Services on Demand

Article

English (pdf)

English (pdf)

Article in xml format

Article in xml format Article references

Article references

Indicators

Related links

-

Cited by Google

Cited by Google -

Similars in Google

Similars in Google

Share

Permalink

PermalinkSouth African Journal of Education

On-line version ISSN 2076-3433

Print version ISSN 0256-0100

S. Afr. j. educ. vol.38 n.2 Pretoria May. 2018

http://dx.doi.org/10.15700/saje.v38n2a1447

ARTICLES

Novice rural principals' successful leadership practices in financial management: Multiple accountabilities

Phumlani Erasmus MyendeI; Michael Anthony SamuelII; Ansurie PillayIII

IEducational Management and Policy Studies, Faculty of Education, University of Pretoria, Pretoria, South Africa phumlani.myende@up.ac.za

IIEducational Studies, School of Education, University of KwaZulu-Natal, Durban, South Africa

IIILanguage and Arts Education, School of Education, University of KwaZulu-Natal, Pinetown, South Africa

ABSTRACT

Research studies on financial management in South African public schools expands recurrent literature, most of which have largely pathologised school leadership and management, and rural schools in particular. This article instead draws from a qualitative case study of success, which examined how five novice principals in a rural setting went beyond the prescriptive administrative requirements to generate context-responsive and creative ways of managing school finances, working with the parent community, with educational peers and the departmental policies to activate situated relevant governance relations. The data is drawn from interviews and documents produced within the setting. Our findings reveal a new set of accountability relations, which counter the hierarchical relations between schools and the community, or between the department and the rural context. These principals began a trajectory of overt training in financial management to ensure their own and collaborating participants' clarity and involvement in a participative management approach. Whilst the school-formulated policies serve as a backdrop to the terms of operations, these principals generate multiple accountabilities in their role as chief financial officers. The study recognises vertical, horizontal and downward accountabilities, which are underpinned by self-driven motivation, moral integrity and social developmental responsibilities. Rather than being a pathological problem, school financial management offers policy and practice potential to develop co-responsible governance.

Keywords: financial management; financially accountability; multiple accountabilities; novice principals; school finances; successful schools

Introduction

The causes of financial mismanagement in public schools, as revealed in a recent South African article (Rangongo, Mohlakwana & Beckmann, 2016), note a recurring research concern: what explains the failure? This article does not provide a new story about financial management in South African schools. Instead, it reassesses a long list of research presenting a one-side and negative discourse about financial management in South African schools and rural schools in particular (Bhengu & Ncwane, 2014; Corruption Watch, 2015; Heystek, 2004; Mbatsane, 2006; Mestry, 2004; Mestry & Govindasamy, 2013; Thenga, 2012; Xaba, 2011). The articles cited above, including a recent article by Rangongo et al. (2016) present the idea that a lack of accountability with respect to the generation and distribution of financial resources in many schools proves problematic. Research also points to the mismanagement and misappropriation of funds in many South African schools (Ahmed & Ahmed, 2012; Corruption Watch, 2015; Joubert & Van Rooyen, 2008). These financial management challenges emanate from, among other things, school governors' confusion about who, principals or school governing bodies, is responsible for financial management (Mestry & Govindasamy, 2013), lack of financial management skills and knowledge amongst school governors (Mestry, 2006), disregard of the law, and treating schools as 'cash cows' (Rangongo et al., 2016). It is a question then as to whether these conceptions of financial accountability are limiting and restrictive, and in need of review.

Research shows that challenges of school financial management are not a specifically South African phenomenon (Brown, Rutherford & Boyle, 2000; Hallak & Poisson, 2007; Koross, Ngware & Sang, 2009; Mncube & Makhasane, 2013; Rangongo et al., 2016; Ochse, 2004; Okon, Akpan & Ukpong, 2011). It can be concluded from evidence presented by scholars cited above that the dominant discourse on school financial management, in South Africa, Kenya, Lesotho, Swaziland, United Kingdom, Germany, Nigeria and France, among others, is that school financial management is a challenge for school managers, administrators and governors.

Research Focus and Aims

Against this largely negative background, some success in school financial management in rural and township communities has been recorded in South Africa (Bhengu & Myende, 2015; Chikoko, Naicker & Mthiyane, 2015; Maringe & Moletsane, 2015). Locally and internationally, principal leadership has been noted to be the most important factor for activating success (Chikoko et al., 2015; Harris, 2002). While there is a great deal of interest in South African schools in difficulty, few research studies locally and internationally have focused exclusively upon leadership practices of successful schools in financial management. This makes the findings of the study reported in this paper important not only for South African scholars and practitioners, but for all local and international communities. Consequently, this paper focuses on successful financial management practices of principals. Its prime aim is to contribute to the knowledge base about leadership practices in financial management in rural contexts, which have hitherto been conceptualised only as problematic. Moreover, this paper chooses to look to success in rural contexts, so that we may learn from such spaces and practices. The paper achieves the above by examining the financial management practices of selected South African novice principals.

We focused on five novice principals, who worked in schools considered to have a good reputation, both academically and organisationally. These schools produced good academic results and they were schools of choice for many parents. According to these principals, although their schools were in rural communities, they had established a good working relationship between the school internal stakeholders and the school-governing bodies (SGBs). The principals further indicated that, unlike many schools in rural communities (Mncube, 2010; Myende, 2015), their SGBs contributed meaningfully in the schools by performing their tasks competently. The study by Heystek (2004), which focused on the role of SGBs in relation to the principal, found that while some schools experienced a good relationship between principals and SGBs, this was not the norm. Importantly, the schools of the novice principals of our case study had not experienced the financial chaos that normally accompanies the mismanagement and misappropriation of school funds (Cebekhulu, 2015). By analysing the nature of these successful schools, we believe that the practices used to manage school finances may provide previously unknown and neglected views about financial management in schools, especially for schools in difficult contexts.

