Servicios Personalizados

Articulo

Inglés (pdf)

Inglés (pdf)

Articulo en XML

Articulo en XML Referencias del artículo

Referencias del artículo

Indicadores

Links relacionados

-

Citado por Google

Citado por Google -

Similares en Google

Similares en Google

Compartir

Permalink

PermalinkJournal of Energy in Southern Africa

versión On-line ISSN 2413-3051

versión impresa ISSN 1021-447X

J. energy South. Afr. vol.25 no.3 Cape Town ago. 2014

ARTICLES

The impacts of energy prices and technological innovation on the fossil fuel-related electricity-growth nexus: An assessment of four net energy exporting countries

Qin FeiI; Rajah RasiahII; JiaShen LeowIII

IDepartment of Economics, Faculty of Economics and Administration, University of Malaya, Kuala Lumpur, Malaysia

IIDepartment of Development Studies, Faculty of Economics and Administration, University of Malaya, Kuala Lumpur, Malaysia

IIILoving Care Early Childhood Centre, Johor Bahru, Malaysia

ABSTRACT

This study uses annual data from 1974 to 2011 to examine the long-run and short-run relationships between fossil fuel powered electricity consumption, economic growth, energy prices and technological innovation for four net energy exporting countries. Canada, Ecuador, Norway and South Africa are chosen as the main research background in order to investigate how the development degree and economic dependence on energy exports affect the electricity-growth nexus. Based on the results drawing from the ARDL approach and the Granger causality test, economic growth positively influences the variation in fossil fuel powered electricity consumption in both the short-run and long-run for all four countries. The reverse causality from electricity consumption to economic growth is only evident in Ecuador and Norway. The degree of dependence on energy exports is a contributory factor of explaining the causality puzzle of the electricity-growth nexus. Given the fact that technological innovation does not benefit fossil fuel powered electricity generation, this paper suggests these net energy exporting countries to replace fossil fuel with more sustainable and effective sources in the electricity generation process.

Keywords: Electricity-growth hypothesis; energy prices; technological innovation; ARDL approach; VEC model; Granger causality.

1. Introduction

Growing concerns over shortages in fossil fuel supply have triggered the interests of many studies on investigating the relationship between electricity consumption and economic growth. Although new results have continued to emerge from empirical studies on the electricity-growth nexus since the 1970s, there is still a lack of consensus on the determinants of this relationship (Payne, 2010). According to Narayan and Prasad (2008), two-thirds of available studies published in Energy Policy and Energy Economics find a unidirectional Granger causality running from electricity consumption to economic growth in both developed and developing countries. In other words, implementing electricity conservation policies could slow down economic growth due to the fact that most countries are economically dependent on the expansion in the electricity-gulping industries to support their social developments (Murry and Nan, 1996; Wolde-Rufael, 2006; Chen et al., 2007; Narayan and Prasad, 2008).

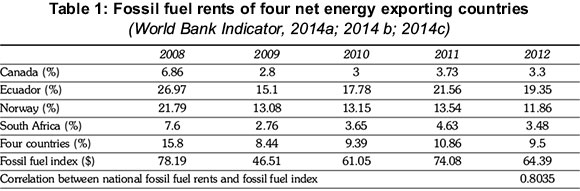

Moreover, although a series of price hikes in fossil fuel and the agreement of phasing out inefficient fossil fuel subsidies in G20 benefited fossil fuel exporting economies in year 2008, this lucrative exporting income stream did not sustain due to the beginning of the first commitment period (20082012) of the Kyoto Agreement (G20 Research Group, 2013). During the first commitment period, the annual average price of crude oil, natural gas and coal has been dropping from $98.69 (per barrel), $8.78 (per MMBTU) and $127.10 (per MT) to $109.39 (per barrel), $2.79 (per MMBTU) and $94.03 (per MT), respectively. A high correlation between fossil fuel rents and fossil fuel prices has significantly caused the income inflows of net energy exporting countries vacillated (reported in Table 1). Further, the energy sustainability and environmental impacts of using fossil fuel have significantly influenced fossil fuel users and energy exporting economies (United Nation, 2005). Therefore, net energy exporting countries are required to gauge the optimal balance (or opportunity costs) between exporting fossil fuel and in-home utilization in electricity generation for the sake of stabilizing their economies.

However, Payne (2010) noticed that the growth hypothesis is usually inapplicable to explain the electricity-growth nexus in net energy exporting countries because of their strong energy security and a significant share of energy exports in GDP Besides, changes in a country's development degree might also influence the electricity-growth nexus in that country since different economic stages require dissimilar policy treatments in electricity generation to support economic developments. Thus, the development trajectory and economic dependence on energy exports of a country are significant criteria for studies on the relationship between energy consumption and economic growth. An attempt to introduce a categorization on the degree of economic development and dependence on energy exports (or fossil fuel rents) is necessary to reduce contradictory results regarding the electricity-growth nexus in the energy exporting economies (Chen et al., 2007; Squalli, 2007; Narayan and Prasad, 2008; Payne, 2010).

According to Tang and Tan (2012; 2013), technological innovation and fossil fuel prices play a significant role in the decision making process of gauging the optimal balance. This is because technological innovation decides the efficiency and sustainability of using a certain type of electricity generating method, such as fossil fuel-fired power plant (Popp, 2001); while energy prices determine the impacts of volatile energy prices on the price of fossil fuel powered electricity (Jamil and Ahmad, 2010). Given the global focus on averting the tragedy of the commons, technological innovation can also serve as a driver of energy-saving technologies (Tang and Tan, 2013), or an alternative measure to reduce a country's reliance on fossil fuel powered electricity (Popp, 2001), in the contemporary context. Hence, without considering the impacts of technological innovations and energy prices on the electricity-growth nexus, policy makers are unlikely to make a sound conclusion regarding the feasibility of implementing energy conservation policies in fossil fuel powered electricity generation.

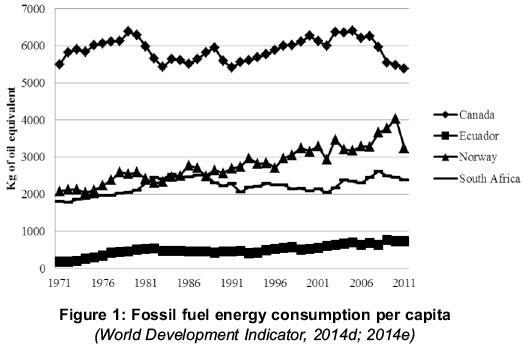

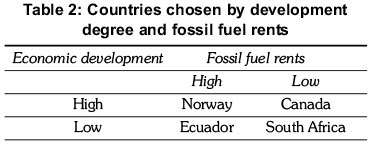

Since numerous studies have concluded the effect of economic development and fossil fuel rents on the electricity-growth nexus (Payne, 2010) and the energy-growth nexus (Ozturk, 2010), we have chosen four countries to incorporate these impacts into the examination of the nexus of fossil fuel powered electricity consumption, economic growth, relative prices of fossil fuel to non-energy goods and technological innovation in net energy exporting countries. Canada and Norway represent developed economies, while Ecuador and South Africa represent developing economies. In addition, Canada and South Africa depend little on energy exports, while Norway and Ecuador are more economically dependent on energy exports (reported in Table 1). Besides, one unique characteristic for the high dependence group is that they have experienced a persistent increasing trend in the fossil fuel energy consumption over 1971 to 2011 (as shown in Figure 1). Table 2 categorizes these countries into a matrix following their respective economic development degree and fossil fuel rents. Worth to mention, both Norway and Canada have introduced explicit energy conservation policies, which are Green Paper and energy efficiency regulations, to curb excessive electricity consumption.

