Servicios Personalizados

Articulo

Inglés (pdf)

Inglés (pdf)

Articulo en XML

Articulo en XML Referencias del artículo

Referencias del artículo

Indicadores

Links relacionados

-

Citado por Google

Citado por Google -

Similares en Google

Similares en Google

Compartir

Permalink

PermalinkSouth African Journal of Science

versión On-line ISSN 1996-7489

versión impresa ISSN 0038-2353

S. Afr. j. sci. vol.119 no.11-12 Pretoria nov./dic. 2023

http://dx.doi.org/10.17159/sajs.2023/15549

RESEARCH ARTICLE

https://doi.org/10.17159/sajs.2023/15549

Corporate tax avoidance: Is South African society negatively affected by chartered accountant CEOs?

Pieter van der SpuyI; Phillip de JagerII

ISchool of Accountancy, Stellenbosch University, Stellenbosch, South Africa

IIDepartment of Finance and Tax, University of Cape Town, Cape Town, South Africa

ABSTRACT

Corporate tax avoidance can impede governments' spending towards social and economic initiatives that can increase infrastructure development, economic growth, and equality, and reduce poverty. Yet, why some companies avoid more tax than others is not adequately understood, and, in particular, research regarding the influence of CEO-characteristics on tax avoidance, is lacking. This study is an empirical investigation into the influence of a CEO's tax knowledge and tax awareness, construed as a 'CEO effect', on corporate tax avoidance, using data from the 112 largest listed companies on the Johannesburg Securities Exchange between 2004 and 2018. We found that the CEO effect, not measured before, does not have an observable influence on the level of corporate tax avoidance. This finding assuages possible concerns that chartered accountants, and particularly chartered accountants in the top leadership positions in large companies, are more shareholder oriented, to the detriment of the interests of society, as suggested in the literature.

SIGNIFICANCE:

Our findings suggest less influence of the CEO, as an upper-echelon member, on companies' behaviour, such as corporate tax avoidance, than other published studies have found. Moreover, the findings indicate that the tax knowledge and awareness construed as a CEO effect, does not influence corporate tax avoidance. In the main, the results provide little support for claims made by the South African Institute of Chartered Accountants, the chartered accountant's regulatory body, that chartered accountants can help companies to avoid tax to increase profits. This may sway society's view of the chartered accountant and their role in the South African economy.

Keywords: corporate tax avoidance, chartered accountants, chief executive officers, effective tax rates

Introduction

An advert by the South African Institute of Chartered Accountants (SAICA), states that "the goal of a [chartered accountant] is to help businesses to profit from their extensive tax experience...to minimise the influence of tax on their profitability"1. Corporate tax avoidance enriches shareholders, but it harms governments and society when less funding is available for social causes. Despite much research on the topic, it is still unclear why some companies avoid more tax than others. Chief executive officer (CEO) characteristics have previously been offered as possible 'determinants' of tax avoidance. However, CEO tax knowledge and awareness, construed as a specific CEO characteristic, has not been explored in quantitative corporate tax avoidance literature.

The chartered accountant (CA) professional qualification is one of the most popular career choices for thousands of ambitious school leavers in South Africa, because the CA designation has become synonymous with prospects of extraordinary income-earning potential and societal status.2 A 4-year university programme equips prospective CAs with integrated knowledge about the intricacies and relationships between taxation, accounting, corporate finance, and auditing, after which they start a 3-year internship at a SAICA-accredited firm. This is where their integrated skill sets are further developed before they can register as CAs. Many CAs later become CEOs of large, listed companies, which means that their power and ability extend beyond those of the 'average' CA. The CAs' integrated skill sets make them uniquely equipped to exploit corporate tax avoidance at the companies they lead. This argument is aligned with the claim in the SAICA advert. Furthermore, Terblanche3 claims that the average CA is shareholder-oriented, which stems from the university curriculum, making them ignorant of social needs. There are arguments to the contrary. For example, CAs' training also exposes them to the increasing importance of social responsibility, and, for example, the King report, which advocates for 'responsible' tax behaviour.4 Therefore, SAICA's advert highlights a contention which we investigated empirically in this paper.