Literature Review

The literature on the mismanagement of finances in schools (referred to above) includes focus on the unresolved challenge of whether financial management is the task of the principal or the SGB (Mestry & Govindasamy, 2013). One way in which this question may be understood is by drawing on different policy frameworks. Firstly, schools are funded from taxpayers' money and, according to Swartz (2009), this makes them publicly accountable when using these national resources. Schools' accounting officers should exercise control of public funds as guided by the Public Finance Management Act (PFMA) (National Treasury, 1999). Principals, according to the South African Schools Act (SASA) (Republic of South Africa (RSA), 1996) and Employment of Educators Act (EEA) (RSA, 1998), are mandated to be accounting officers of their schools. Their roles as accounting officers include maintaining a system of financial controls, internal audits, including appropriate procurement procedures, and accounting for and controlling revenue. Moreover, the principal is expected to account for and control expenditure and take responsibility for the maintenance and safeguarding of school assets.

The above listing of duties suggests, on the one hand, that it is the principal who is chiefly responsible for the management of school finances with largely a surveillance, monitoring and control function to financial management. Section 4 of the EEA (RSA, 1998) stipulates that the principal needs to monitor school accounts, and keep records, so as to best activate the financial resources for the benefit of the learners in consultation with the appropriate structures. The institutional interests of the school guide the action of the chief financial officer, who in this case is the principal. This potentially sets up a dualistic and complex responsibility for the principal as chief financial officer to a wider consultative process (a social democratic developmental agenda), as well as towards an internal quality assurance function of the school as an institution of teaching and learning (an educational agenda). The interplay between the roles and functions straddling the management of finances and social development and education is not clearly demarcated in the policy. The case study of this paper provides insight into how the selected principals manage these multiple agendas successfully.

Conceptualising financial management

Du Toit, Erasmus and Strydom (2010) clarify that financial management entails the acquisition and application of funds. Put in the school context, acquisition comprises ensuring that required funds are available in the school (i.e., the generation of funds: income) and application comprises deciding how available financial resources are going to be used (i.e. the distribution of funds: the expenditure). Income and expenditure considerations are matters that principals make collectively, together with all other stakeholders with respect to the overall needs of the school. Du Preez, Grobler, Loock and Shaba (2003), Motsamai, Jacobs and De Wet (2011) and Ntseto (2009) elaborate that budgeting (i.e. prospective financial planning) constitutes the fourth of the financial management tasks of principals.

Whilst the policy imperatives suggest an apparent demarcation of financial management roles, in practice it is likely that there is a high degree of overlapping between acquisitions, application, needs assessment and budgeting as intertwined responsibilities co-affecting each other in the overall governance of the school environment. SGBs in practice are not simply engaged abstractedly in budgeting and purchasing, since they are also expected indirectly to be making professional management choices in the interests of the school's needs. De Bruin (2014), Mestry (2006) and Rangongo (2011) suggest that financial management involves multiple levels of all four functions in an intersected way. In the absence of an absolute separation of roles and responsibilities in the different policies, co-management of roles and responsibilities is understood to be permissible by policy. The revisions of these policies have not, to date, addressed these potential blurring of roles, since perhaps they are seen as promoting a cooperative collaborative accountability regarding school finances.

However, Mestry (2004) suggests that by contrast, in many rural schools, despite policy expectations of what is required of the SGB and the principals, the task of financial management is left within the hands of principals. Cebekhulu (2015) argues that even in contexts where principals lack necessary expertise in financial management and are consequently unable to resolve practical solutions to practical financial matters (Mestry, 2004), many rural parents do not involve themselves in school financial management issues. This guides our position in this paper that principals are largely responsible for financial management, while the SGB plays a role of ensuring that financial resources are deployed and used in the correct manner. Is this capitulation to the authority of the principal a problem in the specific context of rurality? What accountability factors have generated this practice? Our view is contrary to that of Xaba and Ngubane (2010), who see an overlap in roles as problematic. In contrast, we posit that checking whether funds are acquired and applied, is more closely allied with governance, while the actual acquisition and application of such funds are more closely allied with a management task, as established from the conceptualisation of financial management espoused by Du Toit et al. (2010). Based on the policies highlighted and literature reviewed, we contend that principals are responsible for the holistic educational management of the school, including its financial well-being and how this is executed ought to be understood in its situated context.

Theoretical Framework

Principals as managers of schools and ex-officio members of governing bodies are accountable to the SGB and the Head of Department (HoD) in the province (RSA, 1996). Principals continuously perform their tasks in the schools as systems and potentially as actors, and are observed and evaluated by audience(s) including themselves (Frink & Klimoski, 2004). On this basis, the accountability theory emerges as a relevant frame- work to understand the principals as actors and agents in the financial management activities in schools alongside their multiple audiences. The theoretical lens of financial accountability of actors and audiences (Erkkilä, 2007) focuses on the range of players in a specific context. Accountability theory explains what is lawful as described in organisational policies, and how the actions of individuals, playing different organisational roles, reflect the will to act in the best interest of the organisation and its stakeholders (Rangongo et al., 2016). Furthermore, accountability theory explains the expected behaviour, formal reporting relationships, and performance monitoring and evaluations, and sometimes, the rewards of or sanctions towards individuals or groups, as guided by what emerges during evaluations (Frink & Klimoski, 2004; Hall, Bowen, Ferris, Royle & Fitzgibbons, 2007). To comply with the rules set by the state through the Department of Basic Education (DBE), in the context of South Africa, principals are expected to ensure that financial records are kept, schools' books are audited, and that all stakeholders are aware of how funds are utilised. The principals' actions in the process of financial management are monitored and evaluated by parents, SGBs, other teachers, peer managers and, mostly, the DBE. As a result, there is continuous pressure placed on principals to manage school finances in such a way that the process of accountability is observable by others and themselves as actors.

