Services on Demand

Article

English (pdf)

English (pdf)

Article in xml format

Article in xml format Article references

Article references

Indicators

Related links

-

Cited by Google

Cited by Google -

Similars in Google

Similars in Google

Share

Permalink

PermalinkSouth African Journal of Education

On-line version ISSN 2076-3433

Print version ISSN 0256-0100

S. Afr. j. educ. vol.40 n.1 Pretoria Feb. 2020

http://dx.doi.org/10.15700/saje.v40n1a1658

ARTICLES

Management capability in a structural modelling of the quality of economics and accounting education in Indonesia

Oding SupiadiI; MutrofinII

IDepartment of Education, Faculty of Teacher Training and Education, University of Singaperbangsa, Karawang, Indonesia

IIDepartment of Education, Faculty of Teacher Training and Education, University of Jember, Jember, Indonesia mutrofin.fkip@unej.ac.id

ABSTRACT

The research reported on in this article was motivated by the absence of modifications to A model for the study of classroom teaching proposed by Dunkin and Biddle in 1974. In this paper we aim to provide revision input to A model for the study of classroom teaching by adding management capability to the group of school community context. The research examined the suitability of structural equation modelling between managerial capability and the quality of economic and accounting education based on the data, as well as the effect of managerial capability on the quality of economic and accounting education. The research instrument consisted of two inventory sets that were valid and reliable. The validity and reliability of items were tested using Cronbach's Alpha (Alpha Cronbach's = .89 and .87; R = .78 and R = .82). Data was collected from 150 principals and 150 economics and accounting teachers. Based on the analysis using the linear structural relations (LISREL) 8.80 version, the results of the study show that: 1) the structural equation model of managerial capability, including managing schools and performing management functions, managing human resources and educational personnel, and managing the learning process, can be used to estimate, predict, or explain the quality of economic and accounting education; 2) managerial capability has a significant effect on the quality of economic and accounting education in schools. Based on these findings, management capability can be included as a revision of A model for the study of classroom teaching.

Keywords: managerial capability; quality of economic and accounting education

Introduction

More than four decades since being proposed by Dunkin and Biddle in 1974, A model for the study of classroom teaching, has never been revised or modified. This model consisted of presage variables, context variables, process variables, and product variables. The revision or modification in question was to include management capability in the context or process variables, specifically in the group of school community context other than climate, ethnic composition, bussing, and school size. Even when Schulman (1986) formulated a synoptic map of research on process-product research-based teaching, the classroom processes group also did not include management capability. In fact, from a contemporary perspective, the time has come to apply total quality management (TQM) from economics and business to the education process. TQM focuses on achieving quality that can be defined as philosophy or principles intended to meet the needs and expectations of internal and external customers (Bradley, 1993; Greenwood & Gaunt, 1994; Herman, 1993; Pike & Barnes, 1996).

TQM has been implemented in the education sector in Indonesia since 2001, based on a package of policies - the so-called school-based quality improvement management (Manajemen peningkatan mutu berbasis sekolah - MPMBS) (Depdikbud, 2001). The policy was introduced to respond to quality-related educational problems, which various stakeholders, either from the community or business leaders from the world of work, complained about. The continuous development of this policy may have had a significant impact (Arcaro, 1995; Sallis, 2014) over the years. Including quality in the educational agenda means caring for customers' goals, needs, desires, and interests, as well as ensuring that these can be met (Whitaker & Moses, 1993).

This study focused on exploring the absence of any revisions or modifications to A model for the study of classroom teaching by incorporating management capability as a variable, and to provide alternative revision input for this model. The study, therefore, started with examining the suitability of structural equation modelling between managerial capability and the quality of economic and accounting education. If both were proven suitable, it would be sufficient reason to include the management factor as a variable into A model for the study of classroom teaching.

One of the most difficult economic problems that developing countries struggle with is the prevalence of corruption, for which the only solution is good governance. Good governance can only be achieved if quality economic education and accounting graduates are delivered, because it depends on them to enhance professional responsibility in the field of economic management and accounting. That can only be achieved if the managerial capabilities of school principals were applied to economic education and accounting in schools.

