Serviços Personalizados

Artigo

Inglês (pdf)

Inglês (pdf)

Artigo em XML

Artigo em XML Referências do artigo

Referências do artigo

Indicadores

Links relacionados

-

Citado por Google

Citado por Google -

Similares em Google

Similares em Google

Compartilhar

Permalink

PermalinkSouth African Journal of Science

versão On-line ISSN 1996-7489

versão impressa ISSN 0038-2353

S. Afr. j. sci. vol.118 no.5-6 Pretoria Mai./Jun. 2022

http://dx.doi.org/10.17159/sajs.2022/13289

RESEARCH ARTICLE

Trajectories for South African employment after COVID-19

Miriam Altman

Professor of 4IR Practice, School of Economics, University of Johannesburg, Johannesburg, South Africa

ABSTRACT

The COVID-19 health response shut down the South African economy for a period, and then continued to constrain face-to-face services such as tourism, hospitality and personal services. These industries create the majority of jobs in all middle- and high-income economies. The COVID-19 interventions further aggravated pre-existing and rising unemployment and poverty levels. By 2021, only 42% of the working-age population in South Africa was employed, as compared to the National Development Plan's target of 60% by 2030. South Africa has had high unemployment since at least 1978, with an historical policy path that appears to direct the economy towards slow growth and low employment. This article outlines the results of employment scenarios modelling: the purpose is to envisage the future of employment in South Africa in the context of the COVID-19 pandemic, with a view to 2050. Two 'plausible' scenarios are modelled. The upper and lower trajectories are aligned to historical growth paths between 1970 and 2019, with three decades experiencing an average 1.5% GDP growth and two decades an average 3.6% growth. An average economic growth rate rising from 2% to 3.5% between 2022 to 2050 would result in the achievement of the National Development Plan's employment targets. The modelling also shows what the employment trajectory might have been in the absence of the COVID pandemic.

SIGNIFICANCE:

• This article evaluates the potential pathway for South African employment after COVID-19.

• After a rapid and significant fall caused by policies to manage COVID-19, employment might only recover to peak 2018 levels by 2024-2026.

• The COVID-19 pandemic may have long-term implications for employment. In the absence of the pandemic, there could have been between 500 000 and 1.6 million more people working by 2050.

Keywords: economy, COVID-19, employment, recovery, growth

Introduction

The COVID-19 health response has caused economic crises globally. The interventions specifically targeted face-to-face activity, which is the main source of employment in middle- and high-income economies.1 Constraining these services is especially damaging for women and youth, whose main work opportunities are found in services driven by such face-to-face activity - like personal services, hospitality, tourism and retail. Many countries have implemented some combination of economic lockdown and 'risk-adjusted strategies' to balance the COVID-19 health risks and other social and economic risks. The way that developed economies locked down activity was emulated in some developing economies, including South Africa.

South Africa has extremely high rates of unemployment, poverty and inequality. As a country that seeks to reverse the damaging effects of its apartheid past, achieving full employment, eradicating poverty, and reducing inequality are the apex goals, reflective of the Constitution and as translated into the National Development Plan.2 This article focuses on the employment objective. Since the advent of democracy in 1994, there have been notable successes in creating employment and reducing unemployment. However, there were reversals prior to the onset of the COVID-19 pandemic. The policy responses to contain the COVID-19 pandemic resulted in significant negative impacts on employment, to the extent that unemployment rates have reverted to those seen in the mid-1990s. The economic crisis caused by local and global COVID-19 policy responses and its impact on employment therefore need to be understood in relation to the country's historical challenges and long-range aspirations.

This article presents the potential path for South African employment and unemployment in the aftermath of the COVID-19 pandemic, based on findings of employment scenarios modelling. The employment context as relevant to the scenarios is laid out and the approach to the scenarios is explained. Two employment scenarios to 2050 are presented and compared to what might have happened in the absence of COVID-19.

Employment and unemployment in South Africa

South Africa has had high unemployment since at least 1978, with an historical policy path that appears to direct the economy towards slow growth and low employment.1,2

There has been some debate about whether South Africa leans to jobless or job-creating growth.1 However, the evidence clearly indicates that there is a close relationship between employment and growth. High unemployment has not been caused by jobless growth, but rather the absence of growth.

