Services on Demand

Journal

Article

English (pdf)

English (pdf)

Article in xml format

Article in xml format Article references

Article references

Send this article by e-mail

Send this article by e-mailIndicators

Related links

-

Cited by Google

Cited by Google -

Similars in Google

Similars in Google

Share

Permalink

PermalinkActa Commercii

On-line version ISSN 1684-1999Print version ISSN 2413-1903

Acta Commer. vol.25 n.1 Johannesburg 2025

https://doi.org/10.4102/ac.v25i1.1328

ORIGINAL RESEARCH

Introducing the composite business success index: Enhancing small and medium enterprise competitiveness in South Africa

Donovan M. Jacobs; Boniface Kabaso

Department of Information Technology, Faculty of Information and Design, Cape Peninsula University of Technology, Cape Town, South Africa

ABSTRACT

ORIENTATION: This study explored the composite business success index (CBSI), a novel framework designed to enhance small and medium enterprise (SME) competitiveness in South Africa by integrating financial and cultural metrics.

RESEARCH PURPOSE: The aim was to introduce CBSI as a tool for assessing small and medium enterprise performance, combining financial indicators like the cash conversion cycle (CCC) and Altman Z-score with cultural metrics such as the Configurational Accuracy Score for a more holistic evaluation.

MOTIVATION FOR THE STUDY: Small and medium enterprises in South Africa face significant challenges, including financial instability and misalignment of organisational culture. Existing performance models often fail to address these non-financial factors, which CBSI integrates into one evaluative tool to improve both financial health and cultural alignment.

RESEARCH DESIGN, APPROACH AND METHOD: A pragmatist research approach integrated quantitative and qualitative methodologies, including financial data from small and medium enterprise statements, semi-structured interviews with small and medium enterprise owners and experts and questionnaires to collect cultural data for insight into the role of culture in small and medium enterprise success.

MAIN FINDINGS: Composite Business Success Index proved effective in predicting small and medium enterprise performance. Higher CBSI scores (> 0.65) were associated with successful small and medium enterprises, while lower scores (< 0.50) indicated areas for improvement, highlighting the link between financial stability and organisational alignment

PRACTICAL/MANAGERIAL IMPLICATIONS: The CBSI offers small and medium enterprise leaders actionable insights for enhancing financial performance and organisational culture, boosting competitiveness and long-term sustainability.

CONTRIBUTION/VALUE-ADD: By integrating both financial and cultural metrics into a single framework, the CBSI provides a novel tool for assessing and developing small and medium enterprise performance for the small and medium enterprise managers.

Keywords: small and medium enterprise competitiveness; composite business success index; financial performance; organisational culture; cash conversion cycle; Altman Z-score; configurational accuracy score; South Africa.

Introduction

Small and medium enterprises play a critical role in South Africa's economy, contributing to job creation, innovation and overall economic growth. Despite their importance, small and medium enterprises face numerous challenges that hinder their competitiveness in both domestic and global markets. According to the 2022/2023 report by the governmental organisation, Small Enterprise Development Agency (SEDA), small and medium enterprises encounter issues such as financial instability, poor cash flow management, high operational costs and difficulty in adapting to changing market demands (SEDA 2023). These challenges are compounded by cultural misalignments within organisations, which negatively impact decision-making processes, innovation and overall business performance. While traditional financial metrics, such as profitability and liquidity ratios, are commonly used to assess small and medium enterprise performance, they often fail to account for non-financial factors, such as organisational culture, which significantly influence business outcomes. The importance of cultural alignment is increasingly recognised, with studies like those of Harefa et al. (2024) highlighting its critical role in employee engagement, innovation and leadership effectiveness. However, existing performance evaluation models tend to overlook the connection between financial health and cultural cohesion, both of which are essential for long-term competitiveness.

This study addresses these gaps by introducing the Composite Business Success Index (CBSI), a novel framework that integrates both financial and cultural metrics. The CBSI provides a more holistic approach to small and medium enterprise performance, enabling business leaders to assess and improve financial stability while ensuring organisational alignment with strategic goals. It combines key financial indicators, such as the Cash Conversion Cycle (CCC) and Altman Z-score, with cultural metrics like the Configurational Accuracy Score (CAS) and Telles' Workflow Accuracy to offer a comprehensive evaluation of small and medium enterprise competitiveness. Given the growing recognition of the importance of both financial and cultural dimensions in small and medium enterprise performance, as highlighted by Ahsan (2024:783), this study explores how the CBSI framework can be applied to South African small and medium enterprises.

Social value

Small and Medium Enterprises play a pivotal role in South Africa's economy, contributing significantly to job creation, innovation and overall economic growth (Qomoyi et al. 2024). However, many small and medium enterprises face challenges such as financial instability and misaligned organisational cultures, which hinder their competitiveness in both local and global markets. Enhancing the financial health and cultural alignment of small and medium enterprises is critical not only for their survival but also for promoting economic stability and fostering job creation in South Africa. Research indicates that small and medium enterprises in emerging markets encounter structural challenges, including limited access to financial capital and inadequate business support systems, which undermine their sustainability (Huo 2023:115). Additionally, studies emphasise the importance of effective Enterprise Resource Planning (ERP) implementation in mitigating financial and operational inefficiencies, thus enhancing small and medium enterprise competitiveness (Rahmita et al. 2023:212). By addressing these challenges through the CBSI, this study proposes a structured approach for small and medium enterprises to enhance both their financial and operational alignment.

Scientific value

Traditionally, small and medium enterprise performance evaluations have predominantly focused on financial indicators, often neglecting the impact of organisational culture on business outcomes. This research addresses that gap by proposing an integrated framework that incorporates both financial and cultural metrics, offering a more comprehensive assessment of small and medium enterprises success. Scholarly discourse has increasingly emphasised the importance of aligning financial stability with operational efficiency for business sustainability (Bouncken et al. 2024:76). Additionally, recent studies further support the argument that cultural alignment enhances ERP adoption success, with organisational cohesion serving as a critical determinant of small and medium enterprise competitiveness (Vos & Boonstra 2022:3). By bridging the gap between financial performance and cultural alignment, this study contributes to the broader discourse on small and medium enterprise success metrics and strategic management.

Conceptual framework

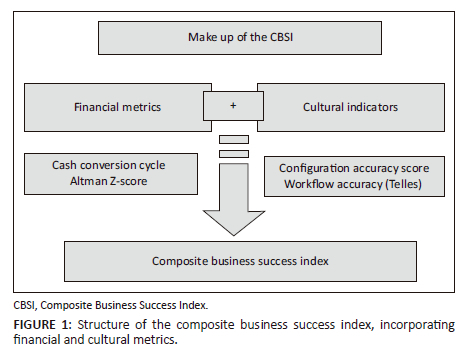

The CBSI provides a structured, multidimensional framework for evaluating small and medium enterprise performance by integrating both financial and operational metrics. Unlike traditional performance assessment models that primarily focus on financial stability, the CBSI incorporates workflow efficiency and strategic alignment, offering a more comprehensive tool for assessing small and medium enterprise competitiveness.

In addition to financial indicators such as the CCC and Altman Z-score, which measure liquidity and bankruptcy risk, the CBSI also integrates Telles' Mathematical Formula to assess workflow accuracy and operational alignment (Iliescu 2020:127). This approach ensures that both financial health and business process efficiency are evaluated simultaneously, reducing performance assessment gaps that exist in conventional models (Van Staden 2022:89).

Interdependence of components

The components of the CBSI are interrelated. For example, improving workflow accuracy (CAS and Telles metrics) can enhance the CCC, leading to better financial stability (Z-Score). Each metric provides valuable insights into different aspects of small and medium enterprise performance, and together, they form a comprehensive evaluation tool. Figure 1 illustrates how the CBSI integrates key financial and cultural metrics, highlighting their interdependence in assessing small and medium enterprise performance.

