Services on Demand

Article

English (pdf)

English (pdf)

Article in xml format

Article in xml format Article references

Article references

Indicators

Related links

-

Cited by Google

Cited by Google -

Similars in Google

Similars in Google

Share

Permalink

PermalinkJournal of the South African Institution of Civil Engineering

On-line version ISSN 2309-8775

Print version ISSN 1021-2019

J. S. Afr. Inst. Civ. Eng. vol.58 n.4 Midrand Dec. 2016

http://dx.doi.org/10.17159/2309-8775/2016/v58n4a6

TECHNICAL PAPER

The possible rate of transition to lower-carbon housing

P Lloyd

ABSTRACT

Two of the challenges facing any transition to a lower-carbon economy in the building sector are the questions of how rapidly the existing low-efficiency stock of domestic housing can be replaced with more efficient housing, and how efficient the new housing stock can be made. This paper therefore develops a model for the replacement of the global housing stock as it ages, and considers what the demand for new housing stock is likely to be. One driver will clearly be the increasing population. Another will be economic growth, which has the counterintuitive effect of reducing the average occupancy of homes as nations develop economically. This not only accelerates the underlying rate of increase in new housing, forced by the increasing global population, but also offers opportunities for higher-value, more energy-efficient homes. Moreover, economic development is usually associated with greater levels of urbanisation, which allows greater use of multi-dwelling buildings with associated improved efficiency potential. Nevertheless, the lifetime of most homes is inherently long in comparison with the apparent urgency of reducing energy demand, and thus lower carbon emissions. It is concluded that, perse, more efficient housing is unlikely to play a significant part in the transition to a lower-carbon world over the next 35 years until 2050.

Keywords: building sector, housing, energy efficiency, demand, population growth, occupancy

INTRODUCTION

The residential part of the global building sector consumed about 16 EWh of energy in 2010 (IEA 2015), and that is expected to grow to about 30 EWh by 2050 (Lucon & Vorsatz 2014) under a business-as-usual scenario.a This is equivalent to a growth rate of about 1.7% per annum. Some of the growth will undoubtedly be due to population growth (Table 1).

Globally the average home houses about 3.4 persons, so the growth from 7.3 billion to 9.7 billion people by 2050 implies about 700 million new homes. In addition, the existing stock of homes will age and will have to be replaced. The new homes create the opportunity to introduce energy-efficient structures, provided there is the political

will to enforce building regulations that require energy efficiency. In addition, there are opportunities to improve the efficiency of the existing stock. This paper therefore aims to develop a model which will enable some quantification of the possibilities for moving the housing stock into a more energy-efficient state, and to develop some ideas about the rate at which this could occur under different levels of policy intervention.

THE PRESENT SITUATION

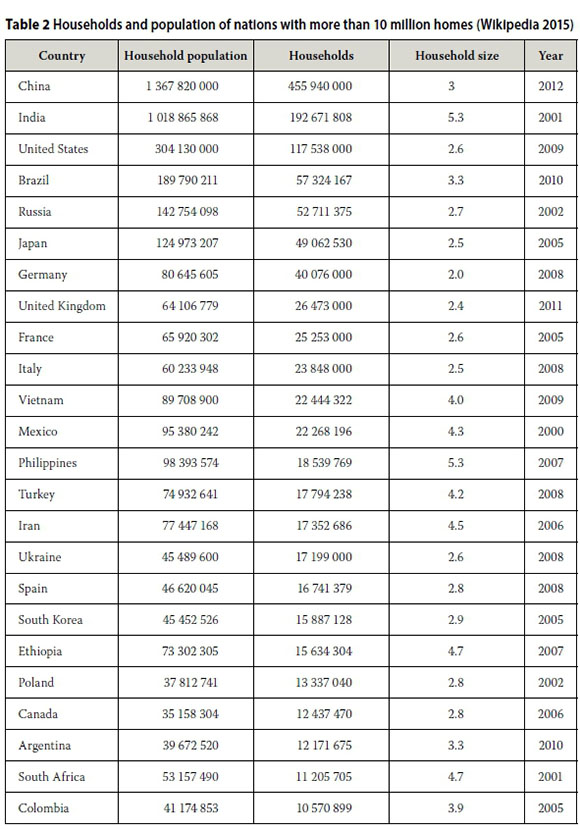

At present there are approximately 1.9 billion homes in the world. This is derived from a large sample reported in Wikipedia (2015), which includes the peer-reviewed sources of the data. A portion of this sample - nations with more than 10 million households in the year reported - is given in Table 2 in descending order of number of households. The population of all countries in the sample totalled 4.8 billion, which was 68% of the global population in 2011. The global population estimate in 2011 was taken from the World Development Indicators (World Bank 2015). The sample totalled 1.4 billion homes, or an average occupancy of 3.4 persons per dwelling.