This study aims at providing two main contributions to the energy literature. First, this paper deploys the Granger causality test under the error correction model to extend the evaluation of the electricity-growth nexus for four net energy exporting countries. Following the matrix that categorizes these countries according to their respective economic development and fossil fuel rents, the causality result will be constructive to determine the statistical magnitude of economic development and fossil fuel rents in the electricity-growth nexus. Second, instead of using total electricity consumption like the majority of the previous researches, this paper employs fossil fuel powered electricity consumption to investigate the necessity of using fossil fuel powered electricity that could endanger the environment. Last, the advancement in technology could result in fossil fuel powered electricity being substituted by other sources to combat the emission issue, or being improved to minimize social costs.

Primarily, this paper targets to examine the direction of causality and both the short-run and long-run relationships between fossil fuel powered electricity consumption, economic growth, relative prices of fossil fuel to non-energy goods and technological innovation for four net energy exporting countries following the preceding matrix. In light of the Kyoto Agreement, global shrinkage in the use of fossil fuel may increase the impact of economic growth on fossil fuel powered electricity consumption to countries with high fossil fuel rents. The reason is that they would convert their energy exports into in-home utilization in commensurate with the variation in international prices. Since the initiatives to combat climatic changes are a global action, a number of developing countries have also embarked to use the energy efficiency practice to control the repercussion of economic growth on the environment (Bildirici and Kayikci, 2012; UNIDO, 2011). If fossil fuel powered electricity consumption positively influences economic growth, an energy conservation policy could only protect the environment at the expenses of economic growth.

The rest of the paper is organized as follows: Section 2 reviews those past studies that have examined the electricity-growth nexus. Section 3 presents the research methodology. Section 4 discusses the results. The final section concludes this study with a summary of the main findings, and with several implications of this study to theoretical contribution and policy making.

2. Literature review

Following the seminal work of Kraft and Kraft (1978), the energy-growth nexus has been studied extensively by many scholars (e.g. Erol and Yu, 1987; Hwang and Gum, 1991; Cheng and Lai, 1997; Soytas and Sari, 2003; Lee and Chang, 2008; Tang and Shahbaz, 2013). The massive accumulation of studies analysing the energy-growth nexus without a substantive consensus has led to a shift from explaining this traditional nexus to generalize the nexus's fundamentals to the scope of electricity consumption (Ozturk, 2010).

According to the literature survey of Payne (2010), empirical results of the electricity-growth nexus can be categorized into four general stances following the direction of causality between electricity consumption and economic growth. First, the electricity-led-growth stance suggests that a laissez-faire approach of expanding electricity is benign to economic growth since electricity consumption oneway Granger causes economic growth. Second, the economy-driven-consumption stance proposes an expansion in economic development unidirectionally elevates the electricity consumption degree. Third, the bidirectional stance postulates that the reciprocal relationship between electricity consumption and economic growth simultaneously interlocks the causal link between electricity consumption and economic growth. Last, the neutrality stance surmises that there is no causality between electricity consumption and economic growth. In short, the direction of causality determines the weight of the pros and cons of implementing electricity conservation policies.

Murry and Nan (1996) investigated the electricity-growth nexus for 23 countries over the period 1970-1990 by deploying the Granger causality test within the vector autoregressive (VAR) model. Their results showed that electricity consumption Granger causes economic growth in Canada, while this relationship is not evident in Norway. However, a subsequent study by Narayan and Prasad (2008) revealed that this relationship does not exist in both Canada and Norway once the research time span had been extended from 1960-2002. Similarly, a following study by Bildirici et al. (2012) suggested that congruence in results could be not archived in Canada via using the autoregressive distributed lag (ARDL) model to investigate the electricity-growth nexus in Canada over the period from 1978 to 2010. Their results suggested a unidirectional Granger causality running from electricity consumption to economic growth, which contradicts the results of Narayan and Prasad (2008). Although all of these studies were adopting the Granger causality test to observe the direction of causality, different model specifications (e.g. VAR and ARDL) and research time spans yielded dissimilar results with the passage of time.

An inconsistency in the results of the nexus is not only limited to Canada, but also present in Ecuador and South Africa. According to the panel study of Mehrara (2007), there is a strong unidirectional Granger causality from economic growth to electricity consumption in 11 oil exporting countries, inclusive of Ecuador, over the period from 1971 to 2002. However, Yoo and Kwak (2010) reported an opposite result against the findings of Mehrara (2007) for Ecuador, for the reason that a panel study may only recapitulate the brief symptom of a region. Yoo and Kwak (2010) found electricity consumption Granger causes economic growth in Ecuador over the period 1975-2006, using the Hsiao version of the standard Granger causality test. Apergis and Payne (2011) also reported a unidirectional Granger causality from electricity consumption to economic growth for the panel of lower-middle income countries, inclusive of Ecuador.

Moreover, employing the Toda-Yamamoto causality test, Wolde-Rufael (2006) concluded that the electricity-growth nexus is not significant in South Africa over the period from 1971 to 2001. Wolde-Rufael's (2006) findings were dismissed by a chronologically later study from Squalli (2007), which found a significant effect of electricity consumption on economic growth in South Africa. In the panel study of Apergis and Payne (2011), they documented a bidirectional relationship between electricity consumption and economic growth in South Africa. The only exception to inconsistent results is that the neutrality in the electricity-growth nexus in Norway has been consistent across different time spans and methodologies (Murry and Nan, 1996; Narayan and Prasad, 2008).

By summarizing 65 studies relating to the electricity-growth nexus, Payne (2010) highlighted that the assessments of the electricity-growth nexus in the past were problematic because of the use of small sample size and mixed integration order in the variable series. He also noticed that a panel study is generally insufficient to capture the inner economic essence of a country, and incapable to reflect that essence in the research output of a panel study. Namely, accurate suggestion to a specific country is unlikely to be yielded from a panel study, even though Narayan et al. (2010) found the globe generally expresses a bidirectional relationship between electricity consumption and economic growth in their global panel study. Therefore, instead of simply extending the research by stretching the research time span, Payne (2010) suggested that a significant progress in dissecting the nexus, and in minimizing the omitted-variable bias, may be achieved by incorporating new endogenous (or exogenous) variables to depict a clearer picture of the relationship between electricity consumption and economic growth.

The contradictory evidences from those past studies support Payne's (2010) and Ozturk's (2010) call to search a new way of structuring the research framework of the nexus. They suggested that using better methodologies and more explanatory variables may obtain a more robust result than those incongruent past studies. This study seeks to stretch the boundaries of previous researches to test the relationship between electricity consumption and economic growth, using the additional variable of technological innovation attempted by Tang and Tan (2013), to explain the variation in fossil fuel powered electricity consumption for net energy exporting countries. Additionally, this study categorizes net exporting countries according to their respective economic development and fossil fuel rents in order to determine if economic development and fossil fuel rents matter in the electricity-growth nexus. It is hoped that these paths will yield some valuable insights on the electricity consumption debate (Payne, 2010).

3. Research methodology

The variables used in this paper include per capita fossil fuel powered electricity consumption, per capita real GDP, relative prices of fossil fuel to non-energy goods and the number of patents filed. The research time span of this study is from 1974 to 2011. All secondary data were extracted from World Bank and World Development Indicators.

Although the scale of technological innovation is difficult to estimate, this paper uses the amount of patenting activities as the proxy of technological innovation following the suggestions of several empirical works that have used the number of patents as a measure of technological innovation (e.g. Grupp, 1996; Pavitt, 1985; Patel and Pavitt, 1994; Anderson, 1999; Hall et al., 2001; Dachs et al., 2007; Schmoch, 2007; Chen et al., 2009; Ang, 2010; Jamasb and Pollitt, 2011; Lee and Lee, 2013; Tang and Tan, 2013). This is because the number of patents can be considered as codified interests of innovators in technological progress (Popp, 2005; Duguet and Macgarvie, 2005; Wong and Goh, 2010).