Growth has been persistently slow over the past 50 years, with per capita GDP growth averaging around 1.6% per annum as seen in Figure 1.3 There were only two meaningful accelerations - in the 1960s and 2000s - but they were not sustained. Table 1 shows that in the past 50 years there were three decades with an average GDP growth rate of between 1.4% and 2.0% and two decades with an average growth rate of 3.6%.4

In South Africa, for every 1% GDP growth, employment can be expected to grow by about 0.6% to 0.7%.1,5 By global standards, this employment elasticity of growth is high and may be explained by slow productivity growth. For example, the average employment elasticity between 1995 and 2003 was 0.14 to 0.18 in East Asia, 0.20 to 0.42 in Southeast Asia, 0.41 to 0.64 in Latin America, and 0.21 to 0.34 in developed economies.5

Between 2001 and 2008, a period of positive economic growth, employment expanded by 2.4 million and the unemployment rate fell from 30% to 23%. The employment elasticity of growth was 0.6 over this period.1

The South African economy experienced falling rates of GDP growth from 2009, and negative growth in 2019 as shown in Figure 2.4 Real GDP per capita in 2019 was the same as for 2007. In the period from the second quarter of 2008 to 2019, employment grew slowly. Approximately 1.7 million jobs were created, as compared to 4.1 million people added to the labour market.6 As a result, the official (broad) unemployment rate rose from 21.5% (26.2%) in the fourth quarter of 2008 to 29.0% (36.6%) in the second quarter of 2019. The proportion of the working-age population in employment fell from 46.2% to 42.4% over the same period.

Falling growth rates over a sustained period suggest the possibility of underlying structural and/or institutional factors that contain potential growth rates. It is possible to break out to higher rates of growth and development with sustained commitment to actions that reform markets and public institutions; however, South African growth metrics indicate that this has not yet happened. Figure 1 compares per capita growth in a number of emerging and developing economies between 1960 and 2020. South Africa has fallen behind comparator countries and especially other middle-income economies, even since the transition in 1994.3

Employment impacts of the COVID-19 pandemic policy response

Some observations can be made about the impact of the COVID-19 pandemic policy response on employment.

The initial lockdown in March to June 2020 resulted in the loss of 2.24 million jobs, and by the second quarter of 2021, total employment was still 1.44 million lower than at the onset of the lockdown.6 These high-level employment indicators mask the possible ways that preexisting inequalities may have deepened.

There are important race, age, and gender dynamics associated with employment, unemployment, and poverty levels in South Africa. These dynamics are found globally, but are particularly extreme in South Africa due to its historical legacy. The imperative to achieve higher economic and employment growth rates is particularly important from the perspective of creating a future in which the whole population enjoys more-equitable access to the opportunity to achieve a decent standard of living.

South Africa has had high black African unemployment since the 1970s; this figure exceeded 20% by 197 82 and the trend has persisted. In 2018, 84% of all those not in education, training or employment (NEET) were black African, accounting for 42% of the black African working-age population. By 2021, 50% of the black African population were NEET. By comparison 25% of the white population were NEET in 2018.7

Women's prominence in face-to-face service work has resulted in disproportionately negative labour market outcomes. Women were more likely to lose their jobs in the initial lockdown period, accounting for two thirds of the jobs lost in the first lockdown period. Employment recovery as the economy opened was slower for women than for men. By March 2021, men's employment and working hours appeared to have restored to pre-pandemic levels, compared with women whose employment and working hours were still 8.4% and 6.0% below pre-lockdown levels, respectively. In addition, the disproportionate domestic responsibility carried by many women was deepened in the context of school closures and families working from home. By March 2021, the presence of children in the household continued to reduce the probability of employment for women, but did not have this effect on men.8

Pre-pandemic, 69% of white adults were employed as compared with 40% of black adults. By mid-2021, these figures had fallen to 67% and 36%, respectively. Women in the informal sector were particularly hard hit, with an employment drop of 16% by mid-2021 as compared with a fall of 3% for men.9

The closure or containment of workplaces has in many cases assumed that work would take place at home. The ability to work from home is positively correlated with socio-economic status, the type of home, educational attainment and earnings. For example, those who could work from home earned an average of about one-third more than those who could not work from home. In the South African context, this therefore translates into a race bias, with black African workers least able to work from home and/or being in types of employment that cannot be done from home.10

Low-paid workers (earning less than ZAR3000 per month) were eight times as likely as top earners (earning more than ZAR24 000 per month) to have lost their jobs in the initial lockdown of March/April 2020. Black African workers had a 43% probability of losing their job, compared with 17% for white workers.11 At the time of writing this article, the pathway of employment recovery is still unclear. There has been significant labour market churn below the aggregate numbers: almost one quarter of those employed in February 2020 were no longer employed a year later, and almost one third of those without employment in February 2020 did find employment by March 2021.

Youth unemployment is a global phenomenon, and is usually about two to three times the national rate. In 2018, about 50% of NEETs were aged 15-24. High unemployment therefore specifically entrenches racial disparities for the future. The pandemic hit youth employment disproportionately, with employment of workers under 35 falling by 14%; they accounted for two thirds of all formal-sector job losses between the first quarter of 2020 and the second quarter of 2021, despite having accounted for only one third of total formal employment pre-COVID.9 There is some indication that older workers left the labour market and that youth were net gainers in the recovery.12

Employment recovery after economic crisis

Previous experience of economic crises may be an indicator of how employment recovery might progress after COVID.