Many company characteristics have been explored in quantitative research as determinants of tax avoidance. Variation in corporate social responsibility performance5, debt levels, growth, profitability, company size, industry, and corporate governance6, have all been considered, but the results are often inconclusive or contrary to theoretical expectations. Variation in the characteristics of corporate leadership is also sometimes investigated, described in the literature as 'CEO effects'. One study found that a CEO's educational background was not associated with tax avoidance, although personal idiosyncrasies were. However, the authors of that study did not specifically investigate a CEO's tax knowledge and tax awareness, because they argue that it is not measurable, and that CEOs are rarely tax experts.7 Recent literature reviews still call for more research on the impact of CEO skills and knowledge on corporate tax avoidance8,9, which is where our study makes its main contribution. A unique feature of the South African corporate landscape is that 30% of CEOs are CAs10, which we use as a proxy for a CEO's tax knowledge and awareness. Our study is conceptualised from upper echelon theory and shareholder value maximisation theory, which postulate that the influence of top leadership permeates corporate behaviour and the company, perceived as a shareholder value maximising entity under control of the CEO, respectively.

We used data from the largest listed companies in South Africa, which we analysed statistically to determine the relationship between effective tax rates, our proxy for tax avoidance, and a CEO's tax knowledge. In contrast with a more general and exploratory earlier study on South African corporate effective tax rates11, in this study, we explored specific aspects regarding the relationship between CEO characteristics and corporate tax avoidance, as the following section explains as the gap where we make our contribution.

Literature review and development of hypotheses

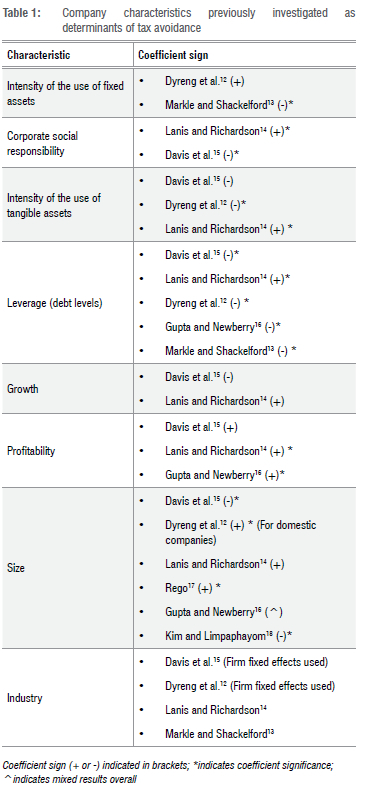

Quantitative research about corporate tax avoidance usually investigates the influence of corporate characteristics as 'determinants' of effective tax rates, as proxy for corporate tax avoidance. This proxy, although widely used in the literature as reported in the table below, is not perfect, nor does it differentiate between corporate tax avoidance and tax evasion, the latter being illegal. Table 1 summarises some of the corporate determinants investigated in the past. This table shows the mixed and inconclusive results pertaining to many cases.

Beyond the influence of the corporate characteristics depicted above, the influence of various CEO characteristics on corporate tax avoidance has also been investigated. Olsen and Stekelberg19 investigated the relationship between a CEO's personality and corporate tax avoidance, and found that companies with CEOs with narcissistic personalities are associated with more tax avoidance. Another study found that CEO compensation was not associated with corporate tax avoidance20, while another21 found a positive association. The CEO's background matters: CEOs with a military background are associated with less corporate tax avoidance.22 Dyreng et al.7 traced a specific person's trajectory as a CEO between different companies and report that similar corporate tax avoidance patterns follow the move. In addition, De Klerk and Mey23 found that companies with a CA appointed as CEO, are associated with less earnings management, possibly suggesting that CAs are less aggressive in this regard.

We argue that a person with a combination of tax-related knowledge and in a position of absolute power, will have the propensity to effect tax avoidance at the company they lead. This is the basis of our hypotheses that there will be greater tax avoidance, on average, at those South African companies where CEOs are CAs. This is referred to as the 'CACEO effect' in this article.

Hypothesis I

H0: The CACEO effect between companies has no association with corporate tax avoidance.

Ha: The CACEO effect between companies will be associated with more corporate tax avoidance.

Hypothesis II

H0: The CACEO within company effect has no association with corporate tax avoidance.

Ha: The CACEO within company effect is associated with more corporate tax avoidance.

Hypothesis I focuses on the cross-sectional CACEO effect, while Hypothesis II focuses on the CACEO effect within individual companies as measured over the 15 years when chartered accountant CEOs were replaced by non-chartered accountant CEOs or vice versa.