Aim and objectives

The primary objective of this study is to develop the CBSI, a framework that integrates both financial and cultural metrics to assess small and medium enterprise performance in South Africa. This framework aims to align financial health, operational success and organisational culture, positioning culture as a critical driver of performance alongside traditional financial indicators. The CBSI provides a comprehensive tool for improving operational efficiency and competitiveness.

The specific objectives are:

To design the CBSI framework as a holistic assessment tool integrating financial and operational metrics for small and medium enterprise evaluation.

To evaluate the impact of the CBSI on small and medium enterprise performance, assessing its ability to predict financial stability, workflow efficiency and long-term competitiveness.

To offer practical recommendations for small and medium enterprise leaders on leveraging the CBSI to improve cash flow management, optimise ERP adoption and enhance organisational cohesion.

Related work

The evaluation of small and medium enterprise performance has traditionally focused on financial indicators such as profitability, liquidity and efficiency metrics, which provide insight into the economic viability of an organisation. However, recent advancements in small and medium enterprise performance evaluation have recognised the importance of non-financial metrics, particularly organisational culture, as noted by Alves and Lourenço (2022:152). As small and medium enterprises navigate an increasingly competitive global landscape, understanding the influence of culture on performance has become pivotal to fostering long-term sustainability and growth (Jardioui, Garengo & El Alami 2020).

Small and medium enterprise performance evaluation: Financial and cultural metrics

Small and medium enterprise performance evaluation has traditionally focused on financial metrics like profitability, liquidity and solvency ratios, which provide critical insights into a business's financial health (Altman et al. 2017). However, these metrics alone fail to capture non-financial factors, particularly organisational culture, which significantly influence business outcomes. Research highlights that while operational efficiency is vital, it does not provide a complete picture of success. For example, Caldeira and Ward (2003) linked financial health in small and medium enterprises to organisational dimensions such as internal processes, leadership and culture.

Recent literature emphasises the critical role of organisational culture in shaping small and medium enterprise success, influencing decision-making, employee engagement and the ability to innovate (Harefa et al. 2024; Roy et al. 2024:8). While financial metrics offer quantitative data, cultural metrics provide qualitative insights into alignment with organisational values, leadership and communication strategies. Small and medium enterprises with strong organisational cultures are better positioned to navigate challenges and engage their workforce (Vargo & Seville 2023).

However, it is important to recognise that culture is not the sole driver of small and medium enterprise performance. Factors like access to financial resources, market conditions and technological capabilities also contribute. Integrating cultural metrics with traditional financial indicators allows for a more holistic evaluation, as seen in the CBSI framework, which emphasises both financial stability and organisational effectiveness (Lin, Jung & Sharma 2024). This integrated approach reflects the complexity of small and medium enterprise operations, where both internal and external factors shape performance (Van Staden 2022:459).

Cultural artefacts and organisational success

Cultural artefacts, both tangible and intangible, reflect a company's values and play a crucial role in shaping its identity and success (Cameron & Quinn 2011). These artefacts, ranging from company policies to behavioural norms, influence employee interactions and external stakeholder relationships. Hofstede (2011:9) demonstrated that organisational culture is a key determinant of business outcomes, including decision-making and customer satisfaction. For small and medium enterprises, aligning cultural artefacts with business goals is essential for fostering innovation and adaptability.

Effective management of these cultural dimensions supports open communication, innovation and swift decision-making, enhancing collaboration and employee retention (Bissessar 2018). While the integration of cultural metrics into business performance frameworks is still underexplored, evidence shows that strong cultural cohesion leads to better business outcomes (Horani et al. 2023). When cultural artefacts align with operational processes, they reduce friction, enhance decision-making and contribute to customer loyalty, which is particularly beneficial in small and medium enterprises where culture is closely tied to leadership and employee engagement (Syafira, Puspitasari & Witjaksono 2021).

The composite business success index: An integrated approach

The CBSI integrates both financial health and operational efficiency (Figure 1), much like financial inclusion strategies that depend on financial education and responsible practices (Samputra & Soesilo 2023). This framework combines financial indicators with cultural metrics (Meyer, Tsui & Hinings 1993; Rao & Li 2019) and Telles Workflow for probability accuracy (Telles 2019), providing a comprehensive assessment of business performance. This dual focus addresses the gap in traditional performance models, which often overlook the role of cultural alignment in business success.

The CBSI incorporates the CAS, which measures how well an small and medium enterprise's operational workflows reflect its cultural values. The CCC and Altman Z-score provide reliable assessments of financial health, including liquidity, efficiency and stability. Cultural alignment is essential for long-term success, particularly for small and medium enterprises that rely on adaptability and innovation to thrive in dynamic markets (Bag et al. 2021; Pudjiarti & Hutomo 2020). By combining financial metrics with operational efficiency and leadership engagement, the CBSI offers a clearer view of an small and medium enterprise's competitiveness, addressing both tangible and intangible drivers of success.

The role of cultural artefacts in enhancing small and medium enterprise competitiveness

Cultural artefacts reflect an organisation's adaptability and openness to innovation, which are essential for small and medium enterprises in competitive markets (Uddin et al. 2023; Vargo & Seville 2011). By integrating these artefacts into the CBSI, small and medium enterprises can better understand the factors driving both financial performance and internal cohesion. This is especially important in the South African context, where studies have shown that organisational culture, including leadership styles and employee engagement, significantly impacts business performance and adaptability in the diverse socio-economic environment (Nungchim & Leihaothabam 2022:12; Sajuyigbe et al. 2024:106). Furthermore, embracing cultural diversity within organisations has been recognised as crucial for improving competitive advantage and operational efficiency (Egu & Chiloane-Tsoka 2023:45).

Methodology

This study adopts a pragmatist paradigm (Kaushik & Walsh 2019:16), emphasising practical application and actionable insights to address real-world challenges. Methodological pragmatism does not inherently prioritise mixed-methods research. Instead, the choice between qualitative, quantitative or mixed methods was made pragmatically, based on the research's specific needs (Foster 2024). This approach aligns with the goal of developing the CBSI, which evaluates small and medium enterprise competitiveness by considering both dimensions (Стошић Панић & Janković Milić 2022:113). Financial performance metrics like the CCC and Altman Z-score provide insights into small and medium enterprise financial health, while cultural factors - such as leadership, organisational values and employee engagement - are critical for small and medium enterprises to adapt to market changes (Rahman et al. 2024:191). The study is rooted in pragmatism, which values the practical application of theories (Ormerod 2024:53). It also incorporates elements of ontology, epistemology and axiology to provide a comprehensive perspective on ERP adoption in small and medium enterprises:

Ontology: This study adopts a pragmatic ontology, viewing reality as shaped by interactions between individuals and their organisational environment, where small and medium enterprises face unique challenges that influence ERP implementation.

Epistemology: Knowledge is viewed as arising from practical experience and empirical evidence, with the study aiming to generate actionable insights into ERP adoption in South African small and medium enterprises.

Axiology: The study emphasises values and ethics in the research process, aiming to provide small and medium enterprise leaders with practical, value-driven recommendations for ERP adoption, while ensuring ethical considerations such as confidentiality and informed consent.

Study design

This study uses a mixed-methods design, combining both quantitative and qualitative approaches to assess small and medium enterprise performance in South Africa (Nowell et al. 2017:5). The quantitative component evaluates financial health through metrics like the CCC and Altman Z-score, providing insights into small and medium enterprise competitiveness. The qualitative component explores how cultural alignment, leadership and employee engagement shape small and medium enterprise operations, using thematic analysis to identify key cultural factors influencing business outcomes. This approach was chosen pragmatically to assess small and medium enterprise performance from both financial and cultural perspectives, offering actionable insights to support ERP adoption and enhance organisational culture.

Quantitative data collection

The quantitative component involved a survey, 'Key Financial Features for small and medium enterprises', conducted via SurveyMonkey. It assessed financial performance indicators (e.g. cash flow management, financial stability) and their relationship with ERP systems. Additional financial data from the small and medium enterprises provided numerical insights into financial health and its correlation with overall performance.