Moreover, this paper uses the relative prices of fossil fuel to non-energy goods as a proxy of energy prices since energy prices in different countries are subject to dissimilar degrees of governmental (e.g. subsidies) and economic (e.g. price disparity) influences. The relative prices of fossil fuel to non-energy goods is superior to the Consumer Price Index in the role of representing energy prices because this proxy deflates international fossil fuel prices by a national deflator, and reflects the real purchasing power of consumers toward fossil fuel in an economy (Tang and Tan, 2012). The relative prices of fossil fuel to non-energy goods are customized in accordance with the historical share of fossil fuel (coal, natural gas and oil) in total electricity production for each country. Hence, adopting the relative prices of fossil fuel price to non-energy goods minimizes the error of using a standardized proxy and raises the reliability of the proxy in capturing the impact of energy prices on electricity consumption (Tang and Tan, 2012; Tang et al., 2013).

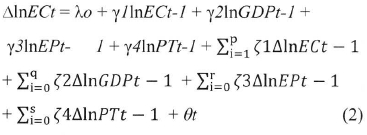

This paper indirectly adapts the model specification from Tang and Tan (2013). Two modifications are applied to the original model of Tang and Tan (2013), in which this paper replaces the indirect measure of energy prices (CPI) by the relative prices of fossil fuel to non-energy goods and substitutes the variable of total electricity consumption by fossil fuel powered electricity consumption. The relationship between fossil fuel powered electricity consumption, energy prices, economic growth and technological innovation is expressed as follows:

where In denotes the natural logarithm, ECt is per capita fossil fuel powered electricity consumption (kg of oil equivalent), GDPt is per capita real gross domestic product (in domestic currency), EPt is the relative prices of fossil fuel to non-energy goods (average fossil fuel prices adjusted by national deflator) and PTt is the number of patents filed by a country. The error term □t is assumed to be normally distributed and homoscedastic. Based on the previous studies, the expected signs for the coefficient of economic growth, energy price and technological innovation are □1 > 0, □2 < 0, and □3 < 0, respective bely. This is because economic growth is triggered by the prosperity of economic activities, where these economic activities are consuming electricity (Payne, 2010). Further, an increase in electricity price will lower the demand for electricity consumption, ceteris paribus (Jamil and Ahmad, 2010). Lastly, technological innovation may contribute to the development of energy-saving technologies (Popp, 2001) and better fuel efficiency (DECC, 2012).

3.1 Unit root tests

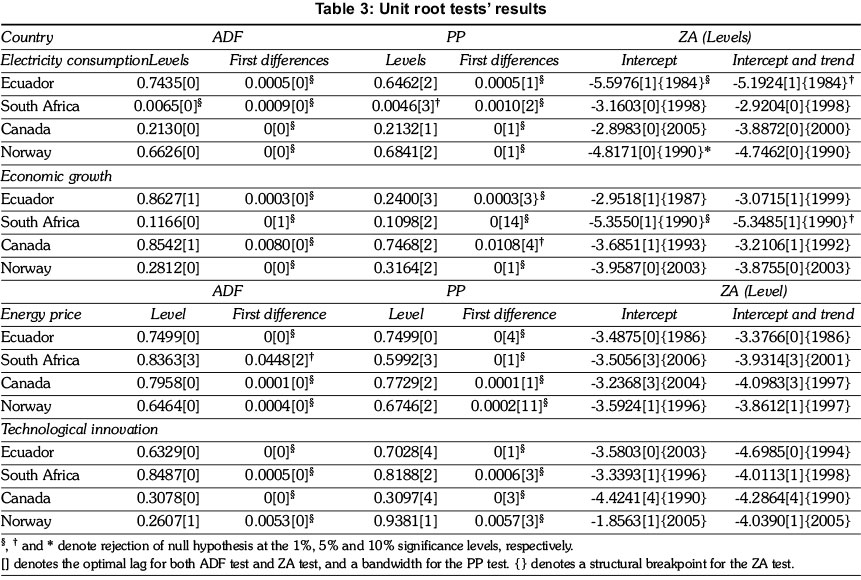

According to Granger and Newbold (1974) and Phillips (1986), a time-series model may produce invalid estimates if the stochastic process is non-stationary. Since the existence of cointegration among the variables is an essential prerequisite for the Granger causality test (Masih and Masih, 1998), applying a stationarity test prior to the cointegration test prevents this research from adopting a wrong cointegration approach in testing the causal relationship between the variables (Granger and Newbold, 1974; Engle and Granger, 1987). Thus, to minimize the possibility of yielding a spurious relationship, this paper provides a preliminary view of the stationarity properties of the variables before embarking on the cointegration approach or causality test.

Prior to the cointegration test, we employ the Augmented Dickey Fuller (ADF, Dickey and Fuller, 1979) and Phillips Perron (PP, Phillips and Perron, 1988) unit root tests to ascertain the order of integration of each series. However, Perron (1997) and Bai and Perron (1998) found the presence of structural breaks within a data series might make traditional standard unit root tests less effective in examining the stationarity properties of data series. Thus, in addition to the Augmented Dickey-Fuller and Phillips Perron unit root tests, this paper also applies the Zivot-Andrews (ZA, Zivot and Andrews, 1992) unit root test with one structural break to confirm the order of integration of each series because traditional unit root tests may be inappropriate when a series contains structural breaks.

This study adopts the Akaike Information Criterion with a maximum lag of 6 lags as the basis for selecting the amount of lagged terms for the Augmented Dicket Fuller and Zivot-Andrews unit root tests. The bandwidth of the Phillips Perron test is chosen on the basis of the Newey and West data-based automatic bandwidth parameter method. The null hypothesis of these unit root tests assumes a unit root in the data series examined. Rejecting the unit root test's null hypothesis is necessary to further the research process of this study. Simultaneously examining the stationarity properties of both the level and first difference data series provides this study the integration order among all data series. This information gauges the appropriateness of using traditional cointegration approaches.

3.2 Autoregressive distributed lag (ARDL) model to cointegration

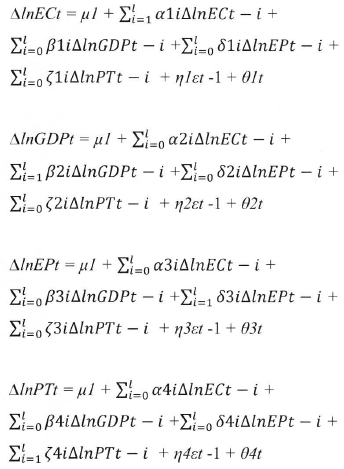

Following the assessment of data series' stationarity, we apply the ARDL bounds testing approach to test the presence of cointegration among electricity consumption, energy prices, economic growth and technological innovation for Canada, Ecuador, Norway and South Africa. Although several approaches exist for testing the presence of cointegration among the variables, the ARDL model is considered to be the best approach for this purpose (Pesaran and Shin, 1999; Pesaran et al., 2001). This is because the Engle and Granger (1987), Johansen (1988) and Phillips and Hansen tests (1990) are subject to the constraint of first difference integration order. When the integration order among the variables is mixed among I(0) and I(I), these cointegration tests might yield unreliable results. However, the ARDL bounds testing approach is flexible to test for the presence of coin-tegration among the variables regardless of I(0), I(1) or I(0)/I(1). Besides, the ARDL model yields a consistent output even if the sample size is small. This is because this model effectively corrects for the endogeniety problem among the explanatory variables and the estimates derived from the approach (Narayan, 2005; Emran, et al., 2007). Hence, we apply the ARDL model over the other approaches to test for the presence of cointegration among electricity consumption, energy price, economic growth and technological innovation. The ARDL model is expressed as follows:

where ∆ denotes the first difference and  is the residual terms of the relationship. The Akaike Information Criterion (AIC) is applied to select an appropriate minimum lag length to test the cointegration property because the Bayesian Information Criterion is too parsimonious for a small sample size (Liew, 2004). Since the F-statistics is susceptible to the lag order selection, an inappropriate lag length selection may create a research output error. Pesaran et al. (2001) generated two sets of asymptotic critical values, which are an upper critical bound and a lower critical bound, to evaluate whether cointegration exists between two or more series. There is a long run relationship between the variables if the calculated F-statistics is greater than the upper critical bound. If the calculated F-statistics is lower than the lower critical bound or is in between the bounds, there is no cointegration among the variables. If all variables are cointegrated, the error correction model is an appropriate method to investigate the long run equilibrium among the variables. This paper adopts the list of critical bounds generated by Narayan (2005) to test for the presence of cointegration among the variables.

is the residual terms of the relationship. The Akaike Information Criterion (AIC) is applied to select an appropriate minimum lag length to test the cointegration property because the Bayesian Information Criterion is too parsimonious for a small sample size (Liew, 2004). Since the F-statistics is susceptible to the lag order selection, an inappropriate lag length selection may create a research output error. Pesaran et al. (2001) generated two sets of asymptotic critical values, which are an upper critical bound and a lower critical bound, to evaluate whether cointegration exists between two or more series. There is a long run relationship between the variables if the calculated F-statistics is greater than the upper critical bound. If the calculated F-statistics is lower than the lower critical bound or is in between the bounds, there is no cointegration among the variables. If all variables are cointegrated, the error correction model is an appropriate method to investigate the long run equilibrium among the variables. This paper adopts the list of critical bounds generated by Narayan (2005) to test for the presence of cointegration among the variables.