Public schools are further required to manage state funds in terms of provisions of Section 20 and 21 of the South African Schools Act (RSA, 1996) and principals' accountability is based on these sections. There is pressure on the principals in this study since their schools are funded from taxpayers' money and the Public Finance Management Act (PFMA) (National Treasury, 1999) mainly guides the utilisation of this money. PFMA aims to secure transparency, accountability and sound financial management in government and public institutions, including schools. Besides these Acts, our experiences indicate that principals undergo internal pressure when members of the school check how they manage school finances. This means there is also a strong desire for accountability inside schools, which, according to Erdogan, Sparrowe, Liden and Dunegan (2004), may push individual actors towards acting in a manner that is ethically acceptable. While we have argued for formal mechanisms of ensuring accountability, Ammeter, Douglas, Ferris and Goka (2004) identify one's willingness to be loyal to the organisation as the strongest drive for acceptance within the organisation.

The above theoretical explorations suggest that accountability is multi-faceted and multilinear, shaping varying directions to establish relations, not only in vertical hierarchical power associations, but also in horizontal interactions between collaborating partners. This accountability holds ethical relationships with those whom it aims to serve (downward accountability). These multiple dimensions of accountability are the subject of this article's explorations of the novice rural principals dealing with the situated management of their school finances. It appears that principals constitute the pivotal nexus between all these levels of participative accountability.

Methods

We undertook a naturalistic enquiry grounded within an interpretive worldview to explore the notion and vantages of what constitutes principals' practices in financial management in specific rural schools, each of which is regarded as successful. From qualitative conversations with five principals working in these rural schools in Northern KwaZulu-Natal (KZN), naturalistic research with an emphasis on eliciting in-depth data was conducted. Our intention was to understand the social constructed realities (Cohen, Manion & Morrison, 2011) about principals' engagement with school finances. Guided by the parameters of interpretive enquiry this study places importance on the subjective meanings the principals attach to their practices (Bertram & Christiansen, 2014).

A group of five novice principals, who worked in schools within the rural context and demonstrated success in several aspects of their schools, were purposively selected to participate in the study. Although there is no single accepted definition of a successful school, a school that obtains 60% average in the matriculation pass rate is considered successful and performing by the Department of Education in KwaZulu-Natal, where this study was conducted (Mukeshimana, 2016). This may differ from one province to another, depending on the overall performance of the province.

We chose to work with these novice principals since they had little former experience of emulating past management practices, and were largely unfamiliar with the rural context in which they were appointed. Over time, the principals had managed to involve parents despite the many challenges of involving parents in rural schools (Mncube, 2010). Furthermore, the final matriculation resultsi of their schools showed that their schools were performing well. Three schools had maintained an average pass rate of over 70% from 2013, and two schools were below 70% but above 65 percent. These schools had also established a positive image in the community. We do not claim that these academic successes necessarily equate to success in managing school finances, but we were interested in the state of financial management in such schools labelled as successful, in contexts characterised as deficient by several scholars (Hansraj, 2007; Xaba, 2011).

The selection of participants was purposive in that only principals who were novices (less than five years in principalship) were considered. Our interest was motivated by attempting to understand how novice principals selected their practices and whether these extended beyond the habituated norms of management practice. While there might have been many principals who succeeded in managing their schools, the selection was based on convenience and prior interactions we had with the principals. These principals gave consent to be interviewed and tape-recorded in order to 'get under the skin' of their encounters, and allow our flexibility in probing (Creswell, 2014; Dahlberg & McCaig, 2010) to make sure their views were not lost. They further gave access to the relevant school documents, which also helped us to understand the schools' financial management.

The data set obtained from interviews and document reviews was analysed, using both data-driven and theoretical-driven interpretive thematic analyses (Dahlberg & McCaig, 2010; Henning, Van Rensburg & Smit, 2004). This process began by familiarising ourselves with the data by transcribing audio-data to textual-data, and reading and re-reading of transcripts. The re-reading process helped in coding and reducing of the data into themes used to report the findings. To ensure quality and rigour, we adopted Guba and Lincoln's (1985, as cited in Denzin & Lincoln, 2000) construct of trustworthiness. We used interviews and documents to triangulate the data and this allowed us to verify from the documents whether what principals were saying was supported by documents. Further, we worked with principals that we knew, which meant there was an established trust enhancing the generation of data.

In dealing with the documents and with the principals, we were obliged to abide by the ethics in research (Bertram & Christiansen, 2014), and we respected all ethical considerations such as the protection of participants' identities, gaining informed consent, and securing permission to conduct the research from the university at which the authors are based and from the Department of Education in KwaZulu-Natal. Guided by these ethics, the names used in this study are not real names of schools and principals.

Findings and Discussion

The questions asked were pertinent to the leadership practices adopted by the novice principals in regards to financial management. The responses from our conversations with principals, while not representative of schools in KwaZulu-Natal, provide some important insights into the management of financial resources at the selected schools. To discuss the findings in this paper, we draw on four themes that emerged during data analysis: (1) developing one's capacity in financial management; (2) developing school-based training for SGB members; (3) participative and collaborative financial management approaches; (4) formulating policies for clear procedure. In the presentation of our findings, we wanted to ensure that the views of principals are not lost, as they provide powerful supporting evidence to our claims. For this reason, verbatim quotes are provided in the discussion of each theme. The names used to refer to principals are novice principal 1-5, which are abbreviated as NP1; NP2; NP3; NP4; NP5. NP2, NP4 and NP5 are males and NP1 and NP3 are females.

