Serviços Personalizados

Artigo

Inglês (pdf)

Inglês (pdf)

Artigo em XML

Artigo em XML Referências do artigo

Referências do artigo

Indicadores

Links relacionados

-

Citado por Google

Citado por Google -

Similares em Google

Similares em Google

Compartilhar

Permalink

PermalinkSouth African Journal of Education

versão On-line ISSN 2076-3433

versão impressa ISSN 0256-0100

S. Afr. j. educ. vol.43 no.4 Pretoria Nov. 2023

http://dx.doi.org/10.15700/saje.v43n4a2307

ARTICLES

Financial management in fee-paying public schools in South Africa: How responsible is the school governing body?

A Aina; A du Plessis

Department of Education Management and Policy Studies, Faculty of Education, University of Pretoria, Pretoria, South Africa adebunmiaina@gmail.com

ABSTRACT

The South African Schools Act, No. 84 of 1996, stipulates how schools should manage and involve stakeholders in financial management. The literature suggests that stakeholders at non-fee-paying schools in the township and rural areas do not play a dominant role in their schools' financial management decision-making processes, which is contrary to the dictates of the South African Schools Act. However, in the study on which this article is based, we focused on the financial management decision-making processes in fee-paying public schools. We followed a qualitative research approach with a multiple case study design. Data were collected using semi-structured interviews and document analysis, and were analysed thematically. The findings reveal that members of school governing bodies in Quintile 5 fee-paying public primary schools were educated professionals who, as required by the South African Schools Act, exerted a strong influence on the financial management responsibilities in their schools.

Keywords: fee-paying schools; financial decision-making processes; responsibilities; school financial management; school governance; school governing bodies

Introduction and Background to the Problem

To ensure the effective and efficient delivery of education, governments worldwide have introduced decentralised decision-making in education by increasing parental and community participation in schools (Androniceanu & Ristea, 2014). This allows for different capabilities to be displayed and for power and influence at the school level to be exerted more strongly (Mestry, 2013). For effective and efficient financial management in schools to occur, role-players need to ensure that their functions are clearly defined and that financial management activities are performed by persons or committees responsible for attaining the goals set by schools (Mestry, 2016). It is, therefore, essential to understand what financial management responsibilities entail and how financial decisions are taken by role-players while adhering to legal requirements to achieve proper financial management.

The South African Schools Act, No. 84 of 1996 (hereafter referred to as the Schools Act) prescribes how financial management should take place in schools. It assigns financial management duties to school governing bodies (SGBs) and principals (Mestry, 2013). The financial responsibilities of SGBs require them to understand the demands of the Schools Act and other relevant financial knowledge. This can influence the way in which SGBs meet their financial responsibilities. Role players involved in the financial management of public schools are expected to work together as a team to perform the functions prescribed by the Schools Act and achieve the objectives of their schools. Studies that were conducted in the township and rural areas have, however, found that this was not the case and that principals and the SGBs lacked an understanding of legislation relating to school finance management (Lekonyane & Maja, 2014; Mestry, 2006; Rangongo, Mohlakwana & Beckmann, 2016). Some researchers contend that there is often a lack of collaboration between principals and parent governors of schools (Mestry, 2006:33; Mestry & Govindasamy, 2013). Lekonyane and Maja (2014) add to this by maintaining that the majority of SGBs in township areas lack the necessary skills and competence to manage school finances due to the members' low or little basic educational background.

Sections 20 and 36 to 44 of the Schools Act allocate responsibility to SGBs and prescribe how they should manage school funds effectively, proficiently, and responsibly. Mahlangu (2005) believes that the main purposes of having an SGB are to ensure that parents have a greater influence on their children's education and to foster devolved school management. Rangongo (2011) supports this view by stating that having parents as the majority component indicates that parent governors should effectively and influentially manage the school's finances. This is in contrast to the findings of Bagarette (2012), Botha (2012) and Mncube (2009) who, by focusing their research on schools in predominantly non-fee paying schools, conclude that principals in schools exercise a dominant influence over the parent governors. Mncube (2009) explains that SGB members regularly accept decisions taken by principals because they are afraid of being accused of disloyalty. They pretend to be part of decision-making processes but seldom question principals in terms of financial matters, which signifies irresponsibility on the part of the SGB. The problems identified in the above studies emerged predominantly in non-fee-paying schools, situated mostly in the township and rural areas, hence a gap on research focussing on schools situated in urban areas was detected in the literature. A need was identified to investigate the financial management of SGB responsibilities in fee-paying schools situated in more affluent urban areas to determine whether the same problems existed.