3.3 Granger causality test

When two variables are cointegrated, these variables will converge into a long run equilibrium which mechanistically prevents these cointegrated variables drifting away from each other in the long run (Engle and Granger, 1987). According to Granger (1969; 1988) and Enders (1995), the Granger causality test is the best fitted model to investigate the causal relationship between two variables by including the lagged terms of both variables to explain the variation in the dependent variable. If the inclusion of lagged observations does significantly explain the variation in the dependent variable, the explanatory variable is said to Granger cause the response variable. Engle and Granger (1987) emphasized that two cointegrated time series will at least yield a unidirectional Granger causality from one variable to another variable.

To examine the direction of causality between the variables, the Granger causality test is used to investigate the relationship between electricity consumption, economic growth, energy prices and technology innovation for Canada, Ecuador, Norway and South Africa. The Granger causality test is performed within the following vector error correction model (VECM):

where ∆ is the first difference operator and l is the optimal lag order determined by the AIC. The error terms ( 1t,

1t,  2t,

2t,  3t,

3t,  4t) are assumed to be normally distributed and homoscedastic. The t-statistics of the estimate of lagged error term, e.g. η1ετ-1, with negative sign is used to test the convergence speed of the relationship against the long run equilibrium. The F-statistics of first difference lagged independent variables is used to investigate the short run causality between the variables under the examination of Wald test. The explanatory variables are said to Granger cause fossil fuel powered electricity consumption, only if β1i, δ1i and ζ1i are significantly different from zero, et cetera. If the variables are not cointegrated, a first difference vector autoregressive model will be adopted to test for the short-run Granger causality between electricity consumption, economic growth, energy prices and technological innovation (Lutkepohl, 1991).

4t) are assumed to be normally distributed and homoscedastic. The t-statistics of the estimate of lagged error term, e.g. η1ετ-1, with negative sign is used to test the convergence speed of the relationship against the long run equilibrium. The F-statistics of first difference lagged independent variables is used to investigate the short run causality between the variables under the examination of Wald test. The explanatory variables are said to Granger cause fossil fuel powered electricity consumption, only if β1i, δ1i and ζ1i are significantly different from zero, et cetera. If the variables are not cointegrated, a first difference vector autoregressive model will be adopted to test for the short-run Granger causality between electricity consumption, economic growth, energy prices and technological innovation (Lutkepohl, 1991).

4. Findings and discussion

As shown in Table 3, the results of the unit roots test consistently reveal that all variables are stationary at first difference with the only exception that electricity consumption is stationary at level in South Africa. By incorporating the presence of a structural break into the unit root test, the results of the Zivot-Andrews test indicate that few data series are also stationary at level. This finding is consistent with the claim that most of the macroeconomic variables are stationary at first difference, although some could also be stationary at level (Perron, 1989). Worth to mention, the presence of structural break amplifies the stationarity issue for South Africa and Ecuador. This is because developing countries are more likely to experience structural economic changes than developed economies. Since all variables are not purely integrated of order one, the Johansen (1988) and Engle and Granger (1987) cointegration tests may be less useful to investigate the presence of cointegration among the variables. Besides, the small sample size of this paper might yield a less consistent result in the traditional cointegration tests. Owing to these reasons, this paper adopts the ARDL approach to cointegration to investigate the presence of long run relationship between the variables.

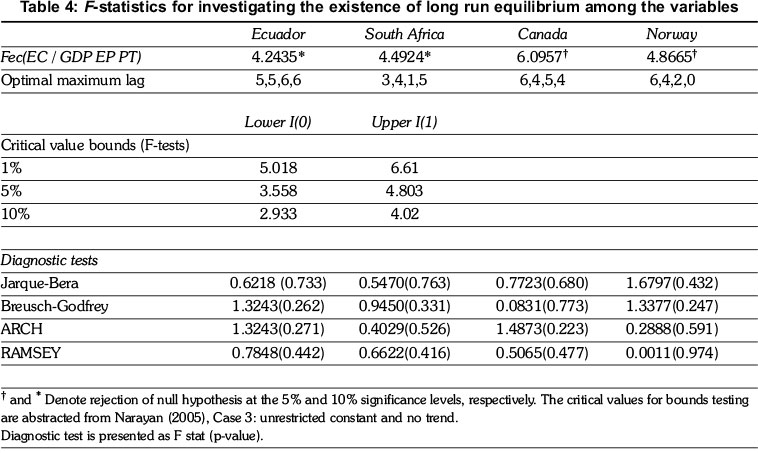

As mentioned earlier, the ARDL approach to cointegration is suitable to investigate the presence of cointegration among the variables when the sample size is small, and when the variables are subject to the issue of I(1)/I(0). Hence, this model is appropriate for this study since the sample size only consists of 38 observations for each variable, and because those variables have possible mixed integration orders below I(2). The F-statistic for the ARDL bounds testing approach and the diagnostic test results are reported in Table 4.

Statistically, a long run equilibrium among the variables is only present when the calculated F-statistic for the bounds test is greater than the upper bound I(1) critical value (Narayan, 2005). The results of Equation (2) suggest that there is a long run relationship between fossil fuel powered electricity consumption, economic growth, relative prices of fossil fuel to non-energy goods and technological innovation for Ecuador, South Africa, Canada and Norway. The model specification for Ecuador and South Africa, i.e. Fec(EC / GDP EP PT), is significant at the 10% significance level, while the same model specification for Norway and Canada is significant at the 5% significance level. The findings suggest that energy prices, economic growth and technological innovation are associated with fossil fuel powered electricity consumption in the long run. Besides, the results also show that the model specification is correct as the presence of cointegration is observed in all the examined countries (Perman, 1991). Hence, the null hypothesis of no cointegration can be rejected.

The Jarque-Bera statistics show that the residuals of the model are normally distributed (see Table 4). In addition, the results of the Breush-Godfrey and ARCH LM tests indicate that those errors terms are free from the issues of serial correlation and heteroscedasticity. Furthermore, the Ramsey RESET test's results show that the model is correctly specified as a linear regression since the null hypothesis of the Ramsey RESET cannot be rejected even at the 10% significance level. Hence, based on these diagnostic tests' results, the ARDL model is unlikely to be affected by any known spurious effect on regression over the sample period from 1974 to 2011.

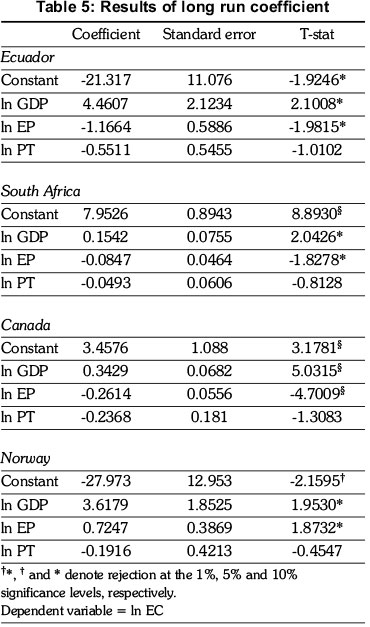

Since the presence of cointegration among the variables is confirmed, an estimation of the long run coefficients from the ARDL model is necessary for observing the long run behaviour of the determinants of fossil fuel powered electricity consumption. Table 5 presents the results of the long run coefficient of fossil fuel powered electricity consumption using the ARDL model.