Qualitative data collection

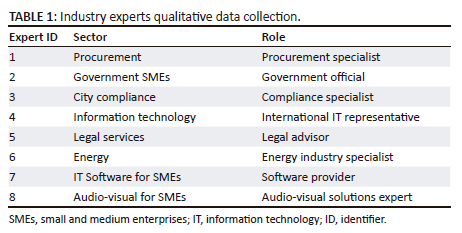

Semi-structured interviews were conducted with industry experts across diverse sectors (Table 1), using Zoom for interviews and Otter for transcription. These interviews focused on leadership, employee engagement and organisational values to understand their impact on small and medium enterprise operations and ERP adoption. Thematic analysis identified key cultural themes affecting performance and competitiveness.

Integration of quantitative and qualitative data

The study integrates both data types to provide a comprehensive view of small and medium enterprise performance. Financial data (CCC, Altman Z-score) offer insights into financial stability, while qualitative data reveal the impact of cultural factors (e.g. leadership, organisational values) on ERP adoption and operations. This integration is crucial for achieving the study's objective of comprehensively evaluating small and medium enterprise performance. The CBSI framework operationalises financial and cultural metrics as performance drivers, linking them directly to small and medium enterprise success. This holistic approach ensures that both financial (tangible) and cultural (intangible) factors are considered in evaluating small and medium enterprise success.

Setting

The research was conducted in South Africa, focusing on small and medium enterprises across various industries, including manufacturing, mining, procurement, retail and services, amongst others. South Africa's dynamic economic landscape, with its blend of large corporations and a growing small and medium enterprise sector, provides a relevant context for studying competitiveness (Saah, Mbohwa & Madonsela 2024:4). According to the SEDA, South Africa boasts over 2 million registered small and medium enterprises. However, less than 1% of these small and medium enterprises meet compliance standards, including value added tax (VAT) registration, Companies and Intellectual Property Commission (CIPC) registration and other regulatory requirements. As a result, the accessible population for this study is restricted to those small and medium enterprises that meet compliance standards. Furthermore, many small and medium enterprises in South Africa face significant challenges in terms of digital accessibility, which affects their capacity to participate in digital surveys, such as those conducted via SurveyMonkey. This factor played a role in the sampling strategy, limiting the sample size to 250 small and medium enterprises across five key industry groups: Manufacturing, Retail, Information Technology (IT), Construction, and Services.

The study evaluates the CBSI framework in the context of small and medium enterprises in South Africa, leveraging both qualitative data collected from industry experts through Zoom interviews (transcribed using Otter) and quantitative data gathered through the 'Key Financial Features for small and medium enterprises' survey on SurveyMonkey. This combination of data sources allows for a wide-ranging and contextualised understanding of how the CBSI framework can address the specific challenges faced by small and medium enterprises.

Study population and sampling strategy

A purposeful sampling method was used to select small and medium enterprises from various sectors in South Africa.

Population

The study targeted registered small and medium enterprises in South Africa that meet regulatory compliance standards, such as VAT registration and CIPC registration. According to the SEDA, South Africa has over 2 million registered small and medium enterprises. However, the study focused on the smaller population of small and medium enterprises (1%) that comply with these regulations.

Sampling size

A sample of 250 small and medium enterprises was selected, with 50 small and medium enterprises from each of the following sectors: Manufacturing, Retail, IT, Construction, and Healthcare. These sectors were chosen to represent a broad spectrum of small and medium enterprises that have adopted ERP systems.

Annual turnover

The sample exhibited a wide range of annual turnovers:

Maximum turnover: R25 000 000 (from the Manufacturing sector).

Minimum turnover: R600 000 (from the Retail sector).

This turnover range reflects the diversity of small and medium enterprises in terms of scale and financial capacity, which was used to assess the impact of ERP systems on financial and operational performance.

Sampling frame

A two-step sampling frame was used to ensure robust data collection:

Test Frame: A pilot test of 50 small and medium enterprises was conducted to assess data-collection methods and refine the survey instrument.

Complete Sample Frame: Following the pilot phase, 250 small and medium enterprises were selected, with 50 small and medium enterprises from each of the five sectors. This approach ensured the sample was representative of the broader small and medium enterprise population in South Africa.

Sampling method

Stratified random sampling was used to ensure proportional representation from each industry sector (Fleetwood 2024). This method allows for a comprehensive analysis of how ERP systems impact small and medium enterprise performance, particularly in financial metrics like the CCC and operational efficiency. The sample size of 250 is considered appropriate for mixed-methods research in the small and medium enterprise sector Creswell & Creswell (2017); Saunders et al. 2018), ensuring robust and generalisable findings.

Data collection

This study used two methods for data collection: a quantitative survey and qualitative interviews. The survey, titled 'Key Financial Features for small and medium enterprises', was administered via SurveyMonkey to 250 small and medium enterprises across South Africa, spanning different industries as mentioned before. The survey focused on ERP adoption's impact on financial tracking, operational efficiency and the role of cultural factors. It was sent to senior management and owners involved in ERP usage.

For the qualitative component, interviews were conducted with eight industry experts from sectors such as procurement, IT, energy and legal services. These Zoom interviews were transcribed using Otter for accurate analysis. The focus was on gathering insights into the challenges small and medium enterprises face in ERP adoption, especially regarding culture and financial management practices.

SurveyMonkey adheres to ISO 27001 and HIPAA standards, ensuring secure handling of data. All survey data were stored securely on password-protected devices, with no personally identifiable information collected, maintaining participant anonymity.

Measures for confidentiality

The measures for confidentiality are as follows:

Anonymity: Personal information was not collected, and responses were anonymised.

Secure data storage: Data were stored on encrypted devices accessible only to the research team.

Confidentiality agreements: Participants were assured their responses would be used for academic purposes only.

Security protocols

The security protocols are as follows:

Physical security: SurveyMonkey's data centres have 24/7 monitoring and restricted access with SOC 2 accredited security controls.

Encryption: Data were encrypted with AES 256 at rest and RSA 2048 during transfer.

Access control: Secure access through VPN and multi-factor authentication ensured data were accessible only to authorised personnel.

These protocols ensured the confidentiality of participant data and adherence to ethical research guidelines.

Data analysis

Data normalisation and preparation

To ensure comparability across small and medium enterprises of varying sizes and industries, data were normalised. Financial metrics, such as the CCC and profitability ratios, were adjusted relative to company size and operational scale. Similarly, cultural metrics like the CAS were standardised to account for differences in workflow practices, allowing for consistent comparison across sectors. This study applied normalisation to ensure meaningful comparisons between small and medium enterprises of varying sizes and industries, preventing bias in subsequent analyses (Boujlil & Alsunbul 2024:37).

What is being normalised and why?

The study primarily normalises financial metrics (e.g. CCC and profitability ratios) to adjust for differences in company size and operational scale. Similarly, cultural metrics like the CAS are standardised to account for sectoral variations. This ensures a fair comparison across small and medium enterprises, regardless of size, while maintaining the data's comparability and integrity.

Example of normalisation

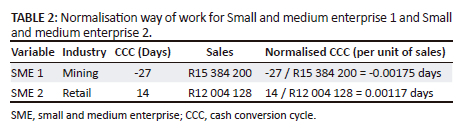

For the CCC, larger companies tend to have longer or shorter cycle times, while smaller companies may show disproportionately high or low figures. To normalise, the CCC is divided by the total revenue of the small and medium enterprise, reflecting operational efficiency relative to size (see Table 2):

Small and medium enterprise 1 (Mining) has a negative CCC of -27 days, suggesting a negative CCC. When normalised, it gives -0.00175 days per unit of sales, which indicates that, in relation to its size, small and medium enterprise 1 is effectively using its capital and resources more efficiently in terms of cash flow management compared to other small and medium enterprises.

Small and medium enterprise 2 (Retail) has a positive CCC of 14 days. When normalised, it gives 0.00117 days per unit of sales, suggesting that Small and medium enterprise 2, although having a positive CCC, is relatively less efficient in terms of cash conversion than Small and medium enterprise 1, especially considering the scale differences between the two.