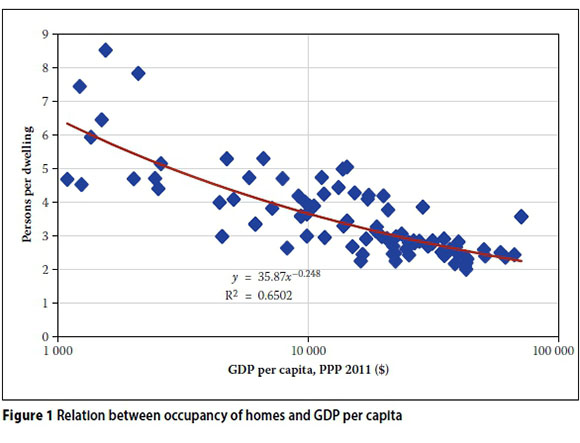

It was observed that there is a tendency for less developed nations to have a higher occupancy than more developed nations. This was tested against all nations in the sample, using the gross domestic product (GDP) per capita (World Bank 2015) as a measure of the state of development. A reasonable correlation resulted, which is shown in Figure 1. The occupancy level in nations for which there was no data on the number of dwellings was therefore estimated from the relationship:

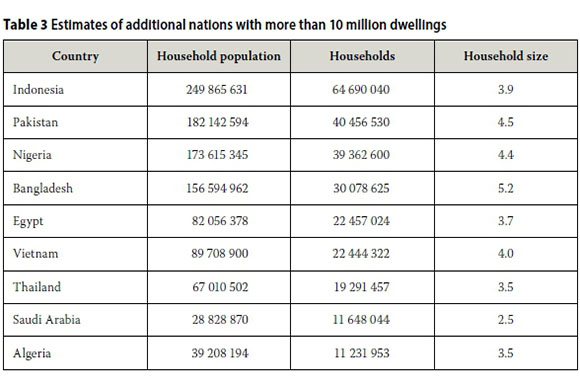

where y is the occupancy and x the GDP per capita for purchasing power parity (PPP) in 2011 US$. When this relationship was used to estimate the number of homes in those countries that were not included in the sample, but for which there were data on the GDP per capita, the total number of homes was estimated to be 1.86 billion with an average occupancy of 3.6 persons per home. The average occupancy (3.6) was somewhat higher than the average occupancy in the original sample (3.4), because poorer nations were under-represented in the original sample. Additional nations with more than 10 million homes were identified, which are shown in Table 3.

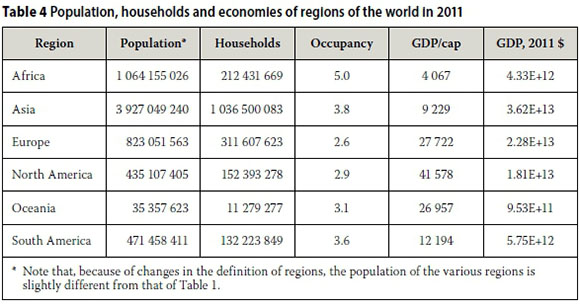

Having derived a reasonably complete picture of the world, it was then possible to aggregate the various nations into regional groupings as shown in Table 4.

FUTURE PROSPECTS

The factors that will change the number of dwelling units over the next 35 years are:

1. An increase in the number of units required to house a growing population.

2. An increase in the number of units driven by improved economies and therefore higher GDP per capita, leading to lower occupancy rates (this is also a reflection in areas such as South America and Africa of growing urbanisation and lower family sizes as a result).