Three unique trends are evident from the results. First, the endogenous growth theory may be inapplicable to the electricity-growth nexus in the fossil fuel powered electricity generation sector. Although technological innovation may have raised the efficiency of overall electricity generation in Malaysia (a net energy exporting country) as suggested by Tang and Tan (2013), it does not show any long-run relationship with the use of fossil fuel in electricity generation for all net energy exporting countries documented in this study. According to World Development Indicator (2014f), the globe, especially developed economies, has been progressively shifting from fossil fuel-fired plant to alternative electricity generation methods (e.g. wind, hydro and etc. ) even though fossil fuel is the cheapest solution to generate electricity. Thus, a progressive shift from the use of fossil fuel to alternative energy (e.g. hydro, wind and etc.) in electricity generation contributes to the divergence in results (Sagar and Holdren, 2002; U.S. EIA, 2011; Wonglimpiyarat, 2010).

Another feasible reason for the insignificance of technological innovation on electricity consumption is that fossil fuel powered electricity consumption has been gradually falling in developed economies over the past few decades, due to the advocacy of environmental protection (Lee and Lee, 2013).

According to Javorcik et al. (2004) and Herzer (2012), there are several economic and development channelling transferring innovation resources from developed economies to developing economies, such as foreign direct investments and technological aids. As developing countries usually absorb technological innovation from developed countries, developing countries would inevitably mimic the technological orientation of developed countries with similar economic characteristics. Thus, developing economies could experience structural changes in electricity generating methods from developed countries due to the spill over effect of technology and environmentally friendly approaches (Herzer, 2012). As a result, the voice of reducing energy-related CO2 emissions, and transforming non-renewable energy into alternative energy, has caused traditional fossil fuel powered electricity to be isolated from the contribution of technological advancement to electricity generation (Ediger and Kentel, 1999; Apergis and Payne, 2014).

Second, the degree of dependence on energy exporting activities does justify the magnitude of economic growth to fossil fuel powered electricity consumption. Norway and Ecuador, which have higher fossil fuel rents than Canada and South Africa, have presented a stronger impact of economic growth on fossil fuel powered electricity consumption than Canada and South Africa. This result explains the reason that Norway (2.2%) and Ecuador (4.2%) have a higher average increment in CO2 emissions from electricity and heat production than Canada (-0.2%) and South Africa (0.55%) over the base year (1990) to the implementation period (up to 2011) of the Kyoto Agreement (World Development Indicator, 2014g). In brief, the results indicate that Norway and Ecuador have used in-home utilization to buffer the side effect of their high economic dependence on fossil fuel exports at the expenses of environmental quality.

Last, the consistency in results also offers some insights to understand the electricity-growth nexus in net energy exporting economies. The economy-driven-electricity stance (or the conservation hypothesis) holds true for all net energy exporting countries documented in this study. This is because net energy exporting countries are not subject to the problems of unstable energy supply and energy insecurity. This crucial characteristic distinguishes an energy exporting country from the other energy importing countries in the electricity-growth nexus (Mehrara, 2007). Besides, energy prices have been a significant explanatory variable to economic growth for Ecuador, South Africa and Canada as an increase in fossil fuel prices lower fossil fuel powered electricity consumption in the long run (see also Tang and Tan, 2012; Tang et al. , 2013). Over the period 1974-2011, the average share of fossil fuel powered electricity in total consumption for Ecuador, South Africa, Canada and Norway was 42.2%, 95.1%, 23.2% and 0.5%, respectively. The unusual price-demand association in Norway could be a result of the extremely low consumption of fossil fuel powered electricity in its overall economy.

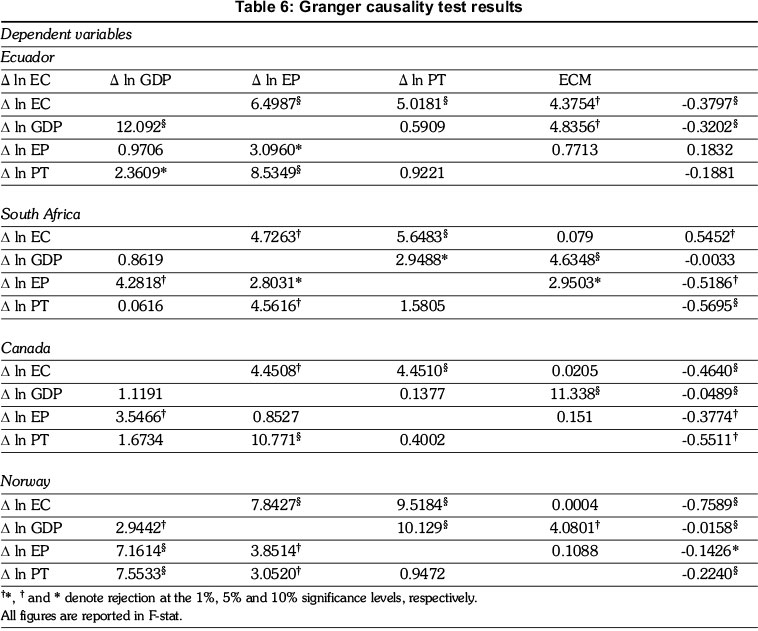

Overall, the diagnostic tests confirm that the ARDL approach to cointegration is correctly specified to identify the cointegration features among the variables. Fossil fuel powered electricity consumption has a long run relationship with energy prices, economic growth and technological innovation in all four energy exporting countries. Since all variables are cointegrated, the short run Granger causality test shall be conducted within the vector error correction model to avoid the issue of output error (Granger, 1988). The results of the short-run Granger causality test using the error correction model are presented in Table 6.

The results of Table 6 show that there is slight incongruence between the long run equilibrium and the short run relationship. For instance, technological innovation has no long run relationship with the fossil fuel powered electricity consumption level in all countries, but the short run causal relationship is limited to Ecuador. Apart from this slight divergence, the short-run dynamic relationships between the variables fully corroborate the findings of long run coefficients. The distinctive characteristic of energy exporting economies is more significant in the short-run dynamics between the variables. Additional four observations can be deduced from the Granger causality test's results.

First, the bidirectional relationship between fossil fuel powered electricity consumption and economic growth only presents itself in Ecuador and Norway, which are the group with high economic dependence on energy exports. Second, electricity consumption has a bidirectional relationship with energy prices in all examined energy exporting countries, except Ecuador which only has a unidirectional causality from energy prices to electricity consumption. This finding is consistent with the studies on Pakistan (Jamil and Ahmad, 2010), Malaysia (Bekhet and Othman, 2011), Romania (Bianco et al., 2010), United States (Harris and Lon-Mu, 1993), Cyprus (Egelioglu et al., 2001), and Sri Lanka (Amarawickrama and Hunt, 2008). Third, technological innovation is bilaterally tied to economic growth in all countries, in which this finding supports the endogenous growth theory (Schumpeter, 1943; Solow, 1956, Romer, 1990). Last, all error correction terms of the model specification, i.e. Fec (EC □ GDP EP PT), are significant at either the 1% or the 5% significance level with negative signs. The results show that any past year disequilibrium triggered by temporary shocks will be gradually resolved in the following years. Although the speed of adjustment is mediocre, the long-run equilibrium among the variables has persisted over the period from 1974 to 2011.