Data and methodology

The data in our sample were obtained from all companies listed on the Johannesburg Securities Exchange (JSE) with a market capitalisation exceeding ZAR4 billion on 31 December 2014. We excluded Real Estate Investment Trusts because they are subject to different tax regimes. Contrary to the approach in many papers, we retained banks and financial institutions in our sample, regardless of the fact that their business models are unique, because research suggests the important role that these companies play as facilitators of corporate tax avoidance.24 Data were collected for the period from 2005 to 2018. A longer time series in the panel helps to allow for more variation in our variable of interest: whether a CEO is a CA or not. Financial data were obtained from Bloomberg, while SAICA's website was used to check whether CEOs are CAs. We did not identify chief financial officers (CFOs) who are CAs, because most CFOs of listed companies are CAs, which provides no variation that is necessary for regression techniques.

We limited our analysis to the larger companies listed on the JSE because we are interested in the tax behaviour of large companies. This resulted in 112 companies, from which we excluded 12 companies due to missing data, resulting in 100 companies.

We tested our hypotheses using multivariate regressions to determine the association between corporate tax avoidance and the CA status of the CEO whilst controlling for other variables. We performed pooled, fixed-effect, cross-sectional and quantile regressions. In the following sections we describe our variables, starting with the regressand, then the regressor, and, finally, the controls.

Effective tax rates as a measure of corporate tax avoidance

The accounting effective tax rate (AETR) is our measure for corporate tax avoidance, calculated as the total expense according to the income statement, expressed as a percentage of pre-tax profit. In addition, we calculate the cash effective tax rate (CETR) as the total of taxes actually paid, expressed as a percentage of profit before tax, as the alternative proxy. These proxies do not capture all types of corporate tax avoidance; however, they are simple, and frequently used in the empirical literature.7,25-27 Low effective tax rates provide evidence of corporate tax avoidance and vice versa. It is accepted that effective tax rates are carefully monitored and perhaps even managed. For example, Investec28, with low effective tax rates, blames a significant drop in profit on a process of "effective tax rate normalisation", indicating that effective tax rates can be managed. Effective tax rates (AETR and CETR) are truncated between 0% and 100%.5

CEOs who are chartered accountants, as a measure of CEO tax knowledge

Our variable of interest as indicator variable is called CACEO, which indicates whether the CEO has tax knowledge. We collected these data for the companies and years under observation, using biographical information on Bloomberg and information on corporate websites and companies' annual reports. The data were verified using SAICA's website. The homogeneous nature of the qualifications of CEOs in the South African landscape29 makes it possible to operationalise tax knowledge attributable to a CEO in this way.

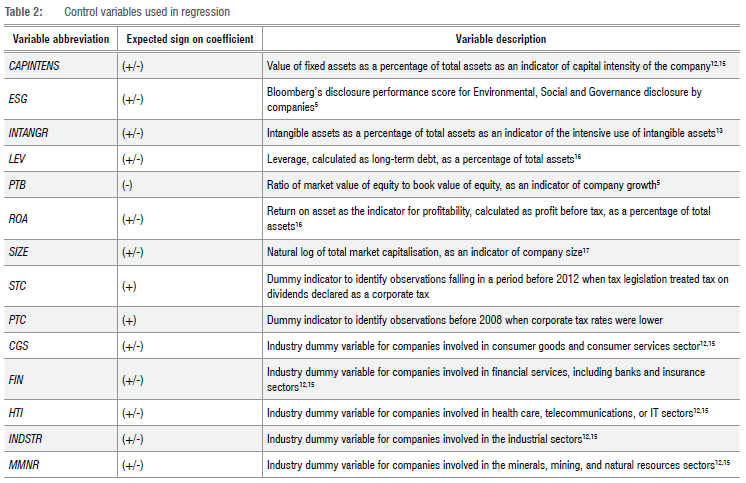

Control variables

Table 2 lists and describes the control variables included in our regressions and the expected coefficient sign.