With this research we aimed to make a relevant contribution to the existing body of knowledge on financial management practices by exploring the financial management responsibilities of SGBs at fee-paying public primary schools. The aim of exploring the financial management responsibilities was to determine factors that influenced the financial management duties of SGB members and illuminate how individual SGB members influenced the financial management processes at the school. The research questions formulated to achieve these objectives are:

• What factors influence the financial management responsibilities of the SGB at fee-paying public primary schools?

• What are the roles and influence of individual SGB members concerning financial management decision-making at fee-paying public primary schools?

Literature Review

There is a substantial international trend towards decentralising school finance management (Mestry & Hlongwane, 2009). Different countries introduced decentralised education systems for a variety of reasons (Diamond, 2015), which suggests that each country has its own reasons for doing so. In the United States of America, the Charter School Program was created in order to create a new type of school where school management teams had extensive autonomy over the selection of the curriculum, learning instruction, staff recruitment, school budget, and student discipline (Bifulco & Ladd, 2006). In England, the Education Reform Act of 1988 was passed to increase parental involvement, decentralise school finances, and institutional autonomy (Bhattacharya, 2013; Reyes & Rodriguez, 2004). Decentralised schools were promoted in New Zealand to give parents a say in their children' s education. As a result, elected parent boards of trustees were given more autonomy and decision-making authority over how the schools distributed government funding for staff and daily operations (Court & O'Neill, 2011). According to Koross, Ngware and Sang (2009), parental involvement in the financial management of schools is low in Kenya. It is admirable when key stakeholders are involved in the financial management of schools around the world, however, the effectiveness of the SGBs in handling their financial responsibilities is more crucial.

In the South African context, the introduction of the Schools Act initiated a practice of decentralisation by involving communities in school governance (Mestry, 2004). As stated in the preamble to the Schools Act, a partnership model is envisaged whereby both the state and local school communities take shared responsibility for the governance of schools at the school level. Thus, the Schools Act resulted in more decision-making authority and responsibility being transferred to those at the school level than previously (Mestry, 2006). The implementation of the Schools Act -Sections 36, 37, 38, 42, 43 and 44 now places greater financial management responsibilities on SGBs and principals (Moloi, 2007; Republic of South Africa [RSA], 1996). The composition of SGBs is such that it involves all relevant role-players in school governance. Therefore, the SGBs must comprise principals (ex officio), parents, teachers, a non-teaching staff member, community representatives, and learners from Grade 8 upwards in secondary schools. Hence, it is important to understand the individual role-players' financial management duties. We focused on explaining the financial management duties of the principal, the non-teaching staff member, and the parent component of the SGBs and their individual influence over the financial management processes at the school.

Section 20 of the Schools Act stipulates the functions of SGBs, while Section 21 provides for additional functions for which SGBs may apply to the provincial Head of Department, which specify how they can effectively apply the additional functions. If approved, SGBs will, among other things, be required to pay for services to the school, purchase of textbooks and learning support materials, and control the extra-mural activities at the school. All these functions have direct financial implications. The schools that were the focus of this study were allocated Section 21 functions and are referred to as self-managing schools (Mestry, 2016), where decision-making powers are decentralised to role-players at the local level. Public schools with Section 21 functions can select their own suppliers instead of depending on the district office to purchase teaching materials for them and negotiate the quoted prices to minimise cost (Mestry, 2016). As determined by the National Norms and Standards for School Funding, the state allocation is deposited directly into the bank accounts of all public schools, and any unspent money for a current year-end is carried forward to the following year (Department of Basic Education [DBE], RSA, 2014). To ensure the effectiveness of financial management roles and responsibilities of SGBs, role-players who are tasked with financial management must have a clear understanding of financial management decision-making processes that should be used in schools. Establishing proper financial management processes contribute to the effective management of financial resources.

The National Norms and Standards for School Funding (NNSSF) provides a statutory basis for school funding which results in the classification of schools into those serving poor communities and those serving rich ones (DBE, RSA, 2014). The introduction of the Education Laws Amendment Act, No. 31 of 2007 (The Presidency, RSA, 2007), provides a legal directive for the Minister of Education to establish Quintile Norms and Minimum Standards for the funding of public schools (Mestry, 2013). Schools are divided into Quintiles 1 to 5. Quintile 1 and 2 schools are generally situated in rural and township areas; Quintile 3 schools serve township and middle-class areas and are declared no fee-paying schools. Quintiles 4 and 5 schools are located within affluent areas and are fee-paying schools (Mestry, 2016). Quintile 1, 2 and 3 schools are regarded as the poorest schools, and they receive nearly six times more subsidy per learner than the wealthier schools (Aina, 2017). This classification method is intended to rectify historical disparities in education (Dibete, 2015). The national table of targets for school funding was established to ensure an equal and fair distribution of state funds to public schools (Marishane, 2013:13). Sound knowledge of decision-making processes concerning school financial matters may reduce school disparities because it will lead to the effective and optimal use of available financial resources.

