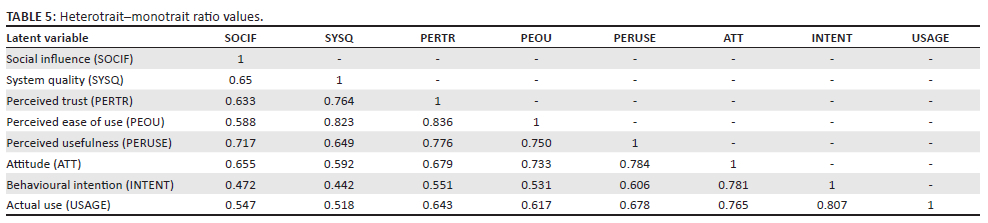

The Fornell and Larcker criterion (1981) and the heterotrait-monotrait (HTMT) ratios were accessed to test for discriminant validity. For the Fornell and Larcher criterion, AVE of any two constructs was compared with the squared correlation (R2) estimate between the two constructs and should the AVE of two constructs is greater than the squared correlation between them, discriminant validity is confirmed (Hair, Page & Brunsveld 2020). The results obtained from the correlation matrix (AVE and squared correlation values) are presented in Table 4. The HTMT ratio values are presented in Table 5. Heterotrait-monotrait ratio values higher than the threshold indicates a lack of discriminant validity. This study used a threshold of 0.85 (Kline 2015).

It is evident from Table 4 and Table 5 that the discriminant validity was achieved.

Model fit statistics

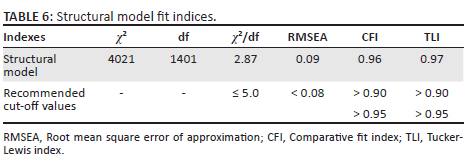

The measurement model was tested by using a two-step SEM process. The model fit was tested through a CFA, and once and acceptable model was obtained, the structural model was tested. Structural equation modelling was used to examine the interrelationships and hypotheses between the constructs of the measurement model (Hair et al. 2019:703). Google forms were used to collect the data, and therefore there were no missing values to manage. Table 6 provides the model fit statistics of the structural model. The model fit indices revealed that the model has an acceptable fit.

Hypotheses testing

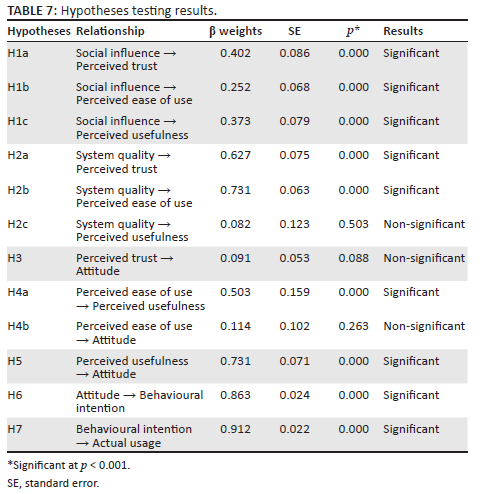

Using SEM, the theoretical relationships were transformed into hypotheses and empirically tested. The standardised regression weights (standardised path coefficients) and structural parameter estimates of the structural paths in the model were investigated, and the results of the hypotheses testing are presented in Table 7.

Based on the results presented in Table 7, the structural model for this study is shown in Figure 3.

Discussion and conclusion

The study adopted the TAM of Davis et al. (1989) and also added social influence, system quality and perceived trust to the model. Consistent with the findings of Bashir and Madhavaiah (2015), Chaouali et al. (2016), Rawwash et al. (2020) and Saprikis, Avlogiaris and Katarachia (2021), this research confirmed that social influence has a positive and significant effect on ease of use, perceived usefulness and perceived trust of Namibian online banking customers. When Namibian online banking customers experience social influence from their social group, they perceive online banking to be easy to use, they believe online banking will improve the functionality of the banking activities and be more convenient. In addition, the social influence experienced by Namibian online banking customers will result in these customers perceiving online banking services as safe, reliable and trustworthy.