Developing One's Capacity in Financial Management

In our initial conversations with the novice principals, we wanted to understand who these principals were in terms of their educational qualifications and whether they had any training for the job of principal. In order to understand this, we collected their biographical data. All five principals indicated that they realised the dilemmas that come with being principals, especially in the context of rurality. The principals revealed that they had invested time in developing their capacity to be principals in order to deal with management issues. In studying their profiles, we learned that three principals possessed Bachelor of Education Honours degrees in Education Management, while the other two had completed an Advanced Certificate in Education Leadership (ACE Leadership). During the interviews, it emerged that they developed themselves before they became principals and whilst they were already within a School Management Team (SMT). This is shown in the views of NP1, NP3 and NP4 below (all responses presented verbatim):

NP1: You know when you are employed as the principal, deputy or HoD [Head of Department], you come in the position only through your experience and there are many things we did not train for as principals, and one important aspect of our work is to ensure that school funds are used accordingly. Unfortunately, principals are not accountants, but they are expected to account. When I became an HoD, I went to do honours, because I knew I needed some skills. I wanted to capacitate myself especially on the issues of financial Management. I had a choice not to do it, but I wanted to ensure that my SGB members know what they are doing.

NP3: I always wanted to be a principal and when I got an HoD post, I attended ACE on school leadership, and part of what we did was a bit of financial management.

NP4: As principals "sibhekwe ngamehlo ukuthi izimali zesikole sizibheke kanjani" (we are being monitored on how we use school funds). I had to ensure that I know what I am doing and I enrolled for my honours, and fortunately we did some school financial management.

The extracts indicate that the principals wanted to capacitate themselves, constituting a form of self-accountability and personal/professional development. The personnel administrative measures, as amended by the DBE (2016), indicates that in order to qualify as a principal, one needs a three- or four-year recognised teaching qualification and seven years of teaching experience. What these requirements confirm is that the principals' experiences need not include financial management and not all principals may have financial management knowledge embedded in their training. The claims of principals in Rangongo et al. (2016) and many other studies in South Africa (Joubert & Van Rooyen, 2008; Mestry, 2010; Xaba, 2011; Xaba & Ngubane, 2010) indicate that a financial management skills shortage is one of the causes for financial mismanagement in schools and some principals identify an opportunity for self-empowerment from the position.

The views of NP1, NP3 and NP4 may be considered through the lens of the accountability theory as the theory allows us to understand the principals as agents in the financial management activities in their schools. In the process of financial management, principals become agents whose behaviour is subject to evaluation by others (Frink & Klimoski, 2004). It is revealed in the extracts above that the principals are aware that they are observed and this pushes them to develop themselves in order to be able to account. This kind of accountability might constitute a form of a horizontal accountability to peers and parents, to the institution they served, as well as to their own self.

Another important element that emerges from the principals' views is the aspect of moral values, which are, according to Hall et al. (2007), about how individual values propel people to act in ways that are ethically acceptable in an organisation, a moral accountability. This is in line with Erdogan et al. (2004) in their claim that one's main evalu-ator is oneself. One principal indicates that there was a choice not to do any training, but he wanted to do what he understood to be correct, which confirms the view of Erdogan et al. (2004). In the same vein, the claims of NP1 show an element of fear as principals are expected, by many, to account. To ensure that they are able to do this, they choose to capacitate themselves. This fear is not necessarily anxiety-driven, but may be ethically motivated.

We asked principals if their perceived capacity helped them in undertaking financial management tasks. All replied positively that they had not experienced any conflict in their schools due to financial issues. This confirms how the training of principals and self-empowerment are important elements in ensuring that principals are able to deal with financial management. In this representation, accountability is not only understood as being answerable to external requirements, authorities or policy expectation; instead, it is also driven by an internal logic of self-worth and responsibility. The personal decision of principals to enrol for further education qualifications and their awareness that they have to do their work well shows integrity and morality, a finding very different to those of Rangongo et al. (2016), who identified a lack of integrity and morality in the principals in Limpopo.

Developing School-Based Training for SGB Members

Against the dominant discourse that many parent governors lack skills to participate in financial management (Hansraj, 2007; Xaba & Ngubane, 2010), the findings in this study reveal that the five principals, using their own knowledge and driven by their interest to make their management approach more accessible, developed school-based training for SGB members. For example, NP2 noted:

Personally, as a school principal and Accounting Officer, I would love to manage a school that is effective. Therefore I have taken the responsibility to capacitate the SGB members myself.

In the same vein, NP3 added, "I have conducted a light training for the SGB about their duties using the SASA and focussed on basic financial aspects."

NP4 explained that "so far there is no training that the SGB has undergone from the DBE on school financial management after six months of its existence." He further added that "I went all out to get information from other experienced principals. That has assisted me to be able to capacitate the SGB myself on issues of school governance."

The element of moral value and the commitment to develop the SGB professionally as part of accountability theory manifests very strongly in the claims of the principals presented above. This stands in contrast to, for example, Rangongo et al. (2016), who have indicated that there is sometimes dishonesty amongst principals. In a context where parents in the SGB are not clear about financial management, principals who are dishonest may capitalise on the opportunity and treat schools as 'cash cows.' However, concern for capacity-building of the community (namely the SGB members), who will regulate the conduct of the principals, constitutes the hallmark accountability of the principals in our study. While the SASA mandates principals to capacitate SGBs (RSA, 1996), their accountability in this role is seldom checked. This may suggest that principals who invest time in SGB capacity-building do it willingly, not because it is regulated or expected, but because they inherently believe in its contribution to good governance. These principals facilitate in practice both upwards and horizontal accountabilities, playing different management roles (community and financial services) simultaneously, driven by operational and ethical concerns.

Participative and Collaborative Financial Management Approaches

All principals indicated that in their attempt to ensure transparency, they make financial management a collective activity. All the principals formed financial management committees (FINCOM) in their individual schools. The FINCOMs comprise teacher representatives, parents from the governing body, and the treasurer and chairpersons of all other committees found in the school. The inclusion of chairpersons of other committees is done to ensure that financial decisions are responsive to the expectations and needs of different groups in the school. NP5 stated:

The school has the finance committee that is guided by the school financial policy on how the school finances should be used. This committee is mandated by the executive committee (SGB) to assist us in managing the school finances. The committee also includes the financial advisor that the SGB co-opted from the community.