Conceptual Framework

The Powell (2008) model for decision-making was deemed relevant for the study and was used to provide a structure to guide the exploration of financial management duties among the relevant stakeholders at fee-paying public schools. Collaboration between different beneficial parties typically influences decision-making (Powell, 2008:388). Powell (2008) identifies four kinds of influence that are frequently part of decision-making: state domination, institutional autonomy, elite theory, and interest representation.

State domination. This type of influence could be described as the state or government's authority over an institution that operates through government instruments to frame policies that individual lower-level institutions implement (Powell, 2008). For this study, it could be described as the legal requirements stipulated by the Schools Act and other relevant legislation covering financial management duties in schools, to which schools must strictly adhere. This suggests that the actions of principals and SGBs are influenced by regulations and policies established by the DBE and Provincial Departments of Education. Understanding this legislation and the relevant policies contributes positively to effective and efficient financial management duties of the relevant role-players, which impacts schools.

Institutional autonomy is described by Kogan and Hanney (2000) as the power and authority given to institutions by central and provincial governments to make and implement their actions. For this study, it may be described as the power given to SGBs to govern schools and to principals to manage school affairs professionally. This indicates that principals and SGBs have power and influence when implementing their responsibilities. Appropriate usage of this power and influence over schools' financial assets assist schools in achieving their goals and satisfy stakeholders.

Elite theory maintains that mainstream power-holders may be differentiated from smaller power-holders. Etzioni-Havely (1993) believes that mainstream power-holders or elites effectively control power. They often make important decisions unilaterally, and smaller power-holders have no choice but to comply. This can be directly related to the findings in the research carried out by Mestry (2006), which suggests that principals are not always willing to relinquish the duties of school governance for fear of sacrificing their power. Hence, they deliberately withhold information related to school finances. Therefore, principals in these schools may be regarded as mainstream power-holders who make financial decisions without properly consulting other relevant stakeholders.

Interest representation refers to the actions to support bulk choices or majority interests in decision-making processes (Powell, 2008). It points to decision-making employing appropriate consultation and collaboration. In this study, interest representation can be related to the composition of the SGBs and their effective consultation and involvement in school financial management as prescribed by the Schools Act.

The concepts (state domination, institutional autonomy, elite theory, and interest representation) in Powell's (2008) model of decision-making are linked and influence one another even though they are distinct. For instance, by establishing policies that are intended to be implemented and to give direction to the pertinent stakeholders, states with a dominant position can influence decision-making. Institutional autonomy can influence decision-making by acting as a check on state domination because each institution has the freedom to conduct its own affairs and make decisions as it deems fit (Kogan & Hanney, 2000). State domination -(through Schools Act) and institutional autonomy (the power given to the principals and SGBs) can be viewed as tools used by the elites to influence decision-making. At the same time, interest representation is to ensure that different stakeholders' interests are considered when making decisions rather than just being dominated by the elites or the government.

Independent institutions may serve as a check on concentrated power, ensuring that choices are not entirely influenced by the desires of a small number of people or organisations.

Methodology

The research paradigm, research approach, research design, sampling technique, data collection methods, and data analysis are explained below to provide a road map of the methods and procedures used in this study.

Research Paradigm

A paradigm is a set of assumptions and guiding principles that influence how a researcher understands or sees the world (Kivunja & Kuyini, 2017). In order to have a better knowledge of the viewpoints and experiences of the participants about the financial management decision-making processes in schools, it was determined that an interpretative paradigm was more appropriate. An interpretive paradigm is a research paradigm that emphasises the understanding and interpreting of social phenomena from the participants' point of view (Creswell & Poth, 2018). An interpretative paradigm also helps to seek information to answer the research questions regarding what are truth/reality (ontology), and the nature of knowledge (epistemology) from the shared experiences of the participants (Creswell & Poth, 2018).

Research Approach

We used a qualitative research approach in this study. The primary goal of qualitative research is to understand what participants are saying (Babbie & Mouton, 2015) and attempt to obtain first-hand knowledge in the research setting (Neuman, 2011). Using a qualitative research approach allows the researcher to gather data directly from the source and understand the participants' points of view (Baxter & Jack, 2008; McMillan & Schumacher, 2014; Nieuwenhuis, 2007). Interaction between us and the participants provided a good understanding of financial management in public schools, and therefore, a qualitative research approach proved to be more suitable.