The 2008 global economic crisis is the most recent pre-COVID-19 example of South Africa's response to a global shock, although its causes and character differed, emanating from a financial crisis with its epicentre in the USA. In that crisis, developing and emerging economies reverted to pre-crisis levels of output within 2 years, while advanced economies that were at the epicentre took longer to be restored.13

Unlike other emerging economies where the impact of the global economic crisis was transmitted largely via decreases in traded manufactures and remittances, South Africa was impacted largely by decreases in private-capital inflows, commodity exports, and trade revenues.14

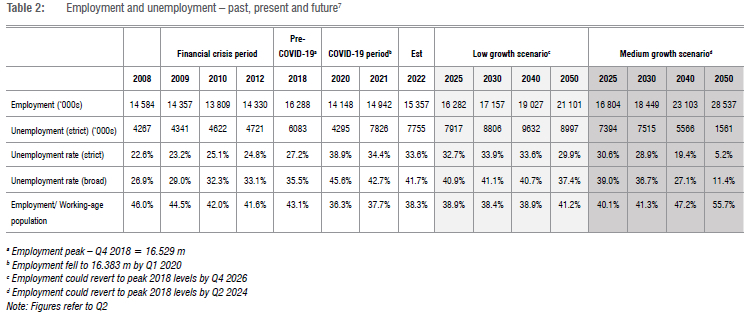

The global economic crisis took some time to reach South Africa. While the financial crisis took place in 2008, South African output fell by 1.5% in 2009 and recovered to pre-crisis levels in 2010. The fall in employment lagged and was substantially larger than that in output. Table 2 offers a picture of employment losses and gains during the global economic crisis. Employment fell by almost 10% (1.466 million) between the fourth quarter of 2008 and the third quarter of 2010 (almost 2 years). Employment recovered to pre-crisis levels by the second quarter of 2013 (almost 3 years). Even though employment levels were restored, unemployment rose.14

The pathway to recovery from the economic crisis emanating from the COVID-19 health response would be different from that due to a domestic or global crisis that is caused by market phenomena. This is because the initial channel into the economy is direct, with government shutting down activity by fiat. The second channel arises through other global phenomena such as trade flows and cross-border movement of people.9,15-17

The World Bank expects developing countries and emerging markets to be slower in reverting to pre-crisis levels of output this time, compared with the majority of developed countries, which have invested heavily to stimulate their economies in a way that developing economies cannot.13

The process of designing and implementing policy to manage the evolving pandemic changed over time, requiring considerable monitoring and adaptation. The impact of the economic policy responses is not yet known, and information is provided here simply for context. The President invoked a State of Disaster and established the National Command Council. The first phase of the response involved an almost complete economic and social lockdown for 35 days, followed by a month in a slightly more open lockdown phase. Thereafter, there was a process of re-opening economic activity. A risk-adjusted approach reflecting an acceptance of the idea that the containment of the pandemic would have to be balanced with other social, economic, and health considerations was introduced in May 2020. In 2021 and 2022 there has been growing capacity to enable the use of non-pharmaceutical interventions and vaccination of the adult population, which together could pave the way for a full return to work.

Some economic and social measures were put in place by the public and private sectors to support individuals and businesses adversely affected by policies aimed at containing the pandemic. Some examples are the loan guarantee schemes; the introduction of a special wage subsidy; and COVID-TERS, which was funded by the Unemployment Insurance Fund.9 Support of ZAR350 per month was introduced as part of the Social Relief of Distress programme for unemployed persons who do not access other social grants, in recognition of the surge in the number of food-insecure adults who would otherwise have no other means.

Government introduced the Economic Reconstruction and Recovery Plan in October 2020.18 It was aimed at driving immediate interventions for economic recovery amid COVID-19, but also at 'rebuilding and growing the economy'. Some of the most prominent elements included a commitment to expanding infrastructure investment and introducing reforms to network industries such as transport and energy. It also introduced an employment stimulus aimed at creating public-sector-funded social-economy jobs aimed especially at youth.

After an overall decline in GDP by 6.4% in 2020, there was a 4.8% recovery in 2021 and a forecast of 1.7% growth for 2022.19 Output, which fell due to the economic shutdown locally and globally, is expected to recover within approximately 2.5 years. By comparison, 2.2 million jobs were lost in the second quarter of 2020, accounting for 13.6% of total employment. Only 800 000 jobs were recovered a year later.6 It is expected that in 2022 there will still be one million fewer employed than in the pre-crisis period, as seen in Table 2.

Employment scenarios in a post-COVID-19 pandemic future

The purpose and design of employment scenarios

I have prepared employment scenarios for South Africa since 2004. They were the foundation for the Human Sciences Research Council's Evidence-based Employment Scenarios, which were prepared before and after the 2008 global economic crisis. These scenarios contributed to the setting of national targets in respect of employment and related policies.1,20 The second major set of scenarios was prepared for the National Planning Commission in the South African Presidency for the National Development Plan.21 A smaller employment scenarios exercise was done in the early phase of the COVID-19 pandemic.22

Futuristic scenarios were used to help visualise the following:

• A future state in which there is significant structural change associated with the development process.

