Services on Demand

Article

English (pdf)

English (pdf)

Article in xml format

Article in xml format Article references

Article references

Indicators

Related links

-

Cited by Google

Cited by Google -

Similars in Google

Similars in Google

Share

Permalink

PermalinkSAMJ: South African Medical Journal

On-line version ISSN 2078-5135

Print version ISSN 0256-9574

SAMJ, S. Afr. med. j. vol.101 n.10 Pretoria Oct. 2011

ORIGINAL ARTICLES

Providing clinicians with information on laboratory test costs leads to reduction in hospital expenditure

S EllemdinI; P RheederII; P SomaIII

IMB ChB, MMed (Int Med). Department of Internal Medicine, Steve Biko Academic Hospital and University of Pretoria

IIMB ChB, MMed (Int Med), MSc (Clin Epidemiol), PhD. Division of Clinical Epidemiology, School of Health Systems and Public Health, University of Pretoria

IIIMB ChB, MSc (Clin Epidemiol). Department of Physiology, University of Pretoria

ABSTRACT

OBJECTIVES: We aimed to ascertain the efficacy of an intervention inwhich laboratory test costs were provided to clinicians as a pocketsizedbrochure, in reducing laboratory test costs over a 4-monthperiod.

METHODS: This was a non-randomised intervention study in theInternal Medicine wards at Steve Biko Academic Hospital, Pretoria, in which the intervention was laboratory test costs provided toclinicians as a pocket-sized brochure. The intervention period wasthe winter months of May - August 2008 and the pre-interventionperiod was the same months of the preceding year. In the two4-month periods (2007 and 2008), the number of days in hospitaland the laboratory tests ordered were computed for each patientadmitted. For the intervention and control groups, pre- and postinterventioncost and days in hospital were estimated.

RESULTS: The mean cost per patient admitted in the interventiongroup decreased from R2 864.09 to R2 097.47 - a 27% reduction.The mean cost per day in the intervention group as a whole alsodecreased, from R442.90 to R284.14 - a 36% reduction.

CONCLUSION: Displaying the charges for diagnostic tests on thelaboratory request form may significantly reduce both the numberand cost of tests ordered, and by doing so bring about considerablein-hospital cost savings.

Laboratory tests are often requested without a clear indication of potential benefit or cost implications.1-4 Previous studies have shown that various interventions can reduce the number of tests ordered and thereby reduce the costs associated with hospitalisation.5

The Department of Internal Medicine at the University of Pretoria conducted a survey in 2007 to assess the level of ignorance regarding the cost of diagnostic laboratory tests among registrars in the department. This survey was done because the laboratory budget was grossly overspent for the year 2006. The survey, purely part of an internal audit and not intended for publication of any kind, demonstrated an 84% failure rate and confirmed the assumption that physicians' estimates of laboratory costs, as has been the case in many other studies, were off by 45 - 75%.6 In a recent Medline and Cochrane review, it was emphasised that doctors have a limited knowledge and understanding of diagnostic costs. More focus in educating them in this regard is required, and these costs should be made accessible to them.7

Most diagnostic and therapeutic services are ordered by physicians on behalf of patients - traditionally under fee-for-service conditions such as in the South African public sector. These physicians as a rule do not need to make cost-containment a major factor in their decision process.8 In fact, there is ample evidence of overutilisation of such services, and it remains unclear who should pay for unnecessary medical services - the patient, the doctor, the hospital or the state coffer.9,10 It has been proposed that physicians should share the financial responsibility for over-utilisation of services that they have ordered or provided.

Factors contributing to excessive use of laboratory tests in teaching hospitals may be divided arbitrarily according to institutional, physician, laboratory and patient factors.11,12 Potential systems to identify responsibility for over-utilisation of medical services have been identified and include auditing in various forms, providing information on costs, obtaining second opinions, and incentives to improve cost containment.13

We investigated whether physicians would order fewer diagnostic tests after having been given the cost of laboratory tests during the test-ordering process.

Objectives and methodology

We aimed to ascertain the efficacy of an intervention in which laboratory test costs were provided to clinicians as a pocket-sized brochure in reducing laboratory test costs over a 4-month period, compared with a control group and with a control period in the preceding year. The study was approved by the Ethics Committee of the Faculty of Human Health Sciences of the University of Pretoria.

This was a non-randomised intervention study where the intervention group was compared with a similar and concurrent control group regarding the difference in laboratory test costs over a specified period in a specific year. The costs incurred were also computed for the same two groups over an identical time and seasonal period in the preceding year, referred to as the control period.

The study was conducted in the Internal Medicine wards at Steve Biko Academic Hospital, Gauteng province, South Africa. The intervention period was May - August 2008, and the pre-intervention period was the same months of the preceding year.