3. The replacement of existing housing due to age or lack of suitability (e.g. abandoned rural homes).

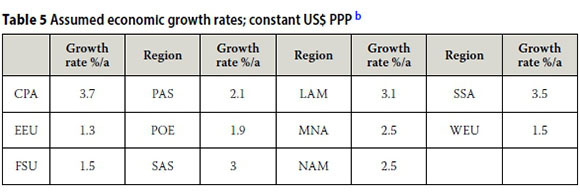

The first of these is derived directly from the growth rates given in Table 1. The second is the subject of considerable guesswork. One set of pundits believes that "growth in the OECD and emerging G20 countries is likely to decelerate from 3.4% in 1996-2010 to 2.7% in 2010-2060." (Braconier et al 2014). Another study (PWC 2015) estimates the "average real GDP growth rates for the 32 economies covered in this study over the period to 2050. Newly emerging economies such as Nigeria and Vietnam could grow at 5% or more per annum on average over this period, whilst the growth of established emerging economies such as China may moderate to around 3-4%. Advanced economies are projected to grow at around 1.5-2.5% per annum in the long run, with variations reflecting different working age population growth to a significant degree." Several other studies have reached similar conclusions, so we assume the economic growth rates shown in Table 5.

The third and final factor is the rate of replacement of the existing housing stock. Data from Europe and North America indicated that demolition rates were of the order of 25% of new construction rates, so that it was necessary to build at least 25% more homes than were needed for new entrants into the market (Carliner 1990). However, the demolition rates are precisely what they indicate - the rate at which homes are physically destroyed. Other homes are lost because they are abandoned, so that the actual loss rate is significantly higher than the demolition rate.

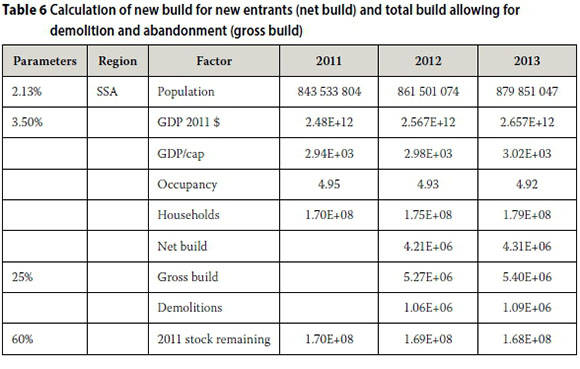

Eventually the lack of data was resolved by making what seemed to be reasonable assumptions about how much of the 2011 housing stock was likely still to be in use by 2050, and calculating how many extra dwelling units would have to be constructed each year, over and above the number of units needed to house the growing population. An underlying assumption is that all of the houses built between 2011 and 2050 will remain in use. The calculations for Sub-Saharan Africa for the first few years are illustrated in Table 6.

The first parameter is the annual rate of population growth (from Table 1), and the second, the assumed annual GDP growth in constant US dollars (from Table 5). The third is the factor giving the additional number of homes to be built each year to make up for demolition or abandonment, and the fourth is the result of the calculation, the percentage of the 2011 housing stock still in use in 2050. First the population and the GDP are calculated each year, from which the GDP per capita is calculated, which gives the occupancy, persons per dwelling, by the equation derived from Figure 1. The population divided by the occupancy gives the number of households in total. The new builds (net build) are then the difference between the number of households from one year to the next. The total of new builds (gross build) is the net build times (1+parameter), where the parameter is 25% in this case. The number of demolitions and abandonments in each year is then the difference between the gross build and the net build, and each year the original stock is reduced by the number of demolitions and abandonments of that year.

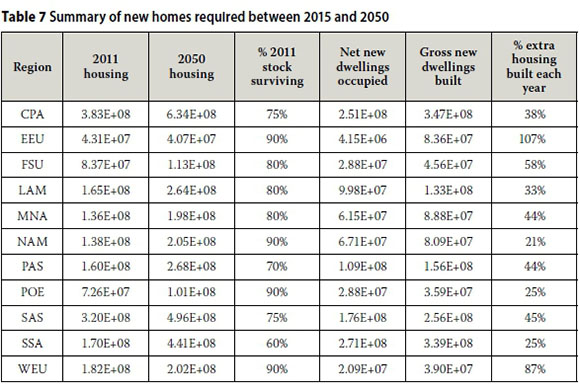

Continuing this process through 2050, the remainder of the 2011 stock is calculated, and the ratio (2011 stock remaining in 2050)/(2011 stock) then gives the fourth parameter, 60% in this case. It is argued that a loss of 40% of the original housing stock over 39 years is quite reasonable in the case of Africa, where the quality of the original stock is low and rapid urbanisation is taking place, so there is likely to be a rapid abandonment of rural homes. The results of this exercise for all the considered regions are summarised in Table 7.