• A pathway to solving for a seemingly intractable challenge such as extreme unemployment, poverty, and inequality as found in South Africa.

• Possible validation of a current path, or the identification of risks that require attention and course correction towards the desired path and end goal.

Employment generally grows incrementally and, if sustained, expands in a cumulative fashion, in some proportion to output growth. In the context of very high unemployment, small variations in economic and employment growth rates can seem trivial in the near term. However, these small differences can make a very significant impact when sustained over decades.

Methodology

When the employment scenarios were done previously at the Human Sciences Research Council and for the National Planning Commission, the government's national target of halving unemployment and achieving full employment was set, and a path to achieving that goal proposed. These scenarios were prepared in the belief that the installation of a new regime and democratic government would bring significant change in institutional and policy orientation that could guide the way to faster employment creation and economic inclusion. The purpose was realising a future with full employment, with a view to the high-level targets as well as second-order targets and dependencies. The method involved defining and calculating the half-unemployment mark and then linking it to other metrics such as employment or labour force participation. In 2004, the target official unemployment rate was 14% by 2014 and 6% by 2024. In the National Development Plan, those targets were shifted outwards to 2020 and 2030, respectively. More importantly, the National Development Plan set an employment target of 11 million jobs created between 2010 and 2030, with the aim of 60% of the working-age population being employed by then.

The employment scenarios presented in this article use a different method. They do not involve the setting of future goals and do not assess how to achieve any specific employment goal. Instead, they focus on two plausible economic trajectories and then apply a set of assumptions to model possible employment and labour market outcomes.

The COVID-19 pandemic has had especially negative impacts in our country that is already challenged by extremely high unemployment. These employment scenarios are aimed at revealing possible trajectories for employment recovery coming out of the pandemic, and up to 2050.

The gravitational pull of South Africa's path was underestimated in this earlier work. Path dependence and the challenges associated with significant institutional and policy reorientation have to be accounted for in any temporal thinking around change. The two scenarios described in this article are shaped by plausible outlooks in the context of this institutional experience.

With this in mind, the employment scenario modelling has been revised from earlier versions to take account of potential economic growth, the relationship between employment and growth, labour market growth, and official versus broad unemployment.

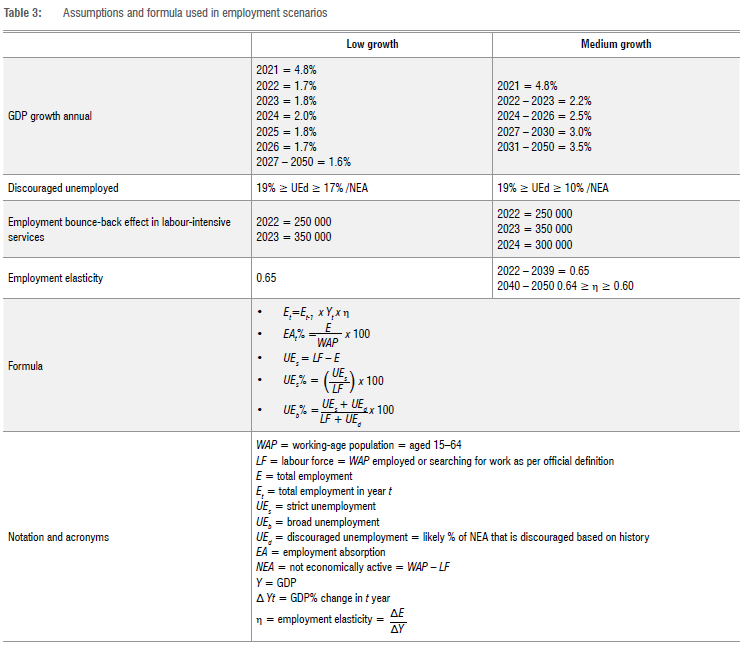

A simple linear model is used. The assumptions and formula are presented in Table 3. The reasoning behind these assumptions are explained in the previous section. It is assumed that:

• The lower-bound GDP growth rate falls to 1.6% per annum on average and the higher-bound growth rate rises to an average of 3.5% per annum. In the near term, the modelling uses recent forecasts by the South African Reserve Bank, which sees GDP growth falling to 1.7% in 2022 and rising to 2% by 2024.23 The potential growth rate rises as economic capacity expands, and can therefore be influenced. It had risen to 3.5% by 2008, but fell to 1.7% between 2010 and 2015.24 The potential growth rate is now estimated to fall below 1%.23,25

• The employment elasticity of growth ranges between 0.60 and 0.65. The modelling assumes that employment grows by more than 0.65% of GDP growth in the near term. This takes account of expected further recovery of jobs in labour-intensive activities such as retail, personal services, tourism, and hospitality. The elasticity then falls to 0.60.

• Between Quarter 3 of 2019 and Quarter 3 of 2021, 1.136 million jobs had still not been recovered in the highly labour-intensive 'trade' and in 'social and community services'. It is assumed that 600 000 to 900 000 jobs are added in a lagged recovery of these services between 2022 and 2024.