The same practice is identified in NP4's explanation that "the school has established the new finance committee with four members. We sat down to do financial planning together, including looking at the needs of the school in this current academic year. We prioritised them and we drafted a school budget." Although NP3 indicated that establishing a committee was a difficult task, his comments ("As difficult as it may be, we managed to set up a new FINCOM all together. We sit down and we do planning with them although we inherited some financial problems from the previous SGB and FINCOM") indicate that the same practices argued for by NP4 and NP5 were found under his leadership.

Two principals (NP2 and NP1) indirectly indicated that they have established FINCOMs in their schools. Both the principals indicated what their committees were responsible for.

NP2: The FINCOM as the sub-committee of the SGB has the functions that are delegated to this committee and to me as an Accounting Officer; for instance, the procurement of goods and services.

NP1: The FINCOM looks at what we are planning to do with the school finances and further plans how we shall achieve our aims and objectives.

The principals in this study concur that financial management happened mostly at committee levels. NP5 indicated that he was convinced that effective management lies in participative approaches, as the view below evidences:

NP5: You know, as principals, we cannot lead schools alone if we want them to be effective. So I make sure that all my teachers participate in all school matters.

Again, the establishment of committees is in line with accountability as espoused by Ammeter et al. (2004). They speak of creating different levels of control and sometimes this is done through organisational units tasked with responsibilities. We consider participative and collaborative financial management as part of accountability amongst principals as, by law, a FINCOM is a legal substructure that ought to be formed by SGBs in schools (RSA, 1996). While participative and collaborative financial management is reported as lacking in some schools (Rangongo et al., 2016), the principals in our study endorse it as a form of accountability, and being in line with what policy requires of them. Furthermore, SASA pushes for decentralised governance to open spaces for participation on the basis that participation presents hope for success, sentiments shared by these principals. Claims by Myende and Chikoko (2014) show that participation is required for success, and since accountability is mandated by the Education Department, principals are obliged to ensure it is implemented.

Previous studies reflect principals' lack of willingness to share their power, especially with the SGB. Power, they suggest, is usually only shared with a few members of the SGB coming together to embezzle school funds, producing a toxic culture of collaborative corruption (Heystek, 2004; Mestry, 2006, 2010; Xaba, 2011). These contaminated relationships between the principal, SGB, teachers and parents on school financial matters produce contested belligerence within the school context and its community. In this study, we saw a different picture, where involvement of stakeholders made it easy for principals to execute respected and responsible school financial management.

Formulating Policies for Clear Procedure As part of our research process, we sought permission from principals to look at several financial documents. Our findings revealed that the work of four principals and their committees was guided by documented school policies. These principals had formulated policies, which explained, among other things, the role of the SGB, FINCOM, the process for financial planning and how financial irregularities were addressed in the school. The voice of NP5 not only emphasises the importance of written policies in financial management, but it indicates that while there are legalised official departmental policies, the school needs its own home-made in situ policies as well. Also important from amongst his views is the emphasis on the involvement of all school stakeholders in designing these situated regulative documents. NP5 stated:

I try to follow the stipulated policies from the Act ... where I do not understand, I consult with experienced principals. The school has the financial policy. To us, the policy is like a Bible: it guides, leads and tells us if we are still within the policies. It is one of the school official documents that we need to follow at all material times. What is also important about our policy is that every stakeholder was involved in the drawing up this policy; therefore it is binding to all of us.

This suggests that official policy was able to be reinterpreted by practitioners in the field, utilising the professional management experience of localised specific contexts and individuals. NP4 further commented that if school-based policies are not put in place, people will use common sense interpretations of financial management, which may be a recipe for conflict. NP3 added that her involvement of all stakeholders brought together the national department policies, as well as the local school-designed interpretations, ensuring that macro- and micro-polices do not diverge. NP1 further emphasised his role in expanding the set of departmental expectations so as to clarify the financial management operations of the SGB and the school. Even in the absence of localised written policy texts, NP2 asserted that they are enacted and practised policies (Bayeni, 2012) which regulate people's conduct. However, when the policies are written, they constitute overt guiding principles of policy in terms of what people do, what is good for the school, and assumptions about how people want finances to be handled, what works in managing finances in the school, and what financial management entails. The conscious value of written policy (national or local) was ever-present across all participants.

Our assumptions about the guiding principles above are contrary to the many studies on school financial management. While the principals in this study all seem to be aware of law and policy, Rangongo et al. (2016) report that principals' ignorance of the law caused mismanagement of funds. Similarly, other studies such as those of Heystek (2004) and Mestry (2004) identify stakeholders' lack of knowledge, including knowledge of policy, as a challenge of financial management. As a result, we became interested in what made the principals of our study different. Responses of NP3 and NP5 helped us explain this awareness of policies and procedures. NP3 states:

I have observed many principals breaching the law and losing their schools because of finances. When I became the principal, I wanted to be transparent. Understanding the policy was the only way I can do this.

Put differently, but suggesting the same notion, NP5 states:

Finances of schools have led to many people I know, losing their jobs. I didn't want to become part of the statistics. I ensured that I educated myself about policies and procedures.

The development of policies, aimed to set clear procedures, may be driven by the need for upward, downward and horizontal accountability. To account for this, organisations/managers may exert some level of control on the behaviours of employees (a downward accountability); and this is usually implemented through policies explaining procedure and guiding actions (Ammeter et al., 2004). It was also established that the actions of principals in formulating policies and involving others in the formulation of policies, are driven simultaneously by both external mechanisms of accountability (upward accountability) and accountability to a body of peers in the profession of educational school management. Erkkilä (2007) refers to this latter form of accountability as a form of professional accountability, which could be seen as a horizontal form of accountability. The multiple levels of accountability serve to keep principles and operations in check. It is debatable whether these multiple accountabilities incapacitate or generate a fearful debilitating disposition amongst principals. It appears from the principals in this study that there was an ever-present conscious knowledge of potential sanction for any misdemeanour, not only from the official employers, but also from within the community inside and outside the school. However, this did not seem to have impeded these actors of performing with, for, and in relation to their audiences.