The short-run results of the Granger causality test reveal that temporary friction of the equilibrium can be lasting for around 1 to 5 years. Further, the Granger causality from economic growth and energy prices to fossil fuel powered electricity consumption suggests that temporary adjustments in economic productions may transiently spur the use of fossil fuel powered electricity consumption in all net energy exporting countries (Payne, 2010). This is because fossil fuel powered electricity is the cheapest method of generating electricity so it could be more flexibly adjusted than other electricity sources to match the invisible hand of the market (Nathan, 2007). The long run convergence and bidirectional relationships between fossil fuel powered electricity consumption and fossil fuel price corroborate the theory of consumer behaviour in Canada, Norway and South Africa. Instead, Ecuador follows a price-led electricity consumption pattern. However, the inverse relationship between prices and demands does not hold true in Norway since fossil fuel powered electricity is insignificant in the composition of Norwegian total electricity consumption. In general, these findings are adequate for policy makers to decide which part of economic planning they should focus on.

5. Conclusions and recommendations

This paper examines both the short-run and longrun relationships between fossil fuel powered electricity consumption, economic growth, relative prices of fossil fuel to non-energy goods and technological innovation for Ecuador, Canada, Norway and South Africa. The traditional Augmented Dickey Fuller and Phillips Perron tests are supplemented with the Zivot-Andrew test to account for the presence of one structural break within the data series. The ARDL bounds testing approach to cointegration is applied to surmount the problems of small sample size and I(0)/I(1). Since the model specification, i.e. Fec(EC / GDP EP PT), is significant in the bounds test for all examined countries, the vector error correction model is applied to investigate the short-run Granger causality between the variables over the period from 1974 to 2011.

The results indicate that there is cointegration among the variables, while fossil fuel powered electricity consumption exhibits a long run equilibrium relationship from the functions of economic growth, energy prices and technological innovation for Ecuador, Canada, Norway and South Africa. Although Tang and Tan (2013) reported that technological innovation could contribute to the development of energy efficiency, this study suggests the contribution of technological innovation may not be generalised on the fossil fuel powered electricity generation sector in the net energy exporting economic context. This is because efficiency improvements in fossil fuel-related electricity production have been stagnant since the 1990s (IEA, 2008). Due to cost concerns and physical conversion limits of transforming sources (e.g. coal) to electricity, the majority of the countries have experienced an improvement in energy efficiency in the fossil fuel areas regardless of their economic development levels. One of the significant examples is that using waste-fired plant and fossil fuel with better quality will impair the cost saving advantage of using fossil fuel in electricity generation (Bellman et al., 2007). Thus, four net energy exporting countries documented in this study did not value the potential saving from improvements in efficiency despite the fact that improving efficiency of fossil fuel may reduce their opportunity costs of exporting fossil fuel.

In summary, Ecuador, Canada, Norway and South Africa share a similar long run nexus between fossil fuel powered electricity consumption, economic growth, energy prices and technological innovation. The matrix derived on the basis of fossil fuel rents and economic development provides this paper some conveniences in addressing further specificities in the electricity-growth nexus. In the narrow sense, the proposed matrix does assist this study in understanding the variation in the electricity-growth nexus. Instead of economic development, the characteristic of economic dependence on energy exports plays a vibrant role in determining the magnitude of economic growth to fossil fuel powered electricity consumption. Further, a bidirectional causal relationship between electricity consumption and economic growth is only limited to the high dependence group, which is inclusive of Norway and Ecuador. Thus, the economic dilemma between fossil fuel rents and in-home utilization has caused serious CO2 emissions issues in Norway and Ecuador.

Broadly speaking, the net energy exporting characteristic justifies the general uniformity of the nexus across all four net energy exporting countries. Besides, there is Granger causality, as well as a long-run impact, running from economic growth to fossil fuel powered electricity consumption in Canada, Ecuador, Norway and South Africa. The share of fossil fuel in total electricity consumption does not influence the direction of causality between electricity consumption and economic growth. This result is consistent with the findings of Mehrara (2007) in dissecting the electricity-growth nexus for 11 oil exporting countries. Namely, energy exporting countries are generally presenting at least a unidirectional causality from economic growth to electricity consumption, even in the fossil fuel powered electricity generation sector. Instead of merely revisiting the electricity-growth nexus in the context of net energy exporting countries, the results suggest a need to overhaul past arguments regarding the causality between electricity consumption and economic growth.

Since the use of fossil fuel powered electricity is a certain output of economic expansion, economic pressure disallows Ecuador and Norway, which have experienced recursive Granger causality from electricity consumption to growth, to simply alter the supply of fossil fuel powered electricity. Although some might suggest the energy insecurity issue considerably impacts the production input aspect of energy importing countries, the repercussion of volatile fossil fuel prices also brings an equal impulse to the national income aspect of energy exporting countries. Poor innovation in the use of fossil fuel in electricity generation might encourage these countries to use fossil fuel as a cheap expendable buffer in the meantime of developing alternative sources for electricity generation. One suggestion for this issue is that Ecuador and Norway, as well as Canada and South Africa, should reconsider the development of fossil fuel-related electricity generation methods to optimize the efficiency of translating fossil fuel into electricity without compromising the environmental quality.

In comparison with global subsidies to renewable energy ($57 billion in 2009), the common approach of subsidizing fossil fuel-associated companies ($312 billion), exclusive of fossil fuel-fired plants, among energy exporting countries should be reformulated to discourage the use of fossil fuel in electricity production for Canada and South Africa. This is because these two countries do not experience any Granger causality from electricity consumption to economic growth. Suggestively, Canada and South Africa could use the open market mechanism to gradually adjust the demand and supply for fossil fuel powered electricity consumption. To be specific, the findings support several important aspects of the Integrated Resource Plan for electricity in South Africa. For example, the aforementioned open market mechanism and decrease in the use of fossil fuel are consistent with the introductions of Independent System and Market Operator Bill (DOE, 2011a) and Electricity Regulation Act No. 4 (DOE, 2011b), which attempt to improve the available coverage of electricity supply via replacing fossil fuel with sustainable sources in the electricity generation process.

According to EPRI (2010), the cost efficiency (ZAR/kW) of building a coal powered plant (e.g. 16,880 ZAR/kW) and a wind farm (e.g. 16,930 ZAR/kW) is almost identical. The sole reason for building a coal powered plant is that there are available technologies requiring lower subsequent expenses to sustain the electricity generation process. However, our findings indicate that fossil fuel powered electricity consumption has been neither benefited nor affected by the advancement in technology over the past few decades. Hence, South Africa, as well as Canada, is at the threshold of choosing either efficiency improvement or environmental friendliness. Selecting either choice is less likely to lead to an expansion in fossil fuel powered electricity production. Therefore, transferring short-term subsidies to long-term development seems to be a more sustainable utility policy to comprehensively take care of different dimensions of using fossil fuel in electricity generation, although this policy might cost the re-election chance of the current ruling party.

Following the global trend of developing sustainable energy (IEA, 2007; REN 21, 2013), greening policies should be encouraged to extend the environment's life span if the use of sustainable energy does not downgrade the living standards of these countries, either explicitly or implicitly.

References

Amarawickrama, H.A. and Hunt, L.C. (2008). Electricity demand for Sri Lanka: a time series analysis. Energy 33(5): 724-739. [ Links ]

Anderson, B. (1999). The hunt for S-curve growth paths in technological innovation: A Patent Study. Journal of Evolutionary Economics 9(4): 487-526. [ Links ]

Ang, J.B. (2010). Research, technological change and financial liberalisation in South Korea. Journal of Macroeconomics 32(1): 457-468. [ Links ]

Apergis, N. and Payne, J.E. (2011). A dynamic panel study of economic development and the electricity consumption-growth nexus. Energy Economics 33(5): 770-781. [ Links ]

Apergis, N. and Payne, J.E. (2014). Renewable energy, output, CO2 emissions and fossil fuel prices in Central America: Evidence from a nonlinear panel smooth transition vector error correction model. Energy Economics 42: 226-232. [ Links ]

Bai, J. and Perron, P (1998). Estimating and testing linear models with multiple structural changes. Econometrica 66(1): 47-78. [ Links ]

Bekhet, H.A. and Othman, N.S. (2011). Causality analysis among electricity consumption, consumer expenditure, gross domestic product (GDP), and foreign direct investment (FDI): case study of Malaysia. Journal of Economics and International Finance 3(4): 228-235. [ Links ]

