Services on Demand

Article

English (pdf)

English (pdf)

Article in xml format

Article in xml format Article references

Article references

Indicators

Related links

-

Cited by Google

Cited by Google -

Similars in Google

Similars in Google

Share

Permalink

PermalinkJournal of Energy in Southern Africa

On-line version ISSN 2413-3051

Print version ISSN 1021-447X

J. energy South. Afr. vol.33 n.2 Cape Town May. 2022

http://dx.doi.org/10.17159/2413-3051/2022/v33i2a13453

ARTICLES

Using liquefied petroleum gas to reduce the operating cost of the Ankerlig peaking power plant in South Africa

S. Clark*; C. McGregor; J.L. van Niekerk

Solar Thermal Energy Research Group, Department of Mechanical and Mechatronic Engineering, Stellenbosch University, Stellenbosch, South Africa

ABSTRACT

Along with the load-shedding problem that Eskom is having with the current generation system, the operator is forced to use its peaking plants at Ankerlig and Gourikwa in the Western Cape much more than planned. The two plants are set up for dual fuel operations, able to be fuelled with diesel as well as gas. As Eskom does not have access to natural gas, both plants have been fuelled with diesel. For the last three years, 2019 through 2021, Eskom has expended an average of over R4 billion per year on diesel fuel for its peaking plants, with the majority of this at Ankerlig and Gourikwa. For 2022, in their request for a rate increase, Eskom noted that their anticipated diesel fuel expenditures will increase to over R6.5 billion. This could be reduced by more than half if the plants were fuelled with natural gas. The problem Eskom faces is sourcing natural gas to fuel these plants. There has been consideration of liquefied natural gas importation into the Western Cape that could be utilised to fuel the Ankerlig plant. However, the high capital cost for this option has led to delay in the commencement of this project. There is another alternative that can be implemented in a short time-frame, using currently available gas, in the form of liquefied petroleum gas. With this fuel, the Ankerlig peaking plant could be switched to gas fuel and Eskom would have a significant reduction in the cost of fuel. In this study the economic benefit of this fuel change option is analysed.

Keywords: Eskom, load-shedding, diesel, LNG

Introduction

Commencing in 2010, the South African government, through the Department of Energy (now the Department of Mineral Resources and Energy), developed a national long-term forecast and plan for electricity production. The process used was the development of an Integrated Resource Plan (IRP) (DoE, 2011). Recognising that the conditions assumed in the IRP process can change, the plan was for the IRP to be a living document that is updated periodically. Updates to the IRP were prepared in 2013, 2016 and 2018 (DoE, 2018).

In the 2018 IRP, it was assumed that the short-term needs of the system were well provided for and no new generation capacity was needed until later in the coming decade. Eskom believed it was well on its way to improving the availability of its base load plants and was in the process of commissioning two new plants, Medupi and Kisule, which would add almost 20% of new capacity. It stated that 'Committed REIPPP [Renewable Independent Power Producer Programme] (including the 27 signed projects) and Eskom capacity rollout ending with the last unit of Kusile in 2022 will provide more than sufficient capacity to cover the projected demand and decommissioning of plants up to around 2025' (DoE, 2018). The 2018 update to the IRP was issued for comment in September 2018. Almost before the 2018 IRP was finalised, Eskom found significant problems with the new coal plants and performance challenges with the existing plants (DoE, 2019a). These problems led to load-shedding in late 2018. Unfortunately, the problems increased in 2019 and so did load shedding. This resulted in level 6 load-shedding for the first time, in December 2019, with Eskom shedding over 6 GW of demand. While the reduced electricity demand during the Covid pandemic reduced load-shedding in 2020, load-shedding returned once normal demand was restored. This generation shortfall has also led to an extensive use of the dispatchable generation and high diesel consumption.