Why is normalisation important?

Normalisation ensures fair comparisons across small and medium enterprises in different contexts (Singh & Singh 2020:1). Without it, size differences would skew the analysis. Larger companies may appear less efficient because of longer cycles, while smaller ones might seem inefficient because of shorter cycles. By adjusting for size, we can assess each small and medium enterprise's performance relative to its scale, enabling more accurate decision-making.

Quantitative data analysis

Descriptive statistics were used to summarise the financial data collected from small and medium enterprises. Although data from JSE-listed companies were initially analysed for comparison, the focus was on small and medium enterprises for brevity. Key financial health indicators, including the CCC, Altman Z-score and profitability ratios, were computed using data sourced from SEDA accountants. The Telles' Mathematical Formula for workflow accuracy was applied to assess how well small and medium enterprises' operational processes aligned with their strategic goals. This provided a numerical score for each small and medium enterprise's workflow efficiency, integrated into the CBSI along with financial and cultural metrics. These metrics offered insights into liquidity, financial stability and operational efficiency across the small and medium enterprises.

Qualitative data analysis

Qualitative data were analysed using Atlas.ti, with manual coding. Thematic analysis identified key patterns in organisational culture and its impact on financial performance. This analysis focused on the alignment between cultural practices and operational processes. For instance, interviews with small and medium enterprise managers highlighted recurring issues of workflow inefficiency and misalignment between organisational values and ERP system functionalities. The analysis also identified key themes from industry expert and small and medium enterprise participant interviews, providing insights into factors influencing small and medium enterprise competitiveness, particularly in ERP adoption. Although other themes were mentioned, the following three emerged as the most significant, highlighting the current challenges and opportunities for small and medium enterprises.

Impact of cultural alignment on business success: A key theme identified from the interviews was the impact of cultural alignment on Small and medium enterprises success, particularly how a business's internal culture aligns with its operational processes. Participants noted that small and medium enterprises with a cohesive culture that reflects operational goals achieve better success in meeting organisational objectives. One participant stated, 'A strong organisational culture in sync with operational processes is the glue that holds everything together. When they align, performance improves, and employees feel more engaged and motivated'. This underscores the importance of aligning business strategy with core company values to drive internal cohesion and overall success.

Enterprise resource planning system integration challenges and benefits: The second major theme concerns the challenges and benefits small and medium enterprises face when integrating ERP systems. Experts highlighted that while ERP adoption can be difficult because of high costs, technical difficulties and employee training, the long-term benefits are significant. One interviewee remarked:

'The early stages of ERP implementation are always a struggle - whether it's the cost or the learning curve for staff. However, once it's in place, the improvements in efficiency, reporting accuracy, and financial oversight are undeniable.' (Industry specialist, O.P., interview 26 October 2024)

This demonstrates the dual nature of ERP adoption: high initial investment with substantial long-term benefits in financial management and workflow efficiency.

Financial transparency and the role of technology: Another prevalent theme was the need for financial transparency, enhanced by technology. Interviewees noted that small and medium enterprises using ERP systems for financial tracking helps gain a clearer understanding of their financial health, directly impacting decision-making. One expert shared, 'The transparency that comes with ERP systems is invaluable. It's not just about tracking numbers - it's about having real-time access to financial data that can guide business decisions'. This underscores the value of digital financial solutions in ensuring financial stability and preventing inefficiencies in the modern business environment.

Validity and reliability

To ensure the robustness of the findings, both validity and reliability were carefully considered. Validity was addressed through data triangulation, incorporating both quantitative and qualitative data to ensure the constructs measured accurately reflected small and medium enterprise performance. The CBSI integrates financial, cultural and operational metrics into a comprehensive measure of business success. The formula for the CBSI is (Equation 1):

Cash conversion cycle: The CCC measures the efficiency of a company's working capital management by indicating how quickly a company can convert its investments in inventory and other resources into cash flows from sales. A shorter CCC indicates better liquidity and cash flow management, which is crucial for small and medium enterprises that need to optimise cash flow to sustain operations and growth (Equation 2).

Where:

DIO (Days Inventory Outstanding) represents the average time that inventory is held before it is sold.

DSO (Days Sales Outstanding) measures the average time it takes for a company to collect payment after a sale.

DPO (Days Payable Outstanding) refers to the average time a company takes to pay its suppliers.

In the context of the CBSI, the CCC is used as one of the weighted factors to measure the financial health of small and medium enterprises and their ability to remain competitive in the market.

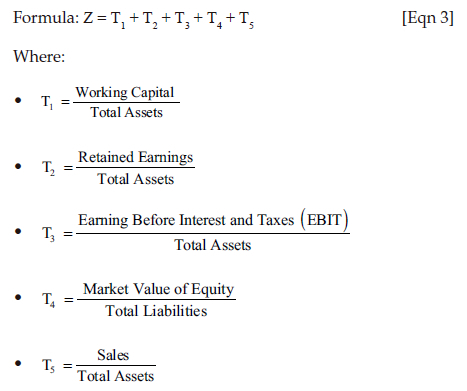

Altman Z-score: The Altman Z-Score is a widely used financial metric for predicting the likelihood of financial distress or bankruptcy (Destriwanti et al. 2022). It evaluates a company's financial health by analysing key ratios related to liquidity, profitability and leverage. A Z-score near 0 indicates a risk of bankruptcy, while a score above 3 suggests the company is in strong financial health (Equation 3).

For the sake of clarity and simplicity, the Altman Z-score formula in this study is represented using T1, T2, T3, and so forth, instead of the traditional X1, X2, X3 notation. This alternative representation ensures consistency with the other formulas in the CBSI and enhances readability throughout the paper.

Configurational accuracy score: The CAS is a key cultural metric designed to measure how well an small and medium enterprise's ERP system configurations align with its operational workflows and strategic goals. It reflects the effectiveness of the configurations implemented in supporting the operational needs of the business, which is crucial for both workflow efficiency and cultural cohesion.

The CAS is calculated using the following formula (Equation 4):

Where:

Effective Configurations refer to the workflow setups within the ERP system that meet the operational requirements and goals of the small and medium enterprise.

Total Possible Configurations represent all the potential workflow setups available within the ERP system.

For example, in small and medium enterprise 1, a CAS of 0.80 indicates that 80% of the system's configurations are effectively aligned with the company's workflow and operational needs. A higher CAS implies that the ERP system is well-configured to meet the business's strategic objectives, while a lower CAS suggests misalignment and potential inefficiencies in workflow management.

Telles' mathematical accuracy: The Telles' Mathematical Accuracy metric is used to evaluate the precision and success rate of critical workflow stages within an small and medium enterprise's ERP system. It provides a probabilistic measure of how accurately workflows align with the intended operational configurations, thereby ensuring that tasks and processes are completed as expected.

The Telles' Mathematical Accuracy is calculated as (Equation 5):

Where:

Event accuracy refers to how precisely each task or process within the workflow matches the intended configuration.

Possible configurations represent the total number of potential workflow setups.

The score reflects the overall likelihood of successful task completion, with higher values indicating greater precision and efficiency.

Financial data from small and medium enterprises

Table 3 presents the detailed financial data for the selected small and medium enterprises, including key metrics such as Working Capital, Total Assets, Retained Earnings, EBIT and Market Value of Equity.

These financial figures are used to compute critical performance metrics, such as the Altman Z-score, discussed in the Altman Z-Score section, and contribute to the overall CBSI evaluation.

Ethical considerations

Ethical clearance for this study was obtained from both SEDA and the Cape Peninsula University of Technology (CPUT) Ethics Committee on 19 September 2024. The ethical clearance number is 189045493/2022/11. The study adhered to ethical research guidelines, ensuring that all participants provided informed consent prior to data collection. Confidentiality was strictly maintained throughout the process, with no personal identifying information collected or disclosed. Participation was entirely voluntary, and participants were given the option to withdraw from the study at any point without any consequences. The data will be retained for 5 years in accordance with institutional guidelines, after which it will be permanently deleted. The study posed no risk to participants, and care was taken to ensure that no harm, physical or psychological, was inflicted.