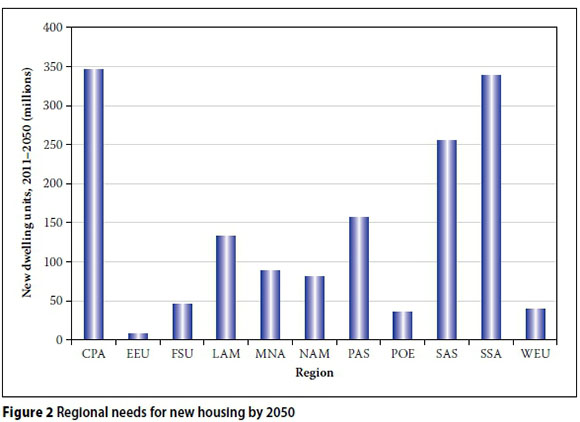

What this indicates is that, over the next 35 years, there will be new stock needed of nearly 750 million dwellings in Asia (CPA+SAS+PAS), 350 million in Africa, over 100 million in Latin America, and less than 100 million in the whole of Europe and in North America. Opportunities for introducing energy-efficient housing are clearly greatest in Asia and Africa. This is illustrated in Figure 2.

BUSINESS-AS-USUAL ENERGY DEMANDS TO 2050

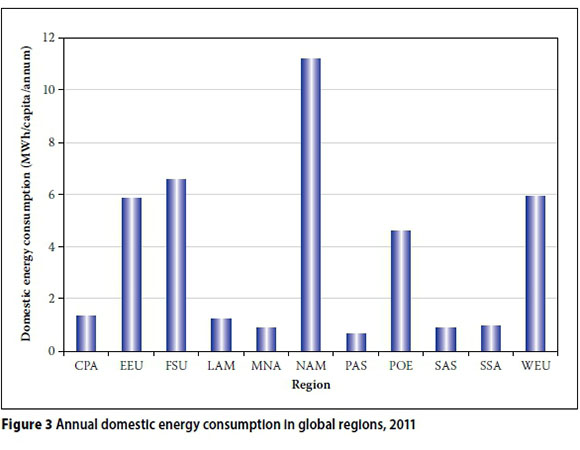

The 2011 energy demand of households in the various regions globally is shown in Figure 3 (Lucon & Vorsatz 2014). Over the next 39 years it may be expected to grow, particularly in less developed regions where at present access to modern energy services is limited. Implicit in this reasoning is that, in these regions at present there is a lack of the household appliances that are taken for granted in more developed regions. There will almost certainly be a rapid increase in the uptake of appliances as economic development occurs, which will be a primary driver of domestic energy demand. Energy-efficient housing may play a role in limiting the increase in energy consumption, which we will consider later.

There is a significant lag between the arrival of modern energy services and the full utilisation of those services. When communities are first electrified, for instance, low-power demands for lighting, communication and computation dominate. This is followed by small appliances such as kettles and irons. It is typically five years before the first major appliance is acquired, usually a refrigerator (Lloyd 2012). After about ten years the recently electrified home will start to look like the average low-income home in a developed society.

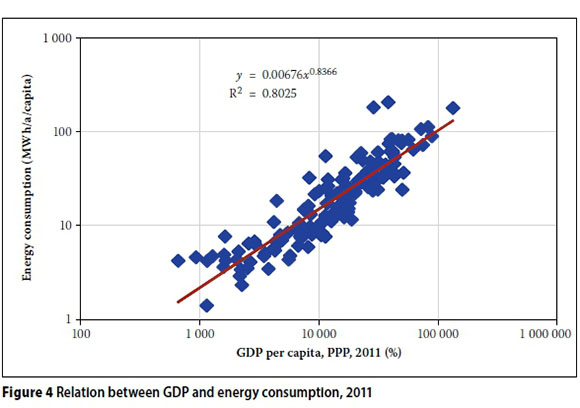

The driver for development will be economic growth. There is a strong relationship between energy consumption and wealth, as indicated in Figure 4 (World Bank 2015). A very similar relationship can be traced back over the past 50 years; it is significant and persistent. High-energy-consuming nations tend to be those having lower ambient temperatures; conversely, lower consuming nations tend to have a tropical climate. It is possible to strengthen the relationship by correcting for the ambient temperature effect, which improves the regression coefficient R2 to over 0.9, but this does not alter the relationship significantly.