• 63% of the growth in the working-age population consists of those entering the labour market each year and 37% becoming not economically active, as has been the case over the period from the fourth quarter of 2008 to the fourth quarter of 2018.6 Over the period from 2008 to 2018, approximately 63% of the growth in the working-age population entered the labour market and 37% were not economically active.

• Estimates on labour market growth rely on United Nations population projections. These foresee annual growth in the South African working-age population falling from about 550 000 currently to about 150 000 by 2050.26 This demographic transition has a significant positive impact on unemployment rates after 2030.

Employment outcomes in the low- and medium-growth scenarios are then compared to what might have happened in the absence of the COVID-19 crisis. It is assumed that employment could have grown by about 1% in 2020 and 2021, had the economy expanded by about 1.6% in each of those years. Growth of 1.6% per annum would be consistent with the South African Reserve Bank and other assessments of the potential growth rate of the South African economy.25

Results

Two simple employment scenarios to 2050 are modelled, with results presented in Table 2. The modelling assumptions are found in Table 3. Figure 3 offers a visual of employment and unemployment pathways in these two scenarios.

Both scenarios are domestically focused, even though South Africa is highly vulnerable to global cycles. Neither scenario is concerned with global dynamics, because resilience domestically will aid in reversing decline, accelerating growth and development, and responding to global up- and downswings.

Scenario 1 envisions low growth, recovery from the COVID-19-policy-induced economic crisis, and a reversal of the pre-COVID-19 economic decline. In this scenario, GDP grows by 1.7% in 2022, falling to an average of 1.6% per annum from 2027 to 2050. This is aligned with forecasts by the South African Reserve Bank and its assessment of potential economic growth prior and subsequent to the onset of COVID-1 9.23,25 Also in this scenario, employment reverts to 2018 levels by 2025; about 5.74 million jobs are created between 2022 and 2050; and strict and broad unemployment both rise, as an average of 205 000 jobs created annually is not sufficient to absorb labour market entrants. By 2050, there are 21 million people working and 12.6 million unemployed or discouraged. The strict and broad unemployment rates are 29.9% and 37.4%, respectively. Only 41.2% of the working-age population is employed.

Scenario 2 envisions medium growth for a sustained period. GDP growth is 2.2% per annum in 2022 and rises to an average of 3.5% per annum from 2031 to 2050. The investment in human and institutional capacity causes the potential growth rate to rise steadily over this period. Also in this scenario, employment reverts to 2018 levels by 2023 or 2024; about 13 million jobs are created between 2022 and 2050; and the rates of strict and broad unemployment both fall, with an average of 470 000 jobs created annually. By 2050, there are 28.5 million people working and almost 3.7 million unemployed or discouraged; the strict and broad unemployment rates are 5.2% and 11.4% respectively; and almost 56% of the working-age population is employed. On the way to full employment, the number of unemployed is far lower than in scenario 1 but is nevertheless significant for most of this period. For example, there are 10.6 million broadly unemployed in 2030, with this falling to 8.6 million by 2040.

Scenario 2 is likely the best possible outcome South Africa could achieve to 2050. However, scenario 1 does not represent the worst South Africa could face.

Failure to reverse the underlying causes of economic decline from 2010 would result in further deterioration in state capacity and services, thereby undermining production capacity of the economy as well as alienating investors, skilled personnel, and communities. Stagnation and/ or economic contraction can result in a downward spiral and dramatic political upheaval, which could in turn lead to economic contraction, employment loss, diminishing human and institutional capacity, as well as reduced availability of public resources to pay for critical economic and social expenditures. Nevertheless, a third scenario was not prepared as it would require a different methodology. South Africa has seen decades of misdirected, wasteful, and harmful resource allocation and practices, and nevertheless muddled through at low rates of growth. Examples range from separate development policies, isolationism that led to international sanctions, and deep military expenditure in the 1970s and 1980s to the arms deal of 1998 and, more recently, state capture. This is the context for historical slow growth and rising unemployment in the black population. The character of economic decline would require an understanding of its special dynamics.

Table 4 shows how these scenarios would have differed in the absence of the COVID-induced crisis. All the assumptions are the same as those in the two scenarios, except insofar as 2020 was a year of anaemic growth and not one of severe contraction. Slow growth, rather than a growth spurt associated with recovery, is found in 2021 to 2023. The losses that take place in 2020 are never fully recovered even by 2050. Employment grows cumulatively wherein each year's growth is on the back of the previous year's. A one-year slide can have significant impacts on long-term success. In a low-growth scenario, 1.6 million more people would have been working by 2050 in the absence of COVID. The strict unemployment rate would have sat at around 28%, with 44% of the working-age population employed. In the medium-growth scenario, faster GDP growth would have narrowed this gap: by 2050, there would have been about 500 000 more people working in the absence of COVID and 56.7% of the working-age population would have been in employment.

Discussion

The initial exuberance in the post-democratic era in envisioning much-improved rates of employment was dampened by the evident challenges in implementing institutional reform aimed at achieving sustained inclusive growth.