Instructional Quality

Since the quality of education needs to be continuously improved, there is currently great interest in applying the philosophy of quality management in the education sector. All processes in organisations, which include educational organisations, contribute directly or indirectly to the quality of the product as defined by the customer (Omachonu & Ross, 2007). Applying the principle of quality to the education sector means that the learning process needs to be assessed to determine quality as defined by learners; it will determine whether or not the needs of learners are met (Arcaro, 1995).

The learning process, as described by Arcaro (1995) covers a variety of subjects including Economics and Accounting. Calvert, Kurji and Kurji (2011) critically argue that in the study of economic and accounting education, many parties neglect students' perceptions, both in the context of learning and in their own learning process.

The results of a study conducted by Steyn (2000) show that students' perceptions about the quality of management affected the quality of economic and accounting learning outcomes. Arcaro (1995) points out that if the principles of quality were applied in a serious and sustainable manner, it will successfully improve the quality of learning outcomes, including those in economics and accounting education. This concurs with the results of Sallis's (2014) study in which quality test instruments were applied in a number of schools in the United Kingdom (UK), resulting in continuous learning quality.

The results of a study conducted by Lee and Hung (2009) show that retention in accounting education had improved, and that the inclusion of whole brain instruction in accounting learning models resulted in the effective long-term retention of accounting information.

Abraham (2006) examined students' perceptions on the learning of accounting in relation to teaching contexts, learning approaches, and learning outcomes. The results show that when the appropriate teaching style was adopted, six key areas, namely, a positive learning milieu, good teaching methods, clear and standard teaching objectives, suitable work loads of teachers (instructors), the use of an appropriate assessment system, and an emphasis on learners' independence, had a positive effect on accounting-learning outcomes. This research is interesting because of the links between teaching context and the approach to learning and outcomes thereof.

However, not all researchers agree. Research conducted by Abraham (2006), Arcaro (1995), Lee and Hung (2009), Sallis (2014), and Steyn (2000) was in response to research by Calvert et al. (2011) about the importance of capturing student perception data in economic education and accounting research. These studies only analysed learning material variables, learning methods, learning styles, student personality types and did not address how the managerial role performed by the principal influenced the economics and accounting learning process. In developed countries, principals' managerial roles may be of little importance in subject teaching because all teachers perform their professional functions, and school principals are recruited in a professionally and institutionalised manner. However, in many developing countries the managerial role of the principal is still lacking. Therefore, research on the managerial role of the principal becomes important. This is especially true in Indonesia where being principal of a school is merely an additional task for a teacher who has not been recruited as such in a professional and institutionalised manner.

Managerial Capability

In Indonesia, the implications and application of results of studies in this regard have not resulted in the improvement of the quality of economics and accounting education in schools. A synthesis of the results of such studies indicated a need for modification of A model for the study of classroom teaching, which, to date, has been embraced by incorporating management capabilities, i.e. the managerial capability of managers, into the education sector (Armstrong, 2011; Donnelly, Gibson & Ivancevich, 1997; Juran, 2003). The rationale for such a modification is simple; no matter how good the input, context, and process variables are, a quality learning product will not be obtained if it is not managed well.

Good management can only be performed by highly capable educational managers. The inclusion of management variables in A model for the study of classroom teaching was in line with the policy of MPMBS and regulation 13 by the minister of National Education of the Republic of Indonesia, 2007, on the Standards of Principals in Public/Islamic Schools. These regulations include managerial competences in addition to personality, entrepreneurship, supervision, and social competences as a factor in improving educational outcomes.

This study aimed at examining the suitability of the structural equation model of managerial capabilities, namely managing schools and performing management functions, managing human resources and educational personnel, and managing the learning process, to evaluate the quality of economic and accounting education, as well as investigating the effect of managerial capability on the quality of economic and accounting education in schools.

The education manager is an individual who is responsible for efforts to achieve the goals of the educational organisation, of which schools are one type (Knezevich, 1990; Lunenburg & Ornstein, 2011). By definition, a headmaster can be considered to be an education manager. According to Donnelly et al. (1997) managers have three common managerial tasks: 1) managing the organisation and work, 2) managing people, and 3) managing production and operating systems.

The first task focuses on organisational management and includes teacher and employee productivity, the quality of work life, job pressure, career advancement, delegation (Armstrong, 2011), psychological contract (Guzzo & Noonan, 1994), occupational relationships (Kessler & Undy, 1996), as well as transactional and relational contracts (MacNeil, 1985; Rousseau & Wade-Benzoni, 1994).