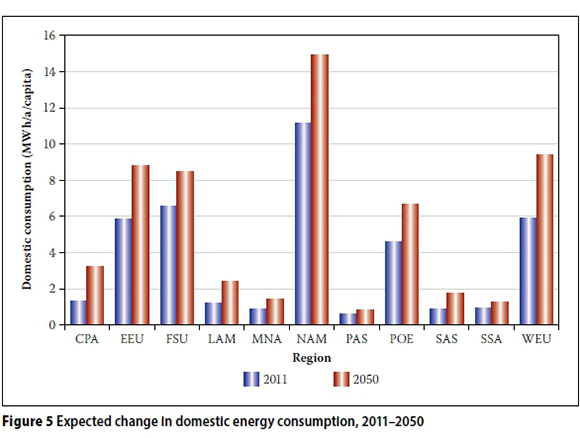

We can therefore use this relationship to estimate the probable growth in energy demand until 2050. To allow for the slow uptake, the economic growth until 2045 will be assumed as the measure to the energy demand growth to be expected until 2050. Then the domestic energy consumption in each region in 2011 shown in Figure 3 is inflated according to the relation between GDP per capita in 2011 and 2045, using the equation y = 0.00 676x0.8366 shown in Figure 4. The results are given in Figure 5.

The results seem reasonable. North America will continue to dominate the per capita consumption. There will be strong growth in Eastern Europe, the Former Soviet Union and the Pacific OECD. The Centrally Planned Asian states will also see strong growth, but off a low base. Per capita consumption in the rest of the world will remain low, but growing.

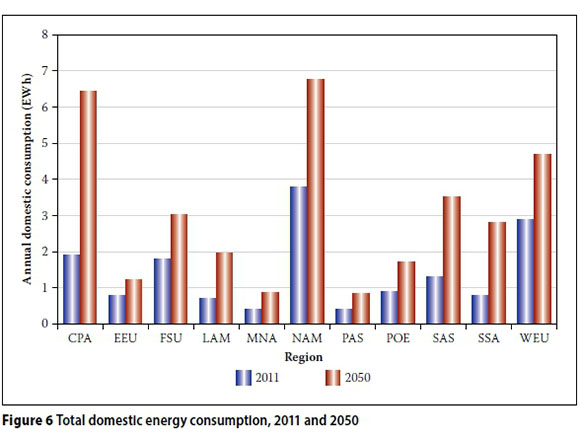

However, the picture changes dramatically when we look at the total energy consumed, as shown in Figure 6. The total energy consumption in the sector will have grown from about 16 EWh in 2011 to nearly 33 EWh. The total consumption in Centrally Planned Asia will be approaching that of North America, and the southern Asian states will be approaching that of Western Europe. The greatest proportional growth will have taken place in Sub-Saharan Africa, with over three times its 2011 consumption.

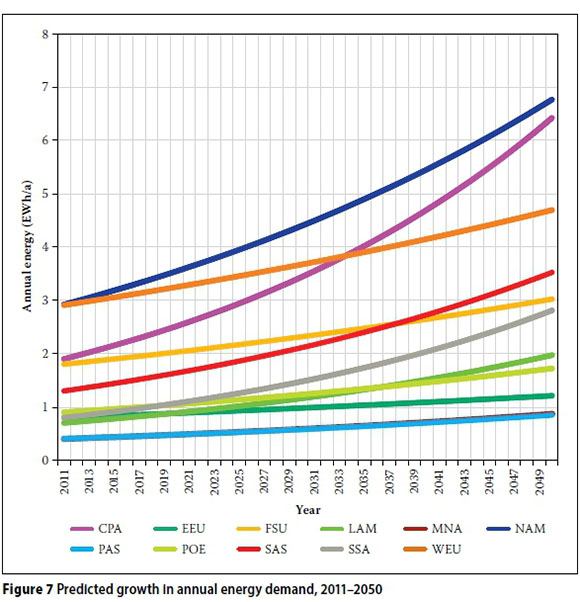

There are interesting features in the way in which the various economies grow their energy consumption in this model. Figure 7 tracks the dynamics for each region. Western Europe (WEU), the Former Soviet Union (FSU), Eastern Europe (EEU) and the Pacific Asian States (PAS) all show essentially linear growth. All have relatively low population growth and/or economic growth. The combination of high population growth and strong economic growth leads to an exponential increase in energy consumption, as so clearly shown by the Centrally Planned Asian (CPA) states. If there is to be any hope of achieving a lower-carbon world, it is clearly important to find means of curbing such exponential growth.