Efforts towards building state capacity development and achieving economic reform that started around 1996 finally seemed to make a positive impact on economic and employment growth from the early 2000s. These gains have been severely reversed as a result of 'state capture', which has hollowed out significant parts of state capacity and therefore undermined the quality of public spending and services, which has in turn undermined economic capacity.21

There are important areas of economic and social policy that have not been addressed sufficiently in the democratic era. Most notably these include a housing policy that located settlements far away from economic activity, weak passenger transport systems that entrench a high cost of living, and limited access to quality health and education systems, with the result that the indices of human development for South Africa align more closely with those of a low-income country. Current policy behaviour in important areas that underpin the employment orientation of the economy persists in mirroring pre-1994 approaches, even though the policy agenda associated with separate development was discontinued. This might also be seen as a form of hysteresis, where historical approaches have not been replaced sufficiently with new know-how appropriate to the structural change that is consistent with the current agenda for inclusive growth.7,21,27-29.

Employment and growth are outcomes of actions and are not impacted directly. Growth is an outcome of success in building the country's capital and human asset base, developing appropriate and strong institutions, and raising technological capability. Employment, in particular, relies on growing urban areas with integrated and well-designed human settlements, policies that enable business activities and competition, thriving productive rural areas, an affordable cost of living, and investment in lifting human development and capabilities. The apartheid separate development policy promoted the opposite approach and was effectively a low-employment policy. This explains why economic growth has been slow since the 1970s and why black African unemployment exceeded 20% by 197 82 and continued to rise for the next 20 years to reach 36% by 1998.6

The economic policies aimed at containing COVID-19 in South Africa must be understood within this context. In a country with high unemployment, extensive poverty and slow growth, constraining or locking down economic activity can be devastating. This is particularly so where the focus of the lockdown is on the industries where most people work. Initially, the rationale for a lockdown was to create opportunity to put into place capacity in the health system. In 2020 and 2021, policymakers juggled health and economic decisions, shifting from lockdowns to 'risk-adjusted strategies'.22 In this vein, possible explanations for each scenario may be found.

Slow positive growth in Scenario 1, rather than continued decline, could arise from actions that stabilise the economy, enable the restoration of economic activity and introduce stronger institutional governance in key institutions. Examples might include21,22,27-29

• Success in vaccinating the population and related actions to manage COVID-19 in ways that enable a return to work.

• Support for businesses specifically harmed by COVID-19, such as tourism businesses and small and microenterprises, a managed opening up of the economy to full services, and stronger commercial diplomacy with key markets to restore and promote trade and tourism.

• A progressive introduction of capable leadership in key locations is found in the public sector, ranging from top infrastructure state-owned enterprises such as Eskom, Prasa and Transnet, to the leadership of key municipalities and oversight of infrastructure procurement and delivery.

• A growing ability for the public and private sectors to partner.

• The worst excesses in crime and corruption in both sectors are brought under control.

Sustained economic growth in Scenario 2 might be found with implementation of actions that go deeper into strengthening key state institutions. Examples include7,21,22,27-29

• implementing meaningful reforms that encourage greater dynamism and institutional learning in public and private sectors and in communities

• strengthening fiscal and financial management

• transforming state-owned enterprises involved in infrastructure delivery to be more dynamic

• building state capacity to strengthen delivery

• deepening quality and impact in public education and health services

• densifying housing and creating thriving human settlements located near economic activity

• activating communities to participate in service delivery

• enabling small local businesses to thrive

Conclusion

Most countries globally have experienced severe labour market impacts as a result of economic interventions aimed at containing the COVID-19 pandemic. These impacts are particularly challenging in South Africa with its extremely high pre-existing unemployment rates. Two scenarios were modelled to assess plausible future pathways for employment growth in South Africa. The scenarios are focused on plausible pathways given the significant institutional resistance to reforming the economy towards a dynamic employment-absorbing path. The low-growth scenario sees an average annual GDP growth rate of 1.6% to 2050, resulting in a 30% unemployment rate. This could not be achieved under status quo conditions: it would require basic reforms in leadership, governance, accountability and in crime and corruption that reverse economic decline. The medium-growth scenario sees an average annual GDP growth rate rising from about 2.2% in 2022 to 3.5% by 2031. If sustained, the unemployment rate falls to 5% by 2050. This would require significant institutional reforms to drive greater economic dynamism, competition, small business activity, regional integration and trade. Most importantly, it would involve intensified investment in human capacity.

Several research questions emanate from this work:

• A scenario of decline was not prepared. I propose that a different methodology would be required to determine the factors that might cause contraction over sustained periods. South Africa has not yet experienced this, despite significant resource mis-allocation over many decades.

• The UN forecasts a demographic transition in South Africa, as the population ages and the youth bulge becomes smaller. Unemployment rates fall faster as a result after 2031. This also has implications for other social policy, most notably sustained fiscal resources to support an aging population that is dependent on a small working population. This should increase pressure to stimulate the economy and provide social protection that can be sustained for decades.