Results

The results offer insights into the performance of small and medium enterprises based on the CBSI model, demonstrating how these metrics interrelate and collectively contribute to the overall competitiveness of small and medium enterprises.

Overview of financial and operational metrics

The performance of small and medium enterprises was assessed using the CBSI, which incorporated four key metrics: (1) CCC; (2) Altman Z-score; (3) CAS; and (4) Telles' Mathematical Accuracy.

The CCC measured how efficiently small and medium enterprises converted inventory into cash. For example, small and medium enterprise 1, with a negative CCC of −27 days, demonstrated superior cash flow management, while small and medium enterprises in the retail sector averaged CCC values of 15-20 days, indicating slower cash conversion.

The Altman Z-score evaluated the financial stability of small and medium enterprises. Small and medium enterprise 1 achieved a Z-score of 2.5, placing it in the 'safe zone' and signalling low bankruptcy risk, while small and medium enterprises with lower Z-scores showed higher financial vulnerability.

We used the CAS to assess how well ERP systems aligned with operational workflows. Small and medium enterprise 1's CAS of 0.80 indicated effective alignment with business processes, whereas small and medium enterprises with lower CAS scores revealed misalignments and inefficiencies.

Telles' Mathematical Accuracy measured the precision of workflow execution. Small and medium enterprise 1 recorded 72.68%, reflecting high accuracy in workflow execution, while small and medium enterprises with lower Telles' Accuracy scores experienced greater workflow inconsistencies.

Collectively, these metrics provide a comprehensive evaluation of small and medium enterprises performance, with higher CBSI scores correlating with stronger financial health, operational efficiency and competitive advantage.

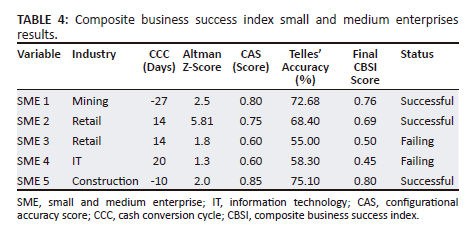

Composite business success index scores and interpretation

The CBSI model enables small and medium enterprises to interpret integrated financial and cultural performance factors, improving both strategic decision-making and sustainability (see Table 4).

Cash Conversion Cycle: Small and medium enterprise 1 (Mining) and Small and medium enterprise 5 (Construction) reported negative CCC values, indicating high efficiency in cash flow management. On the other hand, small and medium enterprise in the Retail and IT sectors exhibited slower cash flow with positive CCC values.

Altman Z-Score: Small and medium enterprises with Z-scores above 2.0, like Small and medium enterprise 1 (2.5) and Small and medium enterprise 5 (2.0), are financially stable and less likely to face bankruptcy. Lower Z-scores, like those of Small and medium enterprise 4 (1.3), suggest higher financial risk. The Altman Z-score not only predicts financial stability but also reflects the broader strategic positioning of small and medium enterprises in competitive markets. For instance, Small and medium enterprise 1's Z-score of 2.5 demonstrates a well-balanced financial structure, allowing it to invest in operational efficiency. Similarly, the CAS metric offers insights into operational alignment, with small and medium enterprises like Small and medium enterprise 1 and Small and medium enterprise 5 leveraging ERP systems to streamline workflows and reduce inefficiencies.

Configurational Accuracy Score: Small and medium enterprise 5 (Construction) scored the highest in CAS (0.85), showing strong ERP alignment with business processes. Small and medium enterprise 3 and Small and medium enterprise 4, both in Retail and IT sectors, had lower CAS scores, indicating potential operational inefficiencies.

Telles' Accuracy: Small and medium enterprise 1 and Small and medium enterprise 5 showed high workflow accuracy with Telles' scores around 72-75%, while small and medium enterprises in Retail and IT (Small and medium enterprise 3 and Small and medium enterprise 4) demonstrated lower workflow precision.

Composite Business Success Index: Based on the CBSI score, Small and medium enterprise 1 (Mining), small and medium enterprise 5 (Construction) and Small and medium enterprise 2 (Retail) are classified as successful. Small and medium enterprises with CBSI scores below 0.60, such as Small and medium enterprise 3 and Small and medium enterprise 4, are considered failing, highlighting their operational and financial struggles.

Table 4 encapsulates the qualitative findings related to the CAS and Telles' Accuracy for each small and medium enterprise. It highlights key operational and cultural factors that influenced these scores, providing context to the numerical data previously discussed.

The qualitative data provided context to the quantitative scores (Table 5), particularly in relation to CAS and Telles' Accuracy. Small and medium enterprises with higher CAS scores, such as Small and medium enterprise 1 and Small and medium enterprise 5, reported strong leadership involvement and alignment between their ERP systems and daily workflows. Employees in these companies expressed satisfaction with how the ERP system supported operational tasks, resulting in smoother processes and higher workflow precision.

In contrast, small and medium enterprises with lower CAS scores, such as Small and medium enterprise 3 and Small and medium enterprise 4, faced challenges with poor leadership engagement and lack of interdepartmental communication. This led to under-utilisation of their ERP systems, contributing to misaligned processes and inefficiencies, as reflected in their lower Telles' Accuracy scores.

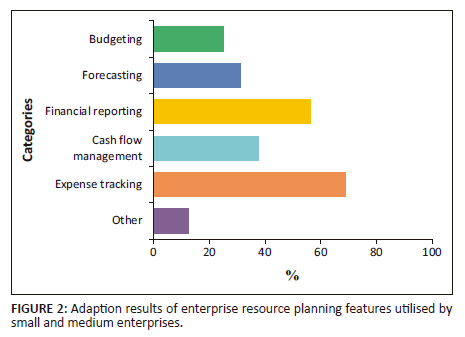

Adaptation results for enterprise resource planning

The qualitative data from five surveys of 50 small and medium enterprises each revealed significant trends in ERP system adaptation and prioritisation. The results show how successful small and medium enterprises have achieved higher operational efficiency through better system alignment, while those that struggle continue to face challenges in integrating ERP functionalities into their workflows. Figure 2 illustrates the trends in ERP system adaptation, providing a clearer depiction of the operational alignment highlighted in the qualitative insights.

Figure 2 also visually represents ERP system adaptation across the selected small and medium enterprises, reinforcing the trend observed in the qualitative data. Successful small and medium enterprises adapted their ERP systems effectively to meet operational needs, while struggling small and medium enterprises faced challenges with integration and system alignment.

Discussion

This section discusses the study's key findings in relation to its primary objectives:

To introduce the CBSI framework as a strategic tool for evaluating small and medium enterprise performance: Addressed in 'Overall business success' section of this article, where the integration of both financial and cultural metrics is explored, providing a comprehensive evaluation of small and medium enterprise performance.

To demonstrate the effectiveness of the CBSI in predicting small and medium enterprise success: In 'Key financial performance' section of this article, the results highlight how the CBSI framework effectively measured small and medium enterprise success, predicting financial stability and operational alignment based on the collected data.

To provide practical recommendations for business leaders on using the CBSI to improve operational efficiency and organisational cohesion: 'Operational and cultural alignment' section of this article, offers actionable insights for small and medium enterprise leaders on how they can utilise the CBSI to improve both financial performance and cultural alignment within their organisations.

The CBSI results offer significant insights into the financial stability and operational efficiency of the selected small and medium enterprises. The metrics used - Cash Conversion Cycle, Altman Z-score, CAS and Telles' Mathematical Accuracy - enable a comprehensive evaluation of small and medium enterprise performance, offering a clearer understanding of the factors that contribute to their success or failure.

Overall business success

Small and medium enterprises with higher CBSI scores, such as Small and medium enterprise 1 and Small and medium enterprise 5, demonstrated strong financial health, efficient operations, and well-aligned ERP systems, marking them as successful. Conversely, Small and medium enterprise 3 and Small and medium enterprise 4, with lower CBSI scores, struggled because of financial instability and operational inefficiencies, limiting their competitiveness.