Conclusion and Recommendations

The paper examined the financial management practices of novice principals in schools deemed to be successful, and how accountability was manifested in the principals' practices. While financial management in schools in general, and rural schools in particular, has been regarded a difficult task for school principals and governors, this paper presents a different discourse challenging the "half-truths" that have only provided a negative discourse about financial management. The findings of this paper have revealed that the principals are willing to share their leadership with others to ensure transparency. To deal with the incapacity of parent members of the SGB, principals are engaging with the training and development of their SGB members and their own capacitation. In an attempt to deal with the widely reported challenge of ignorance towards policies, principals in this study developed their context-responsive policies, drawing from the national policies.

The analysis of the principals' practices indicates that there are schools that are dealing with financial management in a manner we regard as appropriate, and in line with the government expectations. These findings are important, as they provide an alternative discourse to the long-held negative narratives regarding school financial management, both locally and internationally. Moreover, these findings, from the perspective of a developing economy, could provide hope and resourcefulness within both the developing and developed economy contexts.

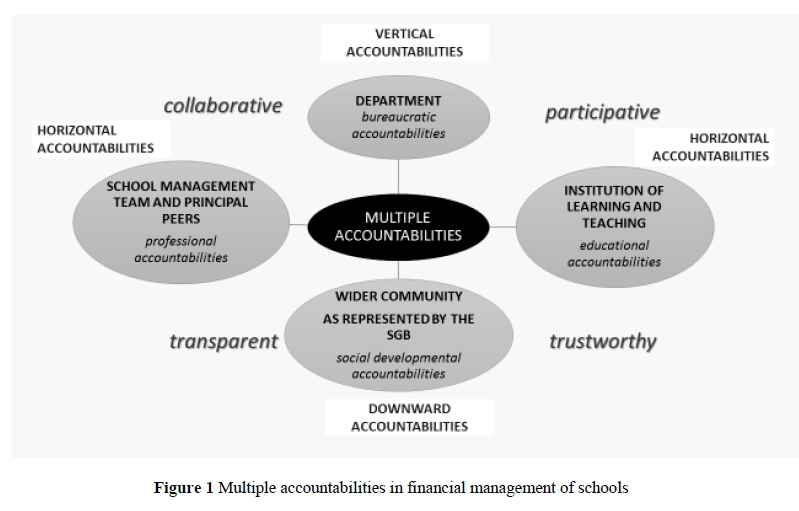

Their practices, if examined closely, are participative and collaborative leading to transparency and trustworthiness. Their moral integrity and commitment are reinforced through being consciously aware of their responsibilities to: the department (bureaucratic accountabilities); their management and educator peers (professional accountabilities); the school as an institution of learning and teaching (educational accountabilities); as well as the wider community as represented by the SGB (social developmental accountabilities). Their accountabilities are multiple and diverse: vertical, horizontal, and downward to different role-players simultaneously. They treat their own readiness to manage as important, hence their involvement in self-monitoring and self-development through engagement in extra-educational qualifications and consultations with their manager-peers, who share common challenges. This lies beyond prescriptive administrative requirements. They tap into the worthwhile knowledges of their own contexts.

Whilst this paper focused only on five novice principals, we contend that multiple financial management practices may be in operation in a wider range of schooling contexts (see Figure 1 below). This requires that we broaden our frames of reference of accountabilities, which will allow us to see more respectfully the range of positive efforts that many educational managers undertake routinely in their specific school contexts. Based on this conclusion, we recommend further research focusing on experienced principals' practices from a variety of contexts. This may help to expose multiple practices, as well as what forms of accountability direct principals to act in a certain way when it comes to, for example, the process of financial management in schools. The findings have also shown that principals had reinforced their capacities by furthering their studies about (financial) management. This may suggest that there is a connection between one's level of study and the ability to deal with complex school tasks. We therefore recommend the review of the minimum requirements for principalship, to include especially relevant qualifications that activate the multiple levels of accountability. Moreover, management is construed as not confined to bureaucratic accountabilities, but also professional, educational and developmental agendas which ought to promote a transparent, participative and collaborative goal to generate trustworthy practice.

Acknowledgements

University Teaching and Learning Office (UTLO) of the University of KwaZulu-Natal funded the writing process of this article through Come Write With Me project. We would like to express our sincere gratitude to the UTLO for support. The views and opinions expressed in this article are those of the authors and the funders (UTLO) cannot be held responsible for any views or opinions expressed in the article.

We would like to further acknowledge and thank Sibongiseni Cebekhulu for conducting field-work (interviews) used in this study and for transcribing the interviews.

Notes

i. In South Africa, learners (students) enrolled in Grade 12, the final high school grade, are called matriculants, or 'matrics,' and the school leaving results obtained by learners referred to as matriculation results.

ii. Published under a Creative Commons Attribution Licence.

References

Ahmed R & Ahmed QM 2012. Petty corruption in the police department: A case study of slum areas of Karachi. Developing Country Studies, 2(6):78-86. Available at http://citeseerx.ist.psu.edu/viewdoc/download?doi=10.1.1.969.4933&rep=rep1&type=pdf. Accessed 12 August 2016. [ Links ]

Ammeter AP, Douglas C, Ferris GR & Goka H 2004. A social relationship conceptualization of trust and accountability in organizations. Human Resource Management Review, 14(1):47-65. https://doi.org/10.1016/j.hrmr.2004.02.003 [ Links ]

Bayeni SD 2012. Principals influencing education policy practice: A case study of two schools. In V Chikoko & KM Jorgensen (eds). Education leadership, management and governance in South Africa. New York, NY: Nova Science. [ Links ]

Bertram C & Christiansen I 2014. Understanding research: An introduction to reading research. Pretoria, South Africa: Van Schaik. [ Links ]

Bhengu TT & Myende PE 2015. Traversing metaphoric boundaries between schools and their communities: An ethnographic study of a rural school. Journal of Social Sciences, 43(3):227-236. https://doi.org/10.1080/09718923.2015.11893440 [ Links ]