Research Design

An in-depth understanding of a difficult problem in a practical setting is achieved through the use of a case study research design (McMillan & Schumacher 2014). Multiple case studies encourage the investigation and examination of two or more cases in order to establish thorough, comprehensive, and understandable explanations of occurrences in their natural surroundings (Yin, 2016). Our research was to gain a comprehensive understanding of the phenomenon across many cases. Therefore, a multiple case study method was adopted by using a sample of four fee-paying Quintile 5 public primary schools in urban areas.

Data Gathering Techniques

Magaldi and Berler (2020) define a semi-structured interview as an exploratory interview that is normally based on a guide and is typically centred on a specific problem that gives a general pattern. We used semi-structured interviews because they provided the opportunity to delve deeper into exploring newly developing lines of inquiry that were specifically pertinent in the study (Nieuwenhuis, 2016). The impact of potential bias that can arise if only one method of data collecting is utilised was decreased by combining document analysis and semi-structured interviews (Nieuwenhuis, 2016).

Primary data were gathered using semi-structured interviews conducted on the schools' premises with the principals, chairpersons of SGBs and financial managers. Secondary data were obtained from documents, such as financial policies and the agendas of finance committee meetings of the participating schools. The data gathering was used to determine the financial management processes in the participating schools and the role of relevant role-players in financial management decision-making.

Sampling

Four fee-paying Quintile 5 public primary schools in an urban area in Pretoria were purposively sampled for this study. Purposive sampling is described as non-probability sampling where the units to be examined are carefully chosen based on the researcher' s thoughts concerning which ones would be most suitable or representative (Babbie, 2007).

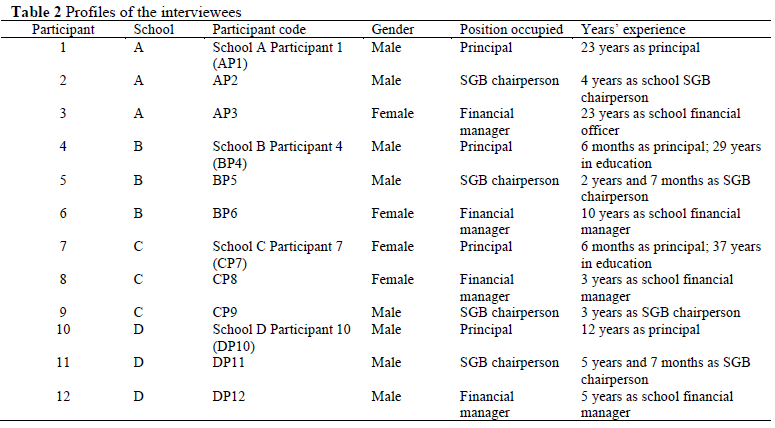

The schools selected were considered to have the potential to provide more information regarding financial management processes. The profiles of the participating schools and the interviewees are summarised in Tables 1 and 2 respectively.

Data Analysis

Thematic analysis is a technique for locating, examining, and deciphering meaningful patterns (or themes) within qualitative data (Clarke, Braun & Hayfield, 2015). The emphasis of the thematic analysis is on creating thorough and high-quality analyses; it has built-in quality controls such as a two-stage review process where prospective themes are evaluated against the coded data and the complete data set (Braun & Clarke, 2013). As such the data analysis in this study was done thematically using the process of systematically coding and categorising data into themes and sub-themes that emerged from the collected data to explain financial management processes in the participating schools. All the collected data were examined in thematic analysis to recognise common recurring events. The key themes are identified from all the opinions reflected in the data (Patton & Cochran, 2002).

Ethical Considerations

It is important and necessary for researchers to be fully aware of ethical and legal principles when conducting research to protect participants' rights and welfare (McMillan & Schumacher, 2014). The rights of the participants in this study were protected, and we ensured ethical responsibility by keeping relevant and applicable ethical issues in mind. We applied for and obtained permission from the Gauteng Department of Education to conduct semi-structured interviews in selected public primary schools in the Tshwane South district of the Gauteng province. We explained the aim and purpose of the study to each interviewee. They were informed that they were entitled to withdraw from the study at any point, that the allocation of pseudonyms would protect the information they provided and that their anonymity and confidentiality were guaranteed.

Findings

The data were analysed by coding the transcribed data into themes. Two themes that emanated from the data were, firstly, the factors that influenced financial management in public schools and, secondly, the factors that impacted the influence that individual role-players exerted on financial management decisions.

Theme 1: Factors that Influence Financial Management in Public Schools

The data revealed that the financial management process is influenced by the following factors: an understanding of regulations, like the Schools Act; the educational background of the SGB; and the financial skills and knowledge of those entrusted with the financial management of schools.