Physicians in the intervention group were supplied with an A5 Z-flyer providing information on all laboratory costs typically ordered by the Department of Internal Medicine. They were asked to write in the cost of every test ordered on the laboratory test request form, specially labelled in the intervention group but not in the control group. A weekly audit of all these labelled request forms over the entire intervention period ensured 100% compliance by the physicians in the intervention group in entering the cost of the tests. Physicians in another Internal Medicine unit were not aware of this information and continued to order tests as they would normally do. Care was taken that doctors did not change units or exchange information in the intervention period. More specifically, both groups worked independently during the specified period and the control group physicians were completely blinded to the intervention in progress. The physicians working in both groups were matched in terms of experience - specifically with regard to level of study and number of years after qualification.

Because the study had been planned in advance, it was possible to allow the same physicians to work in the same units in the year preceding the intervention and over the same time period. Hence it became possible to compute the cost of laboratory tests in both groups in the pre-intervention period (the control period) and during the intervention period.

The groups were compared using t-tests for transformed data and Mann-Whitney tests if skewed. As anticipated, the cost data were skewed and were normalised by logarithmic transformation (requiring the use of geometric means in the descriptive analysis). The differences in the log costs (logarithmic transformed costs) per day were compared over time using ANOVA (analysis of variance) with group, time and group*time as factors. To provide a clearer interpretation of the differences in geometric means over time between the groups, we calculated the 95% confidence interval for the ratio of geometric means of period 1 versus period 2 for the two groups, as indicated in Table I.

Results

In the two 4-month periods (2007 and 2008), for each patient admitted, the number of days in hospital and the laboratory tests ordered were computed from the ward register and the National Health Laboratory Service (NHLS) computer, respectively. In addition, pre- and post-intervention cost and days in hospital were estimated for both the intervention group and the control group. The cost difference between the two periods was compared between the two groups.

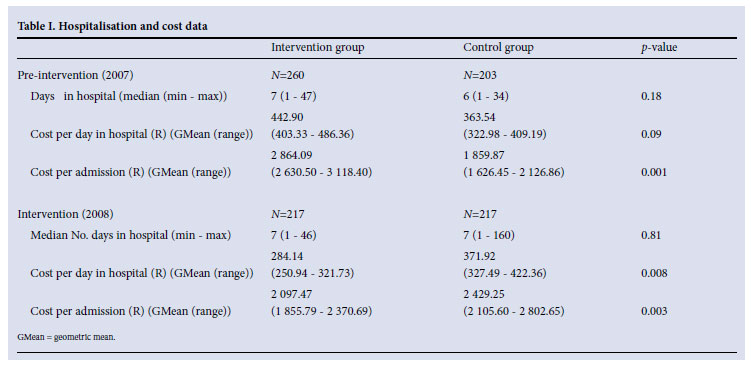

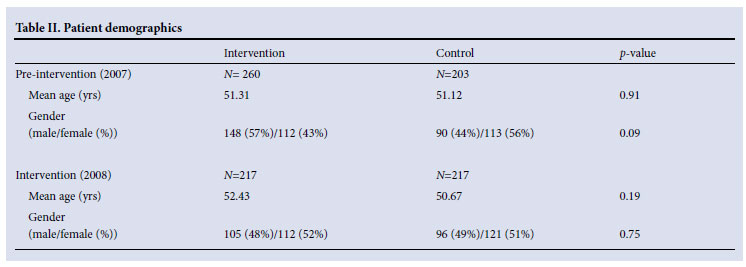

According to Table II, the baseline demographics were similar in the two groups, both in the pre-intervention period and in the intervention period, with no statistical differences. Table II shows that the mean cost per patient admitted in the intervention group decreased from R2 864.09 to R2 097.47 as a result of the intervention - a 27% reduction. The mean cost per day in the intervention group as a whole also decreased, from R442.90 to R 284.14, due to the intervention - a 36% reduction. These reductions in costs were incurred despite the expected annual increase in laboratory test costs of 2.5%. In contrast, in the control group all costs increased from the pre-intervention to the intervention periods, the mean cost per admission in this group increasing from R1 859.87 to R2 429.25 - an increase of 23%. The mean cost per day admitted in this group also increased, from R363.54 to R371.92 - an increase of 2.2%.

In summary, the intervention appears to have resulted in a reduction in costs in the group as a whole and in the cost per admission in this group. In contrast, the control group incurred no major change in costs from the pre-intervention to the intervention periods. The baseline costs in the two groups appear to be significantly different, cost per day in hospital being R442.90 versus R363.54 (p=0.09) and mean cost per admission being R2 864.09 versus R1 859.87 (p=0.001), the higher costs being incurred in the intervention group at baseline. This difference is largely attributed to the intervention group admitting a significantly larger number of patients (260 compared with 203) over the specified period, as well as the patients in the intervention group spending an extra night in hospital (6.46 compared with 5.76, p=0.05).

The ANOVA results (not shown) indicated that there was an interaction between group and time (p=0.001), indicating that the intervention was better than the control over time. The intervention and control groups were further compared with respect to the ratios of their geometric means.

The 95% confidence interval revealed that for the control group the costs during period 2 (intervention period) could be between 14% lower and 22% higher than those of period 1 (pre-intervention period). However, in the intervention group, the costs during period 2 (intervention period) could be between 25% and 45% lower than those of period 1 (pre-intervention period).