Bhengu TT & Ncwane SH 2014. School governance, financial management and learners' classroom needs: Perspectives of primary school teachers. International Journal of Educational Sciences, 7(3):463-470. https://doi.org/10.1080/09751122.2014.11890207 [ Links ]

Brown M, Rutherford D & Boyle B 2000. Leadership for school improvement: The role of the head of department in UK secondary schools. School Effectiveness and School Improvement, 11(2):237--258. [ Links ]

Cebekhulu S 2015. Exploring approaches of managing school finances in a rural context: A case study of five novice principals. Unpublished MEd thesis. Durban, South Africa: University of KwaZulu-Natal. [ Links ]

Chikoko V, Naicker I & Mthiyane S 2015. School leadership practices that work in areas of multiple deprivation in South Africa. Educational Management Administration and Leadership, 43(3):452-467. https://doi.org/10.1177/1741143215570186 [ Links ]

Cohen L, Manion L & Morrison K 2011 . Research methods in education (7th ed). London, England: Routledge. [ Links ]

Corruption Watch 2015. Annual report 2014 -Corruption is growing. Available at http://www.corruptionwatch.org.za/annual-report-2014-corruption-is-growing/. Accessed 30 March 2016. [ Links ]

Creswell JW 2014. Research design: Qualitative, quantitative, and mixed methods approaches (4th ed). London, England: Sage. [ Links ]

Dahlberg L & McCaig C (eds.) 2010. Practical research and evaluation: A start-to-finish guide for practitioners. London, England: Sage. [ Links ]

De Bruin L 2014. Budget control and monitoring challenges for school governing bodies. Unpublished MEd dissertation. Vanderbijlpark, South Africa: North-West University. Available at https://dspace.nwu.ac.za/bitstream/handle/10394/10609/DeBruin_L.pdf?sequence=1. Accessed 8 February 2018. [ Links ]

Denzin NK & Lincoln YS (eds.) 2000. Handbook of qualitative research (2nd ed). Thousand Oaks, CA: Sage. [ Links ]

Department of Basic Education 2016. Personnel administrative measures (PAM). Government Gazette, 608(39684):1-216, 12 February. Available at https://www.naptosa.org.za/doc-manager/30-labour-matter/labour-news/920-pam/file. Accessed 16 February 2018. [ Links ]

Du Preez P, Grobler B, Loock C & Shaba SM 2003. Effective Education Management Series. Sundown: Heinemann. [ Links ]

Du Toit GS, Erasmus BJ & Strydom JW (eds.) 2010. Introduction to business management (8th ed). Cape Town, South Africa: Oxford University Press. [ Links ]

Erdogan B, Sparrowe RT, Liden RC & Dunegan KJ 2004. Implications of organizational exchanges for accountability theory. Human Resource Management Review, 14(1):19-45. https://doi.org/10.1016/j.hrmr.2004.02.002 [ Links ]

Erkkilä T 2007. Governance and accountability - A shift in conceptualisation. Public Administration Quarterly, 31(1/2):1-38. [ Links ]

Frink DD & Klimoski RJ 2004. Advancing accountability theory and practice: Introduction to the human resource management review special edition. Human Resource Management Review, 14(1):1-17. https://doi.org/10.1016/j.hrmr.2004.02.001 [ Links ]

Hall AT, Bowen MG, Ferris GR, Royle MT & Fitzgibbons DE 2007. The accountability lens: A new way to view management issues. Business Horizons, 50(5):405-413. https://doi.org/10.1016/j.bushor.2007.04.005 [ Links ]

Hallak J & Poisson M 2007. Corrupt schools, corrupt universities: What can be done? Paris, France: International Institute for Educational Planning. Available at http://siteresources.worldbank.org/EXTHDOFFICE/Resources/5485726-1239047988859/5995659-1239051886394/5996104-1239987975295/25.Nov_12_paper_Hallak_and_Poisson_2007_Corrupt_schools.pdf. Accessed 20 October 2016. [ Links ]

Hansraj I 2007. The financial management role of principals in section 21 schools in South Durban, KwaZulu-Natal. Unpublished MEd thesis. Pretoria, South Africa: University of South Africa. Available at http://citeseerx.ist.psu.edu/viewdoc/download?doi=10.1.1.514.7898&rep=rep1&type=pdf. Accessed 31 January 2018. [ Links ]

Harris A 2002. Effective leadership in schools facing challenging contexts. Paper presented at the Annual Meeting of the American Educational Research Association, New Orleans, 1 -5 April. [ Links ]

Henning E, Van Rensburg W & Smit B 2004. Finding your way in qualitative research. Pretoria, South Africa: Van Schaik. [ Links ]

Heystek J 2004. School governing bodies - the principal's burden or the light of his/her life? South African Journal of Education, 24(4):308-312. Available at https://www.ajol.info/index.php/saje/article/view/25006. Accessed 31 January 2018. [ Links ]

Joubert HJ & Van Rooyen JW 2008. Trials and tribulations of leadership and change in South African public schools. Pretoria, South Africa: University of Pretoria. Available at http://www.emasa.co.za/files/full/RJoubert.pdf. Accessed 30 March 2016. [ Links ]

Koross PK, Ngware WM & Sang AK 2009. Principals' and students' perceptions on parental contribution to financial management in secondary schools in Kenya. Quality Assurance in Education, 17(1):61-78. https://doi.org/10.1108/09684880910929935 [ Links ]

Maringe F & Moletsane R 2015. Leading schools in circumstances of multiple deprivation in South Africa: Mapping some conceptual, contextual and research dimensions. Educational Management Administration and Leadership, 43(3):347-362. https://doi.org/10.1177/1741143215575533 [ Links ]

Mbatsane PN 2006. The financial accountability of school governing bodies. MEd thesis. Pretoria, South Africa: University of Pretoria. Available at https://repository.up.ac.za/bitstream/handle/2263/26879/00dissertation.pdf?sequence=1. Accessed 26 January 2018. [ Links ]