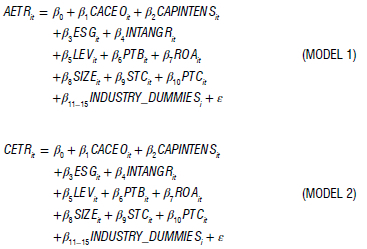

Regression models

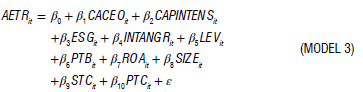

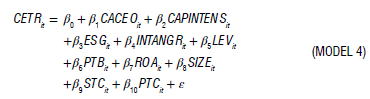

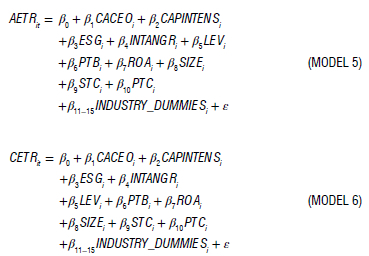

Models 1-2 below are pooled regression models, pooling the observations and disregarding the panel nature of the data. These pooled models combine the within-company and between-company effects. Models 3-1 are company fixed-effect models, run to investigate the within-company effect over the time series only. Models 5-6 present cross-sectional regressions to investigate the between-company effect over the cross-sections only. Models 1-6 investigate the effect of tax knowledgeable CEOs on the conditional average of tax avoidance. Perhaps the effect of a tax knowledgeable CEO is different for different levels of corporate tax avoidance and, therefore, we also perform a quantile regression to investigate this possibility.

Models 3 and 4 are performed to investigate Hypothesis II, and fixed-effect regressions are performed to assess the CACEO effect on tax avoidance within companies. Models 5 and 6 are cross-sectional regressions, aiming to place more emphasis on the between-company effect of CACEO.

Models 1 and 2 (pooled regressions)

Models 3 and 4 (fixed-effect regressions)

Models 5 and 6 (cross-sectional regressions)

The cross-sectional models above (Models 5 and 6) are extended to quantile regressions because of the possibility that CEO effects may vary for different levels of tax avoidance.

Results

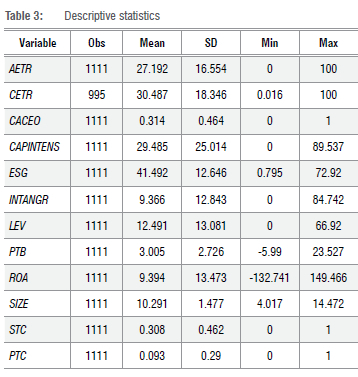

Descriptive statistics

Table 3 presents descriptive statistics for the variables used in the statistical analyses.

Table 3 indicates that the AETR and CETR, the dependent variables in the regressions that follow, are both close to 28%, which is the current corporate tax rate in South Africa (at the time of publication of this paper), although CETR is somewhat higher. The mean of CACEO, the variable of interest being the proxy for a CEO with tax knowledge, is 31.4%, indicating that 31% of the observations had a chartered accountant as CEO (CEO attributed with tax knowledge). The average of CAPINTENS is 29.48%, while some companies appear much more capital intensive, with reference to the maximum of 89.5%. The average of the ESG variable is 41.49%, which seems low perhaps; however, the maximum indicates that some companies are more adept at the disclosure of Environmental, Social and Environmental aspects as based on the maximum score of 72.9%. The average use of intangible assets in business models in large listed South African companies seems moderately low at 9.32%, while the maximum score of 84.74% indicates that some companies are intensive users of intangible assets.

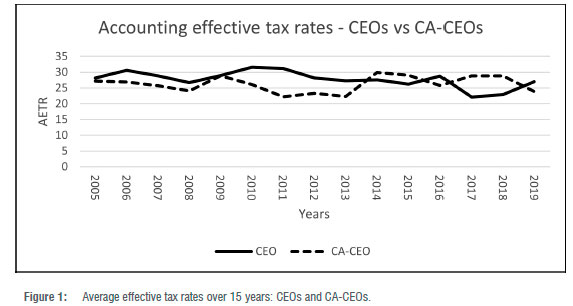

Figure 1 shows descriptive evidence that companies with CAs as CEOs should avoid more tax than other companies, especially relevant to the period from 2005 to 2014. However, in the next section, we subject these data to multivariate regression analyses to investigate the relationship between CACEO and ETRs.

Regression results: Pooled models

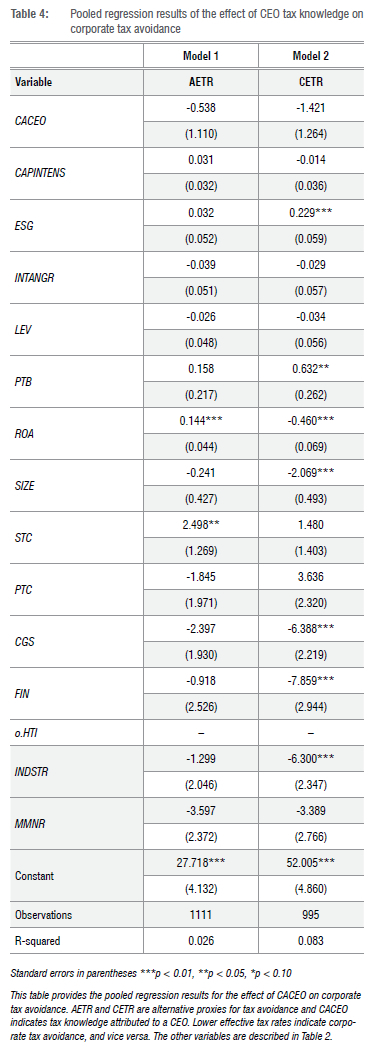

The results of the pooled regression on AETR and CETR are presented in Table 4.