The second task is to manage education personnel (teachers and educational support staff) as well as a number of children who are entrusted to the school by their parents to be educated and taught about science, technology, art, and religion. The vital capability required for this task is communication skills. Armstrong (2011), indicates that managers spend most of their time talking to employees and listening to their ideas, and that good managers listen more than they speak.

The third task is to manage learning. Learning is a unique and complex process (Wittrock, 1986). Therefore, we argue that adequate managerial capability is needed and must be mastered by every education manager.

The tasks performed by the education manager require certain professional capabilities. Based on Juran's (2003) theory about the relational pattern between managerial leadership and the resulting quality, capability has been used as an independent variable in this study. Juran's (2003) proposed theory has been known as the 85/15 Rule, which proposes that 85 percent of the quality problems encountered in an organisation are the result of poor design and management processes. Thus, the correct design and implementation of the system will result in the production of the desired quality. According to Juran, 85 percent of quality problems result from management as management has 85 percent control over an organisational system.

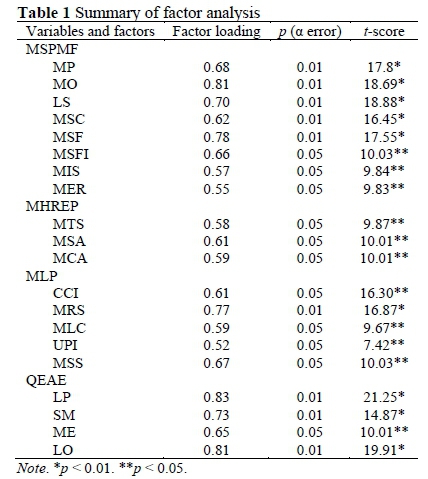

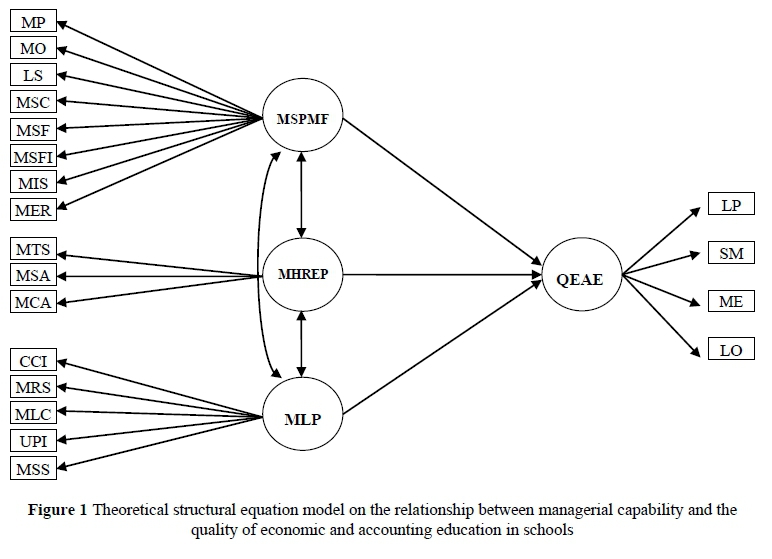

An elaboration of Donnelly et al.'s (1997) thoughts on managerial tasks, Juran's (2003) theory on management responsibilities, and managers' communication skills (Armstrong, 2011) produces a synthesis of educational managers' capabilities with three major indicators: 1) managing schools and performing management functions (MSPMF) (consisting of eight constructs); 2) managing human resources and educational personnel (MHREP) (consisting of three constructs); and 3) managing the learning process (MLP) (consisting of five constructs). The primary object of this study was to determine the effect of managerial capability on the quality of economic and accounting education (QEAE) (consisting of four constructs). The structural equation model of the variables in this study is represented in Figure 1.

The abbreviations in Figure 1 are explained below:

MSPMF: Managing schools and performing management functions.

MP: Managing school planning for various levels of planning.

MO: Managing school organisations as needed.

LS: Leading schools and optimum utilisation of school resources.

MSC: Managing school change and development toward effective learning organisations.

MSF: Managing school facilities and infrastructure for optimum utilisation.

MSFI: Managing school finance in accordance with accountable, transparent, and efficient principles.

MIS: Managing information systems in favour of formulating programmes and making decisions.

MER: Monitoring, evaluating, and reporting the implementation of programmes in schools using appropriate procedures, as well as planning next steps.