The short-to-medium-term problems found with the 2018 update of the IRP led to another IRP update in 2019, just a few months after the 2018 IRP was released. As detailed in the 2019 IRP, the short-term problems will be challenging to resolve, and load-shedding will be around for some years, with new generation capacity taking at least three years to construct (DoE, 2019). In addition to significant load-shedding due to the shortage of baseload generation, Eskom has been using its peaking generation facilities much more than it had planned. These plants are fuelled with diesel fuel. Eskom has forecast in its 2021 integrated report that it had generated an average of over 1300 GWh of power from their peaking plants for the last three years, which necessitated spending over R4 billion on diesel fuel each year (Eskom, 2021). Eskom forecasts that, with the increased price of diesel, the expenditure for diesel fuel for these plants will increase to over R6.5 billion for 2022 (Creamer, 2022).

The two peaking plants, Ankerlig and Gourikwa, are dual fuel plants and could be converted to gas fuel if it was available (Eskom, 2014a). As gas is significantly less expensive on an energy basis (per GJ), Eskom and the government would like to make this change (Western Cape Government, 2021). However, they do not have access to gas. With minimal available local gas production, gas importation would be required. The assumption throughout the development of the various IRPs was that this gas would be provided through importing liquefied natural gas (LNG) (DoE, 2011, 2018). This has proven to be economically challenging, due to the high upfront cost of importation facilities. Liquefied petroleum gas (LPG) is another option for diesel replacement for the peaking plants. It might not fully capture the cost advantage of LNG, but is a hydrocarbon gas and, much like natural gas, is a suitable fuel for gas turbine usage and would provide much of the benefit. In their product brochures, Siemens confirms that their V94.2 turbines, as used in Ankerlig and Gourikwa, can utilise LPG fuel (Siemens, 2020). LPG is currently being imported into Saldanha Bay, has advantages of storage and transport much like diesel and is much less expensive than diesel as will be detailed in the following section on fuel costs. This is a solution that could be implemented in a short time frame.

Fuel costs

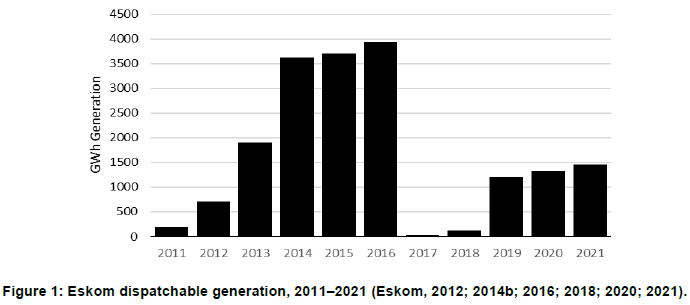

The major issue for diesel is its cost. Table 1, derived from the Eskom 2021 Integrated Report and the Eskom 2022 request for fare increase, shows the cost for diesel fuel that Eskom has expended from 2019 through 2021 and anticipates to expend in the coming year (Eskom, 2012; 2014b; 2016; 2018; 2019; 2020; 2021). To estimate the likely requirement for peaking plant usage going forward, Eskom Integrated Reports since 2011 were reviewed. As shown in Figure 1, Eskom has reported generation from its peaking plants ranging from 29 GWh to over 3 700 GWh per year. This has averaged 1 655 GWh annually for the eleven-year period. The average annual fuel cost has been R4 400 million, which is close to that from the last three years. This would imply that the current usage of the peaking plants is consistent with their use over the last decade and likely to continue into the coming years. Increased utilisation of variable renewable generation will also lead to continued usage of these peaking plants for dispatchable power (Clark, et.al, 2020).

While a change to LPG from diesel would reduce the CO2 emissions from this generation the most significant advantage is lower cost. For the last three years the retail price of diesel fuel in South Africa has averaged approximately R14 per litre, or R377 per GJ (DMRE, 2020). Assuming a usage of 10 000 GJ per GWh of power generation, as noted by the US Energy Information Agency (US EIA, n.d.), this implies a fuel cost for diesel generation of R3.8 per kWh. For 2022, increased international oil prices have increased the local retail price of diesel to over R20 per litre. This would give a cost of over R5.5 per kWh. As shown in Table 1, Eskom pays approximately 80% of the NERSA stated retail price, which in January 2022 was R17.24 per litre (DMRE, 2020).