The participants demonstrated a good understanding of how their schools should manage their finances as prescribed by the Schools Act. The participants' expressed the following opinions:

I should think when you make use of, or you follow, the SASA [South African Schools Act], you may not have difficulty understanding financial management processes. My opinion on the guidelines is that they are straightforward and understandable. They articulate very clearly the expectation on the side of the institution as a school and also give direction on how to deal with finances in terms of having your own school finance policy and also gives assistance on how to give guidance to other people involved in school financial management. (AP3)

My opinion is that SASA [South African Schools Act - own insertion] is very clear on many matters relating to the management and decision-making with regards to finances at schools. There are very clear boundaries and it assists the school in using the schools' finances responsibly. (BP5)

My opinion is that I want to believe that SASA is very clear and helpful when it comes to how finances must be managed and how decisions should be made. You know principals are not accountants; I don't have any economic or business background so now SASA is stipulated in a way that you are given enough guidelines in terms of how you arrive on a decision that has to do with school finance. (CP7)

SASA, for me it's a working act; it must just be in place all the time, and each new stakeholder that comes on board must be made aware of it (DP10).

A sound understanding of the prescriptions of and required procedures in the Schools Act and its role in guiding financial management processes relates to "state domination" as described in Powell's model of decision-making. He explains "state domination" as a type of influence that government has over an institution and which operates through governmental instruments to frame policies or legislation that individual lower-level institutions are obliged to act upon (Powell, 2008). Along the same line, Wairima and Nasieka (2019) indicate that through financial management regulations and policies, government influences school financial management. The data in this study indicate that the participating schools understood the financial management processes prescribed in the Schools Act. This finding agrees with Maronga, Weda and Kengere's (2013) research findings that the majority of schools adhere to the Government Financial Regulations' suggested and approved financial management techniques. This, in turn, has a positive influence on the financial management responsibilities of the relevant stakeholders. However, this finding contrasts with the findings of Mestry (2006) that members of SGBs and school principals only had a slight awareness of the Schools Act, and that they often misinterpreted it, resulting in unprofessional financial management practices in their schools. This contradiction could be ascribed to the differences between the socio-economic contexts of the schools sampled in this study, compared to those sampled in Mestry's study.

In addition, the data support the view that if SGB members did not have sufficient knowledge of the educational environment and some financial skills, principals may influence them inappropriately as the principals are generally better informed on educational matters than the members of the governing body. A lack of financial knowledge or skills may contribute to financial mismanagement and ruin the budget.

Theme 2: Influence of Individual Role-players on Financial Management Decisions in Public Schools Nine of the 12 participants in the study suggested that the parent component of the SGB exerted great influence regarding the school' s financial management. Two participants believed that the school' s financial manager influenced financial decisions, and one participant maintained that all stakeholders influenced school financial management. The participants' responses included the following:

When it comes to making financial decisions, the SGB is the body that has power; then the finance committee and it will come down to the principal. However, I should think the SGB will be the overall decision-makers when it comes to financial matters. (AP3)

The SGB members are the custodians of the school; they look after the school, so they are the final decision-makers. The recommendations and proposals come from the finance committee, but it is the SGB that takes the financial decisions (BP5). The SGB is the highest authority in the financial management process. The SGB chairperson is one who has influence on financial decisions. Let me say the treasurer and the SGB chairperson because they are two different people. They also have some influence on major decisions because they are the ones who must go and sell the plans to the parents. The SGB members have a higher influence; they can actually say 'we hear you, but we don't agree.' (CP7)

The final say of how the money will be spent comes from the SGB. The SGB has the ultimate say on how the money would be spent (CP9). The SGB is the decision-maker of the finance concern of the school - that is our understanding. It is critical that the SGB influences finance decision-making because it sits between the parents and the management (DP12).

This finding is in line with the prescriptions of the Schools Act (sub-section 16A [2] [h]), which states that the principal must support the governing body in school financial matters by advising on issues related to financial decisions. The principals in the participating schools indicated that they supported their SGBs in carrying out their fiduciary responsibilities and that no decisions were reached without the full agreement of the SGB. This result conflicts with Mestry and Govindasamy' s (2013) assertion that principals typically do not create procedures for true teamwork to enable SGBs to take part in school governance. Karlsson (2002) further claims that due to principals' position of authority and the fact that they have first-hand access to information from educational authorities, principals continue to dominate meetings and decision-making. In the context of this study, principals' capacity to effectively incorporate the SGB parent component in the school's financial management was not an issue. However, some principals identified delays in the financial decision-making process due to parent members of the SGB responsible for the financial matters often were not available.