MHREP: Managing human resources and educational personnel.

MTS: Managing teachers and staff to optimally utilise human resources.

MSA: Managing students in the context of acceptance, placement, and capability development.

MCA: Managing school administration in favour of achieving school goals.

MLP: Managing the learning process.

CCI: Creating a conducive and innovative school culture and climate for students' learning.

MRS: Managing a relationship between schools and community in order to find support, ideas, learning resources, and school financing.

MLC: Managing learning curriculum and activity development in accordance with national education goals and objectives.

UPI: Utilising the progress of information technology for the improvement of learning and management.

MSS: Managing the school's specific service units to support teaching and learning activities at schools.

QEAE: The quality of economic and accounting education.

LP: Learning planning.

SM: Selection of learning methods.

ME: Management of learning evaluation.

LO: Learning outcomes.

Method

The study was conducted using a survey research design. The survey for data collection was conducted in the even semesters of 2016/2017, while data analysis was performed in the odd semesters of 2017/2018. A set of questionnaires was distributed in 27 regencies/cities, covering 625 sub-districts of the West Java province, Indonesia.

The population for this study consisted of two groups: a group of principals and a group of economics and accounting teachers. The first group included 441 principals of Senior High School (SHS) (Sekolah Menengah Atas [SMA]) and 406 of Vocational High School (VHS) (Sekolah Menengah Kejuruan [SMK]) - a total of 847 principals. The second group consisted of 488 economics and accounting teachers from SHSs and 634 from VHSs - a total of 1,122 teachers. The study applied a probability sampling technique with a random proportional method using a random number (Cochran, 1977) based on the origin of school (SHS and VHS). The population did not exceed 2,000 participants, so the Harry King Nomogram method (Leedy & Ormrod, 2015) was chosen to determine the size of the representative sample.

Using the method with a sampling error rate of .02, the representative sample consisted of 80 principals of SHSs and 84 of VHSs; 77 economics and accounting teacher of SHSs and 73 of VHSs. Thus, the total sample consisted of 164 principals and 150 teachers. For the purposes of analysis, the two groups were equalled to 150 participants each. Of the 400 questionnaires distributed, only 344 were returned (a response rate of 86%). Based on the completeness of the data, only 300 questionnaires could be analysed (150 completed by principals and 150 completed by teachers).

Two sets of data collection instruments were used in the study - questionnaires distributed among principals to collect data on managerial capability, and questionnaires distributed among economics and accounting teachers to collect data concerning the quality of economics and accounting learning.

In this study, questionnaires with a rating scale developed by Buckingham and Clifton (2001) of the Gallup Organization was used. The model contains various statements as indicators of managerial capabilities for principals and the quality of economics and accounting learning for teachers with a range of answer choices from 1 (Disagree) to 9 (Profoundly agree). Principals and teachers were asked to assess themselves using choices 1 to 9 to respond to each statement. The total score indicates the strong or weak managerial capabilities of principals and the strong or weak quality of economics and accounting learning according to teachers.

The validity of the instrument, i.e. content validity and construct validity, was based on confirmatory factor analysis using LISREL 8.80 (copyright of the researcher). The results are summarised in Table 1.

The reliability of the instrument was measured for its internal consistency by using Cronbach's Alpha. However, the data analysis was carried out using the structural equation model of multiple regression analysis (James, Mulaik & Brett, 1982) with the LISREL software 8.80 version (Jӧreskog & Sӧrbom, 2001). Therefore, the reliability of each instrument applied to the item, i.e., the correction of attenuation (underestimated) resulted from the imperfect reliability of measurement, has automatically been achieved.

In the data analysis, the main variables were positioned as constructs (factors), and the items served as indicators of the measured constructs. Therefore, the resulting regression coefficient was on a true score scale, which was free from the influence of less reliable measurement instruments. The assumption is that the measurement of education only shows its manifest or its indicator, which is not the same as the direct relationship of volume, monetary value, stock prices, et cetera, in business economics (Slavin, 2009).

The data used for the purposes of analysis in this study was the primary data collected from the questionnaires distributed to principals and economics and accounting teachers.

This research was conducted with permission from the Head of the Regional Office of the Education and Culture Office of West Java Province and the Ministry of Education and Culture of the Republic of Indonesia.

