Servicios Personalizados

Articulo

Inglés (pdf)

Inglés (pdf)

Articulo en XML

Articulo en XML Referencias del artículo

Referencias del artículo

Indicadores

Links relacionados

-

Citado por Google

Citado por Google -

Similares en Google

Similares en Google

Compartir

Permalink

PermalinkSAMJ: South African Medical Journal

versión On-line ISSN 2078-5135

versión impresa ISSN 0256-9574

SAMJ, S. Afr. med. j. vol.102 no.10 Pretoria oct. 2012

IZINDABA

Mandatory cover? 'Yes, but not now' - Zokufa

Making medical scheme member contributions mandatory is less important than properly regulating prescribed minimum benefits (PMBs) which pose the biggest, most imminent threat to medical schemes' viability, Board of Healthcare Funders (BHF) CEO Dr Humphrey Zokufa claims.

He was responding to findings which Barry Childs, CEO of Lighthouse Actuarial Consulting and CareGuage presented at the BHF conference in the Drakensberg in July showing that the medical aid industry loses R13.5 billion annually due to anti-selection pressures when cover is not mandatory. Childs compared open and restricted schemes for well over a decade and found open schemes reversed from being 12% cheaper in the 1990s to being 14% more expensive in ensuing years, rising to 30% more expensive between 2000 and 2012. Contributions to open schemes increased 2.6% faster than restricted schemes which in turn increased 2% faster than inflation. He then interrogated the data to see if removing the two largest medical schemes, GEMS (restricted) and Discovery (open), would make a difference. In terms of healthcare and non-healthcare costs, the divergence remained.

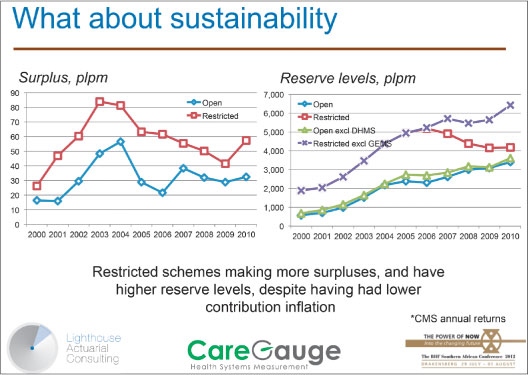

Childs' research did show, however, that the inclusion of GEMS has seen a marked impact on the efficiency of restricted schemes. As for sustainability, Childs found that restricted schemes are making more surpluses and have higher reserve levels despite having had lower contribution inflation. 'Real price inflation is only a part of the cost escalation issue - utilisation is a much bigger force,' he concludes, adding that while mandatory membership would not retrieve the lost money, it would make a difference in the future. While Dr Zokufa does not argue with Childs' findings, he maintains that any changes should be 'contextualised correctly'. He believes mandatory cover should only be introduced as an immediate precursor to the NHI. 'The problem with mandatory cover is that the new (majority) members become cannon fodder for the high-cost members. The people with lesser benefits effectively subsidise those who have more benefits and who claim more. It can only work if the money collected from the new members is ring-fenced for their benefit. Each option level must be self-sufficient,' he stresses. He added that the traditional argument for mandatory membership was that it solved the problem of people only joining medical schemes when they were older or, in the case of women, when they fell pregnant - both categories likely to create higher medical costs.

'I think Barry is missing the point. Each of the members of the (BHF) board of trustees, 43 of them (BHF consists of 73 medical schemes), said "sort out the Reg 8 and PMB issues because they are by far the most viability-threatening for us". In 2008/9 the argument was around a risk equalisation fund but we're moving away from that. There are no listeners for that argument anymore.' He added that another major impediment to the growth and sustainability of medical schemes (especially the smaller ones), was the compulsory solvency ratio of 25%. His point was dramatically illustrated by Christoff Raath, an actuary and CEO of The Health Monitor Company. Raath told delegates that the magnitude of the catastrophe that would have to occur in order to deplete the reserves of large schemes was 'akin to the Black Death - unimaginable'. He said the origin of the 25% figure remained mystery, but the general consensus was that there was no scientific basis for it, and it would 'not be unfair to call it a thumb-suck'.

Current solvency model a tax on members

Raath said 'a simplified, risk-based capital approach' would be preferable, because it would release significant funds and still ensure sufficient reserves. He said the current solvency model rewarded loss-making schemes and penalised surplus-making schemes. It was effectively a tax on members, as contributions were invariably increased to maintain the solvency level. South Africa's two biggest schemes are each obliged to hold close to R11 billion in reserves to meet the solvency requirement of 25%. Zokufa added that 'if we say mandatory membership now, it must be introduced in preparation and pursuit of what would happen under an NHI (mandatory) environment. Whatever is collected from them serves their needs only and not those on higher options,' he said, pointing to the Council for Medical Schemes requirement that each option should be self-sufficient.

Chris Bateman

chrisb@hmpg.co.za