The research determined that system quality has a positive and significant effect on perceived trust and ease of use, corresponding with research by Namahoot and Laohavichien (2018). When Namibian online banking customers perceive online banking systems as flexible to interact with, easy to navigate and well-structured, these individuals will perceive such systems' to be trustworthy, safe, reliable, easy to use and do not require any additional effort to learn to use the system. However, among Namibian online banking customers, system quality has a positive but insignificant effect on perceived usefulness that does not agree with the results obtained by Fearnley and Amora (2020). Therefore, Namibian online banking customers might feel that having good system quality will not necessarily mean that they experience the system as useful.

The implication of including perceived trust in this study holds evidence in the findings by Ibrahim and Chandra (2015) that trust is developed based on service expectations (Marakarkandy et al. 2017). Although Vejacka and Štofa (2017) and Liébana-Cabanillas et al. (2018) confirmed a positive and significant relationship between perceived trust and attitude, this study established a positive relationship; however, the relationship is not significant. The non-significant relationship might be because the respondents are already accustomed to the use of online technology systems and automatically trust these systems; therefore, their attitude towards online banking systems is not affected. Perceived trust was a novel addition to the model of Davis et al. (1989), and social influence had the strongest effect on perceived trust and system quality had the strongest effect on perceived ease of use. To create trust, retail banks should focus on motivating the social groups of their customers to use the system.

Davis (1985) believed that user attitude is influenced by two beliefs, namely perceived ease of use and perceived usefulness, and that perceived ease of use will have a direct effect on perceived usefulness. Various researchers also investigated the relationship between perceived ease of use and usefulness and found a significantly positive effect between the constructs (Cho & Sagynov 2015; Jatimoyo et al. 2021; Venkatesh & Davis 2000). This research supports these findings, which determined that perceived ease of use positively and significantly affects perceived usefulness among Namibian online banking customers. Therefore, when Namibian online banking users are of the opinion that online banking services are easy to use, such services are also deemed useful.

It is postulated that perceived ease of use and usefulness positively and significantly affect consumer attitudes within the online environment (Cho & Sagynov 2015; Matikiti et al. 2018; Normalini 2019; Rasull et al. 2020). In agreement with these researchers, this research determined that among Namibian online banking customers perceived usefulness has a positive and significant effect on consumer attitude towards online banking services. If Namibian online banking customers experience improved banking functionality and convenience when conducting banking activities, they also think that it was a good and wise decision to make use of online banking and will have favourable attitudes towards online banking services.

Although various researchers have established a positive and significant relationship between perceived ease of use and attitude (Linh 2021; Normalini 2019), this research established that the relationship among Namibian online banking customers is positive but not significant. These findings could be attributed to the respondents who grew up in an era where technology is already advanced and were familiar with it and therefore it does not influence their attitude towards online banking.

This research supports the findings by Ahmad et al. (2020), Bashir and Madhavaiah (2015) and Rahi et al. (2017) that a significantly positive relationship exists between customer attitude and behavioural intention. Namibian online banking consumers are more likely to have the intention to use online banking services when they have a positive and favourable attitude towards the online services provided. In addition, researchers Ahmad et al. (2020) and Marakarkandy et al. (2017) established a positive and significant relationship between individuals' behavioural intention towards online banking services and the actual use of the system. In agreement with these findings, this research determined a positive and significant relationship between Namibians' intentions to use online banking services and actual use. Therefore, when Namibian online banking customers have a high intention to use online banking, they will make use of the online banking services.

The TAM applies to the online banking environment and can be used by retail banks in developing countries to increase customer acceptance of online banking services. Retail banks should direct their marketing communication to motivate their customers' social groups to use online banking and must promote their good quality online banking system to increase trust, ease of use and usefulness among their customers. Marketing strategies should focus on the reliability and security of the systems and should communicate to customers that online banking will increase their functionality and be convenient to use.