Hypothesis

Based on the theoretical framework above, the hypothesis of the study can be formulated as follows.

H1: There is a fit model of the structural equation for managerial capability and the quality of economics and accounting education in schools.

H2: The managerial capability of education managers affects the quality of economic and accounting education in schools.

Results

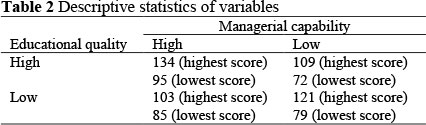

Based on the results of the data scanning and analysis of 150 questionnaires that were feasible for analysis, the data was divided into two groups, namely, that of education managers with high managerial capabilities of 65% (97.5, rounded to 98 principals) and those with low managerial capabilities of 35% (52.5, rounded to 52 principals).

The theoretical scores that were feasible for analysis for the quality of economic and accounting education among from 150 respondents ranged from the lowest of 72 to the highest of 134. The descriptive analysis showed a unique variation of data (see Table 2).

Variation in the data will, certainly, affect the hypothesis test if the difference is actually significant. To determine the difference in variation between the cells, the Tukey test was carried out. The results of the Tukey test (Q) show that the coefficient was 0.93 and the critical price Q was 2.26. H0 was accepted, so it can be stated that the unique variation was not significantly different.

The first stage of analysis conducted was to examine the alternative hypothesis 1 (H1), i.e. to test the fit of the structural equation model for the managerial capability and the quality of economic and accounting education in the schools. The suitability of the theoretical model with the data could be determined by using a goodness of fit referring to the value of Chi square (χ2). If the value of Chi square (χ2) was less than the critical value according to the degree of freedom with the probability of alpha error greater than 0.05 (p > 0.05), then H0 was accepted. This means that suitability existed between the structural equation model and the data collected (Jӧreskog & Sӧrbom, 2001). The summary of Chi square results (χ2) for this study is presented in Table 3.

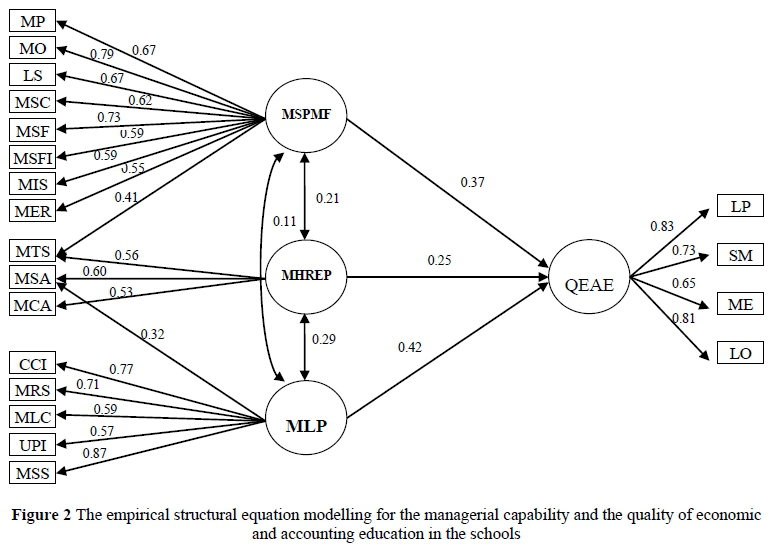

As the model was appropriate, in the second phase analysis we examined the model parameters, so that a decision could be made on how the independent variable (managerial capabilities) affected the dependent variable (the quality of economic and accounting education).

The first stage analysis showed that the value of Chi square (χ2) was 67.87 with p (α error) of .097, indicating that the effect was not significant. H0 thus indicated no difference in the covariance matrix obtained from data, meaning that the expected model could be accepted. This means that the theoretical structural equation model for managerial capabilities of education managers, i.e. managing schools and performing management functions (MSPMF), managing human resources and educational personnel (MHREP), and managing the learning process (MLP), was accepted and can be used to estimate or predict and explain the quality of economic and accounting education in the schools (QEAE).

However, the theoretical model was corrected (modified) as two factors were also indicators of the two main variables, i.e. MTS being added as an indicator of MHREP and MSPMF, and MSA being added as an indicator of MHREP and MLP. The results of model correction without changing the original theoretical model are represented in Figure 2.