The current (January 2022) South African government-regulated refinery gate price for LPG is just under R8.3 per litre (DMRE, 2020). LPG contains approximately 26 MJ per litre, so this converts to R320 per GJ. Using this fuel price for power generation would imply a fuel cost of R3.2 per kWh. Using this price comparison, this would indicate that a conversion from diesel fuel to LPG would reduce the fuel cost by over 40%.

These prices are a snapshot of prices at the current time and do not indicate the long-term price relationship between the cost of the two fuels. To estimate the long-term cost implication of changing to LPG from diesel, we have reviewed several price relationships that might provide insight.

Delphos Engineering conducted the 2019 analysis for the Western Cape government for the feasibility of an LNG importation facility at Saldanha Bay. Besides looking at the cost of imported LNG, which was their focus, in their report they compared the costs of diesel and LPG fuels for the Ankerlig plant. They forecast that LPG delivered to the Ankerlig plant would remain at approximately 50% of the price of diesel on an energy basis going forward (Delphos International Ltd., 2019).

Another comparison, that might be more valid, is the international posted prices for the two fuels. Both diesel and LPG are internationally marketed and have price references. The two international major oil marker prices are West Texas Intermediate and Brent Crude (DailyFX, 2022). South Africa diesel pricing is based on Brent pricing (Gwegwe, 2021). For diesel, the price is the price of oil plus processing and transportation. This works out to a diesel price approximately 15% above the marker oil price. LPG pricing is not directly related to oil or natural gas pricing but is affected by a combination of the two. As in oil pricing there are two main marker prices, Mount Belvieu price in the USA and Saudi LPG pricing (Allen Consulting, 2009). As most markets can be supplied from either source, the two generally move together and result in similar delivered prices. For South Africa, both prices are utilised, with Sunfire, which operates a Saldanha Bay LPG facility, quoting Saudi prices and Bidvest, which operates the Richards Bay LPG facility, utilising LPG sourced from the USA (Bidvest, 2020; MOGs, 2020). New regulations on LPG drafted by the DMRE propose tying the price of LPG in South Africa to the Saudi contract price (DMRE, 2021).

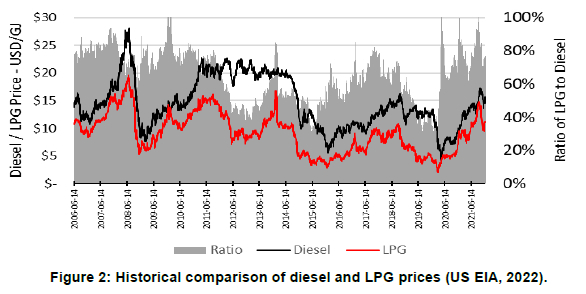

As noted above, one of the internationally accepted market prices for LPG is the price at Mount Belvieu, which is the price at a major storage point near Houston, Texas. The US Gulf Coast is one of the major sources for international supplies of LPG. It is also the source of significant volumes of diesel production. The US Energy Information Agency (US EIA) publishes prices for both products at this location. With these figures, it is possible to observe how the prices for the two products have related over time. For this analysis, we have converted the reference prices from prices per gallon to prices per GJ to put them on the same energy basis. Figure 2 shows the daily market prices in GJ for the two products over the last fifteen years, and the ratio of the prices (US EIA, 2022) . As can be seen from this information, over this period, diesel prices have ranged from below USD 4 per GJ to above USD 28 and LPG prices have ranged from below USD 2 to USD 20. Over this period, LPG has ranged between 20% and 80% of the price of diesel on a GJ basis, with an average of 63%. From 2019 through 2021, the average ratio has been 60%.

Greenhouse gas emissions

Diesel fuel is convenient, but as noted above it is expensive. It is readily available in South Africa and, since it is a liquid, it can be easily transported and stored. It can also be used in internal combustion engines as well as dual fuel gas turbines. It is less polluting than coal, with lower sulphur dioxide, nitric oxide and particulate emissions, as well as less CO2 emissions during combustion, making it a cleaner option than coal-fuelled generation (US EPA, 2013). However, it still has significant pollution and CO2 production, so it is not a preferred fuel.