Limitations and suggestions for future studies

Owing to confidential agreements between clients and banks, the study did not have a sample frame, and thus probability sampling was not possible. The researchers did not focus on the various dimensions of perceived value; however, the most applicable dimension, that is, the utilitarian value dimension was further investigated in this study. Future studies may also include other value dimensions to extend the current knowledge about this topic. The model employed in this study only focused on specific external variables, which could influence customers' perceptions regarding online banking services. Future research may consider including other external variables that could impact customers' perceptions and are relevant to online banking services.

Acknowledgements

Competing interests

The authors have declared that no competing interest exists.

Authors' contributions

The authors accept responsibility for the entire content of this manuscript and approved the submission.

Funding information

This research received no specific grant from any funding agency in the public, commercial or not-for-profit sectors.

Data availability

The authors confirm that the data that support the findings of this research are available, if requested.

Disclaimer

The views and opinions expressed in this article are those of the authors and do not necessarily reflect the official policy or position of any affiliated agency of the authors.

References

Abdullah, F., Ward, R. & Ahmed, E., 2016, 'Investigating the influence of the most commonly used external variables of TAM on students' perceived ease of use (PEOU) and perceived usefulness (PU) of e-portfolios', Computers in Human Behavior 63(1), 75-90. https://doi.org/10.1016/j.chb.2016.05.014 [ Links ]

Ahmad, S., Bhatti, S.H. & Hwang, Y., 2020, 'E-service quality and actual use of e-banking: Explanation through the technology acceptance model', Information Development 36(4), 503-519. https://doi.org/10.1177/0266666919871611 [ Links ]

Ajzen, I. & Fishbein, M., 1975, 'A bayesian analysis of attribution processes', Psycho logical Bulletin 82(2), 261-277. [ Links ]

Ajzen, I., 1991, 'The theory of planned behavior', Organizational Behavior and Human Decision Processes 50(2), 179-211. https://doi.org/10.1016/0749-5978(91)90020-T [ Links ]

Albort-Morant, G., Pedregosa, C.S. & Paredes, K.R.P., 2022, 'Online banking adoption in Spanish cities and towns. Finding differences through TAM application', Economic Research 35(1), 854-872. https://doi.org/10.1080/1331677X.2021.1945477 [ Links ]

Al-Emran, M. & Granić, A., 2021, 'Is It Still Valid or Outdated? A Bibliometric Analysis of the Technology Acceptance Model and Its Applications From 2010 to 2020', in Al-Emran, M., Shaalan, K. (eds) Recent Advances in Technology Acceptance Models and Theories. Studies in Systems, Decision and Control, Springer, Cham. https://doi.org/10.1007/978-3-030-64987-6_1

Amin, A., Almari, H., Isaac, O. & Mohammed, F., 2019, 'Investigating the key factors influencing the use of online social networks in public sector context in the UAE', International Journal of Innovation 7(3), 392-411. https://doi.org/10.5585/iji.v7i3.347 [ Links ]

Amukeshe, L., 2021, 'BoN calls on banks to bank on fintech', viewed 17 June 2021, from https://www.namibian.com.na/210524/archive-read/BoN-calls-on-banks-to-bank-on-fintech.

Bashir, I. & Madhavaiah, C., 2015, 'Consumer attitude and behavioural intention towards internet banking adoption in India', Journal of Indian Business Research 7(1), 67-102. https://doi.org/10.1108/JIBR-02-2014-0013 [ Links ]

Chaouali, W., Yahia, I.B. & Souiden, N., 2016, 'The interplay of counter-conformity motivation, social influence, and trust in customers' intention to adopt internet banking services: The case of an emerging country', Journal of Retailing and Consumer Services 28(1), 209-218. https://doi.org/10.1016/j.jretconser.2015.10.007 [ Links ]

Chatzoglou, P., Chatzoudes, D., Loakeimidou, D. & Tokoutsi, A., 2020, 'Generation Z: Factors affecting the use of social networking sites (SNSs)', in P. Mylonas (ed.), SMAP 15th international workshop on semantic and social media adaptation and personalization, IEEE, pp. 1-6, Piscataway, New Jersey.