The second analysis stage was to test the alternative hypothesis 2 (H2), i.e. to examine whether or not the managerial capabilities of the education managers simultaneously affected the quality of economics and accounting learning outcomes in schools. Based on the LISREL 8.80 output, the simultaneous effect of the dependent variable on the independent variable can be seen from several things, including the significance of the path coefficient (γ) of each variable, the regression coefficient (beta matrix), the Chi square contingency coefficient (χ2), or from the coefficient of structural parameters which connects one endogenous variable to another (α). The summary of hypothesis 2 (H2) test results is presented in Table 4.

Discussion

The results of the alternative hypothesis 1 (H1) test show that the structural equation model for the managerial capabilities of education managers could be used to explain the quality of economic learning and accounting in schools. The model was by no means contradictory to A model for the study of classroom teaching (Dunkin & Biddle, 1974; Schulman, 1986; Wittrock, 1986), but complimentary with the inclusion of the management variable as a correlate feasible to be taking into account. This means that any variables to be addressed in the context of improving the quality of economic and accounting education will not deliver the expected quality outcomes if management factors, particularly the managerial capabilities of education managers (principals), are not addressed.

The result of the alternative hypothesis 2 (H2) test show that the managerial capabilities of education managers (principals), i.e. those managing schools and performing the management functions, managing human resources and education personnel, and managing the learning process, had a positive effect on the quality of economics and accounting learning in schools. This means that the higher the managerial capabilities of the education managers, the higher the quality of economics and accounting learning in the schools. The results of the study were consistent with Juran's (2003) theory on management responsibility, Donnelly et al.'s (1997) theory on a manager's main job, Armstrong's (2011) theory on communication capability required by a manager, and the results of Steyn's (2000) study about the quality management model in learning. The results were also in line with similar studies focusing on the effect of input, context, process, and outcome variables as cited in this article.

Conclusion and Recommendations

Based on the results of this study, it can be concluded that the structural equation model of managerial capabilities could be used to estimate, predict, or explain the quality of economic and accounting education in the schools, and that the managerial capabilities of education managers affected the quality of economic and accounting education in the schools. This means that management factors can be included in A model for the study of classroom teaching as commonly theorised by Dunkin and Biddle (1974).

It is thus recommended that the strengthening of the managerial capabilities of education managers, principals in particular, should be done in a programmed and sustainable manner. Further study should be conducted on managerial capabilities with other indicators such as entrepreneurship and supervision, to support a further revision or modification of A model for the study of classroom teaching by including management factors.

For economics and accounting learning practices in schools in developing countries such as Indonesia, the inclusion of management factors in A model for the study of classroom teaching will have a major impact. Competency in economics and accounting learning has increased, which, in turn is suspected to affect good governance resulting in a positive effect on economic progress.

Authors' Contributions

Oding Supriadi was the lead researcher who conducted the instrument, interviews data collection. Mutrofin worked on the literature review, data analysis of statistics and the conclusion of the article. Nuriman examined the translation from Indonesian into English. All authors reviewed the final manuscript.

Notes

i. Published under a Creative Commons Attribution Licence.

References

Abraham A 2006. Teaching and learning in accounting education: Students' perceptions of the linkages between teaching context, approach to learning and outcomes. In RH Juchau & G Tibbits (eds). Celebrating accounting. Penrith South, Australia: University of Western Sydney. [ Links ]

Arcaro JS 1995. Quality in education: An implementation handbook. Delray Beach, FL: St. Lucie Press. [ Links ]

Armstrong M 2011. Armstrong's handbook of strategic human resource management (5th ed). London, England: KoganPage. [ Links ]

Bradley LH 1993. Total quality management for schools. Lancaster, PA: Technomic Publishing. [ Links ]

Buckingham M & Clifton DO 2001. Now, discover your strengths. New York, NY: The Free Press. [ Links ]

Calvert V, Kurji R & Kurji S 2011. Service learning for accounting students: What is faculty role? Research in Higher Education Journal, 10:1-11. Available at http://citeseerx.ist.psu.edu/viewdoc/download?doi=10.1.1.470.1870&rep=rep1&type=pdf. Accessed 5 January 2020. [ Links ]

Cochran WG 1977. Sampling techniques (3rd ed). New York, NY: John Wiley & Sons. [ Links ]