LPG is an alternative fuel that is also currently available in South Africa. Unlike methane, which is the major component of natural gas, LPG itself is not considered to be a greenhouse gas. Methane has a lower specific gravity than air and any leaked methane will accumulate in the upper atmosphere and is considered to have a higher impact as a greenhouse gas than carbon dioxide emissions (US EPA, 2021). The life span of methane in the atmosphere is in the range of twenty years, compared to centuries for carbon dioxide, but the impact is much higher during that period. The components of LPG, propane and butane, are heavier than air and do not collect in the upper atmosphere. For this reason, they are not classified as greenhouse gases. (Ryskamp, 2017). The CO2 production from burning LPG is approximately 85% of that from diesel fuel. It also produces less pollutants than diesel when burned (US EIA, 2017). However, LPG does produce approximately 15% more CO2 during combustion than natural gas (US EIA, 2017).

The proposed Saldanha LNG terminal

Natural gas sourced by LNG importation is not currently available in South Africa, so the price for this fuel must be inferred from other sources. The major current market for LNG is Japan, so most LNG price comparisons are based on LNG imported into Japan. The recent price for the last few years for LNG into Japan has been in the range of USD 8 per GJ. However, since late 2021 the price has jumped to over USD 35 per GJ due to a gas shortage in Europe and Asia (Investing.com, 2022). Most of the discussion of price for LNG importation has assumed a long-term estimate of USD 10 per GJ (World Bank, 2021; Delphos International Ltd., 2019). This would be 25% less expensive than LPG. However, as noted below, this is the cost of LNG as it arrives at the terminal. The cost of LNG delivered to the power plant will be higher, based on the cost of importation and handling. LNG is a liquid only when kept at -162o Centigrade. Therefore, storage and transport of LNG is a more difficult compared to diesel or LPG.

The major challenge for LNG usage, which has been the reason that the Saldanha Bay importation project is still in feasibility analysis, is that the amortisation of the cost of the facilities must be absorbed by the amount of product throughput. The cost of the LNG importation facilities in Saldanha is estimated to be between USD 600 million and USD 1 billion (R8-14 billion) (Delphos International Ltd., 2019). The USD 1 billion capital cost would work out to over USD 70 million dollars per year amortisation, assuming a 25-year life and 5% cost of capital. Ankerlig has used approximately 7 million GJ per year of fuel for the last three years. With this fuel usage and this amortisation cost, the delivered cost of natural gas would be increased by over USD 10 per GJ, to cover the capital cost of the import terminal, giving a delivered gas cost of over USD 20 per GJ. In an ideal situation, where Eskom would correct the issues with its generation system, the likely fuel requirement should decrease, making it more difficult to justify the investment in an LNG importation facility. To have enough throughput volume to bring this amortisation cost to a competitive level has led the project proponents to suggest that Ankerlig be converted to a mid-merit plant (Delphos International Ltd., 2019).

An LNG importation terminal in Saldanha Bay has been a consideration for many years. In 2009, Gigajoule Corp conducted a pre-feasibility study for this project (Visagie, 2013). In 2012, the Western Cape government expressed an interest in building an LNG terminal at Saldanha Bay and conducted another pre-feasibility study (Visagie, 2013). This was followed by several other studies to understand the environmental considerations and the business case for the project. The latest step in the project was a business case feasibility analysis conducted by the US Trade and Development Agency on behalf of the Western Cape government (Delphos International Ltd., 2019). This was completed in 2019.

While the project was conceived to provide gas for commercial and residential users in the Western Cape, as stated in the 2013 study 'The market evaluation of the Cape West Coast region concluded that gas-fired power generation would play an enabling role to the viability of any of the gas importation options evaluated' (Visagie, 2013). In that study and the 2019 study, the assumption was conversion of the Ankerlig plant from its current peaking service with 5% capacity factor to mid-merit usage with 40-50% capacity factor. This change was necessary to provide enough throughput volume to make the project viable.

It is possible that the project might proceed, but the requirement to utilise Ankerlig in mid-merit usage is not consistent with the IRP planning (DoE, 2019). Due to the cost of fuel, using these plants in mid-merit service results in an overall more expensive system than solar and wind-based generation with minimal peaking generation (Wright et al., 2018). In peaking use, the amount of gas that would be needed for the plant is not enough to justify the cost for the terminal. An LPG alternative fuel should be an option worth pursuing. South Africa risks that the LNG facility is never constructed and Eskom continues to rely on expensive diesel as the fuel for these plants.