Cho, Y.C. & Sagynov, E., 2015, 'Exploring factors that affect usefulness, ease of use, trust, and purchase intention in the online environment', International Journal of Management & Information Systems (IJMIS) 19(1), 21-36. https://doi.org/10.19030/ijmis.v19i1.9086 [ Links ]

Davis, F.D., 1985, 'A technology acceptance model for empirically testing new end-user information systems: Theory and results', doctoral dissertation, Massachusetts Institute of Technology. [ Links ]

Davis, F.D., Bagozzi, R.P. & Warshaw, P.R., 1989, 'User acceptance of computer technology: A comparison of two theoretical models', Management Science 35(8), 982-1003. https://doi.org/10.1287/mnsc.35.8.982 [ Links ]

ElKheshin, S.A. & Saleeb, N., 2020, 'Assessing the adoption of e-government using TAM model: Case of Egypt', International Journal of Managing Information Technology (IJMIT) 12(1), 1-14. https://doi.org/10.5121/ijmit.2020.12101 [ Links ]

Fanta, A.B. & Makina, D., 2019, 'The relationship between technology and financial inclusion: Cross-sectional evidence', in D. Makina (ed.), Extending financial inclusion in Africa, pp. 211-229, Academic Press.

Fearnley, M.R. & Amora, J.T., 2020, 'Learning management system adoption in higher education using the extended technology acceptance model', IAFOR Journal of Education 8(2), 89-106. https://doi.org/10.22492/ije.8.2.05 [ Links ]

Fishbein, M. & Ajzen, I., 1975, Belief, attitude, intention, and behavior: An introduction to theory and research, Addison-Wesley, Reading, MA.

Fornell, C. & Larcker, D., 1981, 'Evaluating structural equation models with unobserved variables and measurement error', Journal of Marketing Research 18(1), 39-50. [ Links ]

Gong, Z., Han, Z., Li, X., Yu, C. & Reinhardt, J.D., 2019, 'Factors influencing the adoption of online health consultation services: The role of subjective norm, trust, perceived benefit, and offline habit', Frontiers in Public Health 7(1), 1-9. https://doi.org/10.3389/fpubh.2019.00286 [ Links ]

Hair, J.F., Black, W.C., Babin, B.J. & Anderson, R.E., 2019, Multivariate data analysis, Cengage Learning, Andover, MA.

Hair, J.F., Page, M. & Brunsveld, N., 2020, Essentials of business research methods, Routledge, New York, NY.

Hair, J.F., Ortinau, D.J. & Harrison, D.E., 2021, Essentials of marketing research, McGraw-Hill, New York, NY.

Hossain, S.K., Bao, Y., Hasan, N. & Islam, M.D., 2020, 'Perception and prediction of intention to use online banking systems: An empirical study using extended TAM', Research in Business and Social Science 9(1), 112-126. https://doi.org/10.20525/ijrbs.v9i1.591 [ Links ]

Ibrahim, A. & Chandra, P., 2015, 'Exploring the influence of trust and perceived system quality on continuance intention toward e-filing system of Malaysian e-government service. A literature review', Journal of Technology and Operations Management 10(2), 65-76. [ Links ]

Indarsin, T. & Ali, H., 2017, 'Attitude toward using m-commerce: The analysis of perceived usefulness perceived ease of use, and perceived trust: Case study in Ikens Wholesale Trade, Jakarta-Indonesia', Saudi Journal of Business and Management Studies 2(11), 995-1007. [ Links ]

Jatimoyo, D., Rohman, F. & Djazuli, A., 2021, 'The effect of perceived ease of use on continuance intention through perceived usefulness and trust: A study on Klikindomaret service users in Malang City', International Journal of Research in Business and Social Science 10(4), 430-437. https://doi.org/10.20525/ijrbs.v10i4.1223 [ Links ]

Kelman, H.C., 1958, 'Compliance, identification, and internalization three processes of attitude change', Journal of Conflict Resolution 2(1), 51-60. https://doi.org/10.1177/002200275800200106 [ Links ]

Kline, R.B., 2015, Principles and practice of structural equation modeling, The Guilford Press, New York, NY.