A LOWER-CARBON WORLD BY 2050

In previous sections we have seen how business-as-usual models and the anticipated growth of global economies, with some large-population nations developing rapidly, are likely to lead to large increases in the demand for energy. Today there are concerns that China and the other Centrally Planned Asian states will not be able to control their emissions before 2030. What we have shown is the following:

■ Those regions that already have high per capita consumption are unlikely to reduce their per capita consumptions, and will probably increase their total consumption.

■ Those regions that are developing rapidly are likely to increase their per capita consumption rapidly, and their population increase means that their total consumption is likely to rise rapidly.

In the light of this, we have to ask what assumptions might be necessary to reduce the growth in energy consumption. First, of course, is the possibility of improving the energy performance of new buildings. By 2050, about 1.5 billion new homes will have been built, of which 1.1 billion will be newly occupied and 0.4 billion occupied by people who previously lived in homes that were demolished or abandoned during the period. The total number of dwellings by 2050 will be about 3 billion, so that new dwellings will represent about half the stock. There are clearly opportunities for improving the energy performance of these new dwellings.

Quite wide experience has shown that it is probably possible to achieve about a 40% reduction in energy consumption in new homes without very significant changes in building practice.c As a thought experiment, therefore, let us assume that by 2020 there is local legislation in some parts of the world requiring such a reduction in the design of every new home, and that by 2025 such legislation is widespread. Then the domestic demand pattern shown in Figure 7 will change to that shown in Figure 8. Comparison between the two figures shows that there is now very low growth in seven of the regions, and that the exponential growth shown in some regions in Figure 7 is now close to linear. The reduction in energy from 33 to 26 EWh/a represents about a 25% reduction from the business-as-usual scenario, but it is still some 75% above the 2011 consumption, with growth driven by NAM, CPA, WEU and SAS in particular. NAM and WEU start from a high level of consumption (and high wealth), and both enjoy quite low population growth rates, so it is evident they should strive for additional curbs on growth in energy consumption. In contrast, CPA and SAS both start from a relatively low base and have to cope with significant development issues, so it seems there is little that they could do to reduce their energy demand further.

Clearly there are opportunities to enforce greater energy efficiency in existing dwellings, which could further reduce the demand, but the model foresees very aggressive action in respect of new homes, which will make up about 50% of the total homes by 2050, so improved efficiency in existing homes will not make a great difference to the outcome.

DISCUSSION AND CONCLUSIONS

It seems that the possibility of achieving a lower-carbon world through improvements in the energy efficiency of homes is limited. Of course, it is possible to improve the energy performance of existing homes, but Table 7 shows that, even though a significant fraction of today's housing stock will survive until 2050, by 2050 the new stock will be as large as the existing stock. The focus should therefore be on ensuring that the new stock is energy efficient.

It should be possible to achieve a lower-energy demand than a business-as-usual scenario, but there is still likely to be a significant growth in energy demand by 2050. The growth in the demand for homes will drive the energy growth regardless of efficiency measures.

There are two drivers for more homes, first and obviously, the growth in the population, and secondly, the tendency for smaller families and thus less people per dwelling as economic development takes place. Even in developing nations, where population control measures have proved effective, there is a marked reduction in the number of people per dwelling and a rise in single-person occupancy (China Daily 2015).

A driver for increased energy consumption has been increasing domestic use of energy, driven by wider use of electricity in homes in developing nations. Clearly, energy-efficient appliances will play a part in helping to reduce the demand for energy, but even if all appliances are A-rated rather than D-rated, at best savings of the order of 50% are achievable (SEIA 2015), which is insufficient to reduce 2050 consumption to less than 2011 consumption. There is already a reasonable population owning A-rated appliances, so the full benefit is no longer available.

It can only be concluded that, in the area of domestic homes, the opportunities for containing the growth of energy consumption over the next 35 years are very limited; the chances of reducing the energy consumption are virtually nil. This is the only conclusion responsible engineers can reach when they look at the likely growth of housing over the next generation. There is a drive to a lower-carbon world, but practical considerations indicate that, from the demand side, there is little that can be done to reduce demand significantly, particularly in the face of a strongly growing market. It is possible that low-carbon energy generation may succeed in reducing emissions on the supply side of the equation, but whether these will be able to do so at the same level of service delivery that fossil fuel-, nuclear- and hydro-powered generation currently afford, is doubtful, unless cost-effective energy storage systems can be developed, something which is widely sought, but tantalisingly remote at present.