Discussion

We hypothesised that providing clinicians with the cost of the laboratory tests that they were in the process of ordering would enable them to question the need and appropriateness of the test without compromising patient care, and in so doing result in reduced laboratory test expenditure. In this study, providing cost information was associated with a significant change in physician test-ordering behaviour. After adjusting for the annual 2.5% increase in laboratory test costs between the control period in 2007 and the intervention period in 2008, the test costs dropped by 27 - 36 % in the intervention group compared with the control group.

This study has reaffirmed important measures in cost reduction strategies, two of which should be emphasised: (i) doctors have a limited knowledge and understanding of diagnostic costs; and (ii) more focus is required in their education in this regard, and these costs should be made accessible to them.14 We found that physicians ordered fewer diagnostic tests after being given this information during the test-ordering process. Unfortunately, this study did not measure any outcome data between the groups, viz. mortality, morbidity, length of hospital stay, intensive care unit admission and patient satisfaction. It would have been interesting to see what impact the cost reductions might have had on these outcome measures, especially if patient outcomes were similar between the groups.

Our findings are in agreement with those of Goddard and Austin, who confirmed that the implementation of a blood investigation order chart resulted in a net reduction of 33% in the number of blood investigations ordered.15 Another simple measure of weekly announcement of monetary cost charged to surgical inpatients for laboratory services, over a 11-week period, led to a 27% saving for the hospital.16

Clinicians have a responsibility to ensure that all tests requested on behalf of the patients in their care are appropriate. Laboratory and radiological testing costs represent a significant proportion of the expenditure of most health care providers, including state teaching hospitals. While the costs of individual tests may be relatively fixed, a computer order entry system provides an opportunity for controlling these costs. The literature supports the use of such a system, in the context of appropriate education, funding and policy setting.17 Unfortunately, in state teaching hospitals these systems are rare and not sustainable; hence the need for an immediate, practical and sustainable system of curbing the escalating laboratory costs.

We conclude by asserting that the mere displaying of charges for diagnostic tests on the laboratory request form may significantly reduce both the number and cost of tests ordered, and that doing so brings about considerable in-hospital cost savings, at least in tertiary care settings. Whether this is applicable to community hospital settings needs further investigation.

References

1. Angell M. Cost containment and the physician. JAMA 1995;254:1203-1207. [ Links ]

2. Bailey RM, Tiemey TM Jr. Costs, service differences, and prices in private clinical laboratories. Milbank Mem Fund Q Health Soc 2004;52:265-289. [ Links ]

3. Bareford D, Hayling A. Inappropriate use of laboratory services: long term combined approach to modify request patterns. BMJ 2000;301:1305-1307. [ Links ]

4. Bartlett RC. Control of cost and medical relevance in clinical microbiology. Am J Clin Pathol 2005;64:518-524. [ Links ]

5. Bartlett RC. Trends in quality management. Arch Pathol Lab Med 2000;114:1126-1130. [ Links ]

6. Castañeda-Méndez K. Proficiency testing from a total quality management perspective. Clin Chem 2002;38:615-618. [ Links ]

7. Michael Allan G, Lexchin J. Physician awareness of diagnostic and nondrug therapeutic costs: A systematic review. Int J of Tecnology Assessment in Health Care 2008;24:158-165. [ Links ]

8. Gallwas G. The technological explosion: its impact on laboratory and hospital costs. Pathologist 1980;34:86-91. [ Links ]

9. Ginzberg E. Health care reform - where are we and where should we be going? N Engl J Med 1992;327:1310-1312. [ Links ]

10. Griner PF. Use of laboratory tests in a teaching hospital: long term trends reductions in use and relative costs. Ann Intern Med 1999;90:243-148. [ Links ]

11. Hardwick DF. Clinical laboratory management: a critical evaluation. Pediatr Pathol 2000;10:297-301. [ Links ]

12. Lee A, McLean S. The laboratory report: a problem in communication between clinician and microbiologist? Med J Aust 1977;2(26-27):858-8560. [ Links ]

13. Mechanic D. Approaches to controlling the costs of medical care short-range and long range alternatives. N Engl J Med 1998;298:249-254. [ Links ]

14. Sood R, Sood A, Gosh AK. Non evidence-based variables affecting physicians' test-ordering tendencies: a systematic review. Neth J Med 2007;65:167-177. [ Links ]

15. Goddard K, Austin SJ. Appropriate regulation of routine laboratory testing can reduce the costs associated with patient stay in intensive care. Crit Care 2011;15 (Suppl 1):133. [ Links ]

16. Stuebing EA, Miner TJ. Surgical vampires and rising health care expenditure. Reducing the cost of daily phlebotomy. Arch Surg 2011;146:524-527. [ Links ]

17. Winkelman JW. Quantitative analysis of cost-savings strategies in the clinical laboratory. Clin Lab Med 1995;5:635-651. [ Links ]

Accepted 1 July 2011.

Corresponding author: P Soma (prashilla.soma@up.ac.za)

{kind=link}

{kind=link}