Regression results - Fixed-effect regression

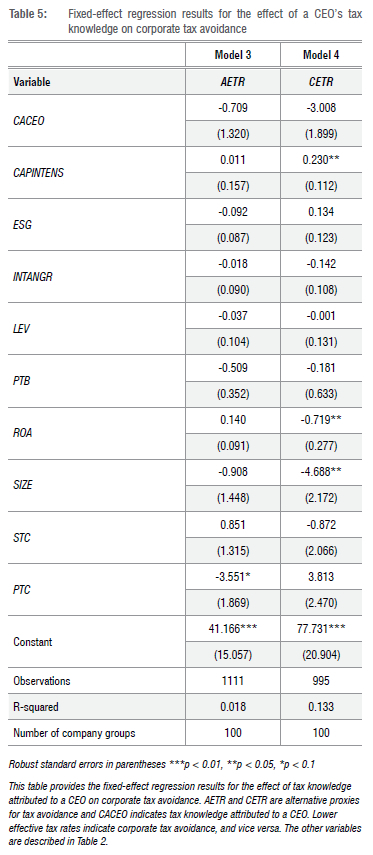

The results of the fixed-effect regression pertaining to Models 3 and 4 are supplied in Table 5. The fixed-effect regression is performed to assess the CEO effect within companies, as CEOs with different tax levels alternate through the years under observation.

Regression results: Cross-sectional regression

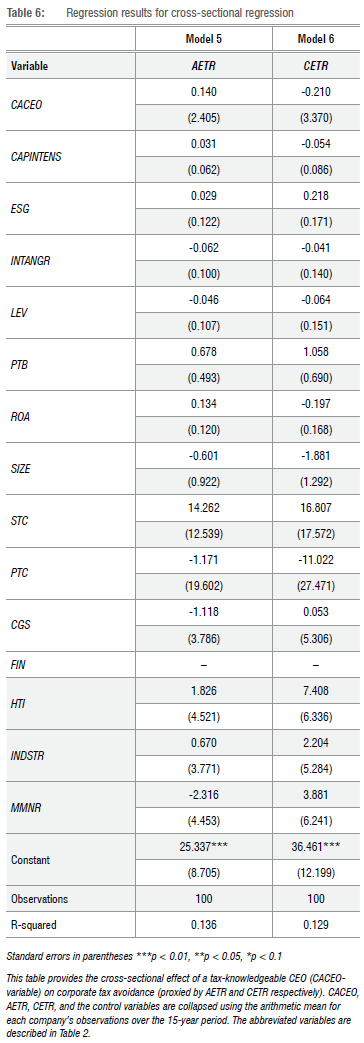

The results of the cross-sectional regression are supplied in Table 6.

Results: Quantile regression

The results of the quantile regression performed on the cross-sectional effect between companies of effect of the CEO's tax knowledge at the different levels are not shown due to space considerations.