Bellman, D.K., Blankenship, B.D., Imhoff, C.H., DiPietro, J.P, Rederstorff, B. and Zheng, X.J. (2007). Power plant efficiency outlook. NPC Global Oil & Gas Study: Working Document. [ Links ]

Bianco, V., Manca, O., Nardini, S. and Minea, A.A. (2010). Analysis and forecasting of non-residential electricity consumption in Romania. Applied Energy 87(11): 3584-3590. [ Links ]

Bildirici, M.E. and Kayikci, F (2012). Economic growth and electricity consumption in emerging countries of Europa: An ARDL analysis. Economic Research 25(3): 538-559. [ Links ]

Bildirici, M.E., Bakirtas, T. and Kayikci, F (2012). Economic growth and electricity consumption: Auto regressive distributed lag analysis. Journal of Energy in Southern Africa 23(4): 29-45. [ Links ]

Chen, S.T., Kuo, H.I. and Chen, C.C. (2007). The relationship between GDP and electricity consumption in 10 Asian countries. Energy Policy 35(4): 2611-2621. [ Links ]

Chen, Y., Yang, X., Shu, F, Hu, Z., Meyer, M. and Bhattacharya, S. (2009). A patent based evaluation of technological innovation capability in eight economic regions in PR China. World Patent Information 31(2): 104-110. [ Links ]

Cheng, B.S. and Lai, T.W. (1997). An investigation of co-integration and causality between energy consumption and economic activity in Taiwan. Energy Economics 19(4): 435-444. [ Links ]

Dachs, B., Mahlich, J.C. and Zahradnik, G. (2007). The technological competencies of Korea's firms: A patent analysis. Innovation and Technology in Korea: 127-146. [ Links ]

DECC (2012). The energy efficiency strategy: The energy efficiency opportunity in the UK. Available from URL: https://www.gov.uk/government/uploads/sys-tem/uploads/attachment_data/file/65602/6927-energy-efficiency-strategy-the-energy-efficiency.pdf. [ Links ]

Dickey, D.A. and Fuller, W.A. (1979). Distribution of the estimators for autoregressive time series with a unit root. Journal of the American Statistical Association 74(366): 427-431. [ Links ]

DOE (2011a). Independent System and Market Operator Bill. Republic of South Africa: Department of Energy. [ Links ]

DOE (2011b). Electricity Regulation Act No. 4 of 2006. Republic of South Africa: Department of Energy. [ Links ]

Duguet, E. and MacGarvie, M. (2005). How well do patent citations measure flows of technology? Evidence from French innovation surveys. Economics of Innovation and New Technology 14(5): 375-393. [ Links ]

Ediger, VS. and Kentel, E. (1999). Renewable energy potential as an alternative to fossil fuels in Turkey. Energy Conversion and Management 40(7): 743-755. [ Links ]

Egelioglu, F., Mohamad, A.A. and Guven, B. (2001). Economic variables and electricity consumption in Northern Cyprus. Energy 26(4): 355-362. [ Links ]

Emran, M.H., Shilip, F. and Alam, M.I. (2007). Economic liberalization and price response of aggregate private investment, time series evidence from India. Canadian Journal of Economics 40(3): 914-934. [ Links ]

Enders, W. (1995). Applied Econometric Time Series. New York: Wiley. [ Links ]

Engle, R.F and Granger, C.W.J. (1987). Co-integration and error correction: representation, estimation, and testing. Econometrica 55(2): 251-276. [ Links ]

Erol, U. and Yu, E.S.H. (1987). On the causal relationship between energy and income for industrialized countries. Journal of Energy Development 13(1): 113-122. [ Links ]

ERPI (2010). Power generation technology data for Integrated Resource Plan of South Africa. Abstracted from URL: http://www.energy.gov.za/IRP/irp%20files/Tech_Data_for_Integ _Plan_of_South_Africa_July_08_2010_Final.pdf. [ Links ]

G20 Research Group (2013). G20 Initiative on rationalizing and phasing out inefficient fossil fuel subsidies: Implementation strategies and timetables, Annex. Available from URL: http://www.eenews.net/assets/2010/06/28/document_cw_03.pdf [ Links ]

Grupp, H. (1996). Spill over effects and the science base of innovations reconsidered: an empirical approach. Journal of Evolutionary Economics 6(2): 175-197. [ Links ]

Granger, C.W.J. (1969). Investigating causal relations by econometric models and cross spectral methods. Econometrica 37(3): 424-438. [ Links ]

Granger, C.W.J. (1988). Some recent development in a concept of causality. Journal of Econometrics 39(1-2): 199-211. [ Links ]

Granger, C.W.J. and Newbold, P. (1974). Spurious regressions in econometrics. Journal of Econometrics 2(2): 111-120. [ Links ]

Hall, B.H., Jaffe, A. and Trajtenberg, M. (2001). Market value and patent citations: A first look. NBER, Available from URL: http://128.118.178.162/eps/dev/papers/0012/0012002.pdf. [ Links ]

Harris, J.L. and Lon-Mu, L. (1993). Dynamic structural analysis and forecasting of residential electricity consumption. International Journal of Forecasting 9(4): 437-455. [ Links ]

Herzer, D. (2012). How does foreign direct investment really affect developing countries' growth? Review of International Economics 20(2): 396 - 414. [ Links ]

Hwang, D. and Gum, B. (1991). The causal relationship between energy and GNP: the case of Taiwan. Journal of Energy Development 16: 219-226. [ Links ]

IEA (2007). Renewables in global energy supply: An IEA fact sheet. Abstracted from URL: http://www.iea.org/publications/freepublications/publication/ renewable_factsheet.pdf [ Links ]

IEA (2008). Energy efficiency indicators for public electricity production from fossil fuels. IEA Information Paper, Abstracted from URL: http://www.iea.org/publications/freepublications/ publication/en_efficiency_indicators.pdf. [ Links ]

IEA (2010). World Energy Outlook 2010. Abstracted from URL: http://www.worldenergyoutlook.org/media/weo2010.pdf. [ Links ]

Jamasb, T. and Pollitt, M.G. (2011). Electricity sector liberalization and innovation: An analysis of the UK's patenting activities. Research Policy 40(2): 209-324. [ Links ]

Jamil, F. and Ahmad, A. (2010). The relationship between electricity consumption, electricity prices and GDP in Pakistan. Energy Policy 38(10): 6016-6025. [ Links ]

Javorcik, B., Saggi, K. and Spatareanu, M. (2004). Does it matter where you come from? Vertical spill overs from foreign direct investment and the nationality of investors. World Bank Policy Research, Working Paper, No. 3449. [ Links ]

Johansen, S. (1988). Statistical analysis of cointegration vectors. Journal of Economics Dynamic Control 12(2-3): 231-254. [ Links ]

Kraft, J. and Kraft, A. (1978). On the relationship between energy and GNP. Journal of Energy and Development 3(2): 401-403. [ Links ]

Lee, C.C. and Chang, C.P (2008). Energy consumption and economic growth in Asian economies: a more comprehensive analysis using panel data. Resource and Energy Economics 30(1): 50-65. [ Links ]

Lee, K. and Lee, S. (2013). Patterns of technological innovation and evolution in the energy sector: A patent-based approach. Energy Policy 59: 415-432. [ Links ]

Liew, V.K.S. (2004). Which lag length selection criteria should we employ? Economics Bulletin 3(3): 1-9. [ Links ]

Lutkepohl, H. (1991). Introduction to Multiple Time Series Analysis. Springer-Verlag. [ Links ]

Masih, A.M.M. and Masih, R.A. (1998). Multivariate cointegrated modelling approach in testing temporal causality between energy consumption, real income and prices with an application to two Asian LDCs. Applied Economics 30(10): 1287-1298. [ Links ]

Mehrara, M. (2007). Energy consumption and economic growth: The case of oil exporting countries. Energy Policy 35(5): 2939-2945. [ Links ]