Mestry R 2004. Financial accountability: The principal or the school governing body? South African Journal of Education, 24(2):126-132. [ Links ]

Mestry R 2006. The functions of school governing bodies in managing school finances. South Africa Journal of Education, 26(1):27-38. Available at http://www.sajournalofeducation.co.za/index.php/saje/article/view/67/63. Accessed 23 January 2018. [ Links ]

Mestry R 2010. The position of principals in school financial management: A South African perspective. Journal of Educational Studies, 9(2):36-50. [ Links ]

Mestry R & Govindasamy V 2013. Collaboration for the effective and efficient management of school financial resources. African Education Review, 10(3):431-452. https://doi.org/10.1080/18146627.2013.853539 [ Links ]

Mncube V 2010. Parental involvement in school activities in South Africa to the mutual benefit of the school and the community. Education as Change, 14(2):233-246. https://doi.org/10.1080/16823206.2010.522061 [ Links ]

Mncube VS & Makhasane S 2013. The dynamics and intricacy of budgeting in secondary schools in Lesotho: Case studies of three high schools. Africa Education Review, 10(2):347-363. https://doi.org/10.1080/18146627.2013.810903 [ Links ]

Motsamai MJ, Jacobs L & De Wet C 2011. Policy and practice: Financial management in schools in the Mafikeng District of Lesotho. Journal of Social Sciences, 26(2):105-116. https://doi.org/10.1080/09718923.2011.11892887 [ Links ]

Mukeshimana M 2016. Leadership practices in selected successful schools. MEd dissertation. Pietermaritzburg, South Africa: University of KwaZulu-Natal. Available at https://researchspace.ukzn.ac.za/bitstream/handle/10413/14431/Mukeshimana_Manasse_2016.pdf?seq uence=1&isAllowed=y. Accessed 22 January 2017. [ Links ]

Myende PE 2015. Tapping into the asset-based approach to improve academic performance in rural schools. Journal of Human Ecology, 50(1):31-42. Available at http://krepublishers.com/02-Journals/JHE/JHE-50-0-000-15-Web/JHE-50-1-2015-Abst-PDF/JHE-50-1-031-2726-15-Myende-P-E/JHE-50-1-031-2726-15-Myende-P-E-Tx[4].pdf. Accessed 22 January 2018. [ Links ]

Myende PE & Chikoko V 2014. School-University Partnership in a South African rural context: Possibilities for an asset-based approach. Journal of Human Ecology, 46(3):249-259. Available at http://krepublishers.com/02-Journals/JHE/JHE-46-0-000-14-Web/JHE-46-3-000-14-Abst-PDF/JHE-46-3-249-14-2629-Myende-P/JHE-46-3-249-14-2629-Myende-P-Tx%5B1%5D.pdf. Accessed 22 February 2018. [ Links ]

National Treasury 1999. Public Finance Management Act No. 1 of1999. Pretoria, South Africa: Government Printers. [ Links ]

Ntseto VE 2009. A programme to facilitate principals' financial management of public schools. PhD thesis. Bloemfontein, South Africa: University of Free State. Available at http://scholar.ufs.ac.za:8080/xmlui/bitstream/handle/11660/7409/NtsetoVE .pdf?sequence=1&isAllow ed=y. Accessed 17 January 2018. [ Links ]

Ochse KL 2004. Preventing corruption in the education system: A practical guide. Eschborn, Germany: Deutsche Gesellschaft für Technische Zusammenarbeit (GTZ) GmbH. Available at http://toolkit.ineesite.org/toolkit/INEEcms/uploads/1038/Preventing_Corruption_In_ The_Education_System.pdf. Accessed 30 March 2016. [ Links ]

Okon FI, Akpan EO & Ukpong OU 2011. Financial control measures and enhancement of principals' administrative effectiveness in secondary schools in Akwa Ibom State. African Journal of Scientific Research, 7(1):335-342. [ Links ]

Rangongo P, Mohlakwana M & Beckmann J 2016. Causes of financial mismanagement in South African public schools: The views of role players. South African Journal of Education, 36(3): Art. # 1266, 10 pages. https://doi.org/10.15700/saje.v36n3a1266 [ Links ]

Rangongo PN 2011. The functionality of school governing bodies with regard to the management of finances in public primary schools. MEd dissertation. Pretoria, South Africa: University of Pretoria. Available at http://repository.up.ac.za/dspace/bitstream/handle/2263/27257/dissertation.pdf ?sequence=1&isAllowed=y. Accessed 21 October 2016. [ Links ]

Republic of South Africa (RSA) 1996. Act No. 84, 1996: South African Schools Act, 1996. Government Gazette, 377(17579). 15 November. [ Links ]

RSA 1998. Employment of Educators Act, 1998 (Act No 76 of 1998). Government Gazette, 401(19420). 2 November. [ Links ]

Swartz L 2009. Financial management in schools. PhD thesis. Houston, TX: Rice University. [ Links ]

Thenga CM 2012. Managing school funds in selected secondary schools in Gauteng province. MEd dissertation. Pretoria, South Africa: University of South Africa. Available at http://uir.unisa.ac.za/bitstream/handle/10500/7061/dissertation_thenga_ cm.pdf?sequence= 1&isAllowed=y. Accessed 15 January 2018. [ Links ]

Xaba M & Ngubane D 2010. Financial accountability at schools: Challenges and implications. Journal of Education, 50:139-160. Available at http://repository.nwu.ac.za/bitstream/handle/10394/ 17960/Jnl%20education-2010-50-Xaba.pdf?sequence=1&isAllowed=y. Accessed 13 January 2018. [ Links ]

Xaba MI 2011. The possible cause of school governance challenges in South Africa. South African Journal of Education, 31(2):201-211. https://doi.org/10.15700/saje.v31n2a479 [ Links ]

{kind=link}