Discussion

Pooled regression, fixed-effect regression, cross-sectional regression as well as quantile regression were performed to investigate the association between a tax-knowledgeable CEO and corporate tax avoidance. Our main hypothesis states that a tax knowledgeable CEO will be associated with lower effective tax rates, meaning higher levels of corporate tax avoidance. Support of this hypothesis would be indicated in the form of a statistically negative coefficient on CACEO, the variable of interest. Neither the pooled regression results presented in Table 4, nor the regression results from the fixed-effect regressions presented in Table 5, nor the results of the cross-sectional regression in Table 6 indicate a statistically significant effect on the CACEO variable of interest. This suggests no evidence of the CACEO variable's influence on AETR or CETR as the measurement indicators for corporate tax avoidance. However, the coefficient signs on the CACEO explanatory variable are negative in the regression models, and often significantly so from an economical perspective with reference to the size of the parameter. For example, in the pooled models (Model 2, Table 4) CETR is associated with a -1.421 decline on average when a CEO is attributed with tax knowledge, while the fixed-effect regression models presented in Table 5 show a CACEO coefficient of -3.008. It should be noted that the regression models performed above analyse the association at the conditional mean between the explanatory variables and the dependent variables. Therefore, when we did not find a statistically significant coefficient in those regression models based on the conditional mean, we extended our analysis to quantile regression on the cross-sectional differences to assess whether the influence of the CACEO variable was not perhaps more significant at specific levels of AETR and CETR. The results of the quantile regressions performed of AETR & CETR respectively on CACEO, also indicate statistically insignificant coefficients on the CACEO variable. However, the positive coefficient sign on the CACEO variable changes to a negative sign at the 50th percentile for CETR, and the same happens for AETR where the positive sign of the CACEO coefficient changes to a negative one at the 40th percentile. This means that the CACEO effect is associated with increases in effective tax rates where tax avoidance levels are very low (suggesting corporate tax avoidance), but associated with higher levels of tax avoidance when effective tax rates trend higher, indicating that the CEO effect is picked up, although not significantly so. The changing coefficient on the CEO effect at different levels of AETR and CETR also indicates existence of a corporate governance mechanism: CEOs with tax knowledge manage effective tax rates upwards when they are too low, but manage them down when they are too high, considering that tax is an expense which reduces shareholder value. A look at the coefficients of other significant variables on the pooled regression results reported in Table 4 indicates a statistically significant positive association between ESG and CETR, providing some evidence that those companies with stronger corporate governance, social responsibility and sensitivity toward environmental impact pay more tax on average. This finding in the South African corporate context aligns with empirical evidence reported in the literature14, meaning that companies with more corporate disclosure of corporate governance, environmental and social impact, pay more tax on average. This means that corporate behaviour related to corporate governance and social responsibility act in a complementary fashion with corporate tax behaviour, which can be seen in this context as an extension of responsible behaviour in other behavioural areas.

Company profitability, as measured by variable ROA, is statistically significant in terms of its association with both measures of effective tax rates, but not consistent in terms of the coefficient sign, which varies between the two proxies for corporate tax avoidance. ROA is positively associated with AETR, but negatively so with CETR. This may be explained by a possible tendency of companies to report higher accounting effective tax rates which are reported more conspicuously in financial statements, compared to CETR as another measure of corporate tax avoidance. SIZE is negatively, and statistically significantly so, associated with CETR, which means that larger companies, on average, pay less tax. This supports the theory that larger companies have more resources to develop tax avoidance strategies, which is also reported in the literature.15,18 The statistically significant coefficient on STC is expected because secondary tax on companies increased effective tax rates as a corporate tax. Companies in the consumer goods and financial services industry, as well as industrial companies, indicated by the CGS, FIN, and INDSTR dummy variables respectively, pay significantly less tax on average as far as a negative coefficient is concerned. The fixed-effect regression results reported in Table 5 indicate no statistically significant effect on either CACEO variable of interest. This confirms the results of the pooled regression. In this regard, a significant coefficient on the CACEO variable of interest would have indicated that alternation in the CEO's tax knowledge over the time period covered in this study is associated with variation in corporate tax avoidance. The same result is reported in Table 6, which presents the results of the cross-sectional regression. Overall, the results of these analyses do not provide statistically significant evidence to reject the null hypotheses stated before. This means that CEO tax knowledge based on this sample did not influence corporate tax avoidance.

Conclusion, limitations, and opportunity for further research

We empirically investigated a CEO effect: the influence of tax-knowledgeable and tax-aware CEOs on corporate tax avoidance for large companies listed on the JSE. Our main hypothesis predicts that such CEOs would use their tax knowledge and complementary knowledge of financial management to effect and emphasise corporate tax avoidance to create shareholder value. The CEO effect is conceptualised from upper-echelon theory which attributes significant influence to members of top leadership on all corporate behaviour, including corporate tax behaviour. We used two different forms of effective tax rates to measure tax avoidance, while a CEO's tax knowledge is measured based on the CEO's status as a chartered accountant. The results of our analyses do not support our hypotheses, also indicating less support for the upper-echelon effect on corporate tax avoidance. The results indicate that corporate disclosure on aspects of corporate governance, social and environmental impacts extends to responsible corporate tax behaviour as well, because those companies are associated with less tax avoidance. Our results suggest little evidence for SAICA's claim that the appointment of chartered accountants could result in a reduction in corporate tax expenses. This result, however, bodes well for the reputation of the chartered accountancy profession, given the negative consequences of tax avoidance. Instead, the results of this study indicate evidence that chartered accountants do not use their specialist tax knowledge to enrich shareholders excessively.