Koukopoulos, Z., Koutromanos, G., Koukopoulos, D. & Gialamas, V., 2020, 'Factors influencing student and in-service teachers' satisfaction and intention to use a user-participatory cultural heritage platform', Journal of Computers in Education 7(3), 1-39. https://doi.org/10.1007/s40692-020-00159-4 [ Links ]

Lazard, A.J. & King, A.J., 2020, 'Objective design to subjective evaluations: Connecting visual complexity to aesthetic and usability assessments of eHealth', International Journal of Human-Computer Interaction 36(1), 95-104. https://doi.org/10.1080/10447318.2019.1606976 [ Links ]

Lee, C.K., Yiu, T.W. & Cheung, S.O., 2021, 'Predicting intention to use alternative dispute resolution (ADR): An empirical test of theory of planned behaviour (TPB) model', International Journal of Construction Management 21(1), 27-40. https://doi.org/10.1080/15623599.2018.1505026 [ Links ]

Liébana-Cabanillas, F., Muñoz-Leiva, F. & Sánchez-Fernández, J., 2018, 'A global approach to the analysis of user behavior in mobile payment systems in the new electronic environment', Service Business 12(1), 25-64. https://doi.org/10.1007/s11628-017-0336-7 [ Links ]

Linh, N.T.C., 2021, 'Exploring factors influencing on online learning and ways to develop online learning after COVID 19 pandemic', PalArch's Journal of Archaeology of Egypt/Egyptology 18(4), 2659-2671. [ Links ]

Mahande, R.D., Jasruddin, J. & Nasir, N., 2019, 'Is success model for EDMODO e-learning user satisfaction through TAM on students', Journal of Educational Science and Technology (EST) 5(2), 140-152. https://doi.org/10.26858/est.v5i2.9575 [ Links ]

Malaquias, F.F. & Hwang, Y., 2016, 'Trust in mobile banking under conditions of information asymmetry: Empirical evidence from Brazil', Information Development 32(5), 1600-1612. https://doi.org/10.1177/0266666915616164 [ Links ]

Marakarkandy, B., Yajnik, N. & Dasgupta, C., 2017, 'Enabling internet banking adoption', Journal of Enterprise Information Management 30(2), 263-294. https://doi.org/10.1108/JEIM-10-2015-0094 [ Links ]

Mashroofa, M.M., Jusoh, M. & Chinna, K., 2019, 'Influence of attitudinal belief on e-learning behavior among academics in state universities of Sri Lanka', International Journal of Recent Technology and Engineering (IJRTE) 8(3), 8-14. https://doi.org/10.35940/ijrte.C1023.1183S319 [ Links ]

Matikiti, R., Mpinganjira, M. & Roberts-Lombard, M., 2018, 'Application of the technology acceptance model and the technology-organisation-environment model to examine social media marketing use in the South African tourism industry', South African Journal of Information Management 20(1), 1-12. https://doi.org/10.4102/sajim.v20i1.790 [ Links ]

Mohammadi, H., 2015, 'A study of mobile banking usage in Iran', International Journal of Bank Marketing 33(6), 733-759. https://doi.org/10.1108/IJBM-08-2014-0114 [ Links ]

Namahoot, K.S. & Laohavichien, T., 2018, 'Assessing the intentions to use internet banking', International Journal of Bank Marketing 36(2), 256-276. https://doi.org/10.1108/IJBM-11-2016-0159 [ Links ]

Naqvi, M.H.A., Jiang, Y., Miao, M. & Naqvi, M.H., 2020, 'The effect of social influence, trust, and entertainment value on social media use: Evidence from Pakistan', Cogent Business & Management 7(1), 1-23. https://doi.org/10.1080/23311975.2020.1723825 [ Links ]