The challenge of dispatchability

Importing LNG for peaking power usage, as well as any other gas source, has a major challenge of balancing use of the gas for dispatchable power with any other usage. Most industrial gas usage is flat, with the user needing a given amount of gas each day. Dispatchable power generation is the opposite. Very large rates of gas are needed for short periods and the total annual volume is quite small. However, when needed, the high rate must be available rapidly. This could be for several hours per day up to several days continuously in the highest demand period, followed by low usage for most months each year. The expected profile for the long-term requirement of dispatchable energy generation in South Africa was detailed in an analysis from Clark, Van Niekerk and Petrie (2020).

Most gas delivery systems have challenges meeting this demand profile, and the only solution is significant buffer storage. Since LPG is stored as a liquid, it acts more like diesel in this regard and can be dispatched as needed.

LPG importation and storage

LPG is currently imported into Saldanha Bay and no new importation facilities would be needed to bring the required volumes of LPG into the area. The Sunrise Energy importation facility currently contains 5 500 tonnes of LPG storage (MOGs, 2020). Avedia Energy also has an import facility in Saldanha Bay, with 2 200 tonnes of LPG storage (Avedia Energy, 2022). As for all fuels, the challenge remains in the cost-effective storage and delivery of the fuel at high rates for dispatchable usage. Besides being locally available, one advantage of LPG is that it is normally in a liquid phase at ambient temperature under pressure slightly above atmospheric pressure, which is significant for this usage.

There is some question regarding the throughput capacity of the Sunrise and Avedia LPG import facilities in Saldanha Bay and their ability to meet the need for the Ankerlig demand. The issue to be determined is the amount of LPG storage that might be required. It would likely be necessary for the facilities to be expanded to provide additional LPG storage. Both Avedia and Sunrise have expressed plans to expand their storage facilities (MOGs, 2020; Avedia Energy, 2022). In addition, LPG fuel storage at Ankerlig would likely be necessary.

In Richards Bay, Bidvest has recently commissioned an LPG storage and delivery project (Bidvest, 2020). The project has four LPG tanks, which will each store 10 000 m3 (4 x 5 500 tonnes). The cost of the plant was listed as less than R1 billion, as compared to an LNG importation facility approaching USD 1 billion (Delphos International Ltd., 2019; Bidvest, 2020). Bidvest commenced the project in June 2017, broke ground on the facility in June 2018, and commissioned the plant in mid-2020 (Bidvest, 2020). A duplicate of this plant would provide for 40 000 m3 of LPG storage, or 1 PJ of fuel. Assuming 10 000 GJ per GWh, this stored volume would generate 100 GWh of power. This would be enough to run the 1.3 GW Ankerlig plant for 76 hours, or slightly more than three days; this compares to the current diesel storage at Anker-lig of 32 million litres (Eskom, 2014a), with 1.2 PJ energy. As importation facilities are in place and no pipeline or alternate delivery system investment is required, developing an equivalent LPG storage and delivery system should be the only investment that is required to allow LPG delivery to Ankerlig.

Fuel delivery to Ankerlig

The Ankerlig generation plant is approximately 100 km from Saldanha Bay and the Sunrise and Avedia LPG importation facilities. For normal gas or LPG delivery a pipeline would be the lowest-cost means. However, due to the dispatchable generation usage intended from the Ankerlig facility, the delivery facilities would be used for a minimum time each year. For diesel delivery to the Ankerlig plant, Eskom has chosen to have the fuel delivered by truck, avoiding the cost of a pipeline. Each diesel truck delivers approximately 50 000 litres of diesel, or 1 900 GJ of fuel. Thus, at 10 000 GJ per GWh, the 1.3 GW plant requires seven truckloads of diesel per hour of generation. The onsite storage for diesel is 32 million litres or 640 truckloads.