The CBSI underscores the importance of both financial and operational performance. Financial stability alone is insufficient if operational processes are misaligned. This aligns with the study's first objective of introducing the CBSI framework as a strategic tool for assessing small and medium enterprise performance, incorporating financial indicators like the CCC and Altman Z-score, along with operational and cultural metrics like CAS and Telles' Accuracy.

Key financial performance

Financial stability is crucial for small and medium enterprise success. Small and medium enterprises with higher Altman Z-scores, such as Small and medium enterprise 1 (Mining) and small and medium enterprise 5 (Construction), demonstrated lower bankruptcy risks and greater resilience. In contrast, small and medium enterprises with lower Z-scores, like Small and medium enterprise 3 (Retail) and Small and medium enterprise 4 (IT), faced higher financial distress. The Z-score reinforces the importance of maintaining liquidity and managing debt effectively for long-term survival.

The CCC also provided insights into working capital efficiency. Small and medium enterprises with low or negative CCC values, such as Small and medium enterprise 1 and Small and medium enterprise 5, efficiently converted inventory into cash, enhancing liquidity and flexibility. On the other hand, small and medium enterprises with higher CCC values, like Small and medium enterprise 3 and Small and medium enterprise 4, faced liquidity challenges and inefficiencies in managing inventory and receivables.

These findings support the second objective of this study, demonstrating that CBSI scores effectively predict small and medium enterprise success. Small and medium enterprises with CBSI scores above 0.60 exhibited stronger financial resilience, operational efficiency and strategic alignment, while those with scores below 0.60 showed signs of financial distress and inefficiencies. The ability of CBSI to distinguish between strong and weak small and medium enterprises reinforces its value as a predictive tool.

Operational and cultural alignment

The CAS and Telles' Mathematical Accuracy were used to assess the alignment of small and medium enterprises' ERP systems. Higher CAS scores in Small and medium enterprise 1 and Small and medium enterprise 5 indicated well-configured ERP systems aligned with business processes, enhancing efficiency. Conversely, Small and medium enterprise 3 and Small and medium enterprise 4 exhibited lower CAS and Telles' Accuracy scores, reflecting misaligned systems and workflow inconsistencies, which contributed to their weaker performance. The lower CAS and Telles' Accuracy scores in failing small and medium enterprises suggest that misaligned systems can hinder performance, even when financial metrics like the CCC are stable.

Strengths and limitations

Strengths

The CBSI offers a holistic approach to evaluating small and medium enterprise success by integrating financial and operational metrics, providing a comprehensive view of business performance.

The study provides actionable insights, helping small and medium enterprises identify areas for improvement in both financial health and operational efficiency.

Limitations

The reliability of the findings depends on the accuracy of the financial data provided, as shown by anomalies in the Retail (failing) and IT sectors' Altman Z-Scores. The operational and cultural metrics, such as workflow accuracy and CAS, were derived from available data, which may not fully capture the complexities of each small and medium enterprise's internal environment.

Comparison with literature

The integration of financial and cultural metrics to assess small and medium enterprise performance notably contributes to existing literature, which has primarily focused on financial metrics. While previous research has shown the importance of financial stability in predicting business success (Okeke, Bakare & Achumie 2024:3), this study highlights the growing recognition of organisational culture as an essential factor for long-term sustainability (Abbasi et al. 2021). The study supports earlier findings by Leso, Cortimiglia & Ghezzi (2023:152), demonstrating that small and medium enterprises with strong organisational cultures and aligned leadership, processes, and employee engagement perform better operationally. Moreover, the study's focus on the CCC aligns with prior research highlighting liquidity management as crucial for financial stability (Okeke et al. 2024:3).

This study's inclusion of cultural alignment represents a shift from traditional models that rely solely on financial metrics. Similar to Bessette and Gregory (2020:2), this study illustrates that financial metrics alone may not fully capture small and medium enterprise performance, especially in dynamic markets like South Africa.

Implications and recommendations

The findings from this study provide several key insights for small and medium enterprises and policymakers. By leveraging the CBSI framework, small and medium enterprises can enhance operational efficiency and organisational cohesion. The results suggest that small and medium enterprises that integrate CBSI metrics into their financial and operational planning show improved workflow integration, better decision-making and stronger competitive positioning.

By using CBSI as a decision-support tool, business leaders can identify areas for strategic intervention, such as optimising cash flow cycles, improving ERP adoption and reinforcing leadership engagement. Policymakers can use CBSI insights to develop targeted small and medium enterprise support programmes, addressing sector-specific challenges and ensuring that small and medium enterprises receive resources to drive sustainability and growth.

Key strategic implications for small and medium enterprises

Financial stability and liquidity management

Small and medium enterprises should focus on minimising their CCC and improving their Altman Z-scores to reduce bankruptcy risk and enhance liquidity. Small and medium enterprises with higher CBSI scores manage their financial cycles effectively, leading to greater resilience and financial sustainability.

Aligning enterprise resource planning systems with operational efficiency

Small and medium enterprises with lower CAS and Telles' Accuracy scores should prioritise optimising workflows and ERP functionalities to align with strategic goals. Effective ERP alignment improves operational performance, reduces inefficiencies and boosts competitiveness.

Leveraging composite business success index for continuous performance evaluation

The CBSI framework offers small and medium enterprises a comprehensive tool for assessing overall business performance and identifying areas for improvement. Regularly monitoring financial and operational metrics helps small and medium enterprises navigate market challenges, refine strategies and improve long-term viability.

Recommendations for future research

The following recommendations are proposed to improve CBSI's effectiveness for small and medium enterprise performance evaluation:

Refinement and sectoral adaptability of composite business success index

Further refinement of the CBSI framework is necessary to enhance its applicability across diverse sectors and regions. Future studies should explore industry-specific adjustments to improve the accuracy and relevance of CBSI metrics in varying business environments.

Integration of additional qualitative measures

Future research should incorporate more qualitative dimensions to deepen the understanding of internal cultural and operational dynamics. Exploring leadership styles, organisational behaviour and small and medium enterprise adaptability could strengthen CBSI's ability to capture non-financial performance drivers.

Addressing data normalisation challenges

A key challenge in applying CBSI universally is the variation in financial and operational metrics across sectors. Future research should focus on developing robust normalisation methods to ensure comparability across different business sizes, sectors and regions, improving CBSI's role as a universal small and medium enterprise performance assessment tool.

Longitudinal analysis of composite business success index's predictive validity

Longitudinal studies would provide deeper insights into the long-term effects of operational efficiency and cultural alignment on financial performance.

Leveraging artificial intelligence to enhance the composite business success index model

AI can optimise both financial and cultural metrics within the CBSI framework. Machine learning and predictive analytics can enhance financial management and operational efficiency, while AI-driven tools like sentiment analysis can improve cultural metrics and employee engagement. Real-time data analysis enabled by AI provides actionable insights, helping small and medium enterprises streamline operations and improve competitiveness (Gabriel & Felix 2024; Schönberger 2023). Future research should explore integrating AI with CBSI to enhance both financial and cultural metrics, significantly aiding small and medium enterprises in improving their competitiveness and sustainability in a rapidly evolving business environment.

Conclusion

This study introduced the CBSI, a novel framework for evaluating small and medium enterprise performance in South Africa by integrating both financial and cultural metrics. This approach provides a more comprehensive understanding of the factors driving small and medium enterprise competitiveness, addressing gaps in traditional evaluation models. Based on the findings, policymakers should consider the following steps:

Encourage enterprise resource planning adoption: Support small and medium enterprises in adopting ERP systems through subsidies or tax incentives to streamline operations, improve financial reporting and enhance market competitiveness.

Promote financial literacy: Introduce targeted financial literacy programmes to help small and medium enterprises understand key metrics like the CCC, improving financial decisions and stability.