The school is very reliant on SGB members, who are not always as available as necessary for the smooth running of the finances of the school. Getting decision-making from SGB members timeously can become difficult and not in the school' s best interests. (AP1)

The availability of the SGB members is often the problem. The bigger problem is that the SGB members are not paid, and they are all full-time employees in most instances. Especially when you get professionals in your SGB members, their availability becomes the problem in decision-making processes. (CP3)

School financial managers are employed by governing bodies of schools to provide them with sound financial management expertise and support the governing body. Fee-paying schools that can afford to employ financial managers openly enjoy the benefits of having healthy budgeting processes, which, in turn, positively impact the schools' financial management processes. The poorer non-fee-paying public schools, whose governing bodies are less likely to be in a position to employ financial managers, do not have such benefits and, therefore, there is a greater risk of poor financial management.

School management teams must make recommendations on school governance, organisation and funding, but they need the support and approval of their respective governing bodies before expenses can be budgeted for and procurements made. This confirms that the power to make financial decisions is vested in the governing bodies of the participating schools - in accordance with Sections 21 and 36 to 44 of the Schools Act. Mahlangu (2005) believes that the primary purpose of having SGBs is to ensure that parents have greater influence on their children' s education. Rangongo (2011) affirms this view by stating that having parent members as a majority on the SGB indicates that the parent governors are expected to act in an effective and influential manner in managing school finances.

Evidently, all the relevant role-players in the financial management of the participating schools were allowed to become involved in financial management processes. Therefore, they influenced decisions through their contributions and input, ensuring effective financial responsibilities. It implies that the aim of decentralising schools' financial management by transferring the financial management responsibilities of public schools to SGBs has been achieved through effective stakeholder participation in school financial management - one of the fundamental expectations behind the introduction of the Schools Act (Khuzwayo, 2009).

Conclusion

A sound understanding of the South Africa Schools Act and other relevant laws is a key factor for effective financial management in a public school. We support the recommendation of previous studies that the DBE should, in terms of Section 19 of the Schools Act, provide frequent and relevant training to the relevant financial management of the role-players in schools.

Previous studies related to school financial management have concentrated on lower quintile schools situated in townships and rural areas. Some of these studies indicate that SGBs did not meet their financial responsibilities as prescribed by the Schools Act. Moving the focus from lower quintile schools and focusing on exploring financial management in higher quintile fee-paying schools in more affluent areas resulted in a far different picture, hence contributing to knowledge. These schools attract educated parents who are most influential in school financial management processes to serve on governing bodies. The study on which this paper is based confirmed that the relevant role-players' educational background and financial knowledge can influence the quality of financial management processes in schools. Therefore, it is important for policymakers and school stakeholders to advocate training and practices that can instruct school principals, financial officers, and parent governing bodies on how to improve financial decision-making, streamline procedures, and increase openness and accountability.

We also underscore that when a qualitative approach is used in research, findings must be weighed against the context in which the participants find themselves. A generalisation of findings must be limited to the participants and not to the general population. Hence, policymakers must be aware of the contextual variations in which public schools operate and must endeavour to make allowances for these contextual disparities. It is, thus, deemed essential that further studies related to financial management in schools should be conducted in other provinces of South Africa to obtain a more comprehensive understanding of the research topic.

Authors' Contributions

Both authors contributed equally to the introduction, literature review, conceptual framework, methodology, discussion and concluding sections.

Notes

i. This article is based on the master's thesis of Adebunmi Yetunde Aina.

References

Aina A 2017. Financial management decision-making processes in public primary schools. MEd dissertation. Pretoria, South Africa: University of Pretoria. Available at https://repository.up.ac.za/bitstream/handle/2263/65455/Aina_Financial_2017.pdf?sequence=1&isAllowed=y. Accessed 22 June 2020. [ Links ]

Androniceanu A & B Ristea 2014. Decision making process in the decentralized educational system. Procedia - Social and Behavioral Sciences, 149:37-42. https://doi.org/10.1016/j.sbspro.2014.08.175 [ Links ]

Babbie E 2007. The practice of social research (11th ed). Belmont, CA: Thomson Wadsworth. [ Links ]

Babbie E & J Mouton 2015. The practice of social research. Cape Town, South Africa: Oxford University Press. [ Links ]

Bagarette N 2012. Partnerships between SGBs and principals in public schools: Reasons for the failure of the partnerships. International Journal of Education Science, 4(2):97-106. https://doi.org/10.1080/09751122.2012.11890032 [ Links ]

Baxter P & Jack S 2008. Qualitative case study methodology: Study design and implementation for novice researchers. The Qualitative Report, 13(4):544-559. [ Links ]

Bhattacharya B 2013. Academy schools in England. Childhood Education, 89(2):94-98. https://doi.org/10.1080/00094056.2013.773845 [ Links ]