• It is possible that there could still be about 8 million unemployed by 2040, even in the best scenario. A faster pace of economic reform and stimulation is needed, combined with a sustainable social protection policy so that all households can reasonably chart to a decent standard of living, even in this challenging context.

• The modelling makes assumptions about the employment elasticity of growth, which has been high in South Africa, possibly due to low productivity growth. Economic policy can be framed to elevate the employment elasticity of growth, with an emphasis on employment absorbing activities.

• It is possible that employment does not fully recover to pre-crisis levels due to hysteresis. Lower employment levels may persist, even once the COVID-19 crisis has passed and industries have become fully operational. If this happens, one explanation would point to employers learning how to deliver the output with fewer workers and/or with fewer work hours. The pandemic-induced postponement of investment plans can also result in foregone job creation.14,15

• In the near term, the scenarios foresee employment recovering to its 2018 peak by 2024 to 2026: in 2022, there may still be a shortfall of over 1.2 million jobs. The pace of employment recovery depends considerably on policy choices in respect of safely restoring economic and social activity and in stimulating the movement of people between major trade and tourism partners.

Acknowledgements

The author thanks the two referees for their helpful advice in refining this article. Mr Dikgang Kekana is also gratefully acknowledged for his language editing. The guidance offered in webinars held by the South African Reserve Bank and by the COVID-19 Economists Group was invaluable.

Competing interests

I have no competing interests to declare.

References

1. Altman M. The challenge of employment creation in South Africa. In: Pillay U, Hagg G, Nyamnjoh F, Jansen JD, editors. State of the nation: South Africa 2012-2013: Addressing inequality and poverty. Pretoria: HSRC; 2013. p. 185-221. Available from: https://miriamaltman.com/research/the-challenge-of-employment-creation-in-south-africa/ [ Links ]

2. Bell T. Unemployment in South Africa: Occasional paper number 10. Durban: University of Durban-Westville Institute for Social and Economic Research; 1984. Available from: http://scnc.ukzn.ac.za/doc/COMM/labour/Bell_Trevor_Unemployment_SA.pdf [ Links ]

3. World Bank. World development indicators. Series on GDP per capita in constant 2010 US dollars. Washington DC: World Bank; 2022. Available from: https://databank.worldbank.org/source/world-development-indicators# [ Links ]

4. South African Reserve Bank. South Africa: Gross domestic product by expenditure approach, 2015 rand. Pretoria: South African Reserve Bank; 2022. [ Links ]

5. Altman M. Revisiting South African unemployment trends in the 1990s. S Afr J Econ. 2008;76(S2):S126-S147. https://doi.org/10.1111/j.1813-6982.2008.00185.x [ Links ]

6. Statistics South Africa. Quarterly labour force survey. Pretoria: Statistics South Africa. Available from: http://www.statssa.gov.za/?s=QLFS&sitem=publications [ Links ]

7. South African National Planning Commission. Economic progress towards the National Development Plan's vision 2030: Recommendations for course correction. Pretoria: National Planning Commission, The Presidency; 2020. Available from: https://www.nationalplanningcommission.org.za/assets/Documents/Review%20of%20Economic%20Progress%20NPC%20Dec%202020.pdf [ Links ]

8. Casale D, Shepherd D. The gendered effects of the COVID-19 crisis and ongoing lockdown in South Africa: Evidence from NIDS-CRAM Waves 1-5. Dev South Afr. Forthcoming 2022. https://doi.org/10.1080/0376835X.2022.2036105 [ Links ]

9. Makgetla N. Industrial policy and the Covid-19 pandemic: The South African experience. Working paper. Pretoria: Trade and Industrial Policy Strategies; 2021. [ Links ]

10. Nwosu C, Kollamparambil U, Oyenubi A. Socioeconomic inequalities in ability to work from home during the coronavirus pandemic: The case of South Africa [document on the Internet]. c2021 [cited 2022 Feb 14]. Available from: https://cramsurvey.org/wp-content/uploads/2021/07/9.-Nwosu-C-Kollamparambil-U.-Oyenubi-A.-2021-Socioeconomic-inequalities-in-ability-to-work-from-home-during-the-coronavirus-pandemic-The-case-of-South-Africa.pdf [ Links ]

11. Ranchhod V Daniels R. Labour market dynamics in South Africa in the time of COVID-19: Evidence from Wave 1 of the NIDS-CRAM survey [document on the Internet]. c2020 [cited 2022 Feb 14]. Available from: https://cramsurvey.org/wp-content/uploads/2020/07/Ranchhod-Labour-market-dynamics-in-the-time-of-COVID-19..pdf [ Links ]

12. Spaull N, Daniels R. Synthesis report NIDS-CRAM Wave 5 [document on the Internet]. c2021 [cited 2022 Feb 14]. Available from: https://cramsurvey.org/wp-content/uploads/2021/07/1.-Spaull-N.-Daniels-R.-C-et-al.-2021-NIDS-CRAM-Wave-5-Synthesis-Report.pdf [ Links ]