From a tax avoidance literature perspective, this study contributes to research on the relationship between CEO characteristics and corporate tax avoidance, specifically regarding CEO skill sets as determinants of corporate tax avoidance. In this regard, it indicates that a CEO's tax knowledge does not necessarily influence corporate tax avoidance. Also, the study contributes to previous studies conceptualised from the upper-echelon effect. To this end, this study shows that the upper-echelon effect is not pervasively present in all aspects of corporate behaviour, in this case corporate tax behaviour.

Indeed, our proxy for a tax-knowledgeable CEO is not a perfect proxy, but others could improve on this attempt by using interviews, or by fine-combing other sources of textual data for biographical information, for example, to identify CEOs with other tax-related education. Our study was partly informed by SAICA's advert which differentiates on this aspect, which we can practically operationalise using publicly available data. Our findings cannot necessarily be extrapolated to all chartered accountants, as the role of CEO of large companies logically exceeds the power and ability associated with the average chartered accountant; however, it is the CEO effect that we investigated as our main focus. Last, effective tax rate, as used and reported in other seminal quantitative studies, is not a perfect proxy for tax avoidance, nor does it distinguish tax evasion from tax avoidance; however, we also did not aim to provide clarity on the difference between tax avoidance and tax evasion, which is becoming ever so grey.

CEOs of large companies are powerful; however, we argue that this power's influence on corporate tax avoidance cannot be reduced to a binary outcome, as far as CEOs could alter their behaviour based on changing priorities as circumstances inform.

Competing interests

We have no competing interests to declare.

Authors' contributions

Rv.d.S.: Conceptualisation; methodology; data collection; sample analysis; validation; writing - the initial draft; writing - revisions; project leadership; project management. Rd.J.: Conceptualisation; methodology; sample analysis; writing - the initial draft; writing - revisions; student supervision; funding acquisition.

References

1. South African Institute of Chartered Accountants (SAICA). You see a healthy profit margin, we see tax implications [webpage on the Internet]. c2015 [cited 2019 Apr 10]. Available from: http://www.accountancysa.org.za/wordpress/wp-content/uploads/issues/2015/ASA-March-2015.pdf [ Links ]

2. De Jager R Van der Spuy R The supply of CAs (SA): A Malthusian trap? Account Rerspect South Afr. 2016;4(1):1-6. https://doi.org/10.2139/ssrn.2796140 [ Links ]

3. Terblanche J. Cultivating socially just responsible citizens in relation to university accounting education in South Africa [document on the Internet]. c2019. [cited 2022 Oct 10]. Available from: https://scholar.sun.ac.za/bitstream/handle/10019.1/107058/terblanche_socially_2019.pdf?sequence=1 [ Links ]

4. Institute of Directors in South Africa (IODSA). King report on governance (King IV) [document on the Internet]. c2016 [cited 2022 Oct 10]. Available from: https://www.adams.africa/wp-content/uploads/2016/11/King-IV-Report.pdf [ Links ]

5. Lanis R, Richardson G. Corporate social responsibility and tax aggressiveness: A test of legitimacy theory. Account Audit Account J. 2012;26(1):75-100. https://doi.org/10.1108/09513571311285621 [ Links ]

6. Kovermann J, Velte R. The impact of corporate governance on corporate tax avoidance - A literature review. J Int Account Audit Tax. 2019;36:1-29. https://doi.org/10.1016/j.intaccaudtax.2019.100270 [ Links ]

7. Dyreng SD, Hanlon M, Maydew EL. The effects of executives on corporate tax avoidance. Account Rev. 2010;85(4):1163-1189. https://doi.org/10.2308/accr.2010.85.4.1163 [ Links ]

8. Wang F, Xu S, Sun J, Cullinan CR Corporate tax avoidance: A literature review and research agenda. J Econ Surv. 2020;34(4):793-811. https://doi.org/10.1111/joes.12347 [ Links ]

9. Bruehne A, Jacob M. Corporate tax avoidance and the real effects of taxation: A review [document on the Internet]. c2019 [cited 2022 Oct 10]. Available from: https://doi.org/10.2139/ssrn.3495496 [ Links ]

10. Hambrick DC, Mason RA. Upper echelons: The organization as a reflection of its top managers. Acad Manag Rev. 1984;9(2):193-206. https://doi.org/10.2307/258434 [ Links ]

11. Greeff C. Corporate effective tax rates: An exploratory study of South African listed firms. S Afr J Account Res. 2019;33(2):99-113. https://doi.org/10.1080/10291954.2019.1638589 [ Links ]