Support organisational culture alignment: Implement policies to foster cohesive organisational cultures aligned with business objectives, with training focused on workflow integration to improve financial performance and efficiency.

Facilitate digital transformation: Provide programmes to assist small and medium enterprises in adopting new technologies, including financial and technical support to upgrade digital infrastructure.

By taking these steps, policymakers can create an environment that supports small and medium enterprise growth, contributing to economic growth and sustainability.

Acknowledgements

This article is partially based on the doctoral research of Donovan M. Jacobs, PhD candidate at the Department of Information Technology, for the Degree of Doctor of Philosophy in Informatics, Cape Peninsula University of Technology, supervised by Dr Boniface Kabaso.

The authors extend their gratitude to the Small Enterprise Development Agency (SEDA) and the Cape Peninsula University of Technology (CPUT) for their invaluable support in providing the necessary data and ethical clearance for this study. Their assistance in facilitating access to both small and medium enterprise and JSE-listed company data has been integral to the successful completion of this research.

They also acknowledge the participating small and medium enterprises and JSE-listed companies for their time and willingness to contribute to this study, offering insights into their financial and operational structures. Without their cooperation, this research would not have been possible.

Finally, they specially thank their supervisor Dr Kabaso and their colleagues of PhD - IT Graduating Class 2024 for their guidance and feedback throughout the research process. Your contributions have greatly enriched the quality of this work.

Competing interests

The authors declare that they have no financial or personal relationships that may have inappropriately influenced them in writing this article.

Authors' contributions

D.J. conducted the empirical research, performed the data analysis, drafted the manuscript. B.K. provided research guidance, contributed to the literature review and reviewed manuscript.

Funding information

This research received no specific grant from any funding agency in the public, commercial or non-profit sectors.

Data availability

All data supporting the findings of this study are available from the corresponding author, D.J., on reasonable request.

Disclaimer

The views and opinions expressed in this article are those of the authors and are the product of professional research. It does not necessarily reflect the official policy or position of any affiliated institution, funder, agency or that of the publisher. The authors are responsible for this article's results, findings and content.

References

Abbasi, B., Akhavan, R., Khameneh, A.G., Zandi, B., Farrokh, D., Rad, M.P. et al., 2021, 'Evaluation of the relationship between inpatient COVID-19 mortality and chest CT severity score', American Journal of Emergency Medicine 45, 458-463. https://doi.org/10.1016/j.ajem.2020.09.056 [ Links ]

Ahsan, M.J., 2024, 'Unlocking sustainable success: Exploring the impact of transformational leadership, organizational culture, and CSR performance on financial performance in the Italian manufacturing sector', Social Responsibility Journal 20(4), 783-803. https://doi.org/10.1108/SRJ-06-2023-0332 [ Links ]

Altman, E.I., Iwanicz-Drozdowska, M., Laitinen, E.K. & Suvas, A., 2017, 'Financial distress prediction in an international context: A review and empirical analysis of Altman's Z-score model'. Journal of International Financial Management and Accounting 28(2), 131-171. https://doi.org/10.1111/jifm.12053 [ Links ]

Alves, I. & Lourenço, S.M., 2022, 'The use of non-financial performance measures for managerial compensation: Evidence from SMEs', Journal of Management Control 33, 151-187. https://doi.org/10.1007/s00187-022-00337-8 [ Links ]

Bag, S., Viktorovich, D.A., Sahu, A.K. & Sahu, A.K., 2021, 'Barriers to adoption of blockchain technology in green supply chain management', Journal of Global Operations and Strategic Sourcing 14(1), 104-133. https://doi.org/10.1108/JGOSS-06-2020-0027 [ Links ]

Bessette, D.L. & Gregory, R., 2020, 'The promise and reality of social and cultural metrics', Ecology and Society 25(3), 11. https://doi.org/10.5751/ES-11730-250311 [ Links ]

Bissessar, C., 2018, 'An application of Hofstede's cultural dimension among female educational leaders', Education Sciences 8(2), 77. https://doi.org/10.3390/educsci8020077 [ Links ]

Boujlil, R. & Alsunbul, S., 2024, 'Enhancing business sustainability through an intelligent framework for unveiling financial frauds', Journal of Sustainable Development and Green Technology 4(1), 36-40. https://doi.org/10.54216/JSDGT.040105 [ Links ]

Bouncken, R.B., Kraus, S., Kiani, A. & He, K., 2024, 'The role of strategic orientations for digital innovation: When entrepreneurship meets sustainability', Technological Forecasting & Social Change 205, 123503. https://doi.org/10.1016/j.techfore.2024.123503 [ Links ]

Caldeira, M.M. & Ward, J.M., 2003, 'Using resource-based theory to interpret the successful adoption and use of information systems and technology in manufacturing small and medium-sized enterprises', European Journal of Information Systems 12(2), 127-141. https://doi.org/10.1057/palgrave.ejis.3000454 [ Links ]

Cameron, K.S. & Quinn, R.E., 2011, An introduction to changing organisational culture: Based on the competing values framework diagnosing and changing organisational culture, Jossey-Bass, San Francisco. [ Links ]

Creswell, J.W. & Creswell, J.D., 2017, Research design: Qualitative, quantitative, and mixed methods approaches, 5th edn., Sage, Thousand Oaks, CA. [ Links ]

Destriwanti, O., Sintha, L., Bertuah, E. & Munandar, A., 2022, 'Analyzing the impact of good corporate governance and financial performance on predicting financial distress using the modified Altman Z Score model', American International Journal of Business Management 5(2), 27-36. [ Links ]

Egu, M.E. & Chiloane-Tsoka, E.G., 2023, 'Does listing on the JSE's Altx improve the performance of small and medium-sized enterprises?', Cogent Business and Management 10(3), 2282750. https://doi.org/10.1080/23311975.2023.2282750 [ Links ]

Fleetwood, D., 2024, Stratified random sampling: Definition, method and examples, QuestionPro. [ Links ]

Foster, C., 2024, 'Methodological pragmatism in educational research: From qualitative-quantitative to exploratory-confirmatory distinctions', International Journal of Research and Method in Education 47(1), 4-19. https://doi.org/10.1080/1743727X.2023.2210063 [ Links ]

Gabriel, M. & Felix, G., 2024, Artificial intelligence-driven competitiveness: Enhancing SME performance in the global market, viewed 11 February 2025, from https://www.researchgate.net/publication/384442301. [ Links ]

Harefa, I., Hartati, T., Hulu, S., Bu'ulolo, N.A., Permata, I. & Hulu, H., 2024, 'Navigating the financial landscape: Unraveling the complexities of SMEs' access to finance', International Journal of Economic Literature 2(1), 229-238. [ Links ]

Hofstede, G., 2011, 'Dimensionalizing cultures: The Hofstede model in context', Online Readings in Psychology and Culture 2(1), 8. https://doi.org/10.9707/2307-0919.1014 [ Links ]

Horani, O.M., Khatibi, A., AL-Soud, A.R., Tham, J., Al-Adwan, A.S. & Azam, S.M.F., 2023, 'Antecedents of business analytics adoption and impacts on banks' performance: The perspective of the TOE framework and resource-based view', Interdisciplinary Journal of Information, Knowledge, and Management 18, 609-643. https://doi.org/10.28945/5188 [ Links ]

Huo, G., 2023, 'Problems and countermeasures in financial analysis of SMEs', BCP Business & Management 38, 2130-2135. https://doi.org/10.54691/bcpbm.v38i.4050 [ Links ]

Iliescu, M.-E., 2020, 'Barriers to digital transformation in SMEs: A qualitative exploration of factors affecting ERP adoption in Romania', in C. Brătianu, A. Zbuchea, F. Anghel, & B. Hrib (eds.), Proceedings of the International Academic Conference, Bucharest, Romania, October 15-16, 2020, pp. 1-929. [ Links ]

Jardioui, M., Garengo, P. & El Alami, S., 2020, 'How organizational culture influences performance measurement systems in SMEs', International Journal of Productivity and Performance Management 69(2), 217-235. https://doi.org/10.1108/IJPPM-10-2018-0363 [ Links ]