Nguyen, V. & Nguyen, T., 2016, 'Perceived risk in the e-payment adoption via social network', Journal of Economic Development 27(12), 66-81. [ Links ]

Normalini, M., 2019, 'Revisiting the effects of quality dimensions, perceived usefulness and perceived ease of use on internet banking usage intention', Global Business and Management Research: An International Journal 11(2), 252-261. [ Links ]

Norrestad, F., 2022, 'Number of active online banking users worldwide in 2020 with forecasts from 2021 to 2024, by region', viewed 23 April 2022, from https://www.statista.com/statistics/1228757/online-banking-users-worldwide/.

Patel, K.J. & Patel, H.J., 2018, 'Adoption of internet banking services in Gujarat', International Journal of Bank Marketing 36(1), 147-169. https://doi.org/10.1108/IJBM-08-2016-0104 [ Links ]

Qalati, S.A., Vela, E.G., Li, W., Dakhan, S.A., Hong Thuy, T.T. & Merani, S.H., 2021, 'Effects of perceived service quality, website quality, and reputation on purchase intention: The mediating and moderating roles of trust and perceived risk in online shopping', Cogent Business & Management 8(1), 1-20. https://doi.org/10.1080/23311975.2020.1869363 [ Links ]

Rahi, S., Ghani, M. & Alnaser, F., 2017, 'Predicting customer's intentions to use internet banking: The role of technology acceptance model (TAM) in e-banking', Management Science Letters 7(11), 513-524. https://doi.org/10.5267/j.msl.2017.8.004 [ Links ]

Rasull, A., Jantan, A.H., Ali, M.H., Jaharudin, N.S. & Mansor, Z.D., 2020, 'Benefit and sacrifice factors determining internet banking adoption in Iraqi Kurdistan region', Journal of International Business and Management 3(1), 1-20. https://doi.org/10.37227/jibm.2020.65 [ Links ]

Rawwash, H., Masad, F., Enaizan, O., Eneizan, B., Adaileh, M., Saleh, A. et al., 2020, 'Factors affecting Jordanian electronic banking services', Management Science Letters 10(4), 915-922. https://doi.org/10.5267/j.msl.2019.10.004 [ Links ]

Raza, S.A., Umer, A. & Shah, N., 2017, 'New determinants of ease of use and perceived usefulness for mobile banking adoption', International Journal of Electronic Customer Relationship Management 11(1), 44-65. https://doi.org/10.1504/IJECRM.2017.086751 [ Links ]

Ryu, H.-S. & Ko, K.S., 2020, 'Sustainable development of Fintech: Focused on uncertainty and perceived quality issues', Sustainability 12(18), 1-18. https://doi.org/10.3390/su12187669 [ Links ]

Safari, K., Bisimwa, A. & Armel, M.B., 2020, 'Attitudes and intentions toward internet banking in an under developed financial sector', PSU Research Review 6(1), 39-58. https://doi.org/10.1108/PRR-03-2020-0009 [ Links ]

Saprikis, V., Avlogiaris, G. & Katarachia, A., 2021, 'Determinants of the intention to adopt mobile augmented reality apps in shopping malls among university students', Journal of Theoretical and Applied Electronic Commerce Research 16(3), 491-512. https://doi.org/10.3390/jtaer16030030 [ Links ]

Sharma, S.K. & Govindaluri, S.M., 2014, 'Internet banking adoption in India: Structural equation modeling approach', Journal of Indian Business Research 6(2), 155-169. https://doi.org/10.1108/JIBR-02-2013-0013 [ Links ]

Sharma, S.K. & Sharma, M., 2019, 'Examining the role of trust and quality dimensions in the actual usage of mobile banking services: An empirical investigation', International Journal of Information Management 44(1), 65-75. https://doi.org/10.1016/j.ijinfomgt.2018.09.013 [ Links ]

Singh, S. & Srivastava, R.K., 2020, 'Understanding the intention to use mobile banking by existing online banking customers: An empirical study', Journal of Financial Services Marketing 25(3), 86-96. https://doi.org/10.1057/s41264-020-00074-w [ Links ]