Departemen Pendidikan dan Kebudayaan (Depdikbud) RI 2001. Manajemen peningkatan mutu berbasis sekolah [School-based quality improvement management]. Jakarta, Indonesia: Ditjen Dikdasmen. [ Links ]

Donnelly JH Jr, Gibson JL & Ivancevich JM 1997. Fundamentals of management. Homewood, IL: Richard D. Irwin. [ Links ]

Dunkin MJ & Biddle BJ 1974. The study of teaching. New York, NY: Holt, Rinehart, and Winston. [ Links ]

Greenwood MS & Gaunt HJ 1994. Total quality management for schools. London, England: Cassell. [ Links ]

Guzzo RA & Noonan KA 1994. Human resource practices as communication and psychological contract. Human Resource Management, 33(3):447-462. https://doi.org/10.1002/hrm.3930330311 [ Links ]

Herman JJ 1993. Holistic quality: Managing, restructuring, and empowering schools. Newbury Park, CA: Corwin Press. [ Links ]

James LR, Mulaik SA & Brett JM 1982. Causal analysis: Assumptions, models, and data. Beverly Hills, CA: Sage. [ Links ]

Jӧreskog K & Sӧrbom D 2001. LISREL 8: User's reference guide. Lincolnwood, IL: Scientific Software International. [ Links ]

Juran JM 2003. Juran on leadership for quality: An executive handbook. New York, NY: Free Press. [ Links ]

Kessler S & Undy R 1996. The new employment relationship: Examining the psychological contract. London, England: Institute of Personnel and Development. [ Links ]

Knezevich SJ 1990. Administration of public education: A sourcebook for the leadership and management of educational institutions (5th ed). New York, NY: Harper & Row. [ Links ]

Lee LT & Hung JC 2009. Effect of teaching using whole brain instruction on accounting learning. International Journal of Distance Education Technologies, 7(3):63-84. https://doi.org/10.4018/jdet.2009070104 [ Links ]

Leedy PD & Ormrod JE 2015. Practical research: Planning and design (11th ed). Harlow, England: Pearson Education Limited. [ Links ]

Lunenburg FC & Ornstein AC 2011. Educational administration: Concepts and practices. Australia: Wadsworth, Cengage Learning. [ Links ]

MacNeil IR 1985. Relational contract: What we do and do not know. Wisconsin Law Review, 4:483-526. [ Links ]

Ministery of National Education of the Republic of Indonesia 2007. Regulation of the Number 13 Year 2007 on the standards of principal in public/Islamic schools. Jakarta, Indonesia: Depdiknas. [ Links ]

Omachonu VK & Ross JE 2007. Principles of total quality (3rd ed). Boca Raton, FL: CRC Press. [ Links ]

Pike J & Barnes R 1996. TQM in action: A practical approach to continuous performance improvement (2nd ed). London, England: Chapman & Hall. [ Links ]

Rousseau DM & Wade-Benzoni KA 1994. Linking strategy and human resource practices: How employee and customer contracts are created. Human Resource Management, 33(3):463-489. https://doi.org/10.1002/hrm.3930330312 [ Links ]

Sallis E 2014. Total quality management in education (3rd ed). New York, NY: Routledge. [ Links ]

Schulman LS 1986. Paradigms and research programs in the study of teaching: A contemporary perspective. In MC Wittrock (ed). Handbook of research on teaching (3rd ed). New York, NY: Macmillan. [ Links ]

Slavin RE 2009. Educational psychology: Theory and practice (9th ed). Upper Saddle River, NJ: Pearson Education. [ Links ]

Steyn GM 2000. Applying principles of total quality management to a learning process: A case study. South African Journal of Higher Education, 14(1):174-184. Available at https://journals.co.za/docserver/fulltext/high/14/1/high_v14_n1_a20.pdf?expires=1578232449&id=id&accname= guest&checksum=0A750AAF5FC4093F65AF0036CFAB7CF5. Accessed 5 January 2020. [ Links ]

Whitaker KS & Moses MC 1993. The restructuring handbook: A guide to school revitalization. Needham Heights, MA: Allyn and Bacon. [ Links ]

Wittrock MC (ed.) 1986. Handbook of research on teaching (3rd ed). New York, NY: Macmillan. [ Links ]

Received: 8 November 2017

Revised: 12 December 2018

Accepted: 15 July 2019

Published: 29 February 2020.

{kind=link}

{kind=link}

{kind=link}