12. Dyreng SD, Hanlon M, Maydew EL, Thornock JR. Changes in corporate effective tax rates over the past 25 years. J Financ Econ. 2017;124:441-463. https://doi.org/10.1016/j.jfineco.2017.04.001 [ Links ]

13. Markle KS, Shackelford DA. Cross-country comparisons of the effects of leverage, intangible assets, and tax havens on corporate income taxes. Tax Law Rev. 2011;65(3):415-432. https://doi.org/10.3386/w16839 [ Links ]

14. Lanis R, Richardson G. Corporate social responsibility and tax aggressiveness: An empirical analysis. J Account Rublic Rolicy. 2012;31(1):86-108. https://doi.org/10.1016/j.jaccpubpol.2011.10.006 [ Links ]

15. Davis AK, Guenther DA, Krull LK, Williams BM. Do socially responsible firms pay more taxes? Account Rev. 2016;91(1):47-68. https://doi.org/10.2308/accr-51224 [ Links ]

16. Gupta S, Newberry K. Determinants of the variability in corporate effective tax rates: Evidence from longitudinal data. J Account Rublic Rolicy. 1997;16(1):1-34. https://doi.org/10.1016/S0278-4254(96)00055-5 [ Links ]

17. Rego SO. Tax-avoidance activities of US multinational corporations. Contemp Account Res. 2003;20(4):805-833. https://doi.org/10.1506/VANN-B7UB-GMFA-9E6W [ Links ]

18. Kim KA, Limpaphayom P. Taxes and firm size in Pacific-Basin emerging economies. J Int Account Audit Tax. 1998;7(1):47-68. https://doi.org/10.1016/S1061-9518(98)90005-2 [ Links ]

19. Olsen KJ, Stekelberg J. CEO narcissism and corporate tax sheltering. J Am Tax Assoc. 2016;38(1):1-22. https://doi.org/10.2308/atax-51251 [ Links ]

20. Phillips JD. Corporate tax-planning effectiveness: The role of compensation-based incentives. Account Rev. 2003;78(3):847-874. https://doi.org/10.2308/accr.2003.78.3.847 [ Links ]

21. Gaertner FB. CEO after-tax compensation incentives and corporate tax avoidance. Contemp Account Res. 2014;31(4):1077-1102. https://doi.org/10.1111/1911-3846.12058 [ Links ]

22. Law KKF, Mills LF. Military experience and corporate tax avoidance. Rev Account Stud. 2017;22(1):141-184. https://doi.org/10.1007/s11142-016-9373-z [ Links ]

23. Mey E, De Klerk M. Association between having a CA (SA) as CEO and accruals quality. Meditari Account Res. 2015;23(3):276-295. https://doi.org/10.1108/MEDAR-09-2014-0056 [ Links ]

24. Gallemore J, Gipper B, Maydew E. Banks as tax planning intermediaries. J Account Res. 2019;57(1):169-209. https://doi.org/10.1111/1475-679X.12246 [ Links ]

25. Dyreng SD, Hanlon M, Maydew EL. Long-run corporate tax avoidance. Account Rev. 2008;83(1):61-82. https://doi.org/10.2308/accr.2008.83.L61 [ Links ]

26. Mills L, Erickson MM, Maydew EL. Investments in tax planning. J Am Tax Assoc. 1998;20(1):1-20. https://doi.org/10.2308/jata.2001.23.L1 [ Links ]

27. Richardson G, Lanis R. Determinants of the variability in corporate effective tax rates and tax reform: Evidence from Australia. J Account Public Policy. 2007;26(6):689-704. https://doi.org/10.1016/j.jaccpubpol.2007.10.003 [ Links ]

28. Investec Bank. Investec pre-close trading update 18 September 2020 [webpage on the Internet]. c2020 [cited 2021 Mar 11]. Available from: https://www.investec.com/content/dam/investor-relations/presentations-and-announcements/investor-briefing/september-2020/Investec-Pre-close-trading-update-18-September-2020.pdf [ Links ]

29. South African Institute of Chartered Accountants (SAICA. On the board [webpage on the Internet]. c2016 [cited 2020 Oct 22]. Available from: http://www.jsemagazine.co.za/company-profiles/board/ [ Links ]

Correspondence:

Correspondence:

Pieter van der Spuy

Email: vanderspuy@sun.ac.za

Received: 01 Feb. 2023

Revised: 31 July 2023

Accepted: 14 Aug. 2023

Published: 29 Nov. 2023

Editor: Ebrahim Momoniat

Funding: None

{kind=link}