NOTES

a. Note that there is some discrepancy in Lucon & Vorsatz 2014. Figure 9.3 gives what appears to be incorrect data for per capita domestic energy consumption. This data led to an estimate of 24.3 PWh in 2010, as shown in Figure 9.4. The data of Figure 9.5, however, gives far more reasonable data for the domestic energy consumption. This data leads to an estimate of 15.8 PWh for the global consumption, which we use here.

b. CPA Centrally Planned Asia; EEU Eastern Europe; FSU Former Soviet Union; LAM Latin America; MNA Middle East North Africa; NAM North America; PAS Pacific Archipelago States; POE Pacific OECD; SAS Southern Asia; SSA Sub-Saharan Africa; WEU Western Europe.

c. The USEPA claims its Energy Star homes to be 15-30% more energy efficient (e.g. https://www.energystar.gov/index.cfm?c=products.pr_save_energy_at_home); British and Australian estimates indicate that improvements of 40% are possible (e.g. Victorian Households Energy Report, Sustainability Victoria, May 2014 RSE014); in Germany, noting that 75% of all houses were built before 1979, the estimate is a potential 40% saving (http://www.bmub.bund.de/en/topics/climate-energy/energy-efficiency/general-information/#c15251).

REFERENCES

Braconier, H, Nicoletti, G & Westmore, B 2014. Policy challenges for the next 50 years. OECD Economic Policy Paper No. 9, Paris: OECD Publishing. Available at: http://www.oecd.org/economy/Policy-challengesfor-the-next-fifty-years.pdf [accessed in September 2015]. [ Links ]

Carliner, M 1990. Replacement demand for housing. Housing Economics, December: 5-9. [ Links ]

China Daily 2015. Size of Chinese family getting smaller. Available at: http://www.chinadaily.com.cn/china/2014-05/15/content_17508456.htm [accessed in September 2015]. [ Links ]

IEA Online Data Services 2015. Environmental issues. Available at: http://data.iea.org/ieastore/statislisting.asp [accessed in September 2015]. [ Links ]

Lloyd, P 2012. Twenty years of knowledge about how the poor cook. Proceedings, International Conference on Domestic Use of Energy, Cape Peninsula University of Technology, 3-4 April 2012, pp 21-30. [ Links ]

Lucon, O & Ürge-Vorsatz, D, Zain Ahmed, A et al 2014. Buildings. In Climate Change 2014: Mitigation of Climate Change, Chapter 9 of 5th Assessment Report (AR5) of the Intergovernmental Panel on Climate Change. Geneva: IPCC. [ Links ]

PWC (PriceWaterhouseCoopers) 2015. The world in 2050. Will the shift in global economic power continue? Available at: http://www.pwc.co.uk/economics [accessed in September 2015]. [ Links ]

SEIA (Sustainable Energy Authority of Ireland) 2015. Electricity use in the home. Available at: http://www.seai.ie/Schools/Post_Primary/Subjects/Home_Economics_JC/Appliances/ [accessed in September 2015]. [ Links ]

UNDESA (United Nations Department of Economic and Social Affairs, Population Division) 2015. World Population Prospects. The 2015 Revision. New York: UN. [ Links ]

Wikipedia 2015. List of countries by number of households. Available at: https://en.wikipedia.org/wiki/List_of_countries_by_number_of_households [accessed in August 2015]. [ Links ]

World Bank 2015. World Development Indicators. Available at: http://www.data.worldbank.org/data-catalog/world-development-indicators [ Links ]

Correspondence:

Correspondence:

P Lloyd

Energy Institute

Cape Peninsula University of Technology

PO Box 1908

Bellville 7535

South Africa

T: +27 21 959 4323

E: lloydp@cput.ac.za

PROF PHILIP LLOYD was trained as a chemical engineer (University of Cape Town) and a nuclear physicist (Massachusetts Institute of Technology). He joined the Chamber of Mines Research Organisation in 1965 and became Director Metallurgy. In 1983 he was made Managing Director, EMS Minerals and in 1988 he joined EL Bateman. On retirement he returned to academic life, first at the University of the Witwatersrand, then at the University of Cape Town, and now he is professor at the Energy Institute of the Cape Peninsula University of Technology. He has been active in the profession his whole life, won several awards, and is an Honorary Fellow of the South African Academy of Engineering.