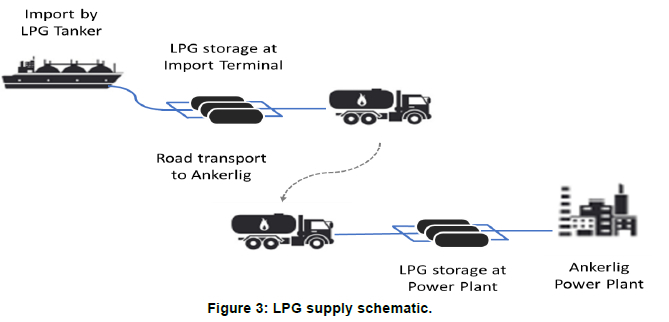

It can be assumed that this same option would likely be considered for LPG delivery to the plant. Each truck can deliver approximately 50 000 litres of LPG fuel or 1 300 GJ. Compared to seven truck-loads of diesel, ten truck-loads of LPG would be required to operate the plant per hour of generation. Assuming 5% capacity factor for the plant, this would mean 4 400 truckloads of LPG per year, duplicating the energy storage of the 32 million litres of diesel would require an LPG storage facility equivalent to the Bidvest LPG plant to be constructed at Ankerlig. The schematic of LPG delivery to Ankerlig is shown in Figure 3.

Fuel change economics

With the information available, it is not possible to perform a definitive breakeven analysis of the change from diesel fuel to LPG for Ankerlig. To make a definitive analysis, it would be necessary to determine the actual LPG price that Eskom would be required to pay. As was shown in Table 1, Eskom has published their current and projected cost for diesel fuel. However, it is not apparent at what price Eskom would be required to pay for LPG. Assuming the international relationship of LPG at 60% of the price of diesel, it is possible to make an economic comparison of the cost savings from the last three years, where actual usage and diesel costs are available.

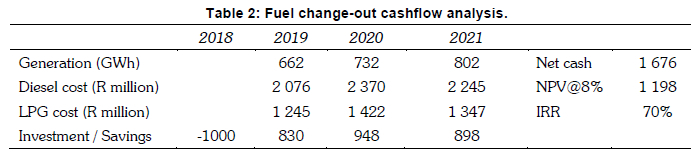

For this analysis, it is assumed that the 1.3 GW Ankerlig generation capacity is 55% of the 2.4 GW of dispatchable power that Eskom has used for the last three years. For the fuel change, the assumption is that new LPG facilities would cost R1 billion, as per the investment by Bidvest in their Richards Bay LPG facility. LPG was assumed to be provided to Ankerlig at 60% of the price of diesel each year. It can be seen from this economic analysis, as shown in Table 2, the payout is slightly over one year and the economics over the three-year period is quite impressive, with a rate of return on the investment of 70% in the three-year term. With the Eskom estimated expenditure for diesel fuel for 2022 of R6 500 million, the change at Ankerlig to LPG would have an additional fuel saving of over R1 400 million for the year.

This simple cashflow analysis does not address the sharing of costs and benefits between Eskom and a potential supply partner, but only shows total cashflow. If Eskom was to turn the requirement for investment in the facilities to a supply partner, they would also share in some of the cash benefit. However, with that arrangement, Eskom can enjoy the lower fuel cost without expending its limited capital.

Greenhouse gas emissions

While the main justification for changing fuel at the generation plant is cost-saving, there is an added benefit of lowering the greenhouse gas emissions from this power generation. For the 2 200 GWh of diesel-fuelled generation from Ankerlig in the last three years, we can estimate that the CO2 production was approximately 1.6 million tonnes (US EIA, 2017). Switching to LPG would have reduced this amount by over 15%. LPG also has lower emissions of pollutants and particulate matter than burning diesel, so there would be improvement in this too.

Change to natural gas

LPG fuel only gets a portion of the improvement in fuel savings that natural gas could potentially give. There is a question of whether this change precludes the change to natural gas. With the minimum investment required to make this fuel change and the quick payout time, this change does not imply that the change to natural gas fuel via LNG importation would not be reasonable, but it means that the economic advantage is reduced. As noted above, the changeout to LNG would require the development of a gas market in the Western Cape that up to now has not happened. Waiting for this to develop could potentially condemn the Ankerlig facility to use more expensive diesel fuel until some other option can be developed.