Tam, C. & Oliveira, T., 2016, 'Understanding the impact of m-banking on individual performance: DeLone & McLean and TTF perspective', Computers in Human Behavior 61(1), 233-244. https://doi.org/10.1016/j.chb.2016.03.016 [ Links ]

Tsourela, M. & Nerantzaki, D.M., 2020, 'An internet of things (IoT) acceptance model. Assessing consumer's behavior toward IoT products and applications', Future Internet 12(11), 1-23. https://doi.org/10.3390/fi12110191 [ Links ]

Um, N., 2021, 'Learners' attitude toward e-learning: The effects of perceived system quality and e-learning usefulness, self-management of learning, and self-efficacy', International Journal of Contents 17(2), 41-47. [ Links ]

Vejacka, M. & Štofa, T., 2017, 'Influence of security and trust on electronic banking adoption in Slovakia', Economics and Management 20(4), 135-150. https://doi.org/10.15240/tul/001/2017-4-010 [ Links ]

Venkatesh, V. & Bala, H., 2008, 'Technology acceptance model 3 and a research agenda on interventions', Decision Sciences 39(2), 273-315. https://doi.org/10.1111/j.1540-5915.2008.00192.x [ Links ]

Venkatesh, V. & Davis, F.D., 1996, 'A model of the antecedents of perceived ease of use: Development and test', Decision Sciences 27(3), 451-481. https://doi.org/10.1111/j.1540-5915.1996.tb01822.x [ Links ]

Venkatesh, V. & Davis, F.D., 2000, 'A theoretical extension of the technology acceptance model: Four longitudinal field studies', Management Science 46(2), 186-204. https://doi.org/10.1287/mnsc.46.2.186.11926 [ Links ]

Venkatesh, V., Morris, M.G., Davis, G.B. & Davis, F.D., 2003, 'User acceptance of information technology: Toward a unified view', MIS Quarterly 27(3), 425-478. https://doi.org/10.2307/30036540 [ Links ]

Venkatesh, V., Thong, J.Y. & Xu, X., 2012, 'Consumer acceptance and use of information technology: Extending the unified theory of acceptance and use of technology', MIS Quarterly 36(1), 157-178. https://doi.org/10.2307/41410412 [ Links ]

Verma, S. & Kumar, T., 2020, 'Antecedents of online banking adoption: An empirical study in an emerging economy', Journal of Services Research 20(1), 7-19. [ Links ]

Wahab, S.A.A. & Azzman, T.S.A.T.M., 2019, 'Factors predicting the trend of using Ita'leem among lecturers in international Islamic university Malaysia', Asian Journal of Applied Communication 1(1), 225-267. [ Links ]

Wang, J., Molina, M.D. & Sundar, S.S., 2020, 'When expert recommendation contradicts peer opinion: Relative social influence of valence, group identity and artificial intelligence', Computers in Human Behavior 107(1), 1-7. https://doi.org/10.1016/j.chb.2020.106278 [ Links ]

Xu, X., Li, Q., Peng, L., Hsia, T.L., Huang, C.J. & Wu, J.H., 2017, 'The impact of informational incentives and social influence on consumer behavior during Alibaba's online shopping carnival', Computers in Human Behavior 76(1), 245-254. https://doi.org/10.1016/j.chb.2017.07.018 [ Links ]

Zhang, T., Lu, C. & Kizildag, M., 2018, 'Banking on-the-go: Examining consumers' adoption of mobile banking services', International Journal of Quality and Service Sciences 10(3), 279-295. https://doi.org/10.1108/IJQSS-07-2017-0067 [ Links ]

Correspondence:

Correspondence:

Mia Bothma

mia.bothma@nwu.ac.za

Received: 13 Oct. 2022

Accepted: 26 Jan. 2023

Published: 20 Mar. 2023

{kind=link}

{kind=link}

{kind=link}

{kind=link}