13. World Bank. Global economic prospects. Washington DC: World Bank; 2021. https://doi.org/10.1596/978-1-4648-1665-9 [ Links ]

14. Ngandu S, Altman M, Cross C, Jacobs P Hart T, Matshe I. The socio-economic impact of the global downturn on South Africa: Responses and policy implications. Pretoria: HSRC; 2010. Available from: https://miriamaltman.com/research/the-socio-economic-impact-of-the-global-downturn-on-south-africa-responses-and-policy-implications-2/ [ Links ]

15. International Labour Organization. World employment and social outlook: Trends 2021 [document on the Internet]. c2021 [cited 2022 Feb 14]. Available from: https://www.ilo.org/global/research/global-reports/weso/trends2021/lang--en/index.htm [ Links ]

16. International Monetary Fund. World economic outlook - Recovery during a pandemic. Washington DC: International Monetary Fund; 2021. https://doi.org/10.5089/9781589068988.081 [ Links ]

17. World Bank. Global economic prospects. Washington DC: World Bank; 2022. https://doi.org/10.1596/978-1-4648-1758-8 [ Links ]

18. Government of South Africa. The South African Reconstruction and Recovery Plan. Pretoria: The Presidency; 2020. Available from: https://www.gov.za/sites/default/files/gcis_document/202010/south-african-economic-reconstruction-and-recovery-plan.pdf [ Links ]

19. South African Reserve Bank. Statement of the Monetary Policy Committee. Pretoria: South African Reserve Bank; 2022. Available from: https://www.resbank.co.za/content/dam/sarb/publications/statements/monetary-policy-statements/2022/statement-of-the-monetary-policy-committee/Monetary%20Policy%20Committee%20Statement%20January%202022.pdf [ Links ]

20. Altman M. Employment scenarios to 2014 & 2024 in the context of a global economic slowdown. HSRC research report. Pretoria: HSRC; 2009. Available from: https://miriamaltman.com/research/employment-scenarios-to-2014-2024-in-the-context-of-a-global-meltdown/ [ Links ]

21. South African National Planning Commission. National Development Plan: Our future - make it work. Pretoria: National Planning Commission, The Presidency; 2012. Available from: http://www.nationalplanningcommission.org.za/Pages/NDP.aspx [ Links ]

22. Altman M. Top Covid-19 policy priorities for protecting employment. Covid-19 Economy Group Policy Brief [webpage on the Internet]. 25 May 2020 [cited 2022 Feb 14]. Available from: https://covid19economicideas.org/2020/05/25/top-covid-19-policy-priorities-for-protecting-employment/ [ Links ]

23. South African Reserve Bank. QPM assumptions summary table January 2022 MPC. Pretoria: South African Reserve Bank; 2022. Available from: https://www.resbank.co.za/content/dam/sarb/publications/statements/monetary-policy-statements/2022/statement-of-the-monetary-policy-committee/Assumptions%20January%202022.pdf [ Links ]

24. Fedderke JW, Mengisteab DK. Estimating South Africa's output gap and potential growth rate. S Afr J Econ. 2017;85(2):159-318. https://doi.org/10.1111/saje.12153 [ Links ]

25. South African Reserve Bank. QPM forecast summary table January 2022 MPC. Pretoria: South African Reserve Bank; 2022. Available from: https://www.resbank.co.za/content/dam/sarb/publications/statements/monetary-policy-statements/2022/statement-of-the-monetary-policy-committee/QPM%20Summary%20tables%20press%20table%20forecast_Jan%202022%20MPC.pdf [ Links ]

26. United Nations. World population prospects 2019. New York: United Nations; 2019. Available from: https://population.un.org/wpp/Download/Standard/Population/ [ Links ]

27. Organisation for Economic Co-operation and Development (OECD). South Africa Economic Snapshot: Reform priorities [document on the Internet]. c2021 [2022 Feb 14]. Available from: https://www.oecd.org/economy/growth/South-Africa-country-note-going-for-growth-2021.pdf [ Links ]

28. International Monetary Fund. South Africa 2021 Article IV Consultation. Country report no. 2022/037 [press release]. 11 February 2022 [cited 2022 Feb 14]. Available from: https://www.imf.org/en/Publications/CR/Issues/2022/02/10/South-Africa-2021-Article-IV-Consultation-Press-Release-Staff-Report-and-Statement-by-the-513001 [ Links ]

29. National Treasury. Medium term budget policy statement. Pretoria: National Treasury; 2021. Available from: http://www.treasury.gov.za/documents/mtbps/2021/default.aspx [ Links ]

Correspondence:

Correspondence:

Miriam Altman

Email: info@miriamaltman.com

Received: 14 Feb. 2022

Revised: 11 Apr. 2022

Accepted: 09 May 2022

Published: 31 May 2022

Guest Editor: Shabir Madhi

Funding: None

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}