Business structure

Given the probability of load-shedding by Eskom continuing for the next several years, this concept should be followed up immediately with all interested parties, which should include potential investors, Eskom as the customer, and the government as the coordinating party. This could be conducted like the REIPPP projects, where companies can bid on the supply of LPG fuel to the Eskom Ankerlig plant, which can be done on a capacity plus usage payment or a simple competitive supply arrangement. This fuel change-over should not require any investment on the part of Eskom nor government guarantee to take the risk out of the project. Outside investors, like Sunrise, Avedia, Bidvest or others, would likely be interested in building the required infrastructure, with a suitable fuel supply agreement for Ankerlig.

Conclusions

• The current situation with the South African grid indicates that the diesel peaking plants will continue to be used at a reasonably high levels for the coming years.

• Diesel fuel costs will remain a major burden on Eskom finances.

• Switching out the diesel at Ankerlig to LPG fuel can significantly reduce this cost, with a low-risk, low-capital cost project.

• This fuel change would be feasible, with no cost to Eskom, as it can be done as a service provided by a private company.

• The fuel change out should have a quick payback with long lasting benefits, even when load-shedding is resolved. This change should be pursued as a matter of urgency to reduce the burden on Eskom from the current cost of diesel.

• The fuel changeout will also improve greenhouse gas emissions.

Author contributions

S. Clark: Formulation and execution of research, data analysis and write-up.

C. McGregor, J. van Niekerk: Research formulation and supervision.

References

Allen Consulting. 2009. Review of the appropriateness of the current LPG international benchmark in the setting of domestic LPG prices. Available: https://www.accc.gov.au/system/files/Review_of_the_appropriateness_of_the_current_LPG_international_benchmark_in_the_setting_of_domestic_LPG_prices-October_2009.pdf. [ Links ]

Avedia Energy. 2022. Avedia Energy. Available: https://avediaenergy.com/. [ Links ]

Bidvest. 2020. LPG and the Mounded LPG Facility Mounded LPG Facility fast facts. Available: https://www.bidvest.co.za/bidvest-tank-terminals/about-Mounded-LPG-Facility.php [2020, September 20]. [ Links ]

Clark, S., Van Niekerk, J. & Petrie, J. 2020. The Use of Natural Gas to Facilitate the Transition to Renewable Electric Power Generation in South Africa. Stellenbosch University. Available: https://scholar.sun.ac.za/handle/10019.1/109312. [ Links ]

Creamer, T. 2022. Eskom seeks to show prudency of running diesel plants as its pegs cost of load-shedding at R9.53/kWh. Engineering News. Available: https://www.engineeringnews.co.za/article/eskom-seeks-to-show-prudency-of-running-diesel-plants-as-its-pegs-cost-of-load-shedding-at-r953kwh-2022-01-20. [ Links ]

DailyFX. 2022. Crude Oil Prices. Available: https://www.dailyfx.com/crude-oil. [ Links ]

Delphos International Ltd. 2019. Feasibility Study for the Western Cape Integrated Liquefied Natural Gas Importation and Gas-to-Power Project. Cape Town. Available: https://www.westerncape.gov.za/110green/download-lng-feasibility-study. [ Links ]

Eskom. 2012. Integrated Report for the year ending 31 March 2012. Available: www.eskom.co.za/IR2012/027.html. [ Links ]

Eskom. 2014a. Ankerlig and Gourikwa gas turbine power stations. Available: https://www.eskom.co.za/sites/heritage/Pages/ANKERLIG-AND-GOURIKWA.aspx [2020, September 20]. [ Links ]

Eskom. 2014b. Integrated Results for the year ending 31 March 2014. Available: https://www.eskom.co.za/wp-content/uploads/2022/01/full-integrated2014.pdf. [ Links ]

Eskom. 2016. Integrated Report for the year ending 31 March 2016. Available: https://www.eskom.co.za/wp-content/uploads/2021/02/Eskom_integrated_report_2016.pdf. [ Links ]

Eskom. 2018. Integrated Report for the year ending 31 March 2018. Available: www.eskom.co.za/IR2018. [ Links ]

Eskom. 2019. Integrated report for the year ending 2019. Available: https://www.eskom.co.za/IR2019/Documents/Eskom_2019_integrated_report.pdf. [ Links ]