Kaushik, V. & Walsh, C.A., 2019, 'Pragmatism as a research paradigm and its implications for Social Work research', Social Sciences 8(9), 255. https://doi.org/10.3390/socsci8090255 [ Links ]

Leso, B.H., Cortimiglia, M.N. & Ghezzi, A., 2023, 'The contribution of organizational culture, structure, and leadership factors in the digital transformation of SMEs: A mixed-methods approach', Cognition, Technology and Work 25(1), 151-179. https://doi.org/10.1007/s10111-022-00714-2 [ Links ]

Lin, M.S., Jung, I.N. & Sharma, A., 2024, 'The impact of culture on small tourism businesses' access to finance: The moderating role of gender inequality', Journal of Sustainable Tourism 32(3), 480-499. https://doi.org/10.1080/09669582.2022.2130337 [ Links ]

Meyer, A.D., Tsui, A.S. & Hinings, C.R., 1993, 'Configurational approaches to organizational analysis', Academy of Management Journal 36(6), 1175-1195. https://doi.org/10.2307/256809 [ Links ]

Nowell, L.S., Norris, J.M., White, D.E. & Moules, N.J., 2017, 'Thematic analysis: Striving to meet the trustworthiness criteria', International Journal of Qualitative Methods 16(1), 1-16. https://doi.org/10.1177/1609406917733847 [ Links ]

Nungchim, B.N. & Leihaothabam, J.K.S., 2022, 'Impact of organizational culture on the effectiveness of organizations: A case study of some service sector organizations in Manipur', Jindal Journal of Business Research 11(1), 44-54. https://doi.org/10.1177/22786821221082592 [ Links ]

Okeke, N.I., Bakare, O.A. & Achumie, G.O., 2024, 'Forecasting financial stability in SMEs: A comprehensive analysis of strategic budgeting and revenue management', Open Access Resear ch Journal of Multidisciplinary Studies 8(1), 139-149. https://doi.org/10.53022/oarjms.2024.8.1.0055 [ Links ]

Ormerod, R., 2024, 'Pragmatism as practice theory: The experience of systems and OR scholars', Systems Research and Behavioral Science 41(1), 1-15. https://doi.org/10.1002/sres.2929 [ Links ]

Pudjiarti, E.S. & Hutomo, P.T.P., 2020, 'Innovative work behaviour: An integrative investigation of person-job fit, person-organization fit, and person-group fit', Business: Theory and Practice 21(1), 39-47. https://doi.org/10.3846/btp.2020.9487 [ Links ]

Qomoyi, E., Mlambo, L., Chikozho, C. & Makoni, M., 2024, 'The role of SMEs in the economic development of South Africa: Challenges and growth opportunities', Journal of Business and Economics 8(1), 45-56. [ Links ]

Rahman, M., Hack-Polay, D., Shafique, S. & Igwe, P., 2024, 'Institutional and organizational capabilities as drivers of internationalisation: Evidence from emerging economy SMEs', International Journal of Entrepreneurship and Innovation 25(3), 145-216. https://doi.org/10.1177/14657503221106181 [ Links ]

Rahmita, F., Raharjo, T., Genia, V. & Prasetyo, A., 2023, 'Navigating the ERP landscape: Unveiling the key drivers in enterprise resource planning success - A comprehensive literature exploration', Indonesian Journal of Computer Science 12(6), 3262-3279. https://doi.org/10.33022/ijcs.v12i6.3517 [ Links ]

Rao, C.C. & Li, R.W., 2019, 'Development and application of model of configuration for order-engineered enterprise resource', International Journal of Wireless and Mobile Computing 16(4), 358-363. https://doi.org/10.1504/IJWMC.2019.100067 [ Links ]

Roy, A., Newman, A., Round, H. & Bhattacharya, S., 2024, 'Ethical culture in organizations: A review and agenda for future research', Business Ethics Qua rterly 34(1), 97-138. https://doi.org/10.1017/beq.2022.44 [ Links ]

Saah, P., Mbohwa, C. & Madonsela, N.S., 2024, 'The role of adaptive management in the resilience and growth of small and medium size enterprises', International Review of Management and Marketing 14(1), 1-10. https://doi.org/10.32479/irmm.15139 [ Links ]

Sajuyigbe, A.S., Oyedele, O., Oke, O.D., Sodeinde, G.M., Ayo-Oyebiyi, G.T. & Adeyemi, M.A., 2024, 'Financial behavior and SMEs performance: The mediating influence of financial literacy and organizational culture', Journal of Business and Technology 8(2), 99-116. https://doi.org/10.4038/jbt.v8i2.126 [ Links ]

Samputra, P.L. & Soesilo, N.I., 2023, 'Evaluation of national financial inclusion strategies in non-profit institution: SME Center UI', JEJAK Journal of Economics and Policy 16(1), 116-134. https://doi.org/10.15294/jejak.v16i1.39214 [ Links ]

Saunders, B., Sim, J., Kingstone, T., Baker, S., Waterfield, J., Bartlam, B. et al., 2018, 'Saturation in qualitative research: Exploring its conceptualization and operationalization', Quality & Quantity 52, 1902. https://doi.org/10.1007/s11135-017-0574-8 [ Links ]

Schönberger, M., 2023, 'Artificial intelligence for small and medium-sized enterprises: Identifying key applications and challenges', Journal of Business Management 21, 89-112. https://doi.org/10.32025/JBM23004 [ Links ]

Singh, D. & Singh, B., 2020, 'Investigating the impact of data normalization on classification performance. Applied Soft Computing 97(Part B), 105524. https://doi.org/10.1016/j.asoc.2019.105524 [ Links ]

Small Enterprise Development Agency (SEDA), 2023, 2022-23 Annual stakeholders report, SEDA, Pretoria, viewed 03 November 2023, from https://www.seda.org.za/Publications/Pages/Annual-Reports.aspx. [ Links ]

Syafira, A., Puspitasari, W. & Witjaksono, W., 2021, 'Analysis and evaluation of user acceptance on the use of Enterprise Resource Planning (ERP) systems at PT trisco tailored apparel manufacturing', IJAIT International Journal of Applied Information Technology 4(1), 18-26. https://doi.org/10.25124/ijait.v4i01.2852 [ Links ]

Telles, C.R., 2019, 'A mathematical modelling for workflows', Journal of Mathematics 2019, 784909. https://doi.org/10.1155/2019/4784909 [ Links ]

Uddin, A., Cetindamar, D., Hawryszkiewycz, I. & Sohaib, O., 2023, 'The role of dynamic cloud capability in improving SME's strategic agility and resource flexibility: An empirical study', Sustainability (Switzerland) 15(11), 8467. https://doi.org/10.3390/su15118467 [ Links ]

Van Staden, L.J., 2022, 'The influence of certain factors on South African small and medium-sized enterprises towards export propensity', Development Southern Africa 39(3), 457-469. https://doi.org/10.1080/0376835X.2021.2019573 [ Links ]

Vargo, J. & Seville, E., 2011, 'Crisis strategic planning for SMEs: Finding the silver lining', International Journal of Production Research 49(18). https://doi.org/10.1080/00207543.2011.563902 [ Links ]

Vos, J. & Boonstra, D., 2022, 'Organizational culture and ERP implementation success in SMEs', Journal of Enterprise Information Management 35(2), 102451-102463. https://doi.org/10.1016/j.jeim.2022.102453 [ Links ]

Стошић Панић, Д. & Janković Милић, В., 2022, 'Entrepreneurial self-efficacy and business success of entrepreneurs in the Republic of Serbia: A pilot study', TEME: Journal for Social Sciences XLVI(1), 113-128. https://doi.org/10.22190/TEME200323006S [ Links ]

Correspondence:

Correspondence:

Donovan Jacobs

donovan@onomax.com

Received: 24 Aug. 2024

Accepted: 19 Feb. 2025

Published: 05 June 2025

{kind=link}

{kind=link}