Murry, D.A. and Nan, G.D. (1996). A definition of the gross domestic product-electrification interrelation-ship. Journal of Energy and Development 19(2): 275-283. [ Links ]

Narayan, PK. (2005). The saving and investment nexus for China: Evidences from cointegration tests. Applied Economics 37(17): 1979-1990. [ Links ]

Narayan, PK. and Prasad, A. (2008). Electricity consumption-real GDP causality nexus: evidence from a bootstrapped causality test for 30 OECD countries. Energy Policy 36(2): 910-918. [ Links ]

Narayana, PK., Narayan, S. and Popp, S. (2010). Does electricity consumption panel Granger cause GDP? A new global evidence. Applied Energy 87(10): 3294-3298. [ Links ]

Nathan, S.L. (2007). Powering the Planet. San Francisco: Materials Research Society Spring Meeting, [ Links ]

Ozturk, I. (2010). A literature survey on energy-growth nexus. Energy Policy 38(1): 340-349. [ Links ]

Pavitt, K. (1985). Patent statistics as indicators of innovative activities: Possibilities and Problems. Scientometrics 7(1-2): 77-99. [ Links ]

Patel, P and Pavitt, K. (1994). The nature and economic importance of national innovation systems. STI Review 14. Paris: OECD. [ Links ]

Payne, J.E. (2010). A survey of the electricity consumption-growth literature. Applied Energy 87(3): 723-731. [ Links ]

Perman, R. (1991). Cointegration: an introduction to the literature. Journal of Economic Studies 18(3): 3-30. [ Links ]

Perron, P. (1997). Further evidence on breaking trend functions in macroeconomic variables. Journal of Econometrics 80(2): 355-385. [ Links ]

Pesaran, M.H. and Shin, Y. (1999). An autoregressive distributed-led modelling approach to cointegration analysis. Cambridge: Cambridge University Press. [ Links ]

Pesaran, M.H., Shin, Y. and Smith, R.J. (2001). Bounds testing approaches to the analysis of level relationships. Journal of Applied Econometrics 16(3): 289-326. [ Links ]

Perron, P. (1989). The great crash, the oil price shock, and the unit root hypothesis. Econometrica 57(6): 1361-1401. [ Links ]

Phillips, P.C.B. (1986). Understanding spurious regressions in econometrics. Journal of Econometrics 33(3): 311-340. [ Links ]

Phillips, PC.D. and Hansen, B.E. 1990. Statistical inference in instrumental variables regression with I(1) process. Review of Economic Studies 57(1): 99-125. [ Links ]

Phillips, P.C.B. and Perron, P. (1988). Testing for a unit root in time series regression. Biometrika 75(2): 335-346. [ Links ]

Popp, D. (2001). The effect of new technology on energy consumption. Resource and Energy Economics 23(3): 215-239. [ Links ]

Popp, D. (2005). Lessons from patents: Using patents to measure technological change in environmental models. Ecological Economics 54(2-3): 209-226. [ Links ]

Romer, P.M. (1990). Endogenous technological change. Journal of Political Economy 98(5): 71-102. [ Links ]

REN 21. (2013). Renewables 2013: Global status report. Abstracted from URL: http://www.ren21.net/portals/0/documents/resources/gsr/2013 /gsr2013_lowres.pdf. [ Links ]

Sagar, A.D. and Holdren, J.P. (2002). Assessing the global energy innovation system: Some key issues. Energy Policy 30(6): 465-469. [ Links ]

Schmoch, U. (2007). Double-boom cycles and the comeback of science-push and market-pull. Research Policy 36(7): 1000-1015. [ Links ]

Schumpeter, J.A. (1943). Capitalism, Socialism and Democracy, London: Allen and Unwin. [ Links ]

Solow, R.M. (1956). The production function and the theory of capital. Review of Economics Studies XXIII: 101-108. [ Links ]

Soytas, U. and Sari, R. (2003). Energy consumption and GDP: causality relationship in G-7 countries and emerging markets. Energy Economics 25(1): 33-37. [ Links ]

Squalli, J. (2007). Electricity consumption and economic growth: bounds and causality analyses of OPEC countries. Energy Economics 29(6): 1192-1205. [ Links ]

Tang, C.T. and Tan, B.W. (2012). The linkages among energy consumption, economic growth, relative price, foreign direct investment and financial development in Malaysia. Quantity and Quality 48(2): 781-797. [ Links ]

Tang, C.T. and Tan, E.C., (2013). Exploring the nexus of electricity consumption, economic growth, energy prices and technology innovation in Malaysia. Applied Energy 104: 297-305. [ Links ]

Tang, C.F. and Shahbaz, M. (2013). Sectoral analysis of the causal relationship between electricity consumption and real output in Pakistan. Energy Policy 60: 885-891. [ Links ]

Tang, C.F., Shahbaz, M. and Arouri, M. (2013). Reinvestigating the electricity consumption and economic growth nexus in Portugal. Energy Policy 62: 1515-1524. [ Links ]

UNIDO (2011). Industrial Energy Efficiency for Sustainable Wealth Creation: Capturing Environmental, Economic and Social Dividends. Industrial Development Report, Vienna: United Nations Industrial Development Organization. [ Links ]

United Nations (2005). Sixth compilation and synthesis of initial national communications from Parties not included in Annex 1 to the Convention. Available from URL: http://unfccc.int/resource/docs/2005/sbi/eng/18.pdf. [ Links ]

U.S. EIA, (2011). Annual Energy Review 2011. DOE/EIA 0384, Abstracted from URL: http://www.eia.gov/totalenergy/data/annual/pdf/aer.pdf [ Links ]

Wolde-Rufael, Y. (2006). Electricity consumption and economic growth: a time series experience for 17 African countries. Energy Policy 34(10): 1106-1114. [ Links ]

Wong, C.Y and Goh, K.L. (2010). Modeling the behavior of science and technology: Self propagating growth in the diffusion process. Scientometrics 84(3): 669-686. [ Links ]

Wonglimpiyarat, J. (2010). Technological change of the energy innovation system: From oil-based to bio-based energy. Applied Energy 87(3): 749-755. [ Links ]

World Development Indicator (2014a). Coal rents (% of GDP). Abstracted from URL: http://data.worldbank.org/indicator/NY.GDPCOAL.RT.ZS [ Links ]

World Development Indicator (2014b). Oil rents (% of total). Abstracted from URL: http://data.worldbank.org/indicator/NY.GDPPETR.RT.ZS. [ Links ]

World Development Indicator (2014c). Natural gas rents (% of total). Abstracted from URL: http://data.world-bank.org/indicator/NY.GDPNGAS.RT.ZS. [ Links ]

World Development Indicator (2014d). Fossil fuel energy consumption (% of total). Abstracted from URL: http://data.worldbank.org/indicator/EG.USE.COMM.FO.ZS. [ Links ]

World Development Indicator (2014e). Energy use (kg of oil equivalent per capita). Abstracted from URL: http://data.worldbank.org/indicator/EG.USE.PCAP.KG.OE. [ Links ]

World Development Indicator (2014f). Alternative and nuclear energy (% of total energy use). Abstracted from URL: http://data.worldbank.org/indicator/EG.USE.COMM.CL.ZS. [ Links ]

World Development Indicator (2014g). CO2 emissions (metric tons per capita). Abstracted from URL: http://data.worldbank.org/indicator/EN.ATM.CO2E.PC. [ Links ]

World Nuclear Association (2013). Renewable Energy and Electricity. Available at URL: http://www.world-nuclear.org/info/Energy-and-Environment/Renewable-Energy-and-Electricity/. [ Links ]

Yoo, S.H. and Kwak, S.Y. (2010). Electricity consumption and economic growth in seven South American countries. Energy Policy 38(1): 181-188. [ Links ]

Zivot, E. and Andrews, K. (1992). Further evidence on the great crash, the oil price shock, and the unit root hypothesis. Journal of Business and Economic Statistics 10(10): 251-270. [ Links ]

Received 28 April 2014

Revised 21 August 2014

{kind=link}

{kind=link}

{kind=link}