Bifulco R & Ladd HF 2006. Institutional change and coproduction of public services: The effect of charter schools on parental involvement. Journal of Public Administration Research and Theory, 16(4):553-576. https://doi.org/10.1093/jopart/muj001 [ Links ]

Botha RJ 2012. The role of the school principal in the South African school governing body: A case study of various members' perception. Journal of Social Science, 30(3):263-271. https://doi.org/10.1080/09718923.2012.11893003 [ Links ]

Braun V & Clarke V 2013. Successful qualitative research: A practical guide for beginners. London, England: Sage. [ Links ]

Clarke V, Braun V & Hayfield N 2015. Thematic analysis. In JA Smith (ed). Qualitative psychology: A practical guide to research methods (3rd ed). London, England: Sage. [ Links ]

Court M & O'Neill J 2011. 'Tomorrow's Schools' in New Zealand: From social democracy to market managerialism. Journal of Educational Administration and History, 43(2):119-140. https://doi.org/10.1080/00220620.2011.560257 [ Links ]

Creswell JW & Poth CN 2018. Qualitative inquiry and research design: Choosing among five approaches (4th ed). Thousand Oaks, CA: Sage. [ Links ]

Department of Basic Education, Republic of South Africa 2014. South African Schools Act (84/1996): Amended National Norms and Standards for School Funding. Government Gazette, 583(37230):1-4, January 17. Available at https://www.saflii.org/za/gaz/ZAGovGaz/2014/32.pdf. Accessed 25 November 2023. [ Links ]

Diamond L 2015. The role of parent members of school governing bodies in school financial management. MEd dissertation. Cape Town, South Africa: University of Cape Town. Available at https://open.uct.ac.za/server/api/core/bitstreams/6c05156b-6f92-417c-963e-977412857498/content. Accessed 24 November 2023. [ Links ]

Dibete KJ 2015. The role of the school governing bodies in managing finances in no-fee schools in the Maraba Circuit of Limpopo Province. MEd dissertation. Pretoria, South Africa: University of South Africa. Available at https://core.ac.uk/download/pdf/43177887.pdf. Accessed 25 November 2023. [ Links ]

Etzioni-Havely E 1993. The elite connection: Problems and potential of Western democracy. Cambridge, MA: Polity Press. [ Links ]

Karlsson J 2002. The role of democratic governing bodies in South African schools. Comparative Education, 38(3):327-336. https://doi.org/10.1080/0305006022000014188 [ Links ]

Khuzwayo O 2009. The role of parent governor in school financial management decision-making: The experiences of parent governor in Ndwendwe rural schools. MEd dissertation. Durban, South Africa: University of KwaZulu-Natal. [ Links ]

Kivunja C & Kuyini AB 2017. Understanding and applying research paradigms in educational contexts. International Journal of Higher Education, 6(5):26-41. https://doi.org/10.5430/ijhe.v6n5p26 [ Links ]

Kogan M & Hanney S 2000. Reforming higher education. London, England: Jessica Kingsley. [ Links ]

Koross PK, Ngware MW & Sang AK 2009. Principals' and students' perceptions on parental contribution to financial management in secondary schools in Kenya. Quality Assurance in Education, 17(1): 61 -78. https://doi.org/10.1108/09684880910929935 [ Links ]

Lekonyane BC & Maja FM 2014. Financial management of schools in the Ekurhuleni North District in Gauteng Province. In Proceedings of the First Asia-Pacific Conference on Global Business, Economics, Finance and Social Sciences (AP14Singapore Conference). Available at https://www.readkong.com/page/financial-management-of-schools-in-the-ekurhuleni-north-3727297. Accessed 25 November 2023. [ Links ]

Magaldi D & Berler M 2020. Semi-structured interviews. In V Zeigler-Hill & TK Shackelford (eds). Encyclopedia of personality and individual differences. Cham, Switzerland: Springer. https://doi.org/10.1007/978-3-319-24612-3_857 [ Links ]

Mahlangu VP 2005. The relationship between the school principal and the school governing body. PhD thesis. Pretoria, South Africa: University of Pretoria. Available at https://repository.up.ac.za/bitstream/handle/2263/23178/00thesis.pdf?sequence=1&isAllowed=y. Accessed 24 November 2023. [ Links ]

Marishane RN 2013. Management of school infrastructure in the context of a no-fee school policy in rural South African schools: Lessons from the field. International Journal of Education Policy & Leadership, 8(5):1-13. Available at https://files.eric.ed.gov/fulltext/EJ1016289.pdf. Accessed 24 November 2023. [ Links ]