Eskom. 2020. Integrated Report of the year ending 31 March 2020. Available: https://www.eskom.co.za/IR2020/Documents/Eskom2020_integrated_report.pdf. [ Links ]

Eskom. 2021. Intergrated Report for the year ending 31 March 2021. Available: https://www.eskom.co.za/wp-content/uploads/2021/08/2021IntegratedReport.pdf. [ Links ]

Gwegwe, S. 2021. Petrol and diesel price: Fuel costs go up for November. The South African. (November). Available: https://www.thesouthafrican.com/news/petrol-and-diesel-price-increase-november-south-africa/. [ Links ]

Investing.com. 2022. LNG Japan/Korea Marker PLATTS Future Historical Prices. Available: https://www.investing.com/commodities/lng-japan-korea-marker-platts-futures-historical-data [2022, January 23]. [ Links ]

MOGs. 2020. Sunrise Energy LPG Terminal. Available: https://mogs.co.za/oil-gas-services/operations/sunrise-energy/ [2020, September 20]. [ Links ]

Ryskamp, R. 2017. Emissions and Performance of Liquefied Petroleum Gas as a Transportation Fuel: A Review. Available: https://auto-gas.net/wp-content/uploads/2019/11/2017-WLPGA-Literature-Review.pdf. [ Links ]

DMRE [Department of Mineral Resources and Energy] 2021. Published for public comments: Draft Liquefied Petroleum Gas Rollout Strategy, Available: http://www.energy.gov.za/files/policies/Gazette44384-for-comments-Draft-LPG-rollout-strategy.pdf. [ Links ]

DMRE. 2020. Breakdown of petrol, diesel and paraffin prices as of 05 February 2020. Available: http://www.energy.gov.za/files/esources/petroleum/February2020/Breakdown-of-Prices.pdf. [ Links ]

DoE.[Department of Energy] 2011. Integrated Resource Plan for Electricity 2010-2030. DOI: 10.1016/j.wneu.2010.05.012. [ Links ]

DoE. 2018. Integrated Resource Plan for South Africa (2018). Available: http://www.energy.gov.za/IRP/irp-update-draft-report2018/IRP-Update-2018-Draft-for-Comments.pdf. [ Links ]

DoE. 2019. Integrated Resource Plan for South Africa (2019). SouthAfrica. Available: http://www.energy.gov.za/files/docs/IRP_2019.pdf. [ Links ]

US EIA [US Energy Information Agency]. 2017. How much carbon dioxide is produced when different fuels are burned? Available: https://www.eia.gov/tools/faqs/faq.php?id=73&t=11 [2020, September 20]. [ Links ]

US EIA. 2022. Petroleum and other Liquids - Spot Prices. Available: https://www.eia.gov/dnav/pe1/PET_PRI_SPT_S1_M.htm [2022, January 23]. [ Links ]

US EIA. n.d. How much coal, natural gas, or petroleum is used to generate a kilowatthour of electricity? Available: https://www.eia.gov/tools/faqs/faq.php?id=667&t=6 [2020, September 20]. [ Links ]

US EPA.[US Environmental Protection Agency] 2021. Global Methane Initiative, Importance of Methane. Available: https://www.epa.gov/gmi/importance-methane#:~:text=Methane_is_also_a_greenhouse,-influenced)_and_natural_sources.&text=Methane_is_more_than_25,trapping_heat_in_the_atmosphere. [2021, May 25]. [ Links ]

Western Cape Government. 2021. Parliament of the Province of the Tablings and Committee Reports - chapter 5. Available: https://www.wcpp.gov.za/sites/default/files/Final_Atc_14-2021_19_February_2021_Report_Oversight_visit_Eskom_Atlanitis_Eng..pdf. [ Links ]

World Bank. 2021. World Bank Commodities Price Forecast (nominal US dollars). Available: https://thedocs.worldbank.org/en/doc/ff5bad98f52ffa2457136bbef5703ddb-0350012021/related/CMO-October-2021-forecasts.pdf. [ Links ]

* Corresponding author: Email: sclark@sun.ac.za

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}