McMillan J & Schumacher S 2014. Research in education: Evidence based inquiry (7th ed). Harlow, England: Pearson Education Limited. [ Links ]

Mestry R 2004. Financial accountability: The principal or the school governing body? South African Journal of Education, 24(2):126-132. Available at https://www.ajol.info/index.php/saje/article/view/24977. Accessed 23 November 2023. [ Links ]

Mestry R 2006. The functions of school governing bodies in managing school finances. South African Journal of Education, 26(1):27-38. Available at https://www.sajournalofeducation.co.za/index.php/saje/article/view/67/63. Accessed 23 November 2023. [ Links ]

Mestry R 2013. A critical analysis of legislation on the financial management of public schools: A South African perspective. De Jure, 46(1):162-177. Available at https://journals.co.za/doi/epdf/10.10520/EJC136268. Accessed 23 November 2023. [ Links ]

Mestry R 2016. The management of user fees and other fundraising initiatives in self-managing public schools. South African Journal of Education, 36(2):Art. # 1246, 11 pages. https://doi.org/10.15700/saje.v36n2a1246 [ Links ]

Mestry R & Govindasamy V 2013. Collaboration for the effective and efficient management of school financial resources. Africa Education Review, 10(3):431-452. https://doi.org/10.1080/18146627.2013.853539 [ Links ]

Mestry R & Hlongwane S 2009. Perspectives on the training of school governing bodies: Towards an effective and efficient financial management system. Africa Education Review, 6(2):324-342. https://doi.org/10.1080/18146620903274654 [ Links ]

Mncube V 2009. The perception of parents of their roles in the democratic governance of schools in South Africa: Are they on board? South African Journal Education, 29(1):83-103. https://doi.org/10.15700/saje.v29n1a231 [ Links ]

Moloi K 2007. An overview of education management in South Africa. South African Journal of Education, 27(3):463-476. Available at https://www.sajournalofeducation.co.za/index.php/saje/article/view/113/34. Accessed 23 November 2023. [ Links ]

Neuman WL 2011. Social research methods: Qualitative and quantitative approaches (7th ed). Boston, MA: Allyn and Bacon. [ Links ]

Nieuwenhuis J 2007. Qualitative research designs and data gathering techniques. In K Maree (ed). First steps in research. Pretoria, South Africa: Van Schaik. [ Links ]

Nieuwenhuis J 2016. Qualitative research designs and data gathering techniques. In K Maree (ed). First steps in research (2nd ed). Pretoria, South Africa: Van Schaik. [ Links ]

Patton MQ & Cochran M 2002. A guide to using qualitative research methodology. London, England: Medecins Sans Frontieres. [ Links ]

Powell B 2008. Stakeholders' perception of who influence the decision-making processes in Ontario's public postsecondary education institutions. Higher Education Research & Development, 27(4):385-397. https://doi.org/10.1080/07294360802406841 [ Links ]

Rangongo P, Mohlakwana M & Beckmann J 2016. Causes of financial mismanagement in South African public schools: The views of role-players. South African Journal of Education, 36(3):Art. # 1266, 10 pages. https://doi.org/10.15700/saje.v36n3a1266 [ Links ]

Rangongo PN 2011. The functionality of School Governing Bodies with regard to the management of finance in public schools. MEd dissertation. Pretoria, South Africa: University of Pretoria. Available at https://repository.up.ac.za/bitstream/handle/2263/27257/dissertation.pdf?sequence=1&isAllowed=y. Accessed 23 November 2023. [ Links ]

Republic of South Africa 1996. Act No. 84, 1996: South African Schools Act, 1996. Government Gazette, 377(17579), November 15. [ Links ]

Reyes AH & Rodriguez GM 2004. School finance: Raising questions for urban schools. Education and Urban Society, 37(1):3-21. https://doi.org/10.1177/0013124504268103 [ Links ]

The Presidency, Republic of South Africa 2007. Act No. 31, 2007: Education Laws Amendment Act, 2007. Government Gazette, 510(30637), December 31. [ Links ]

Wairima SN & Nasieku T 2019. Factors affecting financial management effectiveness in public secondary schools in Kenya: A case of Gatanga sub-county. International Journal of Management and Commerce Innovations, 6(2): 123-143. Available at https://www.researchpublish.com/papers/factors-affecting-financial-management-effectiveness-in-public-secondary-schools-in-kenya-a-case-of-gatanga-sub-county. Accessed 21 November 2023. [ Links ]

Yin RK 2016. Qualitative research from start to finish (2nd ed). New York, NY: Guilford Press. [ Links ]

Received: 11 May 2019

Revised: 12 May 2023

Accepted: 15 July 2023

Published: 30 November 2023

{kind=link}

{kind=link}